microfinance clients /services and market niches · pdf filemicrofinance clients,...

TRANSCRIPT

MICROFINANCE NETWORK

MICROFINANCE CLIENTS,

PRODUCTS/SERVICES AND MARKET NICHES:

WHAT are we delivering? HOW are we delivering? WHO are we reaching?

Summary of the MicroFinance Network Conference on “Microfinance Clients, Products/Services, and

Market Niches”

Convened in Bali, Indonesia October 7-10, 2003

Edited by Kelly Hattel

2004

MicroFinance Network The MicroFinance Network is a global association of microfinance institutions committed to improving the quality of life of the poor through the provision of credit, savings, and other financial services. Network members believe in applying a commercial approach to the establishment of sustainable financial institutions that reach large volumes of clients who are not served by traditional financial institutions. The MicroFinance Network serves as a vehicle for facilitating the information flow from leading microfinance organizations to other microfinance practitioners through international conferences, technical exchanges and publication of best practice materials. The Network is committed to expanding the frontier of microfinance by challenging member practitioners to new levels of excellence and, where regulatory frameworks exist, to become regulated financial institutions. Number of Members: 29 microfinance institutions, 1 second-tier institution and 2 support institutions in 18 countries Total Loan Portfolio: US$ 2.2 billion (2002)

Total Number Borrowers: 9.1 million (2002) Steering Committee: Carlos Labarthe, Compartamos; James Obama, PRIDE Tanzania; Jason Meikle, FINCA Microcredit Company; Maria Otero, ACCION International; Martin Connell, Calmeadow; Md. Shafiqual Choudhury, ASA

Regulated Financial Institutions

ACLEDA Bank, Cambodia Compartamos, Mexico K-REP Bank, Kenya Banco ADEMI, Dominican Republic Cooperativa Emprender, Colombia Los Andes, Bolivia BancoSol, Bolivia FINAMERICA, Colombia Mibanco, Peru Bandesarrollo, Chile FINCA Microcredit Company, PRODEM FFP, Bolivia BRI Unit Desa, Indonesia Kyrgyzstan Share Microfin Limited, CERUDEB, Uganda Equity Building Society, Kenya India Citi Savings and Loan, Ghana Kafo Jiginew, Mali SogeSol, Haiti

Non-Governmental Organizations

ABA, Egypt BRAC, Bangladesh PRIDE Tanzania Al Amana, Morocco Constanta, Georgia Tanzania ASA, Bangladesh Fundusz Mikro, Poland TSPI, Philippines

PADME, Benin UMU, Uganda

Support Institutions

ACCION International, USA Calmeadow, Canada

MICROFINANCE CLIENTS, PRODUCTS/SERVICES AND MARKET NICHES:

WHAT are we delivering? HOW are we delivering? WHO are we reaching?

Summary of the MicroFinance Network Conference on “Microfinance Clients, Products/Services, and

Market Niches”

Convened in Bali, Indonesia October 7-10, 2003

Edited by Kelly Hattel

2004

Microfinance Clients, Products/Services and Market Niches

i

TABLE OF CONTENTS

TABLE OF CONTENTS ........................................................................................i

LIST OF ACRONYMS AND DEFINITIONS .........................................................iii

FOREWORD ........................................................................................................v

INTRODUCTION ..................................................................................................1

DEDICATION: ..................................................................................................................................3

WELCOME...........................................................................................................5

THEME I: WHO ARE WE REACHING? HOW DO WE KNOW WHO OUR CLIENTS ARE?....................................................................................................7

1. Who are our Clients? ................................................................................................................8 1.1 Serving a Range of Clients – Starting with the Poorest..........................................................8 1.2 The Creation of a Multi-product Bank to Foster Microfinance ................................................9

2. Knowing our Clients through Assessment Tools ................................................................11 2.1 Poverty Assessment Tools – The ACCION Approach .........................................................11

THEME II: WHAT KINDS OF SERVICES & PRODUCTS ARE WE DELIVERING?....................................................................................................17

1. Specialization or Diversification .............................................................................................17 1.1 PRIDE Tanzania – A Single-Product Example.....................................................................19 1.2 Uganda Microfinance Union (UMU)......................................................................................22 1.3 An MFI caught in the middle – what approach to take? .......................................................24

THEME III: WHAT KINDS OF SERVICES & PRODUCTS ARE WE DELIVERING?....................................................................................................27

1. The Experience of Bank Rakyat Indonesia (BRI) – Simple Products, Big Impact.............27

2. Housing Microfinance in Mibanco and Other ACCION Affiliates........................................30

THEME IV: HOW ARE WE EVALUATING MFIS?.............................................33

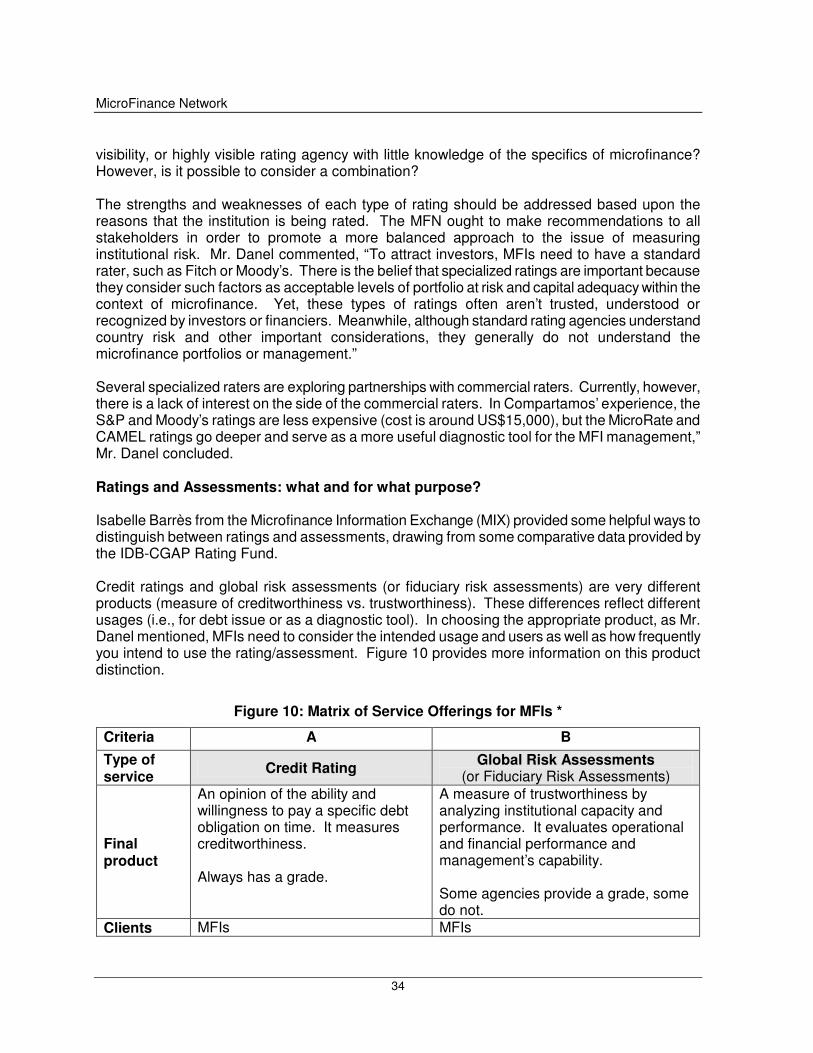

1. Commercial and Microfinance Ratings/ Ratings and Assessments – What is the

MicroFinance Network

ii

Difference?....................................................................................................................................33

2. Benchmarking and Transparency...........................................................................................37

THEME V: HOW ARE MFIS DELIVERING SERVICES & PRODUCTS? - METHODOLOGY............................................................................................... 41

1. Models and Modes ..................................................................................................................41 1.1 Share Microfin Limited (SML) – An Evolving Model .............................................................41 1.2 ASA – A Model of Simplicity .................................................................................................44

THEME VI: HOW ARE MFIS DELIVERING SERVICES & PRODUCTS? – FOCUS ON EFFICIENCY .................................................................................. 51

