middle market report - madison capital funding€¦ · [email protected] m | pitchbook.com bet t er...

TRANSCRIPT

S T RONG S TAR T F OR U.S . MIDDL E M ARKE T IN 20 15 F UNDR AISING CON T INUE S AT FA S T CL IP

Average time on fundraising trail keeps fallingPAGE 15»

MIDDLEMARKETREPORT

2Q 2015

U.S.

S P O N S O R E D B Y

Exits slow in 1Qfollowing 2014 sell-offPAGE 12»

C O - S P O N S O R E D B Y

Announcing a merger between confidence and value

M & A is one of the quickest paths to growth. But it’s not always the surest. That’s why at PwC, we help you understand the risks in your transactions, so you can be confident that you are making informed strategic decisions. From your deal negotiations, to capturing synergies during integration, we help clients gain value. And ultimately, deliver this value to stakeholders. Like we’ve done for countless stakeholders of middle-market companies, private equity funds and families. Leverage the experience of our global network of firms. Learn how at pwc.com/us/deals

© 2015 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

MW-15-1858-Middle-Market Pitchbook Ad.indd 1 3/16/2015 6:55:02 PM

®

CONTENTSIntroduction

Middle Market Overview

Deals by Region

Deals by Industry

Middle Market Breakdown

Exit Activity

Fundraising Activity

League Tables

4

5-6

8

9

10-11

12-13

14-15

16

CREDITS & CONTACT

PitchBook Data, Inc.

JOHN GABBERT Founder, CEO

ADLEY BOWDEN Senior Director, Analysis

Content, Design, Editing & Data

ALEX LYKKEN Editor

ANDY WHITE Lead Data Analyst

DANIEL COOK Senior Data Analyst

GARRETT BLACK Senior Financial Writer

BRIAN LEE Data Analyst

JENNIFER SAM Senior Graphic Designer

JESS CHAIDEZ Graphic Designer

Contact PitchBook

www.pitchbook.com

RESEARCH

EDITORIAL

SALES

COPYRIGHT © 2015 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means—graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems—without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.

“PwC has a deep presence in the middle market and knows first hand its importance in today’s economy. We are uniquely positioned to serve private businesses and their owners by drawing upon the breadth and depth of knowledge, experience, and skills of professionals from our global network of member firms.”

- John Poth, PwC Partner, Private Company Services

PwC helps you achieve your growth initiatives from deal strategy through value capture. PwC’s Deals professionals support clients on a wide range of transactions including domestic and cross-border acquisitions, divestitures, business restructuring and spin-offs, capital events such as IPOs and debt offerings.

As part of the PwC’s Deals practice, PricewaterhouseCoopers Corporate Finance LLC and its professionals specialize in providing M&A related investment banking advisory services. PwC CF specializes in advising domestic and international clients on divestitures and acquisitions across the globe.

3 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

®

IntroductionComing off a record year in 2014, private equity (PE) activity in the U.S. middle market remains

strong in the early innings of 2015. Final first quarter numbers have been tabulated and both capital invested and deal counts kept pace with quarterly totals seen last year, which added up to $359.7 billion across 1,791 deals. Total value was up 21% last year compared to 2013, while counts were up 24%.

Valuations outside the middle market, particularly at the highest end, have pushed more PE investors downstream. Last year, 72% of all PE buyouts occurred in the middle market, the highest ratio on record and a testament to investor enthusiasm. That percentage has already increased in 2015, to 78% through the the first quarter. That ratio will likely come down a bit as the year drags on, but it’s clearly not an aberration. It will likely stay relatively high over the next few years, if fundraising totals are any indicator; the $140 billion raised in 2014 was the most raised for middle-market funds since the recession. The momentum continued into 2015, with another 32 middle-market funds closing through 1Q totaling $33.1 billion. Dry powder won’t be drying up any time soon, in other words.

As we’ll detail further on pages 9 and 10, investor appetite for the upper middle market (UMM) is growing. Both in absolute terms and relative to the core and lower middle markets (CMM, LMM), activity in the $500 million to $1 billion range has strengthened. That’s due in large part to the amount of cheap and available credit in the current market. Also at play, however, is a push by PE firms to cut larger checks for UMM companies when they hit the market. While it’s

true that smaller targets are more plentiful and oftentimes command smaller multiples, PE firms would still rather put their money to work in a few relatively large transactions, rather than several smaller deals. It’s not surprising to see that corner of the middle market seeing more activity today, at least while interest rates remain low. If and when debt becomes

more expensive, we may see some changes in middle-market figures. Until then, the data shows a vibrant U.S. middle market that hasn’t yet slowed.

