michael kern - james cook university - strategic oversight of controlled entities

TRANSCRIPT

University Governance and Regulations Forum

Strategic oversight of “Controlled Entities”

Presentation by:

Michael KernUniversity SecretaryJames Cook UniversityPast PresidentAssociation of Australian University Secretaries

Overview of Presentation

v Why we use a Controlled Entity – a quick recap

v The Voluntary Code’s “Requirements”

v Use of Controlled Entities by Australian universities – a 2015 sector scan

v Oversight Frameworks within/outside of the Higher Education Sector

v Strategies for effective oversight by a university

v Common risks and challenges and how can these be overcome?

v Good governance practice Principles and Guidelines -‐ Opportunity?

Why use a Controlled Entity

v Nature and Purpose of the activities being undertaken

v Underlying pressure on reduced government funding reliance

v Commercial V public sector modus operandi

v Legal separation for liability and reputation purposes

v Core business activities

v Non-‐core business activities

v Commercial exploitation and “spin off” readiness

Requirements Under the Voluntary Code

The Voluntary Code of Best Practice for the Governance of Australian Universities requires each University Council to exercise oversight and risk management of its Controlled Entities

Requirements Under the Voluntary Codev ensuring that the entity's board possesses the skills, knowledge and

experience necessary to provide proper stewardship and control of the entity;

v appointing some directors to the board of the entity who are not members of the governing body or officers or students of the university;

v ensuring that the board of the entity adopts and regularly evaluates a written statement of its own governance principles;

v ensuring that the board documents a clear corporate and business strategy which reports on and updates annually the entity's long-‐term objectives and includes an annual business plan containing achievable and measurable performance targets and milestones; and

v establishing and documenting clear expectations of reporting to the governing body, such as a draft business plan for consideration and approval before the commencement of each financial year and at least quarterly reports against the business plan.

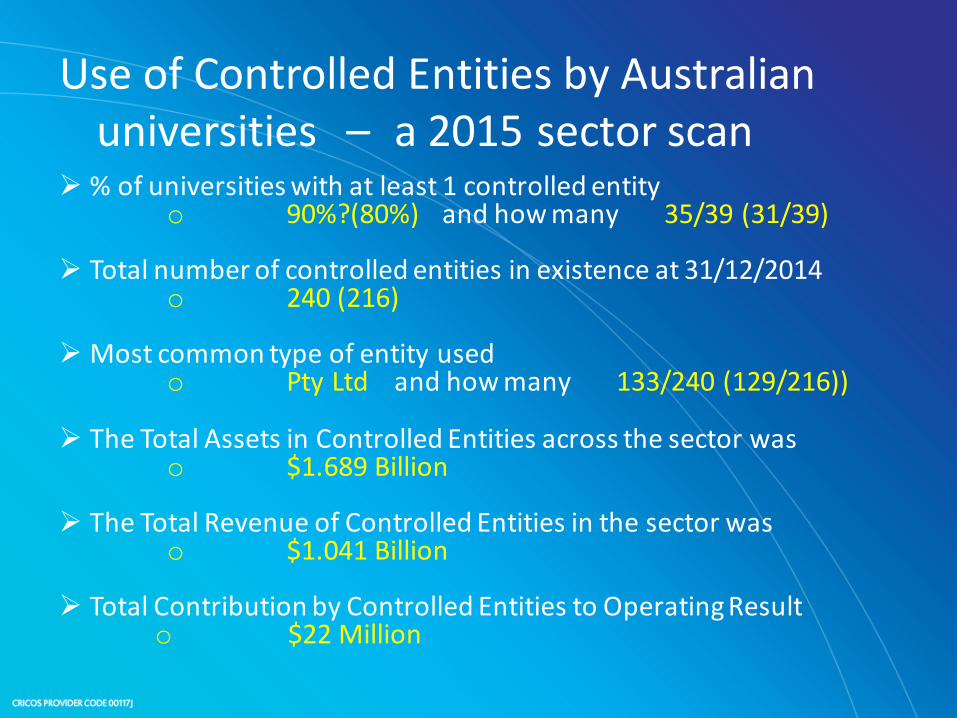

Use of Controlled Entities by Australian universities – a 2015 sector scan

Ø % of universities with at least 1 controlled entityo 90%?(80%) and how many 35/39 (31/39)

Ø Total number of controlled entities in existence at 31/12/2014o 240 (216)

