mind the gap - financial conduct authority | fca · mind the gap consumer research ... •...

TRANSCRIPT

AuthorsBecky RoweDamon De IonnoDominique PetersHannah Wright

November 2015

Mind the gapConsumer research exploring experiences of financial exclusion across the UK

Acknowledgements

The research team at ESRO are extremely grateful to numerous individuals and or-ganisations for their valuable contributions to this project. Of most importance are the many individuals who shared their stories and experiences with us during the re-search process. Without their willing participation and candour this research would not have been possible.

We would also like to extend special thanks to those subject experts who kindly shared their time and knowledge to give additional context to this research – includ-ing representatives of the following organisations:

• Age UK• Barnardo’s• CAB• Consumer Council of Northern Ireland• DOSH• Friends, Families & Travellers• Homeless Link• Joseph Rowntree Foundation• Macmillan Cancer Support• Money Advice Trust• National Numeracy• NUS• Passcard• Prison Reform Trust• Rees Foundation• Royal British Legion• Scope• Scottish Refugee Council• Stepchange• Toynbee Hall• Unlock• Viridian Housing

• Barclays• Building Societies Association• Experian• Federation of Small Businesses• Financial Ombudsman Service

We’d also like to thank the team at the Financial Conduct Authority for their support throughout the research process, and Professor Sharon Collard for laying some of the groundwork for this research.

ESRO is a multiple award-winning, independent research and innovation consultancy that works with clients across the public, private and third sectors. We specialise in conducting research on com-plex and sensitive issues, and we are committed to designing and delivering projects that make sense of some of the most challenging research questions.

This research was led by Becky Rowe and Damon De Ionno. The research team comprised Hannah Wright, Dominique Peters, Catriona Hay, Evie Breese and Nick Lane.

1. Executive Summary 4

2. Introduction 9

3. Overviewof findings 11

4. Makingsenseof access 15

5. ‘TheMaze’–Process,requirementsandeligibility 21

6. ‘TheFog’–Marketnavigationandcomprehension 31

7. ‘TheVoid’–Physicalanddigitalbarriers 41

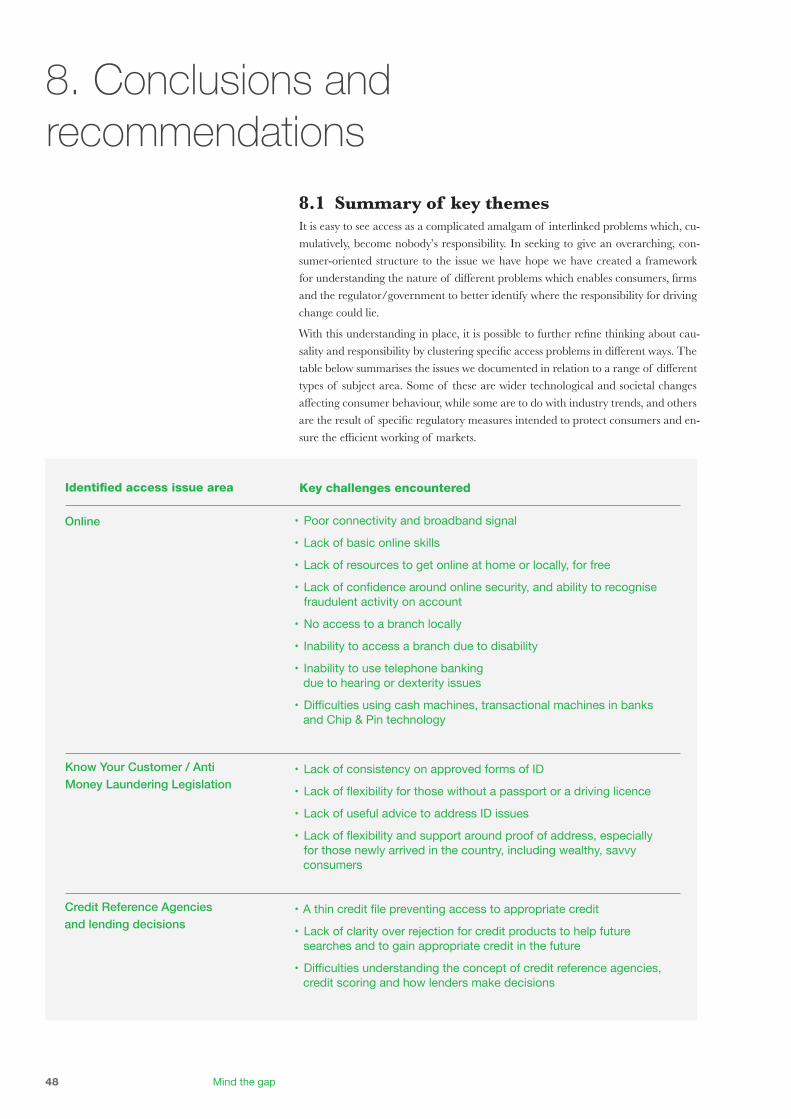

8. Conclusionsandrecommendations 48

9. Appendix 52

Contents

3

1. Executive Summary

1.1 Project overviewThis independent research was commissioned by the Financial Conduct Authority to shed new light on the consumer experience of issues associated with access to financial services. The objective was to explore in depth the nature of problems encountered by a range of different customers, experiencing different types of chal-lenges when accessing a variety of financial products and services.

As the culmination of a four-phase work stream undertaken by the FCA’s Consumer Insight department, the overarching aim was to bring new clarity to the causes and impact of these complex and challenging problems – helping the regulator to better understand how it might address access issues in future.

Fieldwork was conducted across England, Scotland, Wales and Northern Ireland between July and November 2015. The research was qualitative in nature and con-sisted of a number of different strands, including:

• 50 x qualitative depth interviews with consumers

• 28 x interviews with ‘expert’ representatives from a range of charities, consumer bodies, industry organisations and firms

• 6 x focus groups with consumers

In seeking to understand a range of different types of access issues, the consumer re-search focused on those who had experienced one or more of five problems:

• Digital and physical barriers

• Barriers to banking (notably the impact of Know Your Customer and Anti-Money Laundering)

• Barriers caused by credit file issues

• Barriers facing older mortgage borrowers

• Barriers to accessing insurance

1.2 Why access mattersAccess can feel like an overwhelmingly complex, even insurmountable, challenge. In covering a huge range of issues – from practical challenges of digital or geographic exclusion through to matters of ineligibility – the questions raised by the ‘access’ de-bate simultaneously demand consideration of the minutiae of process, technological and demographic trends, and big, society-defining decisions about who is entitled to what, and how financial inclusion should be achieved.

Just because the issue appears unwieldy, however, does not mean that the problems it causes should be ignored. Time and again, this research demonstrated how access issues clearly cause secondary complications or detriment to consumers. It revealed clear gaps in the market, with consumers in certain circumstances simply unable to find products to meet their needs – whether due to health conditions, geography, or simple questions of affordability. Furthermore, regardless of their actual eligibility or ineligibility for certain products, all consumers were at risk of difficulties in access-ing or navigating the market, understanding technical features or the reasons behind a rejection, or meeting the bureaucratic requirements of application and verification procedures (particularly in terms of identification).

Above all, the urgency of the issue lies in its ubiquity – spanning not just the whole customer journey, but all different types of consumer groups. Far from revealing a niche phenomenon, experienced exclusively by low-income groups or those living in

4 Mind the gap

anomalous circumstances, this research showed how access issues can affect all con-sumer segments, irrespective of digital capability, affluence or financial literacy. Almost all of us will have experienced an access issue at some point in our financial lives, and many of us are likely to face more serious access-related complications at some juncture.

1.3 Classifying access issuesIn seeking a simple classification of access issues which accurately reflects the con-sumer experience, our analysis allocated problems to three different layers:

• ‘The Maze’ – Process, requirements and eligibility

• ‘The Fog’ – Market navigation and comprehension

• ‘The Void’ – Digital and physical barriers

Key findings related to each layer are detailed below.

