microinsurance the next revolution in financial services for the poor dr. jaime aristotle b. alip...

TRANSCRIPT

Microinsurance

Dr. Jaime Aristotle B. AlipDr. Jaime Aristotle B. AlipAIRDC/AISADC ForumAIRDC/AISADC ForumSeptember 7, 2012 September 7, 2012

Poverty and Poverty and VulnerabilityVulnerability

4.7 M families live under poverty threshold and 1 out of 3 Filipinos is considered poor (NSCB, 2006)

44% of the population live on less than US$2 a day and 14% on US$1 a day or less (WB, 2007)

The poor is vulnerable to risks, i.e, life cycle needs and unpredictable risks such as illness, death, theft, natural & man-made disasters (Llanto et al., ‘Microinsurance in the Phils: Policy and Regulatory Issues and Challenges,’ 2007)

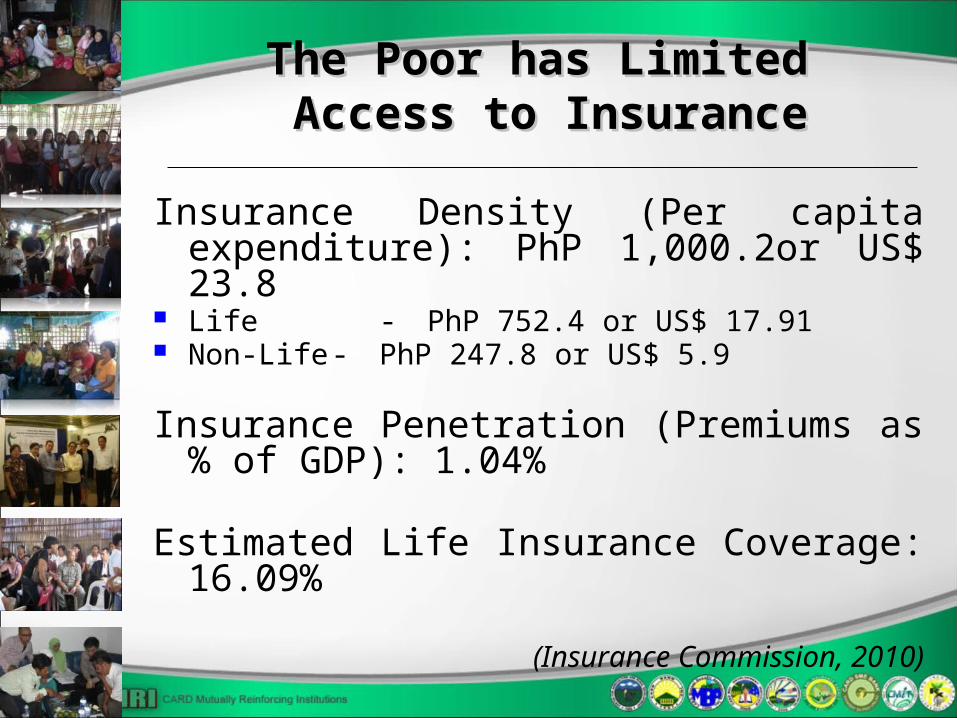

The Poor has Limited The Poor has Limited Access to InsuranceAccess to Insurance

Insurance Density (Per capita expenditure): PhP 1,000.2or US$ 23.8

Life - PhP 752.4 or US$ 17.91 Non-Life - PhP 247.8 or US$ 5.9

Insurance Penetration (Premiums as % of GDP): 1.04%

Estimated Life Insurance Coverage: 16.09%

(Insurance Commission, 2010)

