misclassification of independent contractors: addressing ... · misclassification of independent...

TRANSCRIPT

Misclassification of Independent

Contractors: Addressing Costly Industry Trends

and Past Practices This webcast will begin promptly at 12:00 PM Eastern

Follow Steptoe & Johnson on Twitter: @Steptoe_Johnson

ALSO FIND US ON http://www.linkedin.com/companies/216795

© 2017 Steptoe & Johnson PLLC . All Rights Reserved.

Today’s Presenters

Susan Llewellyn Deniker Member

304.933.8154 [email protected]

Zachary D. Bombatch Associate

724.749.3133 [email protected]

Introduction Businesses must properly evaluate and classify the types of relationships they have with their workers

Employee: person paid to perform work under the control and direction of another Independent Contractor: provider of services under the terms of a contract who controls the means by which the outcome is achieved

3

Independent Contractor

• Who is an independent contractor? – Worker who contracts

with individuals or businesses to provide services in exchange for compensation

– The worker does not regularly work for any particular business

4

Independent Contractor • A contract controls the relationship between the

business and the independent contractor (not an employment contract) – Fees for service – Defined time to perform service/tasks – Defined outcome – Method and manner of work determined by worker – Economically independent – Worker responsible for his/her taxes – No eligibility for benefits with contracting business

5

Employee • Who is an employee?

– Worker who works directly for a business

– Subject to significant oversight

– Receives fringe benefits and other perks because of relationship

– Protected by federal, state, and local laws (discrimination, etc.)

6

Employee

• An employment relationship governs the interaction between the individual and business – Paid wages and company-sponsored benefits – Continuous employment (at-will) – Taxes withheld and paid by employer – Economically dependent upon the employer – Subject to internal policies and procedures

7

Benefits of Independent Contractor Relationship

• Businesses enjoy significant advantages when engaging independent contractors – Wages – Tax – Flexibility

• Individuals also enjoy benefits of being independent contractors

8

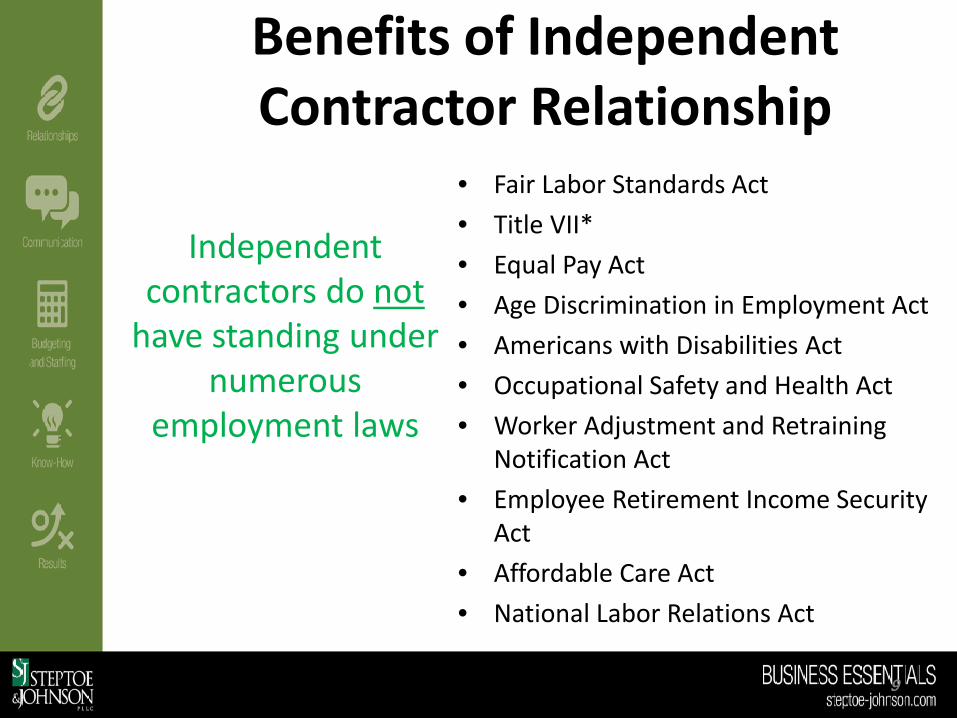

Benefits of Independent Contractor Relationship

Independent

contractors do not have standing under

numerous employment laws

• Fair Labor Standards Act • Title VII* • Equal Pay Act • Age Discrimination in Employment Act • Americans with Disabilities Act • Occupational Safety and Health Act • Worker Adjustment and Retraining

Notification Act • Employee Retirement Income Security

Act • Affordable Care Act • National Labor Relations Act

9

Independent Contractors

• Fair Labor Standards Act (“FLSA”) – Minimum wage – Overtime

• Independent contractor

compensation structure is governed by the contract

10

Independent Contractors • Title VII of the Civil Rights Act

of 1964 – Race – Religion – Sex – National Origin – Color

• Businesses cannot discriminate against independent contractors when contracting