‘The Maze’ – Process, requirements and eligibility• There are often practical barriers to accessing financial products, in particular

relating to the provision of the required/requested ID documentation

• Staff often give consumers contradictory or limited information on their options, and messaging can change between firms, and even between branches

• Consumers can struggle to understand and use their products once they have purchased them

• A lack of explanation as to why someone has been denied a product – along with a lack of suggested alternatives – can lead to future self-limiting behaviours

• Issues relating to income, health and place of residence mean that, for some, there are simply no products available that meet their needs

‘The Fog’ – Market navigation and comprehension• Consumers can struggle to understand technical language used to describe

financial products and services

• There are also difficulties experienced by many when it comes to understanding not only the benefits of products, but their costs and exclusions too

• There are many myths around credit scoring that can impede access to mainstream credit, or consumers’ ability to improve their scores

• Consumers struggle to search for the most appropriate product, despite the advent of price comparison websites

• Those who are ineligible for products can have their difficulties compounded by the length of time it takes to establish their ineligibility

‘The Void’ – Digital and physical barriers• Practical exclusion of consumers from financial products and services is primarily

linked to physical access issues, or digital exclusion

• Older people, those with disabilities, and those living in rural areas, are most likely to struggle with physical access, due to branch closures and practical impediments

• The same groups are also more likely than others to experience digital exclusion, along with some low-income consumers

• A lack of access to the required technology, alongside a lack of confidence or computer literacy, can exclude some consumers from access to products and services

1.4 Causes and responsibilitiesIn attributing causes and identifying potential mitigations, this research has revealed a landscape which is effectively stuck in a kind of stalemate. Much of the discourse surrounding access issues – both at a personal level, between consumers and firms, and a macro level – is characterised by a ‘blame game’, in which all of the possible agents of change (consumers, firms, government/regulator) point the finger at each other, ‘pass the buck’, or simply remain silent. Much of the time, it is this stand-off which allows access issues to continue to occur and, in some cases, intensify.

Executive summary 5

Superficially, this state of affairs suggests a complexity to access issues which borders on the intractable – as if they are inevitable artefacts of the free market, to be tol-erated rather than solved. Our research, however, reveals this impression to be false. In truth, many of the problems documented in this research could have been easily resolved – benefiting firms and consumers alike – if simple changes had been made, particularly in terms of greater responsibility being taken by one or more parties. As for those which are more challenging, they too could have been mitigated (if not necessarily resolved in the consumer’s favour) if greater guidance and clarity had been offered to consumers at critical points in their journey.

Behind it all lies the question of responsibility: whose job is it to address any given issue? An important feature of the ‘layers’ classification of access issues is that the problems belonging to each layer are causally distinct – in other words, each lay-er exists independently of the others in terms of the nature of the problem, and what is required (and from whom) to solve it. A consumer may experience problems across one or more of the layers – and occasionally across all three as part of the same product journey – but no one party (whether firm, consumer or government/regulator) can realistically be expected to solve all types of consumer access issues.

The research has shown clearly that while some problems are caused by firms’ pol-icies, others arise from a dissonance between policy and frontline practice, while others still are the result of industry-wide impenetrability or inconsistency. Others may be regarded as the inadvertent consequence of rules and regulation designed to protect firms and/or consumers, while some are firmly the province of government

– notably hard-and-fast questions about entitlement, inclusion, infrastructure and what can fairly be expected from consumers in terms of digital or financial literacy.

1.5 Opportunities for changeLooking ahead, our detailed study of the problems experienced by consumers with-in each layer revealed a number of clear opportunities for different bodies – whether on the consumer, firm or regulatory/government side – to reconsider policies, prac-tices and procedures.

The table overleaf outlines key questions for each of these parties to consider.

6 Mind the gap

‘The Fog’ – Market navigation and comprehension

• Howcanfirmsensurethatfinancialproductsarecommunicatedandmarketedinawaythatmakesthemaccessibletoconsumers,usingplainEnglishandmakingT&Csasaccessibleaspossible

• Howcanfirmsmaketimetoensurecustomersarepurchasingproductswhicharesuitabletotheirneedsandcircumstances?

• Howcanfirmsbetterfacilitateeffectiveconsumersearches,sothatconsumersareaccessingthoseproductswhichbestmeettheirneeds?

• Howcanfirmsprovideproductswhichworkforthemcommerciallyandalsoplugthosegapsinthemarketwhereconsumersstruggletoaccessanyproducts?

•Whatcanconsumersreasonablybeexpectedtounderstandwhenitcomestofinancialproductsandservices?

• Howcanwebettersupportconsumerstomakeeffectivechoicesaboutfinancialproducts?

• Istheguidanceavailabletoconsumersaccessibleandappropriatetomeetthewiderangeofindividualneeds?

• Dowehaveunrealisticexpectationsofconsumerswhenevenpeoplewithgoodfinancialliteracystruggle–areweexpectingthemtoconductsearchesofthemarketbeyondtheirmeansandabilities?

• Canweprovidebetterframeworkstohelpconsumerscompareproductsandunderstandwhatisbestforthem?

• Howcanwebestsupportinnovationtoensurethatcomparisonandswitchingismadeeasieracrossthefullrangeoffinancialproducts?

•Whatisthebestwaytoensurefirmsareusingstandardisedlanguageandlessjargon,inordertoaidcomprehensiononthepartofconsumers?

• Howcanweclarifyresponsibilityaroundsign-posting,sothatconsumersareabletoconductthewidestpossiblesearchesofthemarket,andaren’tmissingoutonproductsthatmeettheirneedssimplybecausetheyareunawareoftheirexistence?

• Whoshouldconsumers(andtheirrepresentatives)turntowhentheysimplycannotfindaproductwhichmeetstheirneeds,andwhoshouldtakeresponsibilityforsuchgapsinthemarket?

Layer Firms Consumers Govt / Regulator / Other

‘The Maze’ – Process, requirements and eligibility

• Howcanfirmsbehonestandupfrontaboutexclusionsandrejections,withoutcompromisingtheirrulesandtheregulationinquestion?

• Howcanfirms/tradebodiesmonitorcustomerexperiencesofusingtheirproductsandservices?Forexample,thecustomerjourneyoftryingtofindsuitableand/oraffordableinsuranceproductswhicheventhemostsavvyofconsumersstrugglewith?

• Firmsneedtobettersupporttheirfrontlinestafftoensureallarecomfortableandfamiliarwithprocedures,andinformationandadviceisthereforeconsistentacrossbranchesandbetweenmembersofstaff.Whoisbestplacedtoencouragethis?

• Howcanstaffprovideappropriateadviceandsupportwhenconsumershavebeenrejected,inordertohelpthemimprovetheirfuturechancesofacceptance?

• Inwhatwayscanwebettersupportconsumerstomakeeffectivechoicesaboutfinancialproductsandfindproductsthatsuittheirneedswhenevenmainstreamconsumers,whohaverelativelygoodlevelsoffinancialcapability,struggle?

• Istheguidanceavailabletoconsumersaccessibleand/orappropriatetomeetthewiderangeofindividualneeds?

•Whatcanwereasonablyexpectconsumerstounderstandaroundrejections?

•Whenregulationisimposedonthefinancialservicesindustry,isthereclarityaroundwhattheexpectedindustryresponseis,andachancetoreviewanydifficultiesandunexpectedconsequences?

• Bothexpectedandunexpectedconsequencesofeventhebestintentionedregulationmustberegularlymonitoredandtracked.

•WhenitcomestoID,howcantheregulatorandgovernmentworktogethertocreateclarityaboutacceptabledocumentationand/orencouragefirmstobetterservethoseconsumerswithoutthemoststandardformsofID?

•Whatistheroleoftheregulatorand/orgovernmentwhenitcomestosupportingfirmstosignpostconsumerstoalternativeproviderswhentheyareunabletoprovideaproductorservice?

•Whatistheroleoftheregulatorandgovernmentwhenthemarketdoesnotseemtobeprovidingconsumerswithsuitableproductsatanaffordableprice,evenaftercomprehensivesearchesbymanyconsumers?

