microfinance and financial inclusion conference ucsp

TRANSCRIPT

GLOBUSManagement & Advisory Services

MICROFINANCE AND FINANCIAL INCLUSION

Importance and Perspectives

Luis GárateMicrofinance SpecialistArequipa, 01 April 2015

Agenda

Importance

What Financial Inclusion means?

How is going on in Peru? Financial System Microfinance Institutions

What else to do?

IMPORTANCE … Financial inclusion is a key factor to improve the life quality

and the economic development

In turn, the microfinance industry is demonstrating to be an efficient mechanism to reach the financial inclusion vision

Poor Population 2.5 Billions

Microcredit’sclients

150 millions

Rate6%

World Poor Population 12 millions

Microcredit’sclients

4.4 millones

Rate36.7%

Peru

… IMPORTANCE

The society is increasingly concerned about the relevance of the Financial Inclusion. As result, the gap between people with and without access to financial services is being progressively reduced.

However,

Does not exist consensus about its definition

What Financial Inclusion means?

So far, several terminology has been used when referring to financial inclusion:

Bank the unbanked, Democratization of financial services, Decentralization of financial services, Banking penetration, Financial deepening, Access to Finance, etc.

Include the Excluded

Concepts The poverty is determined by an diversity

of exclusions / absences of basics goods and services necessary to enable quality-of-life.

As opposite, inclusion allows the access to goods and services to alleviate those exclusions.

Proposed DefinitionsCenter for Financial Inclusion (*)

“Full financial inclusion is a state in which all people who can use them have access to a full suite of quality financial services, provided at affordable prices, in a convenient manner, and with dignity for the clients … including disabled, poor, rural, and other excluded populations”. _________________________(*) Center for Financial Inclusion at Accion International, Financial Inclusion: What’s the Vision?, page 1.

Proposed Definitions

United Nations (*)

“… a continuum of financial institutions that, together, offer appropriate products and services to all segments of the population. This would be characterized by:

a) access at a reasonable cost of all households and enterprises;b) sound institutions, guided by appropriate internal management systems,

industry performance standards, and performance monitoring by the market, as well as by sound prudential regulation where required;

c) financial and institutional sustainability; andd) multiple providers of financial services, wherever feasible, so as to bring

cost-effective and a wide variety of alternatives to customers.____________________________(*) United Nations 2004, Building Inclusive Financial Sectors for Development, Page 17.

Proposed Definitions

Superintendencia de Banca y Seguros (Peru)

“financial inclusion is the access and sustainable use of a range of financial products and services, including credits, savings accounts, insurance, retirement pension and payment’s services, among others”.