11

Independent Contractors

• No employee benefits are provided to independent contractors – Health insurance – Retirement or pension plan – Stock options – Paid vacations and sick days – Life insurance – Disability insurance – Fringe benefits

12

Affordable Care Act • ACA compliance mandates coverage depending

upon how many employees work for an employer

• Large businesses must submit returns to the IRS regarding coverage offered or not offered – Report on number of employees – Classify employees under the “Common Law”

test • Contracting with independent contractors may

reduce employee workforce and limit ACA coverage

13

Tax & Insurance • Tax withholding and insurance coverage is

required for employees • No such obligations for independent

contractors – businesses can avoid the obligations – Federal, state, local income tax – Social Security and Medicare – Federal unemployment insurance taxes – State unemployment insurance taxes – Workers’ compensation insurance

14

Misclassification

• Land agents • Rig workers

– Laborers – Riggers – Operators

Employer tells the worker that s/he is

an independent contractor

Independent contractor enters into contract for

specific work

15

“We’re going to 1099 you.”

Misclassification

Private Lawsuits

• Back pay, including overtime compensation

• Employee benefits, including stock options, retirement benefits, health insurance

• Disability payments • Monetary penalties • Liquidated damages

Government Enforcement

• DOL enforcement for the

same • Tax and insurance

obligations, plus penalties • Potential extensive audits

16

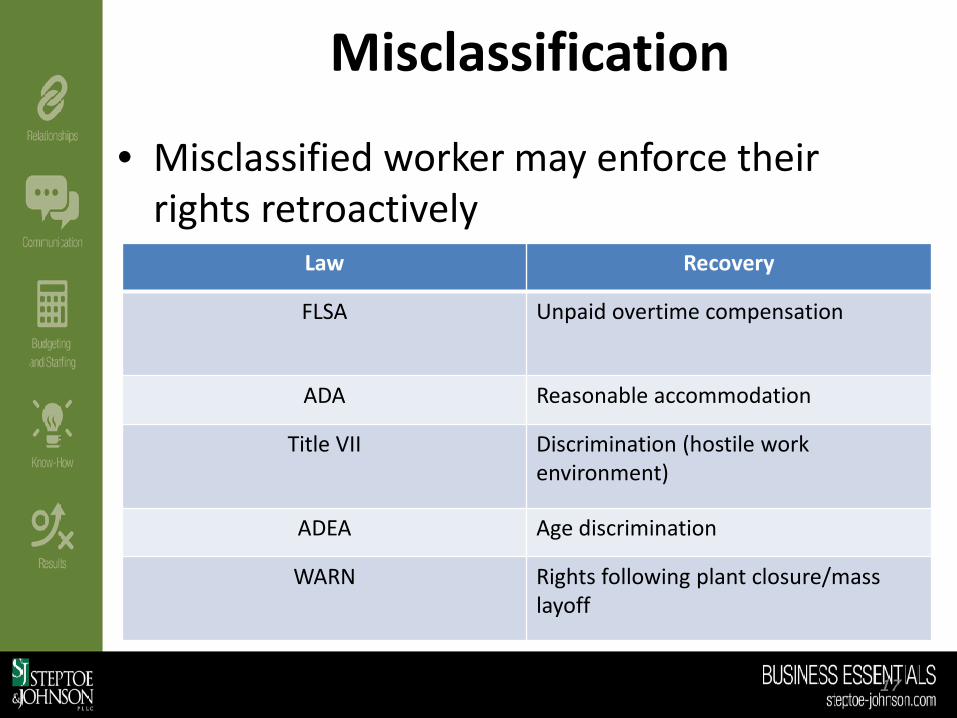

Misclassification

• Misclassified worker may enforce their rights retroactively

17

Law Recovery

FLSA Unpaid overtime compensation

ADA Reasonable accommodation

Title VII Discrimination (hostile work environment)

ADEA Age discrimination

WARN Rights following plant closure/mass layoff

Misclassification • Insurance coverage

– Reimbursement for uninsured and unreimbursed medical expenses

• Stock options – Stock purchase plan – Critical if stock gains value during the time of

misclassification – Vizcaino v. Microsoft Corp. - $97 million

settlement

18

Misclassification Targets • The Department of Labor

(“DOL”) and Internal Revenue Service (“IRS”) have identified industries likely misclassifying workers

• These industries are targets of highly coordinated enforcement efforts

• The enforcement efforts involve corresponding state agencies

Targeted Industries Construction

Transportation Cable

Janitorial Landscaping

Nursing Child care

Home health care Oil and gas

19

Misclassification Targets

20

Oil & Gas Industry • Accurate data on misclassification in the

industry is unavailable – no voluntary reporting

• No government agency has conducted comprehensive research

• The DOL still perceives that industry participants misclassify because of purported past practices and industry trends