Executive summary 7

Layer Firms Consumers Govt / Regulator / Other

‘The Void’ – Physical and digital barriers

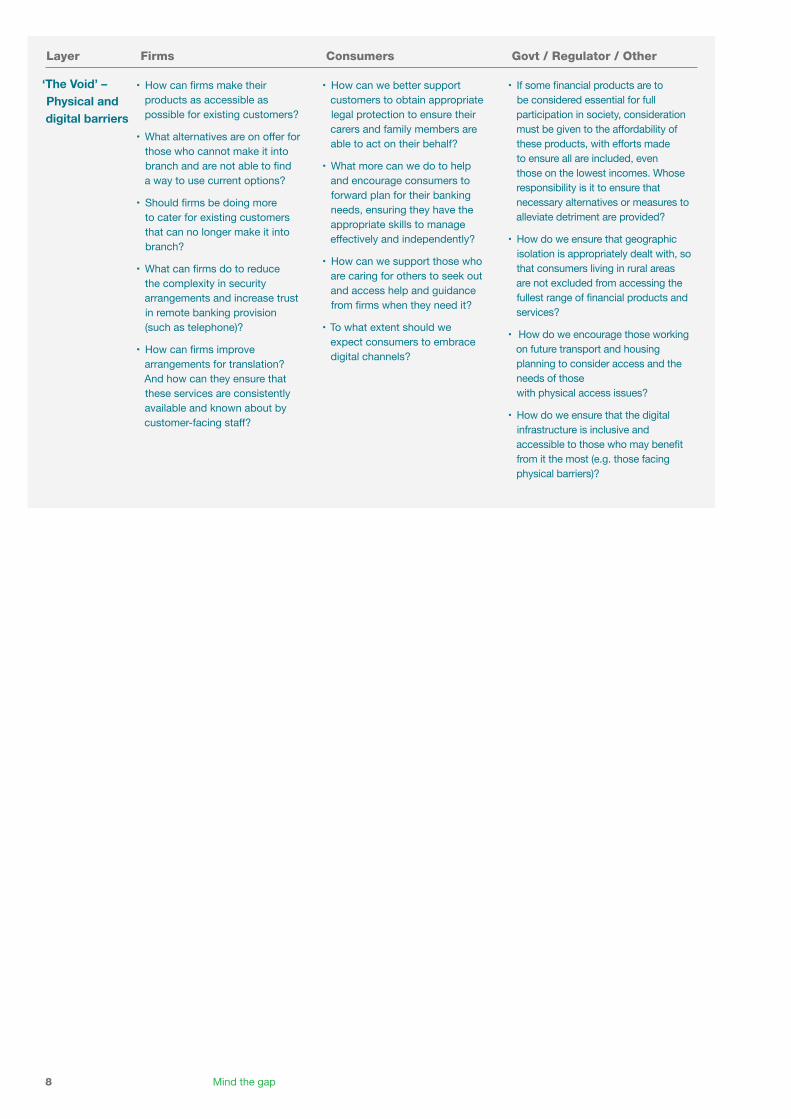

• Howcanfirmsmaketheirproductsasaccessibleaspossibleforexistingcustomers?

•Whatalternativesareonofferforthosewhocannotmakeitintobranchandarenotabletofindawaytousecurrentoptions?

• Shouldfirmsbedoingmoretocaterforexistingcustomersthatcannolongermakeitintobranch?

•Whatcanfirmsdotoreducethecomplexityinsecurityarrangementsandincreasetrustinremotebankingprovision(suchastelephone)?

• Howcanfirmsimprovearrangementsfortranslation?Andhowcantheyensurethattheseservicesareconsistentlyavailableandknownaboutbycustomer-facingstaff?

• Howcanwebettersupportcustomerstoobtainappropriatelegalprotectiontoensuretheircarersandfamilymembersareabletoactontheirbehalf?

•Whatmorecanwedotohelpandencourageconsumerstoforwardplanfortheirbankingneeds,ensuringtheyhavetheappropriateskillstomanageeffectivelyandindependently?

• Howcanwesupportthosewhoarecaringforotherstoseekoutandaccesshelpandguidancefromfirmswhentheyneedit?

•Towhatextentshouldweexpectconsumerstoembracedigitalchannels?

• Ifsomefinancialproductsaretobeconsideredessentialforfullparticipationinsociety,considerationmustbegiventotheaffordabilityoftheseproducts,witheffortsmadetoensureallareincluded,eventhoseonthelowestincomes.Whoseresponsibilityisittoensurethatnecessaryalternativesormeasurestoalleviatedetrimentareprovided?

• Howdoweensurethatgeographicisolationisappropriatelydealtwith,sothatconsumerslivinginruralareasarenotexcludedfromaccessingthefullestrangeoffinancialproductsandservices?

• Howdoweencouragethoseworkingonfuturetransportandhousingplanningtoconsideraccessandtheneedsofthosewithphysicalaccessissues?

• Howdoweensurethatthedigitalinfrastructureisinclusiveandaccessibletothosewhomaybenefitfromitthemost(e.g.thosefacingphysicalbarriers)?

8 Mind the gap

2. Introduction

2.1 ContextThe issue of ‘financial inclusion’ has come to the fore in recent years. Inclusivity requirements such as the EU Payments Accounts Directive, efforts by The G201 and UK Financial Inclusion Commission, and a notable recent report by the UK Financial Inclusion Commission2 (published ahead of the 2015 General Election) have all made a passionate and cogent case for greater financial inclusion. Government initiatives such as the agreement to reduce the fees charged on failed payments from basic bank accounts3 have further raised the profile of ‘access’.

The trend has been accelerated by significant external pressure, exerted both by ad-vocacy groups representing marginal, vulnerable or disadvantaged consumers, as well as an emerging consensus regarding the long-term importance and value of access to basic financial services.

At the same time, growing pressure is being placed on consumers to take more re-sponsibility for their lives and to make better plans for their financial futures. New polices such as auto-enrolment in pension schemes are intended to ensure people are saving adequately for retirement4, while reductions to welfare benefits aim to promote the value of work and independence5.

2.2 State of playTogether, these trends have meant that access to an ever wider range of financial services and products is being increasingly recognised as a pre-requisite for full par-ticipation in society. Yet whilst there has been some progress with financial provision over the years (e.g. introduction of basic bank accounts), evidence from a wide range of sources continues to suggest that a diverse range of consumers continue to strug-gle to access the most suitable financial products and services for their needs and circumstances. For example:

• Age UK suggested in their response to the FCA scoping work on access to financial services that “there are significant access issues for the regulator to study” when it comes to older people’s use of financial services6

• Considering the needs of victims of domestic violence, Citizens Advice Bureau recommended that “Creditor trade associations, individual firms and the Financial Conduct Authority should come together to write and agree best practice guidance to tackle financial abuse and support victims”7

• National Numeracy call for “support from government, the education sector, business and the media” to improve numeracy and financial literacy across the country8

1 https://g20.org/wp-content/uploads/2014/12/2014_g20_financial_inclusion_action_plan.pdf2 http://www.financialinclusioncommission.org.uk/3 https://www.gov.uk/government/news/new-basic-fee-free-bank-accounts-to-help-

millions-manage-their-money4 A New Pension Settlement for the Twenty-First Century, The Pensions Commission, November 20055 Universal Credit: Welfare that Works, Department for Work and Pensions, November 20106 Response to FCA scoping study of access to financial services, Age UK, 17th April 20157 Controlling money, controlling lives: Financial abuse in Britain, CAB, November 20148 Response to the Financial Inclusion Commission’s consultation on the state of financial inclusion in the

UK, National Numeracy, December 2014

Introduction 9

• The Centre for the Study of Financial Innovation recommended that “the regulator should make more of its regard for access to financial services by clarifying the position on banking and insurance for former convicts”9 in their paper ‘Locked Out?’

• The Extra Costs Commission concluded that “where action by disability organisations cannot fully tackle this issue, there is a need for regulators and government to intervene where features of markets result in unfair extra costs for disabled people.”10

• The All Party Parliamentary Group on financial education for vulnerable young people recommended that financial institutions “signpost young people to appropriate support around managing their money, particularly when an account is first opened or if it is apparent that the account holder is in financial difficulty or requires support.”11

For some consumers the impact of this exclusion will be minimal, as they have the resources and ability to work around the problem. For others, however, it can be devastating – resulting in prolonged periods of difficulty, and having many knock-on consequences (e.g. inability to gain access to paid employment or ‘making do’ with-out appropriate insurance cover, despite understanding the need).

2.3 The purpose of this research This research was commissioned by the FCA to provide an independent examina-tion of the issues surrounding access to financial services. The main objective was to understand in greater depth the specific nature of the problems experienced by a broad range of individuals living across the UK.

This report marks the culmination of a four-phase work stream undertaken by the Consumer Insight department at the FCA. Beginning in September 2014, the work stream has reviewed existing research and evidence regarding the barriers faced by consumers in terms of access to financial services, followed by analysis to provide a sense of the numbers of people potentially affected by the various challenges iden-tified. Work has also been undertaken to explore the potential role of the FCA in addressing the identified access challenges, alongside that of the government and others.

