microbank de “la caixa”, s.a. - home | caixabank. was the dominant company of a group of...

TRANSCRIPT

MicroBank de “la Caixa”, S.A. Annual Financial Statements for the year ended 31 December 2009, prepared in conformity with Banco de España Circular 4/2004 of 22 December, and Directors’ Report, together with the Auditors’ Report

MicroBank de “la Caixa”, S.A. Notes to the financial statements for the financial year ended 31 December 2009

1. Description of the Entity and Other Information

a) Description of the Entity

MicroBank de “la Caixa”, S.A. (hereinafter referred to as “the Entity”) is an extension of Banco de Europa, S.A. Around the middle of 2007, when the change in the Bylaws and the business activities took place, Banco de Europa, S.A. was the dominant company of a group of entities whose corporate purpose was the provision of financial services and financial leasing and whose activities it controlled either directly or indirectly. At the end of 1996, the Bank sold all its branches and the banking business conducted therein to Caixa d’Estalvis i Pensions de Barcelona, “la Caixa”, transferring all asset and liability transactions with clients, with the exception of the asset transactions that were recognised at the time of the sale as doubtful loans and the real property originating from foreclosed assets, which continued to be managed within the Entity.

Until the aforementioned change of activity, Banco de Europa had no employees. These went on to form part of the staff of GDS-Cusa, S.A. and Caixarenting, S.A., with the latter companies taking over all rights and obligations.

At the Extraordinary General Meeting of “la Caixa” held on 19 October 2006, it was announced that a microcredit bank was to be created as part of the implementation of a group of social initiatives. It was also announced that the Entity that would be used for the implementation of this initiative would be Banco de Europa, S.A., which from the 2007 financial year would take the name of MicroBank de “la Caixa”, S.A.

Thus the previous activities of Banco de Europa, S.A., essentially connected with the holding of equity interests, ceased. More specifically, 99.67% of FinanciaCaixa II, E.F.C., S.A., 99.998% of GDS-Cusa, S.A., 99% of CaixaRenting, S.A., 55% of Finconsum, E.F.C., S.A. and 20% of Telefónica Factoring, E.F.C., S.A. were transferred to “la Caixa” on 20 March 2007. This transfer generated a profit for the Company of approximately €78,000,000.

At the General Meeting of Shareholders of Banco Europa, S.A. held on 24 January 2007, the change in trading name was approved, and the company took the name of MicroBank de “la Caixa”, S.A.

The corporate purpose of the company was also defined at the same Meeting of Shareholders; this consisted of the receipt of funds from the public under irregular deposit contracts or similar, to be applied on the Company’s own behalf to credit and microcredit activities, i.e., the granting of unsecured loans, with the aim of financing small business ventures launched by individuals who, owing to their socio-economic status, find it difficult to obtain traditional bank financing, and providing customers with drawing, transfer, custodianship and brokerage services.

MicroBank is integrated within the Caixa d’Estalvis i Pensions de Barcelona Group, whose dominant company is Caixa d’Estalvis i Pensions de Barcelona, governed by the commercial legislation currently in force in Spain and having its registered office at Avenida Diagonal 627, Barcelona, this being the company that prepares the consolidated financial statements. The consolidated annual financial statements of the Caixa d’Estalvis i Pensions de Barcelona Group for the 2009 financial year were prepared by the Directors at the meeting of the Board of Directors held on 4 February 2010. The consolidated annual financial statements of the Caixa d’Estalvis i Pensions de Barcelona Group for the 2008 financial year were approved by its General Meeting of 23 April 2009.

b) Basis of presentation of the annual financial statements

The Entity’s annual financial statements were prepared in accordance with the accounting models and criteria and the valuation standards established in Banco de España Circular 4/2004 of 22 December, (hereinafter referred to as “Circular 4/2004”), amended by Circular 6/2008 of 26 November, so as to provide a faithful image of the Entity’s capital and financial situation at 31 December 2009, its trading results, changes in equity and the cash flows generated during the financial year ended on that date. Circular 4/2004 constitutes the adaptation by the Spanish credit institutions sector of the International Financial Reporting Standards adopted by the European Union by means of Community Regulations, in accordance with Regulation No, 1606/2002 of the European Parliament and of the Council, of 19 July 2002, on the application of International Accounting Standards.

6

The accounting standards defined by Circular 4/2004 are detailed in Note 2. No criteria have been applied that might entail any difference in the respect of the former or have a material impact. The annual financial statements have been prepared on the basis of the accounting records kept by the Entity.

c) Responsibility for information and estimates

The Entity’s annual financial statements for the 2009 financial year were formulated by its Directors at the meeting of the Board of Directors held on 15 March 2010 and are pending approval by the Entity’s General Meeting of Shareholders, which is expected to approve them without any significant changes. The annual financial statements for the 2008 financial year were approved by the General Meeting of Shareholders held on 8 June 2009 and are presented exclusively for the purposes of comparison with the information relating to the 2009 financial year. The information contained in these annual financial statements is the responsibility of the Directors of the Entity. In the Entity’s annual financial statements for the 2009 financial year, occasional use has been made of estimations made by its Directors in order to quantify certain of its assets, liabilities, income, expenses and obligations recorded in the statements. Essentially, these estimations relate to:

• Losses due to impairment of certain assets (see Notes 2.h, 2.n and 2.o).

• The hypotheses used in the actuarial calculation of post-employment benefit liabilities and obligations and other long-term obligations vis-à-vis employees (see Note 2.k).

• The useful life of tangible and intangible assets (See Notes 2.n and 2.o).

Although these estimates were made on the basis of the best information available at 31 December 2009, future events might make it necessary to revise them (upwards or downwards) in the years to come. Any such revisions would be made in conformity with the provisions of Regulation Nineteen of Circular 4/2004. d) Investments in credit institutions

In conformity with the provisions of Royal Decree 1245/1995 on the publicising of equity interests, MicroBank de ”la Caixa”, holds no direct equity interest equal to or greater than 5% of the capital or voting rights of any credit institutions. The information relating to the publicising of the equity interests of the “la Caixa” Group, of which the Bank forms part as a dependent company of Caixa d’Estalvis i Pensions de Barcelona “la Caixa”, is contained in the consolidated annual financial statements of the “la Caixa” Group. e) Capital adequacy ratio Law 13/1992, as amended, and Banco de España Circular 3/2008 govern the minimum levels of capital that must be maintained by Spanish credit institutions, at both individual and consolidated group level, and the form in which such capital is constituted. The Entity, in accordance with the aforesaid rules, has requested and obtained from Banco de España exemption from individual compliance with the general capital requirements, having demonstrated that the company satisfies the requirements established by current legislation in this regard, there being no current or foreseeable future practical or legal impediments to the immediate transfer of capital or redemption of liabilities. Currently, in accordance with Transitional Provision Three of Circular 3/2008, the Company determines its individual requirements by applying a reduction of 50% to the general requirements. f) Minimum reserve ratio By virtue of Monetary Circular 1/1998 of 29 September, effective from 1 January 1999, the ten-year cash ratio was repealed and superseded by the minimum reserve ratio. The Entity, in accordance with the aforesaid rules, has requested and obtained from Banco de España exemption from individual compliance with the general minimum reserve ratio requirements, there being no current or foreseeable future practical or legal impediments.

7

g) Agency contracts The Entity has designated “la Caixa” as exclusive Agent, with whom it has signed a contract of indeterminate duration for the provision of a service of full management of the internal and external processes arising from the financial operations carried out by the Entity with its clients. h) Environmental impact

Given the business in which the Entity is engaged, it has no responsibilities, expenses, assets, provisions or contingencies of an environmental nature that might be of significance in relation to its equity or financial situation and their results. Consequently, no specific breakdown of information on environmental matters is included in these notes to the annual financial statements.

i) Subsequent events

Between the end of the financial year and the date of preparation of these annual financial statements, no events have occurred that have a significant impact on them.