1. Use of Staff Incentives ............................................................................................................51 1.1 Key Observations of Staff Incentive Schemes .....................................................................51 1.2 Alexandria Business Association (ABA) ...............................................................................53 1.3 Building a Path to Increased Productivity – Staff Incentives at Centenary Rural Development Bank, Uganda.......................................................................................................55 1.4 Incentives for both Staff and Clients – Share Microfin Limited.............................................60

2. Efficiencies Through Investment Capital: A Means to Encourage Expansion of Commercial Banking in Microfinance ........................................................................................64

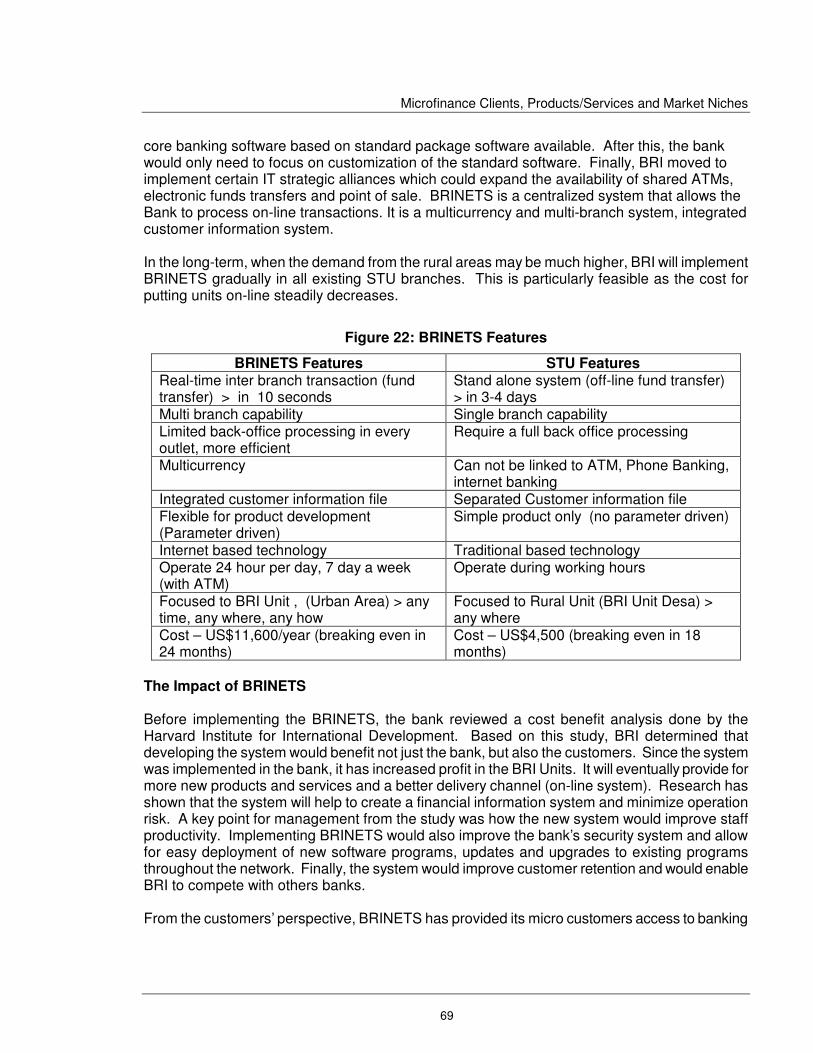

3. How are MFIs Delivering Services/Products – New Products, New Technologies ..........66 3.1 BRINETS for Delivering BRI Unit’s Products and Services..................................................66 2.2 Innovative Use of Technology to Build a Market ..................................................................70

CONCLUSION ................................................................................................... 75

ANNEX I: CONFERENCE AGENDA.................................................................. 77

ANNEX II: SPEAKER BIOGRAPHIES............................................................... 79

ANNEX III: PARTICIPANT LIST ........................................................................ 85

Microfinance Clients, Products/Services and Market Niches

iii

LIST OF ACRONYMS AND DEFINITIONS

ACP Acción Comunitaria del Perú APS Autonomous Points of Sale ATM Automatic Teller Machine BRBD Bangladesh Rural Development Board BRI Bank Rakyat Indonesia BRINETS BRI Integrated Network and Information System CAMEL Capital Adequacy, Asset Quality, Management, Earnings, and Liquidity

Management CGAP Consultative Group to Assist the Poorest EFT Electronic Funds Transfer EO Extension Officer FFP Fondo Financiero Privado (Private Financial Fund) FINCA Foundation for International Community Assistance FFP Fondo Financiero Privado, Private Financial Fund IDB Inter-American Development Bank IFC International Finance Corporation IT Information Technology LSMS Living Standards Measurement Survey MBB MicroBanking Bulletin MIX Microfinance Information eXchange MFI Microfinance Institution MFN MicroFinance Network MIF Multilateral Investment Fund MIS Management Information System NGO Non-Governmental Organization NORAD Norwegian Agency for Development PKSF Palli Karma Sahayak Foundation POS Point of Sale PRIDE Promotion of Rural Initiatives and Development Enterprises PRPS Performance Related Payment Scheme RLF Revolving Loan Fund SATM Smart Automatic Teller Machine SGL Solidarity Group Lending SOGEBANK Societé Generale Haitienne de Banque SOGESOL Societé Generale de Solidarite STU Teller Unit System UMU Uganda Microfinance Union USAID United States Agency for International Development VSAT Virtual Satellite $ Refers to US$ if not otherwise specified

MicroFinance Network

iv

Microfinance Clients, Products/Services and Market Niches

v

FOREWORD The MicroFinance Network is a global association of leading microfinance practitioners. The Network provides a forum where the most advanced microfinance institutions can convene to engage in high level discussions that allow them to learn from each other’s experiences. Each year, the executive directors of these institutions meet for several days in one of the member countries to discuss the most important issues in the industry. The 10th annual conference of the Network was held in Bali, Indonesia in October 2003. This year’s topics focused on service delivery. The conference addressed the following questions:

• What do we know about our clients? What do we know about the poverty level of our clients?

• What products are we offering? Under what circumstances do we add new products? How do new products affect our institutions?

• What have we learned about how to deliver with greater efficiency? What have we learned about customer satisfaction?

The Network would like to extend a special thanks to Mr. Rudjito, President Director, Bank Rakyat Indonesia, who helped to host and facilitate this year’s conference. He and his staff contributed a great deal of personal and professional time to ensure a dynamic and professional meeting of the members of the MicroFinance Network. The Network also would like to thank the special guests who joined us during the conference. We were honored to have Mr. I Gusti Made Oka, President and Founder of Bank Dagang Bali, a pioneer in commercial microfinance, welcome us to his native island and participate in the conference. The Network would also like to thank the two other invited guests, Isabelle Barrès from the Microfinance Information eXchange (MIX) and Leesa Shrader, formerly with the Microfinance Centre of Poland, both of whom provided valuable perspective to the discussions held during the conference. The editor of this report thanks Beth Rhyne and Patty Lee Devaney of ACCION International and Isabelle Barrès of the MIX for taking time to review this document and for providing valuable comments on the final draft. Finally, the MicroFinance Network would like to thank all of its members who contributed to making the conference a success, reaffirming the relevance of this very special forum of leaders in the field of microfinance.