ØMost common type of entity usedo Pty Ltd and how many 133/240 (129/216))

Ø The Total Assets in Controlled Entities across the sector waso $1.689 Billion

Ø The Total Revenue of Controlled Entities in the sector waso $1.041 Billion

Ø Total Contribution by Controlled Entities to Operating Resulto $22 Million

Oversight Frameworks within and outside of the Higher Education Sector

v Frameworks in the HE Sector v Frameworks outside of the HE

Sectorv Good Governance Principles and

Guidance for Not-‐for-‐Profit Organisations (AICD 2014)

v The Higher Education Code of Governance (CUC 2014)

v Providing your Board with comfort on the accountability mechanisms operating your company (GIA 2014)

v Directors of wholly-‐owned subsidiary companies (GIA 2014)

Oversight Frameworks – Characteristics

1. Authority – understand the internal/external regulatory regimes 2. Policy – clear articulation of various processes and delegations3. Organisational Structure – clear control/ownership arrangements4. Constitutional Documents -‐ clarity of roles and responsibilities5. Board and CEO appointments – skills, knowledge and experience6. Training and Inductions -‐ for the Chair, other Directors and CEO7. HEP approval -‐ of Business Plan, Budget and KPIs8. Review/monitoring -‐ of performance against plan and KPIs9. Risk Management -‐ annual risk assessment/investment review10. Business Continuity Planning – clear arrangements for disruption11. Continuous improvement– of oversight Framework and controls

Risks and challenges

v Failure to closely monitor financial position of entityv Failure to appoint skilled and experienced Chair, Directors or CEOv Failure to address control breakdowns and systemic control weaknesses

raised in external Auditor’s Management Letterv Lack of integrity in reporting from Controlled Entityv Failure to properly assess risks of indemnities/underwriting issuedv Failure to recognise underlying operating/management problems

masked by subsidies and cross-‐ subsidisationv Failure to manage Conflicts of Interests

Strategies to overcome Risks and Challenges

v Controlled Entity establishment requiring HEP approvalv Constitutional documents – ensure adequate and include rules

around Director communication of informationv Directors -‐ highly skilled/experienced external Council members,

executive staff members and/or external professionalsv Periodic (¼ly, ½yrly) reporting against KPIs and Business Plan

objectivesv Properly assessed and reviewed indemnities/underwritings v Clarity of officers’ roles and responsibilities especially where

staff involved (COIs) v Governance manual accessible by all CEs and officersv Approval of a Business Plan for each CE < commencement of the

year v Annual Risk Assessments undertaken on each CE

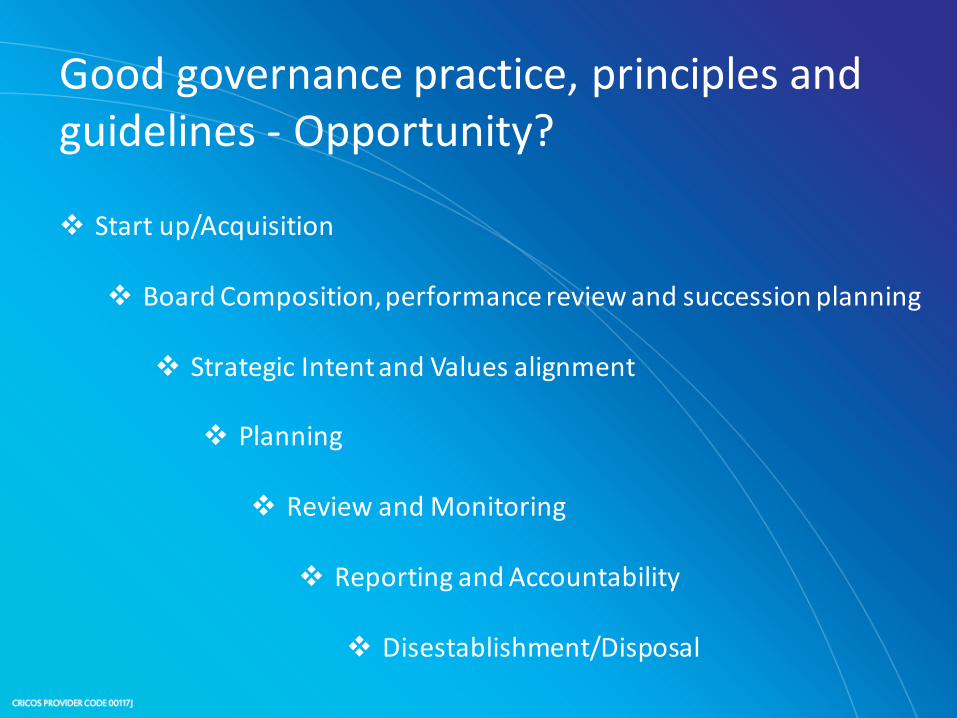

Good governance practice, principles and guidelines -‐ Opportunity?