2. Accounting principles and policies and valuation criteria applied

In the preparation of the Entity’s annual financial statements for the 2009 financial year, the following accounting principles and policies and valuation criteria have been applied:

a) Financial instruments

Initial recognition of financial instruments

Financial instruments are initially recognised on the balance sheet when the Entity becomes a party to the contract giving rise to them, in accordance with the conditions of that contract. More specifically, debt instruments, such as loans and deposits, are recognised on the date from which the legal right to receive or the legal obligation to pay cash, respectively, arises. Financial derivatives are generally recognised on the trade date.

Financial asset purchase and sale transactions arranged through conventional contracts, i.e., contracts in which the reciprocal obligations of the parties must be fulfilled within a timescale established by regulations or market conventions and that cannot be settled by offset, such as stock exchange contracts and forward currency purchases and sales, are recognised on the date on which the rewards, risks, rights and obligations pertaining to any owner are applicable to the acquiring party, which, depending on the type of financial asset bought or sold, may be the trade date or the settlement or delivery date. In particular, transactions carried out on the spot currency market are recognised, as applicable, on the settlement date; transactions carried out on equity instruments traded on secondary Spanish markets are recognised, as applicable, on the trade date and transactions carried out on debt instruments traded on secondary Spanish securities markets are recognised, as applicable, on the settlement date. Derecognition of financial instruments

A financial asset is derecognised on the balance sheet when one of the following circumstances arises:

• The contractual rights to the cash flows from the financial asset expire; or

• The financial asset is transferred and the risks and rewards of the asset are substantially transferred or, even if these are not substantially transferred or retained, control of the asset is transferred (see Note 2.f).

A financial liability is derecognised on the balance sheet when the related obligations are extinguished or when it is acquired by the Entity with the intention of either placing it again or cancelling it.

Fair value and amortised cost of financial instruments

At the time of their initial recognition on the balance sheet, all financial instruments are recognised at fair value, which, in the absence of evidence to the contrary, is the transaction price. After initial recognition, at a determined date, the fair value of a financial instrument is understood as the amount for which it could be bought or sold on that date between two well-informed parties in a transaction conducted under conditions of mutual independence. The most objective and most commonly used reference for the fair value of a financial instrument is the price that would be paid for it on an organised, transparent and deep market (“quoted price” or “market price”).

8

If a market price does not exist for a given financial instrument, its fair value is estimated by reference to the price established in recent transactions involving similar instruments and, in the absence of any such transactions, by reference to valuation models that have been sufficiently tested and acknowledged by the international financial community, taking account of the specific features of the instrument to be valued and, most particularly, the various types of risk associated with the instrument. Notwithstanding the foregoing, the limitations of the valuation models used and the possible inaccuracies of the assumptions required by those models may mean that the estimated fair value of a financial instrument does not coincide precisely with the price at which the instrument might be bought or sold on the date of its valuation.

The fair value of derivatives not traded on organised markets or traded on organised markets lacking depth or transparency is determined on the basis of the sum of the future cash flows arising from the instrument, discounted on the valuation date (“present value” or “theoretical closing”), using valuation methods recognised by the financial markets such as: “net present value” (NPV), option pricing models, etc.

Financial instruments are classified under one of the following categories according to the methodology used to determine their fair value:

Level 1: Financial instruments whose fair value is determined by reference to their quoted prices on

active markets, without making any change to those prices.

Level 2: Financial instruments whose fair value is estimated on the basis of prices quoted on organised markets for similar instruments or through the use of other valuation techniques in which all significant inputs are based on directly or indirectly observable market data.

Level 3: Instruments whose fair value is estimated through the use of valuation techniques in which one or more significant inputs are not based on observable market data.

For the purposes of the provisions of the foregoing paragraphs, an input is regarded as significant when it is important in determining the fair value as a whole. For the majority of financial assets and liabilities, the criterion used for recognition on the balance sheet is that of the amortised cost. This criterion is applied to financial assets included under “Lending investments” and “”Held-to-maturity investments” and, for financial liabilities, to those recognised as “Financial liabilities at amortised cost”. Amortised cost is understood to be the acquisition cost of a financial asset or liability plus or minus, as appropriate, the repayments of principal and interest and the portion recognised on the income statement, using the effective interest method, of the difference between the initial amount and the maturity amount of such financial instruments. In the case of financial assets, amortised cost also includes any reductions for impairment.

The effective interest rate is the discount rate that exactly matches the initial value of a financial instrument for all its estimated cash flows of all kinds through its remaining life. For fixed-interest financial instruments, the effective interest rate matches the contractual interest rate established on the acquisition date, adjusted where applicable for the fees and transaction costs which, in accordance with the provisions of Circular 4/2004, must be included in the calculation of such effective interest rate. In the case of floating-rate financial instruments, the effective interest rate is estimated in a manner similar to that used for fixed-interest transactions, and is recalculated on each date of review of the contractual interest rate on the transaction according to the changes that have affected future cash flows. Classification and measurement of financial assets and liabilities

Financial instruments are classified on the Entity’s balance sheet principally in one of the following categories:

• Lending investments: This category includes unlisted debt instruments, financing granted to third parties in connection with normal credit activities, loans made by the Entity, and debts contracted with the Entity by purchasers of its goods and services. The financial assets included in this category are initially measured at their fair value, adjusted by the amount of the fees and transaction costs directly attributable to the acquisition of the financial asset, which, in accordance with the provisions of Banco de España Circular 4/2004 of 22 December, must be recognised on the income statement using the effective interest method until maturity. After acquisition, the assets included in this category are valued at amortised cost.

Assets acquired at a discount are measured at the cash amount paid, and the difference between their repayment value and the cash amount paid is recognised as financial income on the income statement over the remaining term until maturity.

9

It is generally the Entity’s intention to maintain the granted loans and credit facilities until their final maturity, for which reason they are presented on the balance sheet at amortised cost.

The interest earned on these assets is recognised under “Interest and Similar Income” on the income statement, and is calculated using the effective interest rate method. Any impairment losses on these assets are recognised in accordance with the provisions of Note 2.h).

• Financial liabilities at amortised cost: The financial liabilities included in this category are initially

measured at fair value adjusted by the amount of the transaction costs directly attributable to the issue or contracting of the financial liability, which are recognised on the income statement by applying the effective interest rate method defined in Circular 4/2004 until maturity. They are subsequently measured at amortised cost, calculated by applying the effective interest rate method defined in Circular 4/2004.

The interest incurred by these financial liabilities, calculated by the effective interest rate method, is recognised under “Interest and Similar Charges” on the income statement. Financial liabilities included in this category that are covered in hedging operations are recognised in accordance with the provisions of Note 2.b).

Inter-portfolio reclassifications of financial instruments

In the 2009 financial year there were no inter-portfolio reclassifications of financial instruments.