MicroFinance Network

vi

Microfinance Clients, Products/Services and Market Niches

1

INTRODUCTION The 10th anniversary of the founding of the MicroFinance Network is a good time to reflect on what has been accomplished to date and what the future holds for the Network. The members of the MicroFinance Network are among the strongest microfinance institutions (MFIs) around the world – those that are setting the pace, forging new paths, and providing leadership in their countries and regions. The annual MFN conference is a unique opportunity to meet in a setting that encourages frank and open exchange. The Network was founded based on a common interest in the transformation of non-governmental organizations into regulated financial institutions and its origins are grounded in three concerns shared by all its members:

• Keeping our mission of establishing sustainable financial institutions • Meeting the challenge of scale in reaching the poor • Making microfinance permanent

From the outset, Network members turned to financial principles applied by sound financial institutions as the basic tenets behind microfinance. The application of these principles – what we came to call the financial systems approach – made permanence possible by emphasizing financial viability and scale, and establishing permanent sources of funding for microfinance institutions. This shared vision has remained constant in the Network. This global network is committed towards a commercial model, inspired by the member-pioneers, BRI and BancoSol. The microfinance institutions in the Network have gathered annually since it’s founding in 1994 at a BancoSol-hosted workshop in Bolivia. Since then, as a formal Network, members met in South Africa, Canada, the Philippines, Egypt, Bangladesh, the United States, Poland, and this year in Indonesia. These conferences address issues key to arriving at our shared goals, engage members in discussion and debate, and use presentations by members to inform and challenge each other. At times the Network has opened its meetings for a broader attendance. Hundreds benefited from the MFN conference on Governance in 1998, and the second conference on Commercialization in 2001. The MFN has taken on key issues and provided leadership in the field, sharing the experiences of its members and voicing key support for the commercial model. Its work has continued to develop along several significant paths, and the MFN has succeeded in:

1. Gathering the best information on key issues, such as transformation of NGOs to regulated institution and supervision and regulation of MFIs;

2. Developing standards that extend to the field in areas such as internal controls, and governance;

3. Facilitating exchanges among its member institutions;

MicroFinance Network

2

4. Offering a broad array of publications, including manuals on topics that are essential for best practice in microfinance.

It is particularly interesting that the Network is agnostic about methodology. Its members utilize all the leading methodologies in microfinance – village banking, solidarity groups and individual loans. Their experience highlights the often ignored dictum that it is the best application of a methodology, and not the methodology itself, that yields results. As the Network completes its first ten years, it is a good time to ensure that the Network will continue its path-breaking work, that it is well-oriented to maintain its position of leadership and that it will continue to influence the field in general. We must see ourselves as social entrepreneurs, poised to make an increasingly profound impact on the lives of poor families. We have the opportunity to do so because our work combines finance with development in a synergy that is seldom accomplished. This Network helps us do that. This report provides a summary of the presentations and discussions of the Microfinance Network members at this year’s annual conference. Rather than provide a transcript of the proceedings, this report organizes the ideas and discussion topics to draw out the key issues. For some sections, presentations are included in their entirety. In other sections, the ideas are presented as key points generated from the rich discussion. The leading microfinance institutions from around the world that comprise the MicroFinance Network have made substantial progress in extending financial services to unserved markets. However, each MFI recognizes that there is much that can be learned from one another. This report seeks to provide insight for the members of the MicroFinance Network and other practitioners who are open to new ideas and learning from the successes and challenges of others. Maria Otero Chair, Steering Committee MicroFinance Network Washington, DC, USA December 2003

Microfinance Clients, Products/Services and Market Niches

3

DEDICATION:

The MicroFinance Network dedicates this conference summary to Nabil El Shami, for his committed service to the MicroFinance Network since its inception. We recognize his leadership on the Steering Committee, as well his many contributions to the industry as a whole. We wish him all the best in his retirement.

MicroFinance Network

4

Microfinance Clients, Products/Services and Market Niches

5

WELCOME

Bank Rakyat Indonesia –Conference Host At the opening reception of the 10th Annual Conference of the MicroFinance Network, Mr. Rudjito, President Director of Bank Rakyat Indonesia (BRI), welcomed guests with the following words: “Starting tomorrow, you will work on important issues and challenges of microfinance. I believe that having this conference in Indonesia is the right choice because we have a history of rich experience in commercial microfinance. With a population of over 220 million people on over 17,000 islands with 300 types of dialects, BRI was established over a century ago in 1895 in Java, representing the beginning of rural finance in Indonesia. In the 1970’s, BRI’s microfinance operations served as a supply-driven channel of government support. This proved to not be sustainable. From this model evolved a demand-driven product based on the principles of commercial banking. BRI has had many successful experiences in dealing with low-income people. During its long journey, BRI has overcome many different circumstances – whether political, social, economic or technological in nature. BRI also has experienced a severe economic crisis which started in 1997 and still exists until now. However, our work in microbanking consistently has demonstrated impressive performance throughout all those years. Using simple technology, BRI, through its Unit Desa system grew to become a leading commercial microfinance provider. Since the beginning of the commercial era of BRI in 1984, we have delivered credit in the amount of almost Rp. 80.5 trillion [US$ 9.5 billion]. Now, loans outstanding as of June 2003 are Rp. 13 trillion [US$ 1.6 billion] with more than three million customers spread out all over Indonesia, from the urban to rural areas, even in very remote areas where other banks would think ten times before operating in that area. BRI has 3,931 BRI Unit offices to serve micro business customers. Not only in loans do BRI Units show successful performance. In savings, its performance is even more astonishing. When BRI mobilized savings in rural areas, many people were skeptical. However, BRI Units’ success has turned around the old paradigm that low-income people cannot save and will not save. Now our savings amount exceeds our loans outstanding. More than 29 million savers deposit their money in BRI, with a total amount of Rp. 24.6 trillion [US$ 2.9 billion] in our microbanking network. Our success does not mean that our job has finished. New challenges always come up in the development of the bank. After more than two decades in operation, we do not want to just sit down and enjoy our success. Even now we have to work harder if we want to maintain our success as the business environment and customers’ preferences have changed. We must address the challenge of how to increase the economic welfare of the people and how to

MicroFinance Network

6

empower micro, small and medium entrepreneurs. BRI must work to strengthen its capital base and continue to find ways to manage the many risks the bank faces including credit, market and legal risks. It must also continue to build a foundation of good corporate governance, recapitalizing lending operations day by day. Last September, the Indonesian government recognized BRI as the best state-owned enterprise in finance because of its successful outreach. Countries around the world are sharing the common millennium targets for 2025 to slash poverty up to half. It is possible. Therefore, I am very grateful for being the host of MicroFinance Network annual conference. I believe that during the three-day conference, your deliberation and your wealth of experiences shared in this conference will widen our perspective in providing the best services to low-income people and hopefully increase their wealth as well, which eventually will have a positive impact on society. Finally, I hope this meeting can develop and explore many kinds of cooperation and partnership among members based on mutual benefits. I wish you good luck to this meeting and enjoy your stay in this paradise island of Bali.” Mr. Rudjito President Director Bank Rakyat Indonesia MFN Conference Host

Microfinance Clients, Products/Services and Market Niches

7

THEME I: WHO ARE WE REACHING? HOW DO WE KNOW WHO OUR

CLIENTS ARE? “The provision of microfinance services is evolving from focusing only on microentrepreneurs to reaching the working poor. This evolving definition includes poor salaried workers and others with need for capital (for education, home improvement, insurance, etc.) As regulated microfinance institutions expand their operations toward a full service approach, their loan products reflect this new definition of the market.” - Maria Otero, ACCION International “Since the beginning of the commercial era of BRI in 1984, we have delivered credit in the amount of almost Rp. 80.5 trillion [US$ 9.5 billion]. Now, loans outstanding as of June 2003 are Rp. 13 trillion [US$ 1.6 billion] with more than three million customers spread out all over Indonesia, from the urban to rural areas.” - Mr. Rudjito, President Director of Bank Rakyat Indonesia

* * * * * The definition of microfinance has expanded both in terms of customer demand and the profiles of microfinance applicants. MFIs recognize that many clients want more than working capital loans and that they come from more diverse populations than those served in the past. More MFIs are serving a broader range of clients who fall somewhere between the extremely poor and higher-income salaried workers who still cannot access financial services from traditional commercial banks. MFIs are now offering consumer loans, housing loans and other new products and services that respond to the needs of not just microentrepreneurs, but also their families and their employees. Microentrepreneurs of all levels are benefiting from these expanded services. Conference participants were asked to think about how they define their respective markets, considering particularly when they would decide to broaden their target market and why. Why are MFIs moving beyond their traditional markets? Has this expansion been driven by increased demand from different market segments or from a supply-side institutional decision? How has this shift been supported or stifled by donors or other interested parties?

