minimum variance portfolio: the art of constraints - ossiam · minimum variance portfolio: the art...

TRANSCRIPT

OSSIAM RESEARCH TEAM

Minimum variance portfolio: the art of constraints

May, 16, 2013

WHITE PAPER

1

Minimum variance portfolio: the art ofconstraints

Ksenya Rulik

May, 16, 2013

Abstract

Ksenya Rulik, PhD, CFAHead of Quantitative [email protected]

Minimum variance portfolio is an attractive theoretical op-portunity to have equity-like return with less market risk.However in practice such portfolios have complex design asminimum variance engine needs portfolio constraints to putthe concept at work. Investors face today a broad offer ofminimum variance methodologies, so how can one comparethe different implementations and evaluate what constraintsare really needed in minimum variance portfolio? We showin this paper how to read the constraint map and ensure thatthe necessary is made to make minimum variance enginework. We also list extra constraints that one encounters inexisting minimum variance methodologies and discuss howthey impact the ability of the strategy to reduce volatilityand improve diversification.

Minimum variance portfolio: the art of constraints

2

Minimum variance portfolio: the art of constraints

3

Introduction

In the aftermath of the global financial crisisefficient use of risk budgets became a prior-ity for many investors. Minimum variance in-vesting, that attracted a great deal of atten-tion in this regard, allows achieving risk re-duction via selecting stocks with high diver-sification potential: low volatility and/or lowcorrelations to other stocks. Minimum vari-ance uses the principle of portfolio optimiza-tion introduced by Harry Markowitz and is afully invested portfolio with minimal possiblevolatility. However the sound theoretical prin-ciples behind minimum variance approach arenot enough to build a real-life minimum vari-ance portfolio. Optimization procedure is sen-sitive to estimation errors in stock volatilitiesand correlations. Numerous solutions to theproblem exist, including cleaning of covariancematrix with advanced statistical methods andportfolio resampling techniques. But the mostwidely used solution was and remains the use ofportfolio constraints that allow redressing thebiases in the optimized portfolio. Hence, min-imum variance, as any other optimized portfo-lio, can benefit from a wisely devised constraintset. But what constraints should be imple-mented? It happens that different providersof minimum variance solutions have no con-sensus on the subject: existing minimum vari-ance methodologies have different design, andas a result quite a few differences in the riskand performance of the respective minimumvariance portfolios. This article provides anoverview of the minimum variance investingapproach that is a part of a wider trend calledalternative beta. We attempt to give investorstools to interpret the constraints in the context of minimum variance portfolio and com-pare different minimum variance methodolo-gies.

Alternative beta story

Why should investors be interested in strate-gies like minimum variance? Passive in-vestment industry is currently dominatedby market-capitalization weighted portfolios,called simply market portfolios or traditionalbenchmarks. Their popularity amongst in-vestors is to a great extent due to the statusof efficient portfolio that the market alloca-tion has in the Capital Asset Pricing Model(CAPM), the classical financial pricing theorydeveloped in 1960s. Today investment indus-try remains faithful to the mark et portfolioparadigm notwithstanding the important ad-vances in financial theory since the CAPM.One of the crucial findings of academic researchsince 1970s is the empirical inefficiency of mar-ket portfolio. From a theoretical standpointthe attack on the CAPM came first throughunrealistic nature of some of its assumptions.Real markets can hardly be approximated bya homogeneous group of investors with simi-lar views and no investor-specific constraints,and an entire field of behavioral finance devel-oped around irrationality and biases of marketparticipants. Another weak point of CAPMturned out to be the replication of the truemarket portfolio. Indeed, CAPM advocatesefficiency of a global market portfolio, ag-gregating all the possible risky holdings in-vestors can have. In reality, investors can ac-cess only market proxies, often in the formof narrow regional indices. Finally, impor-tant pricing anomalies were discovered in the1990s, following the work of Fama and French(1992). It is widely admitted nowadays thatrisk factors other than the market affect stockreturns: value, size, momentum, and lateron, volatility. Following these theoretical ad-vances, a family of new approaches to efficientpassive investing was developed, known un-der the name of alternative beta. Alternativebeta portfolios address inefficiencies of mar-