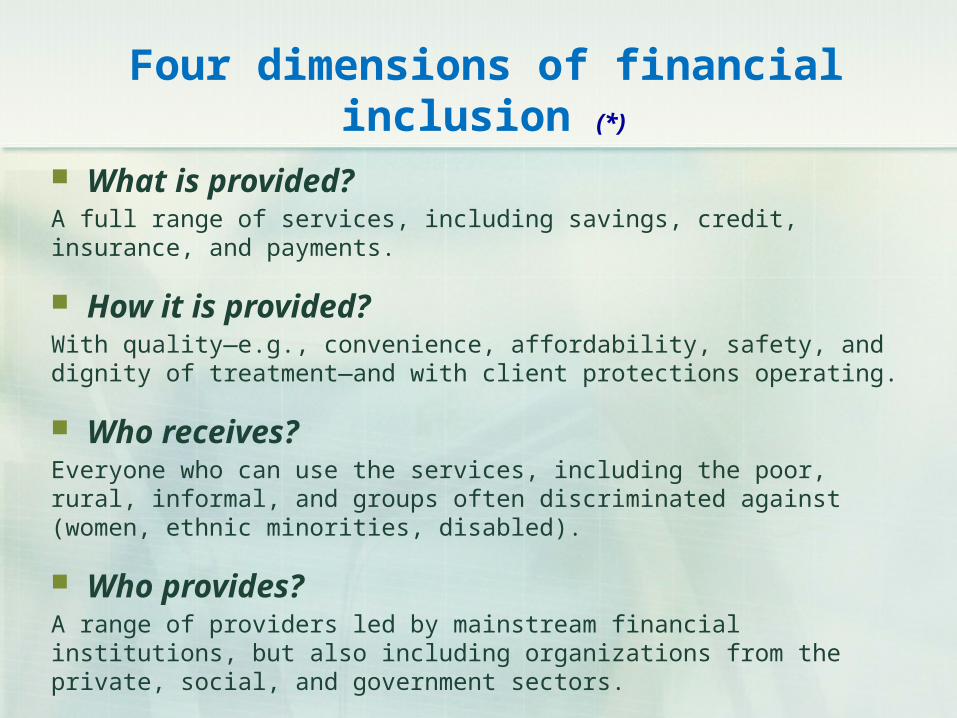

Four dimensions of financial inclusion (*)

What is provided?A full range of services, including savings, credit, insurance, and payments.

How it is provided?With quality—e.g., convenience, affordability, safety, and dignity of treatment—and with client protections operating.

Who receives?Everyone who can use the services, including the poor, rural, informal, and groups often discriminated against (women, ethnic minorities, disabled).

Who provides?A range of providers led by mainstream financial institutions, but also including organizations from the private, social, and government sectors. _____________________________(*) Center for Financial Inclusion at Accion International, Financial Inclusion: What’s the Vision?

How is going on in Peru?

Expanding levels of financial intermediation, as result of the increasing volume of loans and deposits.

However, the size of the Peruvian financial system is still relatively small.

Fuente: SBS, Perú Indicadores de Inclusión Financiera, Junio 2014, Pág. 8

Banking Channels

Offices: Branches, outlets ATMs Correspondent Agents (Correspondent cashiers) POS Internet banking Mobile banking

Access to Financial Services

The expansion strategy is based on increasing use of correspondent cashiers and less use of traditional banking offices.

Fuente: SBS, Perú Indicadores de Inclusión Financiera, Junio 2014, Pág. 9

Increasing banking services coverage

Créditos Ahorros

The new modalities of banking attention allow that millions of persons located in distant places may access to services provided by the Banks.

. But . . . .

Fuente: SBS, Perú Indicadores de Inclusión Financiera, Junio 2014, Pág. 14

Coverage at Districts level

… the financial system reaches a fragment of the population only.

The 49% of the districts at national level do not count with the presence of the financial system.

Fuente: SBS, Perú Indicadores de Inclusión Financiera, Junio 2014, Pág. 12

Transactions performed on banking offices are being swapped by transactions performed on alternative channels, especially on banking agents.

Changes on Behavioural patterns of banking users

Banking Agents Peruvian Banks have created wider networks of retailer

entrepreneurs operating outside of the traditional banking branches or outlets. There are around 10,000 banking agents (pharmacies, groceries, and other retailer shops).

Banks are using technology to ensure efficient and safe interaction between the bank and their clients throughout banking agents.

The expansion of point of services, both physical and non-physical is vital step in benefit of the market segments that so far have not access to products and services offered by the banks.

THE MICROFINANCE INDUSTRY

Rather than the banks, the MFIs have more presence in the poorest regions

Fuente: SBS, Perú Indicadores de Inclusión Financiera, Junio 2014, Pág. 20

Peru: Microfinance World’s Leader

During seventh consecutive years Peru have been ranked as the country with more favourable conditions for the microfinance industry, according to the world ranking conducted by the GLOBAL Microscope, that included 55 countries.

“Peru is a leader in developing innovative and co-ordinated strategies to support financial inclusion across various objectives, ranging from increasing banking penetration, to improving financial literacy, to reducing transaction costs and encouraging the use of technology”. (Global Microscope, 2014, pag. 56)

Main Characteristics of the Microfinance Sector in Peru

The Peruvian microfinance sector is one of the most developed in the region attributable to:

The effective supervision capability of the SBS. The favourable legal framework for regulated and non-

regulated MFIs. The authorities are committed to use the microfinance as

vehicle to expand the financial inclusion. Adequate balance between easy access to the marked and

prudent credit risk management. The absence of subsidised competitions from the public

sector.