MFIs in different countries, operating under varying regulatory structures are frequently moving up market, providing higher loans to higher income clients often to compensate for lower returns

MicroFinance Network

8

on portfolios with smaller loans. At the same time, other MFIs are taking a second look at their mission and are beginning to move down-market to better meet the needs of microentrepreneurs. In the following section, two MFIs offer an analysis of their clients and offer insight into why they target certain sectors of the market.

1. WHO ARE OUR CLIENTS?

1.1 Serving a Range of Clients – Starting with the Poorest Presented by Udaia Kumar, Managing Director, Share Microfin Limited (India) Share (Society for Helping and Awakening Rural Poor through Education) Microfin Limited (SML) provides financial and support services to skilled and unskilled rural poor women entrepreneurs. This enables them to undertake income-generating activities, such as becoming vendors, home-based producers, artisans or traders. SML is a community-owned institution with a paid up share capital of Rs. 8.28 crore (US$ 1.8 million) and has disbursed over Rs. 274.29 crore (US$59.6 million) in loans to about 216,000 women entrepreneurs since its inception. Share started microcredit operations as a Society in 1993 as a two-year action research project with a recoverable grant from the Asia Pacific Development Center in Malaysia and a soft loan from the Grameen Trust in Bangladesh. In 1999, due to legal constraints as a Society, Share Microfin Limited transformed into a Non-Banking Financial Company (NBFC). Share’s prime activity is to reduce poverty by providing poor women continuous access to collateral free credit, creating opportunities for self-employment. The objective in creating the public limited company was to leverage a significant quantity of mainstream commercial funding, to expand the outreach of microfinance in India. Share provides financial and support services to the bottom 50 percent of women living below the poverty line. The loan term is for one year, and loans are disbursed as general loans, seasonal loans, special loans and microenterprise loans. Loan delivery begins with a public orientation meeting that is organized in villages. These meetings are designed to brief women and other villagers on the loan delivery programs. Women form groups of five members based on general criteria. There should not be blood relationship between members, women should be of the same age group, and should come from the same area. Once enrolled in a group, the members are responsible for loan approval, disbursement and repayment. A staggered disbursement ratio at 2:2:1 is maintained in order to build up group peer pressure. The process is as follows:

• Two members of the group receive a loan in the beginning of the first cycle. • Once weekly repayments are established and four weeks have passed, the next two

members can receive their loans. • After another four weeks, the group leader finally receives a loan.

Microfinance Clients, Products/Services and Market Niches

9

The loan period is one year with repayments spread over 50 weeks of equal installments. The field staff and the monitoring department of SHARE closely monitor the loan utilization, repayments and credit discipline of the groups. As of August 31, 2003, Share had worked in 2,755 villages through a network of 99 branches and had disbursed about Rs. 268.37 crore (USD 58.34 million) to 215,254 poor rural women. The institution has reached operational self-sufficiency of 111 percent, with a total loan portfolio of about Rs. 68.44 crore (USD 14.88 million) and a repayment rate of 100 percent. Share has minimized risk through an insurance fund that is used in the case of death of a borrower. Seed capital is provided based upon mutual trust, discipline and peer pressure, rather than collateral or guarantee. Share is quite clear about who they are reaching. They aggressively target the poorest of the poor by handpicking them off the streets and inviting them to join the program. Share believes that their targeting efforts have had an important effect on their high repayment rate. To effectively target clients, loan officers rely on assessments of the clients’ housing and household assets. Through a general home visit and discussions with neighbors, the loan officers are able to determine the level of poverty of potential clients. Then, through the lending program, borrowers are lifted out of poverty gradually during each loan cycle. Recent impact studies of Share indicated that 77 percent of their mature clients, those that have been members for at least three years, have experienced significant reduction in their poverty over the past four years, and half of these are no longer poor. Sixty-four percent of mature clients had been very poor when they began receiving SML microfinance loans three to four years ago, while the remaining 36 percent had been moderately poor. Today, only 7.2 percent remain very poor, while 56.8 percent are moderately poor and 36 percent have moved completely out of a state of poverty. At the end of 2001, The International Food Policy Research Institute (IFPRI) in Washington, D.C., USA, undertook a CGAP-supported study to assess the poverty levels of Share’s clients. The survey results indicated that 85 percent of Share’s clients come from the lowest 20 percent of people living below the poverty line in India. The remaining 15 percent of clients are below the poverty line, but have income levels above the bottom 20 percent. The survey demonstrated that Share’s targeting tool is indeed effective in targeting the poorest of the poor. However, while Share continues to target the very poor, they have also begun reaching out to slightly wealthier borrowers to balance risk and acquire more savings that can in turn be used to support more loans for the poor.

1.2 The Creation of a Multi-Product Bank to Foster Microfinance Presented by Alvaro Retamales, General Manager, Banco del Desarrollo Microempresas S.A. (Chile) Chile has a population of 15.6 million with a GNP per capita of US$4,260. With 20.3 percent of the population below the poverty line, there are approximately 1.1 million microentrepreneurs in the country, while only about 135,000 are currently being served. Banco del Desarrollo (Bandesarrollo) is a private company that focuses on sectors of the population with few

MicroFinance Network

10

opportunities to access the traditional financial system in Chile. Bandesarrollo’s mission is to provide financial services to the full range of the microenterprise sector in Chile, including medium, small and micro entrepreneurs. As of June 30, 2003, Bandesarrollo had 42,191 clients in the microfinance program, with 38,437 microloans outstanding (35,934 loans for microentrepreneurs and 2,503 for solidarity group loans) and an outstanding portfolio of US$26.6 million. Bandesarrollo decided to broaden its services towards new segments when they became aware that only 10 to 15 percent of Chile’s microentrepreneurs are actually being served. The bank also aims to be a development partner which is able to impact the socioeconomic growth of its clients. The bank sees their role as a pioneer provider of financial services in Chile. Because of this, they continuously explore how to serve new segments with new tools. Bandesarrollo’s strategy to broaden services includes several key elements:

1. Periodically reviewing of the impact of existing products and services 2. Revising and improving the risk management system for assessing new products 3. Increasing productivity through the use of new technologies 4. Using an increasingly a more differentiated price structure on loans for different levels of

clients As a private bank looking to broaden services, Bandesarrollo began a steady down-scaling strategy which included a decision to include non-registered microenterprises and microentrepreneurs without collateral. They also lowered the minimum loan size from US$240 to US$120 and re-incorporated the group lending methodology for the most risky segments of the market. Finally, they stimulated savings among these same population segments. Through this down-scaling strategy, the bank has opened more than 15,000 new accounts in just three years. To continue outreach to new sectors of the population, Bandesarrollo has also engaged in a diversification strategy which has led to the launch of some very interesting and innovative loan products, including loans for fishermen working in specific fishing areas, flexible loans for families (offered to clients with good repayment history), forestry loans, and loans to small farmers. The bank also began to focus more on innovation potential through market research studies (quantitative and qualitative), the use of different polling techniques, and utilizing effective listening skills with regards to clients. The process flows from bottom to top - from clients, to loan officers, to management. The bank continuously observes existing markets and services in order to find out how to make existing tools better. In addition, the bank has put together a flexible, multidisciplinary team focused on the design and development of new products and methodologies. This team recognizes the importance of field testing through pilot phases of new products and the importance of making necessary adjustments as they continue to gradually expand throughout the country. Averaging three new product launches per year, Bandesarrollo has succeeded in tripling the total number of clients in three years. This increase has come with high client satisfaction and has had a significant impact on the socio-economic status of its clients (as measured by an independent agency).

