midas holdings limitedmidas.listedcompany.com/misc/ar2007.pdfmidas holdings limited 1 corporate...

TRANSCRIPT

Midas Holdings Limited

On Right Track

annual report 2007

MIDAS HOLDINGS LIMITED 1

Corporate Structure

Contents

1 Corporate Structure2 Corporate Profi le5 Corporate Information6 Message from the Executive Chairman8 Message from the Chief Executive Offi cer10 Board of Directors11 Executive Offi cers12 Financial Highlights13 Financial Contents

Corporate Offi ceChen Wei Ping, Executive ChairmanChew Hwa Kwang, Patrick, Chief Executive Offi cerTan Kai Teck, Chief Financial Offi cerYang Xiao Guang, General Manager (Business Development)

Jilin Midas Aluminium Industries Co., LtdWang Jiaxin, General Manager

Shanxi Wanshida Engineering Plastics Co., LtdMa Mingzhang, General Manager

Midas Beijing (Trading) Co., LtdChew Hwa Kwang, Patrick, General Manager

Annual Report 20072

Corporate Profi le

Incorporated on 17th of November 2000 as an investment holding

company, Midas Holdings Limited has grown over the years to gain

recognition as a leading manufacturer of aluminium alloy extrusion

products and polyethylene (“PE”) pipes for the rail transportation

and infrastructure sectors in the PRC.

Under the Midas Group are three business divisions, namely:

(a) the Aluminium Alloy Division,

(b) the PE Pipe Division and

(c) the Agency and Procurement Division.

These three divisions are strategically located in the PRC to take on

the opportunities as well as capitalise on the potential benefi ts of

the vast developments that are taking place in the infrastructure

and rail transport sectors.

Our customer base has evolved over the years to include MNCs

and PRC state-owned companies such as ALSTOM Transport

SA, Siemens Transportation Systems Group, CNR Changchun

Railway Vehicles Co., Ltd, CNR Tangshan Rolling Stock Works,

Nanjing SR Puzhen Rail Transport Co., Ltd, CSR Zhuzhou Electric

Locomotives, etc.

Besides our core business, we have a 32.5% stake in a licensed

metro train manufacturing company in the PRC, Nanjing SR Puzhen

Rail Transport Co., Ltd (“NPRT”).

Aluminium Alloy DivisionOur Aluminium Alloy Division, Jilin Midas Aluminium Industries Co.,

Ltd, has achieved the distinction of being the only manufacturer in

the PRC to be accredited with the Quality Focus Global Sourcing

Grade “A” international certifi cation by ALSTOM Transport SA

(“ALSTOM”), in accordance to Alstom Transport Standard. As a

testimony to our capability to manufacture large-section aluminium

alloy extrusion products, this certifi cation enables us to be the

global sourcing partner of all ALSTOM Transport units.

In addition, our Aluminium Alloy Division has entered into a Master

Agreement with Siemens Aktiengesellschaft, Berlin and Munich,

Transportation Systems Group (“Siemens”). Under this agreement,

Siemens will engage our Aluminium Alloy Division as a long term

high technology supplier of aluminium alloy extrusion products

in the context of long term partnership-based cooperation on

a global basis.

In recognition of our ability to supply the highest quality aluminium

extrusion products, our Aluminium Alloy Division was certifi ed as

an approved supplier to Changchun Bombardier Railway Vehicles

Co., Ltd (CBRC) in January 2006. CBRC is a joint venture between

Bombardier Transportation and China’s leading train manufacturer,

CNR Changchun Railway Vehicles Co., Ltd, with Bombardier

Transportation being the world leader in rail cars manufacturing.

We are now the only PRC certifi ed supplier for the world’s

three renowned train manufacturers, which is a testimony and

endorsement of the quality of our aluminium alloy extrusion

products. This recognition given by ALSTOM, Siemens and CBRC

has provided us the platform to expand and grow our business both

in the PRC and the international export markets.

In September 2007, our Aluminium Alloy Division was named

“2007 China’s Top Brand” by the General Administration of Quality

Supervision, Inspection and Quarantine of the People’s Republic of

China (“AQSIQ”) (国家质量监督检验检疫总局), in recognition of

our product quality and strong brand position.

MIDAS HOLDINGS LIMITED 3

Corporate Profi le

Our Aluminium Alloy Division currently has two production

lines, with annual production capacity of up to 20,000 tonnes.

Our production lines can produce large section aluminium

alloy extrusion products of up to 28 metres in length and 0.7

meters in width for profi les and 0.48 metres in diameter for

large diameter tubes and rods. Our large section aluminium

alloy products are used in a variety of industries. They are

utilised in the rail transportation industry to manufacture

body frames of high-speed trains and MRT/LRT trains. In

addition, our aluminium alloy products are also used in

power stations for power transmission purposes, electrical

energy distribution, transmission cables as well as production

of mechanical parts for industrial equipment.

In FY2004 and FY2005, we successfully exported our large

section aluminium alloy profi les to manufacture MRT body

frames for the Singapore Circle Line Project and the Metro

Oslo MRT project in Norway. We have further demonstrated

our capabilities in supplying aluminium alloy profi les of

international standards

and meeting the stringent

requirements of our

international customers

by securing the Valero

Rus Project for the Russian

market, the Desiro

Mainline Project for the

European and ex-European

markets and the Helsinki –

St. Petersburg high speed

train project in FY2007.

We are involved in many high profi le rail transport projects in the

PRC since 2003. Some of these projects include:

• Regional Line Phase 1 Project • Shanghai MRT Line 1 Extension 2 Project • Shanghai MRT Line 1 Extension Project • Shanghai Yangpu MRT Line Phase 1 Project • Shanghai Pearl Line Project • Nanjing MRT Project • Guangzhou MRT Line 3 Project • Tianjin MRT Project • Magnetic Levitation Train Prototype Project • Beijing - Tianjin High Speed Train Project • Changchun City Light Rail Transit Phase 1 Project • Shanghai MRT Line 2 Extension 1 Project • Shanghai Metro Line 9 Project • Shenzhen MRT Line 1 Extension Project • Shanghai Metro Line 7 Project • Nanjing Metro Line 2 Project • Shanghai Metro Line 10 Project

We are currently the market leader in supplying large section

aluminium alloy profi les for the railway industry in the PRC.

Signifi cantly, we have been appointed as the sole supplier for the

local content portions of two major high speed train projects in the

PRC, namely:

• Regional Line Phase 1 Project, by Changchun Railway Vehicles in collaboration with Alstom

• Beijing to Tianjin High Speed Train Project by Tangshan Rolling Stock Works in collaboration with Siemens

The recognition for our manufacturing capability of aluminium

alloy extrusion products positions us for greater growth in

the PRC market. Moving forward, we aim to expand our

presence internationally by capitalising on opportunities

emanating from the overseas market.

PE Pipe DivisionOur PE Pipe Division, manufactures and installs PE Pipes for

use in various types of piping networks, including gas piping

networks and water distribution networks.

Made of high density polyethylene, our PE Pipes are relatively

light-weight and chemically inert. Considered as viable

substitutes for traditional concrete and metal pipes, PE Pipes

are easier and safer to install, more durable and fl exible. A

proponent that is non-toxic in nature, our PE Pipes are cost

effi cient and possess high resistance to corrosion.

Broadly categorised into two types of PE Pipes, namely the

Gas PE Pipes and the Water PE Pipes which are manufactured

through the extrusion process, we manufacture the various

parts required in a piping network, including pipes, joints and

fi ttings.

Annual Report 20074

Corporate Profi le

Our markets segments include new and replacement markets

for the PRC municipal cities gas transmission and water

distribution infrastructure projects, where PE Pipes are used

in the cities’ transmission and distribution networks.

Agency and Procurement DivisionWe set up our Agency and Procurement Division in

November 2005. This division deals with the import, export

and wholesale of aluminium alloy, polyethylene pipes, metal

materials and other related products. It also serves as the

procurement centre for our two other business divisions. We

intend to leverage on our existing established relationships

and networks, by bringing together both suppliers and

customers, to expand our product range to our existing and

potential customers. In this manner, we can value add and

better serve the requirements and needs of our customers.

Joint VentureWe have a 32.5% equity stake in a Sino-foreign joint venture, Nanjing SR Puzhen Rail Transport Co., Ltd. (“NPRT”), which started commercial production in FY2007. Through NPRT, we are able to further entrench our position in the PRC railway industry as NPRT is only one of the four rolling stock companies in the PRC licensed to manufacture and sell metro trains on a nationwide basis. Many PRC cities have plans to build metro lines to facilitate urban transportation, we believe that NPRT will be a direct benefi ciary of the high growth metro train industry in the PRC given the limited number of players in

the market.

Since inception, NPRT, together with its consortium partners,

has secured four high profi le metro train projects in the PRC,

namely:

• Nanjing Metro Line 2 Project,

• Shanghai Metro Line 10 Project,

• Nanjing Metro Line 1 Extension Project and

• Shanghai Metro Line 2 Eastern Extension Project.

Our Aluminium Alloy Division has entered into a Master

Supply Agreement with NPRT to supply aluminium alloy

profi les for metro train projects that NPRT secure up till 31

December 2010.

Moving ForwardIn December 2007, we have also entered into a Framework

Agreement with Aluminium Corporation of China

(“Chinalco”), the largest aluminium producer in the PRC and

one of the largest producers of aluminium and alumina in the

world. Under the terms of the Framework Agreement, both

parties will actively collaborate in the business development

of aluminium alloy plates, sheets and profi les. The fi rst

collaboration will be in respect of China Northeast Light Alloy

Co., Ltd’s “thick aluminium alloy plates and sheets project”.

In addition, Chinalco will also seek collaboration with Midas

in the development and investment of aluminium alloy

extrusion profi les for rail car bodies.

In our comparatively short history, we are encouraged by

our current success. Moving forward, we are committed

to springboard towards greater expansion, growth value

creation, as well as strengthen our key competencies.

