milk and milk products november 2015 · 2015-12-22 · milk and milk products: price and trade...

TRANSCRIPT

Milk and milk products: price and trade update December 2015

Weekly Newsletter

Milk and Milk Products

Price and Trade Update: December 20151

INTERNATIONAL PRICES: Weak import demand causes prices to fall

After rising in September and October, limited buying interest resulted in international dairy

prices falling in November, a sign that major importers had accumulated adequate stocks for

their immediate needs. Quotations for butter and milk powders dropped, while those for cheese

were steady. Milk production in Oceania is anticipated to be lower for the current dairy year,

while output in the European Union is expected to be similar to last year.

The FAO Dairy Price Index averaged 151.1 points in November 2015, down 4.6 points (2.9

percent) from October. Compared with November 2014, quotations for all dairy products

covered in the Index were lower: falling by 21.1 percent to USD 1949 per tonne for skimmed

milk powder (SMP); by 18.2 percent to USD 3150 per tonne for cheddar cheese; by 10.3 percent

to USD 2420 per tonne for whole milk powder (WMP); and by 6.8 percent to USD 2978 per

tonne for butter.

1 The Milk and Milk Products: Price and Trade Update is prepared by the meat and dairy section of the Trade and Markets Division,

FAO. The present issue covers developments up to the end of November 2015.

Milk and Milk Products Price and Trade Update

December 2015

Milk and milk products: price and trade update December 2015

Trade Outlook: Overview

First decline in more than a decade

Trade in dairy products is forecast to fall by 1.2 percent in 2015 to 71.8 million tonnes of milk

equivalent, which would represent the first drop since 2001.

Although the majority of importing countries are expected to raise their level of importation in

2015, including Malaysia, the United States, the United Arab Emirates, Mexico, Venezuela,

Brazil, Egypt, Oman and Japan, a sharp downturn in China’s purchases, especially of WMP,

may cause total dairy trade to fall. Imports by the Russian Federation and, to a lesser extent,

Saudi Arabia and the EU, are also forecast to decline. Purchases by the Russian Federation are

predicted to fall markedly for the second year in a row, reflecting devaluation of the rouble,

along with the continuation of the ban imposed by the country in August 2014 on trade with

Australia, Canada, the EU, Norway and the United States, which has particularly affected

cheese.

Among exporters, high domestic prices in the United States and India, relative to those

prevailing in the world market, are anticipated to truncate external sales from these countries,

especially of skimmed milk powder. Deliveries by Argentina and New Zealand are also

expected to fall, following a contraction in output that was partly triggered by low world prices.

50

100

150

200

250

300

350

400

2008 2009 2010 2011 2012 2013 2014 2015

2002-2004=100

FAO Dairy Export Price Indices: 2008 - 2015

WMP

SMP

Cheese

Dairy Index

Butter

Milk and milk products: price and trade update December 2015

To a limited extent, a decline in exports by the above countries and elsewhere will be

counterbalanced by increased sales by Belarus, Australia and the EU.

0

2000

4000

6000

8000

10000

12000

14000

* Milk Equivalent, '000 tonnes

Milk and Milk Products Imports *

2013

2014

2015 f'cast

0

5000

10000

15000

20000

25000

New Zealand EU United States Belarus Australia Argentina

* Milk Equivalent, '000 tonnes

Milk and Milk Products Exports *

2013

2014

2015 f'cast

Milk and milk products: price and trade update December 2015

Whole milk powder (WMP)