This research was specifically intended to explore the impact of access challenges directly from consumers’ viewpoint – triangulating this evidence with the experi-ence and perspective of individuals from organisations who represent their interests, as well as some of those working within financial services. In addition, this report highlights consumer and expert perspectives on opportunities for change and im-provement that will help the financial services market to better address these issues.

Fieldwork was conducted in England, Scotland, Wales and Northern Ireland, be-tween July and November 2015. The research was qualitative in nature and consist-ed of a number of different strands, including:

• 50 x qualitative depth interviews

• 28 x expert interviews

• 6 x focus groups

9 Locked out?: Ex-offenders need better access to financial services, Centre for the Study of Financial Innovation, July 2015

10 Driving Down the Extra Costs that Disabled People Face, Extra Costs Commission, June 201511 Financial education for vulnerable young people: Report, All Party Parliamentary Commission,

October 2013

10 Mind the gap

3. Overview of findings

Access issues are extremely diverse and affect a broad range of different people, ranging from some of the most vulnerable to more ‘mainstream’ individuals with good financial literacy

3.1 A diverse range of issuesThe research identified a diverse range of challenges, barriers and problems affect-ing a huge variety of consumers. Many consumers, both with good financial literacy and those who struggle to understand financial products and concepts, have experi-enced some form of struggle or challenge trying to access a financial product. Such problems do not solely affect those on a lower income, with many wealthier consum-ers also experiencing a range of access-related problems. The difficulties also span many different types of financial product – including bank accounts, general insur-ance and protection and various types of credit and lending products.

Examples of the range of evidence uncovered by the research include: an elderly couple living in rurally located sheltered housing and struggling to access any bank-ing locally (and resorting to using doorstep lenders which they know are far higher cost than they should be paying); cancer survivors desperate to get some respite in warmer climes who can’t find insurers willing to provide cover; and foreign entrepre-neurs moving to urban centres across the UK, but struggling to set up banking due to prohibitive ID requirements. The research clearly demonstrated that access issues have an impact on everyday banking and insurance transactions for many people, up and down the country.

3.2 Access issues leading to gaps in the marketSome of the experiences studied as part of this research clearly illustrate the exist-ence of ‘gaps’ in the market, which can arise out of a variety of access issues. These are instances where consumers are simply unable to find a product that adequately meets their needs, and fall into two broad categories.

Firstly, some consumers were unable to find any products that suited their needs, de-spite undertaking extensive research through all recommended channels. Common causes included income, health conditions and place of residence. In these instances, there were simply not any suitable products available across the industry.

Secondly, consumers struggled to understand where they should search for products to meet their needs. In such circumstances, consumers were unable to locate prod-ucts through online searches or telephone enquiries. Specialist providers were poorly signposted, if at all, by more mainstream providers, and perhaps not prevalent on price comparison websites.

Overview of findings 11

3.3 Strategies for overcoming access problemsAcross the research, we saw a lot of evidence of consumers investing significant amounts of time and effort into overcoming access issues – demonstrating high lev-els of resourcefulness and coming up with inventive strategies. For example, one new bank account applicant who was struggling to open an account simply visited as many branches of the same bank as he could until he found a member of staff who had a more ‘problem solving’ attitude. Indeed, some individuals had managed to ‘solve’ their access problem simply by chancing upon the ‘right’ staff member; a person with the necessary knowledge, resources or ‘creativity with the rules’ to find a route through a problem. Customers with these experiences were often unclear as to whether their ‘access problem’ was actually more of a ‘customer service’ problem

– as there was often some sense lingering in their mind that if they could find the right staff member, who would listen and properly understand their situation, then there could be a potential resolution.

Regularly, however, strategies for overcoming access problems involved reliance on a third party (often a close family member or friend, but sometimes also individu-als with more transactional relationships to the individual – such as hairdressers or neighbours). Examples of this dependency on others included formal measures like

‘Power of Attorney’ or ‘Special Guardianship’ arrangements, but were also often in-formal – a child or grand-child supporting someone who struggles with the internet to do online banking, getting someone else to take out a product or account in their name and ‘lending’ it to you, or borrowing money from an informal community money lending scheme. Amongst older and more vulnerable people, the research encountered numerous examples of individuals handing over their debit cards and pins to third parties in order to get support using an ATM or chip & pin machine.

In some cases individuals were worried about their relationship with this third party – often feeling a sense of dependence, but also sometimes anxious about the risk they put themselves in. Equally, however, in many cases individuals had become acclima-tised to the potential problems – often feeling that they had no alternative.

“If I go into the bank they direct me over to the machines and say, now Madam… and I just think, I can’t do this. I don’t really know what it is. They’ve shown me a lot of times, but I just don’t know. So I just give them my card and whisper the pin. What’s the difference me doing that in the bank, to me doing that with my neighbour? I probably trust my neighbour more.” (Consumer, Yeovil )

3.4 What’s fair? Many of those customers affected by access problems not only felt let down by the financial services industry, but also by those with the power to make change happen. At an individual level, individuals regularly suffered chains of problems as a result of being denied access to products – and were often unclear about the reasons why. Many blamed themselves for not being able to ‘find’ the right product or provider for them, despite often having invested a large amount of time in searching and making applications, some even resorting to consulting industry bodies and other advice-giv-ing organisations. Others simply felt that financial firms had decided that they were not good customers (despite their willingness to pay for products!) and had lost faith that any firm would want to service their needs.

Many of those who took part in the research were frustrated by financial service providers and exasperated by a market where, on the surface, there seemed to be a wealth of choice, but as far as they could tell, there was ‘nothing for them’. Some individuals described the powerlessness they faced at ‘not being able to buy’, as they themselves can do little about market provision, and their struggles with a lack of appropriate products did not have an obvious way of being documented, reported or otherwise communicated.

12 Mind the gap

“Who do you tell that you can’t get access to a product? You don’t ever really know why, or if it was something to do with you or if it’s even the right or the wrong decision? What would you say?

‘They wouldn’t sell me something.’ Isn’t it their right to refuse to sell you something if they choose to?’ (Consumer, London)

For those consumers who are often excluded from the market, financial isolation can become a part of daily life. The feeling that you are not wanted as a customer, or not the right kind of customer for mainstream firms, can lead to self-limiting and self-destructive behaviours. Some individuals we met exhibited a strong sense of learned helplessness – often as a result of unfruitful searching or poorly explained rejections. This sense of helplessness frequently resulted in consumers distancing themselves from the mainstream market, rightly or wrongly seeing themselves as not

‘the sort of person’ who could ever be catered for by ‘normal’ providers. In the case of credit products (where there seem to be many providers clearly targeting those who feel excluded from the mainstream), many had given up on the idea of ‘choos-ing’ or ‘selecting’ products – feeling that they would probably never have that luxury. Instead, many relied entirely on ‘opportunity’ or ‘chance’ provision – e.g. going with a provider simply because they were in the right place at the right time, and made an offer of service (e.g. responding to a pre-filled credit application sent through the post or a doorstep lender knocking on the door).

3.5 Whose responsibility is it?A key feature of the access ‘landscape’ to have emerged in this research is the ex-istence of a self-perpetuating stalemate. Much of the discourse surrounding access issues – both at a personal level, between consumers and firms, and a macro level

– is characterised by a ‘blame game’, in which all of the possible agents of change (consumers, firms, government/regulator) point the finger at each other, ‘pass the buck’, or simply remain silent. Much of the time, it is this stand-off which allows ac-cess issues to continue to occur and, in some cases, intensify. With no single authority determining which problems are attributable to whom, uncertainty persists on all sides. For example, it could be that there are simply consumers that fall into ‘gaps between providers’. Equally, willing providers may exist, but it might not be reasona-ble to expect consumers to invest the time and resources needed to seek them out. In the current climate, even ‘rules’ themselves can be interpreted in a range of different ways. Some issues we studied were seemingly caused by poor, inconsistent or overly stringent interpretation of existing guidance – perhaps highlighting a lack of clarity about how exactly firms (or individual staff members) should respond when faced with complex situations or customers who don’t fit a ‘standard mould’.

The upshot of this status quo is that access often feels like an impossibly complex, al-most intractable problem. Our research, however, suggests that this may be mislead-ing. When seen in plain view, many of the problems we documented could actually have been easily resolved – benefiting firms and consumers alike – if simple changes had been made, particularly in terms of greater responsibility being taken by one or more parties. As for those which are more challenging, they too could have been mitigated (if not necessarily resolved in the consumer’s favour) if greater guidance and clarity had been offered to consumers at critical points in their journey.