MIDAS HOLDINGS LIMITED 5

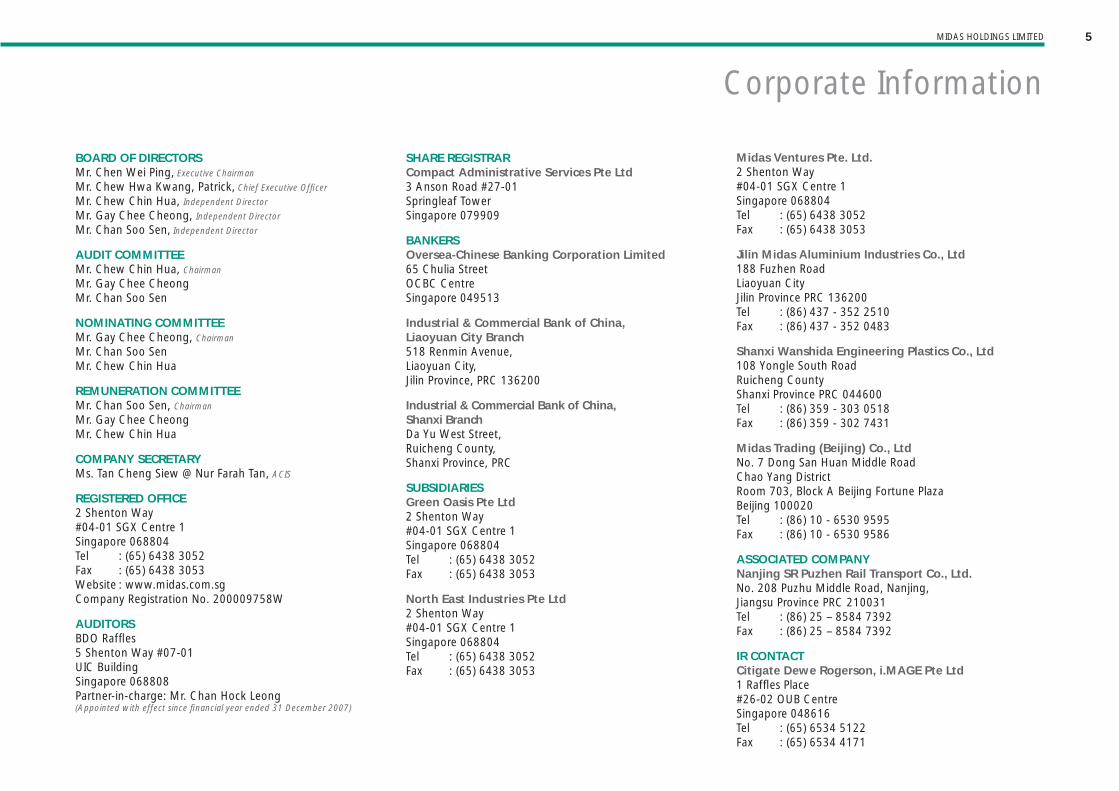

BOARD OF DIRECTORSMr. Chen Wei Ping, Executive Chairman

Mr. Chew Hwa Kwang, Patrick, Chief Executive Offi cer

Mr. Chew Chin Hua, Independent Director

Mr. Gay Chee Cheong, Independent Director

Mr. Chan Soo Sen, Independent Director

AUDIT COMMITTEEMr. Chew Chin Hua, Chairman

Mr. Gay Chee CheongMr. Chan Soo Sen

NOMINATING COMMITTEEMr. Gay Chee Cheong, Chairman

Mr. Chan Soo SenMr. Chew Chin Hua

REMUNERATION COMMITTEEMr. Chan Soo Sen, Chairman

Mr. Gay Chee CheongMr. Chew Chin Hua

COMPANY SECRETARYMs. Tan Cheng Siew @ Nur Farah Tan, ACIS

REGISTERED OFFICE2 Shenton Way#04-01 SGX Centre 1Singapore 068804Tel : (65) 6438 3052Fax : (65) 6438 3053Website : www.midas.com.sgCompany Registration No. 200009758W

AUDITORSBDO Raffl es5 Shenton Way #07-01UIC Building Singapore 068808Partner-in-charge: Mr. Chan Hock Leong(Appointed with effect since fi nancial year ended 31 December 2007)

SHARE REGISTRARCompact Administrative Services Pte Ltd3 Anson Road #27-01Springleaf Tower Singapore 079909

BANKERSOversea-Chinese Banking Corporation Limited65 Chulia StreetOCBC CentreSingapore 049513

Industrial & Commercial Bank of China, Liaoyuan City Branch518 Renmin Avenue, Liaoyuan City, Jilin Province, PRC 136200

Industrial & Commercial Bank of China, Shanxi BranchDa Yu West Street, Ruicheng County, Shanxi Province, PRC

SUBSIDIARIESGreen Oasis Pte Ltd2 Shenton Way#04-01 SGX Centre 1Singapore 068804Tel : (65) 6438 3052Fax : (65) 6438 3053

North East Industries Pte Ltd2 Shenton Way#04-01 SGX Centre 1Singapore 068804Tel : (65) 6438 3052Fax : (65) 6438 3053

Midas Ventures Pte. Ltd.2 Shenton Way#04-01 SGX Centre 1Singapore 068804Tel : (65) 6438 3052Fax : (65) 6438 3053

Jilin Midas Aluminium Industries Co., Ltd188 Fuzhen RoadLiaoyuan CityJilin Province PRC 136200 Tel : (86) 437 - 352 2510Fax : (86) 437 - 352 0483

Shanxi Wanshida Engineering Plastics Co., Ltd108 Yongle South RoadRuicheng CountyShanxi Province PRC 044600Tel : (86) 359 - 303 0518Fax : (86) 359 - 302 7431

Midas Trading (Beijing) Co., LtdNo. 7 Dong San Huan Middle RoadChao Yang DistrictRoom 703, Block A Beijing Fortune PlazaBeijing 100020Tel : (86) 10 - 6530 9595Fax : (86) 10 - 6530 9586

ASSOCIATED COMPANYNanjing SR Puzhen Rail Transport Co., Ltd.No. 208 Puzhu Middle Road, Nanjing, Jiangsu Province PRC 210031Tel : (86) 25 – 8584 7392Fax : (86) 25 – 8584 7392

IR CONTACTCitigate Dewe Rogerson, i.MAGE Pte Ltd1 Raffl es Place #26-02 OUB CentreSingapore 048616Tel : (65) 6534 5122Fax : (65) 6534 4171

Corporate Information

Annual Report 20076

Message from the Executive Chairman

Dear Shareholders,

On behalf of the Board of Directors, I am pleased to present to you our annual report for the fi nancial year ended 31 December 2007.

2007 was a fruitful year for Midas. This year, we focused on growing our market share in the PRC and increasing our penetration of the international market. We continue to secure new contracts throughout the year and our customers included top global train manufacturers and PRC licensed train manufacturers. We are fl attered by their continued support, which attest to our reputation for quality products.

During the year under review, we secured several major projects in the PRC. We were appointed as the main supplier for the Shanghai Metro Line 2 Extension 1 Project, Shanghai Metro Line 9 Project, Shenzhen Metro Line 1 Extension Project, Shanghai Metro Line 7 Project, Nanjing Metro Line 2 Project and Regional Line Phase 1 project.

While the fast-growing PRC market continues to be the main focus of our expansion plans, we are also seizing growth opportunities in the international markets, as the PRC is increasingly becoming the preferred sourcing hub for global train manufacturers. In 2007, we secured three projects in the international markets from Siemens and Alstom including:

• The Valero Rus Project in Russia, • The Desiro Mainline Project for European and ex-European

markets and • The Helsinki – St Petersburg High Speed Train Project.

The recognition and confi dence accorded to us by these global train manufacturers refl ect our high product quality and our ability to meet stringent international standards. We will continue to intensify our business development and marketing efforts overseas to increase our presence globally.

Our associated company, Nanjing SR Puzhen Rail Transport Co., Ltd (“NPRT”), made a strong debut in 2007. Since it began operations in 2007, it has secured four high profi le metro train projects in the PRC, namely the Nanjing Metro

Line 2 Project, the Shanghai Metro Line 10 Project, the Nanjing Metro Line 1 Extension Project, and the Shanghai Metro Line 2 Eastern Extension Project. Given that NPRT is one of four rolling stock companies approved to undertake metro train projects on a nationwide basis in China, we believe that NPRT will continue to be a key benefi ciary of the rapid infrastructural development in the PRC.

Apart from being known as a quality manufacturer, we were recognised in 2007 for having a strong brand name within the industry. In 2007, our Aluminium Alloy Division was named “2007 China’s Top Brand” by the General Administration of Quality Supervision, Inspection and Quarantine of the People’s Republic of China (“AQSIQ”) (国家质量监督检验检

疫总局). We were judged under the category of “Aluminium Alloy Materials (Railway Cars Structural Usage)” category, which reaffi rms our leadership position in this sector.

In the year ahead, we will not rest on our laurels and will strive to stay ahead of the market, and more importantly, meet the ever-increasing technical demands of our customers. We are committed to seeking out new growth opportunities for the Group and in turn, enhancing shareholders’ value.

On behalf of the Board of Directors, I would like to express my most sincere appreciation to our shareholders for their support. I would also like to take this opportunity to express my appreciation to our staff and management for their commitment to the Group, and to our customers, suppliers and business associates for their confi dence in us. Finally, as we enter 2008, we look forward to your continued support as we strive to take Midas to its next level of growth!

Chen Wei Ping Executive Chairman

Chen Wei PingExecutive ChairmanChen Wei PingExecutive Chairm

MIDAS HOLDINGS LIMITED 7

Message from the Executive Chairman

对麦达斯来说,2007年取得的成果可说得上是硕果累累。在这一年里,我们继续扩大在中国市场上的市场份额,并在国际市场上取得新突破。我们连续取得多个新项目的合约,其中的客户包括国际和国内顶尖的火车制造商。我们非常荣幸获得他们对我们高品质产品的持续支持。

在这一年里,我们在中国继续获选参与多个大

型项目,包括成为以下项目主要的供应商:上海地铁2号线延伸线第一期项目、上海地铁9号线项目、深圳地铁1号线延伸线项目、上海地铁7号线项目、南京地铁2号线项目与区域线第一阶段项目。

在着重于发展中国市场的同时,我们也不断在国际市场上争取发展机会。随着中国逐渐成为国际火车制造商的首选采购对象的枢纽,我们很荣幸能在国际市场上获选参与三项 Siemens 与 Alstom 的项目:

• 俄罗斯的 Valero Rus 项目• 欧洲及欧洲以外市场的 Desiro Mainline 项目• 赫尔辛基 - 圣彼得堡高速列车项目

这些国际火车制造商对我们的信心与支持证明我们高品质的产品符合严格国际标准。我们将继续加强我们在国际市场上的销售网络,以扩大我们在国际上的市场份额。

我们的合资公司,南京南车浦镇城轨车辆有限责任公司(“NPRT”),在2007年取得良好的成绩。从2007年1月份开始投产以来,NPRT已取得四个大型的城轨项目,包括南京地铁2号线项目、上海地铁10号线项目、南京地铁1号线延伸线项目与上海2号线东延线项目。NPRT是获准承接中国全国城市城轨项目的四家拥有资质的城轨车辆厂之一,我们相信NPRT将能够抓紧蓬勃发展的城轨基建业所带来的发展机会。

我们除了在品质上获得同业的认同,品牌方面也在过去一年里受到认可。在2007年,吉林麦达斯铝业的产品获得国家质量监督检验检疫总局认可为“中国名牌产品 [铝合金型材(轨道车辆结构用)]”。能够获得此项肯定,再次证明我们在这行业的领导地位。

在未来的一年里,我们将继续走在市场的前端 。 更 重 要 的 是 , 我 们 将 力 求 达 到 并 超 越客户不断提升的技术要求。我们会继续努力追 求 发 展 机 会 , 并 且 尽 心 尽 力 地 提 升 股 东价值。

我谨此借这个机会代表全体董事会,致以我们的股东最真诚的感谢,谢谢您坚定的支持。感谢我们的职员和管理层对公司的投入,以及客户、供应商和业务伙伴的信赖。我们期待您在 2008年继续支持我们,把麦达斯带入另一个高峰!

陈维平执行主席

亲爱的股东们:

很荣幸再次为您呈上麦达斯控股截至2007年12月31日财政年的年报。

Annual Report 20078

Dear Shareholders,

In 2007, we further entrenched our position as the leading manufacturer of aluminium alloy extrusion products for the rail transportation sector in the PRC. With the robust speed of development in the rail transportation networks in the PRC, our Aluminium Alloy Division, Jilin Midas Aluminium Industries Co., Ltd (吉林麦达斯铝业有限公司) continued its strong performance, driving the Group’s overall growth.

For the full year ended 31 December 2007, our net profi t

grew 24.8% to S$31.9 million on the back of a 34.0%

increase in Group’s revenue to S$140.4 million.

Our Aluminium Alloy Division was the key contributor to

the Group’s growth in 2007, accounting for 76.9% of total

revenue and 92.5% of the Group’s profi t before interest

and tax. Revenue from the Aluminium Alloy Division jumped

50.3% to S$107.9 million in 2007, up from S$71.8 million in

the fi nancial year ended 31 December 2006.

Strengthening Our Leadership Position

Over the past few years, we have been steadily building our

track record as a leading supplier of quality aluminium alloy

profi les for rail car bodies in the PRC. Since 2003, we have

participated in more than 20 projects in the PRC and the

international markets.

In 2007, our Aluminium Alloy Division secured a number

of contracts in the PRC including: Shanghai Metro Line

2 Extension 1 Project, Shanghai Metro Line 9 Project,

Shenzhen Metro Line 1 Extension Project, Shanghai Metro

Line 7 Project, Nanjing Metro Line 2 Project and Regional Line

Phase 1 project. We are the main supplier of aluminium alloy

extrusion profi les for these projects, refl ecting our customers’

confi dence in our high quality products.