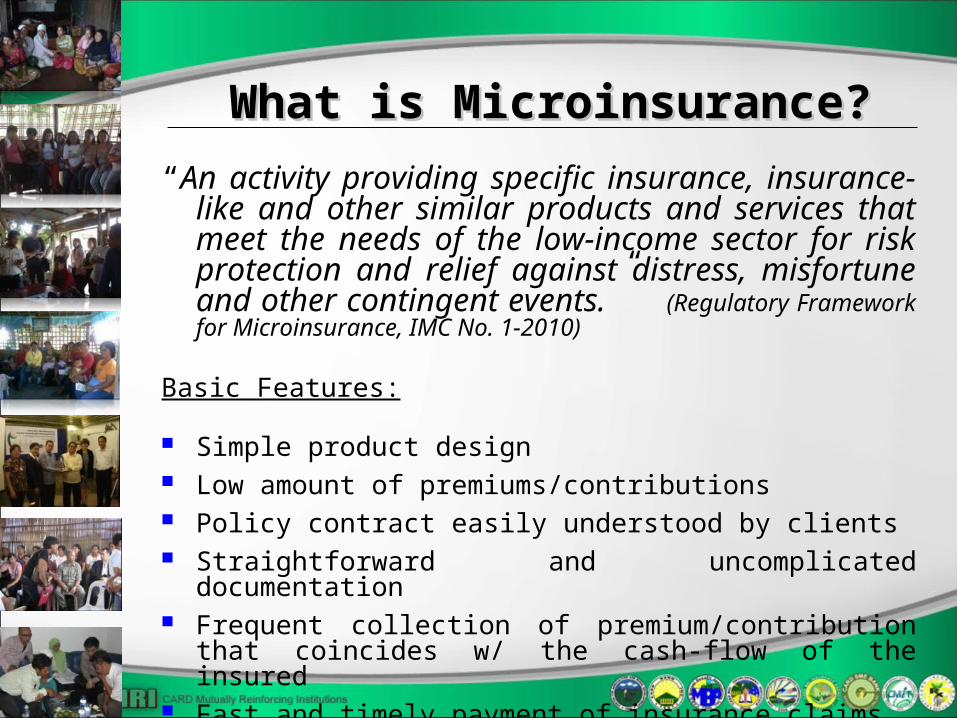

What is Microinsurance?What is Microinsurance?“An activity providing specific insurance,

insurance-like and other similar products and services that meet the needs of the low-income sector for risk protection and relief against distress, misfortune and other contingent events.” (Regulatory Framework for Microinsurance, IMC No. 1-2010)

Basic Features:

Simple product design Low amount of premiums/contributions Policy contract easily understood by clients Straightforward and uncomplicated documentation Frequent collection of premium/contribution that

coincides w/ the cash-flow of the insured Fast and timely payment of insurance claims

“ MICROINSURANCE PRODUCT ” is a financial product or service that meets the risk protection needs of the poor where:

a. the amount of premium computed on a daily basis does not exceed five percent (5%) of the current daily minimum wage rate for non-agricultural workers in Metro Manila.

Php 446.00 x 5% = Php 22.30 per day ($0.53) Php 22.30 x 7 = Php 156.10 per week ($3.72)

b. the maximum amount of life insurance coverage is not more than five hundred (500) times the daily minimum wage rate for non-agricultural workers in Metro Manila.

Php 446.00 x 500 = Php 223,000.00 ($5,309.52)

(The minimum wage for non-agri cultural workers in Metro Manila is Php 446.00 as of June 3, 2012)