v Start up/Acquisition

v Board Composition, performance review and succession planning

v Strategic Intent and Values alignment

v Planning

v Review and Monitoring

v Reporting and Accountability

v Disestablishment/Disposal

Start up/AcquisitionvAre the objects of the CE clear and aligned to the HEP?v Is the authority for forming/acquiring a controlling interest in a CE clear?vAre the delegations of authority appropriate?v Is the appropriate entity being formed, acquired or used?vHow does the HEP wish to be able to exert its control over the CE? vWhat are the CE Board’s primary responsibilities.vAre Director communications to HEP authorised?vAre the roles and responsibilities of the CE’s Board, Directors, Chair and

management vis a vis any concurrent HEP roles clear and documented?v Is the constitutional document appropriate?v Is there a clear schedule of delegations of authority of the CE?v Is the induction and ongoing training, including COI training, adequate?v Is it clear to what extent HEP policies will be applied or modified to the

CE or replaced with CE specific policy?

Board composition, performance review and succession planningv Is size, structure and composition of CE Board appropriate to achieve intent? v Does the CE’s board have its own objectives clearly articulated?v Is there a clear and transparent process for nominating, selecting, appointing,

retiring, removing and replacing board members?v Is there a process to ensure an appropriate mix of skills, knowledge and

experience with Directors?v Is the Board’s performance evaluated against its objectives on a periodic basis

and action taken to improve in areas identified for improvement?v Is poor attendance, participation and contribution by CE Directors addressed?v Is the CE’s succession planning appropriate for the short and long term?v Are CE Directors aware of their general/specific legislative compliance

obligations?v Is the program of Induction and PD for directors of CE’s adequate?v Is the CE receiving appropriate secretariat support including timely and

adequate agendas, agenda papers, reports, SOBs, minutes etc.v Are the terms of appointment of board members appropriately staggered?

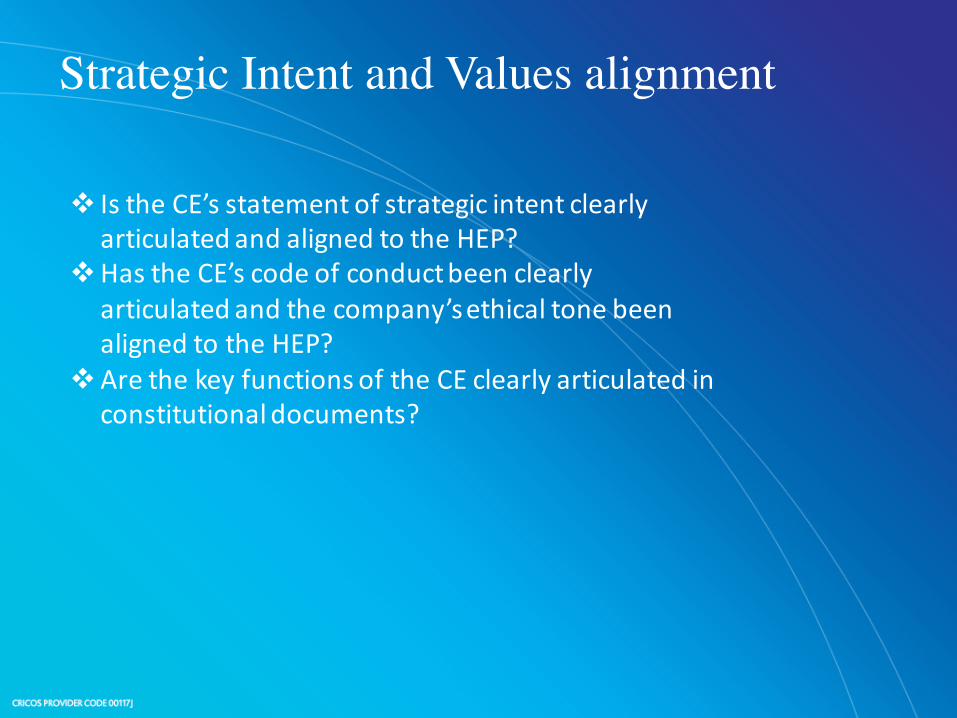

Strategic Intent and Values alignment

v Is the CE’s statement of strategic intent clearly articulated and aligned to the HEP?

vHas the CE’s code of conduct been clearly articulated and the company’s ethical tone been aligned to the HEP?

vAre the key functions of the CE clearly articulated in constitutional documents?