Minimum variance portfolio: the art of constraints

4

ket capitalization-weighted benchmarks: thestrategies employ systematic rules in portfo-lio construction aiming at adding to the broadmarket beta an extra (risk- adjusted) benefit.It is common to distinguish several subgroupswithin the alternative beta family: risk-basedapproaches incorporating risk management ob-jectives in portfolio construction (such as min-imum variance and risk parity), fundamental-based strategies built upon return forecastsbased on micro or macroeconomic data (suchas Fundamental index and weighting by GDP),and diversification-based approaches that ig-nore completely return as well as risk forecastsand concentrate on smoothing the distributionof portfolio weights (such as equal weight ap-proach). Alternative beta strategies and mini-mum variance in particular, are meant to bebroad portfolios and are not dedicated to anarrow investment theme or a specific sector.This distinguishes them from style portfolios,like value and size, as well as from narrow sec-tor benchmarks. While the concepts behindthe alternative beta strategies are widely dis-cussed, the constraints that play an importantrole in definition of the alternative beta port-folios are often left out. However it is due toconstraints that the strategies can be imple-mented in a systematic way, remain diversi-fied notwithstanding unfavorable market con-ditions and mitigate risks that are not con-trolled by the investment model, such as liq-uidity risk and estimation risk. Without theconstraints one is forced to introduce discre-tionary human oversight, and thus foregos agreat deal of transparency and investment dis-cipline that is a clear advantage of passive in-vesting.

Minimum variance portfolio:the basic setup

Technically, to construct a minimum-varianceportfolio one needs a forecast of covariancematrix and an optimization engine. The lat-ter is a mathematical procedure that decideswhich stocks to pick and what weights to givethem to obtain the lowest possible volatilityof the overall portfolio. As the smallest pos-sible risk is an exact zero, one needs also aconstraint that forces the allocation to be non-empty, such as the budget constraint forcingthe sum of weights to be equal to one. Furtheron, to have a broad investment benchmark onewould like to avoid having negative weights inthe minimum variance allocation. This moti-vates the second necessary constraint: no shortsales.

Diversification constraints

The basic configuration: a covariance matrix,an optimizer and the two constraints above,give an essential minimum variance portfo-lio. This is not enough however for an in-vestment benchmark for two reasons. First,common sense as well as the financial regu-lating authorities suggest that a financial in-dex should satisfy a set of diversification cri-teria. A basic minimum variance portfolio hasno control over diversification and is too con-centrated to be an eligible investment bench-mark. Moreover, an extreme concentration inminimum variance allocation is often a conse-quence of underestimation of expected covari-ance, so some stocks seem too attractive to theminimum variance algorithm. Here diversifi-cation constraints bring additional benefit ofreducing misallocations due to the estimationnoise. There exist two main types of diversi-fication constraints: limiting maximal weightper stock or targeting diversification in terms

Minimum variance portfolio: the art of constraints

5

of effective number of assets, that is the ex-act number of assets required to construct anequally-weighted portfolio with the same con-centration1 . The constraints in effective num-ber of assets (that are quadratic in portfolioweights), have several advantages with respectto the maximal weight limits (that are linearin weights). In particular, the former allowconstructing more diversified portfolios for agiven level of maximal weight, as well as pre-serving the information on the relative riski-ness of stocks that is usually erased by con-servatively low weight limits. Here we give anillustration of the diversification achieved byboth methods. On Figure 1 we show the levelof diversification of minimum variance portfo-lios constructed using the two different typesof diversification constraints.

Figure 1: Maximal weight limit versus target-ing effective number of assets. Source: Datas-tream

The portfolios on the blue line were op-timized using the linear constraint with themaximal weight threshold gradually shifte dfrom 1% to 15%. The portfolios on the redline were constructed via optimization withthe quadratic diversification constraint target-

ing effective number of assets ranging from 10to 100. For any given level of maximal weightthe red portfolios are more diversified than theblue ones. For example, if one targets the max-imal weight of 5%, the hard limit of 5% willresult in a portfolio of 20 effective assets, whilethe same maximal weight is respected by a redportfolio that is two times more diversified.