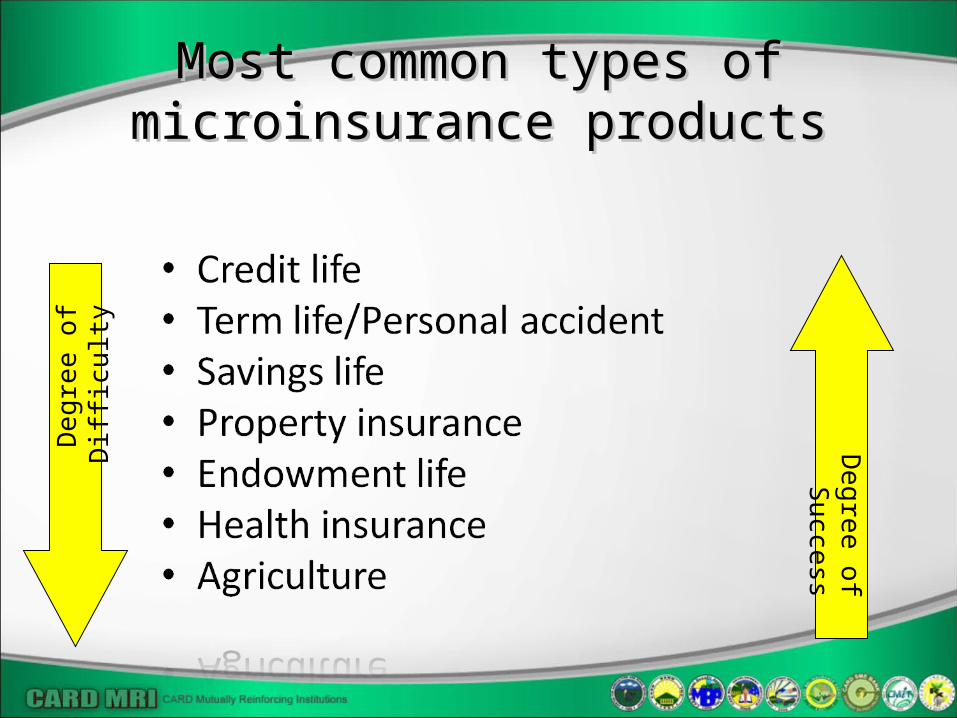

Most common types of microinsurance Most common types of microinsurance productsproducts

Deg

ree

of D

iffi

culty

Degree of S

uccess

To what risks and economic stresses are low-income persons vulnerable?

RIMANSI: Advocating RIMANSI: Advocating Microinsurance thru MBAsMicroinsurance thru MBAs

RIMANSIRIMANSI is a regional is a regional resource center that resource center that aims to help poor aims to help poor households improve households improve their access to their access to affordable yet affordable yet adequate adequate microinsurance, microinsurance, through microinsurance through microinsurance business support business support services services

RIMANSI

RIMANSI Founding Members

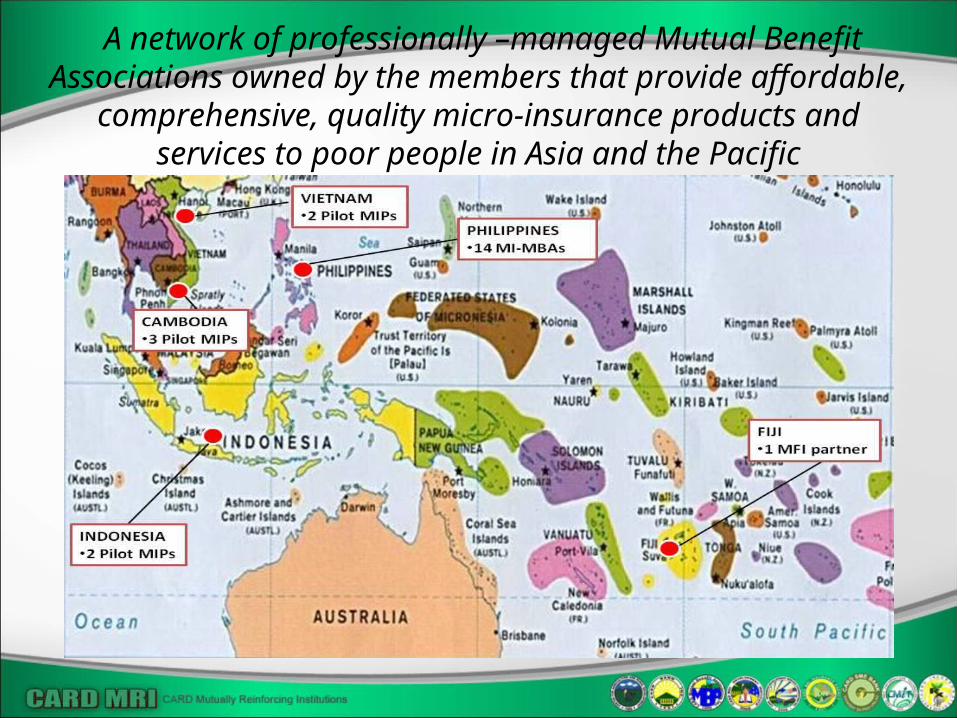

A regional resource centre (non-profit) based in the Philippines to help rural and urban poor households in Asia and the Pacific improve their access to affordable yet adequate micro-insurance services, through micro-insurance business support services.

2005

RIMANSI Business Development Support Services

A network of professionally –managed Mutual Benefit Associations owned by the members that provide affordable, comprehensive, quality micro-insurance products and services to poor people in