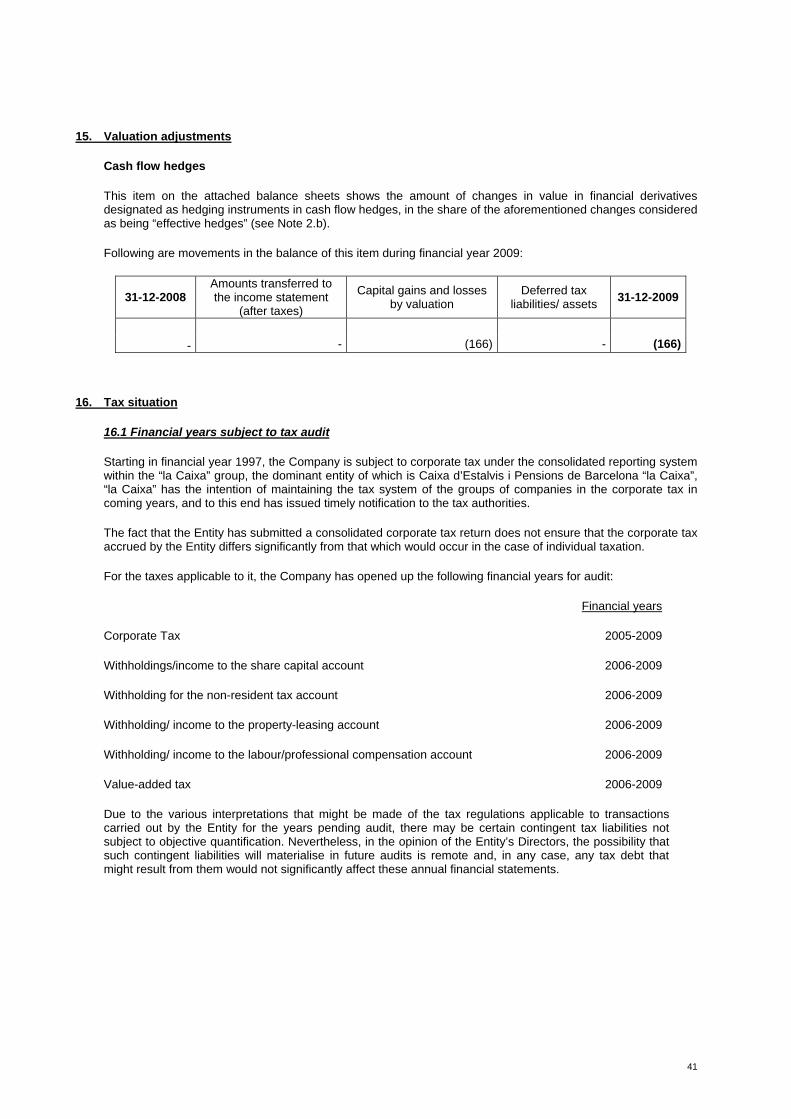

b) Hedge accounting and risk mitigation

The Entity uses financial derivatives as part of its strategy to reduce its exposure to interest rate risks. When these transactions satisfy certain requirements established in Rules 30.1 or 30.2 of Circular 4/2004, they are regarded as “hedges”.

When the Entity designates an operation as a hedging operation, it does so from the initial moment of the operation or the instrument included in the hedging, and documents the operation appropriately. The documentation of these hedging operations adequately identifies the hedged instrument or instruments and the hedging instrument or instruments, as well as the nature of the risk to be hedged against, and the criteria or methods applied by the Entity to evaluate the effectiveness of the hedge over its entire lifetime according to the risk to be hedged against.

The Entity considers only those operations which are considered to be highly effective throughout their life as hedging operations. A hedge is considered to be highly effective if, during its expected life, the changes in fair value or in the cash flows attributed to the risk hedged in the hedging operation of the hedged instrument or instruments are almost entirely offset by changes in the fair value or in the cash flows, as appropriate, of the hedged instrument or instruments.

To measure the effectiveness of hedges defined as such, the Entity analyses whether, from the beginning to the end of the term defined for the hedge, it may be prospectively expected that the changes in fair value or in the cash flows of the hedged item that are attributable to the hedged risk will be almost entirely offset by changes in the fair value or in the cash flows, as appropriate, of the hedging instrument or instruments and, retrospectively, that the results of the hedge will be within a range of 80% to 125% of the results of the hedged item.

All hedging operations carried out by the Entity are cash flow hedges aimed at hedging the changes in cash flows that are attributable to a particular risk associated with a financial asset or liability or to a highly probable forecast transaction, provided that they may affect the income statement. In the specific case of financial instruments designated as hedge items or qualifying for hedge accounting, the valuation differences arising on the portion of the hedging instruments qualifying as an effective hedge are recognised temporarily under “Equity - Valuation Adjustments - Cash Flow Hedges” and are not recognised on the income statement until the gains or losses on the hedged item are recognised on the income statement or until the date of maturity of the hedged item, or in certain cases until the hedge is discontinued. The gains or losses on the derivative are recognised under the same heading on the income statement as that of the gains or losses on the hedged item. Financial instruments hedged in this type of hedging transaction are recognised using the methods described in Note 2.a), without any changes in view of their considered status as hedged instruments. The Entity discontinues hedge accounting when the hedging instrument expires or is sold, when the hedge no longer qualifies for hedge accounting, or when the designation as a hedging operation is revoked.

10

Derivatives embedded in other financial instruments or in other contracts are accounted for separately as derivatives if their risks and characteristics are not closely related to those of the host instrument or contract, provided a reliable fair value can be attributed to the embedded derivative considered separately. c) Foreign currency transactions

The Entity’s functional currency is the Euro. Consequently, all balances and transactions denominated in currencies other than the Euro are deemed to be denominated in “foreign currency”. The Entity maintained no assets or liabilities in foreign currency during the 2008 and 2009 financial years.

d) Recognition of Income and Expenses

The most significant criteria used by the Entity for the recognition of its income and expenses are summarised below:

a) Interest income, interest expenses, dividends and similar items:

Interest income, interest expenses and similar items are generally recognised on an accrual basis using the effective interest method defined in Circular 4/2004. Interest accrued on doubtful loans, including loans exposed to country risk, is credited to income upon collection, which is an exception to the general rule. Dividends received from other companies, where applicable, are recognised as income when the Entity’s right to receive them arises, which is when the dividend is officially declared by the company’s relevant body.

b) Fee and commission income and expenses:

Fee and commission income and expense are recognised on the income statement on the basis of different criteria according to their nature.

Financial fees and commissions, which include loan and credit origination fees, form part of the effective income or cost of a financial transaction and are recognised under the same heading as finance income or expenses, namely “Interest and Similar Income”. These fees and commissions, which are collected in advance, are recognised on the income statement over the life of the transaction, except for the portion offsetting the related direct costs. Fees and commissions offsetting related direct costs, which are understood as those that would not have arisen if the transaction had not been arranged, are recognised under “Other Operating Income” when the loan is taken out. Individually, the total amount of these fees and commissions may not exceed 0.4% of the principal of the financial instrument, subject to a maximum limit of €400, and any excess is recognised on the income statement over the life of the transaction. If the total amount of these fees and commissions does not exceed €90, they are recognised immediately on the income statement. In any event, related direct costs that are individually identified can be recognised directly on the income statement upon inception of the transaction, provided they do not exceed the fee or commission collected. These direct costs are recognised under “Other Operating Income – Financial fees and commissions offsetting direct costs” on the income statement (see Note 23). Non-financial fees and commissions arising from the provision of services are recognised under “Fee and Commission Income” and “Fee and Commission Expense” over the life of the service, except for those relating to services provided in a single act, which are accrued when the single act is carried out.

c) Non-financial income and expense:

These are recognised for accounting purposes on an accrual basis.

d) Deferred collections and payments:

These are recognised for accounting purposes at the amount resulting from discounting the expected cash flows to net present value at market rates.

e) Offsetting of balances

Financial asset and liability balances will be offset, and therefore reported on the balance sheet at their net amount, only if they originate in transactions for which there is a contractually or legally enforceable right to offset the amounts concerned and the entities concerned intend either to settle them on a net basis or to realise the asset and settle the liability simultaneously.

11

f) Transfers of financial assets

The accounting treatment of transfers of financial assets depends on the form in which the risks and rewards associated with the transferred assets are themselves transferred to third parties:

• If the risks and rewards of the transferred assets are substantially transferred to third parties (as would

be the case for unconditional sales, sales with an agreement to repurchase the assets at the fair value on the repurchase date, sales of financial assets with call options acquired or put options granted deeply out of the money, securitisations of assets in which the grantor does not hold any subordinated financing or grant any credit enhancements to the new holders, or other similar cases), the transferred financial asset is derecognised on the balance sheet, with simultaneous recognition of any right or obligation retained or created as a consequence of the transfer.

• If the risks and rewards associated with the transferred financial asset are substantially retained (as would be the case for sales with an agreement to repurchase the asset at a fixed price or at the selling price plus interest, securities loan contracts in which the borrower has the obligation to return the same or similar assets, securitisations of financial assets in which subordinated financing or other types of credit enhancement are maintained which substantially absorb the credit losses expected for the securitised assets, and other similar cases), the transferred financial asset is not derecognised on the balance sheet and continues to be valued according to the same criteria used before the transfer. However, the following are recognised without any offsetting between them:

- An associated financial liability for an amount equal to the consideration received, which is subsequently valued at its amortised cost; or, if the requirements indicated above for its classification under other financial liabilities at fair value through profit or loss are satisfied, at its fair value, in accordance with the criteria indicated above for this category of financial liabilities.