Trade falls

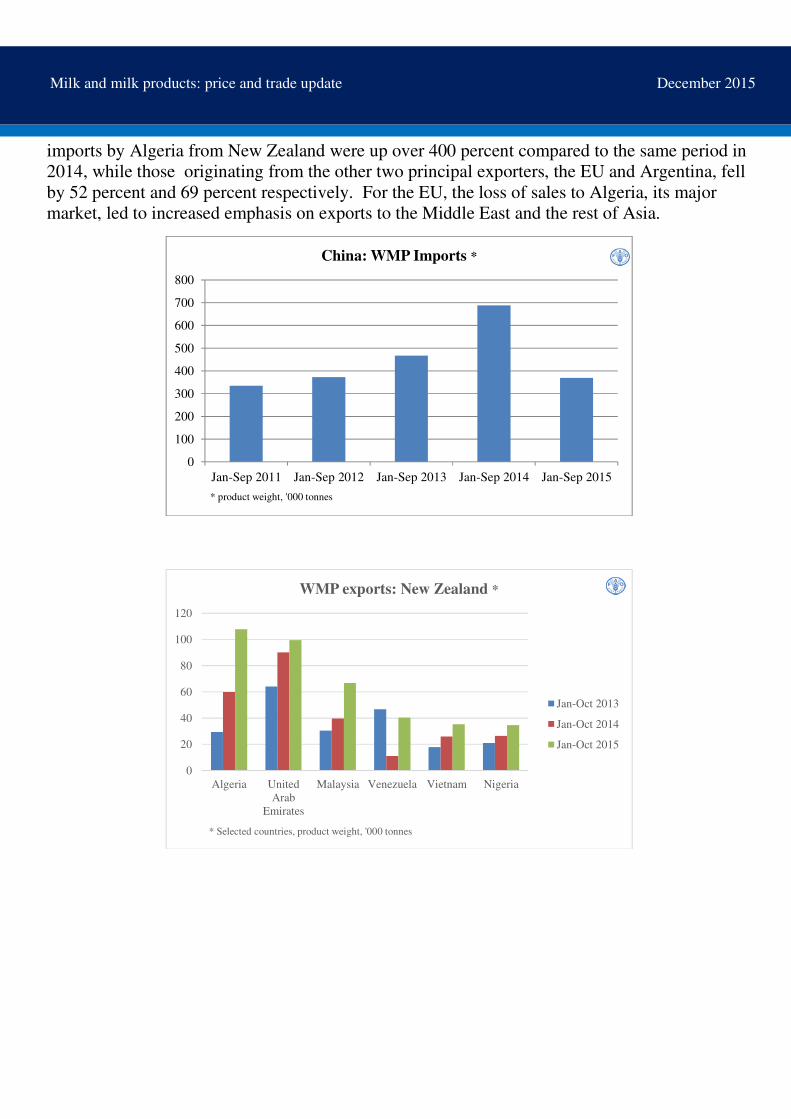

World trade in WMP is projected to drop by 4.1 percent to 2.5 million tonnes in 2015, the first

decline since 2007. Slashed purchases by China, which accounted for nearly 40 percent of

world imports in 2014, has been the primary factor influencing the market this year. China’s

year-to-August WMP imports were 48 percent down from 2014, stemming from reduced

demand and processors utilizing previously imported stock. The sudden, sharp fall mainly

affected trade with New Zealand. WMP prices remained weak during 2015, well below their

peak reached at the start of 2014. For example, in November 2015, prices averaged USD 2 420

per tonne, 53.1 per cent below their level in January 2014. Low international prices have

stimulated imports in several major markets, including Venezuela, Algeria, Brazil, the United

Arab Emirates, Vietnam, Oman, Malaysia and Indonesia.

The decline in world import demand for WMP in 2015 is anticipated to impact negatively

exports by all the principal exporters, namely New Zealand, Argentina, the EU and Australia,

with some smaller scale exporters, such as Chile and the United States also affected. New

Zealand, as the largest international supplier of WMP with a 55 percent world market share,

furnishing over 80 percent of China’s WMP imports in 2014, has had to make the most

adjustment. Despite seeing January-September deliveries to China drop by almost 60 percent

year-on year, New Zealand’s exports of WMP only fell by 4 percent overall during the same

period. This was achieved by substantially increasing sales to a wide geographical range of

countries, including Algeria, Venezuela, Malaysia, Vietnam, the United Arab Emirates and

Nigeria. In some cases, such as Algeria and Nigeria, this substituted for shipments by other

exporters that traditionally supply these markets. For example, during the first half of 2015,