We hope the data and commentary in this report prove helpful and informative in your decision-making process in the coming quarters. If you have any questions, comments or suggestions, please reach out to us at [email protected].

Middle-market activity hasn’t shown any signs of slowing in 2015. Another big

year in the works?

Madison Capital’s focus is to provide superior financing solutions to a wide range of private equity sponsors. Our products and services support the acquisition, recapitalization and growth investment efforts of private equity firms focused on middle market companies.

Our reputation is built on key relationships and effective communication.

We build relationships by concentrating on the needs of our clients and delivering outstanding services.

4 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

®

Middle Market Overview

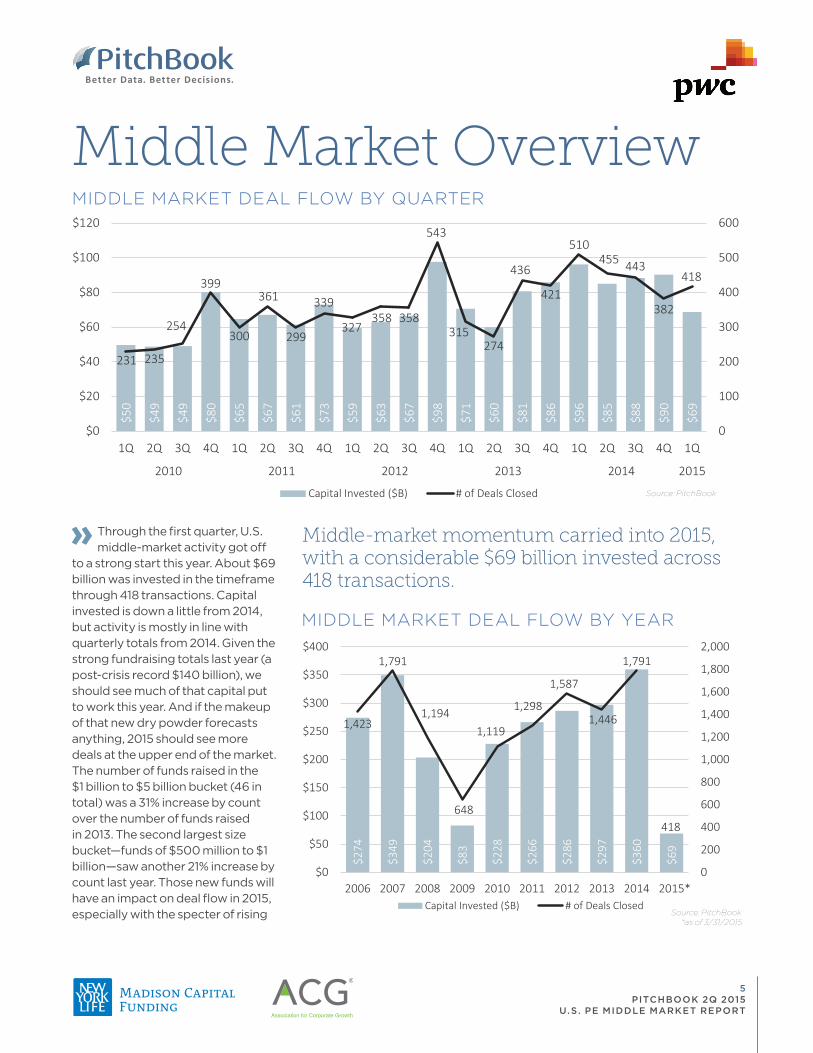

Through the first quarter, U.S. middle-market activity got off

to a strong start this year. About $69 billion was invested in the timeframe through 418 transactions. Capital invested is down a little from 2014, but activity is mostly in line with quarterly totals from 2014. Given the strong fundraising totals last year (a post-crisis record $140 billion), we should see much of that capital put to work this year. And if the makeup of that new dry powder forecasts anything, 2015 should see more deals at the upper end of the market. The number of funds raised in the $1 billion to $5 billion bucket (46 in total) was a 31% increase by count over the number of funds raised in 2013. The second largest size bucket—funds of $500 million to $1 billion—saw another 21% increase by count last year. Those new funds will have an impact on deal flow in 2015, especially with the specter of rising

MIDDLE MARKET DEAL FLOW BY QUARTER

Source: PitchBook

MIDDLE MARKET DEAL FLOW BY YEAR

Source: PitchBook

Middle-market momentum carried into 2015, with a considerable $69 billion invested across 418 transactions.