- Income from the financial asset transferred but not derecognised as well as the expenses of the

new financial liability.

• If the risks and rewards associated with the transferred financial asset are neither substantially retained nor substantially transferred (as would be the case for sales of financial assets with call options acquired or put options granted which are neither deeply in nor deeply out of the money, securitisations of assets in which the grantor takes on a subordinated financing or other type of credit enhancement for a portion of the transferred asset, and other similar cases), a distinction is made between the following two cases:

- If the Entity does not retain control of the transferred financial asset: in this case, the transferred asset is derecognised on the balance sheet, and recognition is given to any right or obligation retained or created as a consequence of the transfer.

- If the Entity retains control of the transferred financial asset: it continues to recognise the asset on the balance sheet for an amount equal to its exposure to the changes in value that it may experience, and recognises a financial liability associated with the transferred financial asset. The net amount of the transferred asset and the associated liability will be the amortised cost of the rights and obligations retained, if the transferred asset is measured by the amortised cost method, or the fair value of the rights and obligations retained, if the transferred asset is measured by the fair value method.

In accordance with the above, financial assets are derecognised on the balance sheet only when the cash flows that they generate have expired or when the associated risks and rewards are substantially transferred to third parties. g) Asset swaps

An “asset swap” means the acquisition of tangible or intangible assets in exchange for the delivery of other non-monetary assets or a combination of monetary and non-monetary assets.

The financial assets received in a financial asset swap are recognised at fair value, provided the swap transaction can be regarded as having a commercial nature, as defined by Circular 4/2004, and when the fair value of the received asset or, failing this, of the delivered asset can be reliably estimated. The fair value of the received instrument is determined as the fair value of the delivered asset plus, if applicable, the fair value of the delivered monetary counterparts, unless there is clearer evidence of the fair value of the received asset.

During the 2009 and 2008 financial years there were no asset swaps.

12

h) Impairment of financial assets

A financial asset is deemed to be impaired, and its carrying value is consequently adjusted to reflect the effect of its impairment, when there is objective evidence that events have occurred which give rise to:

• In the case of debt instruments (loans and securities representing debt), a negative impact on the

future cash flows that were estimated at the transaction date.

• In the case of equity instruments, the inability to recover the carrying value in full.

As a general rule, the carrying value of impaired financial instruments is adjusted with a charge to the income statement for the period in which the impairment becomes evident, and the reversal, if any, of previously recognised impairment losses is recognised on the income statement for the period in which the impairment is reversed or reduced.

When the recovery of any recognised amount is considered unlikely, the amount is written off on the balance sheet, without prejudice to any actions that the Entity may initiate to seek collection until its rights are definitively extinguished due to expiry of the statute of limitations period, forgiveness or any other cause. Details are given below of the criteria applied by the Entity to determine the possible impairment losses in each of the different categories of financial instruments, as well as the method used for calculating the hedges recognised for such impairment.

Debt instruments carried at amortised cost

The amount of an impairment loss incurred on a debt instrument is equal to the positive difference between its carrying value and the present value of its projected future cash flows. The market value of a quoted debt instrument is regarded as a reasonable estimation of the present value of its future cash flows.

In estimating the future cash flows of debt instruments, the following elements are taken into account:

• All amounts expected to be obtained during the remaining life of the instrument, including, if applicable,

those originating in the guarantees that underlie it (after deduction of the necessary costs for its foreclosure and subsequent sale). The impairment loss considers the estimated possibility of collecting the interest accrued, due and not collected.

• The different types of risk to which each instrument is subject, and

• The circumstances in which the collections are expected to be made.

Subsequently, these cash flows are discounted at the effective contractual interest rate of the instrument (if the rate is fixed) or at the effective contractual interest rate at the discount date (if the rate is variable).

With specific regard to impairment losses resulting from materialisation of the insolvency risk of the obligors (credit risk), a debt instrument is impaired due to insolvency:

• When there is evidence of a deterioration of the obligor’s ability to pay, which becomes evident either

because the obligor is in arrears or for other, different reasons, and/or

• Upon materialisation of country risk, understood as the risk due to circumstances other than normal commercial risk, associated with debtors resident in a given country.

Potential impairment losses on these assets are assessed as follows:

• Individually: for all significant debt instruments and for instruments which, although not individually significant, are not susceptible to being classified in homogeneous groups of instruments with similar risk characteristics in terms of the type of instrument, the debtor’s business sector and geographical area of activity, the type of guarantee or collateral, the age of past-due amounts, etc.

• Collectively: the Entity establishes distinct classifications on the basis of the nature of the obligors, transaction status, type of guarantee, age of past-due amounts, etc, and for each of these risk groups it establishes the impairment losses (“identified losses”) that it recognises on the financial statements.

13

In addition to the identified losses, the Bank recognises an overall impairment loss on risks classified as “standard”, which are not specifically identified and correspond to inherent losses incurred at the date of preparation of the financial statements. This loss is quantified by applying the statistical parameters established by Banco de España based on its experience and on the information available to it concerning the Spanish banking system, which is modified when circumstances make it advisable to do so. The method used to estimate the global impairment loss basically consists of aggregating the outcome of the various risks classified as “standard” on the basis of the statistical parameters established by Banco de España, less the specifically identified losses (specific provisions). When these specifically identified losses are greater, pursuant to applicable legislation the provision established for inherent losses (general provision for insolvencies) can be used, subject to certain limitations. On the other hand, debt instruments which, while not satisfying the criteria for individual classification as doubtful, show weaknesses that might result in significant losses for the Entity over and above the hedging against impairment due to specially monitored risks, are classified as substandard risks.

i) Financial guarantees and provisions established on them

”Financial guarantees” are defined as contracts whereby the Entity is required to make specific payments on behalf of a third party if that party is unable to pay, irrespective of the contractual form of the obligation: guarantee, technical or financial surety, irrevocable documentary credit issued or confirmed by the Entity, etc.

Financial guarantees are recognised upon execution at fair value (understood as the present value of the future cash flows) under “Lending investments – Loans and advances to customers”, with a balancing entry under “Financial liabilities at amortised cost – Other financial liabilities”. Financial guarantees, regardless of the principal, contractual form or other circumstances, are reviewed periodically in order to determine the credit risk to which they are exposed and, if appropriate, to consider whether any provision must be established for that risk. The credit risk is determined by applying criteria similar to those established for quantifying impairment losses on debt instruments carried at amortised cost, described in Note 2.h) above. The provisions established to cover these transactions are entered under “Provisions for Contingent Liabilities and Commitments” on the liabilities side of the balance sheet. The appropriation and recovery of these provisions are recognised with a balancing entry under “Contributions to Provisions (Net)” on the income statement. j) Leasing transactions Operating leases In operating leases, ownership of the leased asset and substantially all the risks and rewards incidental thereto remain with the lessor. When the Entity acts as lessor in an operating lease transaction, it presents the acquisition cost of the leased assets under “Tangible assets”, either as “Investment Property” or as “Property, Plant and Equipment – Leased out under an Operating Lease”, depending on the nature of the asses forming the subject of the lease. The depreciation policy for these assets is consistent with that for similar plant, property and equipment for own use, and income from leasing contracts is recognised under “Other Operating Income” on the income statement, on a straight-line basis. When the Entity acts as lessee in an operating lease transaction, the leasing expenses, including any incentives granted by the lessor, are charged to “Administrative Expenses – Other general administrative expenses” on the income statement, on a straight-line basis. k) Personnel expenses

Post-employment benefits and other post-employment benefits

Post-employment benefits are the sums paid to employees upon termination of their period of employment. Post-employment benefits, including those covered by internal or external pension funds, are classified as defined-contribution or defined-benefit plans, according to the conditions of the obligations concerned, taking account of all the commitments assumed both within and outside the terms formally agreed with employees.

14

The Entity must complete the Social Security payments relating to determined employees, or to their successors in title, in the event of retirement, death of spouses, death of parents, permanent incapacity or serious invalidity.

In accordance with the current collective agreement, MicroBank de “la Caixa”, S.A. (formerly Banco de Europa, S.A.) has the obligation towards employees who have been with the bank since before 8 March 1980, to supplement the Social Security contributions paid by its employees or their successors in title in the event of retirement, permanent incapacity, death of spouses or death of parents.