Highlights of the Microfinance Sector in Peru …

Is a dynamic sector Significant competition growth in the last years

Continuous operational development and expansion of point of services

… Highlights of the Microfinance Sector in Peru

• “CMACs” and “Financieras” are leading in volume and number of credits.• The credit average differs significantly among the types of entities.• “EDPYMEs” and “Financieras” show healthier levels of portfolio quality.

Source: COPEME, Reporte Financiero de Instituciones de Microfinanzas, September 2014.

… Highlights of the Microfinance Sector in Peru

High accounting standards and transparency for regulated MFIs Strict requirements for external auditory, financial

statements reports and effective interest rates. Different standards among the MFIs, where the

financial information availability is generally acceptable and consolidated by the MFI’s networks.

Transparency in calculating and publishing interest rates.

What else to do?

Despite the significant microfinance sector growth, still enormous challenges in relation to rural financial inclusion.

What else to do?Financial Institutions

Better understanding of the demand (financial needs) and appropriated services design for excluded segments.

Understand the reasons why the poor clients do not look for - or not get- more Access to formal financial services.

The innovative capability of the financial institutions and MFIs joined with the technological developments could be key to offer profitable financial services to the excluded segment or underserved. Doing it, the microfinance operations will impulse even more their services to underserved markets.

What else to do?

Framework Regulations Regulations about transparency (related to rates/fees charged

by agents, claim channels and processes accessible to users)

Use of agents to expand the Access to banking accounts (this is possible with adequate financial education)

Improve the customer protection

What else to do?Financial Education

Financial education programs (secondary schools, teachers training), that at the end would improve the customers decisions, which is beneficial to the financial inclusion process

The knowledge of the regulation is key to for innovative microfinance products development oriented to satisfy their client’s needs. In this sense, is convenient to deliver disseminating activities related to those regulations.

Banking Agents training in order to offer consistent, reliable and quality services.

Opportunities

Mobile Banking Mobile phones / Inhabitants 95% Debtors / Inhabitants 26%

There are above 29 millions of active mobile phone accounts (it means a density of 95%). The mobile phone penetration differs significantly between urban and rural zones as well as between regions with higher or lower income levels.

In Peru, the coverage of mobile networks in rural zones with higher poverty levels is relatively low. This fact limits the potential to implement mobile banking services in that regions.

Opportunities The MFIs transaction's capacity is limited and they are

not yet prepared to operate with huge quantity of transactions in real time.

Electronic Money – Mobile Money The recent legislative initiative (Law Nº 29985) intends to

promote the financial inclusion with electronic money and mobile money.

However, protocols for claim’s processing have not been foreseen. Utmost administrative instance could be the SBS, OSIPTEL or INDECOPI, depending on the case.

Opportunities

Non-Banking Cashiers (Agents) The figure of non-banking cashiers is defined in

the Peruvian legislation stipulating solvency, safety, risk control and due information.

The regulation about basic accounts promote the deepening of financial services, allowing the non-banking cashiers to open that kind of accounts oriented to the less income population segment (SBS resolution Nº 2108- 2011).

Final Notes: Thoughts

The mobile money combined with banking agents or cash correspondents are cost-efficient as increase the offer of financial services with a lower cost in comparison with other more costly channels like the banking offices (branches).

This scheme could contribute to reduce the cost of the financial services as well as lower transactional cost for both clients and financial institutions.

Final Notes: Thoughts Not all MFIs count with the dimension and resources

(financial, staff and technology) to implement mobile money services. Therefore, it would be convenient that institutions counting with such resources, could supply their computerized platform to the MFIs. Doing it, the MFIs could offer those services.

For instance: Banco de la Nacion >>> informatics Platform Mobile operators >>> mobile platform Networks (Asomif, FEPCMAC, Copeme) >>> Training

Thanks