Overview of findings 13

Behind it all lies the question of responsibility: whose job is it to address any given issue? The research suggests that while some problems are caused by firms’ policies, others arise from a dissonance between policy and frontline practice, while others still are the result of industry-wide impenetrability or inconsistency. Others may be regarded as the inadvertent consequence of rules and regulation designed to protect firms and/or consumers, while some are firmly the province of government – no-tably hard-and-fast questions about entitlement, inclusion, infrastructure and what can fairly be expected from consumers in terms of digital or financial literacy.12

3.6 Opportunities for change On the one hand, consumers recognise that much progress has been recently made in improving the way firms interact with consumers (e.g. the benefits that online and mobile banking have brought to many consumers; the growing sophistication of price comparison websites and ‘product finders’). At the same time, those affected by access issues feel frustrated and trapped by a financial services market without any real choice, or range. Many feel that there is little to distinguish between products offered by different firms, and those features which are different are often difficult to understand and compare.

When asked ‘who is responsible for ensuring you have the product you need’, con-sumers automatically default to financial service providers and banks. From their perspective this makes sense: they are simply a customer wanting to buy a product

– the solution therefore should lie with the seller. Despite the problems they expe-rienced, consumers often highlighted to us their understanding of the benefits of competition in keeping prices low and, despite struggling with the array of choices available, did appreciate the fact that a diverse range of different kinds of products were available.

Few spontaneously thought about the government or state being involved, whether to encourage a wider provision or to itself provide products that meet more niche or specific needs. When they did, consumers often found the idea of government prod-ucts unappealing, both in terms of trust but also potentially in functionality. Despite sometimes feeling overwhelmed by the choices available in the current marketplace, consumers were deterred by the very basic service offering which they imagined government products would offer, lacking the sophistication or features available in the private sector. The idea of intervention or encouragement was more warmly received, although there were some concerns about the effects of government in-volvement on competition, which many perceived to be a founding tenet of the UK economy and financial sector.

The current reality, however, is that with no coordination of the market or duty to provide, consumers can too easily be left in limbo. Gaps between policy and practice leave consumers and firm staff unsure of their rights and responsibilities, and often solutions are only to be found in the form of individual staff members who are will-ing to bend the rules.

In seeking to resolve these uncertainties and inconsistencies, we classified the access problems we encountered according to a simple new framework which does justice to access issues as they are experienced by consumers. In so doing, we suggest a range of potential opportunities for reducing the impact of access issues on consum-ers and firms alike – being clear, wherever possible, about where the responsibility for different issues appears to lie.

12 In thinking about the opportunities for change and improvement we identified three main areas of responsibility: firms themselves, consumers and ‘others’ (government/regulator – combined into a single category to reflect consumer confusion around the division of responsibility between social policy and regulation). Throughout this report, we use this categorisation to frame opportunities for change.

14 Mind the gap

4.1 Different ways of discussing ‘access’Arguably the biggest obstacle to those seeking solutions for access-related issues is the sheer diversity of the phenomenon – spanning not only the entire customer journey (from product purchase to product exit), but also different product types and sectors. From the literature review and expert interviews conducted as part of this research, it is clear that this range gives rise to three distinct strategies among those seeking to address the issue of access:

• Generalism: Simply discussing ‘access’ and the consumer right to ‘access financial services and products’ in general terms

• Specificity: Dealing with single issues or groups of related issues, often discussing the needs of a particular group they impact

• Cataloguing: Listing out all the issues, which can feel overwhelming, jumbled and inconsistent

Whilst each of these approaches has its merits in different contexts, none achieves the balance of depth, breadth and structure needed to make sense of the access co-nundrum as a whole.

4.2 The ‘layers model’ of accessTo overcome these challenges, we have classified the problems highlighted to us by consumers in a framework which we’ve called the ‘layers model of access’. In essence, it’s sampling a grouping of access issues by consumer experience and out-come, rather than by demographic or product type. The layers themselves are not discrete, but overlap. They also can be experienced simultaneously during any given access problem – and this lack of clarity in itself is part of the point, as it is often unclear where the ‘blame’ lies. As one consumer searching for an insurance product said to us: ‘How do you know when you’ve fully exhausted the search? At what point do you stop?’ – highlighting that she felt her access problems might not just have been caused by lack of provision but by simply not having searched hard enough (despite, in this case, the customer actually devoting many hours to the search over a prolonged period of time and seeking professional advice).

For the purpose of this report, we’ve outlined three layers:

• ‘The Maze’ – Process, requirements and eligibility

• ‘The Fog’ – Market navigation and comprehension

• ‘The Void’ – Physical and digital barriers

An important feature of this classification is that the problems belonging to each layer are causally distinct – in other words, each layer exists independently of the others in terms of the nature of the problem, and what is required (and from whom) to solve it. A consumer may experience problems across one or more of the layers – and occasionally across all three as part of the same product journey – but no one party (whether firm, consumer or government/regulator) can realistically be expect-ed to solve all types of consumer access issues.

Prevalence of issues Each of the layers encompasses problems which are very common and affected a wide range of consumers in our research sample, while also including barriers which were more niche, and specific to a certain group of consumers. Whilst some consumers only experience one aspect of the numerous challenges posed by access,

4. Making sense of access

Making sense of access 15

others can experience a range of different issues and challenges from all three layers.

Consumers in the latter category can find it particularly difficult to extricate the cause of particular problems and to work out a solution. Those who, for exam-ple, experience a range of physical access issues due to rural location and disability, could also see their situation compounded by a lack of suitable photographic ID re-quired to open a new account. Others may lack access to a computer or the skills to research financial products online, and therefore, when faced with more expensive deals, feel priced out of insurance policies.

Together, the full range of access issues experienced by consumers and explored throughout this work pose a clear problem to the financial services industry, regula-tor and government, as well as to consumers themselves. It is clear that much work needs to be done in order to ensure the diversity of barriers and challenges is effec-tively addressed in the future.

NOTE: As well as identifying the access issues encountered by individuals, this report aims to con-sider the future of financial access, and the responsibility which firms, consumers and others have in making this future fairer for all. For the purposes of this report we have identified three groups where responsibility and a need for action might lie: consumers, firms, and the regulator/government. Clarity of responsibility is crucial if consumers are to avoid being passed from pillar to post when it comes to their access challenges, and if real and meaningful progress is to be made in the future.

16 Mind the gap

Making sense of access 17

THEFOG Market navigation and comprehensionFinancial products are often communicated and marketed in a way which makes them more difficult for consumers to search for and to understand.

THEVOID Physical and digital barriersConsumers can get ‘stuck’ or be ‘blocked’ from accessing financial products and services because of physical ability or capability issues.

THEMAZE Process, requirements and eligibility

Complex and bureaucratic processes lead to a lack of transparency, or make it difficult for both staff and consumers to be clear what needs to happen in order to solve a problem. Certain consumer characteristics and circumstances can make obtaining a suitable product or service at an affordable price difficult or impossible.

18 Mind the gap

Summary of key problems experienced: 3 Jargon can be difficult to understand or can add further confusion

3 Products are difficult to compare as they use different terminology and concepts to describe features

3 Offers and introductory rates can mask the ‘true’ costs of products

3 Not easy to have ‘oversight’ of the whole market, with products from different providers more or less easy to find

Summary of key problems experienced: 3 Move to online can mean that consumers with poor digital literacy or limited internet access have increasingly limited choice

3 Customers with disabilities can struggle to access banking services that increasingly rely on technology or automated systems

3 Customers in rural areas may face long and/or costly journeys to visit branches

Summary of key problems experienced include: 3 Customers who have slightly unusual needs can challenge systems that are seemingly designed for ‘average customers’

3 Poor and inconsistent communication can leave customers ‘in the dark’ about what they are expected to do in order to overcome an access challenge or problem

3 Customers are unable to find tailored products for their needs at a price they can afford

3 Measures put in place to protect consumers from fraud can make access more difficult or impossible

Making sense of access 19

20 Mind the gap

5. ‘The Maze’ – Process, requirements and eligibility

Bureaucracy, rules and other measures – some of them designed to protect consumers – can add process complexity and pose additional barriers to access. Some consumers are simply not eligible for certain products, or eligible at a price they can afford

Across the various situations, products and firms we studied as part of this research, many consumers had encountered difficulty dealing with mandated procedures and reasoning, often experiencing ineffective support and guidance when trying to pick their way through the process. The research also revealed how the technical and bureaucratic requirements of certain products are clearly preventing people in par-ticular circumstances from obtaining products and services that meet their needs.