$50

$49

$49

$80

$65

$67

$61

$73

$59

$63

$67

$98

$71

$60

$81

$86

$96

$85

$88

$90

$69

231 235

254

399

300

361

299

339

327358 358

543

315274

436

421

510455 443

382

418

0

100

200

300

400

500

600

$0

$20

$40

$60

$80

$100

$120

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2010 2011 2012 2013 2014 2015

Capital Invested ($B) # of Deals Closed

$274

$349

$204

$83

$228

$266

$286

$297

$360

$69

1,423

1,791

1,194

648

1,119

1,298

1,587

1,446

1,791

418

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

$0

$50

$100

$150

$200

$250

$300

$350

$400

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*Capital Invested ($B) # of Deals Closed

*as of 3/31/2015

5 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

2015* DEALS BY SECTOR AND SEGMENT

Source: PitchBook

interest rates on the horizon. Generally speaking, the U.S. PE

industry has been selling more than it’s been buying in recent quarters. While that is evident in the exit totals, the historic trend for first quarters shows sharp declines following heavy fourth quarter sell-offs. That appears to be the case again in 2015, with

The ratio of PE deals being done in the middle market keeps hitting record highs.

just $16 billion of PE capital exited through the end of 1Q through 205 liquidity events. All four quarters of 2014 hovered around the $25 billion level, a substantially higher sum. The differentiating factor this year is that, amidst the buoyant seller’s market of 2014, many of the best portfolio companies held by PE firms were sold off while demand and multiples were high. Should interest rates rise later this year, we may see a drop-off in secondary buyouts (SBOs), since sponsor-to-sponsor deals are highly impacted by financing costs. Should SBOs decline, that may have

a cooling effect on the deal-making side, as well, as PE firms will have to set their sights on deal origination outside of the PE market.

As the graph below shows, though, the middle market has become a

haven for PE firms, anyway. Almost four of five buyouts completed in 2015 have been for middle-market companies, another record percentage.

Source & filter

investment opportunities

Monitor peer activity &

industry trends

Identify the right LPs for

your next fund

Benchmark your fund

performance

Run public & private

comparables

Augment portfolio

executive teams

PitchBook for Private Equity [email protected] m | pitchbook.com

Bet ter Data. Bet ter Decisions.PitchBook

No one offers more insight on the private equity landscape than

What will you do with it?PITCHBOOK FOR PE FIRMS

27%

18%

33%

20%

9%

33%

7%

18%

17%

13%

9%

17%

7%

14%

13%

18%

13%

14%

0% 20% 40% 60% 80% 100%

LMM

CMM

UMM

Business Products and Services (B2B) Consumer Products and Services (B2C)Energy Financial ServicesHealthcare Information TechnologyMaterials and Resources

MIDDLE MARKET AS % OF ALL BUYOUTS

65.5%68.0%

62.7%

58.5%

65.7%66.8%

68.5% 68.9%

72.2%

78.3%

55%

60%

65%

70%

75%

80%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

*as of 3/31/2015

Source: PitchBook*as of 3/31/2015

®

Deals by Region

MIDDLE MARKET DEALS (#) BY REGION

Source: PitchBook

Source: PitchBook

So far this year, there appears to be no sizable shift in regional

deal flow from the numbers seen last year, apart from the increase in middle-market dealmaking on the West Coast. It’s worth noting that the South, which enjoyed a resurgence in activity over the past few years, may continue to attract substantial PE interest, especially given its capital invested numbers. Part of this is due to industry consolidation across the relatively fragmented healthcare sector and strong interest in energy currently. The South and Southeast have collected the most capital invested in 2015 to date—a hefty $16.8 billion and $27.7 billion, respectively.

The map corresponds to the graph below, which shows relative middle-market deal flow between eight U.S. regions.

LEGEND

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

West Coast

Southeast

South

Great Lakes

New England

Mountain

Midwest

Mid-Atlantic

*as of 3/31/2015

8 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

®

Deals by Industry

MIDDLE MARKET DEAL FLOW ($) BY INDUSTRY

MIDDLE MARKET DEAL FLOW (#) BY INDUSTRY

Another strong year expected for B2B, which is coming off its biggest year in decades.