21

Oil & Gas Industry

• It is no defense that the majority of the industry misclassifies independent contractors

• Past practices are not defenses to misclassification

22

Oil & Gas Industry

• Class and collective action lawsuits have been filed against oil and gas industry businesses for misclassifying independent contractors

• The lawsuits typically result in substantial settlement amounts under court supervision

• Damages include back pay, liquidated damages, and fringe benefit contributions

• The lawsuits can upend workforce management and morale

23

Independent Contractor Tests

• Employers carry the burden of properly classifying their workers

• There is no “bright line” test to distinguish whether a worker is an independent contractor

• “Tests” can and should be utilized to properly classify workers

24

The Economic Realities Test • Utilized by DOL to enforce FLSA • The FLSA defines an “employee” as “any

individual employed by an employer” who is “permitted” or “suffered” to work

• This ambiguous definition has resulted in the DOL and courts establishing tests to determine whether an employment relationship exists

• This test is also used for Title VII, ADA, and ADEA purposes

25

The Economic Realities Test

• A worker’s specific work circumstances determines proper classification

• Multiple factors are used to determine the worker’s classification, but no factor is determinative

26

The Economic Realities Test

27

• Is the work an integral part of the employer’s business?

• Does the worker’s managerial skill affect his or her opportunity for profit and loss?

• Relative investments of the worker and the employer

• The worker’s skill and initiative • The permanency of the worker’s relationship

with the employer • Employer control of employment relationship

The Economic Realities Test

28

• Factors that are not determinative: – Contract language – Worker’s title – Worker’s label

The Economic Realities Test • Degree of control over

manner and means: – Cost of work – Hiring/firing workers to

assist – Delegating which tasks are

completed – Assuming responsibility for

licenses, taxes, and other administrative obligations

– Mandating work schedule – Supervising day-to-day

tasks

29

– Furnishing tools and equipment

– Profit/loss flexibility of worker

– Permanency of relationship – Skills required

Department of Labor • Time and mode of

payment are not conclusive of classification

• A signed agreement that a worker is an independent contractor is not conclusive

• The worker’s corporate entity (e.g., LLC) is not conclusive

30

Department of Labor

– Hiring others to assist – Purchasing equipment and

materials – Advertising services – Renting space to manage

an independent business – Time management – Investment into providing

services (not just investing in equipment to perform work for particular employer)

– Utilizing skill, judgment, and initiative (technical skills are insufficent)

– Continuous, indefinite relationship

– Autonomy • Rate of pay • Working hours • Hiring helpers

31

An independent contractor is truly independent

Trump Administration

32

• Rescinded 2015 Administrator’s Interpretation regarding independent contractor classification

• Where does this leave us?

The IRS Standard • The focus of the IRS is

on taxes – Taxes of the individual

• Deductions

– Taxes withheld by the employer

• Extensive 20-factor test • Now, examines three

categories of factors • Holistic approach to

determine classification

33

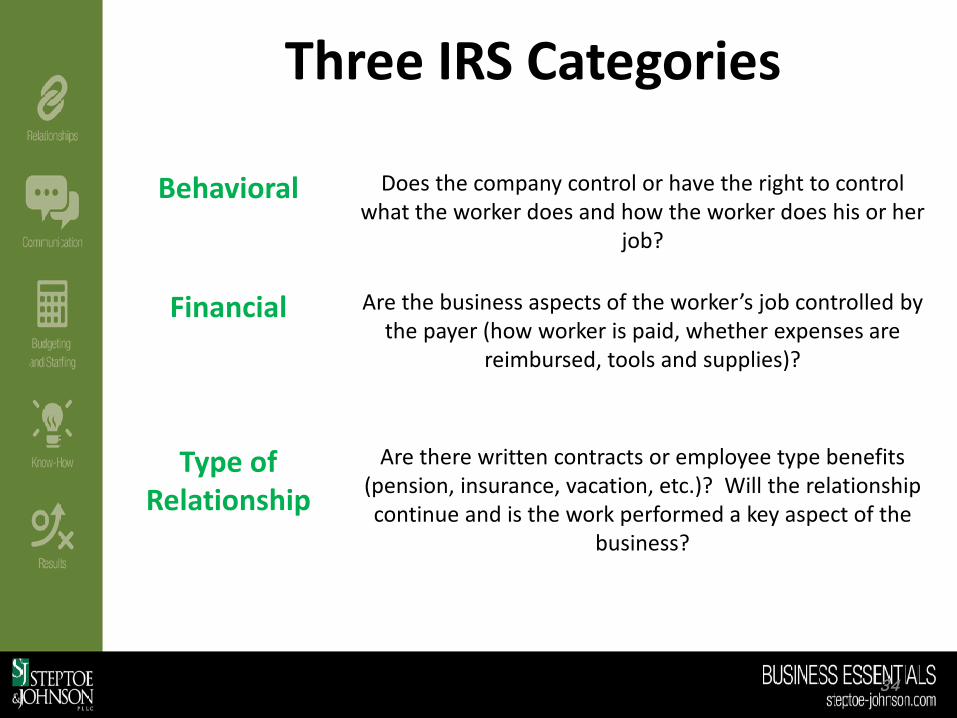

Three IRS Categories

Behavioral Does the company control or have the right to control what the worker does and how the worker does his or her

job?