Besides projects in the PRC, our Aluminium Alloy Division

also made signifi cant progress in growing the international

markets. During the year, we successfully secured international

projects from Alstom and Siemens, including: Valero Rus

Project in Russia, Desiro Mainline Project for European and

ex-European markets and Helsinki – St Petersburg High

Speed Train Project. Our ability to secure projects from these

established multinational corporations – which possess

stringent international standards and appoint only the

highest quality suppliers - speak for our potential to compete

in the global arena.

2007 also marked the maiden contribution from our

associated company, Nanjing SR Puzhen Rail Transport Co.,

Ltd (“NPRT”). In 2007, NPRT contributed S$1.3 million to

our bottomline. Together with its consortium partners, NPRT

has since secured four high profi le metro train projects in the

PRC, namely the Nanjing Metro Line 2 Project, the Shanghai

Metro Line 10 Project, the Nanjing Metro Line 1 Extension

Project, and the Shanghai Metro Line 2 Eastern Extension

Project. Going forward, we believe NPRT will continue to win

new contracts and improve on its production effi ciency.

Just before the year ended, we made another signifi cant

breakthrough with a Framework Agreement signed with

Aluminum Corporation of China (“Chinalco”), the largest

aluminium producer in the PRC and one of the largest

producers of aluminium and alumina in the world. Under

the agreement, we will actively explore collaboration in the

business development of aluminium alloy plates, sheets

and profi les. We will leverage on each other’s competitive

strengths and support each other in strategic co-operations

that would be mutually benefi cial to both parties.

Chew Hwa Kwang, PatrickChief Executive Offi cer

Message from the Chief Executive Offi cer

Chew HwChief Exe

MIDAS HOLDINGS LIMITED 9

Message from the Chief Executive Offi cer

Under this agreement, the fi rst collaboration by both parties

will be in respect of China Northeast Light Alloy Co., Ltd.’s

(“NELA”) (东北轻合金有限责任公司) “thick aluminium

alloy plates and sheets project”. Chinalco has a controlling

stake in NELA and detailed terms of the collaboration will be

fi nalised at a later date. In addition, Chinalco will also seek

collaboration with Midas in the development and investment

of aluminium alloy extrusion profi les for rail car bodies.

Strong Outlook and Prospects

With infrastructural and transportation development as

integral parts of the PRC’s 11th fi ve-year plan, we are

optimistic about the industry outlook for Midas as the PRC

government accelerates investments in public railways and

metro networks to support the country’s economic growth.

With growing urbanisation

and increasing population

in cities, major cities in

the PRC are building new

metro lines or expanding

their existing metro

networks to facilitate

urban transportation. In

addition, the improvement

of inter-city transportation

is also leading to more

opportunities for railway

projects across the country.

Meanwhile, our strategic partnership with Chinalco will also

open doors to opportunities in the market of aluminium

alloy sheets and plates. We are in the midst of discussions

with Chinalco on potential collaborations and will update

shareholders on developments once details are fi nalised.

We will also continue to further our expansion into the

international markets, especially in Europe and Asia. As

global train manufacturers increasingly turn to the PRC for

their sourcing needs, we believe that demand for quality

suppliers that can meet stringent international standards can

only increase. Given that we have obtained international

certifi cations from the world’s leading train companies –

Alstom and Siemens, we are in a strong position to capitalise

on the rising outsourcing trend to the PRC to secure more

international contracts.

Words of Thanks

In conclusion, I would like to take this opportunity to express

my appreciation to all shareholders who have supported

Midas and believed in us over the years. In addition, I would

like to thank all our valued customers and business partners

who have given us the many opportunities for growth. To

our Board of Directors, thank you for the invaluable advice

you have contributed to the Group. Last but not least, my

gratitude goes out to all staff of Midas who have worked

hard to make 2007 a fruitful year. Looking ahead, we are

optimistic about Midas’ outlook and prospects in 2008.

We look forward to delivering another year of growth for

shareholders!

Chew Hwa Kwang, Patrick

Chief Executive Offi cer

Annual Report 200710

since November 2000. He played a major role in the listing of our Company’s shares on the Singapore Exchange Securities Trading Limited on 23 February 2004. Mr. Chew has more than twenty years of management experience and currently holds directorship in several companies in Singapore.

Mr. Chew is concurrently the General Manager of our Agency and Procurement Division, responsible for the overall business operations of this division.

Mr. Chew Chin HuaIndependent DirectorMr. Chew Chin Hua, age 52, was appointed as an Independent Director of our Company on 6 January 2004. Mr. Chew is a member of the Association of Chartered Certifi ed Accountants and the Institute of Certifi ed Public Accountants in Singapore and has more than twenty years of experience in the accounting and auditing profession. He is also a director of several other listed companies in Singapore.

Mr. Gay Chee CheongIndependent DirectorMr. Gay Chee Cheong, age 51, was appointed as an Independent Director on 23 June 2004. Mr. Gay co-founded 2G Capital Pte Ltd, a private equity investment company investing in the Asia Pacifi c economies. Prior to 2G Capital, Mr.

Mr. Chen Wei PingExecutive ChairmanMr. Chen Wei Ping, age 47, was appointed as our Director on 21 August 2002 and has been Executive Chairman since March 2003. Mr. Chen is instrumental in developing and steering our Group’s corporate directions and strategies. He is responsible for the effective management of business relations with our strategic partners. In addition, Mr. Chen spearheaded the listing of our Company’s shares on the Singapore Exchange Securities Trading Limited on 23 February 2004. Mr. Chen has more than twenty years of management experience and currently holds directorship in several companies in the PRC and Singapore. He holds a Bachelor Degree in Economics from Jilin Finance & Trade College (PRC) and a Master Degree in Economics from Jilin University (PRC).

Mr. Chew Hwa Kwang, PatrickChief Executive Offi cerMr. Chew Hwa Kwang, Patrick, age 45, is a founding member of our Group and is our Chief Executive Offi cer who is responsible for the overall operations and fi nance of our Group and its fi nancial well-being. Mr. Chew is responsible for identifying future business opportunities and services which our Group may provide to drive future growth. Mr. Chew is also in charge of overseeing the day-to-day management of our Group as well as our Group’s strategic and business development. Mr. Chew has served as our Executive Director

Gay was the Group Executive Director of JIT Holdings Limited and the Managing Director to the various JIT companies in Singapore, China and Europe. Mr. Gay holds directorships in several listed and non-listed companies in Singapore. Mr. Gay holds a Bachelor Degree in Electronics Engineering (Honours) from the Royal Military College of Science Shrivenham, UK, a Bachelor Degree in Economics (Honours) from the University of London, UK and a Master of Business Administration from the National University of Singapore.

Mr. Chan Soo SenIndependent DirectorMr. Chan Soo Sen, age 51, was appointed as an Independent Director of our Company on 29 June 2006. He is currently the Director, Chairman’s Offi ce and Director, Group Human Resources for Keppel Corporation Limited, and Member of Parliament for Joo Chiat Constituency. Mr. Chan was previously a Minister of State and has served in several ministries including the Ministry of Education, Ministry of Trade and Industry and Ministry of Community Development, Youth and Sports. Before entering the political scene, Mr. Chan started up the China-Singapore Suzhou Industrial Park as the founding CEO in 1994, laying the foundation and framework for infrastructure and utilities development. Mr. Chan holds a Master in Management Science from the University of Stanford, United States of America and is a director of a few listed companies in Singapore.

Board of Directors

1

2

3

4

5

1 Mr. Chen Wei Ping (Executive Chairman)

2 Mr. Chew Hwa Kwang, Patrick (Chief Executive Offi cer)

3 Mr. Chew Chin Hua (Independent Director)

4 Mr. Gay Chee Cheong (Independent Director)

5 Mr. Chan Soo Sen (Independent Director)

2

MIDAS HOLDINGS LIMITED 11

Executive Offi cers

Mr. Tan Kai Teck, Chief Financial Offi cerMr. Tan Kai Teck, age 38, is our Chief Financial Offi cer responsible for our fi nancial management and the reporting functions of our Group. Mr. Tan holds a Bachelor Degree in Accountancy (Second Upper Class Honours) from the Nanyang Technological University and is a member of the Institute of Certifi ed Public Accountants of Singapore.

Mr. Yang Xiao Guang, General Manager (Business Development)Mr. Yang Xiao Guang, age 48, is our General Manager (Business Development) responsible for the execution and implementation of the development and business strategies of our Group. He is also involved in new business development and new venture management. Mr. Yang holds a Bachelor Degree in Economics from Jilin Finance & Trade College (PRC) and a Master Degree in the Science of Law from Jilin University (PRC).

Mr. Wang Jiaxin, General ManagerMr. Wang Jiaxin, age 52, is the General Manager of Jilin Midas Aluminium Industries Co., Ltd. Mr. Wang is responsible for the overall business operations of the Aluminium Alloy Division. Mr. Wang holds a Bachelor Degree in Mechanical Engineering from Jilin University (PRC).

Mr. Ma Mingzhang, General ManagerMr. Ma Mingzhang, age 54, is the General Manager of Shanxi Wanshida Engineering Plastics Co., Ltd. Mr. Ma is responsible for the overall business operations of the PE Pipe Division. Mr. Ma holds a Bachelor Degree in Industrial Automation Instrument from Harbin Industry University (PRC) and a Master Degree in Science and Engineering from Chengdu Science and Technology University (PRC).