On 30 December 2002, the Bank externalised its pension obligations for current employees. The obligations entered into with its former employees are covered by means of an internal fund. In 2003, for the purposes of transferring staff to GDS-Cusa S.A. and CaixaRenting S.A., these two companies took over the obligations towards current employees.

The current value of these post-employment benefit obligations assumed by the Entity, and the manner in which those obligations are covered, are as follows:

2009 2008

Obligations assumed Current employees 188 174 Former employees 3,732 3,933 Total 3,920 4,107

Coverage Internal funds 3,732 3,933 Assets allocated to the coverage of obligations 188 174 Total 3,920 4,107

Unrecognised Actuarial gains or losses - - Cost of non-accrued past services - - Total - -

These amounts are recognised under “Provisions – Provisions for pensions and similar obligations” (Note 12).

On 31 December 2009 and 2008, actuarial valuations were made of the post-employment benefit obligations by applying the projected unit credit method and considering, as the estimated retirement age of each employee, the first age at which he or she is eligible for retirement. The most significant actuarial hypotheses used in these calculations for former employees are as follows:

2009 2008

Technical interest rate 4.00% 4.00% Mortality tables PERM/F 2000P PERM/F 2000P Annual rate of pension increase 2% 2% Annual rate of pay increase Not applicable Not applicable Cumulative annual increase in RPI 2% 2%

Assets allocated to the coverage of obligations or allocated to the plan are the assets with which the obligations are settled, and do not belong to the Entity. They are available only for the payment or financing of financing post-employment benefits and cannot devolve to the Entity.

The actuarial gains and losses are those that arise from differences between previous actuarial hypotheses and reality and, where applicable, those that arise from changes in the actuarial hypotheses used. At 31 December 2009 and 2008 there were no actuarial gains or losses not recognised by the Entity.

15

Post-employment benefit obligations are recognised on the income statement as follows:

i. Under “Interest and similar expenses” for the interest expense that corresponds to the increase produced during the financial year in the current value of the obligations due to the passing of time.

ii. Under “Contributions to Provisions (net)” for the actuarial gains and losses.

Termination benefits

In accordance with current legislation, the Entity is obliged to compensate employees who are dismissed without justified cause. There is no staff reduction plan in existence that makes it necessary to create a provision in this regard.

Credit facilities to employees

In accordance with Circular 4/2004, credit facilities made available to employees at rates below those of the market are considered to be non-monetary benefits and are calculated as the difference between market rates and the agreed rates. These items are recognised under “Administrative Expenses – Personnel Expenses”, with a balancing entry under “Interest and Similar Income” on the income statement. l) Income tax Expenditure on Spanish corporation tax is recognised on the income statement, unless it arises from a transaction whose results are recognised directly in equity, in which case the related income tax is recognised with a balancing entry in equity. Income tax expenditure for the year is calculated as the tax payable on the taxable profit for the year, adjusted for the changes arising during the year in the assets and liabilities recognised as a result of temporary differences, tax credits and allowances, and any tax losses (see Note 16).

The Entity considers that a temporary difference exists when there is a difference between the carrying amount of an asset or liability and its tax base. The tax base of an asset or liability is taken to be the amount attributed to that asset or liability for tax purposes. A taxable temporary difference is one that will generate a future obligation for the Entity to make a payment to the tax authorities. A deductible difference is one that will generate a future right to a refund or to make a smaller payment to the tax authorities. Tax credits and allowances are amounts that, after performance of the activity or obtaining of the profit or loss giving entitlement to them, are not used for tax purposes on the tax return until the conditions for doing so as established in tax regulations have been met, provided that the Entity considers it likely that they will be used in future periods. Current tax assets and liabilities are considered to be those amounts that are expected to be recovered from or paid to the tax authorities, respectively, within a period not exceeding 12 months from the date of their recognition. Deferred tax assets or liabilities, for their part, are considered to be those amounts that are expected to be recovered from or paid to the tax authorities, respectively, in future periods. Deferred tax liabilities are recognised for all taxable temporary differences. However, deferred tax liabilities arising from the recognition of goodwill are not recognised. The Entity recognises deferred tax assets arising from deductible temporary differences, tax credits and allowances or the existence of tax losses only if the following conditions are satisfied:

• Deferred tax assets are recognised only if it is considered likely that the Entity will obtain sufficient future taxable profit to be able to offset them; and

• In the case of deferred tax assets arising from tax losses, such losses have been generated by identified causes that are unlikely to be repeated.

No deferred tax asset or liability is recognised upon the initial recognition of an asset or liability, unless it arises in a combination of trades and, at the time of its recognition, it did not affect either accounting profit/loss or taxable profit/loss.

16

The deferred tax assets and liabilities recognised are reassessed at each balance sheet date in order to ascertain whether they still exist, and appropriate adjustments are made on the basis of the findings of the analyses performed. Since 2007, the Entity has paid Corporation Tax, under the Consolidated reporting system, within the Group whose dominant Entity is Caixa d’Estalvis i Pensions de Barcelona “la Caixa”, “la Caixa” intends to continue using the Consolidated reporting system in future years. m) Subsidies The Company statements for the subsidies received from the European Social Fund and from the “la Caixa” Welfare Projects are as follows:

• The social actions of the “la Caixa” Welfare Projects relating to the financing of disadvantaged groups are channelled through MicroBank de “la Caixa”. Consequently, and by virtue of a collaboration agreement, each year the “la Caixa” Welfare Projects transfers to MicroBank the funds that it has earmarked for partially defraying structural costs and the costs associated with covering defaults associated with the financing of disadvantaged groups. The funds received are recognised under “Other operating income” (See Note 23).

• The subsidies from the European Investment Fund are made to cover the losses arising from collapses of social and financial micro-credits granted during a given period of time. They are recognised on the income statement in proportion to the extent to which the Bank recognises the corresponding insolvency provisions corresponding to the social and financial micro-credits granted. The income obtained in this regard is recognised user “Other operating income” (see Note 23).

n) Tangible assets

Tangible assets for own use

“Property, plant and equipment for own use” comprises the assets, owned or acquired under financial leases, held by the Entity for present or future use for administrative purposes or for the production or supply of goods that are expected to be used over more than one economic period. This category includes the tangible assets received by the Company for the total or partial liquidation of financial assets representing collection rights against third parties and which it expects to use continuously for its own purposes, “Property, plant and equipment for own use” is recognised on the balance sheet at acquisition cost (revalued, for certain assets, in conformity with Transitional Provision One of Circular 4/2004), determined on the basis of the fair value of each consideration released, plus the sum of monetary disbursements made or promised, less:

• The corresponding accumulated amortisation; and

• If applicable, the estimated losses arising from a comparison between the net value of each item and the corresponding recoverable amount.

For these purposes, the acquisition cost of the foreclosed assets that come to form part of the Entity’s tangible assets for own use is compared with the net amount of the financial assets delivered in exchange for their foreclosure.

Depreciation is calculated using the straight-line method on the basis of the acquisition cost of the assets less their residual value. However, land containing buildings and other constructions is not depreciated since it is considered to have an indefinite life. The annual tangible asset depreciation charge is recognised under “Depreciation and Amortisation” on the income statement, and is basically calculated on the basis of the estimated years of useful life of the various assets, as detailed below:

Years of useful life Furniture 5-10 Computer equipment 4 Data processing equipment 5

At the end of each accounting period, the Entity assesses whether there is any internal or external indication that the net value of its tangible assets exceeds the recoverable amount. If this is the case, the carrying amount of the asset concerned is reduced to its recoverable amount, and future depreciation charges are adjusted in

17

proportion to the revised carrying amount and to the new remaining useful life, if the useful life has to be re-estimated. Any reduction in the carrying amount of tangible assets for own use is recognised, where necessary, under “Impairment Losses (Net) – Other Assets” on the income statement. Similarly, if there is an indication of a recovery in the value of an impaired tangible asset, the Entity recognises the reversal of the impairment loss recognised in previous periods by means of a corresponding credit under “Impairment Losses (Net) – Other Assets” on the income statement, and the future depreciation charges are adjusted accordingly. Under no circumstances may the reversal of an impairment loss raise its carrying amount above the amount at which it would have been stated if no impairment losses had been recognised in previous years.