Planning

v Does the CE prepare the following annually?q Business planq Budget (including clearly defined assumptions and risks)q Clearly defined Performance Measures and Targets

v Is the CE’s Risk Management appetite reviewed periodically and aligned to operational strategies?

v Is the Budget/ KPIs/ Business Plan submitted to the HEP for approval prior to the commencement of the year?

v What is the process to review the effectiveness / appropriateness of any subsidy or underwriting commitment by the HEP?

Review and Monitoring

v Is operational performance reviewed against Budget and KPIs at appropriate intervals including at EOY and reported to the HEP?

v Is a dashboard report provided periodically to the HEP of appropriate financial / non-‐financial information and position?

v Are forecast results reported to the HEP which reflect changing assumptions, risks and known variances?

v Are there mechanisms for taking corrective / remedial action to address non achievement of approved strategies and performance targets?

v Are there mechanisms for varying the HEP subsidy / underwriting?v Is information being provided to the HEP in a transparent manner and

on a timely basis?

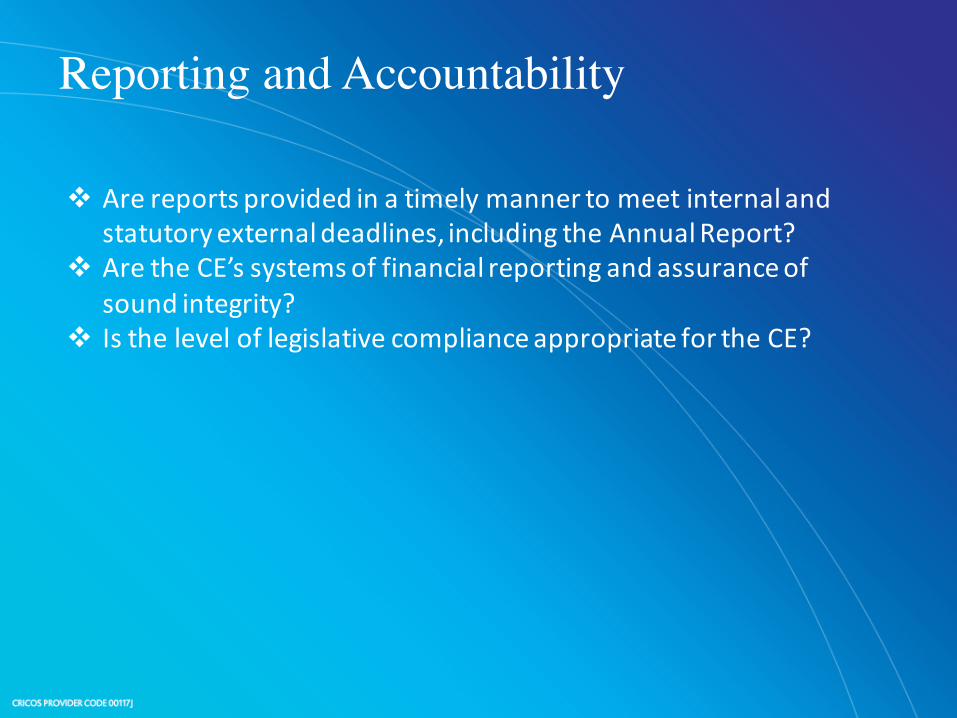

Reporting and Accountability

v Are reports provided in a timely manner to meet internal and statutory external deadlines, including the Annual Report?

v Are the CE’s systems of financial reporting and assurance of sound integrity?

v Is the level of legislative compliance appropriate for the CE?

Disestablishment / Disposal

v Are the triggers for the winding up or dissolution of a CE clearly documented and appropriate and furthermore, understood and monitored?

v Is the delegated approval authority for the disestablishment / disposal of the CE or a controlling interest in the CE clearly documented and appropriate?

When the Controlled Entity is under control