Source: PitchBook

Source: PitchBook

One of the bigger PE storylines last year was the boom in B2B

investment. Driven by improving fundamentals in the U.S. economy, B2B benefited from stronger growth expectations across the board. PE firms seized the opportunity last year and, based on the data seen in 2015 to date, continue to do so, particularly in the middle market, where purchase price multiples are not quite as high as elsewhere.

Healthcare saw a surge not only in deal count last year but also in value, reaching $59.2 billion in total capital invested. Factors driving that growth have been well documented: Widespread fragmentation among care providers, an increase in niche opportunities, anticipated growth in retirees and a substantial uptick in the number of insured Americans. A slowdown is unlikely, especially in the middle market, because the same growth drivers active last year are still very much in place.

Unsurprisingly, PE interest in the energy sector is off to a strong start. $10.8 billion worth of deals has already closed in 2015, which represents 36% of total 2014 value ($29.9 billion) with another three quarters to go. Given the amount of dry powder available for energy investments, not to mention the new funds popping up left and right, PE will likely be one of the most active investors in the industry this year and likely for the next few years. It wouldn’t be unexpected if 2015 breaks the all-time record of capital invested, currently held by 2013 ($47.2 billion).

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

B2B B2C EnergyFinancial Services Healthcare IT

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

B2B B2C EnergyFinancial Services Healthcare IT

*as of 3/31/2015

*as of 3/31/2015

9 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

®

Middle Market Breakdown% OF MIDDLE MARKET DEALS (#) BY SEGMENT

% OF MIDDLE MARKET INVESTMENT ($) BY SEGMENT

Source: PitchBook

Source: PitchBook

All segments of the middle market saw considerable

activity in 2014, with the bulk occurring in the core—$100 million to $500 million. The front half of 2014 saw capital invested outpacing even the heights of 2007. The UMM also saw gradual (if slight) growth in its proportion of deals, with the totals in 2015 thus far adding to that increase. Meanwhile, the LMM bounced back from a relatively quiet 4Q 2014 to post healthy numbers in early 2015.

These trends are in line with some predictions for the industry made at the beginning of the year: With plenty of dry powder to burn but facing high valuations, PE firms would continue or even increase activity in the middle market, much as they did in 2014. Some concluded the UMM would not see much investment, as higher purchase multiples could depress activity there, but that doesn’t appear to be the case—at least so far. Cheap and abundant credit played, and continues to play, a significant role in UMM activity.

However, the upswing in activity in the LMM in 2015 to date also could portend what the rest of the year has in store. If higher valuations are maintained or spread across the board even further, PE firms may well have no other recourse than to pay up or sit on the sidelines or continue to move downstream in search of lower price tags.

2015: The Year of the Upper Middle Market? $500M-$1B activity off to a strong start.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*LMM CMM UMM