IMPORTS: TOTAL MILK

thousand tonnes (Milk Equivalent)

2013 2014 2015

Change

2015

over

2014 (%) prelim. f'cast

World 65063 69130 68022 -1.6

China 12388 13228 10317 -22.0

Mexico 2913 2866 3172 10.7

Algeria 2231 3115 3152 1.2

Russian Fed. 4918 3912 2892 -26.1

Saudi Arabia 2269 3024 2805 -7.2

Indonesia 2644 2536 2598 2.4

Malaysia 1803 2087 2470 18.3

UAE 1734 2077 2406 15.9

EXPORTS: TOTAL MILK

thousand tonnes (Milk Equivalent)

2013 2014 2015

Change

2015

over

2014 (%) prelim. f'cast

World 68546 72651 71769 -1.2

New Zealand 17831 19136 18946 -1.0

EU 15735 17726 18041 1.8

United States 10434 10653 9377 -12.0

Belarus 4388 4370 4958 13.4

Australia 3365 3514 3855 9.7

Argentina 2546 2144 1907 -11.1

Milk and milk products: price and trade update December 2015

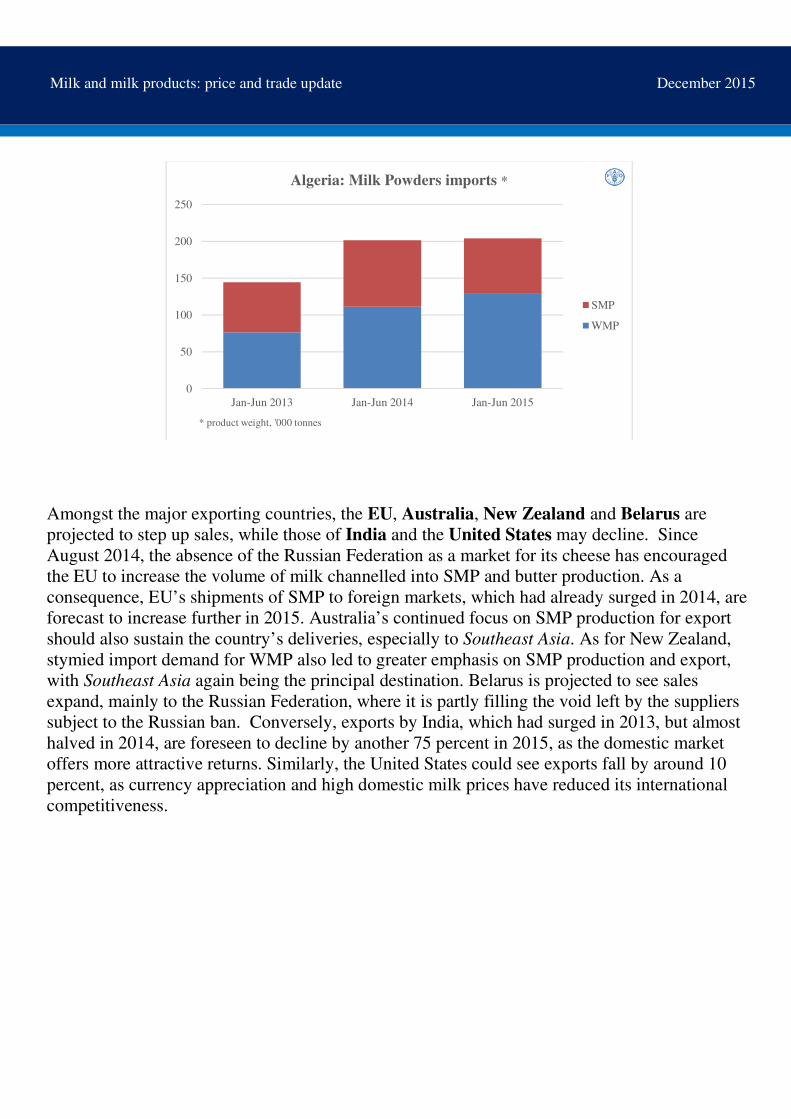

imports by Algeria from New Zealand were up over 400 percent compared to the same period in

2014, while those originating from the other two principal exporters, the EU and Argentina, fell

by 52 percent and 69 percent respectively. For the EU, the loss of sales to Algeria, its major

market, led to increased emphasis on exports to the Middle East and the rest of Asia.