Microfinance Clients, Products/Services and Market Niches

11

2. KNOWING OUR CLIENTS THROUGH ASSESSMENT TOOLS

2.1 Poverty Assessment Tools – The ACCION Approach Presented by Elisabeth Rhyne, Senior Vice President, ACCION International (USA) Poverty assessment is used to understand and measure the poverty levels of the clients reached. This is done by developing special indicators that are used to monitor outreach to the poor on a regular basis. These indicators measure an institution’s social performance alongside its financial performance. This information collected about poor clients can be used in many ways, among them in product and service design. The effective use of a poverty assessment can ultimately enhance the ability of an institution to reach down-market. It is important to note that ACCION’s poverty assessment is NOT a targeting tool and should not be considered as an impact study. There are several approaches to poverty assessment currently under way. Each has special methods and objectives that differentiate them from one another. CGAP has been working to develop a targeting tool which serves as an institutional assessment that looks at whether the MFI is making an effort to reach the poor and what tools the MFI itself has in place to measure their success in doing so. Both Freedom from Hunger and FINCA International have developed their own instruments. However, since these institutions use the village banking methodology, they must use proxy indicators for client income. Each of these tools is simple to use, yet effective. As a natural extension of their organizational focus, Freedom from Hunger focuses on the issue of food security. The loan officer asks the client’s family “which one of the following statements best describes the food eaten in your household?”

a) Enough and the kinds of food we want to eat b) Enough but not always what we want to eat c) Sometimes not enough to eat d) Often not enough to eat.

FINCA has developed a “poverty index”, using seven indicators and an overall score. The indicators include 1) food; 2) healthcare; 3) housing quality; 4) children in school; 5) empowerment; 6) social capital; and 7) expenditure. They use a brief questionnaire which takes the loan officer about 30 minutes to administer. A third approach, one being developed by ACCION, flows from the individual lending methodology that is used by most of our affiliate organizations. It draws from two datasets: the national data of the World Bank’s Living Standards Measurement Surveys (LSMS1) and management information systems (MIS) of the MFI. Because detailed information on household and business expenditure is already available in the MIS from the loan analysis process, no additional data collection is needed. The analyst only needs to understand the value of the data and put it into a form that is useful for interpretation and can be used for decision-making.

1 LSMS is a large-scale household survey project that pulls together information from a number of country organizations and is coordinated by the World Bank.

MicroFinance Network

12

ACCION Poverty Assessment Methodology Using the example of Mibanco in Peru, data from their MIS was compared with data from national household expenditure surveys, as well as national and international poverty lines. First, the MIS data was downloaded from the system. The relevant data on income and expenses of the household unit was originally collected during the client application process and credit analysis. Next this data was compared to the World Bank’s Living Standard Measurement Study (LSMS) data. The ACCION poverty assessment of Mibanco used LSMS data from the 1994 survey which provides a sample of 3,623 households. From this national sample, ACCION selected 830 households in the Lima metropolitan area in order to compare with Mibanco’s clients located in Lima. The ACCION methodology assesses absolute poverty levels by comparing income and expenditure to a number of fixed poverty lines, including the national Peruvian poverty line, the Lima metropolitan line, and the US$1/day and US$2/day international poverty lines. Finally, the two data sets are compared, with certain adjustments to make the data comparable. The results of the ACCION study show that the poverty rate of Mibanco clients is higher than the Lima sample population, in terms of both national and Lima poverty lines. Forty-nine percent of Mibanco’s clients are living in poverty, while 40 percent of the Lima population falls into the same category. Twenty-seven percent of Mibanco’s clients are below the national poverty line, while twenty-two percent of the Lima sample population had incomes below the national poverty line. These results and other comparisons suggest that Mibanco is serving Lima’s poor and near-poor majority.

Figure 1: Household Annual Income Per Capita, Mibanco vs. Peru 2000-2001

Lessons about Measuring Poverty

0%

20%

40%

60%

80%

100%

- 1,000 2,000 3,000 4,000 5,000 6,000

Income (nuevos soles)

% o

f pop

ulat

ion

Mibanco National PopulationLima National Poverty LineLima Poverty Line $1/day$2/day

Microfinance Clients, Products/Services and Market Niches

13

When trying to assess poverty levels, it is important to keep in mind that poverty lines are arbitrary and subject to great error and manipulation. From ACCION’s experience, it is better to compare population distributions than to focus on a distinct poor/non-poor cut-off. For example: Haiti’s national poverty line is below the international US$2/day line, while Peru’s national poverty line is well above the US$2/day line. However, all purport to measure the same thing: the ability to buy basic food necessities plus a minimum of non-food items. What is a Social Scorecard? A social scorecard is a set of indicators that captures the social mission of an organization. It is analogous in nature and uses to key financial, demographic and enterprise-focused indicators. An effective social scorecard should be able to effectively capture the organization’s social mission, should be easily measured and used in regular monitoring. Finally, it should be actionable: the results of the data can influence management decisions. While there are various strategies for creating social scorecards, standard indicators of outreach include the number and/or growth of clients: this is an essential part of any scorecard. Standard indicators also include the percentage of women: this is optional depending on an institution’s mission. The average loan size is often used, but this is a very poor, misleading indicator because of the range of loans that many MFIs offer. Impact studies touch on many of these issues, but they are often complicated and expensive. They are also open to methodological challenge and not actionable by management. Finally, they are difficult to use as a means for ongoing monitoring. ACCION’s proposed approach uses the client profile to track the poverty distribution of clients. The loan size distribution is used in place of the often used indicator of average loan size.

Figure 2: Proposed Social Scorecard for Mibanco (Summary)

Clients Income/Capita Loan Size2 Portfolio3 New Clients4

Income as Percent of

Poverty Line1 % USD USD % No.

A: 0-50% 7 1,500 844 2.3

B: 50-75% 21 2,263 1,230 10.2

C: 75-100% 21 3,140 1,705 14.1

D: 100-120% 13 3,955 2,136 11.1

E: >120% 38 7,489 4,131 62.4

Total/Mean 100 4,610 2,529 100

Notes: 1. Macroeconomic indicators needed to calculate poverty lines, 2. Mean initial loan size 3. Distribution of the portfolio by loan size, 4. Column shown here as an example of number of clients who received their first loan from Mibanco during given period (Actual numbers not included in this table) It is recommended that the full report include the following: number of clients, household income, average initial loan size, average outstanding loan balance, the value of the

MicroFinance Network

14

portfolio, total assets, and the number of new clients. In addition, we recommend that the report include a break-down of the value of the portfolio, number of clients, and clients’ income by specific loan size categories. MFIs can use the scorecard in a number of ways. The board and management can agree on preferred indicators to reflect the organization’s goals (in a tailored, non-standardized manner). Specific goals for these indicators can be set during business planning and can be monitored regularly (quarterly, annually, biannually). The results could be published in annual reports or places such as the MIX (www.mixmarket.org). Social scorecards would differ for each organization. That is, different MFIs would focus on different goals such as job creation, reaching women, etc. A social scorecard could be more relevant than an impact study as an information tool for management because management cannot make decisions on the basis of impact alone. It would probably be advisable for management to review the scorecard on a quarterly basis – less frequently than they would review financial performance data. Key Issues and Discussion on Poverty Assessment Tools and their Use With better social indicators, we would do a better job of measuring performance to meet specific goals. Some practitioners in the industry believe that it should become standard practice for microfinance institutions to develop a social scorecard to accompany indicators of financial performance. However, a broader question is whether or not microfinance institutions could produce appropriate scorecard information? How can management use the information in a scorecard? A scorecard is like a photo of an organization at one period in time. As such, it can show trends in an MFI’s ability to reach their target population over time if it is used regularly. One drawback, however, is that it is not possible to see changes as particular clients move from one poverty level to another. So the scorecard is unclear on whether clients are “moving up” or whether new products are bringing in new clients from different income categories. It is important to tie data directly to clients so that it is possible to cross-reference the scorecard results to individual data files for specific clients. One important issue to consider is the fact that for MFIs with many clients or limited resources, targeting and measuring can be very expensive. An MFI’s competition may have an advantage simply because they are not targeting. However, with ACCION’s approach, the cost of collecting the data is negligible because it uses information that already exists in the MIS. Nonetheless, an MFI must pay to have the report built into their MIS and must pay for validation to make sure the data is accurate – this can be expensive. The goal of the scorecard is to find a way to take advantage of the data that loan officers are already collecting and to find a low-cost way to gauge actual client composition on a regular basis. For MFIs without this kind of information, a proxy-based system is often more appropriate. That would mean that some additional questions would be included during loan analysis. Because of biases inherent to the loan application process, it is not advised to completely rely on information provided by the clients. It is important to learn to interpret the information given. Loan officers learn the skill of probing and use a system of cross checks to verify that information is correct. In terms of poverty data, the key is to understand systematic biases and to adjust the