Liquidity Risk

The second reason why one needs more so-phisticated minimum variance portfolio con-struction than the basic setup is the controlover invisible liquidity risk. This risk is notmeasured by stocks volatility, and thus theoptimized portfolio might allocate large posi-tions to rather illiquid stocks. This can be ad-dressed by adding explicit constraints in termsof stocks absolute or relative liquidity. For ex-ample, one can set a threshold of minimumaverage daily volume that future constituentsof minimum variance portfolio should exhibit.Relative thresholds however work better (e.g.selecting N most liquid stocks from the un-derlying universe), as this keeps portfolio con-struction free from predefined levels expressedin currency units and suits to a portfolio ofarbitrary size. The liquidity screening is bet-ter being done before the launch of the opti-mization process, and not by fine-tuning theoptimal allocation eliminating illiquid stocks.The reason is simple: posterior adjustment ofminimum variance composition makes it sub-optimal, and there will be always another port-folio with the same level of liquidity that willgive smaller volatility than the one of the read-justed portfolio. As an alternative to liquid-ity screening, some providers impose limitson portfolio turnover. However this addressesonly partially the liquidity risk. Turnover con-straint helps to reduce the risk of treating toobig orders in illiquid stocks at once; however

Minimum variance portfolio: the art of constraints

6

it does not prevent the strategy from gradu-ally accumulating important positions in thesestocks. This constraint also introduces a pathdependency, so that optimization today de-pends on the portfolio composition yesterdayand further back into the past.

Summary of necessary con-straints

An investor willing to allocate to minimumvariance and get market beta return with re-duced market risk, would be interested in thefollowing necessary set of conditions to get arobust portfolio:

• full investment, or budget constraint

• no short sales

• diversification constraint

• liquidity constraint

Minimum variance portfolio with necessaryconstraints will be somewhat more volatilethan an equivalent portfolio with, for exam-ple, only a budget constraint. Each additionalconstraint forces the solution to depart fromthe true volatility minimum, at least ex-ante.However, this volatility increase is a price onepays for a robust and controlled investmentprocess that can be implemented in a system-atic way and result in a diversified and in-vestable minimum variance benchmark.

Minimum variance portfolio:extra constraints

Once the necessary setup is respected, one canadd few other constraints to pursuit additionalinvestment objectives. Two words of cautionhere: first, any additional constraint raises theportfolio ex-post volatility, as it drives the al-location further away from the true volatility

minimum; secondly, it is worth checking if ex-tra constraints are not in conflict with one ofthe necessary constraints imposed, or with themain objective of the optimization: volatilityreduction.

Sector and country constraints

The most common extra constraint is limit-ing sector and/or country exposure. This con-straint actually can be considered as one of thenecessary ones if implemented in an objectiveway. Limiting important factor exposures al-lows th e portfolio being more representativeof the broad market beta and limits the riskof becoming a single-sector bet. However, thisrisk is limited if the thresholds for sector orcountry exposures are not variables out of thestrategy control. An example is limiting sec-tor allocations to be within a certain rangearound the current sector exposure of the mar-ket capitalization-weighted portfolio. In thiscase there is no guarantee that exposure to asingle sector will not peak following a marketbubble.

Individual security capping rel-ative to its market capitaliza-tion

This type of constraints is used in the firstplace to approach minimum variance portfo-lio to the market capitalization bench mark.A clear secondary objective here is to reducethe tracking error of minimum variance port-folio vis--vis the market portfolio. An exam-ple of this constraint is limiting a stock weightto be not more than twice of its weight in themarket cap portfolio. Indirectly this constraintalso aligns the sector and country exposures ofminimum variance portfolio to that of the mar-ket portfolio, and addresses to some extent liq-

Minimum variance portfolio: the art of constraints

7

uidity concerns.