Likewise, the estimated useful life of tangible assets for own use is reviewed at least each year with a view to detecting any significant changes, which, if they arise, are adjusted by a corresponding correction in the amortisation charge to the income statements of future years on the basis of the new useful life.

Upkeep and maintenance expenses on tangible assets for own use are charged to profits for the period in which they are incurred, under “Administrative Expenses – Other General Administrative Expenses” on the income statement.

Tangible assets that require a period greater than one year to be in conditions of use include, as part of their acquisition cost or production cost, the financial expenses that are payable before the fulfilment of operating conditions and that are drawn by the supplier or correspond to loans or other types of external financing directly attributable to their acquisition, manufacture or construction. The capitalisation of financial costs is suspended, where applicable, during periods in which the performance of the assets is interrupted, and ends on substantial completion of all the activities necessary for preparing the asset for its intended use. o) Intangible assets

Intangible assets are identifiable non-monetary assets without physical substance which arise as a result of a legal trade or are developed internally by the Entity. However, only intangible assets whose cost can be estimated objectively and from which it is considered likely that the future economic benefits will be obtained are recognised.

Intangible assets are recognised initially at acquisition or production cost and subsequently measured at cost less any accumulated amortisation and any accumulated impairment losses.

Other intangible assets

Intangible assets other than goodwill are recognised on the balance sheet at acquisition or production cost, net of accumulated amortisation and any impairment losses. Intangible assets may have an “indefinite useful life” when, on the basis of the analyses conducted on all relevant factors, it is concluded that there is no foreseeable limit to the period during which they are expected to generate net cash flows for the Entity, or a “finite useful life” in all other cases. Intangible assets with an indefinite useful life are not amortised, but at the end of each accounting period the Entity reviews, where applicable, their respective remaining useful lives, in order to ensure that these remain indefinite. Intangible assets with a finite useful life are amortised accordingly, applying criteria similar to those used for the amortisation of tangible assets. The annual amortisation charge for intangible assets with a finite useful life is recognised under “Depreciation and Amortisation” on the income statement. For assets with an indefinite useful life and those with a finite useful life, the Entity recognises any loss that may have occurred in the recorded value of those assets due to impairment, with a balancing entry under “Impairment Losses (Net) – Other Assets – Goodwill and other intangible assets” on the income statement. The criteria for recognition of impairment losses on these assets and, where applicable, recoveries of impairment losses recognised in previous years are similar to those applied to tangible assets for own use (see Note 2.n). p) Provisions and contingent liabilities

In preparing the Entity’s annual financial statements, the Directors differentiate between:

• Provisions: credit balances covering present obligations at the date of presentation of the balance

sheet arising from past events that could give rise to a loss for the Entity, which are considered as likely to occur and certain as to their nature but uncertain as to their amount and/or time of cancellation, and

18

• Contingent liabilities: possible obligations that arise from past events and whose existence depends on the occurrence or non-occurrence of one or more future events beyond the Entity’s control.

The Entity’s annual financial statements include all the material provisions with respect to which it is considered more likely than not that the obligation will have to be settled. Contingent liabilities are recognised in the Entity’s annual financial statements only if it is informed about them, in conformity with the requirements of Circular 4/2004 (see Note 18.a). Provisions - which are quantified on the basis of the best available information regarding the consequences of the event that gives rise to them, and are re-estimated at the end of each accounting period - are used to cover the specific obligations for which they were originally recognised, and are reversed in full or in part when those obligations cease to exist or are reduced. The accounting and release of the provisions considered necessary on the basis of the above criteria are recognised as charges or credits under “Contributions to Provisions (Net)” on the income statement. q) Cash flow statements The following terms are used in the presentation of cash flow statements:

• Cash flows: inflows and outflows of cash and cash equivalents, which are short-term, highly liquid

investments subject to a low risk of changes in value.

• Operating activities: the core activities of credit institutions and other activities that are not investment or financing activities. Operating activities also include the interest paid on any financing received, even though these are regarded as financing activities. Activities carried out on the different categories of financial instruments cited in Note 2.a, above are regarded as operating activities for the purposes of preparing these statements, with the exception, where applicable, of held-to-maturity investments, subordinated financial liabilities and strategic investments in held-for-sale equity instruments. For these purposes, investments are regarded as strategic when they are made with the intention of establishing or maintaining a long-term operating relationship with the investee on account of any of the situations that could result in determination of the existence of significant influence, without any such significant influence existing in reality.

• Investment activities: activities of purchase, sale or disposal by other means of long-term assets and other investments not included under “Cash and Cash Equivalents”, such as tangible assets, intangible assets, equity interests, held-for-sale non-current assets and their associated liabilities, and strategic investments in held-for-sale equity instruments and held-to-maturity debt instruments, as applicable.

• Financing activities: activities entailing changes in the size and composition of equity and of liabilities that do not form part of operating activities, such as subordinated liabilities.

r) Statement of changes in equity

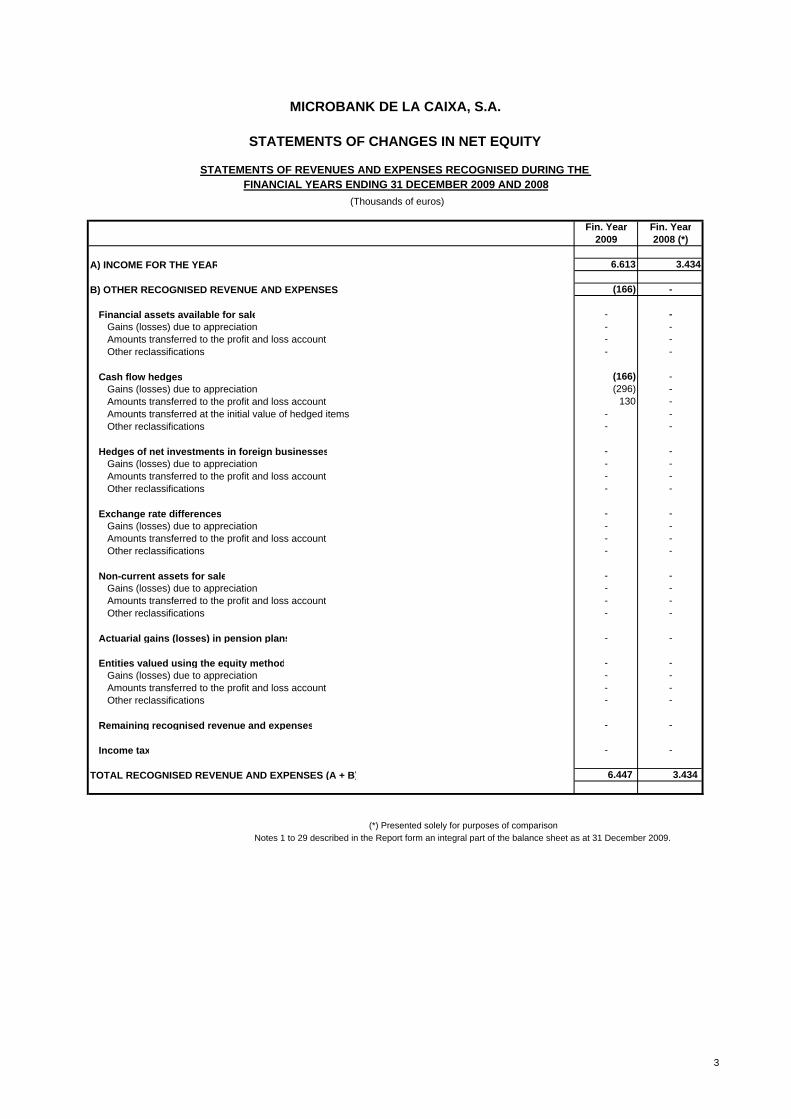

The statement of changes in equity presented in these annual financial statements shows all changes in equity that occurred during the financial year. This information is subdivided into two statements: the statement of recognised income and expenses, and the statement of total changes in equity. The principal characteristics of the information contained in both parts of the report are explained below: Statement of recognised income and expenses

This part of the statement of changes in equity shows the income and expenses generated for the Entity as a result of its activities during the year, distinguishing between items recognised as results on the income statement for the financial year and other income and expenses recognised directly in equity in accordance with the provisions of current legislation.