Annual Report 200712

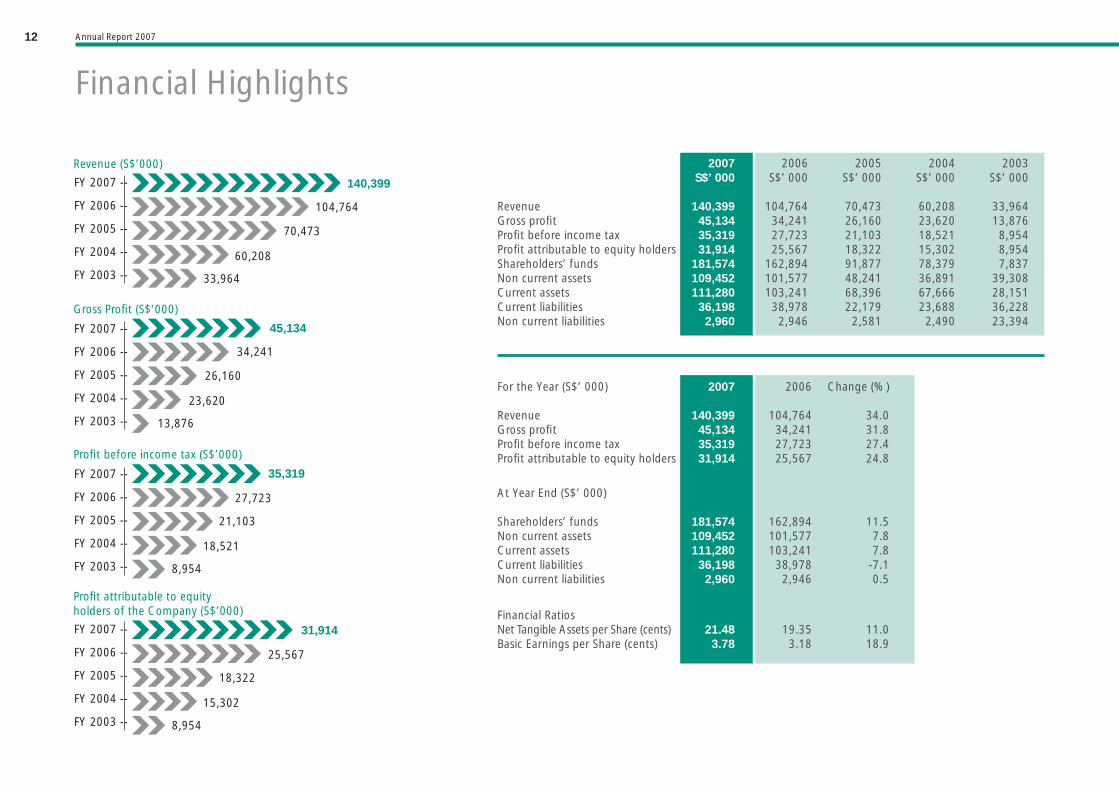

Financial Highlights

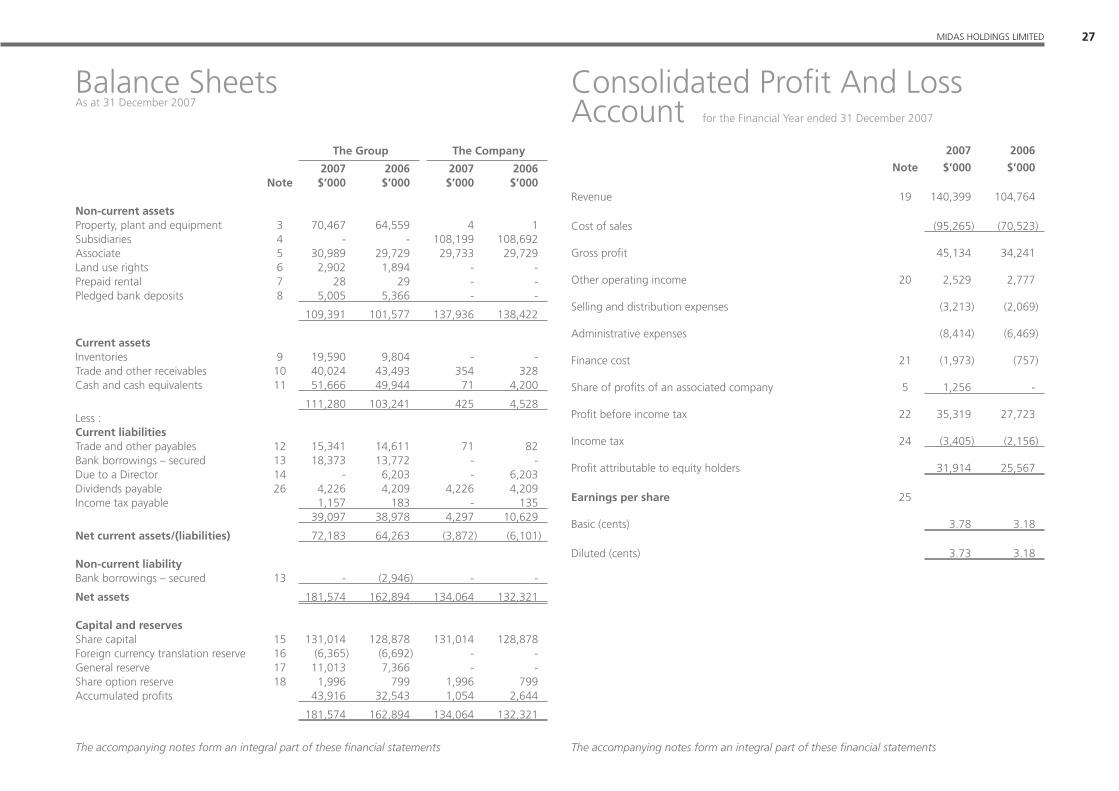

2007 2006 2005 2004 2003 S$’ 000 S$’ 000 S$’ 000 S$’ 000 S$’ 000

Revenue 140,399 104,764 70,473 60,208 33,964Gross profi t 45,134 34,241 26,160 23,620 13,876Profi t before income tax 35,319 27,723 21,103 18,521 8,954Profi t attributable to equity holders 31,914 25,567 18,322 15,302 8,954Shareholders’ funds 181,574 162,894 91,877 78,379 7,837Non current assets 109,452 101,577 48,241 36,891 39,308Current assets 111,280 103,241 68,396 67,666 28,151Current liabilities 36,198 38,978 22,179 23,688 36,228Non current liabilities 2,960 2,946 2,581 2,490 23,394

For the Year (S$’ 000) 2007 2006 Change (%)

Revenue 140,399 104,764 34.0Gross profi t 45,134 34,241 31.8Profi t before income tax 35,319 27,723 27.4Profi t attributable to equity holders 31,914 25,567 24.8

At Year End (S$’ 000)

Shareholders’ funds 181,574 162,894 11.5Non current assets 109,452 101,577 7.8Current assets 111,280 103,241 7.8Current liabilities 36,198 38,978 -7.1Non current liabilities 2,960 2,946 0.5

Financial RatiosNet Tangible Assets per Share (cents) 21.48 19.35 11.0Basic Earnings per Share (cents) 3.78 3.18 18.9

FY 2007 --

FY 2006 --

FY 2005 --

FY 2004 --

FY 2003 --

Revenue (S$’000)

33,964

60,208

70,473

104,764

140,399

FY 2007 --

FY 2006 --

FY 2005 --

FY 2004 --

FY 2003 --

Gross Profi t (S$’000)

13,876

23,620

26,160

34,241

45,134

FY 2007 --

FY 2006 --

FY 2005 --

FY 2004 --

FY 2003 --

Profi t before income tax (S$’000)

8,954

18,521

21,103

27,723

35,319

FY 2007 --

FY 2006 --

FY 2005 --

FY 2004 --

FY 2003 --

Profi t attributable to equityholders of the Company (S$’000)

8,954

15,302

18,322

25,567

31,914

Midas Holdings Limited

2 Shenton Way #04-01 SGX Centre 1, Singapore 068804Tel : (65) 6438 3052Fax : (65) 6438 3053Company Registration No. 200009758W

www.midas.com.sg

14 Financial Review16 Risk Management 17 Corporate Governance Statement22 Directors’ Report25 Statement by the Directors26 Independent Auditors’ Report27 Balance Sheets27 Consolidated Profi t And Loss Account28 Statement of Changes in Equity31 Consolidated Statement of Cash Flow32 Notes to the Financial Statements58 Statistics of Shareholdings58 Substantial Shareholders59 Notice Of Annual General Meeting Proxy Form

Financial Statements

Annual Report 200714

Financial Review

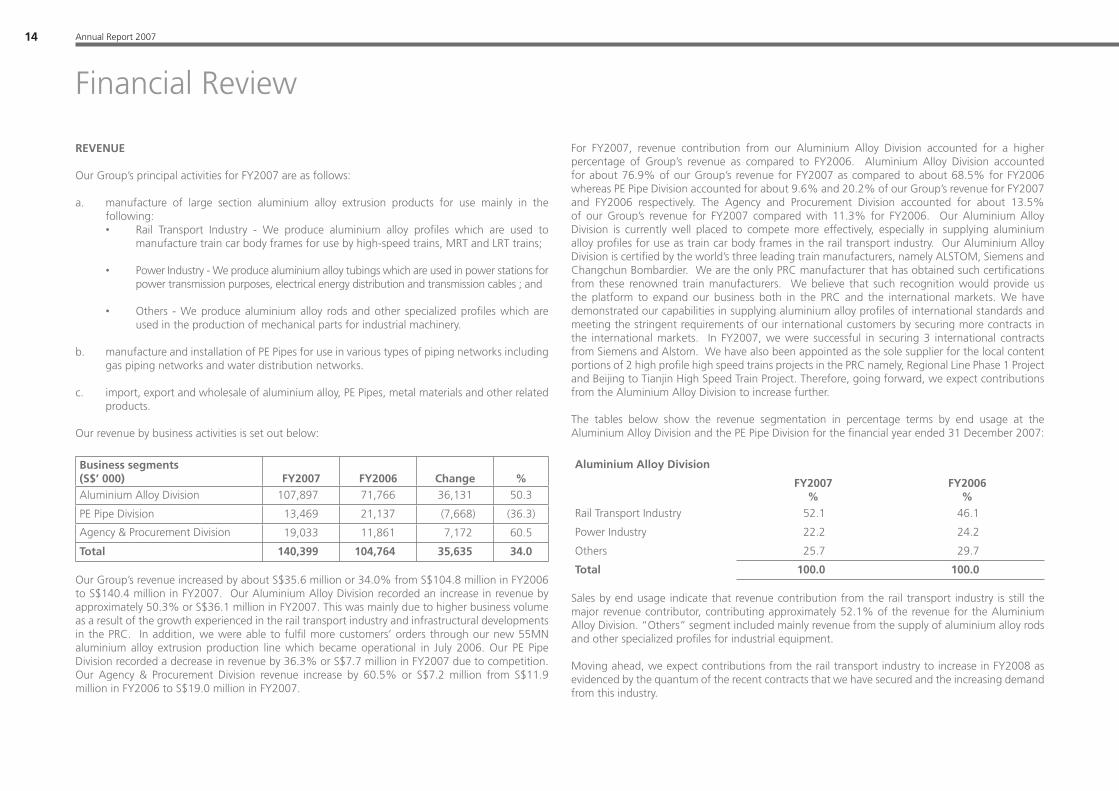

REVENUE

Our Group’s principal activities for FY2007 are as follows:

a. manufacture of large section aluminium alloy extrusion products for use mainly in the following:

• Rail Transport Industry - We produce aluminium alloy profi les which are used to manufacture train car body frames for use by high-speed trains, MRT and LRT trains;

• Power Industry - We produce aluminium alloy tubings which are used in power stations for power transmission purposes, electrical energy distribution and transmission cables ; and

• Others - We produce aluminium alloy rods and other specialized profi les which are used in the production of mechanical parts for industrial machinery.

b. manufacture and installation of PE Pipes for use in various types of piping networks including gas piping networks and water distribution networks.

c. import, export and wholesale of aluminium alloy, PE Pipes, metal materials and other related products.

Our revenue by business activities is set out below:

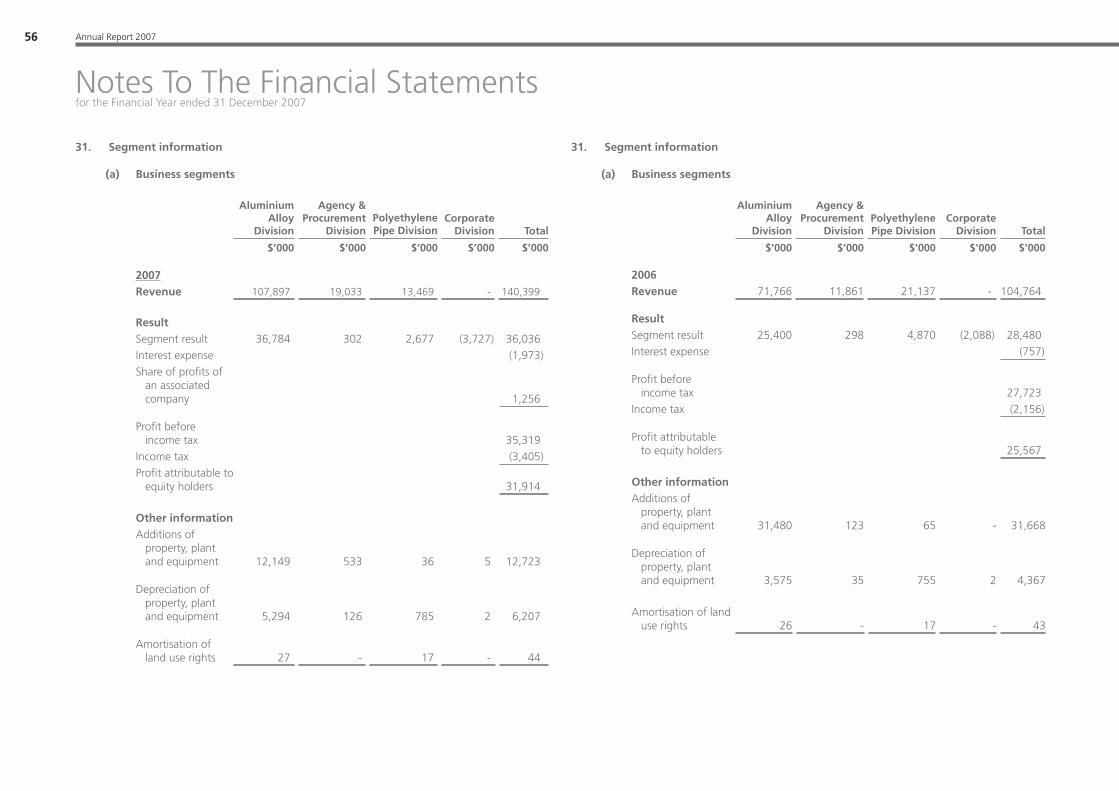

Business segments (S$’ 000) FY2007 FY2006 Change %Aluminium Alloy Division 107,897 71,766 36,131 50.3

PE Pipe Division 13,469 21,137 (7,668) (36.3)

Agency & Procurement Division 19,033 11,861 7,172 60.5

Total 140,399 104,764 35,635 34.0

Our Group’s revenue increased by about S$35.6 million or 34.0% from S$104.8 million in FY2006 to S$140.4 million in FY2007. Our Aluminium Alloy Division recorded an increase in revenue by approximately 50.3% or S$36.1 million in FY2007. This was mainly due to higher business volume as a result of the growth experienced in the rail transport industry and infrastructural developments in the PRC. In addition, we were able to fulfi l more customers’ orders through our new 55MN aluminium alloy extrusion production line which became operational in July 2006. Our PE Pipe Division recorded a decrease in revenue by 36.3% or S$7.7 million in FY2007 due to competition. Our Agency & Procurement Division revenue increase by 60.5% or S$7.2 million from S$11.9 million in FY2006 to S$19.0 million in FY2007.