“They questioned about the source of the money for the deposit and it was a bit complicated, it came from a number of different inheritance pots from different grandparents. Ultimately we got turned down, and with no real explanation. It left us in a very difficult situation.” (Consumer, Poole)

5.1 Identification requirementsThe majority of misunderstandings and process complications came from Identification (ID) requirements. Importantly, these problems were experienced by a wide variety of different consumer types, in terms of financial literacy, vulnerability and background. Many of the challenges were wholly practical – distinct from any financial decisions around eligibility, and instead relating to unreasonable or even impossible demands, which prohibited customers from even being considered.

“It’s ridiculous that I can’t get a new account, just because I don’t have photo ID. I haven’t been abroad and I don’t plan on going, so why should I have to buy a passport?” (Consumer, Wales)

For many consumers, the seemingly illogical nature of these demands created genu-ine bafflement. Moreover, the need to then find a ‘way around’ obstacles whose pur-pose was unclear and which made no sense to them, demanded additional time and energy from a process which was often already quite stressful.

“We were just going round in circles a bit, because I really needed a UK bank account so that I could get set up to pay the deposit quickly on all of these flats that kept going so fast, but they wouldn’t let me have an account without post to the flat. But I haven’t got a flat yet! Eventually the university wrote a standard letter to one bank, and so we all just went there quick to get accounts.” (Consumer , London)

“They said I couldn’t have a bank account with them because my name was too long for their system.” (Consumer , London)

In some situations, consumers had found themselves unable to navigate the security measures required for online or telephone banking, on occasion being locked out of their accounts because procedures have been difficult to follow.

The Maze 21

“I have a poor memory related to Bell’s Palsy and I struggle to remember the answers to my security questions. If I hesitate too much or get an answer wrong or they hear someone trying to help me, the bank just hangs up on me.” (Consumer, Glasgow)

Others had felt embarrassed to make repeat requests for help or security informa-tion to be re-issued, perceiving themselves as a burden, an added cost to the service for others, or simply not ‘up-to-date’ enough to cope with the realities of modern banking. For some, the system was too difficult to manage without the help and sup-port of those around them.

“My mum just doesn’t understand how PIN numbers work. She tells the person in the shop what hers is, and so we were constantly having to request new ones from the bank. Now we get cash for her, and try to avoid the problem that way.” (Consumer, Leeds)

These problems came into particularly sharp focus for those in more unusual cir-cumstances – including both permanent and temporary living arrangements.

“I went into my bank to ask if I could get a proper bank account, because I wanted to get a mobile phone contract and they told me [in the shop] that I couldn’t do it without a proper bank account. But then the bank said I couldn’t get a proper bank account without proof of address. People don’t listen, especially if you’re living in a caravan and then how could you get proof of address? When you tell them you’re a traveller they look at you like you’re shit.” (Consumer, Brighton)

Whilst some of these individuals were in particularly difficult situations, such as ref-ugees fleeing conflict and looked-after children leaving the care system, others were simply coming to the UK to study, or to work.

Often those arriving from outside of the UK struggled to find acceptable proof of address without first moving into a rented property – yet they often encountered problems acquiring a property without a UK bank account. Others lived in proper-ties without being the named recipient of utility bills or without an accepted tenancy agreement.

“Almost every firm has an alternative list [of ID]. And so what we’d really like to see is people asked instead ‘How can we help you get the right ID?’ ” (Expert interviewee)

For many, however, the most confusing aspect of the processes around ID verifica-tion was the different and conflicting information given by various firms. Indeed, for the most part, consumers’ problems – and their ease of resolution – had less to do with their own characteristics and abilities, and more to do with the inconsistent at-titudes and responses of branch staff. Not only did consumers have experience of different staff at the same firm being more or less helpful, but they also received con-tradictory messages. Moreover, there was an awareness among consumers that some staff were happier than others to bend or ‘be creative’ with rules and regulations.

Conscious of these variations, one respondent trawled seven different branches of the same high street bank before he found someone willing to take a more detailed look at the ID he was able to provide.

“Nobody was willing to look or engage their brain. In the end it turned out to be OK. They gave me a really basic account that you could only withdraw limited cash from. I just needed someone to look at the problem and say ‘you know, this is probably something we can do something about’.” (Consumer, London)

Aside from the frustration and confusion that arises with inconsistencies in staff ap-proaches, the willingness of some more sympathetic staff to adapt to some consum-ers’ needs suggests an awareness and acceptance that existing procedures are not designed as flexibly, intuitively or intelligently as they should be – further supporting the claims of some of in our sample that certain identification requirements simply do not work for those in particular circumstances (both mainstream and niche).

22 Mind the gap

5.2 Procedural support and guidanceMany of the process-related problems we encountered were made worse by the in-effectiveness of related support and guidance, which customers often found to be unclear, unhelpful, contradictory or simply insufficient.

On some occasions, consumers were left dealing with the consequences of being giv-en outdated, contradictory or inaccurate information about how to solve a problem. Frontline staff were often unable to resolve queries, or did not possess the knowledge to signpost to other potential sources of support and information.

For example, respondents who had no passport or photo ID were offered no further advice or support. In the case of one respondent:

“[The customer service assistant] just said ’Well, I see your point. I’m not sure what the answer is, it’s a bit of a catch 22 isn’t it!’ which wasn’t very helpful.” (Consumer, Manchester)

“We might see someone who’s homeless being told, ‘You must have a passport, go away and get one and that will cost you £80,’ and of course that person hasn’t got the proof to get a passport in the first place and they certainly haven’t got £80.” (Expert interviewee)

Language barriers are also a problem for some consumers. Translation require-ments differ from firm to firm. Some will allow a friend or family member to trans-late, while others will only permit this if the friend/family member also holds an account with the firm. Others still will demand a certified translator. Where they are given some help, consumers are often signposted to other sources of support such as local charities or a Citizens Advice Bureau, which may or may not be able to provide them with the services they require.

“When I asked them if it was possible to get a translator to help open a bank account, they said we’d need to get a list of ‘approved translators’ from the library. The library said that they hadn’t provided this service for about 18 months and that we should try the council. The council provided the number of a company who supplied translators to businesses. The company said they could only be referred by the company directly, so back to the bank. And then they just said no.” (Ethnographic research, Bradford)

These challenges of complexity and confusion were further compounded by the number of potential sources of information available to consumers, many of which are contradictory. Many of those we interviewed were triangulating help and advice received from frontline staff with information gathered from online sources, alterna-tive providers and friends and family.

5.3 Exclusion due to ineligibilityAlongside those consumers who experienced exclusion due to process were those who had successfully negotiated the bureaucratic ‘maze’, only to find themselves un-able to find a product suited to their particular needs and circumstances.

In many of these cases – and particularly regarding insurance – this was related to long-term illness or medical conditions, with risk assessments often felt to unfairly reflect reality.

“We aren’t going on holiday this year because I just cannot get any travel insurance cover, and we just won’t go without. Everyone I called said that my arthritis is just too bad this year.” (Consumer, Watford)

Geographic location can also play a role in ‘pricing consumers’ out of the insurance market.

“Our insurance, if we had it and we don’t, would be expensive because it’s a bad area. People get burgled and cars get burnt out a lot. There’s no way we can afford to have contents or something like that.” (Consumer, Manchester)

The Maze 23

‘Thin’ credit files were also a problem for some of those in our sample – creating par-ticular difficulties when accompanied by ambiguity about what exactly the nature of the problem was, leaving customers uncertain as to how best to ‘fix’ their situation in future.

“I got refused and they led me to believe that I had bad credit. In reality, I probably had no credit history. I wish they had told me things like going on the electoral role or getting a phone contract would help.” (Consumer, Glasgow)

Affordability per se also plays a key role in excluding consumers from the financial services market. Even those with access to the widest available range of products (i.e. able to access both digital and physical offers) sometimes struggled to access func-tional bank accounts due to their low level of monthly incomings.