This statement therefore presents:

a) The income for the year.

b) The net amount of income and expenses temporarily recognised under valuation adjustments to

equity.

19

c) The net amount of income and expenses definitively recognised in equity.

d) The income tax payable in respect of the items cited in points b) and c) above. Changes in income and expenses recognised in equity as valuation adjustments are broken down, where applicable, into the following headings:

1. Valuation gains (losses): shows the amount of income, net of expenses incurred during the year,

recognised directly in equity. The amounts recognised under this item during the financial year are maintained under this item, even if they are transferred to the income statement in the same financial year, at the initial value of other assets and liabilities or are reclassified to another item.

2. Amounts transferred to the income statement: shows the amount of valuation gains or losses

previously recognised in equity, even if recognised in the same financial year on the income statement. 3. Amounts transferred to the initial value of hedged items: shows the amount of valuation gains or

losses previously recognised in equity, even if recognised in the same financial year at the initial value of the assets or liabilities as a result of cash flow hedges.

4. Other reclassifications: shows the amount of transfers made during the year between valuation adjustment items in conformity with the criteria established by current legislation.

The amounts of these items are presented gross, showing their corresponding tax impact under “Income Tax” on the statement, except as previously indicated for items corresponding to valuation adjustments for entities measured using the equity method. Statement of total changes in equity This part of the statement of changes in equity shows all changes in equity that occurred during the year, including those arising from changes in accounting policy and the correction of errors. This statement therefore shows a reconciliation of the carrying value, at the start and end of the year, of all items forming part of equity, grouping the changes by nature under the following headings:

a) Adjustments due to changes in accounting policy and adjustments made to correct errors: this includes

changes in equity arising from the retroactive restatement of financial statement balances due to changes in accounting policy or the correction of errors.

b) Income and expenses recognised in the year: shows, in aggregated form, the total of the above-

mentioned items recognised on the income statement. c) Other changes in equity: shows the other items recognised in equity, such as capital increases or

reductions, distribution of dividends, transactions with own equity instruments, payments with equity instruments, transfers between equity items and other increases/decreases in equity.

3. Risk management

Global risk management is essential for the business of any credit institution. At MicroBank, the purpose of this global risk management is to optimise the risk/return ratio, through the identification, measurement and assessment of risks and their ongoing consideration in the business’s decision-making process, always within a framework that enhances the quality of the services provided to customers. The risks incurred as a result of the Bank's activities are classified as follows: credit risk (arising from both commercial and investment banking activities); market risk (which includes structural balance sheet interest rate risk, the price or rate risk associated with treasury positions, and foreign exchange risk); liquidity risk; operational risk; and compliance risk. The same “la Caixa” model is applied to each of these types of risk, using a set of quantification and monitoring tools and techniques considered to be adequate and coherent with the standards and best practices for managing the financial risks of a financial institution. All operations within the sphere of risk measurement, monitoring and management are undertaken, with the knowledge and review of the Bank, by the various specialist areas of “la Caixa” and pursuant to the recommendations of the Basel Committee on Banking Supervision: “International Convergence of Capital Measurement and Capital Standards: A Revised Framework”, commonly referred to as Basel II, and the subsequent transposition of the corresponding EU directives and Banco de España Circular 3/2008 of 22 May.

20

a) Credit risk Credit risk arises in relation to the possibility of losses resulting from default of payment obligations by our customers in the repayment of their loans, in terms of both form and timescale. This risk, which is inherent to the activities of credit institutions, is the most significant risk on the Bank’s balance sheet and therefore the only one described in detail in this document. The Bank’s credit risk policy, as approved by the Board of Directors of MicroBank on 24 October 2007, is detailed below:

• In accordance with Banco de España Circular 4/2004, the Board of Directors approves the Bank’s credit risk criteria, adopting the same risk criteria as “la Caixa”, as the parent of the Group, contained in its credit risk measurement principles and policies, and assuming the same powers to grant risk operations.

• Although these criteria refer to a wider range of products than that currently handled by the Bank, they are adopted in a broad sense and with the expectation of an increase in the types of products handled.

• The same approval process applies to the Bank’s micro-credit rules on permitted operations, which detail the procedures for the granting, monitoring and any possible default of social and financial micro-credits. The Management Committee has the power to modify these rules by means of operational or procedural changes that do not affect the criteria and powers to which the aforementioned policies refer.

• There are other operational aspects to be monitored which are reflected in the application and granting policy for asset operations.

The Bank’s lending activities are essentially geared towards covering the financing needs of collectives with limited resources. To this end, the range of products aims to provide the market with three lines of micro-credits:

o Social micro-credits: the programme of social micro-credits responds to financing requests

channelled by MicroBank’s collaborating institutions, which provide their services to the requesting collectives and can also collaborate in the development of business plans for the projects and in giving support during their startup and implementation phases. These micro-credits involve small-scale loans of up to €15,000, or exceptionally up to €25,000, intended to finance self-employment projects set up by people who have no access to traditional financing and cannot provide any type of collateral.

o Financial micro-credits: these are aimed at entrepreneurs (individuals), falling within the category of micro-entrepreneurs, with annual turnover of less than €60,000. They are designed to provide financing for business ventures that create wealth and, more particularly, that create or preserve jobs and job stability, with a consequent contribution to social cohesion. These micro-credits are subject to maximum limit of €25,000 and are managed directly by the network of "la Caixa" branches, which cannot accept any type of collateral on them. The current financing policy aims to support self-employment and projects for the creation, consolidation or expansion of new and existing small businesses.

o Family micro-credits: this line of products aims to answer the needs of families by helping them to overcome temporary difficulties and facilitating personal development. These are unsecured loans of up to €25,000 for customers with a net annual income of up to €18,000 per borrower (maximum of two borrowers). These micro-credits are granted and managed through the network of “la Caixa” branches.

In order to make its entire product range available to customers, with the highest possible service quality and proximity, the Bank carries out its commercial activity through the network of “la Caixa” branches. To this end, the Bank has signed an Agency and Service Provision Contract with “la Caixa”, which covers all procedural and legal aspects governing this relationship, (Note 1.g) During the course of 2009, loans totalling €176,778,000 were granted, of which €2,751,000 were in Social Micro-credits, €40,688,000 in Financial Micro-credits and €133,339,000 in Family Micro-credits.

21

Granting procedure There are certain differences in the operational procedures for the granting and formalisation of social, financial and family micro-credits. The main points of these procedures are detailed below.

• Social micro-credits: The handling of applications for social micro-credits initially involves the collaborating Community Entities. These are able to provide the applicant with advice on drawing up the business plan, assessing the viability of the project and preparing the financing proposal. Subsequently, in all cases, they refer the applicant to a branch of “la Caixa”, which analyses the proposed project, evaluates its viability, and approves or rejects the operation, without any security other than the personal guarantee of the applicant.

• Financial micro-credits: these are granted directly by “la Caixa” branches to entrepreneurs who

approach them either directly or through the collaborating Community Entities, provided the applicant’s profile matches that established for this type of loan. The branches follow the acceptance, analysis and approval procedures established for this type of operation, and in all cases there is a requirement to attach a business plan or document explaining the project so that the intended purpose and viability of the proposed operation can be evaluated.

• Family micro-credits: these are granted directly by “la Caixa” branches, and are handled in accordance with the same analysis, approval and formalisation procedures as “la Caixa” personal loans.