Asia and the Pacific

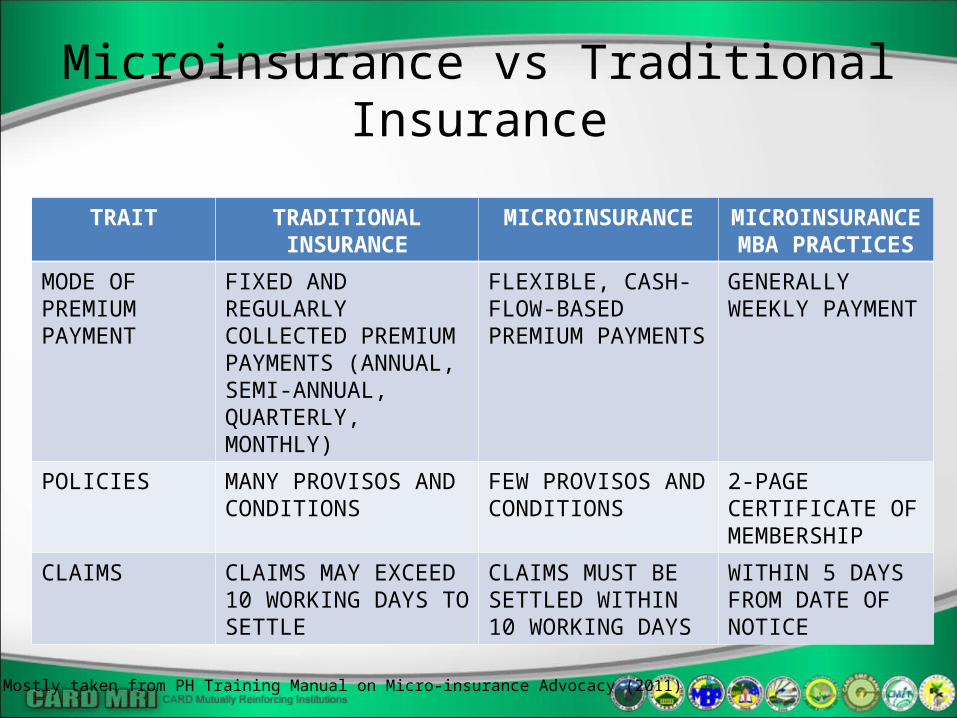

Microinsurance vs Traditional InsuranceTRAIT TRADITIONAL

INSURANCEMICROINSURANCE MICROINSURANCE

MBA PRACTICES

TARGET MARKET MIDDLE-TO-HIGH-INCOME SECTOR

LOW-INCOME AND INFORMAL SECTOR

GENERALLLY CLIENTS OF MFIS

DELIVERY CHANNELS

SOLD THROUGH INDIVIDUAL LICENSED AGENTS OR BROKERS

SOLD THROUGH LICENSED NON-TRADITIONAL AGENTS SUCH AS COOPERATIVES, NGOS, AND RURAL BANKS

MFIS AND OTHER ORGANIZED GROUPS

UNDERWRITING REQUIREMENTS

COMPLEX (MAY INCLUDE MEDICAL EXAMS, ETC.)

SIMPLE, EASY TO UNDERSTAND AND MINIMAL

COMPULSORY MEMBERSHIP

PREMIUM NO LIMITATIONS ON PREMIUM PAYMENT

LESS THAN P1 PER DAY BUT NOT MORE THAN 5% OF THE DAILY MINIMUM WAGE RATE IN METRO MANILA

PHP 12 TO 30 CONTRIBUTION PER WEEK

Source: Mostly taken from PH Training Manual on Micro-insurance Advocacy (2011)

Microinsurance vs Traditional Insurance

TRAIT TRADITIONAL INSURANCE

MICROINSURANCE MICROINSURANCE MBA PRACTICES

MODE OF PREMIUM PAYMENT

FIXED AND REGULARLY COLLECTED PREMIUM PAYMENTS (ANNUAL, SEMI-ANNUAL, QUARTERLY, MONTHLY)

FLEXIBLE, CASH-FLOW-BASED PREMIUM PAYMENTS

GENERALLY WEEKLY PAYMENT

POLICIES MANY PROVISOS AND CONDITIONS

FEW PROVISOS AND CONDITIONS

2-PAGE CERTIFICATE OF MEMBERSHIP

CLAIMS CLAIMS MAY EXCEED 10 WORKING DAYS TO SETTLE

CLAIMS MUST BE SETTLED WITHIN 10 WORKING DAYS

WITHIN 5 DAYS FROM DATE OF NOTICE

Source: Mostly taken from PH Training Manual on Micro-insurance Advocacy (2011)