0

100

200

300

400

500

600

700

800

Jan-Sep 2011 Jan-Sep 2012 Jan-Sep 2013 Jan-Sep 2014 Jan-Sep 2015

* product weight, '000 tonnes

China: WMP Imports *

0

20

40

60

80

100

120

Algeria United

Arab

Emirates

Malaysia Venezuela Vietnam Nigeria

* Selected countries, product weight, '000 tonnes

WMP exports: New Zealand *

Jan-Oct 2013

Jan-Oct 2014

Jan-Oct 2015

Milk and milk products: price and trade update December 2015

IMPORTS: WMP

‘000 tonnes (product weight)

2013 2014 2015

Change

2015

over

2014 (%) prelim. f'cast

World 2266 2418 2298 -5.0

China 725 785 462 -41.2

Algeria 142 204 231 12.9

Venezuela 170 143 179 25.0

UAE 101 132 155 17.7

Oman 74 72 90 25.5

Vietnam 39 62 81 30.0

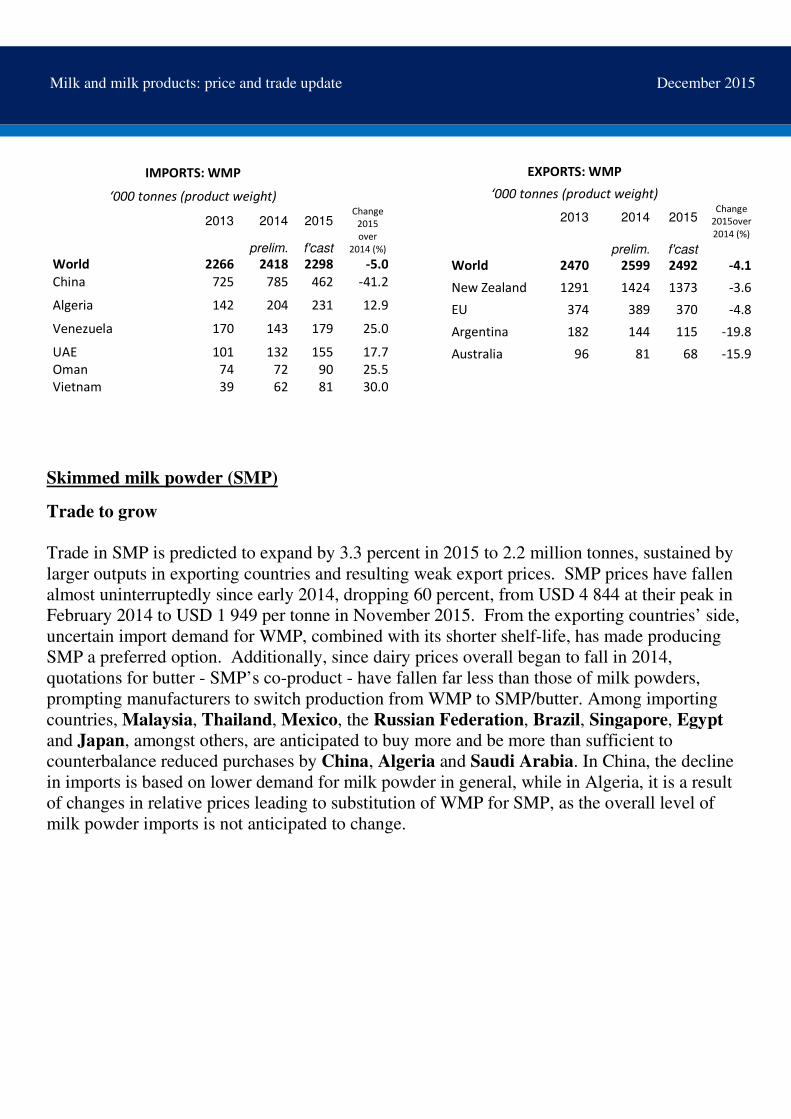

Skimmed milk powder (SMP)

Trade to grow

Trade in SMP is predicted to expand by 3.3 percent in 2015 to 2.2 million tonnes, sustained by

larger outputs in exporting countries and resulting weak export prices. SMP prices have fallen

almost uninterruptedly since early 2014, dropping 60 percent, from USD 4 844 at their peak in

February 2014 to USD 1 949 per tonne in November 2015. From the exporting countries’ side,

uncertain import demand for WMP, combined with its shorter shelf-life, has made producing

SMP a preferred option. Additionally, since dairy prices overall began to fall in 2014,

quotations for butter - SMP’s co-product - have fallen far less than those of milk powders,

prompting manufacturers to switch production from WMP to SMP/butter. Among importing

countries, Malaysia, Thailand, Mexico, the Russian Federation, Brazil, Singapore, Egypt

and Japan, amongst others, are anticipated to buy more and be more than sufficient to

counterbalance reduced purchases by China, Algeria and Saudi Arabia. In China, the decline

in imports is based on lower demand for milk powder in general, while in Algeria, it is a result

of changes in relative prices leading to substitution of WMP for SMP, as the overall level of

milk powder imports is not anticipated to change.

EXPORTS: WMP

‘000 tonnes (product weight)

2013 2014 2015

Change

2015over

2014 (%)

prelim. f'cast

World 2470 2599 2492 -4.1

New Zealand 1291 1424 1373 -3.6

EU 374 389 370 -4.8

Argentina 182 144 115 -19.8

Australia 96 81 68 -15.9

Milk and milk products: price and trade update December 2015

Amongst the major exporting countries, the EU, Australia, New Zealand and Belarus are

projected to step up sales, while those of India and the United States may decline. Since

August 2014, the absence of the Russian Federation as a market for its cheese has encouraged

the EU to increase the volume of milk channelled into SMP and butter production. As a

consequence, EU’s shipments of SMP to foreign markets, which had already surged in 2014, are

forecast to increase further in 2015. Australia’s continued focus on SMP production for export

should also sustain the country’s deliveries, especially to Southeast Asia. As for New Zealand,

stymied import demand for WMP also led to greater emphasis on SMP production and export,

with Southeast Asia again being the principal destination. Belarus is projected to see sales

expand, mainly to the Russian Federation, where it is partly filling the void left by the suppliers

subject to the Russian ban. Conversely, exports by India, which had surged in 2013, but almost

halved in 2014, are foreseen to decline by another 75 percent in 2015, as the domestic market

offers more attractive returns. Similarly, the United States could see exports fall by around 10

percent, as currency appreciation and high domestic milk prices have reduced its international

competitiveness.

0

50

100

150

200

250

Jan-Jun 2013 Jan-Jun 2014 Jan-Jun 2015

* product weight, '000 tonnes

Algeria: Milk Powders imports *

SMP

WMP

Milk and milk products: price and trade update December 2015

0

20

40

60

80

100

120

* product weight, '000 tonnes

EU: SMP exports *

Jan-Sep 2013

Jan-Sep 2014

Jan-Sep 2015

0

20

40

60

80

100

120

China Singapore Philippines Malaysia Indonesia Thailand

* product weight, '000 tonnes

New Zealand: SMP exports *

Jan-Oct 2014

Jan-Oct 2015

Milk and milk products: price and trade update December 2015

IMPORTS: SMP

‘000 tonnes (product weight)

2013 2014 2015 Change

2015

over

2014 (%) prelim. f'cast

World 1932 2070 2147 3.7

China 266 286 240 -16.2

Mexico 198 203 221 9.0

Malaysia 102 138 175 27.2

Algeria 120 168 148 -11.8

Indonesia 155 146 141 -3.6

Russian Fed. 131 95 109 15.0

EXPORTS: SMP

‘000 tonnes (product weight)

2013 2014 2015

Change

2015

over

2014 (%)

prelim. f'cast

World 1897 2129 2200 3.3

EU 407 646 698 8.0

United States 555 554 510 -8.0

New Zealand 392 383 420 9.7

Australia 119 164 213 30.2

Belarus 95 90 112 25.0

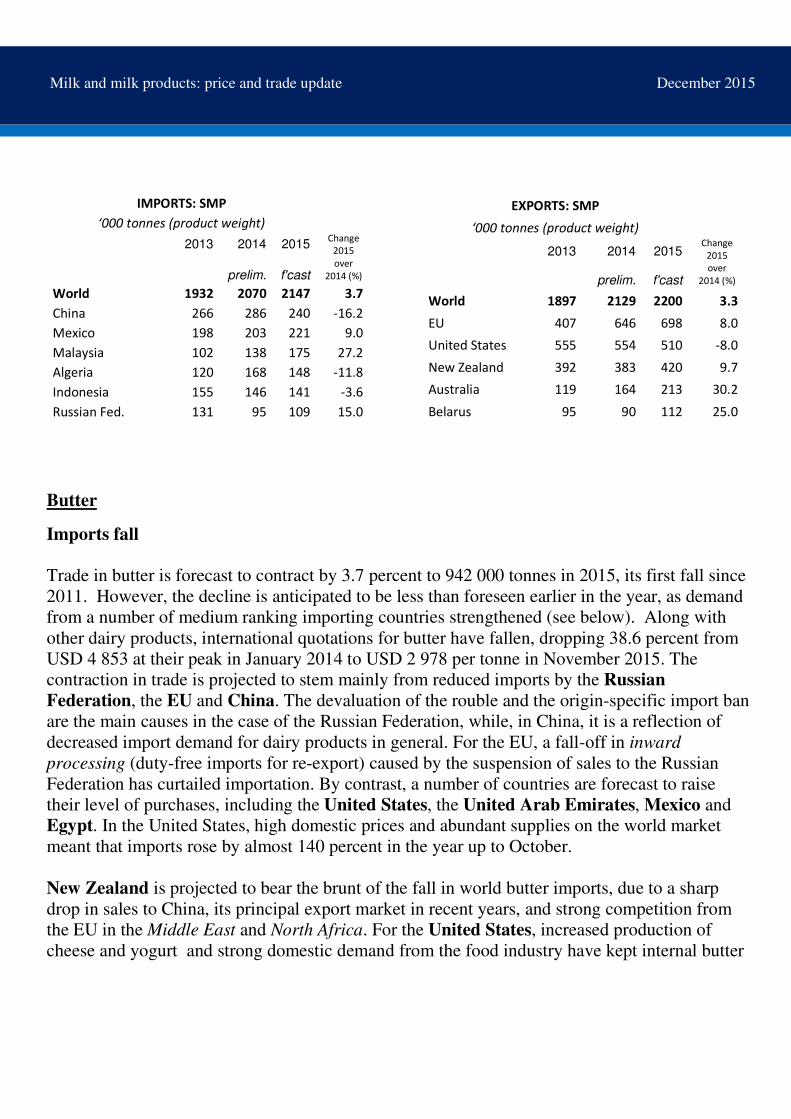

Butter

Imports fall

Trade in butter is forecast to contract by 3.7 percent to 942 000 tonnes in 2015, its first fall since

2011. However, the decline is anticipated to be less than foreseen earlier in the year, as demand

from a number of medium ranking importing countries strengthened (see below). Along with

other dairy products, international quotations for butter have fallen, dropping 38.6 percent from

USD 4 853 at their peak in January 2014 to USD 2 978 per tonne in November 2015. The

contraction in trade is projected to stem mainly from reduced imports by the Russian

Federation, the EU and China. The devaluation of the rouble and the origin-specific import ban

are the main causes in the case of the Russian Federation, while, in China, it is a reflection of

decreased import demand for dairy products in general. For the EU, a fall-off in inward

processing (duty-free imports for re-export) caused by the suspension of sales to the Russian

Federation has curtailed importation. By contrast, a number of countries are forecast to raise

their level of purchases, including the United States, the United Arab Emirates, Mexico and

Egypt. In the United States, high domestic prices and abundant supplies on the world market

meant that imports rose by almost 140 percent in the year up to October.

New Zealand is projected to bear the brunt of the fall in world butter imports, due to a sharp

drop in sales to China, its principal export market in recent years, and strong competition from

the EU in the Middle East and North Africa. For the United States, increased production of

cheese and yogurt and strong domestic demand from the food industry have kept internal butter

Milk and milk products: price and trade update December 2015

prices high, which is likely to depress US exports for the second year in a row: sales from

January to October were two-thirds lower than in the same period in 2014. Meanwhile, as the

devaluation of the Euro against several currencies has improved its competitiveness, EU exports

are expected to grow beyond last year’s substantial level. Elsewhere, Belarus and Uruguay may

gain from reduced competition in the Russian Federation’s market.

0

20

40

60

80

100

120

140

160

180

2011 2012 2013 2014 2015 f'cast

* Selected countries, product weight, '000 tonnes

Butter Imports *

Russian Fed.

China

Egypt

Mexico

United States

UAE

EU

0

10

20

30

40

50

60

70

80

* product weight, '000 tonnes

New Zealand: Butter exports *

Jan-Oct 2014

Jan-Oct 2015

Milk and milk products: price and trade update December 2015

IMPORTS: BUTTER

‘000 tonnes (product weight)

2013 2014 2015

Change

2015

over

2014 (%) prelim. f'cast

World 861 944 890 -5.8

Russian Fed. 160 150 90 -40.1

China 81 113 90 -20.2

Egypt 42 47 60 30.0

Saudi Arabia 52 66 60 -9.1

Mexico 40 30 45 47.9

United States 15 23 45 94.2

EXPORTS: BUTTER

‘000 tonnes (product weight)