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

LMM CMM UMM*as of 3/31/2015

*as of 3/31/2015

10 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

®

Company Name

1Q ‘15 Deal Month

Size ($M) Industry

Deal Type

North American Breaker

Jan. $87 B2B SBO

Cimarron Jan. $80 Energy SBO

ChemAid Jan. $70 B2C Add-on

Chaparral Gold Feb. $59 Materials P2P

Manna ProProducts

Jan. $41 Materials LBO

Company Name

1Q ‘15 Deal Month

Size ($M) Industry Deal Type

EmployBridge Feb. $410 B2B Add-on

Axia Energy March $200 Energy LBO

Nomacorc Jan. $200 B2B LBO

ChyronHego March $120 B2B P2P

Meridian Healthcare Group

Feb. $100 Healthcare Add-on

Company Name

1Q ‘15 Deal Month

Size ($M) Industry Deal Type

PODS Feb. $1,000 B2C SBO

Neovia Logistics

March $1,000 B2B SBO

Digital River Feb. $840 B2B P2P

Moda Midstream

March $750 Energy LBO

Cassidy Turley

Jan. $600 B2C Add-on

UPPER MIDDLE MARKE T SELEC T DEAL S

CORE MIDDLE MARKE T SELEC T DEAL S

LOWER MIDDLE MARKE T SELEC T DEAL S

UMM DEAL FLOW

CMM DEAL FLOW

LMM DEAL FLOW

Source: PitchBook

Source: PitchBook

Source: PitchBookSource: PitchBook

Source: PitchBook

Source: PitchBook

$13

$24

$36

$48

$38

$20

$35

$37

$36

$35

$42

$40

$28

22

38

65

100

63

29

6067

53

6268

61 58

0

20

40

60

80

100

120

$0

$10

$20

$30

$40

$50

$60

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2012 2013 2014 2015

Capital Invested ($B) # of Deals Closed

$10

$9 $6 $7 $7 $5 $8 $5 $8 $6 $6 $3 $5

169 182

149

189

121

93

174

139

182

156

164

92

146

0

20

40

60

80

100

120

140

160

180

200

$0

$2

$4

$6

$8

$10

$12

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2012 2013 2014 2015

Capital Invested ($B) # of Deals Closed

$36

$30

$24

$42

$26

$35

$38

$44

$52

$44

$39

$47

$36

136 139 144

255

131

152

201216

276

237

211

229

214

0

50

100

150

200

250

300

$0

$10

$20

$30

$40

$50

$60

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2012 2013 2014 2015

Capital Invested ($B) # of Deals Closed

11 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

®

Exit ActivityMIDDLE MARKET EXITS BY QUARTER

Source: PitchBook

From 1Q 2013 to the end of 2014, PE sellers enjoyed a

nearly uninterrupted quarter-on-quarter increase in exit counts, capping off 2014 with an impressive 235 in 4Q. Capital exited totals nearly rose in tandem: Last year saw a combined $100.6 billion exited through corporate acquisitions, IPOs and secondary buyouts alone, easily dwarfing any other tally in middle-market sales of the decade.

These elevated figures were the result of several positive trends, some of which were still in place heading into 2015. PE firms seized the opportunity presented by bull markets worldwide last year and took many portfolio companies public, and low interest rates helped buoy SBO activity to a decade high.

Maintaining that momentum

Source: PitchBook

MIDDLE MARKET EXITS BY YEAR

Exits are off to a slower start in 2015, possibly due to the massive sell-off last year.

$14

$18

$18

$32

$11

$16

$16

$26

$24

$26

$25

$26

$16

186 188

161

243

129

163 171

227

187 193

221235

205

0

50

100

150

200

250

300

$0

$5

$10

$15

$20

$25

$30

$35

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2012 2013 2014 2015

Capital Exited ($B) # of Exits

*as of 3/31/2015

$61

$76

$38

$21

$64

$69

$81

$69

$101

$16

509586

379

223

532

601

778

690

836

205

0

100

200

300

400

500

600

700

800

900

$0

$20

$40

$60

$80

$100

$120

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Capital Exited ($B) # of Exits

12 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

®

MIDDLE MARKET EXITS ($) BY TYPE

MIDDLE MARKET EXITS (#) BY SIZE

Source: PitchBook

Source: PitchBook

If interest rates rise later this year, SBO activity may take a hit, since PE buyers are so sensitive to financing costs.

will be difficult in 2015. The public markets have become more volatile as discussions of an interest rate rise heat up. If and when interest rates increase, the cost of borrowing will head north, which should have an impact on price-sensitive SBO activity. At the same time, if higher interest rates have a downward effect on the stock markets, we may also see a marked decrease in PE-sponsored IPOs this year, at least until the markets stabilize.

Outside of SBOs and IPOs, however, it’s less likely that strategic sales will slow significantly. Interest rate levels have had relatively little correlation with the overall M&A market. Aiming for synergy capture, strategics have stretched their bids for target companies, including many PE portfolio companies, in order to grow market share in a low-growth environment. Strategics did so in large numbers last year, acquiring $53.6 billion worth of PE middle-market holdings, an all-time high and a 56% increase over 2013 levels. Given that the fundamentals in the M&A market haven’t changed, we should see another strong year for corporate acquisitions, which should help prop up overall exit numbers.

That said, the kind of seller’s market that we witnessed in 2012-2014 doesn’t come too around often, and it may have played out somewhat. As many have pointed out, PE firms by and large have been selling off their best portfolio companies while investor demand is high and multiples are buoyant.