Management of default The Investment and Risk Control Area oversees the acceptance and monitoring of the associated risk. This function is carried out through a process that allows the managers to have a complete view of the situation of each customer. In the case of social micro-credits, the collaboration of specialist personnel is drawn upon, in addition to the normal procedures used by “la Caixa”. These operations are handled on the basis of an individual case-by-case analysis. The procedure for financial micro-credits and family micro-credits is the same as that used by “la Caixa”. With the aim of achieving greater efficiency in recovery management, the Bank has signed a contract with GDS-Cusa, S.A., a member of the “la Caixa” group, for the provision of recovery services in relation to doubtful or unpaid debts and bankruptcies. It is also important to note that the Bank has taken over the agreement previously entered into between “la Caixa” and the EIF (European Investment Fund) whereby, under the MAP (Multiannual Programme for Enterprise and Entrepreneurship), the EIF covers 75% of defaults in social and financial micro-credits satisfying the admission criteria of the programme and granted between 1 July 2006 and 31 December 2007, up to a maximum of 11.25% of the portfolio covered by the said agreement, with a ceiling of €1,668,000. In the 2008 financial year, a new agreement was signed between the Bank and the EIF (European Investment Fund), similar to that signed in 2006. This new agreement falls within the scope of the CIP (Competitiveness and Innovation Framework Programme), and covers the same percentage of defaults as the previous agreement (75%) in relation to the same type of loans granted between 1 January 2008 and 31 December 2009, up to a maximum of 7.5% of the portfolio covered by that agreement, with a ceiling of €9,825,000. In the current financial year, the Bank and the EIF signed a renewal of the agreement in force until 31 December 2009. The renewal extended the agreement for a further 2 years, thus covering financial and social micro-credits satisfying the CIP admission criteria and granted between 1 January 2008 and 31 December 2011, up to a maximum of 7.5% of the portfolio covered by that agreement, with a new ceiling of €18,000,000. Meanwhile, the "la Caixa" Welfare Projects, through which the social micro-credit activity was first begun, will continue its economic collaboration with the Bank in developing and maintaining training programmes for community entities and assisting them by covering defaults in social micro-credits not covered by the EIF and other operating costs, thus helping to defray the expenses of the Bank's social initiatives. To this end, an agreement was signed between MicroBank and the “la Caixa” Welfare Projects covering the years 2008 to 2010.

22

b) Liquidity risk This is defined as any potential inability by the Entity to meet its payment commitments, even temporarily, due to a lack of liquid assets or inability to access the markets for refinancing at a reasonable price. This risk may be caused by outside factors due to financial or systematic crises, reputational problems or, internally, owing to an excessive concentration of liabilities due. The Entity is basically exposed to the daily requirements of its available liquid funds for its own contractual obligations to supply credit. In order to provide for efficient hedging of sources of liquidity, the Entity has been granted two loans from the Council Europe Bank (CEB) for a total of €80,000,000, of which €55,000,000 had been drawn as at 31 December 2009. The Entity also has another source of liquidity, obtained through a credit line engaged with Caixa d’Estalvis i Pensions de Barcelona, up to a limit of €30,000,000, and thus together with client funding, the Entity met its liquidity needs for financial year 2010 and thereafter, to be able to make the investment provided for in its budgets. For further hedging of its future liquidity needs, in financial year 2009 the Entity obtained several loans granted by Caixa d’Estalvis i Pensions de Barcelona to cover all investments made the previous month, while the line of credit mentioned above is used as a source of liquidity for the current year, with the monthly supply being completely hedged by the loans granted by Caixa d’Estalvis i Pensions de Barcelona. Following is a breakdown, by remaining instalments, of the balances of specific items on the Entity’s balance sheet for financial years 2009 and 2008, not including the corresponding valuation adjustments: 31 December 2009

(Thousands of euros)

Sight Up to 1 month

Over 1 month to 3

months

Over 3 months to 12

months

Over 1 year to 5

years Over 5 years Total

Cash and deposits with central banks - - - - - - -Deposits with credit institutions 6,193 - - - - - 6,193Loans to customers 39 6,433 12,955 53,498 155,527 9,236 237,688Debt instruments

- - - - - 12 12

Assets 6,232 6,433 12,955 53,498 155,527 9,248 243,893 Deposits from central banks - - - - - - -Deposits from credit institutions - 3,367 3,210 18,821 93,150 9,404 127,952Customer deposits 1,580 9,599 - - - - 11,179Remaining liabilities

- 112 - - - - 112

Liabilities 1,580 13,078 3,210 18,821 93,150 9,404 139,243 Liquidity gap by tranche 4,652 (6,645) 9,745 34,677 62,377 (156) 104,650Accumulated liquidity gap

4,652 (1,993) 7,752 42,429 104,806 104,650 104,650

23

31 December 2008

(Thousands of euros)

Sight Up to 1 month

Over 1 month to 3 months

Over 3 months to 12 month

s

Over 1 year to 5 years

Over 5 years Total

Cash and deposits with central banks - - - - - - -Deposits with credit institutions 114 - - - - - 114Loans to customers 11 3,408 7,022 30,635 96,559 7,744 145,379Debt instruments - - - - - 12 12Assets 125 3,408 7,022 30,635 96,559 7,756 145,505 Deposits from central banks - - - - - - -Deposits from credit institutions - 39,277 - 1,502 4,286 3,214 48,279Customer deposits 949 1,098 - - - - 2,047Remaining liabilities - 242 - - - - 242Liabilities 949 40,617 - 1,502 4,286 3,214 50,568 Liquidity gap by tranche (824) (37,209) 7,022 29,133 92,273 4,542 94,937Accumulated liquidity gap (824) (38,033) (31,011) (1,878) 90,395 94,937 94,937

c) Interest rate risk Changes in interest rates may have two effects on the Entity’s financial instruments: their change in value, or change in the future cash flows to which they give rise. For example, fixed-rate instruments or those determined at the time of contracting are typically subject to the first effect. By contrast, instruments whose appreciation is determined over their lifetime in a manner referenced to market conditions may suffer from the second effect. All lending transactions are awarded at a fixed rate, and therefore the Entity seeks to obtain financing at fixed rates (natural balance hedges) or engage in IRS (Interest Rate Swaps), by which it converts its variable-rate financing to fixed-rate financing. In this way, the financing of future cash flows is predictable. The Entity has financial instruments that are exposed to unexpected movements in interest rates, which may, in the end, result in unexpected variances in financial margins if, as is typical in banking activity, total liabilities or off-balance-sheet items are subject to temporary shifts due to revaluation periods or different asset maturity dates. In order to establish an efficient and stable hedge over time for interest rate risk, which is affected to a greater extent by the loan granted by the CEB and by lending policy, an agreement has been entered into with “la Caixa” consisting of the monthly provision of a loan granted for the total investment made during that month by MicroBank de “la Caixa,” S.A., at an interest rate of Euribor plus a spread of 0.5% corresponding to that of the day the loan was granted, which permits the conversion of variable rate risk into fixed rate risk. . This hedging system prevents shifts in interest rates, and thus allows for maximum adjustment of the ratio between the Entity’s investment and financing. The Entity has also entered into an IRS to hedge the variable interest rate risk of the loan granted by the CEB. Thus, the Bank’s balance sheet is presented through a matrix of maturities or revisions, without taking valuation adjustments into account:

24

31 December 2009

Thousands of euros Periods until the review of effective interest rate or maturity

Up to 1 month

1 to 3 months

3 to 6 months

6 to 12 months

Over 1 year

Assets sensitive to interest rate risk Deposits with central banks - - - - - Deposits with credit institutions 6,193 - - - - Loans to customers 16,825 19,619 26,621 44,741 125,934 Debt instruments - - - - - Total sensitive assets 23,018 19,619 26,621 44,741 125,934 Liabilities sensitive to interest rate risk Deposits from central banks - - - - - Deposits from credit institutions 1,632 3,219 4,685 14,221 99,420 Customer deposits 1,600 1,191 783 954 6,652 Long-term funding 7,600 8,862 12,024 20,209 56,883 Total sensitive liabilities 10,832 13,272 17,492 35,384 162,955 Sensitivity measures Difference: Assets – Liabilities 12,186 6,347 9,129 9,357 (37,021) Accumulated difference: Assets – Liabilities 12,186 18,533 27,662 37,019 (2)

31 December 2008

Thousands of euros

Periods until the review of effective interest rate or maturity Up to 1 month

1 to 3 months

3 to 6 months

6 to 12 months

Over 1 year