For FY2007, revenue contribution from our Aluminium Alloy Division accounted for a higher percentage of Group’s revenue as compared to FY2006. Aluminium Alloy Division accounted for about 76.9% of our Group’s revenue for FY2007 as compared to about 68.5% for FY2006 whereas PE Pipe Division accounted for about 9.6% and 20.2% of our Group’s revenue for FY2007 and FY2006 respectively. The Agency and Procurement Division accounted for about 13.5% of our Group’s revenue for FY2007 compared with 11.3% for FY2006. Our Aluminium Alloy Division is currently well placed to compete more effectively, especially in supplying aluminium alloy profi les for use as train car body frames in the rail transport industry. Our Aluminium Alloy Division is certifi ed by the world’s three leading train manufacturers, namely ALSTOM, Siemens and Changchun Bombardier. We are the only PRC manufacturer that has obtained such certifi cations from these renowned train manufacturers. We believe that such recognition would provide us the platform to expand our business both in the PRC and the international markets. We have demonstrated our capabilities in supplying aluminium alloy profi les of international standards and meeting the stringent requirements of our international customers by securing more contracts in the international markets. In FY2007, we were successful in securing 3 international contracts from Siemens and Alstom. We have also been appointed as the sole supplier for the local content portions of 2 high profi le high speed trains projects in the PRC namely, Regional Line Phase 1 Project and Beijing to Tianjin High Speed Train Project. Therefore, going forward, we expect contributions from the Aluminium Alloy Division to increase further.

The tables below show the revenue segmentation in percentage terms by end usage at the Aluminium Alloy Division and the PE Pipe Division for the fi nancial year ended 31 December 2007:

Aluminium Alloy Division

FY2007%

FY2006%

Rail Transport Industry 52.1 46.1

Power Industry 22.2 24.2

Others 25.7 29.7

Total 100.0 100.0

Sales by end usage indicate that revenue contribution from the rail transport industry is still the major revenue contributor, contributing approximately 52.1% of the revenue for the Aluminium Alloy Division. “Others” segment included mainly revenue from the supply of aluminium alloy rods and other specialized profi les for industrial equipment.

Moving ahead, we expect contributions from the rail transport industry to increase in FY2008 as evidenced by the quantum of the recent contracts that we have secured and the increasing demand from this industry.

MIDAS HOLDINGS LIMITED 15

Financial Review

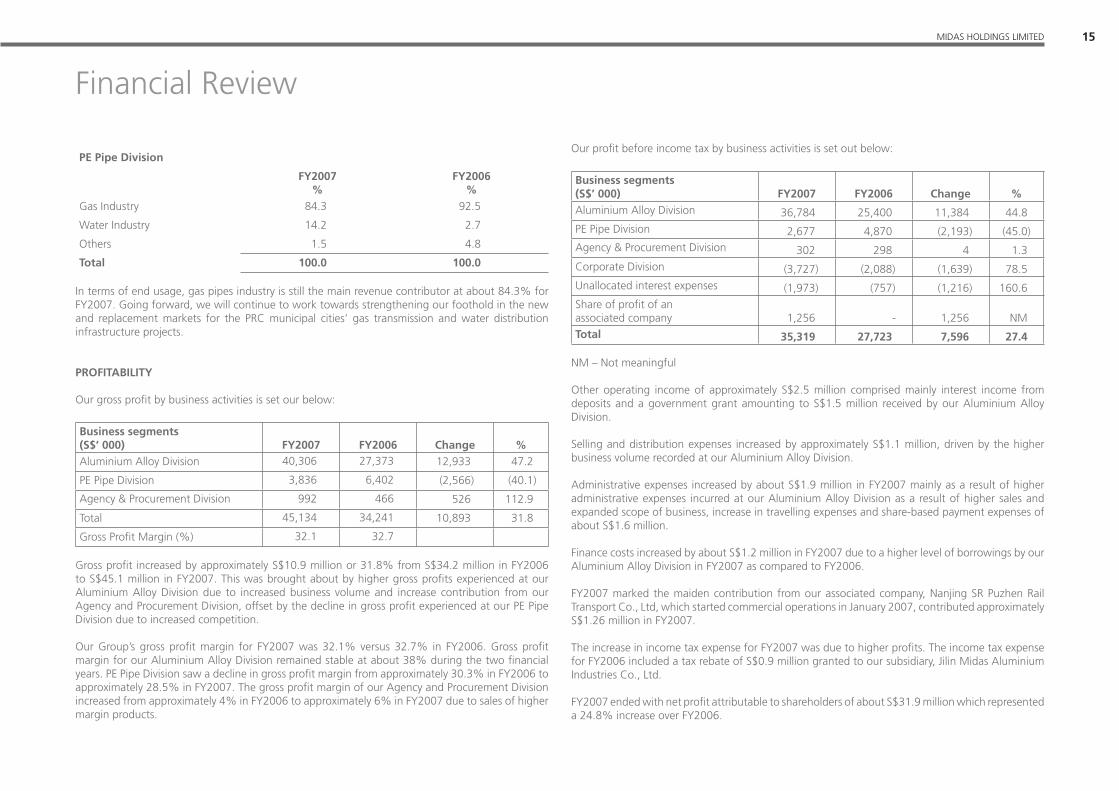

PE Pipe Division

FY2007%

FY2006%

Gas Industry 84.3 92.5

Water Industry 14.2 2.7

Others 1.5 4.8

Total 100.0 100.0

In terms of end usage, gas pipes industry is still the main revenue contributor at about 84.3% for FY2007. Going forward, we will continue to work towards strengthening our foothold in the new and replacement markets for the PRC municipal cities’ gas transmission and water distribution infrastructure projects.

PROFITABILITY

Our gross profi t by business activities is set our below:

Business segments(S$’ 000) FY2007 FY2006 Change %Aluminium Alloy Division 40,306 27,373 12,933 47.2

PE Pipe Division 3,836 6,402 (2,566) (40.1)

Agency & Procurement Division 992 466 526 112.9

Total 45,134 34,241 10,893 31.8

Gross Profi t Margin (%) 32.1 32.7

Gross profi t increased by approximately S$10.9 million or 31.8% from S$34.2 million in FY2006 to S$45.1 million in FY2007. This was brought about by higher gross profi ts experienced at our Aluminium Alloy Division due to increased business volume and increase contribution from our Agency and Procurement Division, offset by the decline in gross profi t experienced at our PE Pipe Division due to increased competition.

Our Group’s gross profi t margin for FY2007 was 32.1% versus 32.7% in FY2006. Gross profi t margin for our Aluminium Alloy Division remained stable at about 38% during the two fi nancial years. PE Pipe Division saw a decline in gross profi t margin from approximately 30.3% in FY2006 to approximately 28.5% in FY2007. The gross profi t margin of our Agency and Procurement Division increased from approximately 4% in FY2006 to approximately 6% in FY2007 due to sales of higher margin products.

Our profi t before income tax by business activities is set out below:

Business segments(S$’ 000) FY2007 FY2006 Change %Aluminium Alloy Division 36,784 25,400 11,384 44.8PE Pipe Division 2,677 4,870 (2,193) (45.0)Agency & Procurement Division 302 298 4 1.3Corporate Division (3,727) (2,088) (1,639) 78.5Unallocated interest expenses (1,973) (757) (1,216) 160.6Share of profi t of an associated company 1,256 - 1,256 NMTotal 35,319 27,723 7,596 27.4

NM – Not meaningful

Other operating income of approximately S$2.5 million comprised mainly interest income from deposits and a government grant amounting to S$1.5 million received by our Aluminium Alloy Division.

Selling and distribution expenses increased by approximately S$1.1 million, driven by the higher business volume recorded at our Aluminium Alloy Division.

Administrative expenses increased by about S$1.9 million in FY2007 mainly as a result of higher administrative expenses incurred at our Aluminium Alloy Division as a result of higher sales and expanded scope of business, increase in travelling expenses and share-based payment expenses of about S$1.6 million.

Finance costs increased by about S$1.2 million in FY2007 due to a higher level of borrowings by our Aluminium Alloy Division in FY2007 as compared to FY2006.

FY2007 marked the maiden contribution from our associated company, Nanjing SR Puzhen Rail Transport Co., Ltd, which started commercial operations in January 2007, contributed approximately S$1.26 million in FY2007.

The increase in income tax expense for FY2007 was due to higher profi ts. The income tax expense for FY2006 included a tax rebate of S$0.9 million granted to our subsidiary, Jilin Midas Aluminium Industries Co., Ltd.

FY2007 ended with net profi t attributable to shareholders of about S$31.9 million which represented a 24.8% increase over FY2006.

Annual Report 200716

Business Risk

Our revenue is mainly derived in the PRC from the sales of aluminium alloy extrusion products, PE Pipes as well as trading of aluminium alloy, PE pipes, metal materials and other related products. We intend to further our growth opportunities by marketing our products overseas to minimise any over reliance on the local PRC markets. During the previous fi nancial years, the Group has successfully exported its aluminium alloy extrusion profi les for the Singapore Circle Line Project and the Metro Oslo MRT Project in Norway. In FY2007, we have further secured three contracts to supply aluminium alloy profi les for the Valero Rus Project in Russia, the Desiro Mainline Project for the European and Ex-European markets and the Helsinki – St. Petersburg high speed train project.

The raw materials used in our manufacturing processes are plastic resins (for our PE Pipe Division) and aluminium alloy billets (for our Aluminium Alloy Division). Raw materials make up a signifi cant component of the cost of sales. We are therefore vulnerable to fl uctuations in the prices of these raw materials and components. We generally do not purchase or store raw materials in advance. Purchases of raw materials are generally made in response to customers’ order. Our Group makes use of this natural hedge to minimise any impact of fl uctuations in raw materials prices on our Group’s profi tability.

Interest Rate Risk

The Group’s cash balances are placed with reputable banks and fi nancial institutions. Financing is obtained through bank borrowings. Our Group’s policy is to obtain the most favourable rates available.

Liquidity Risk

The objective of liquidity management is to ensure that our Group has suffi cient funds to meet its contractual and fi nancial obligations. Management is of the view that there is no liquidity risk as our Group maintain adequate lines with fi nancial institutions and the cash fl ow from operations is suffi cient for present working capital requirements.

Foreign Currency Risk

Our revenue is denominated mainly in RMB while our purchases/expenses are mainly incurred in RMB. Our Group makes use of natural hedge in the above situation to minimise exposure to foreign currency movements.

