mining strategic excellence: south america what …

TRANSCRIPT

September 6, 2016

Nelson PizarroCEO

MINING STRATEGIC EXCELLENCE: SOUTH AMERICA

WHAT NEXT FOR CODELCO? A STRATEGIC OUTLOOK

CODELCO HIGHLIGHTS

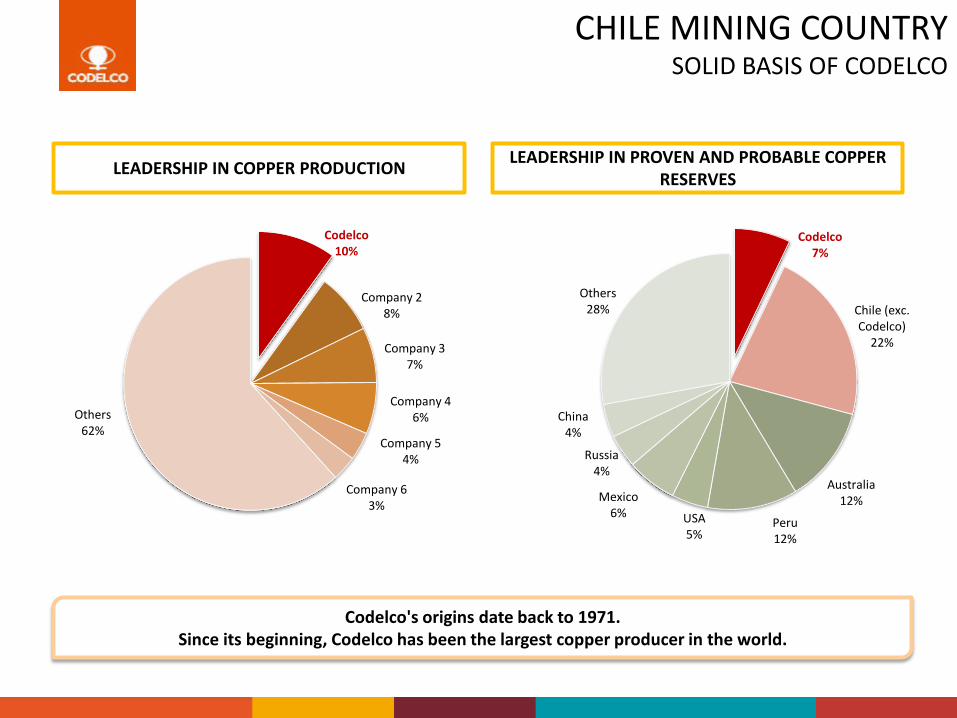

CHILE MINING COUNTRYSOLID BASIS OF CODELCO

Codelco7%

Chile (exc. Codelco)

22%

Australia12%

Peru12%

USA5%

Mexico6%

Russia4%

China4%

Others28%

Codelco10%

Company 28%

Company 37%

Company 46%

Company 54%

Company 63%

Others62%

LEADERSHIP IN COPPER PRODUCTION LEADERSHIP IN PROVEN AND PROBABLE COPPER RESERVES

Codelco's origins date back to 1971.Since its beginning, Codelco has been the largest copper producer in the world.

CODELCO: HISTORICAL PERFORMANCE

Contribution to Treasury

Copper Production*

Copper pricec/lb, 2015 currencyContribution to Treasury c/lb, 2015 currency

Copper production‘000 fmt

* Includes Codelco’s stake in El Abra and Anglo American Sur.

Copper Price

CODELCO HAS CONTRIBUTED US$104,000 MILLION TO THE STATE OF CHILE AND THE COUNTRY’S DEVELOPMENT AND PROGRESS

450

700

950

1,200

1,450

1,700

1,950

0

20

40

60

80

100

120

1971 1975 1979 1983 1987 1991 1995 1999 2003 2007 2011 2015

US$ million, 2015 currency ‘000 fmt

1: Includes Codelco’s interest in El Abra and in Anglo American Sur. 2: Percentage of the population living below the national poverty lines.Sources: IMF, BLS and Codelco.