Impact of constraints on port-folio volatility

To estimate the impact of the extra constraintson volatility of the minimum variance port-folio, we selected four commercially availableminimum variance indices that are constructedfrom European stocks and based on differentconstraint sets. The indices are:

• STOXX Minimum Variance Uncon-strained and Constrained Indices (SAX-PUNP and SAXPMVP)

• iSTOXX Europe Minimum Variance In-dex (ISEMVP)2

• MSCI Europe Minimum Volatility Index(MXEUMVOL)

The Unconstrained minimum variance indexof STOXX (SAXPUNP) has the simplest con-struction and can be viewed as a proxy ofthe necessary constrained setup without ex-plicit liquidity constraint. The index includesbudget, no short sales and diversification con-straints, along with a limit on rebalancingturnover of 5%. The next in terms of con-straint complexity is the iSTOXX Europe Min-imum Variance index (ISEMVP) that includesnecessary constraints with a relative liquidityfilter, as well as one extra constraint: limit-ing the weight of each sector to a maximum of20% of the portfolio. Further on, the STOXXEurope 600 Minimum Variance Constrainedindex (SAXPMVP) adds sector, country andfactor constraints relative to the STOXX Eu-rope 600 market capitalization-weighted index.And finally, the most complex of the four,the MSCI Europe Minimum Variance index(MXEUMVOL) adds an additional constrainton individual security capping vis--vis its mar-ket cap counterpart3.

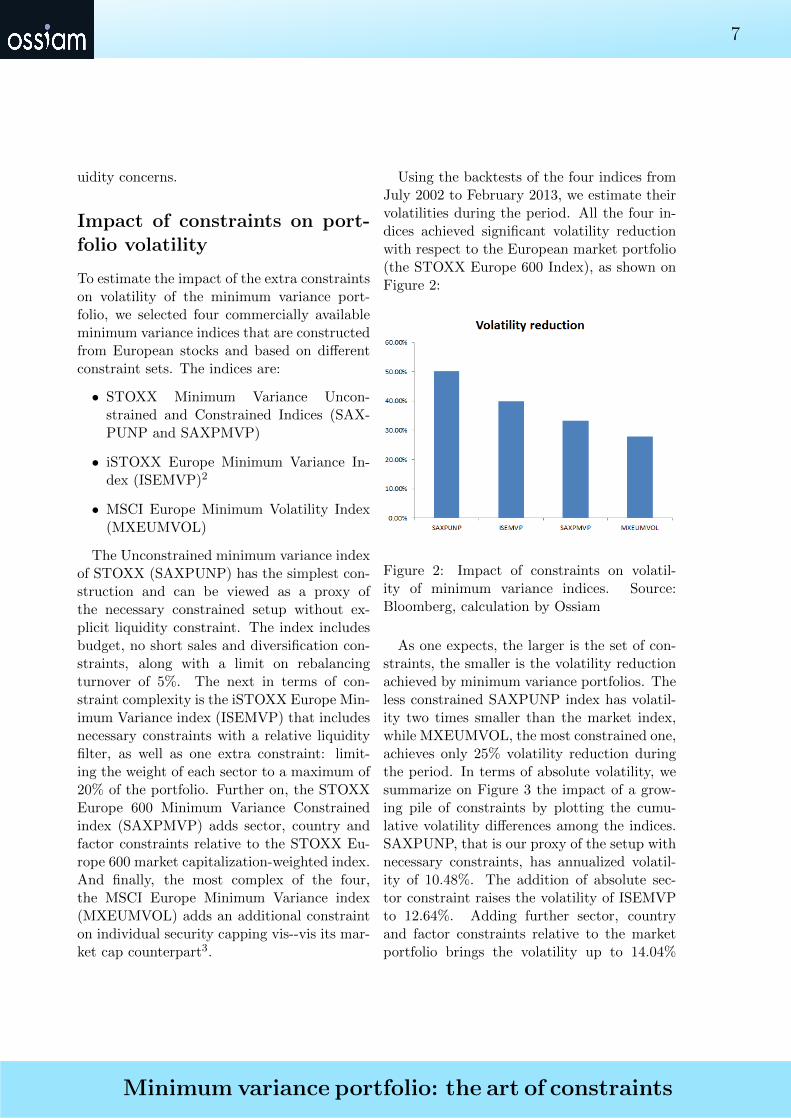

Using the backtests of the four indices fromJuly 2002 to February 2013, we estimate theirvolatilities during the period. All the four in-dices achieved significant volatility reductionwith respect to the European market portfolio(the STOXX Europe 600 Index), as shown onFigure 2:

Figure 2: Impact of constraints on volatil-ity of minimum variance indices. Source:Bloomberg, calculation by Ossiam

As one expects, the larger is the set of con-straints, the smaller is the volatility reductionachieved by minimum variance portfolios. Theless constrained SAXPUNP index has volatil-ity two times smaller than the market index,while MXEUMVOL, the most constrained one,achieves only 25% volatility reduction duringthe period. In terms of absolute volatility, wesummarize on Figure 3 the impact of a grow-ing pile of constraints by plotting the cumu-lative volatility differences among the indices.SAXPUNP, that is our proxy of the setup withnecessary constraints, has annualized volatil-ity of 10.48%. The addition of absolute sec-tor constraint raises the volatility of ISEMVPto 12.64%. Adding further sector, countryand factor constraints relative to the marketportfolio brings the volatility up to 14.04%

Minimum variance portfolio: the art of constraints

8

for SAXPMVP. And, finally MXEUMVOL hasthe highest volatility of 15.18% due to ex-tra relative constraints on individual securityweights.

Figure 3: Cumulative impact of constraints onvolatility of minimum variance indices. Source:Bloomberg, calculation by Ossiam

Conclusion

Because of the challenges in implementing theminimum variance approach the methodolo-gies differ significantly from one provider toanother. Minimum variance portfolios can bevery basic, including only full-investment andperhaps long-only constraints: one encounterssuch ”plain-vanilla” minimum variance portfo-lios in academic research papers. Too simplis-tic implementation suffers from highly concen-trated portfolios and has no control over port-folio liquidity that is unacceptable for an in-vestment benchmark. On the other hand, aheavy set of constraints, especially those bind-ing the portfolio weights to resemble the mar-ket capitalizations, might conflict with the veryobjective of portfolio variance minimization.We showed in this paper that there is a nec-essary set of constraints; otherwise the min-imum variance portfolio is empty or danger-ously concentrated and illiquid. Adding con-straints beyond the necessary set helps to de-

fine extra investment objectives but should becarefully balanced to avoid the conflict withrespect to the primary objective of volatilityreduction. Next time you face a new minimumvariance methodology: check if the necessaryconstraints are incorporated, then question therole the extra constraints involved.

Notes

1This constrained is called also Herfindahl con-straint, the name that refers to the Herfindahl-Hirschman index used by antimonopoly regulators tomeasure concentration inside industrial sectors.

2 Disclaimer: Ossiam licenses the iSTOXX Eu-rope Minimum Variance Index for the use in exchange-traded fund.

3This description represents an approximate com-parison of the four indices, since the constraints arenot applied in the same way. No index can be strictlyconsidered as a special case of another index with lessor more constraints. For example, only the index iS-TOXX uses the explicit liquidity constraint while theother three indices rather use the turnover constraint.Besides, there are differences in the implementation ofdiversification constraints among the indices that we donot detail here.

Minimum variance portfolio: the art of constraints

About Ossiam

Ossiam is a research-driven French asset management firm (authorized by the Autorité des Marchés Financiers) and specializes in delivering smart beta* solutions. Efficient indexing is at the core of Ossiam’s business model. The firm was founded in response to a post-subprime crisis demand from investors for simplicity, liquidity and transparency. Given the environment, there was a growing need among investors for enhanced beta exposure and risk hedging. Ossiam is focused on the development of innovative investment solutions for investors via a new generation of indices.

*'Smart beta' refers to systematically managed, non-market-cap-weighted strategies covering any asset class.

This document is of a commercial and not of a regulatory nature.

Ossiam, a subsidiary of Natixis Global Asset Management, is a French asset manager authorized by the Autorité des Marchés

Financiers (Agreement No. GP-10000016). Although information contained herein is from sources believed to be reliable, Ossiam

makes no representation or warranty regarding the accuracy of any information of which it is not the source. The information

presented in this document is based on market data at a given moment and may change from time to time.