However, our Company’s working capital is derived from dividend income from our subsidiaries. Hence, our Company would be exposed to foreign exchange risks when our Company receives dividends from our PRC subsidiaries.

Our Group currently does not have a formal hedging policy with respect to our foreign exchange exposure as we do not currently have a signifi cant foreign exchange currency exposure in our operations.

Credit Risk

Our Group performs ongoing credit evaluation of its customers’ fi nancial condition and generally does not require collateral. This evaluation includes assessing and valuation of customers’ credit reliability and periodic review of their fi nancial status to determine credit limits to be granted.

The maximum exposure to credit risk in the event that the customers fail to perform their obligations as at the end of the fi nancial year is the carrying amount stated in the balance sheet.

The Group’s trade receivables are mainly located in the PRC. There are no concentrations of credit risk with any customers or group of customers.

Risk Management

MIDAS HOLDINGS LIMITED 17

Corporate Governance Statement

Midas Holdings Limited (“the Company”) is committed to maintaining a high standard of corporate governance in complying with the benchmark set by the Code of Corporate Governance 2005 (“the Code”) issued by the Ministry of Finance on 14 July 2005.

The main corporate governance practices that were in place since are set out below.

A BOARD MATTERS

Board’s conduct of its affairs

The Board of Directors (“the Board”) supervises the management of the business and affairs of the Company and its subsidiaries (“the Group”). The Board approves the Group’s corporate and strategic direction, appointment of Directors and key managerial personnel, major funding and investment proposals, and reviews the fi nancial performance of the Group.

To assist in the execution of its responsibilities, the Board has established an Audit Committee (“AC”), a Remuneration Committee (“RC”) and a Nominating Committee (“NC”). Each of these committees has its own written terms of reference and whose actions are reported to and monitored by the Board. The Company has adopted internal guidelines setting forth matters that require Board approval.

The types of material transactions that require the Board’s approval under such guidelines included the following:

• Approval of quarterly results announcement; • Approval of the annual reports and accounts; • Declaration of interim dividends and proposal of fi nal dividends; • Convening of shareholders’ meetings; • Approval of broad policies, strategies and fi nancial objectives of the Group and

monitoring the performance of management; • Oversee the processes for evaluating the adequacy of internal controls, risk management,

fi nancial reporting and compliance; • Approval of nominations of Directors; • Approval of material acquisitions and disposals of assets; and • Authorisation of major transactions.

The Board comprises business leaders and professionals with fi nancial backgrounds. Profi les of our Directors are found on page 10 of this Report.

The Board conducts scheduled meetings on a regular basis. Ad hoc meetings will be convened to deliberate on urgent substantive matters when necessary. Telephonic attendance and conference via audio-visual communications at Board meetings are allowed under the Company’s Articles of Association. The attendance of the Directors at meetings of the Board and Board committees, as well as the frequency of such meetings, is disclosed in Part E of this Report.

The Directors are provided with important and relevant information of the Company and the Group. The Directors are also provided with the phone numbers and email addresses of the Company’s senior management and Company Secretary to facilitate access to information.

Newly appointed Directors are given an orientation on the Group’s business strategies and operations, including factory visits to ensure their familiarity with the Group’s operations and governance practices.

The Company Secretary and/or her representative attend(s) all Board meetings and, together

with the Directors, are responsible for ensuring that the Board procedures are followed and that applicable rules and regulations are complied with. The Company Secretary and/or her representative administer(s), attend(s) and prepare(s) minutes of all Board and Board committee meetings.

Directors are welcome to request further explanations, briefi ngs or informal discussions on any aspects of the Company’s operations or business issues from the management. The Chief Executive Offi cer (“CEO”) will make the necessary arrangements for the briefi ngs, informal discussions or explanations required by the Directors.

Annual Report 200718

Board composition and balance

The Board comprises two Executive Directors and three Independent Directors. Key information regarding the Directors can be found under the Board of Directors’ Profi le section in this annual report.

Name of Director

Board Committee as Chairman or member

Directorship:Date of fi rst appointment/Date of last re-election

Board appointment:Executive or non-executive/Independent

Due for re-election at next AGM

Chen Wei Ping NA 21 August 2002/27 April 2005

Executive Retirement pursuant to Article 91

Chew Hwa Kwang, Patrick

NA 17 November 2000/30 April 2007

Executive NA

Chew Chin Hua

Chairman of AC, Member of NC and RC

6 January 2004/28 April 2006

Independent Retirement pursuant to Article 91

Gay Chee Cheong

Chairman of NC, Member of AC and RC

23 June 2004/ 30 April 2007

Independent NA

Chan Soo Sen Chairman of RC, Member of AC and NC

29 June 2006 / 30 April 2007

Independent NA

The independence of each Independent Director is reviewed annually by the NC. The NC adopts the Code’s defi nition of what constitutes an Independent Director in its review, and the Company requires the Independent Directors to declare their independence annually. As a result of the review of the independence of each Director for the year, the NC is satisfi ed with the independence of all the Independent Directors.

Role of Chairman and CEO

The roles for both Chairman and CEO in the Company are separately assumed by Mr. Chen Wei Ping and Mr. Chew Hwa Kwang, Patrick. As such, there is a clear division of responsibilities at the top of the Group. Mr. Chen bears responsibility for the workings of the Board and ensures that the procedures are introduced to comply with the Code while Mr. Chew bears executive responsibility for the Group’s business.

Nominating Committee (“NC”)

The NC comprises 3 Independent Directors:

• Mr. Gay Chee Cheong, Chairman of the NC and Independent Director • Mr. Chew Chin Hua, Independent Director • Mr. Chan Soo Sen, Independent Director

The principal functions of the NC are to:

• Identify suitable candidates and review all nominations for the appointment to the Board of Directors before making recommendations to the Board for appointment.

• Assess the independence of the Directors annually and is of the opinion that the Directors who have been classifi ed as independent under the “Board of Directors” section are indeed independent.

• Decide whether or not a Director is able to and has been adequately carrying out his duties as a Director of the Company particularly where the Director has multiple board representations.

• Access the effectiveness of the Board. • To recommend Directors who are retiring by rotation to be put forward for re-election,

having regard to their contribution and performance.

The NC is of the view that the current Board comprises persons who as a group, provide core competencies necessary to meet the Company’s targets and that the current board size is adequate, taking into account the nature and scope of the Company’s operations.

Key information on the individual Directors of the Company is set out on page 10 of this Annual Report. Their shareholdings are also disclosed on page 22 in the Directors’ report. None of the Directors hold shares in the subsidiaries of the Company.

Board Performance

The NC will use its best efforts to ensure that Directors appointed to the Board possess the relevant background, experience and knowledge to enable balanced and well-considered decisions to be made. The performance criteria the NC will consider in relation to an individual Director include the Director’s industry knowledge and/or functional expertise, contribution and workload requirements, sense of independence and attendance at the Board and committee meetings. One of the NC’s responsibilities is to undertake a review of the Board’s performance. The NC will consider practicable methods to assess the effectiveness of the Board.

Corporate Governance Statement

MIDAS HOLDINGS LIMITED 19

B REMUNERATION MATTERS

Remuneration Committee (“RC”)

The RC comprises 3 Independent Directors:

1 Mr. Chan Soo Sen, Chairman of the RC and Independent Director 2. Mr. Gay Chee Cheong, Independent Director 3. Mr. Chew Chin Hua, Independent Director

The principal functions of the RC are to:

• Review and advise the Board on the remuneration packages of senior management employees of the Group.

• Review and approve annually the remuneration for the Directors. • Determine targets for any performance related pay schemes operated by the Company. • Administer the Midas Employees Share Option Scheme (“the Scheme”).

The members of the RC do not have specialized knowledge in the fi eld of executive compensation. However, they have gained experiences in this area via managing the business and/or the human resources matters of the Group and companies outside the Group. The Company will ensure that the RC has access to expert advice on the human resource matter whenever there is a need to consult externally. In setting remuneration packages, the Group takes into account pay and employment conditions within the same industry and in comparable companies, as well as the Group’s performance and individual performance. No Director or executive will be involved in deciding his own remuneration.

The remuneration packages for our Executive Chairman and CEO include a basic salary component, a profi t sharing component as well as share option elements, which are performance related. Both our Executive Chairman and CEO have entered into service agreements with the Group with effect from 1 January 2006 for a period of three years.

Independent Directors do not have service contracts with the Company. Independent Directors will receive directors’ fees, in accordance with their contributions, taking into factors such as effort and time spent, responsibilities of the Directors and the need to pay competitive fees to attract, retain and motivate the Directors. Director’s fees have been recommended by the Board for approval at the Company’s Annual General Meeting (“AGM”).

Disclosure on Remuneration

A breakdown of each individual Director’s remuneration, in percentage terms showing the level and mix for the year ended 31 December 2007, is as follows:

Fees%

Salary%

Other Benefi ts%

Total%

S$250,000 to S$499,999:Chen Wei Ping - 77 23 100

Chew Hwa Kwang, Patrick - 76 24 100

Below S$250,000:Chew Chin Hua 100 - - 100

Gay Chee Cheong 100 - - 100

Chan Soo Sen 100 - - 100

The remuneration of the top 5 key executives (who are not Directors) is not disclosed in this report. The Company believes that disclosure of the remuneration of individual executives is disadvantageous to its business interests, in view of the shortage of talented and experienced personnel in the industry.

There are no persons occupying managerial positions in the Company who are related to a Director or substantial shareholder of the Company or any of its principal subsidiaries who earned more than S$150,000 per annum for the fi nancial year ended 31 December 2007.

C ACCOUNTABILITY AND AUDIT

Audit Committee (“AC”)

The AC comprises 3 Independent Directors:

• Mr. Chew Chin Hua, Chairman of the AC and Independent Director • Mr. Gay Chee Cheong, Independent Director • Mr. Chan Soo Sen, Independent Director

Corporate Governance Statement

Annual Report 200720

The chairman of the AC, Mr. Chew Chin Hua, has many years of experience in the auditing and accounting profession. Mr. Chan Soo Sen and Mr. Gay Chee Cheong have many years of experience in business and fi nancial management. The AC members bring with them extensive managerial and fi nancial expertise. All of them are also board members of various listed companies in Singapore. The AC meets at least 4 times a year, with further meetings if circumstances require. The Board is of the view that the members of the AC have suffi cient fi nancial management expertise and experience to discharge the AC’s functions.

The AC assists the Board to maintain a high standard of corporate governance, particularly in

the areas of effective fi nancial reporting and the adequacy of internal control systems of the Group.

During the year, the AC reviewed and approved the audit plans submitted by both the internal and external auditors. The AC reviewed the fi ndings and recommendations from the auditors. The AC also reviewed and discussed the announcements of the quarterly, half year and full year results.

The AC evaluates the assistance given by management to the external auditors and also reviews any interested person transactions.

The AC has full access to management and is given the resources required for it to discharge its functions. It has the full authority and discretion to invite any Director or executive offi cer to attend its meetings.

The AC meets with the external auditors, without the presence of management, at least once a year.

The AC, having reviewed all non-audit services provided by the external auditors to the Group, is satisfi ed that the nature and extent of such services would not affect the independence of the external auditors. The AC recommends BDO Raffl es to the Board of Directors for re-appointment as external auditors of the Company.

Internal Control

The Board believes that, in the absence of any evidence to the contrary, the system of internal control maintained by the Group throughout the fi nancial year and up to the date of this report, provides reasonable, but not absolute, assurance against material fi nancial misstatements or loss, and include the safeguarding of assets, the maintenance of proper accounting records, the reliability of fi nancial information, compliance with appropriate legislation, regulation and best practice, and the identifi cation and containment of business risk. The Board notes that no system of internal control could provide absolute assurance against the occurrence of material errors, poor judgement in decision-making, human error, losses, fraud or other irregularities.

Internal Audit

The internal audit function is outsourced to a fi rm of certifi ed public accountants. The internal auditors report directly to the Chairman of the AC. The AC reviews and approves the annual internal audit plans and reviews the scope of internal audit procedures. The internal auditors report to the AC directly their signifi cant fi ndings and recommendations arising from the internal audit carried out.