MINING: KEY DRIVER FOR CHILE’S DEVELOPMENT:

1990 2015GDP per capita, PPP (const. 2015 US$) 9,741 23,334Poverty2 (% of population) 38.6 14.4 (2013)Life expectancy at birth, total (years) 72.7 81.5 (2014)

CODELCO: KEY PLAYER / THE REAL DRIVER

2016 Estimation

2017PreliminaryBudget

ANNUAL COPPER PRODUCTION*

ACCUMULATED CONTRIBUTION

0

10

20

30

40

50

0% 20% 40% 60% 80% 100%

URB

CO

N_C

0

10

20

30

40

50

0 10,000 30,000 50,000 70,000 90,000

PPP_C

CO

N_C

GDP per capita (PPP)(US$)

Usa

ge p

er c

apita

(Kg.

)

Urbanization rate(%)

IN THE LONGER TERM, FUNDAMENTALS REMAIN STRONG

Usa

ge p

er c

apita

(Kg.

)

Copper usage per capita and GDP per capita (PPP)

Usage per capita and urbanization rate

WORLD*: COPPER USAGE PER CAPITA, GDP PER CAPITA (PPP) AND URBANIZATION RATE 1980-2015

*: It includes all countries which consume copper.Source: Prepared using data from World Bank, Codelco and IMF.

2015 weighted average: 57%2015 weighted average: US$ 18,100

HEALTHY COPPER

2015 average: 3.7 kg. per capita

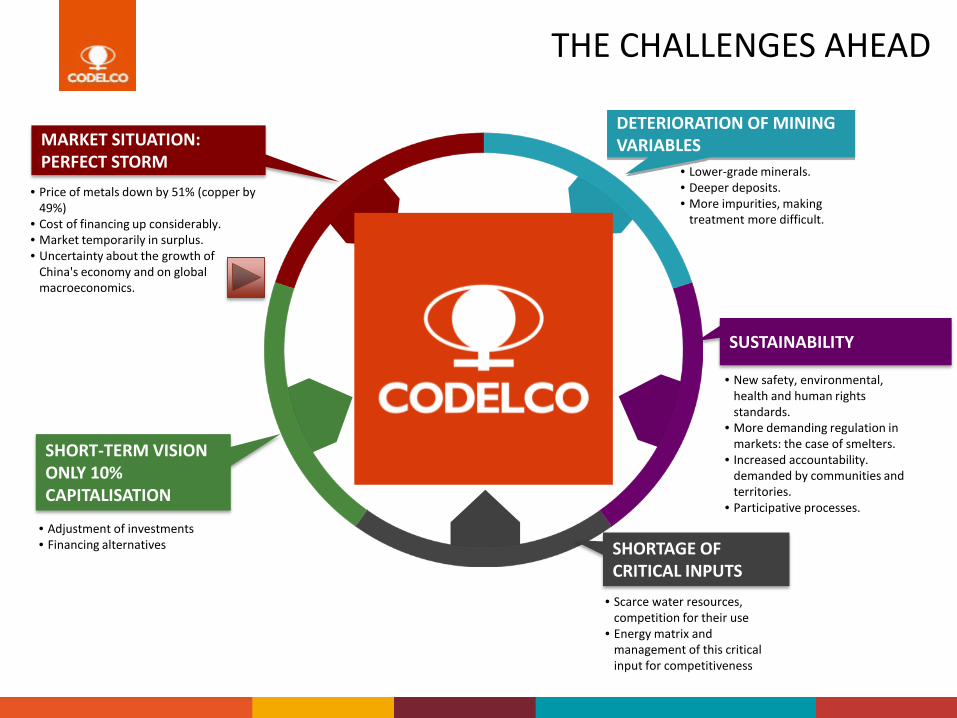

• Price of metals down by 51% (copper by 49%)

• Cost of financing up considerably.• Market temporarily in surplus.• Uncertainty about the growth of

China's economy and on global macroeconomics.