$0

$20

$40

$60

$80

$100

$120

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Corporate Acquisition IPO Secondary Buyout

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

$25M-$100M $100M-$500M $500M-$1B

*as of 3/31/2015

*as of 3/31/2015

13 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

®

Fundraising Activity

Source: PitchBook

Source: PitchBook

PE firms have closed 32 funds thus far in 2015 on a

combined $33 billion in capital commitments. The tally puts the year on a slightly slower pace than last; similar counts haven’t been seen since 2Q and 3Q of 2012. The slowdown was foreshadowed somewhat, as fund counts slid a little in the back half of 2014. Unpacking the fundraises by size buckets, we see roughly similar proportions to years past, with a little over 28% of all funds raised to date in 2015 in the $1 billion to $5 billion range, while the smallest size bucket—$100 million to $250 million—boasts the largest single share of fund count, over 34%. That 34%, and the fact the number of $1 billion+ funds is on pace to decline, may indicate what we’ve been hearing from GPs: Plenty of competition on the fundraising trail, even with allocations to PE increasing.

MIDDLE MARKET FUNDRAISING BY QUARTER

MIDDLE MARKET FUNDRAISING BY YEAR

LP commitments continue to flood into middle-market funds, which bodes well for future deal activity.

$18

$17

$17

$16

$33

$30

$24

$19

$32

$30

$25

$20

$26

$38

$26

$30

$42

$37

$28

$32

$33

33 27

18

29

36 34

29

38 41

32 31 36

44 44 42 46

50

43 40 41

32

0

10

20

30

40

50

60

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q

2010 2011 2012 2013 2014 2015

Capital Raised ($B) # of Funds Closed

$126

$145

$143

$83

$68

$106

$108

$120

$140

$33

181

218196

110 107

137140

176 174

32

0

50

100

150

200

250

$0

$20

$40

$60

$80

$100

$120

$140

$160

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*Capital Raised ($B) # of Funds Closed

*as of 3/31/2015

14 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

®

MIDDLE MARKET FUNDS (#) BY FUND SIZE

MIDDLE MARKET BUYOUT FUNDS AVERAGE TIME TO CLOSE (IN MONTHS)

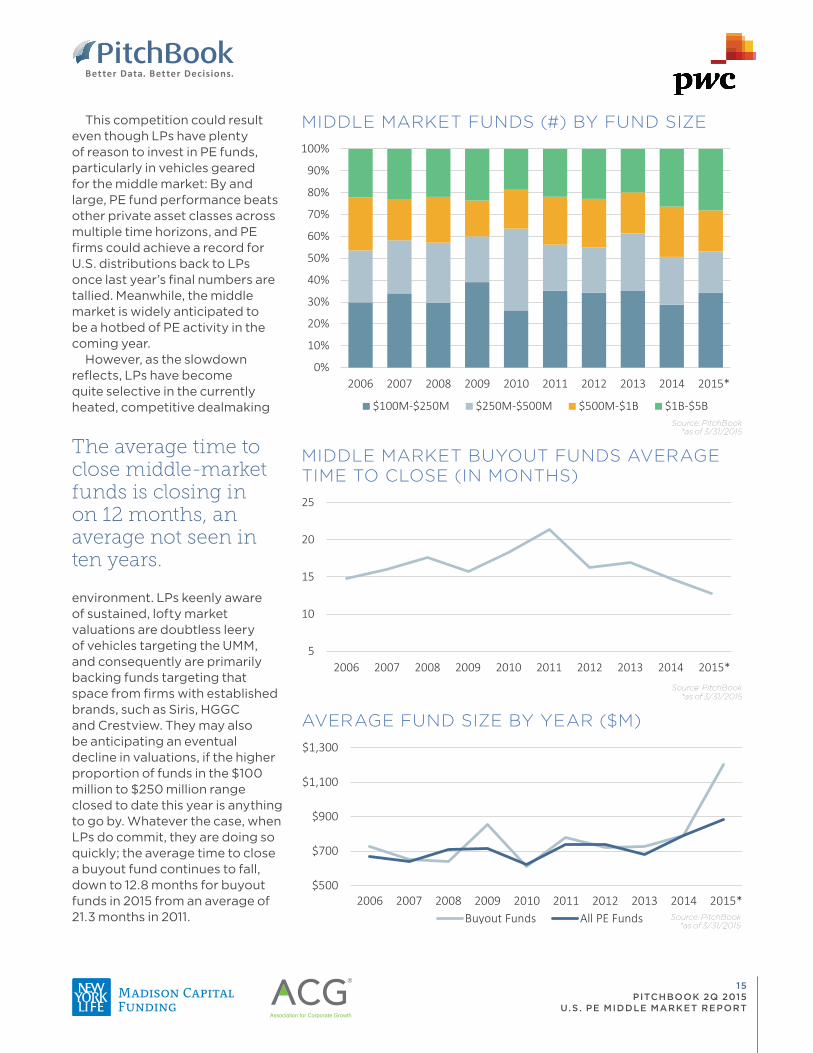

This competition could result even though LPs have plenty of reason to invest in PE funds, particularly in vehicles geared for the middle market: By and large, PE fund performance beats other private asset classes across multiple time horizons, and PE firms could achieve a record for U.S. distributions back to LPs once last year’s final numbers are tallied. Meanwhile, the middle market is widely anticipated to be a hotbed of PE activity in the coming year.