D COMMUNICATIONS WITH SHAREHOLDERS

The Group is mindful of the obligation to provide regular, effective and fair communication with shareholders on a timely basis. The Group does not practice selective disclosure. The Company holds analysts briefi ng after announcing its half-year and full-year results. The announcements of results are published through the SGXNET and news releases. All information on the Company’s and/or the Group’s new initiatives are fi rst disseminated via SGXNET followed by a news release. Results and annual reports are announced or issued within the mandatory period.

All shareholders of the Company receive the annual report, circulars and notices of the shareholders’ meetings. The notices are also advertised in newspapers. The Company encouraged shareholders to attend the AGM to ensure a high level of accountability and to stay informed of the Company’s and/or the Group’s strategies and goals. The notice of this AGM has been dispatched to the shareholders, at least 14 working days before the meeting. The Board welcomes questions from shareholders either formally or informally before or at the AGM.

The Company’s Articles of Association allow a shareholder of the Company to appoint one or two proxies to attend and vote instead of the shareholder.

Corporate Governance Statement

MIDAS HOLDINGS LIMITED 21

E OTHERS

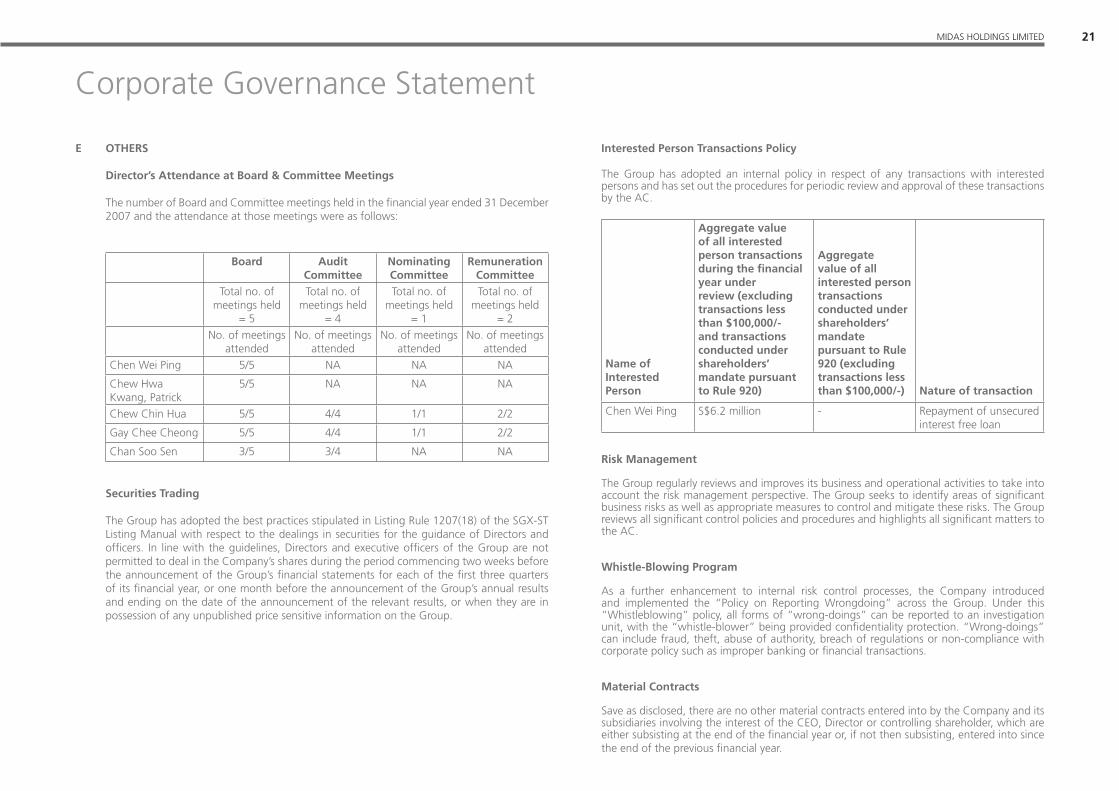

Director’s Attendance at Board & Committee Meetings

The number of Board and Committee meetings held in the fi nancial year ended 31 December 2007 and the attendance at those meetings were as follows:

Board Audit Committee

Nominating Committee

Remuneration Committee

Total no. of meetings held

= 5

Total no. of meetings held

= 4

Total no. of meetings held

= 1

Total no. of meetings held

= 2No. of meetings

attendedNo. of meetings

attendedNo. of meetings

attendedNo. of meetings

attendedChen Wei Ping 5/5 NA NA NA

Chew Hwa Kwang, Patrick

5/5 NA NA NA

Chew Chin Hua 5/5 4/4 1/1 2/2

Gay Chee Cheong 5/5 4/4 1/1 2/2

Chan Soo Sen 3/5 3/4 NA NA

Securities Trading

The Group has adopted the best practices stipulated in Listing Rule 1207(18) of the SGX-ST Listing Manual with respect to the dealings in securities for the guidance of Directors and offi cers. In line with the guidelines, Directors and executive offi cers of the Group are not permitted to deal in the Company’s shares during the period commencing two weeks before the announcement of the Group’s fi nancial statements for each of the fi rst three quarters of its fi nancial year, or one month before the announcement of the Group’s annual results and ending on the date of the announcement of the relevant results, or when they are in possession of any unpublished price sensitive information on the Group.

Interested Person Transactions Policy

The Group has adopted an internal policy in respect of any transactions with interested persons and has set out the procedures for periodic review and approval of these transactions by the AC.

Name of Interested Person

Aggregate value of all interested person transactions during the fi nancial year under review (excluding transactions less than $100,000/- and transactions conducted under shareholders’ mandate pursuant to Rule 920)

Aggregate value of all interested person transactions conducted under shareholders’ mandate pursuant to Rule 920 (excluding transactions less than $100,000/-) Nature of transaction

Chen Wei Ping S$6.2 million - Repayment of unsecured interest free loan

Risk Management

The Group regularly reviews and improves its business and operational activities to take into account the risk management perspective. The Group seeks to identify areas of signifi cant business risks as well as appropriate measures to control and mitigate these risks. The Group reviews all signifi cant control policies and procedures and highlights all signifi cant matters to the AC.

Whistle-Blowing Program

As a further enhancement to internal risk control processes, the Company introduced and implemented the “Policy on Reporting Wrongdoing” across the Group. Under this “Whistleblowing” policy, all forms of “wrong-doings” can be reported to an investigation unit, with the “whistle-blower” being provided confi dentiality protection. “Wrong-doings” can include fraud, theft, abuse of authority, breach of regulations or non-compliance with corporate policy such as improper banking or fi nancial transactions.

Material Contracts

Save as disclosed, there are no other material contracts entered into by the Company and its subsidiaries involving the interest of the CEO, Director or controlling shareholder, which are either subsisting at the end of the fi nancial year or, if not then subsisting, entered into since the end of the previous fi nancial year.

Corporate Governance Statement

Annual Report 200722

Directors’ Report

The Directors are pleased to present their report to the members together with the audited consolidated fi nancial statements of the Group and the balance sheet and statement of changes in equity of the Company for the fi nancial year ended 31 December 2007.

1. Directors

The Directors of the Company in offi ce at the date of this report are:

Mr. Chen Wei Ping Mr. Chew Hwa Kwang, Patrick Mr. Chew Chin Hua Mr. Gay Chee Cheong Mr. Chan Soo Sen

2. Arrangements to enable Directors to acquire shares and debentures

Neither at the end of nor at any time during the fi nancial year was the Company a party to any arrangement whose object is to enable the Directors of the Company to acquire benefi ts by means of the acquisition of shares in or debentures of the Company or any other body corporate, other than as disclosed under “Share Options” of this report.

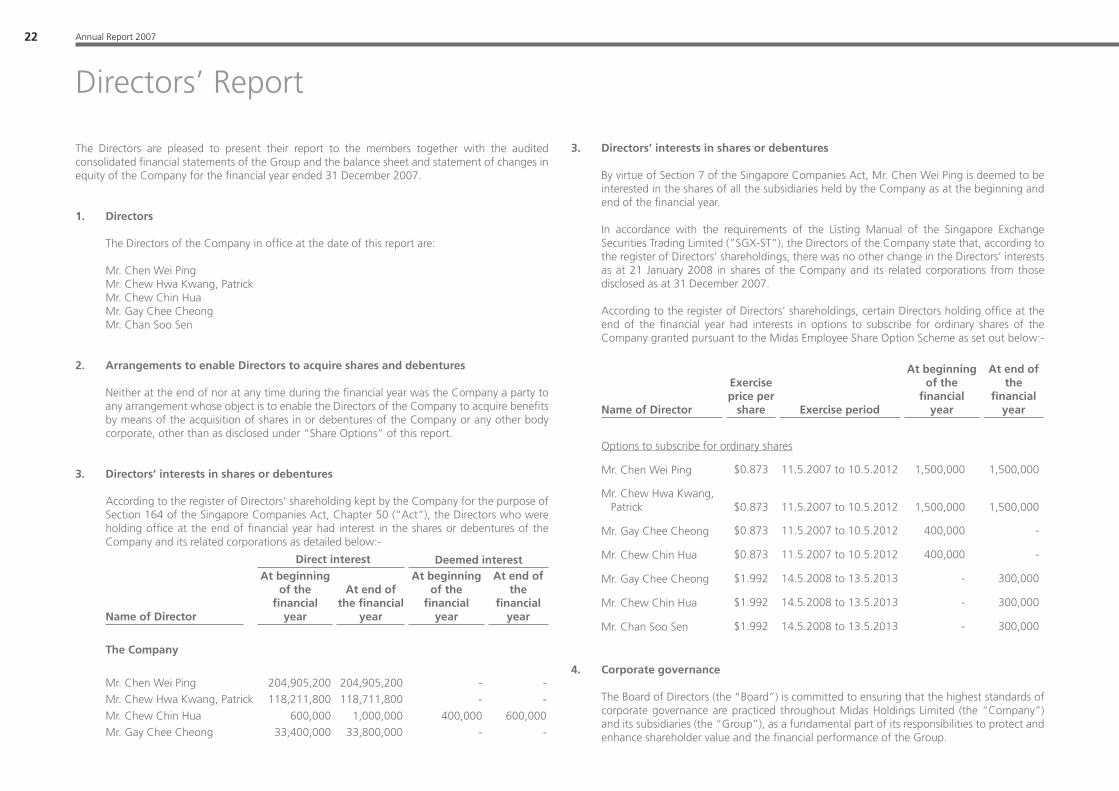

3. Directors’ interests in shares or debentures

According to the register of Directors’ shareholding kept by the Company for the purpose of Section 164 of the Singapore Companies Act, Chapter 50 (“Act”), the Directors who were holding offi ce at the end of fi nancial year had interest in the shares or debentures of the Company and its related corporations as detailed below:-

Direct interest Deemed interest

Name of Director

At beginning of the

fi nancial year

At end of the fi nancial

year

At beginning of the

fi nancialyear

At end of the

fi nancial year

The Company

Mr. Chen Wei Ping 204,905,200 204,905,200 - -Mr. Chew Hwa Kwang, Patrick 118,211,800 118,711,800 - -

Mr. Chew Chin Hua 600,000 1,000,000 400,000 600,000Mr. Gay Chee Cheong 33,400,000 33,800,000 - -

3. Directors’ interests in shares or debentures

By virtue of Section 7 of the Singapore Companies Act, Mr. Chen Wei Ping is deemed to be interested in the shares of all the subsidiaries held by the Company as at the beginning and end of the fi nancial year.

In accordance with the requirements of the Listing Manual of the Singapore Exchange

Securities Trading Limited (”SGX-ST”), the Directors of the Company state that, according to the register of Directors’ shareholdings, there was no other change in the Directors’ interests as at 21 January 2008 in shares of the Company and its related corporations from those disclosed as at 31 December 2007.