THE CHALLENGES AHEAD

MARKET SITUATION: PERFECT STORM • Lower-grade minerals.

• Deeper deposits. • More impurities, making

treatment more difficult.

DETERIORATION OF MINING VARIABLES

• New safety, environmental, health and human rights standards.

• More demanding regulation in markets: the case of smelters.

• Increased accountability. demanded by communities and territories.

• Participative processes.

SUSTAINABILITY

• Scarce water resources, competition for their use

• Energy matrix and management of this critical input for competitiveness

SHORTAGE OF CRITICAL INPUTS

• Adjustment of investments • Financing alternatives

SHORT-TERM VISION ONLY 10% CAPITALISATION

CODELCO STRATEGY

OUR STRATEGY

Strengthen corporate

governance

Manage with safety and

occupational health

Operate in harmony with environment, communities and territory

Strengthen the

organization and

management processes

Create value through

innovation and new

technologies

Incorporate and maximize

talent development

GROWTH BEYOND OUR MINING BASE

PROJECTS AND EXPANSIONS TO TAKE ADVANTAGE OF OUR MINING BASE

CURRENT OPERATIONS: COST CONTROL AND INCREASING PRODUCTIVITY

SUSTAINABILITY AS BUSINESS MODEL

CODELCO'S STRENGTHS

• Leader in copper production: 10% of global production.

• World-class assets: 7% of global copper reserves.

• Second largest molybdenum producer: 10% of global production.

• Long-life reserves and resources (75 years* for reserves and mineral resources; 245 years* for geological resources).

• Portfolio of profitable projects.

• Highly-trained human resources with mining experience.

• Technological and commercial know-how.

• Institutional framework.

I II

*: Weighted average. Source: Based in Annual Report.

0200400600800

1,0001,2001,4001,6001,8002,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

STRUCTURAL PROJECTS PRODUCTION

0200400600800

1,0001,2001,4001,6001,8002,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

CODELCO: PILLAR OF DEVELOPMENTWHAT NEXT?

CONTINUE TO BE A PILLAR OF CHILE’S DEVELOPMENT

BUT THE ROAD IS NOT EASY

Develop 7 Structural Projects.

CODELCO IDENTIFIES SUSTAINABILITY AS ITS BUSINESS MODEL

Address changes in the business environment.

‘000 tonnes

CURRENT OPERATION WITHOUT PROJECTS*

* Includes Traspaso Andina Project.

Productivity, no matter what

Address the present through cost savings

Assure the future through innovation

COST CONTROL AND HIGHER PRODUCTIVITY

1

2

COST CONTROL PROGRAMME IS STEADILY DELIVERING EXPECTED RESULTS

c/lb

164 163

150

139

128

110

120

130

140

150

160

170

2012 2013 2014 2015 2016Jan-Jun

CODELCO CASH COST C1

Productivity gains Lower input prices (exchange rates, energy, fuels, other supplies and services)

Despite 36% lower molybdenum prices in 2015, Codelco has

reduced its costs significantly

2015 Cost Reductions: Main Drivers

500

750

1,000

1,250

1,500

1,750

2,000

2012 2013 2014 2015 2015Jan-Jun

2016Jan-Jun

Divisiones El Abra AAS

FOCUS ON PRODUCTIVITY AND COST MANAGEMENT HAS REDUCED THE FINANCIAL IMPACT OF COPPER PRICE DECREASE

Adjusted EBITDA Margin (%)

Copper Price c/lb

*: 2012 Adjusted EBITDA excludes the extraordinary fair value accounting effect of Anglo American Sur 20% acquisition. Law 13,196 considered as a tax.