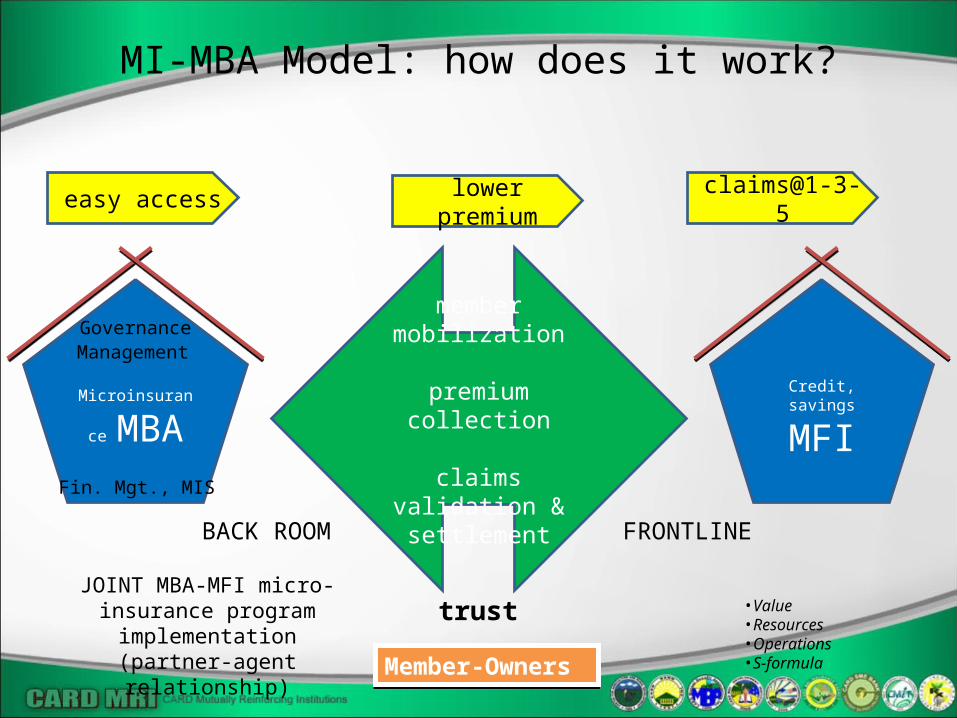

MI-MBA Model: how does it work?

member mobilization

premium collection

claims validation & settlement

Microinsurance

MBACredit, savings

MFI

JOINT MBA-MFI micro-insurance program implementation

(partner-agent relationship)