Microfinance Clients, Products/Services and Market Niches

15

data used in the analysis accordingly. Data is credible as long as the researcher is up-front and transparent about its biases. Another concern from an MFI’s point of view is that a government or donor agency may decide to take action on an MFI because a segment of the MFI’s clientele is not “poor” in terms of the official poverty line. This could put an MFI in a difficult position. However, for MFIs with a specific mission, the scorecard is designed to push the boundary of defining a social mission. Other MFIs believe that it is not useful to measure the poverty levels of clients if the organization has grown steadily over time. It is easy to demonstrate the effect of new services on clients by seeing how the services are valued. However, perhaps in rural areas, it is easier to prove that an MFI is serving the poor. The scorecard could still provide valuable quantitative market data which can help an MFI better understand their clients. ACCION’s poverty assessment work is not about measuring impact, but about understanding to whom an MFI is lending. With the example of Mibanco, the data shows that a commercial bank (Mibanco) has a clientele that is 50% under the poverty line. This helps answer the big question being raised right now about whether there is a relationship between microfinance and poverty. This tool helps management gauge whether there is mission drift. Another consideration is how credible the data or assessment results will be if conducted by the MFI itself and not an independent entity. If there is any question of bias, policymakers will not see the data as credible. One conference participant believes that the question should go beyond just knowing who your clients are, but knowing if the services provided have helped to move people our of poverty.

MicroFinance Network

16

Microfinance Clients, Products/Services and Market Niches

17

THEME II: WHAT KINDS OF SERVICES & PRODUCTS ARE WE DELIVERING?

* * * * *

Having discussed some of the types of clients that MFIs have reached, we now look at how MFIs are actually reaching them. The types of products and services that MFIs offer are often determined by location, institutional structure and certainly by management. Conference participants looked at some specific products being offered by MFIs, including housing loans, simple savings and loan products and discussed when an MFI might want to consider specializing in fewer products or look to diversify with many loan products.

1. SPECIALIZATION OR DIVERSIFICATION MFIs following a strategy of specialization focus their staff and resources on a few products and services, developing an expertise in a particular market for microfinance. A strategy of diversification is one where an MFI offers many products and services, sometimes referred to as “one-stop shopping.” The question of whether to move beyond one product and one market is a difficult choice for an institution whose entire structure and even mission is based on a one-product model. Moving beyond one product or changing a core methodology can expose an MFI to uncertain risk. However, it can also help to assure long-term sustainability in competitive markets and is the primary way for an MFI to grow. This section will look at this question from the perspective of several MFIs – those that currently specialize in one primary loan product and those that offer multiple products either to the same target market or to a range of clients. How do MFIs define what they offer to clients? An informal survey of MFN members conducted by the Microfinance Information eXchange (MIX) for internal use by the MicroFinance Network shows that most MFI’s have a range of two to five products. The survey found that MFIs were using different criteria to differentiate products: for example, seven MFIs used the loan term, one MFI used “currency, three “loan amount” and four “type of client receiving loan” (such as micro medium or small entrepreneurs). This highlights the importance of looking at the criteria used by MFIs before comparing the breadth of product offering. Let’s assume for example that 2 MFIs offer 2 types of loans with similar characteristics, except for the fact that one in US dollars and the other in local currency. The MFI that uses “currency” to differentiate its products will indicate that it has 2 loan products, while the other will indicate that it has only one product. Other criteria used to differentiate loan products includes loan payment frequency, guarantees required, the minimum and maximum amounts of the loans, lending methodology, and the

MicroFinance Network

18

ultimate use of the loan by the client. Some common criteria used to define savings products included the type of account (voluntary vs. mandatory), the initial deposit amount, minimum balance and the interest rate charged. Other financial products mentioned by MFIs include cash management (payroll, supplier payments, payment of utility bills), transfers and insurance. Also, even among the common criteria, actual definitions can vary widely.

Figure 3: Diversification/ Specialization as Stated by the MFI

Number of MFIs w ith X Loan Products

0

1

2

3

1 2 3 4 5 6 7 8

Number of Loan Produc ts

Num

ber

of M

FIs

Number of MFIs w ith X Savings Products

0

1

2

3

4

0 1 2 3

Number of Sav ings Products

Num

ber

of M

FIs

Microfinance Clients, Products/Services and Market Niches

19

Number of MFIs w ith X Other Financial Products

0

1

2

3

4

5

6

0 1 2 >3

Number of Other Financial Products

Num

ber

of M

FIs

Of the MFN members surveyed:

1. Loan terms ranged from three to 416 months 2. Microfinance loan amounts ranged from US$200 to US$100,000 (housing loans) 3. Criteria used to segment were different: by income, by number of employees, etc.

1.1 PRIDE Tanzania – A Single-Product Example Presented by James Obama, General Manager, PRIDE Tanzania (Tanzania) The Promotion of Rural Initiatives and Development Enterprises (PRIDE) Tanzania started as a government project funded by the Norwegian Agency for Development (NORAD) through a bilateral agreement between the Government of Norway and the Government of Tanzania and was incorporated in 1993 as a company limited by guarantee without share capital. PRIDE Tanzania started operations in 1994. PRIDE’s mission is “to create a sustainable financial and information services network for small and micro entrepreneurs in order to stimulate business growth, enhance income and generate employment in Tanzania.” Tanzania has a population of 34.2 million, covers an area of 945,000 square kilometers, and has a GDP per capita of US$ 2,180. Commercial lending rates average between 11 and 20 percent and the inflation rate is around 4.5 percent. Approximately 18 percent of the country lives below the poverty line.

MicroFinance Network

20

Figure 4: Conventional Business Dynamics – the Big Picture

Supply Driven Demand Driven

Production concept Product concept Selling concept

Marketing & Societal concepts

Assumptions: • Unlimited demand for

products and services, • Less or no competition, • Homogeneous market Limitations: • Does not take into

account market needs, changes

Emergence of stiff Competition: • Focus on

improved quality of products and services through R & D function

Challenges: • Product did not

sell as expected

• Application of aggressive selling strategy to push products and services out

Challenges: • Hard selling

became a nuisance, did not meet expectations of the market

Assumptions: • Market is heterogeneous • Concern for social

responsibility - Focus on market

needs and retention of customers through use of market research

- Responsiveness to social concerns

Advantages: • Promotes a win-win

situation Dynamics of Tanzania’s Microfinance Industry The level of economic, socio-cultural, political development in Tanzania as well as the technological environment is reflected in the nature and character of Tanzania’s microfinance industry. Until the late 1990s, microfinance was viewed as a social intervention in the poverty eradication initiatives. The industry, which is about 30 years old, has undergone drastic changes in terms of character and focus over the last decade and microfinance is now widely regarded as a business in its own right. The current drive advocates the application of commercial principles in microfinance while at the same time MFIs are seeking to maintain their social mission. MFIs have to adjust to changes in clients’ needs or they risk losing business or failing to be sustainable. The issue is therefore not a question of whether an MFI wants to specialize or diversify in order to survive, but rather if an MFI has the ability to respond to changes in market tastes. PRIDE’s sole product, the solidarity group loan (SGL), was launched in 1994. The microfinance industry in Tanzania at the time was not very developed, with very little competition, while the market was starved for credit, with huge demand relative to supply. The basic concern for MFIs was reaching out to the poor, yet prospective/target clients were considered to be risky. The market was considered to be more or less homogeneous. PRIDE’s particular product design was borrowed from the successful Grameen model and modified to suit what was considered to be the market needs at the time (supply driven). From the beginning, PRIDE Tanzania established a system of obtaining regular feedback from its clients in order to capture client views and concerns on an ongoing basis. The approach focused mainly on the performance of existing product rather than looking to the development of new

Microfinance Clients, Products/Services and Market Niches

21

products. Modifications of the product were carried out in 1997, 1998, 2000 and 2002 as attempts to address clients’ concerns were expanded. However, it was difficult to address all client concerns because the MIS could not support delivery of multiple products. The staff and structure of PRIDE were familiar with the SGL product and it would take a great deal of time to adjust. In 2002, the organization made the decision to innovate as a result of increased competition. Adjustments to loan products have helped the institution grow, a welcome change from the nearly flat growth from the previous year.