‘000 tonnes

361

332

311

249

269

213

150

200

250

300

350

400

0

13

26

39

52

65

2012* 2013 2014 2015 2015Jan-Jun

2016Jan-Jun

Mining EBITDA Margin (%) Copper Price

1,7921,841

Total Copper Production Mining EBITDA Margin and Copper Price

1,891

1,758

906910

Permanent Good Practices

management

PRODUCTIVITY AND COSTS AGENDAGOAL 2020: US$ 2,000 MILLION IN COST REDUCTION

Valu

e

2016 2017 2018 2019 2020

Integrated management of the Productivity Agenda and

incorporation of disruptive initiatives

Development of the Productivity Agenda and kick off of initial

corporate initiatives

Productivity as part of the regular management of the Corporation,

results in sustainability and growth

Efficient Accreditation

Maintenance Planning

Optimization

Services Productivity Model

Implies

Positively contribute to Codelco's

Competitiveness

IMPLIES

New Third Party Management

Practices

New China-Low Cost Procurement

Office Strategy

C+ Lean as part of corporate

management

Innovation applied to the Divisions

District Contracts

Optimization

Installation of Proactive

Maintenance

Inventory Optimization

EARLY RESULTS (US$ million)

2015 2016 2017 - 2020

≈ 500 237 - 300 2,000

At Codelco, innovation will focus

primarily on transforming

knowledge into value.

Research

Innovation

Value Knowledge

Innovation is to create economic, environmental and social value from knowledge.

Research is to create knowledge from economic value.

Source: Dr. Hartmut Raffler, VP Innovation, Siemens.

FOCUS ON APPLICATION OF INNOVATION

ASSURING THE FUTUREINNOVATION TO ADDRESS DETERIORATION OF MINING VARIABLES

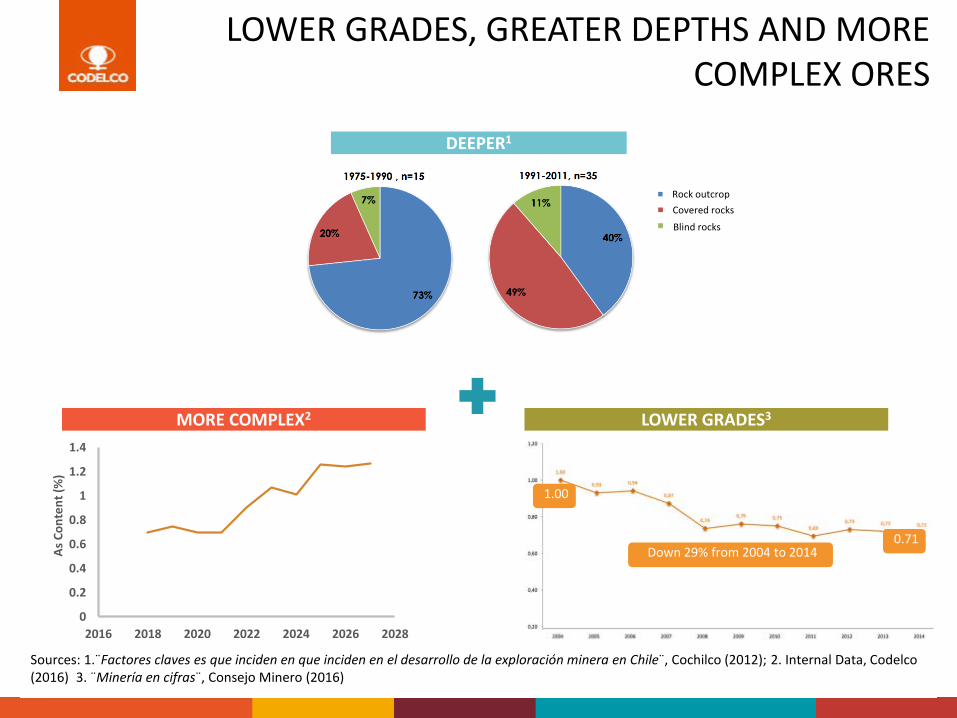

LOWER GRADES, GREATER DEPTHS AND MORE COMPLEX ORES

0

0.2

0.4

0.6

0.8

1

1.2

1.4

2016 2018 2020 2022 2024 2026 2028

As C

onte

nt (%

)

DEEPER1

1.00

0.71

Sources: 1.¨Factores claves es que inciden en que inciden en el desarrollo de la exploración minera en Chile¨, Cochilco (2012); 2. Internal Data, Codelco (2016) 3. ¨Minería en cifras¨, Consejo Minero (2016)

MORE COMPLEX2 LOWER GRADES3

Rock outcrop

Blind rocks

Covered rocks

Down 29% from 2004 to 2014

EXPENDITURE ON INNOVATION AT CODELCO

0.0%

0.4%

0.8%

1.2%

1.6%

2.0%

2.4%

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015 2016 E

% COPPER EFFECTIVE SALES

1,5% COPPER SALES

INNOVATION EFFECTIVE SPENDING

INNOVATION SPENDING(ASSUMING 1.5% COPPER SALES)

• Spending on Innovation, for a company, should tend to 1.5% of sales.

• Innovation should be seen as an investment, managed with method and discipline.

US$ million % copper sales

INNOVATION MANAGEMENT SYSTEM IN CODELCO

CodelcoTec

Suppliers and Technology Partners

• The results are the result of amethodical and disciplinedprocess, developed within aManagement Innovation System.

Corporate Strategy

Results

Innovation Process & R+D

Strategic Level

Execution Level

Enablers

Support

I

II

III

IV

Role, Goals and Aims of Innovation

Innovation Portfolio Management

Innovation & R+D Project management

Intra- entrepreneurs management

Control People and Incentives Marketing Technology

Vigilance

R&D Centers and

Network

Resources

Organization

CURRENT FOCUS OF R&D IN CODELCO

ROBOTIC CONCENTRATE SAMPLING

SEMI-AUTONOMOUS LHDsLEACHING OF SULPHIDES

GRADE > 2% GRADE ~ 0,5%

• BREAKTHROUGHS FOR COMPETITIVE ADVANTAGES

– Increased productivity and lesser environmental impact / Leaching of sulphides

• SOLUTION OF OPERATIONAL DIFFICULTIES

– Hazardous areas of pits / Remote mining.

– Operational control / Robotic concentrate sampling.

– Preventive maintenance / Big data.

• TRANSFORMATION OF RESOURCES INTO RESERVES

– Increased productivity and safety / Semi-autonomous LHDs.

– More impurities / Processing of complex concentrates.

MINING OPERATIONS

Stage

CODELCO IS SO FAR WORKING ON SEVERAL CORPORATE INITIATIVES TO INCREASE ITS COMPETITIVENESS

Impact

Tailings dams metals recovery

Integrated Corporate Information CenterBath Smelting

instrumentation

Engineering improvement Biosigma

Hangout Handler

Autonomous trucks software update

Electro-oxidation leaching

LHD Semi -Autonomous

Tires treatment

High productivity pit technologies

Continuous conversion

In addition,• Codelco is working with several companies on innovative developments in divisional projects.• Redefinition of the Cluster as an Open Innovation Strategy.• Technological cooperation agreements with leading global companies.

• This year, CodelcoTec is being developed by merging all the technological subsidiaries.• It is installing a Management Innovation System at corporate level and in all divisions.

Examples of innovation initiatives

EnargitaSelective Flotation

ProcessesPitUndergroundSmelting & refining

Sustainability

Automation

Technological conceptualization

Experimentation Industrial validation Basic engineering

Implementation Operation

SUMMARY

SUMMARY

• Large mining resource base.

• High-quality projects underpinned by our mining base.

• Focus on operating cost control and productivity.

• Innovation and technology geared to enhancing productivity.

• High credit rating.

• Optimisation of investments through the cycle.

• Experienced management with proven track record.

• Strong owner support.

CODELCO'S STRENGHT AND FUTURE GROWTH

September 6, 2016

Nelson PizarroCEO

MINING STRATEGIC EXCELLENCE: SOUTH AMERICA

WHAT NEXT FOR CODELCO? A STRATEGIC OUTLOOK