GovernanceManagement

FRONTLINEBACK ROOM

•Value•Resources•Operations•S-formulaMember-OwnersMember-Owners

trust

easy access lower premium claims@1-3-5

Fin. Mgt., MIS

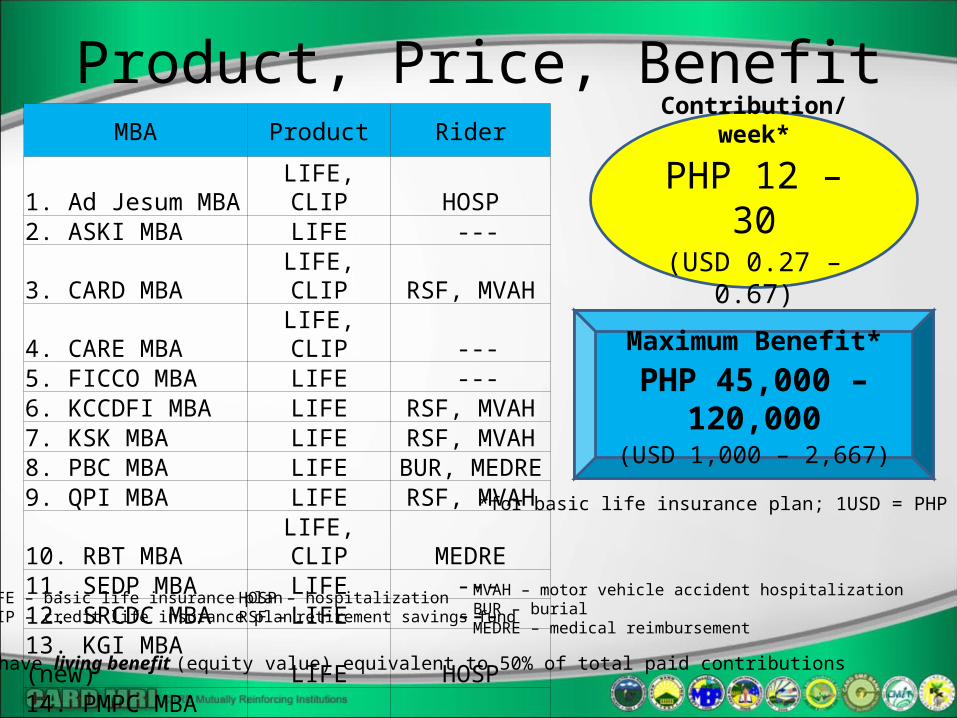

Product, Price, BenefitMBA Product Rider

1. Ad Jesum MBA LIFE, CLIP HOSP2. ASKI MBA LIFE ---3. CARD MBA LIFE, CLIP RSF, MVAH4. CARE MBA LIFE, CLIP ---5. FICCO MBA LIFE ---6. KCCDFI MBA LIFE RSF, MVAH7. KSK MBA LIFE RSF, MVAH8. PBC MBA LIFE BUR, MEDRE9. QPI MBA LIFE RSF, MVAH10. RBT MBA LIFE, CLIP MEDRE11. SEDP MBA LIFE ---12. SRCDC MBA LIFE ---13. KGI MBA (new) LIFE HOSP14. PMPC MBA (new) LIFE RSF

Note: All have living benefit (equity value) equivalent to 50% of total paid contributions

LIFE – basic life insurance planCLIP – credit life insurance plan

HOSP – hospitalizationRSF – retirement savings fund

MVAH – motor vehicle accident hospitalizationBUR – burialMEDRE – medical reimbursement

*for basic life insurance plan; 1USD = PHP 45

Maximum Benefit*

PHP 45,000 – 120,000(USD 1,000 – 2,667)

Contribution/week*

PHP 12 – 30(USD 0.27 – 0.67)

Outreach (2011)

*at least four (4) in a family is covered by the microinsurance certificate

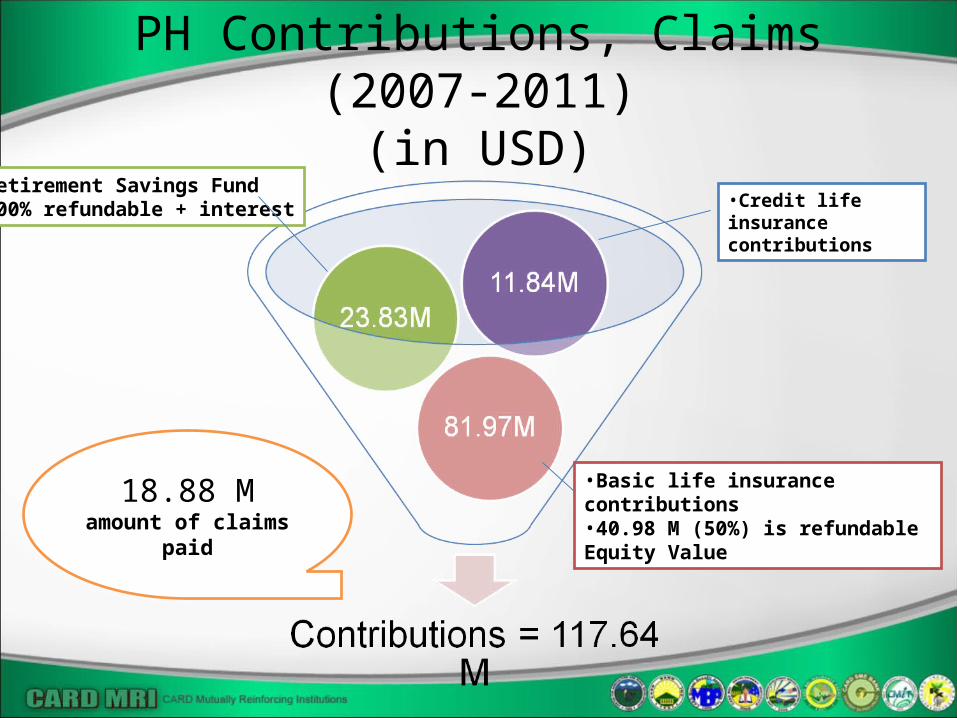

PH Contributions, Claims (2007-2011)(in USD)