“I wanted a proper bank account, like one you can use the card for anytime and anywhere, and that lets you go into the red and stuff. But I couldn’t get a proper one because I don’t get £800 going in a month. It’s better than the Post Office but it’s not proper.” (Consumer, Bolton)

Allied to these affordability ‘gaps’ were issues around the perceived value of products. Some less affluent consumers were simply unable to see how insurance was relevant and valuable to them. Aside from motor and buildings insurance, other policies were often described as an outgoing that wasn’t completely necessary. Consumers strug-gled to see the value of such products to their everyday lives, and were cynical about their worth in relation to other commitments.

“I just look at our monthly outgoings and there isn’t much room for an extra £30 on contents insurance that I’m pretty sure in the majority of cases they’d find a reason not to pay out or it would take weeks on end to get sorted.” (Consumer, Epsom)

Importantly, these ‘ineligibility’ exclusions were not just limited to customers seeking to access new products; they also applied to those who had successfully obtained a product, only to discover that they were excluded from accessing specific product services or features – notably insurance claims.

“I wanted to reduce the premium slightly, to make monthly outgoings easier to manage. But they said I can’t change anything on my policy without being a new customer, and if I do that they won’t cover me for existing conditions. But I’ve been treated, with them covering it, in the past year. So I can’t have that or what’s the point of the policy?” (Consumer, St Albans)

The challenges posed by ‘in-product’ exclusions such as these are twofold. On the one hand, there is the technical issue itself to consider (i.e. the justification for deny-ing a person the product they seek, at a price they can afford); on the other, there are the cultural factors which give rise to consumers’ misunderstandings. In particular, we found that many in-product exclusions were caused by the difficulty customers experienced in accessing and/or understanding the full range of product T&Cs – and firms’ role in failing to clarify these – at the point of purchase. This phenome-non, which may be considered a symptom of the complexity and confusion which characterises the marketplace at large, is explored in greater detail in the next chap-ter (‘The Fog’).

5.4 Explanation of denial or rejection For many consumers who are unable to access the product or service they need at an affordable price, their difficulties are compounded by a lack of clear explanation as to why they have been denied. This is particularly true in relation to credit, insur-ance and current accounts. Beyond the short-term panic and confusion sometimes caused by such occurrences, this issue can also lead to self-limiting behaviours – for example, applying in future for higher-cost, lower eligibility products, or to damag-ing behaviours such as repeated applications for credit.

24 Mind the gap

“I just keep trying and trying and trying. Surely someone will give me a credit card eventually!” (Consumer, Birmingham)

Poor explanations, and a lack of consumer understanding as to the reasoning be-hind their rejection, ensures that behaviours are not changed for the better. In order to learn from a situation and be in a stronger position for an application in the future, consumers need to fully and precisely understand why they have been turned away.

Where consumers are unable to take out an insurance product, for example, there is often a lack of explanation as to the influence of prior, legitimate claims on such a decision. This can lead to consumers feeling powerless and excluded from the mar-ket, with no clear sense of how to improve their eligibility – or when the issues they face might cease to be a problem.

“So I’m asking for a quote after doing all the right things and looking at the best-rated contents provider, etc. And they’re just refusing to even provide a quote! Most people would have given up but I persevered and it was only after I complained they said they wouldn’t quote because I’d claimed three times in the past five years, on different policies.” (Consumer, Devon)

Similarly, it is important that consumers do not have their worries compounded by reference to indistinct or irrelevant issues. Vague mentions of ‘credit reference agencies’, for example, can push consumers towards higher cost options, or imply that credit is poor when consumers have in fact been turned down for other reasons.

“It said: ‘We consulted a credit reference agency’. I wasn’t asking for any credit, just a current account, and I know my credit is good! So I panicked. Why didn’t they want me?” (Consumer, London)

Some older consumers reported difficulties accessing mortgage products, possibly as a result of misinterpretation or inconsistent application of the rules regarding affordability checks. Often this led to confusion for the applicants, who did not per-haps see themselves as ‘too old’ for a new mortgage or mortgage product.

“They said they wouldn’t give me the mortgage, despite it being for only 25% of the property value and me having more than enough salary wise. It was because of my age, but it was a ridiculous decision. They should have been able to easily see that I could pay it back.” (Consumer, Watford)

Consumers are adept at post-rationalisation and easily jump to conclusions about their eligibility, some of which later prove to be detrimental. Signposting to alter-native providers, therefore, is an important opportunity to help to alleviate con-sumer reactions and concerns in the event that services or products are refused or unaffordable.

“The lady did actually say: ’Look, we can’t cover you but we know someone who probably can.’ She said she shouldn’t really tell me but I’m so glad she did, as they covered me and I can keep driving now.” (Consumer, Watford)

Where services are withdrawn after an initial acceptance – for those with convictions, for example – the combination of a lack of full explanation and a lack of suggested alternatives can leave consumers in particularly challenging circumstances.

“Just out of the blue I get this letter saying that’s it, you’re done. They’re terminating my banking with them because of information about me that is apparently in the public domain. Well I’ve been out of prison [ for a fraud conviction] for two years, so why not terminate it earlier? I disputed it as my case is being reviewed [by Criminal Case Review Commission] but they just said no. So what am I supposed to do now?” (Consumer, London)

In analysing these particular issues, the underlying challenge that emerged is that no one body – whether a firm or intermediary organisation – currently feels compelled to take responsibility for outlining to consumers why they have been turned down for products, and providing advice, if requested, on how consumers could make them-selves more eligible for products in the future.

The Maze 25

Addressing this issue, and ensuring roles and responsibilities are clearly outlined, may help to reduce self-limiting behaviours among consumers, and better help them to develop their own eligibility for mainstream products which could potentially serve their needs well.

“When you start getting turned down, it’s easy to just assume that everyone is going to turn you down. They [firms] don’t give the impression that someone else might be able to help – it’s kind of a firm ‘no’”. (Consumer, Birmingham)

5.5 Summary• There are often practical barriers to accessing financial products, in particular

relating to the provision of the required/requested ID documentation

• Staff often give consumers contradictory or limited information on their options, and messaging can change between firms, and even between branches

• Consumers can struggle to understand and use their products once they have purchased them

• A lack of explanation as to why someone has been denied a product – along with a lack of suggested alternatives – can lead to future self-limiting behaviours

• Issues relating to income, health and place of residence mean that, for some, there are simply no products available that meet their needs

26 Mind the gap

5.6 The Maze: Opportunities for change and improvement Firms

• How can firms be honest and upfront about exclusions and rejections, without compromising their rules and the regulation in question?

• How can firms/trade bodies monitor customers’ experiences of using their products and services? For example, the customer journey of trying to find suitable and/or affordable insurance products which even the most savvy of consumers struggle with?

• Firms need to better support their frontline staff to ensure all are comfortable and familiar with procedures, and information and advice is therefore consistent across branches and between members of staff. Who is best placed to encourage this?

• How can staff provide appropriate advice and support when consumers have been rejected, in order to help them improve their future chances of acceptance?

Consumers • In what ways can we better support consumers to make effective choices about

financial products and find products that suit their needs when even mainstream consumers, who have relatively good levels of financial capability, struggle?

• Is the guidance available to consumers accessible and appropriate to meet the wide range of individual needs?

• What can we reasonably expect consumers to understand around rejections?

Government / Regulator / Other• When regulation is imposed on the financial services industry, is there clarity

around what the expected industry response is, and a chance to review any difficulties and unexpected consequences?

• Both expected and unexpected consequences of even the best intentioned regulation must be regularly monitored and tracked.

• When it comes to ID, how can the regulator and government work together to create clarity about acceptable documentation and/or encourage firms to better serve those consumers without the most standard forms of ID?

• What is the role of the regulator and/or government when it comes to supporting firms to signpost consumers to alternative providers when they are unable to provide a product or service?

• What is the role of the regulator and government when the market does not seem to be providing consumers with suitable products at an affordable price, even after comprehensive searches by many consumers?

The Maze 27

Fedyenka is a businessman (half French, half Russian), looking to relocate his technology start-up to the UK from Paris. When he arrived, he made it a priority to look up banks with the best business services, aiming to open both a personal account and a business account. He made appointments at 7 different banks, aiming to identify the ones with the best customer service. Out of the 2 who managed to keep their scheduled appointment time, neither were able to help or offer any guidance about how Fedyenka could open an account with the range of ID documents he currently had, despite the fact that he had assets in French accounts. In the end he went from branch to branch until he found a bank employee who had experienced a situation like his before, and was a bit more solution focussed. The whole process wasted a lot of time and effort - leaving him feeling that the UK was not ‘open for business’.