According to the register of Directors’ shareholdings, certain Directors holding offi ce at the end of the fi nancial year had interests in options to subscribe for ordinary shares of the Company granted pursuant to the Midas Employee Share Option Scheme as set out below:-

Name of Director

Exercise price per

share Exercise period

At beginning of the

fi nancialyear

At end of the

fi nancial year

Options to subscribe for ordinary shares

Mr. Chen Wei Ping $0.873 11.5.2007 to 10.5.2012 1,500,000 1,500,000

Mr. Chew Hwa Kwang, Patrick $0.873 11.5.2007 to 10.5.2012 1,500,000 1,500,000

Mr. Gay Chee Cheong $0.873 11.5.2007 to 10.5.2012 400,000 -

Mr. Chew Chin Hua $0.873 11.5.2007 to 10.5.2012 400,000 -

Mr. Gay Chee Cheong $1.992 14.5.2008 to 13.5.2013 - 300,000

Mr. Chew Chin Hua $1.992 14.5.2008 to 13.5.2013 - 300,000

Mr. Chan Soo Sen $1.992 14.5.2008 to 13.5.2013 - 300,000

4. Corporate governance

The Board of Directors (the “Board”) is committed to ensuring that the highest standards of corporate governance are practiced throughout Midas Holdings Limited (the “Company”) and its subsidiaries (the “Group”), as a fundamental part of its responsibilities to protect and enhance shareholder value and the fi nancial performance of the Group.

MIDAS HOLDINGS LIMITED 23

Directors’ Report

5. Directors’ contractual benefi ts

Since the beginning of the fi nancial year, no Director of the Company has received or become entitled to receive a benefi t by reason of a contract made by the Company or a related corporation with the Director or with a fi rm of which he is a member or with a company in which he has a substantial fi nancial interest, except as disclosed in the accompanying fi nancial statements.

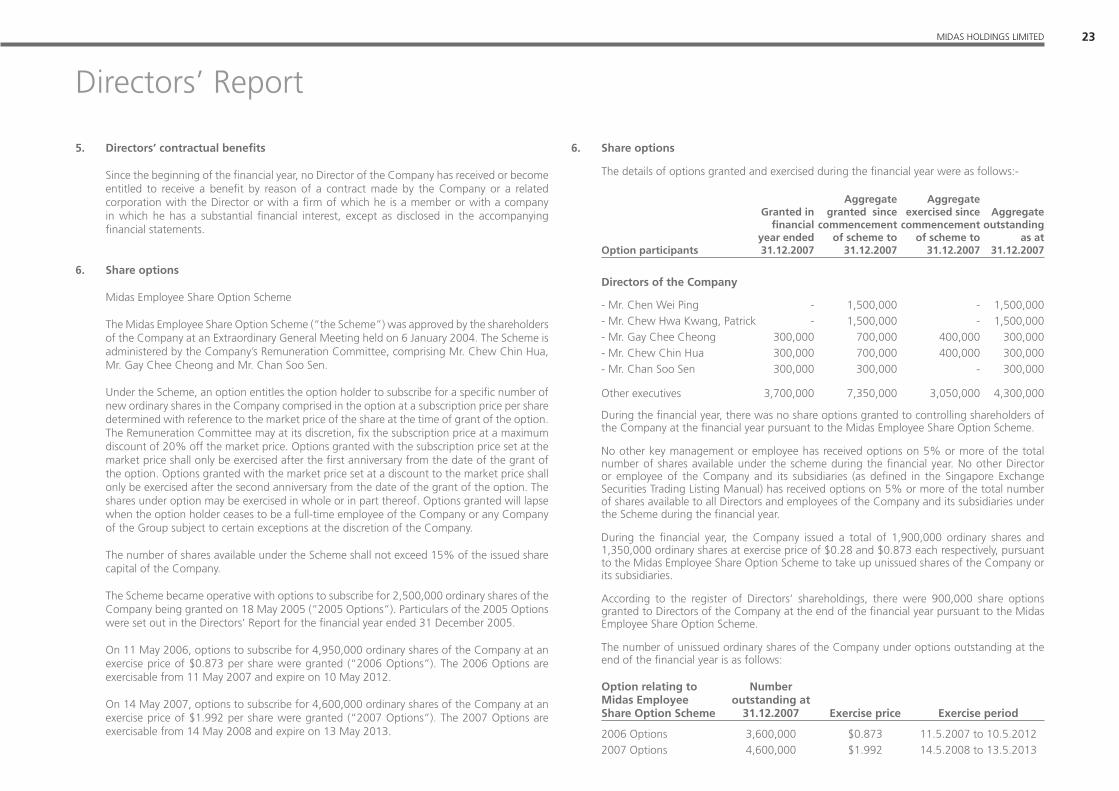

6. Share options

Midas Employee Share Option Scheme

The Midas Employee Share Option Scheme (“the Scheme”) was approved by the shareholders of the Company at an Extraordinary General Meeting held on 6 January 2004. The Scheme is administered by the Company’s Remuneration Committee, comprising Mr. Chew Chin Hua, Mr. Gay Chee Cheong and Mr. Chan Soo Sen.

Under the Scheme, an option entitles the option holder to subscribe for a specifi c number of new ordinary shares in the Company comprised in the option at a subscription price per share determined with reference to the market price of the share at the time of grant of the option. The Remuneration Committee may at its discretion, fi x the subscription price at a maximum discount of 20% off the market price. Options granted with the subscription price set at the market price shall only be exercised after the fi rst anniversary from the date of the grant of the option. Options granted with the market price set at a discount to the market price shall only be exercised after the second anniversary from the date of the grant of the option. The shares under option may be exercised in whole or in part thereof. Options granted will lapse when the option holder ceases to be a full-time employee of the Company or any Company of the Group subject to certain exceptions at the discretion of the Company.

The number of shares available under the Scheme shall not exceed 15% of the issued share capital of the Company.

The Scheme became operative with options to subscribe for 2,500,000 ordinary shares of the Company being granted on 18 May 2005 (“2005 Options”). Particulars of the 2005 Options were set out in the Directors’ Report for the fi nancial year ended 31 December 2005.

On 11 May 2006, options to subscribe for 4,950,000 ordinary shares of the Company at an exercise price of $0.873 per share were granted (“2006 Options”). The 2006 Options are exercisable from 11 May 2007 and expire on 10 May 2012.

On 14 May 2007, options to subscribe for 4,600,000 ordinary shares of the Company at an exercise price of $1.992 per share were granted (“2007 Options”). The 2007 Options are exercisable from 14 May 2008 and expire on 13 May 2013.

6. Share options

The details of options granted and exercised during the fi nancial year were as follows:-

Option participants

Granted in fi nancial

year ended 31.12.2007

Aggregate granted since

commencement of scheme to

31.12.2007

Aggregate exercised since

commencement of scheme to

31.12.2007

Aggregate outstanding

as at 31.12.2007

Directors of the Company

- Mr. Chen Wei Ping - 1,500,000 - 1,500,000- Mr. Chew Hwa Kwang, Patrick - 1,500,000 - 1,500,000- Mr. Gay Chee Cheong 300,000 700,000 400,000 300,000- Mr. Chew Chin Hua 300,000 700,000 400,000 300,000- Mr. Chan Soo Sen 300,000 300,000 - 300,000

Other executives 3,700,000 7,350,000 3,050,000 4,300,000

During the fi nancial year, there was no share options granted to controlling shareholders of the Company at the fi nancial year pursuant to the Midas Employee Share Option Scheme.

No other key management or employee has received options on 5% or more of the total number of shares available under the scheme during the fi nancial year. No other Director or employee of the Company and its subsidiaries (as defi ned in the Singapore Exchange Securities Trading Listing Manual) has received options on 5% or more of the total number of shares available to all Directors and employees of the Company and its subsidiaries under the Scheme during the fi nancial year.

During the fi nancial year, the Company issued a total of 1,900,000 ordinary shares and 1,350,000 ordinary shares at exercise price of $0.28 and $0.873 each respectively, pursuant to the Midas Employee Share Option Scheme to take up unissued shares of the Company or its subsidiaries.

According to the register of Directors’ shareholdings, there were 900,000 share options granted to Directors of the Company at the end of the fi nancial year pursuant to the Midas Employee Share Option Scheme.

The number of unissued ordinary shares of the Company under options outstanding at the end of the fi nancial year is as follows:

Option relating to Midas Employee Share Option Scheme

Number outstanding at

31.12.2007 Exercise price Exercise period

2006 Options 3,600,000 $0.873 11.5.2007 to 10.5.20122007 Options 4,600,000 $1.992 14.5.2008 to 13.5.2013

Annual Report 200724

Directors’ Report

7. Audit committee

The members of the Audit Committee during the fi nancial year and the date of this report are:

Mr. Chew Chin Hua (Chairman) - Independent Director

Mr. Gay Chee Cheong - Independent Director

Mr. Chan Soo Sen - Independent Director

The Audit Committee performs the functions specifi ed in Section 201B of the Singapore Companies Act.

The Audit Committee has held four meetings since the last Directors’ report. In performing its functions, the Audit Committee met with the Company’s external and internal auditors to discuss the scope of their work, the results of their examination and evaluation of the Company’s internal accounting control system.

The Audit Committee also reviewed the following:

• the Group’s fi nancial and operating results and accounting policies;

• the quarterly, half-yearly and annual results announcements as well as the related press releases on the results and fi nancial position of the Company and the Group;

• the co-operation and assistance given by the management to the Group’s internal and external auditors;

The Audit Committee has recommended to the Board that the auditors, BDO Raffl es, be nominated for re-appointment at the forthcoming Annual General Meeting of the Company.

8. Auditors

The auditors, BDO Raffl es, have expressed their willingness to accept re-appointment.

On behalf of the Board of Directors

MR. CHEN WEI PING MR. CHEW HWA KWANG, PATRICKDirector Director

Singapore

20 March 2008

MIDAS HOLDINGS LIMITED 25

Statement by the Directors

In our opinion:

(a) the accompanying consolidated fi nancial statements of the Group and the balance sheet and statement of changes in equity of the Company are properly drawn up in accordance with the provisions of the Act, Cap. 50 and Singapore Financial Reporting Standards so as to give a true and fair view of the state of affairs of the Group and of the Company as at 31 December 2007 and of the results, changes in equity and cash fl ow of the Group and the changes in equity of the Company for the fi nancial year ended on that date; and

(b) at the date of this statement, there are reasonable grounds to believe that the Company will be able to pay its debts as and when they fall due.

On behalf of the Board of Directors

MR. CHEN WEI PING MR. CHEW HWA KWANG, PATRICKDirector Director

Singapore

20 March 2008

Annual Report 200726

Opinion

In our opinion,

(a) the consolidated fi nancial statements of the Group and the balance sheet and statement of changes in equity of the Company are properly drawn up in accordance with the provisions of the Act and Singapore Financial Reporting Standards so as to give a true and fair view of the state of affairs of the Company and of the Group as at 31 December 2007 and of the results, changes in equity and cash fl ows of the Group and the changes in equity of the Company for the fi nancial year ended on that date.

(b) the accounting and other records required by the Act to be kept by the Company and those subsidiary companies incorporated in Singapore of which we are the auditors, have been properly kept in accordance with the provisions of the Act.

BDO Raffl es Public Accountants andCertifi ed Public Accountants Singapore

20 March 2008

We have audited the accompanying consolidated fi nancial statements of Midas Holdings Limited (“the Company”) and its subsidiaries (collectively the “Group”), which comprise the balance sheets of the Group and of the Company as at 31 December 2007, profi t and loss account, statement of changes in equity and statement of cash fl ow of the Group and the statement of changes in equity of the Company for the fi nancial year then ended, and a summary of signifi cant accounting policies and other explanatory notes as set out on pages 32 to 57.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these fi nancial statements in accordance with the provisions of the Singapore Companies Act, Cap. 50 (the “Act”) and Singapore Financial Reporting Standards. This responsibility includes: