milton johnson svp and controller

DESCRIPTION

Milton Johnson SVP and Controller. Mark Kimbrough VP, Investor Relations. HCA. 2004. Goldman Sachs. - PowerPoint PPT PresentationTRANSCRIPT

Milton JohnsonMilton JohnsonSVP and ControllerSVP and Controller

Goldman SachsGoldman Sachs20042004HCAHCA

Mark KimbroughMark KimbroughVP, Investor RelationsVP, Investor Relations

This press release contains forward-looking statements based on current management expectations. Those forward-looking statements include all statements regarding our estimated results of operations in future periods and all statements other than those made solely with respect to historical fact. Numerous risks, uncertainties and other factors may cause actual results to differ materially from those expressed in any forward-looking statements. These factors include, but are not limited to (i) increases in the amount and risk of collectability of uninsured accounts and deductibles and co-pay amounts for insured accounts, (ii) the ability to achieve operating and financial targets and achieve expected levels of patient volumes and control the costs of providing services, (iii) the highly competitive nature of the health care business, (iv) the efforts of insurers, health care providers and others to contain health care costs, (v) possible changes in the Medicare and Medicaid programs that may impact reimbursements to health care providers and insurers, (vi) the ability to attract and retain qualified management and personnel, including affiliated physicians, nurses and medical support personnel, (vii) potential liabilities and other claims that may be asserted against the Company, (viii) fluctuations in the market value of the Company’s common stock, (ix) the impact of the Company’s charity care and self-pay discounting policy changes, (x) changes in accounting practices, (xi) changes in general economic conditions, (xii) future divestitures which may result in charges, (xiii) changes in revenue mix and the ability to enter into and renew managed care provider arrangements on acceptable terms, (xiv) the availability and terms of capital to fund the expansion of the Company’s business, (xv) changes in business strategy or development plans, (xvi) delays in receiving payments for services provided, (xvii) the possible enactment of Federal or state health care reform, (xviii) the outcome of pending and any future tax audits and litigation associated with the Company’s tax positions, (xix) the outcome of the Company’s continuing efforts to monitor, maintain and comply with appropriate laws, regulations, policies and procedures and the Company’s corporate integrity agreement with the government, (xx) changes in Federal, state or local regulations affecting the health care industry, (xxi) the ability to successfully integrate the operations of Health Midwest, (xxii) the ability to develop and implement the payroll and human resources information system within the expected time and cost projections and, upon implementation, to realize the expected benefits and efficiencies, and (xxiii) other risk factors detailed in the Company’s filings with the SEC. Many of the factors that will determine the Company’s future results are beyond the ability of the Company to control or predict. In light of the significant uncertainties inherent in the forward-looking statements contained herein, readers should not place undue reliance on forward-looking statements, which reflect management’s views only as of the date hereof. The Company undertakes no obligation to revise or update any forward-looking statements, or to make any other forward-looking statements, whether as a result of new information, future events or otherwise.

All references to “Company” and “HCA” as used throughout this document refer to HCA Inc. and its affiliates.

Goldman SachsGoldman Sachs20042004HCAHCA 22

Goldman SachsGoldman Sachs20042004HCAHCA 33

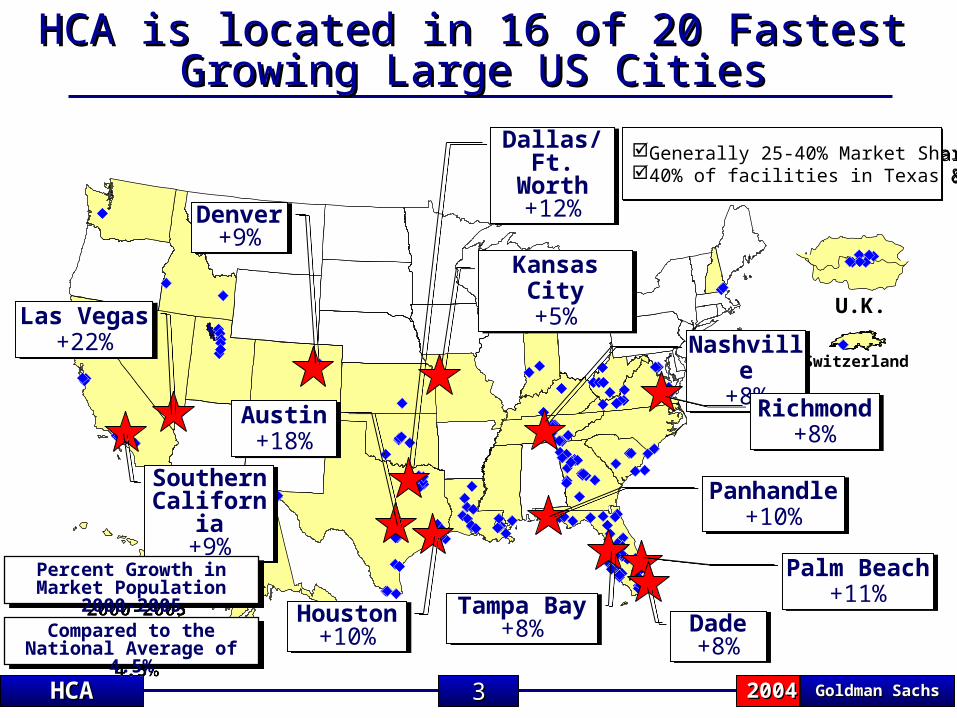

HCA is located in 16 of 20 Fastest HCA is located in 16 of 20 Fastest Growing Large US CitiesGrowing Large US Cities

Switzerland

U.K.

%%

%

%%%

Compared to the National Average of 4.5%

Compared to the National Average of 4.5%

Las Vegas+22%

Las Vegas+22%

Southern California

+9%

Southern California

+9%

Denver+9%

Denver+9%

Dade+8%

Dade+8%

Nashville+8%

Nashville+8%

Panhandle+10%

Panhandle+10%

Tampa Bay+8%

Tampa Bay+8%

Dallas/Ft. Worth+12%

Dallas/Ft. Worth+12%

Austin+18%

Austin+18%

Richmond+8%

Richmond+8%

Palm Beach+11%

Palm Beach+11%

Houston+10%

Houston+10%

Kansas City+5%

Kansas City+5%

Percent Growth in Market Population 2000-2005

Percent Growth in Market Population 2000-2005

Generally 25-40% Market Share40% of facilities in Texas & Florida

Generally 25-40% Market Share40% of facilities in Texas & Florida

Goldman SachsGoldman Sachs20042004HCAHCA 44

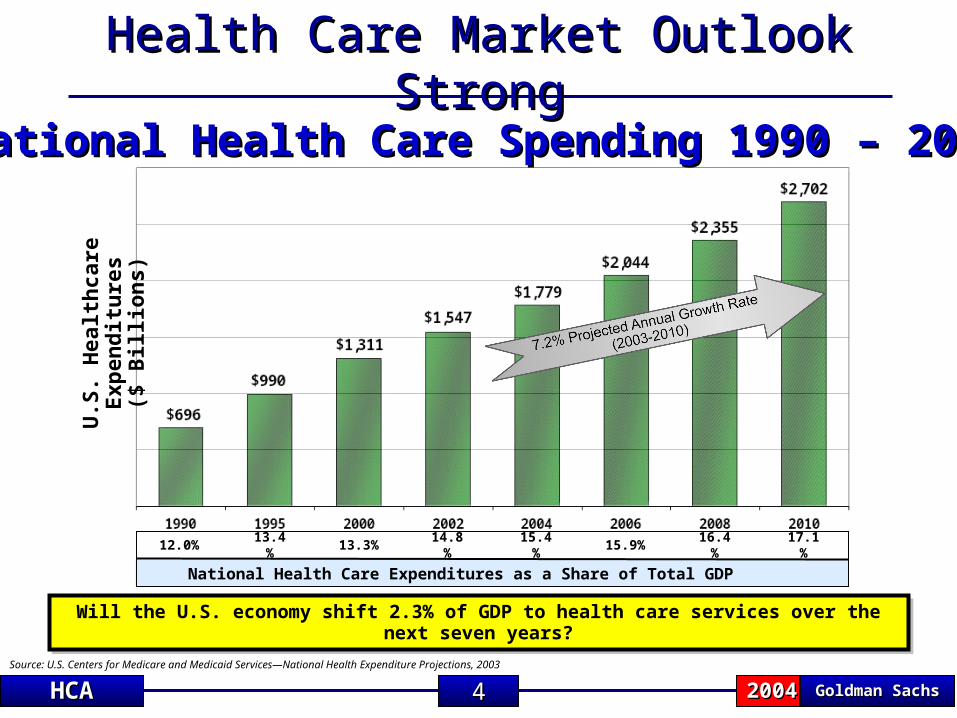

Health Care Market Outlook StrongHealth Care Market Outlook StrongU

.S. H

ealt

hca

re E

xpen

dit

ure

s($

Bill

ion

s)

National Health Care Spending 1990 – 2010National Health Care Spending 1990 – 2010

National Health Care Expenditures as a Share of Total GDP

12.0%13.4%

13.3% 14.8% 15.4% 15.9% 16.4% 17.1%

Source: U.S. Centers for Medicare and Medicaid Services—National Health Expenditure Projections, 2003

Will the U.S. economy shift 2.3% of GDP to health care services over the next seven years?Will the U.S. economy shift 2.3% of GDP to health care services over the next seven years?

Goldman SachsGoldman Sachs20042004HCAHCA 55

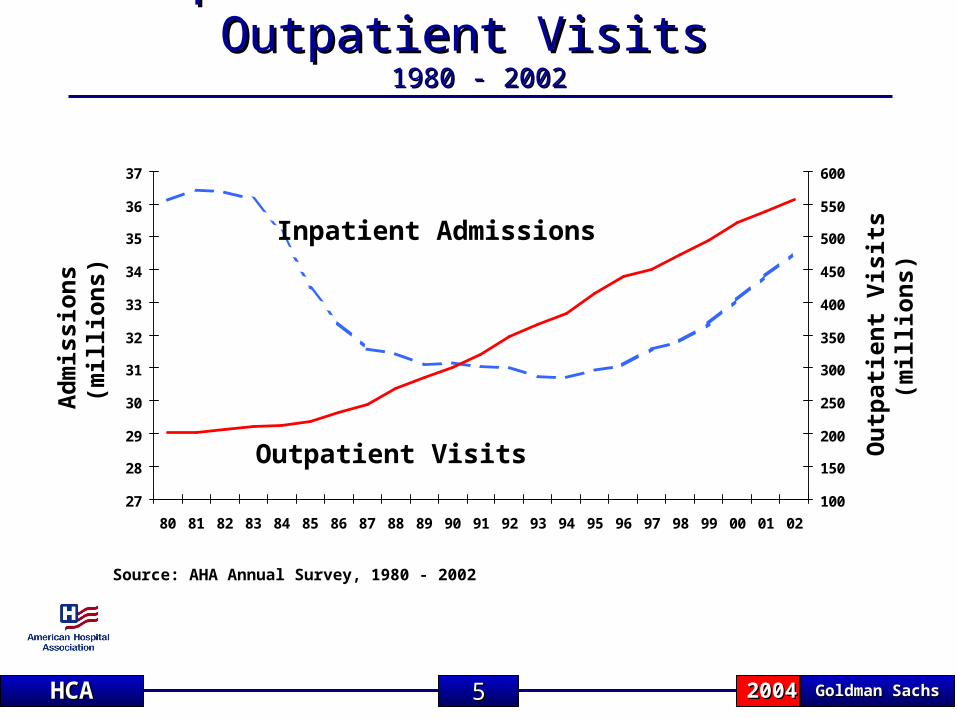

Source: AHA Annual Survey, 1980 - 2002

27

28

29

30

31

32

33

34

35

36

37

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02

100

150

200

250

300

350

400

450

500

550

600

Outpatient Visits

Inpatient Admissions

Ad

mis

sio

ns

(mil

lio

ns)

Ou

tpat

ien

t V

isit

s (m

illi

on

s)

Inpatient Admissions and Outpatient Visits Inpatient Admissions and Outpatient Visits 1980 - 20021980 - 2002

Goldman SachsGoldman Sachs20042004HCAHCA 66

-1.0%

1.0%

3.0%

5.0%

7.0%

1Q 00 2Q 00 3Q 00 4Q 00 1Q 01 2Q 01 3Q 01 4Q 01 1Q 02 2Q 02 3Q 02 4Q 02 1Q 03 2Q 03 3Q 03 4Q 03 1Q 04

Admissions Rolling 12 mo. Avg

HCA Admission Trends 2001 to 1Q 2004HCA Admission Trends 2001 to 1Q 2004Same FacilitySame Facility

6.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

HCAMarket

Competitors

15.4%

HCA Growing Medicare Market Share

Growth in Medicare Admissions 1998-2001

HCA Growing Medicare Market Share

Growth in Medicare Admissions 1998-2001

Goldman SachsGoldman Sachs20042004HCAHCA 77

Admissions growth rates vary by market Admissions growth rates vary by market A

dm

issi

on

s C

han

ge

Admissions % Change

(1,500)

(1,000)

(500)

-

500

1,000

1,500

2,000

2,500

-15% -10% -5% 0% 5% 10% 15%

Total Admissions Determine Bubble

Size

Top 15 Top 15 Markets in Markets in AdmissionAdmissions Growths Growth+11,860/+11,860/

+5.9% vs. +5.9% vs. PYPY

Top 15 Top 15 Markets in Markets in AdmissionAdmissions Growths Growth+11,860/+11,860/

+5.9% vs. +5.9% vs. PYPY

Bottom 15 Bottom 15 Markets in Markets in AdmissionAdmissions Growths Growth

-2,773/-2,773/-2.6% vs. -2.6% vs.

PYPY

Bottom 15 Bottom 15 Markets in Markets in AdmissionAdmissions Growths Growth

-2,773/-2,773/-2.6% vs. -2.6% vs.

PYPY

Average Chg.+2.5% 1

Volume Variance by Market – 1st Quarter – Same Market

Houston-2.6%

So. Cal-5.6%

Indiana-12.3%

Far West Una.-3.2%

Treasure Coast-2.4%

Switzerland-6.4%

Las Vegas-0.8%

Dallas/Dallas/Ft. WorthFt. Worth

+5.6%+5.6%

Tampa Tampa BayBay

+3.1%

Austin +6.1%

El Paso+9.7%

Ft. Myers+5.9%

San Antonio

+3.1%

No. VA-3.9%

N. Cent. Fla.+5.2%

Jacksonville+4.5%

San Jose+3.9%

Panhandle+2.7%

N. Monroe-11.0%

Mid America-5.2%

Columbus+1.6%

S.Carolina0.1%

Rio Grande+12.8%

NW Ga.+12.9%

Mid. GA+0.3%

Cent. La.-1.4%Corpus Christi

-1.7%

Nashville+14.9%

Denver 2+6.1%

Richmond+4.9%

1: Same Facility2: Denver is a non-

consolidating JV Market

Goldman SachsGoldman Sachs20042004HCAHCA 88

HCA Capital ExpendituresHCA Capital Expenditures

ER & Outpatient Services19%/$720

Replacement Facilities3%/$98M

New & Expanded Services

18%/$740M

New Facilities10%/$395MBeds

14%/$550M

Surgery/Spec'l Units

22%/$870M

Land & Improvements

14%/$565M

1,565 New Beds

54 Facilities with Surgeryand/or ICU/CCU

expansions

Four NewFacilities

378 Beds

Open Heart, ImagingCardiology, Oncology, etc.

37 ERExpansions

37 ERExpansions

Distribution of Capital Dollars2002 and Beyond

Distribution of Capital Dollars2002 and Beyond

New Denver FacilityNew Denver Facility

Expansions

$0.0

$0.5

$1.0

$1.5

$2.0

2000 2001 2002 2003 2004E

Billions2000

$1.22001

$1.42002

$1.72003

$1.82004E

$1.8

Routine

Patient Safety & Infrastructure

New Facilities

Expansions

Goldman SachsGoldman Sachs20042004HCAHCA 99

The Genesis of the Bad Debt/Charity The Genesis of the Bad Debt/Charity Care IssueCare Issue

22.222.2%%

23.523.5%%

21.221.2%%

22.222.2%%

17.017.0%%

19.219.2%%

29.729.7%%

23.523.5%%

15.115.1%% 15.415.4%%

19.719.7%%

16.716.7%%20.320.3%%15.415.4%%

19.319.3%%15.915.9%%

16.416.4%%

NationalAverage:15.2% 1

NationalAverage:15.2% 1

18.118.1%%

>20% Uninsured

15-20% Uninsured

<15% Uninsured

25.625.6%%

14.6%

22.822.8%%

HCA is in 14 of the 20 highest uninsured states, with 72% of its hospitals in those states

HCA is in 14 of the 20 highest uninsured states, with 72% of its hospitals in those states

HCAHCAWeightedAverage:22.6% 2

HCAHCAWeightedAverage:22.6% 2

1: U.S. Census Bureau “Health Insurance Coverage in the United States: 2002”.2: Kaiser Commission: Health Ins. Coverage of Nonelderly Adults 2001-2002.

13.1%13.1%

Goldman SachsGoldman Sachs20042004HCAHCA 1010

ER has the highest volume of uninsured… ER has the highest volume of uninsured… requires interventionrequires intervention

MedicareMedicare

103,820103,820

MedicareMedicare

103,820103,820

UninsuredUninsured

13,31313,313

UninsuredUninsured

13,31313,313

Managed/ Managed/ MedicaidMedicaid

92,86992,869

Managed/ Managed/ MedicaidMedicaid

92,86992,869

AdmittedAdmitted 210,002AdmittedAdmitted 210,002

ER VisitsER Visits 1,025,639ER VisitsER Visits

1,025,639

ER VisitsER Visits1,235,641 2.3%

ER VisitsER Visits1,235,641 2.3%

MedicareMedicare

109,235109,235

MedicareMedicare

109,235109,235

UninsuredUninsured

231,436231,43695%95%

UninsuredUninsured

231,436231,43695%95%

Managed/ Managed/ MedicaidMedicaid

684,968684,968

Managed/ Managed/ MedicaidMedicaid

684,968684,968

17% 83%

5% 95%

Admitted 6.6% Managed/Medicaid 6.4% Medicare 5.9% Uninsured 15.2%

ER Visits 1.5% Managed/Medicaid 3.3% Medicare 0.5% Uninsured 20.1%

Net % Change 1Q03-04 Net % Change 1Q03-04

1st Quarter 2004 – Eastern & Western Groups

1010

Goldman SachsGoldman Sachs20042004HCAHCA 1111

Outpatient Svcs.6%

Direct Admissions

14%

ER Visits41%

Admissions Thru ER39%

75-80%Uninsured Patients

“ “How System is Accessed”How System is Accessed”

20-25%Co-Pay &

Deductibles

Origination of Bad Debt ExpenseOrigination of Bad Debt Expense

1Q 01 vs. 1Q 04 front- 1Q 01 vs. 1Q 04 front- end collections end collections 93%, 93%, percent collected percent collected 53%, 53%, co-pays/deductibles co-pays/deductibles 25%25% Intensify collections atIntensify collections at discharge and postdischarge and post dischargedischargeMinimum front-end Minimum front-end deposit requirementsdeposit requirements

1111

Goldman SachsGoldman Sachs20042004HCAHCA 1212

Outpatient Svcs.6%

Direct Admissions

14%

ER Visits41%

Admissions Thru ER39%

Bad Debt Action Plan75-80%

Uninsured Patients

Screen all potential non-emergent patients by qualified medical personnelOnce stabilized or deemed non-emergent, proceed with collection effort Mandatory ER case management

Patient Financial Management Committee In-house case management Concurrent financial counseling Standard discharge process

Executive Management approval must be obtained

Minimum deposit standards

Enhanced front-end collection goals

Follow-up care criteria established.

1212

Goldman SachsGoldman Sachs20042004HCAHCA 1313

9.4%

37.2%

OutpatientOutpatientERER

OutpatientOutpatientERER

Enhanced Outpatient Services FocusEnhanced Outpatient Services Focus

12.5%Hospital BasedHospital BasedHospital BasedHospital Based

FreestandingFreestandingFreestandingFreestanding

OutpatientOutpatientDiagnostic Diagnostic ServicesServices

OutpatientOutpatientDiagnostic Diagnostic ServicesServices

ImagingImagingCardiologyCardiologyOncologyOncologyOrthopedicsOrthopedicsNeurologyNeurology

ImagingImagingCardiologyCardiologyOncologyOncologyOrthopedicsOrthopedicsNeurologyNeurology

Hospital BasedHospital BasedHospital BasedHospital BasedOutpatient Outpatient SurgeriesSurgeriesOutpatient Outpatient SurgeriesSurgeries

15.3%ASC BasedASC BasedASC BasedASC Based

70%

30%

2003% of HCA

Net Revenue

As a % of Outpatient Surgeries

O/P Comprised of Three Business LinesO/P Comprised of Three Business Lines

Goldman SachsGoldman Sachs20042004HCAHCA 1414

2004 Managed Care Contracting

2005 Contract

Pricing Timeline*

6,844 Facility Level Active Contracts

*Anticipated Completion Dates

Pre-2004 1Q04 2Q04 3Q04 4Q04

83% of 2004 and 42% of 2005 contracts 83% of 2004 and 42% of 2005 contracts completed.completed.

83% of 2004 and 42% of 2005 contracts 83% of 2004 and 42% of 2005 contracts completed.completed.

2005Cumulative

42%42% 55%55% 75%75% 95%95%35%35% 100%100%

15.0%

10.5% 11.4%13.0% 13.3%

9.6%7.0% 7.3%

11.1%

0%

16%

1Q 02 2Q 02 3Q 02 4Q 02 1Q 03 2Q 03 3Q 03 4Q 03 1Q 04

11.1% 9.9%

Net Revenue per Adjusted AdmissionManaged Care & Other Discounted

1414

Goldman SachsGoldman Sachs20042004HCAHCA 1515

4.7%

8.1%5.4%

5.6% 5.5% 5.3%

3.8%

6.0%6.2%

7.5%

9.3%

7.4%7.8%

5.5%

10.4%

7.6%

8.9%

10.8%10.2%

8.0%

6.0%7.0%

8.8%8.5%8.0%

5.2%

-1%

1%

3%

5%

7%

9%

11%

13%

15%

1Q 01 2Q 01 3Q 01 4Q 01 1Q 02 2Q 02 3Q 02 4Q 02 1Q 03 2Q 03 3Q 03 4Q 03 1Q 04

20012001 20022002 20032003 20042004

7.0% 9.4%7.4%

6.4%6.7%6.5%

Same Facility – Percent Change from Prior Year

Operating Expenses per Operating Expenses per Adjusted Admission Managed EffectivelyAdjusted Admission Managed EffectivelyO

per

atin

g E

xpe

nse

s /A

A –

Pe

rce

nt

Ch

ang

e f

rom

Pri

or

Yea

r

Operating Expense/AA Operating Expense/AA (Adj. For Bad Debt)

1515

Goldman SachsGoldman Sachs20042004HCAHCA 1616

Employee Satisfaction at Record LevelsEmployee Satisfaction at Record Levels

26.7%25.9%

22.8%

20.1%

18.8%18.3%

17.0% 16.8%

3.5%

3.6%

3.7%

3.8%

15%

20%

25%

30%

2000 2001 2002 2003

3.3%

3.4%

3.5%

3.6%

3.7%

3.8%

3.9%

Employee Satisfaction(Gallup Score)

Employee Turnover

Nurse Turnover

Tu

rno

ver

Rat

eS

atisfaction

Sco

re

1616

Goldman SachsGoldman Sachs20042004HCAHCA 1717

Strong Cash Flow Trends Provide Strong Cash Flow Trends Provide OpportunitiesOpportunities

$1,301

$1,584

$2,046

$2,786 $2,822

$0

$3,500

1999 2000 2001 2002 2003

Net Cash Provided by Operating ActivitiesDollars in Millions

Excluding settlements with government agencies and investigation related costs.

New New Dividend PolicyDividend Policy

Share Share Repurchase Repurchase ProgramProgram

Capital Capital ReinvestmentReinvestment

BalanceBalanceSheetSheet

Goldman SachsGoldman Sachs20042004HCAHCA 1818

$7.3 Billion$7.3 Billion

244 Million Shares244 Million Shares

38% of outstanding 38% of outstanding sharesshares

Average Price: Average Price: $30.03$30.03

Opportunities Of Having Opportunities Of Having Strong Cash FlowStrong Cash Flow

Share Share repurchase repurchase programprogram

$1.3B: 37.9M Shares1997

1998

1999

2000

2001

20032002

YTD 20041

1: 2004 purchases through 5-6-04 2: Includes other activities affecting share balance (stock option exercises, restricted grants, and ESPP activity).

$33.59/share$22.68/share

$930M: 41M Shares

$1.4B: 55.6M Shares $24.61/share$1.3B: 43.5M Shares $28.65/share$706M: 19.2M Shares$706M: 19.2M Shares $36.88/share$1.1B: 31.1M Shares $35.76/sh

are

$422M: 10.0M Shares$42.19/share

650M Shares 12/31/96

465M Shares2 4/30/04

$282M: 6.2M Shares$45.53/share

Goldman SachsGoldman Sachs20042004HCAHCA 1919

HCA is Investing Significantly in Programs HCA is Investing Significantly in Programs for Patient Safety and Improved Patient Outcomesfor Patient Safety and Improved Patient Outcomes

E MAR: Medication Error Prevention

E POM: Physician Order Entry

100% Participation in CMS Quality Reporting Initiative

Member of NQF and Leapfrog

Cardiovascular, OB and Emergency Department Initiatives

Goldman SachsGoldman Sachs20042004HCAHCA 2020

A prudent financial strategy that provides for a strong A prudent financial strategy that provides for a strong balance sheet and return of cash to shareholders through balance sheet and return of cash to shareholders through

share repurchase and/or dividendsshare repurchase and/or dividends

Excellent Investment OpportunitiesExcellent Investment Opportunities

Strong Cash FlowsStrong Cash Flows

Excellent Long-Term Earnings Growth OutlookExcellent Long-Term Earnings Growth Outlook

Great AssetsGreat Assets

In Summary We Have….In Summary We Have….