Figure 5: Advantages and Disadvantages of Single Product

Advantage of Single Product Disadvantage of Single Product • Good starting point • Limited to reaching a narrow market • Likely to prolong the product life cycle • Over-extended product life cycle inhibits

innovation • Allows for standardization • Product may not fare well in a competitive

environment • Works well in a relatively homogenous, less

competitive market • Product is less responsive to changes in

market taste • Allows for a market segment focus • Requires rigorous sales drive • Can lead to fast growth of outreach • Susceptible to limited yield potential • Tendency for staff to become stereotyped As Figure 5 indicates, there are certain advantages of an institution focusing on one primary product. The institution will be better able to prolong product life cycle where there is a strong Research & Development function. A single product works very well in a relatively homogenous market where the environment is less competitive. This approach allows for standardization in a number of areas such as the service delivery mechanism. This makes it easier to handle the product across the branch network. Staff training becomes less costly because of the more focused level of expertise. Specialization also reduces the cost and complexity of incentive programs by allowing the MFI to establish a uniform system of staff appraisals and rewards. Specialization also allows an MFI to focus on a specific market segment. This can help lead to fast outreach and growth. For example, PRIDE Tanzania has been able to expand to 64,000 clients with a loan portfolio of USD 8.5 million and 26 branches throughout the country, 22 of which were established between 1994 and 1998. At the same time, there are disadvantages of specialization. Focusing on a few specific products, an MFI will likely be limited to reaching out to a narrow market. An over-extended product life cycle inhibits innovation and can often lead to serious portfolio risks if not closely monitored. The product may not fare well in a competitive environment, especially if the product is less responsive to changes in the market taste. Focus on a single product requires a rigorous sales drive and the institution is susceptible to limited yield potential. The institution takes on greater risk if there the product is negatively impacted for some reason. Finally, there is a tendency for staff to become stereotyped.

MicroFinance Network

22

1.2 Uganda Microfinance Union (UMU) Presented by Charles Nalyaali, Managing Director, Uganda Microfinance Union (Uganda) The Uganda Microfinance Union (UMU) is a strong, dynamic leader that provides quality financial services to entrepreneurs and low-income people throughout Uganda. UMU works to partner with its clients to move them into the economic mainstream by providing quality financial services tailored to meet their needs. UMU’s knowledge and experience in microfinance drives it to approach each client with honesty, respect and sensitivity. UMU has a “full service approach” which has allowed it to grow quickly. They encourage clients to set goals and determine how they want to take advantage of services. UMU is a locally managed, non-governmental organization that incorporated and became operational in August of 1997. With the help of Victoria White of ACCION International and others, UMU is in advanced stages of transforming in to a for-profit, licensed financial institution regulated by the Bank of Uganda (the central bank of Uganda). The new company will be considered a micro-deposit taking institution and will have a set of shareholders. UMU’s mission is “to offer quality financial services to microentrepreneurs and low-income people (female or male) living in the rural, peri-urban, and urban areas in the Republic of Uganda. The financial services offered include the provision of a safe and secure place to keep savings and the extension of credit for working and investment capital at reasonable, fair and transparent interest rates.” UMU offers a wide array of quality financial products to meet the needs and diversity of its client base including the extension of agriculture and agricultural-related loans. UMU understands that there is often a fundamental difference between an individual engaged in agriculture and a person running a retail shop. Both individuals may be considered poor, but this does not directly translate into the two entrepreneurs having identical financial needs, thus UMU’s impetus to develop a variety of financial products. To deliver its services, UMU uses a hybrid methodology referred to as the “UMU WAY”, which is based on the following core principles: • Quality - Microfinance should be delivered in a manner that you and I would expect from our

own financial institution. • Innovation - Microentrepreneurs are a constantly changing and evolving group. Therefore,

UMU believes that it must design new products in order to meet the needs of this dynamic group.

• Flexibility - No entrepreneur is the same, the delivery methodology needs to be able to mold to the needs of each individual within certain parameters.

As a diversified microfinance provider, UMU offers a variety of loans and financial services to its clients. UMU currently offers five primary loan products: working capital loans, capital asset loans, employment guaranteed loans, micro corporate loans and healthcare provider’s credit. Under working capital loans, clients form self-selected groups ranging from five to ten individuals of whom at least 50 percent must be female. The groups are required to attend a one to two hour lecture on the UMU’s rules and procedures. The capital asset loan product was developed from

Microfinance Clients, Products/Services and Market Niches

23

a needs assessment study on borrowers who indicated that they wanted to borrow larger sums of money over a longer period of time to buy fixed assets. Loans are extended only to clients who have completed at least five working capital loan cycles without any arrears. The employer guaranteed loan product targets individuals who are in formal employment. This is a salary-based loan that targets the “working poor.” The micro corporate loan product is the newest UMU innovation. This loan product extends individual loans based on a financial and personal assessment made by the UMU field staff. This product targets the small and medium microenterprises who do not qualify for loans from the formal financial sectors. Finally, for the healthcare providers’ credit, UMU identified healthcare workers as a particular niche market, which has been marginalized by the formal financial sector. This product is designed to cater for working and investment capital needs of all healthcare providers.

Figure 6: Loan Portfolio by Product as of July 2003 (US$)

Product Portfolio (‘000’s)

% of Portfolio Borrowers

Working Capital 1,500 29.5% 19,291 Capital Asset 211 4.1% 432 Employer Guarantee 750 14.7% 1,005 Rural Employer Guarantee 800 15.7% 3,205 Micro Corporate 1,600 31.5% 1,607 Healthcare Provider’s Credit 220 4.3% 367 Back to School Fee Loan 6 0.1% 112

TOTAL 5,087 100% 26,118 MU firmly believes in offering its clients comprehensive financial services, and believes savings products are a critical component of these services. UMU members are able to access two types of savings services – restricted and fixed deposit savings – from UMU at present. Members may deposit their savings into a restricted savings account, which has unlimited withdrawals and deposits. When a member is borrowing from the UMU, access to the minimum balance or collaterized savings is restricted during the life of a loan. A monthly fee is charged for the service while interest is credited to the account at the end of every month. UMU currently also offers clients a fixed deposit savings product as well, though this product has not been aggressively marketed throughout the branch network. This product is a high interest, long-term investment.

Figure 7: Savings Portfolio by Product as of July 2003 (US$)

Product Value

(‘000’s) Percentage Restricted Savings 1,750 98.4% Fixed Deposit Savings 26.5 1.5% Total 1,776.5 100.0%

Other services offered by UMU include local money transfers which allow clients the option of transferring funds from one UMU location to another without the risk of carrying physical cash. UMU recently signed a sub-agency license with Nile Bank the agent for Western Union in Uganda to offer money transfer services worldwide. UMU offers its clients loan insurance services through a reputable insurance company. In the event of an accident or sudden death of

MicroFinance Network

24

a client, the estate of the deceased receives US$600 from the insurance company and pays off the outstanding balance of the client’s UMU loan. Two new products in the pipeline include a back-to-school loan and a home improvement loan. The back-to-school loan is tailored to parents with children attending school. UMU is currently assessing the feasibility of offering a loan for home improvement or construction. UMU has clearly defined itself in the Ugandan microfinance market from the beginning by its wide range of products. This was part of UMU’s early strategic plan and continues to play a significant role in the future plans of the institution.