This material has been prepared solely for informational purposes only and it is not intended to be and should not be considered as

an offer, or a solicitation of an offer, or an invitation or a personal recommendation to buy or sell participating shares in any

Ossiam Fund, or any security or financial instrument, or to participate in any investment strategy, directly or indirectly.

It is intended for use only by those recipients to whom it is made directly available by Ossiam. Ossiam will not treat recipients of

this material as its clients by virtue of their receiving this material.

This material reflects the views and opinions of the individual authors at this date and in no way the official position or advices of

any kind of these authors or of Ossiam and thus does not engage the responsibility of Ossiam nor of any of its officers or employees.

All performance information set forth herein is based on historical data and, in some cases, hypothetical data, and may reflect

certain assumptions with respect to fees, expenses, taxes, capital charges, allocations and other factors that affect the computation

of the returns.

Past performance is not necessarily a guide to future performance. Any opinions expressed herein are statements of our judgment

on this date and are subject to change without notice. Ossiam assume no fiduciary responsibility or liability for any consequences,

financial or otherwise, arising from, an investment in any security or financial instrument described herein or in any other security,

or from the implementation of any investment strategy.

This information contained herein is not intended for distribution to, or use by, any person or entity in any country or jurisdiction

where to do so would be contrary to law or regulation or which would subject Ossiam to any registration requirements in these

jurisdictions.

This material may not be distributed, published, or reproduced, in whole or in part.

80, avenue de la Grande Armée

75017 Paris – France

+ 33 1 78 40 56 90

“The STOXX® Indices and the data composed therein (the “Index Data”) are the intellectual property (including registered trademarks) of

STOXX Limited, Zurich, Switzerland (“STOXX”) and/or its licensors (the “STOXX Licensors”). The use of the Index Data requires a license

from STOXX. STOXX and the STOXX Licensors do not make any warranties or representations, express or implied with respect to the

timeliness, sequency, accuracy, completness, currentness, merchantability, quality or fitness for any particular purpose of the Index Data. In

particular, the inclusion of a company in a STOXX® Index does not in any way reflect an opinion of STOXX or the STOXX Licensors on the

merits of that company. STOXX and the STOXX Licensors are not providing investment, tax or other professional advice through the

publication of the STOXX® Indices or in connection therewith.” STOXX and its licensors have no relationship to Ossiam, other than the

licensing of the iSTOXX ® Europe Minimum Variance, STOXX ® Europe 600 Equal Weight and EURO STOXX ® 50 Equal Weight indices

and the related trademarks for use in connection with OSSIAM ETF indexed to the indices (hereafter the Products). STOXX and its Licensors

do not:

- Sponsor, endorse, sell or promote the Products.

- Recommend that any person invest in the Products or any other securities.

- Have any responsibility or liability for or make any decisions about the timing, amount or pricing of Products.

- Have any responsibility or liability for the administration, management or marketing of the Products.

Consider the needs of the Products or the owners of the Products in determining, composing or calculating the above mentioned indices or

have any obligation to do so.

STOXX and its Licensors will not have any liability in connection with the Products. Specifically, STOXX and its Licensors do not make any

warranty, express or implied and disclaim any and all warranty about:

- The results to be obtained by the Products, the owner of the Products or any other person in connection with the use of the above mentioned

indices and the data included in the above mentioned indices;

- The accuracy or completeness of the above mentioned indices and its data;

- The merchantability and the fitness for a particular purpose or use of the above mentioned indices and its data;

- STOXX and its Licensors will have no liability for any errors, omissions or interruptions in the above mentioned indices or its data;

- Under no circumstances will STOXX or its Licensors be liable for any lost profits or indirect, punitive, special or consequential damages or

losses, even if STOXX or its Licensors knows that they might occur.

The licensing agreement between Ossiam and STOXX is solely for their benefit and not for the benefit of the owners of the Products or any

other third parties.

Although Natixis Global Asset Management believes the information provided in this material to be reliable, it does not guarantee the accuracy, adequacy, or completeness of such information.