However, as the slowdown reflects, LPs have become quite selective in the currently heated, competitive dealmaking

Source: PitchBook

Source: PitchBook

The average time to close middle-market funds is closing in on 12 months, an average not seen in ten years.

environment. LPs keenly aware of sustained, lofty market valuations are doubtless leery of vehicles targeting the UMM, and consequently are primarily backing funds targeting that space from firms with established brands, such as Siris, HGGC and Crestview. They may also be anticipating an eventual decline in valuations, if the higher proportion of funds in the $100 million to $250 million range closed to date this year is anything to go by. Whatever the case, when LPs do commit, they are doing so quickly; the average time to close a buyout fund continues to fall, down to 12.8 months for buyout funds in 2015 from an average of 21.3 months in 2011.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

$100M-$250M $250M-$500M $500M-$1B $1B-$5B

AVERAGE FUND SIZE BY YEAR ($M)

5

10

15

20

25

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

$500

$700

$900

$1,100

$1,300

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*Buyout Funds All PE Funds

Source: PitchBook

*as of 3/31/2015

*as of 3/31/2015

*as of 3/31/2015

15 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

®

MOST ACTIVE INVESTORS MOST ACTIVE LAW FIRMS

MOST ACTIVE ADVISORS

Source: PitchBook Source: PitchBook

Source: PitchBook

The Carlyle Group 14

Hellman & Friedman 12

ABRY Partners 10

GTCR Golder Rauner 8

Audax Group 6

Vista Equity Partners 6

Goldman Sachs 5

Marlin Equity Partners 5

The Blackstone Group 5

The Riverside Company 5

TPG Capital 5

Wasserstein 5

First Capital Partners 4

Genstar Capital 4

Insight Venture Partners 4

Kohlberg Kravis Roberts 4

Ontario Teachers’ Pension Plan 4

TSG Consumer Partners 4

Welsh, Carson, Anderson & Stowe 4

Wind Point Partners 4

Firm Deals

Kirkland & Ellis 22

Jones Day 20

Ropes & Gray 12

Morgan, Lewis & Bockius 8

Debevoise & Plimpton 7

Weil, Gotshal & Manges 7

Willkie Farr & Gallagher 7

Hogan Lovells 6

Shearman & Sterling 6

Morrison & Foerster 6

Paul, Weiss, Rifkind, Wharton & Garrison 5

Goodwin Procter 5

Skadden, Arps, Slate, Meagher & Flom 5

Proskauer 4

Winston & Strawn 4

Latham & Watkins 4

Vinson & Elkins 4

DLA Piper 4

Foley & Lardner 4

Wilson Sonsini Goodrich & Rosati 4

Houlihan Lokey 8

William Blair & Company 7

Lincoln International 6

Harris Williams & Co. 5

KPMG 5

Deloitte 5

Morgan Stanley 5

Piper Jaffray 4

Macquarie Capital 4

Moelis & Company 4

Duff & Phelps 4

Goldman Sachs 4

Raymond James & Associates 4

Robert W. Baird & Co. 4

Firm Deals

Firm Deals

MOST ACTIVE LENDERS

Source: PitchBook

GE Capital 16

BMO Harris Bank 7

Golub Capital 6

Wells Fargo 4

Bank of Ireland 4

TCF Capital Funding 3

Regions Financial 3

PNC Financial Services Group 3

Babson Capital Management 3

Firm Deals

1Q 2015 Middle Market League Tables

16 PITCHBOOK 2Q 2015

U.S . PE MIDDLE MARKET REPORT

YOU WOULDN’T DRESS FOR TODAY BASED ON L AST MONTH’S WEATHER

SO WHY VALUE YOUR INVESTMENTS BASED ON L AST YEAR’S MARKET ?

Get a better understanding of today’s valuation

landscape with the PitchBook Platform

Get started now

TODAY ’S

Valuation forecast TOMORROW NEXT WEEK