1.3 An MFI caught in the middle – what approach to take? Carlos Labarthe, Executive Director, Compartamos (Mexico) Both models of specialization and diversification work; the question is which is right for you? Compartamos, an institution with over 215,000 active clients, located primarily in rural areas, has four basic products, all of which can be “specialized” to the entrepreneur. The advantage to this approach is the possibility for high growth. From the beginning, Compartamos has kept its focus on “keeping it simple”. However, at the same time, Compartamos is faced with the difficulty of being too supply-oriented. It seems that client needs are changing faster than products were being offered. This weakness arises from a rigidity and an “over-focus” on a specific approach to doing business (i.e. keeping it simple) and can leave the institution vulnerable to competition. In the experience of Compartamos, competition seems to be the key driver for diversification. “If we look at a business model, General Electric is a company that has pursued diversification and Ford is a company that has specialized. Both companies have experienced great successes and great failures, so the answer to the question is not entirely clear. To know if or when to diversify or specialize, each organization must understand its own context and remember what business they are in,” commented Mr. Labarthe. Group Discussion For an institution using a traditional lending methodology such as village banking, a move to diversification can carry a certain degree of risk, particularly with regards to repayment. In the case of PRIDE Tanzania, this has meant a strategy focused on reconciling the two methodologies that changes the people who deliver the services. “It involves a lot of personnel training. The key need is to prepare staff and make sure they are positive and looking forward to the change,” noted Mr. Obama. MFIs considering the question of specialization or diversification would do well to observe the lessons offered by BRI. They have two products, KUPEDES for loans and SIMPEDES for savings. These products are very flexible and responsive. From these basic loans, BRI has developed different marketing packages for clients and more flexible terms for corporate loans.

Microfinance Clients, Products/Services and Market Niches

25

Share in India began their lending program with many products, but it became too complicated for the accounting system. Share quickly learned that products have to be simple and flexible for the very poor. Today, Share has just two products that are tied to a client’s ability to repay. On the other side of the spectrum, as an institution that has focused on diversification of products, UMU believes that flexible products are good. New products can bring additional interest from clients. However, in some cases, there is a need for standardization and flexibility must be limited (i.e. farming loans and, solidarity group loans). An MFI must understand their market segments in order to design flexible products and avoid needless product multiplicity. Part of the reason that UMU, in particular, has chosen to offer many products, is because of the context of Uganda. UMU wanted to respond to the lack of banks in the rural areas and serious problems with highway robbery of rural clients headed to urban centers to buy inputs. For this reason, UMU has ventured into local money transfers. They designed a product to allow borrowers to deposit money at the rural branch level and receive a check issued to a major city bank, where they can cash the check and get on with their business. In addition, UMU has now become a Western Union agent. They have also designed a loan insurance product tied to sudden death or accidents. UMU believes that if the client wants a product or service, UMU will give it to them. Whether an MFI chooses to focus on further developing existing products or to diversify to new products and services, it is important that each institution understand how a particular strategy can help achieve its longer-term goals. One must consider many factors, including whether the existing methodology, staff commitment and available resources are sufficient for a particular plan. In the presence of strong competition, an MFI must be able to identify its comparative advantage in the market with more products and services or ones that are more focused.

MicroFinance Network

26

Microfinance Clients, Products/Services and Market Niches

27

THEME III: WHAT KINDS OF SERVICES & PRODUCTS ARE WE DELIVERING?

“BRI has a rural mandate and its product offerings reflect this with 30 percent of its loan portfolio present in microloans, 20 percent in corporate loans, 20 percent in medium loans and 10 percent in farming loans.” - Sulaiman Arief Arianto, Denpasar Regional Manager, Bank Rakyat Indonesia

* * * * *

Members of the MicroFinance Network working in developing countries around the world have been leaders in expanding financial services to the poor in both urban and rural areas. MFN member institutions have been able to demonstrate that rural outreach is possible because they offer demand-driven products on a sustainable basis and have access to resources that enable them to take on the risk involved in working in rural markets. MFN member Bank Rakyat Indonesia’s Microbusiness Division (BRI Unit Desa) has been particularly successful in penetrating rural markets. Since 1984, the BRI Unit Desa system has provided financial services to the rural poor throughout Indonesia. Their experience provides many useful lessons for other MFIs looking to expand or initiate rural outreach. In urban areas housing is one of the most important issues affecting the lives of the poor and their families. Despite the growth of microfinance, services are often limited to income-generating activities. Mibanco, an MFN member and regulated commercial bank is Latin America's second largest microfinance institution with over 70,000 active clients. Mibanco began offering Micasa (“My home”), a home improvement loan program, in 2000. Since then, the demand for the housing product has steadily grown. Mibanco anticipates that these loans will grow to 50 percent of its overall portfolio within the next five years. The following cases from BRI and Mibanco provide good examples of MFIs whose specific products and services have allowed them to serve their target markets and have placed them ahead of their competition in terms of both scale and outreach.

1. THE EXPERIENCE OF BANK RAKYAT INDONESIA (BRI) – SIMPLE PRODUCTS, BIG IMPACT Presented by Sulaiman Arief Arianto, Regional Manager – BRI Denpasar, Bank Rakyat Indonesia (Indonesia)

MicroFinance Network

28

Bank Rakyat Indonesia sees microfinance both as a tool for poverty alleviation and as a commercial business, as indicated in Figure 8 below. This perspective has emerged since the institution’s inception as a state-owned bank, functioning as an agent of development. From 1969 to 1983, BRI used a non-commercial approach to microenterprise development through the Unit Desa system, a subsidized loan program for farmers. However, during this time, the bank suffered significant repayment problems. After 1984, the system was reengineered into BRI units, where the unit was made up of four to eight people. Once an office had a staff of more than eight, it was split into two branches. Another important change after 1984 was that the units were relocated to village markets in order to be closer to clients. Units assumed full authority over loans, as long as they could cover their costs.

Figure 8: Financial Services in BRI’s Poverty Alleviation Toolbox

An important part of this shift in structure within the bank was the switch to a commercial approach. The success of the BRI Unit demonstrated the potential for massive outreach to the bank. However, the beginning of the economic and monetary crisis in 1997 prompted a great decline in banking in Indonesia. Despite the widespread crisis, BRI Unit Desas not only survived, but remained profitable throughout. Following the crisis, the government (as a shareholder of BRI) made an important choice to restructure and recapitalize BRI to provide the support necessary to build up management, information technology systems, and audit and risk management systems. All these efforts paid off, and in 2002, BRI was named the best state-owned bank in Indonesia.

Subsidized Poverty Alleviation Programs

Commercial Financial ServicesIncome Level

Extremely poor and displaced households

Economically active poor

Lower middle income

Off icial P over t y L ine

Standard commercial bank loans; full range of

savings services Commercial

microloans

Interest-bearing savings

accounts for small savers

Poverty programs for such purposes as food and water,

medicine and nutrition,

employment generation, skills

training, and relocation

BRI-Unit Grameen Bank

Microfinance Clients, Products/Services and Market Niches

29

BRI’s road to success as a commercial microfinance provider was marked by several key points in its transformation. 1983 - 1984

1. BRI Unit became an autonomous entity within BRI Beginning of 1986

2. Reallocation of some BRI Unit offices to local market centers Gradually from the late 1980’s

3. More loan approval authority and loan repayment responsibility given to BRI Unit manager and officers

4. Establishing a good monitoring and supervisory system 5. Developing transfer prices between BRI branches and BRI Units

These milestones have contributed to making the BRI Unit a strong, profitable microfinance provider in Indonesia, as indicated by the financial highlights provided in Figure 9.

Figure 9: BRI’s Financial Highlights and Projection (in billion IDR)

2000 2001 2002 2003

Net interest income 2,822 4,300 5,364 6,509

Net Income 335 1,030 873 1,007

Total Assets 65,187 72,240 80,787 92,640

Capital Adequacy Ratio

14.35% 13.60% 15.70% 15.40%

Deposits 50,519 58,760 66,030 76,619

Loans • SMEs • Micros

27,519 80% 29%

32.000 85% 30%

35,050 85% 30%

39,731 85% 30%

The key factors to the success of the BRI Unit have been the simplicity of products, transparency in operations and services, accessibility to clients, ability to recover costs, and demand-driven products. Furthermore, BRI offers effective incentives to both clients and staff (who receive bonuses tied to repayment rates of over 95 percent). In addition, the success of BRI Units has been the result of BRI’s commitment, consistency and the capacity of management to combine a development finance approach with a business approach that is inherent in the system and products of BRI Units. These products and services include a basic loan product (KUPEDES), a

MicroFinance Network

30