London

Age:27 Occupation:Entrepreneur Living situation:Livingalone

Product area:Retailbanking(personalandSME)

Journey stage:Application

Fedyenka’s story Facts about Fedyenka

THE MAZE

Fedyenka:Poor customer service and inconsistent information about ID requirements when setting up a bank account.

THEMAZE

THEVOID THEFOG

Ididn’tneedthemtojusttellmewhatwasthere,I need them to problem-solve,tohelpmeworkoutwhatwaspossible

28 Mind the gap

“Idon’ttrustthatthepolicywillactuallycovermeforwhatIwillneed.Iunderstanditwon’tcovermycondition,butthey have given themselves a very convenient get-out clauseanddidn’texplainittomeupfront.”

Alan suffers from a congenital heart problem, which was treated when he was a child many years ago. He recently purchased a critical illness policy, as “the sensible thing to do” now he is in his 50s and still the main income earner in the household. Alan did not expect to be covered for his illness but upon receipt of his policy and a read-through of the T&Cs he was disappointed to see he was also not covered for “any associated conditions”. This was not explained to him when taking out the policy and it was not clear what these associated conditions were, which left him feeling that the policy was virtually worthless.

Unexpectedly excluded from claiming on many aspects of a policy due to an existing healthcare condition

Ala

n

Leed

sIn

sura

nce

| U

sage

“I couldn’t believe it!Theywouldn’tgiveusthemortgageandIwassoconfidentwecouldpayitback,andIdidn’tfeellikeweposedarisk.Peoplelikeusdon’tnormallygetturneddownforthings.”

Simon and his wife are becoming unable to manage the upkeep of their large family home. Their children have moved out, and Simon’s wife struggles with arthritis. They decided to downsize to a more manageable flat, close to their family and with security to reassure them in their old age. Simon made an appointment at his local bank branch to enquire about taking out a mortgage for around 25% of the property value. He was asked to bring in records of his income, which primarily comes from his property business. After a protracted process of proving his income and submitting accounts, Simon was eventually refused a mortgage on the basis of his age and ‘unreliable’ work status.

Turned down for a mortgage because of age

Sim

on

Wat

ford

Mor

tgag

es |

App

licat

ion

“We were in a panic,thesellerwantedtomovequicklyandweweregoingtolosethisplace.Weaskedthebanktospeakdirectlytooursolicitorwhocouldworkoutwhatdocumentswereneededtoprovewherethemoneycamefrombuttheyrefusedandwithdrewtheoffer.”

Last year, Kate (and occupational therapist) and her husband (a teacher) found the perfect home. They had been searching for months because Kate has a disability and they needed to find a bungalow close to their family. Kate had recently inherited twice and her husband had also had an inheritance to use as a deposit on their new property. They had an Agreement in Principle for a 20% LTV mortgage when they placed their offer, however a few weeks later the mortgage was withdrawn due to money laundering regulation as the firm felt they could not prove where their inheritance money come from. Kate and her husband were at risk from losing their new home and the process of applying to a different firm would take too long. Eventually, Kate’s parents offered to lend her the money instead.

Turned down for a mortgage because of difficulty proving the source of inheritance

Kat

e B

our

nem

out

hM

ortg

ages

| A

pplic

atio

n

“It was a mess.Differentbranchesofthesamebankweretellingusdifferentthings.Intheend,Ihadtoasktospeaktoamanageranddemandtheydidsomethingforus.”

Josh and his wife came to the UK at the start of 2015 when his wife’s employer transferred her to their London office. When they arrived, they brought around £4000 in cash with them to live on whilst they were setting up bank accounts and waiting for their first pay cheques. Josh and his wife hid their money in among their clothes to keep it safe. When Josh and his wife tried to open an account they were turned down due to lack of proof of address because they were staying in a temporary rental apartment. Different branches of the firm that they were dealing with gave them different information about how to obtain proof of address and what was acceptable. Several weeks later, the firm finally let Josh’s wife open an account using her employment contract as a form of ID, during this time they lived on the cash they had hidden. It took a further 6 months for them to allow them to open a joint account and for Josh to get a debit card of his own.

Inconsistent information and long delays in setting up a UK bank account

Josh

G

uild

ford

Cred

it &

Reta

il Ban

king

| Us

age

Fiona made three legitimate claims on 2 different buildings & contents policies over a 3 year period. Once looking to renew, she discovered that the vast majority of providers would not provide her with a quote due to her claim history. Fiona is now unable to switch providers or negotiate a cheaper premium for her buildings & contents cover, and has been discouraged from making any further claims (even if legitimate) as she is unsure how they will affect her in the future.

Limited options for buildings & contents cover due to previous claims

Fio

na

Exe

ter

Insu

ranc

e |

Usag

e

“Whatisthepointofhavinginsuranceifyoucan’tuseittoclaimon?I did everything rightfromaresearchpointofview,Ifoundthetoprecommendedinsurers,buttheywouldn’tevenprovideaquote.”

The Maze 29

30 Mind the gap

For many consumers, each with varying degrees of education and confidence, the financial services market is complicated. For some this involves confusion about the amount of products available, how best to search for them, and understanding the differences between them. For others, there are questions around the differences be-tween product categories. The advent of internet search engines and comparison websites has brought the consumer face-to-face with the most diverse range of prod-ucts ever available, and consumers can often feel overwhelmed by the sheer number of potential options. What is more, despite a seeming plethora of options, some con-sumers can struggle to identify products which aren’t aimed at the ‘ideal consumer’.

6.1 Accessing and comparing product details Consumers often feel that it is simply impossible to understand the ‘whole market’, and therefore to conduct an exhaustive search of it. Many are perplexed by the va-riety of providers, before they have even begun to think about the detail of different product categories and the features of each individual product within such a cate-gory. A standard consumer response has become to say “I understand a little” or

“as much as I need to”, demonstrating the kind of ‘fog’ that envelops much of the market, leading to a lack of confidence when it comes to making effective choices.

“I mean, I think I’m ok but I wouldn’t say I’m particularly good at financial stuff or understand everything. Definitely not. There’s so much out there I don’t think anyone really gets all of it.” (Consumer, Birmingham)

Once consumers move from looking at the market in its entirety, they are further confused and intimidated by the features of specific products. Whilst many are con-fident understanding the basic features, there remains a fear of hidden costs and limitations that are not clearly explained. The ability to compare products when as-sessing upfront features often disguises consumers’ inability to compare across a full range of features, and thus conduct a thorough and comprehensive search of the market. For these reasons, it is not always easy to work out what constitutes value for money in a particular context, or for a particular product. Even when using price comparison sites to compare different products and their individual features, many consumers still feel that they are not getting to the bottom of what a product entails.

A particular pain point for consumers centres on the ‘cost’ of products and whether or not they offer ‘good value for money’. Many stated that their strategy for choos-ing a product was simply to go for the option that “seemed to fit their needs”, “was middle of the market” (i.e. not too expensive, not too cheap), and was provided by

“someone they had heard of ”. Whilst exciting, new and enticing product features are shown on adverts, comparison sites and discussed by family and friends, the ‘small

The way financial products are communicated and marketed can make it difficult for consumers to understand and identify the right products for them

6. ‘The Fog’ – Market navigation and comprehension

The Fog 31

print’ of fees and charges was felt to make accurate comparison very difficult, even for those who were willing to put in the effort. The relative difficulty of finding out this sort of information only serves to make consumers more wary and/or confused by the product and less able to compare across similar products.

“They always have all the good stuff there in big type and it’s all shouty shouty. But the bits you really need to see, like how much they’ll charge you to be in your overdraft, you can never find that bit!” (Consumer, Birmingham)

“The issue of course is that marketing is trying to get us to buy, so it’s highlighting all of the benefits, but people need to know the risks too.” (Expert Interviewee)

“There isn’t clear information about how much products are going to cost or how they’re going to work. When you’re taking out the account, anticipating problems isn’t built in to [the process] so something that’s supposed to help you manage your money undermines your ability to do that.” (Expert interviewee)

What is more, price comparison sites do not always show or highlight the more niche providers of certain products, and consumers may therefore not be able to use them in order to conduct a comprehensive search of the whole market for the most appro-priate product. Many consumers are not willing or able to pursue a lengthy process of methodical searching across all providers, particularly if they are likely to face multiple rejections along the way.