2013 2014 2015

Change

2015

over

2014 (%) prelim. f'cast

World 914 979 942 -3.7

New Zealand 461 510 459 -10.0

EU 128 149 187 25.0

Belarus 66 69 96 40.0

Australia 49 43 39 -9.4

United States 94 74 30 -59.3

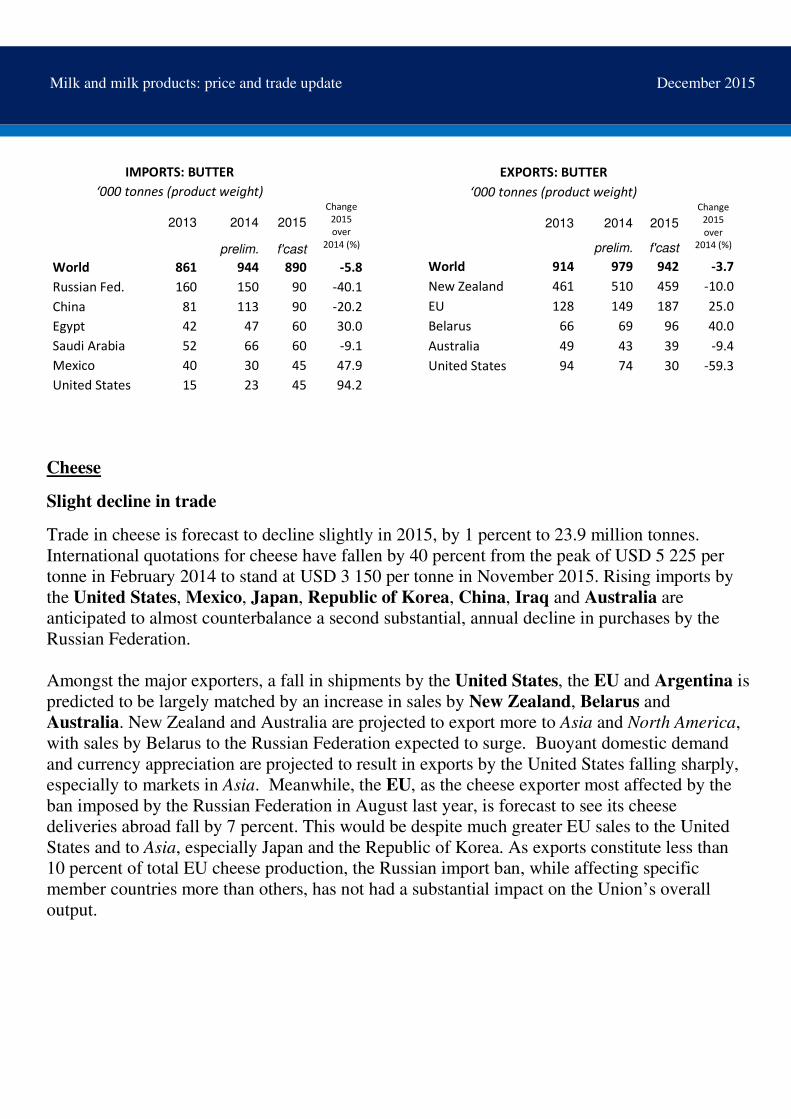

Cheese

Slight decline in trade

Trade in cheese is forecast to decline slightly in 2015, by 1 percent to 23.9 million tonnes.

International quotations for cheese have fallen by 40 percent from the peak of USD 5 225 per

tonne in February 2014 to stand at USD 3 150 per tonne in November 2015. Rising imports by

the United States, Mexico, Japan, Republic of Korea, China, Iraq and Australia are

anticipated to almost counterbalance a second substantial, annual decline in purchases by the

Russian Federation.

Amongst the major exporters, a fall in shipments by the United States, the EU and Argentina is

predicted to be largely matched by an increase in sales by New Zealand, Belarus and

Australia. New Zealand and Australia are projected to export more to Asia and North America,

with sales by Belarus to the Russian Federation expected to surge. Buoyant domestic demand

and currency appreciation are projected to result in exports by the United States falling sharply,

especially to markets in Asia. Meanwhile, the EU, as the cheese exporter most affected by the

ban imposed by the Russian Federation in August last year, is forecast to see its cheese

deliveries abroad fall by 7 percent. This would be despite much greater EU sales to the United

States and to Asia, especially Japan and the Republic of Korea. As exports constitute less than

10 percent of total EU cheese production, the Russian import ban, while affecting specific

member countries more than others, has not had a substantial impact on the Union’s overall

output.

Milk and milk products: price and trade update December 2015

0

50

100

150

200

250

300

350

400

450

500

2011 2012 2013 2014 2015 f'cast

* product weight, '000 tonnes

Cheese Imports *

Japan

United States

Russian Fed.

Saudi Arabia

Mexico

China

Rep. of Korea

0

50

100

150

200

250

300

* product weight, '000 tonnes

EU: Cheese exports *

Aug 12 -July 13

Aug 13- July 14

Aug 14- July 15

Milk and milk products: price and trade update December 2015

For comments or queries please use the following email contact: [email protected]

Use of material is subject to credit being given to source:

Milk and Milk Products: price and trade update

Trade and Markets Division

Food and Agriculture Organization of the United Nations

IMPORTS: CHEESE

‘000 tonnes (product weight)

2013 2014 2015

Change

2015 over

2014 (%)

prelim. f'cast

World 2268 2206 2182 -1.1

Japan 236 232 250 7.8

United States 148 165 206 25.0

Russian Fed. 462 316 176 -44.3

Saudi Arabia 134 148 138 -7.0

Mexico 103 99 118 19.0

China 87 108 114 6.2

Rep. of Korea 85 97 113 16.2

EXPORTS: CHEESE

‘000 tonnes (product weight)

2013 2014 2015 Change

2015

over

2014 (%) prelim. f'cast

World 2394 2410 2385 -1.0

EU 787 721 671 -6.9

New Zealand 277 278 327 17.7

United States 318 371 315 -15.0

Belarus 140 166 201 21.3

Australia 163 151 166 10.3

Saudi Arabia 111 115 120 4.3