•Basic life insurance contributions•40.98 M (50%) is refundable Equity Value

•Retirement Savings Fund•100% refundable + interest •Credit life insurance

contributions

18.88 Mamount of claims paid

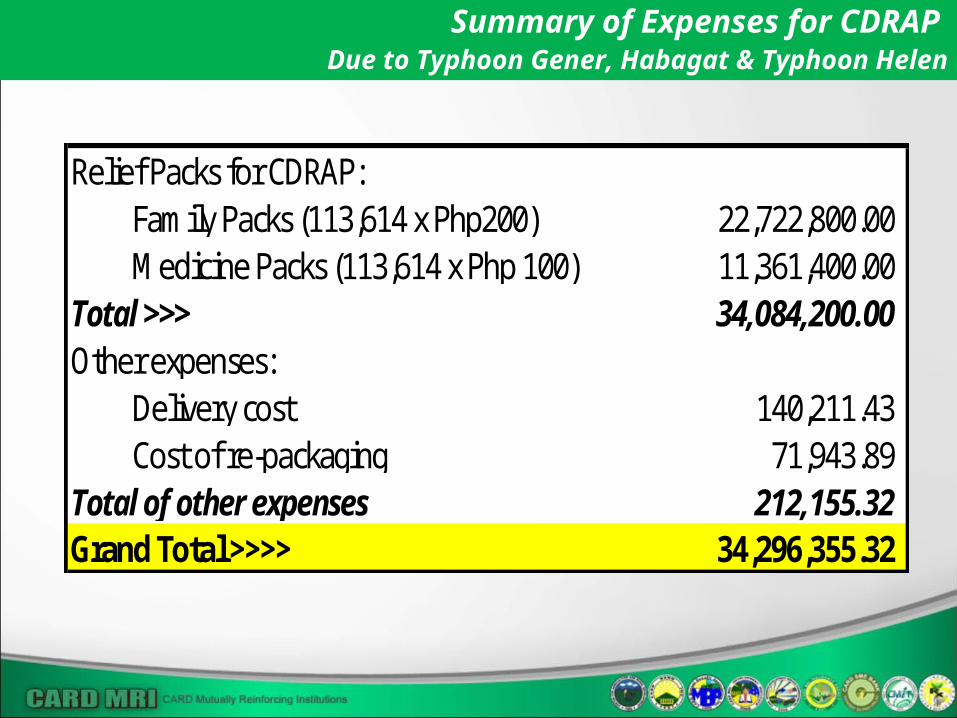

Summary of Expenses for CDRAP Due to Typhoon Gener, Habagat & Typhoon Helen

Relief Packs for CDRAP:Family Packs (113,614 x Php200) 22,722,800.00 Medicine Packs (113,614 x Php 100) 11,361,400.00

Total >>> 34,084,200.00 Other expenses:

Delivery cost 140,211.43 Cost of re-packaging 71,943.89

Total of other expenses 212,155.32 Grand Total >>>> 34,296,355.32

CDRAP UPDATEAs of August 31, 2012

NO. OF AFFECTEDMEMBERS

Typhoon 669 154,394.97 0.53%Flood 125,072 37,130,497.87 98.27%Fire & Lightning 436 272,606.08 0.34%Twister 1 240.50 0.00%Earthquake 1,095 297,899.50 0.86%TOTAL 127,273 37,855,638.92 100.00%

PARTICULARS AMOUNT %

MEMBER

2,499SPOUSE

4,411CHILDREN

1,871PARENTS

308

TOTAL DEATH CLAIMS = 9,035 Average death = 1,291/Mo

or 43/day

As of July 2012

DEATH STATISTICS FOR JAN-JULY 2012

As of June 2012

TOTAL DEATH CLAIMS = 7,424 Average death = 1,237/Mo

or 41/day

Recommendations basis International market practices

Constraints / Challenges Recommendations Insurer Customer Market Reference

a) Large number of informal quasi-insurance schemes run by cooperatives, churches;

b) Policyholder protection

Provision to recognize the informal schemes triggering consolidation activity or partnering informal operators with formal underwriters

Philippines - MBAs are allowed to offer insurance products under a reduced regulatory burden and with lower capital requirements

South Africa - The institutional space for microinsurance is opened up to friendly societies and coop

a) High capital requirement of over discourage established insurers from offering services to low income House Holds

Lower prudential requirement or evaluate the minimum capital requirements for the locally organized small Micro-insurance institutions

Philippines - Guaranty fund for new / existing MBAs has been reduced from Php 125M to Php 5M insurers)

Constraints / Challenges

Recommendations Insurer Customer Market Reference

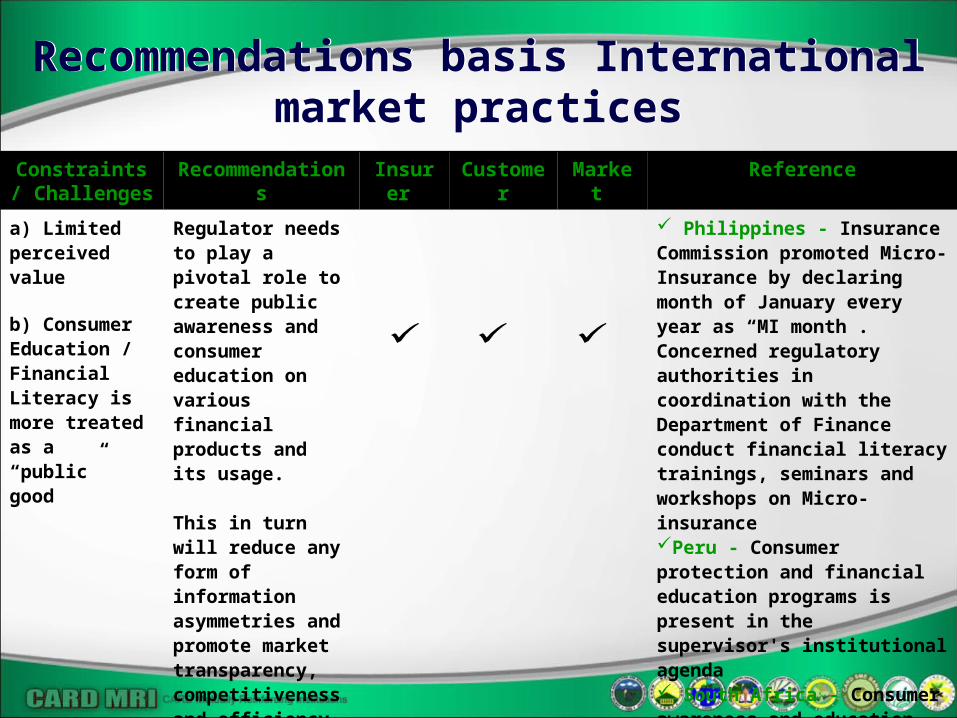

a) Limited perceived value

b) Consumer Education / Financial Literacy is more treated as a “public” good

Regulator needs to play a pivotal role to create public awareness and consumer education on various financial products and its usage.

This in turn will reduce any form of information asymmetries and promote market transparency, competitiveness and efficiency

Philippines - Insurance Commission promoted Micro-Insurance by declaring month of January every year as “MI month”. Concerned regulatory authorities in coordination with the Department of Finance conduct financial literacy trainings, seminars and workshops on Micro-insurance Peru - Consumer protection and financial education programs is present in the supervisor's institutional agenda South Africa - Consumer awareness and education campaign to be implemented by the Financial Services Board with focus on creating awareness of insurance and its value proposition

Recommendations basis International market practices

Recommendations basis International market practices

Constraints / Challenges

Recommendations Insurer Customer Market Reference

Low –income clients also show a disproportionately high distrust of insurers and insurance, requiring particular attention to product design, the sales process and claims payment

Claim settlement should be given a higher priority with a well defined regulations

Mexico - Claims should be paid within 5 working days; paid through a variety of channels, e.g. microfinance networks, through utility companies, or distribution networks

Philippines - All entities providing MI products shall process and settle claims within 10 working days. Submission of the required documents through electronic means shall be accepted

Peru - Claims should be paid within 10 days

Recommendations basis International market practices

Recommendations basis International market practices

Constraints / Challenges Recommendations Insurer Customer Market Reference

Low renewal rate (high lapsation / low persistency) as the policyholders mostly have irregular income

In addition to consumer education and awareness on insurance the regulator should also encourage features such as extended grace period

Philippines - The manner and frequency of premium collections shall, if possible, coincide with the cash flow of the insured and may be collected (e.g. weekly; monthly) whichever is applicableSouth Africa - As a minimum, cover will continue for 1 month after the due date of the premium. For policies that have been in force for one year or more, the grace period will be extended by one month for each completed twelve month period that the policy has been in force with no reduction in cover. However, the maximum grace period for a policy will be 6 months.

Recommendations basis International market practices

Recommendations basis International market practices