Financial Are the business aspects of the worker’s job controlled by the payer (how worker is paid, whether expenses are

reimbursed, tools and supplies)?

Type of Relationship

Are there written contracts or employee type benefits (pension, insurance, vacation, etc.)? Will the relationship continue and is the work performed a key aspect of the

business?

34

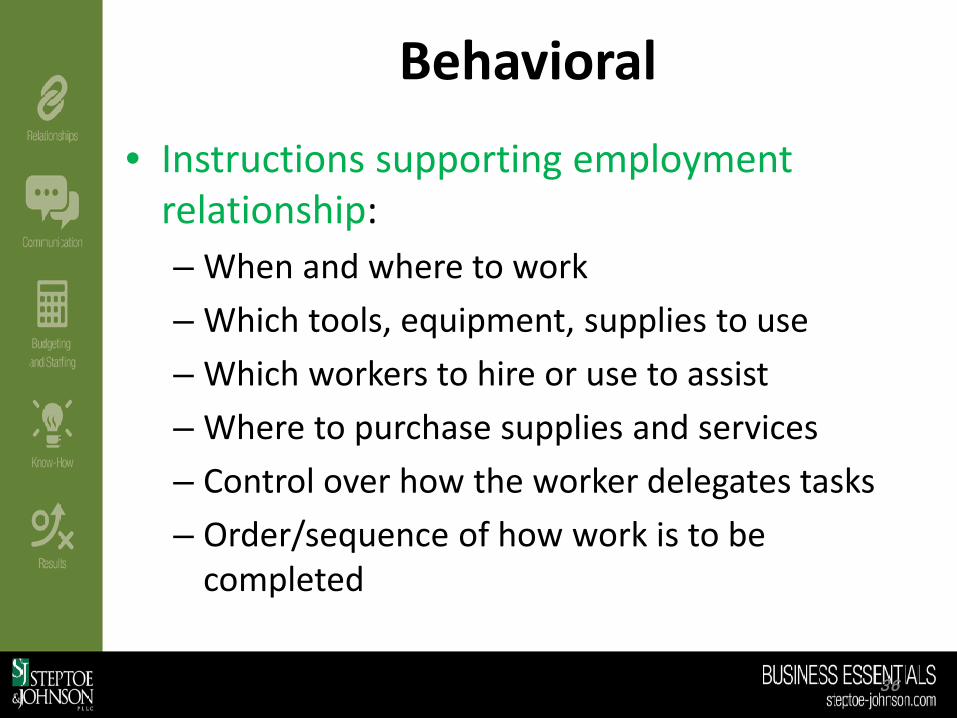

Behavioral • A worker is an employee if the business directs and

controls the worker, or has the right to do so. • A business that controls what a worker does and

how she/he does, it has an employment relationship

• Behavioral controls – Type of instructions given – Degree of instruction – Work evaluation – Training needed or provided by business

35

Behavioral

• Instructions supporting employment relationship: – When and where to work – Which tools, equipment, supplies to use – Which workers to hire or use to assist – Where to purchase supplies and services – Control over how the worker delegates tasks – Order/sequence of how work is to be

completed

36

Financial

• Focus is on whether business controls the economic aspects of the worker’s job (not just compensation) – Compensation (bi-

weekly direct deposit) – Expense reimbursement – Tools and supplies

provided by business

37

Financial • The IRS expects independent contractors to:

– Make significant investments in tools, training, office space, and similar resources. No dollar amount threshold.

– Pay their own expenses – Earn profit/loss per project (not just paid wages

for completing work, but earning rewards for efficiency on their own balance sheet)

– Offer services to general public – Be compensated per task, not per hour or pay

period

38

Type of Relationship

• Focus on the structure of the relationship between the employer and worker

• How does the worker view the relationship?

• How does the employer view the relationship?

39

Type of Relationship • Written contract

– Starting point to examine the relationship, but not conclusive • Employee-type benefits

– Pension plan contributions, health insurance, vacation pay • No end date

– Specific time period or project is expected of independent contractor; continuous relationship appears to be employment relationship

• Key activities of the business – Activities completed by the worker that are necessary for the

business to function point toward an employment relationship (land agents)

40

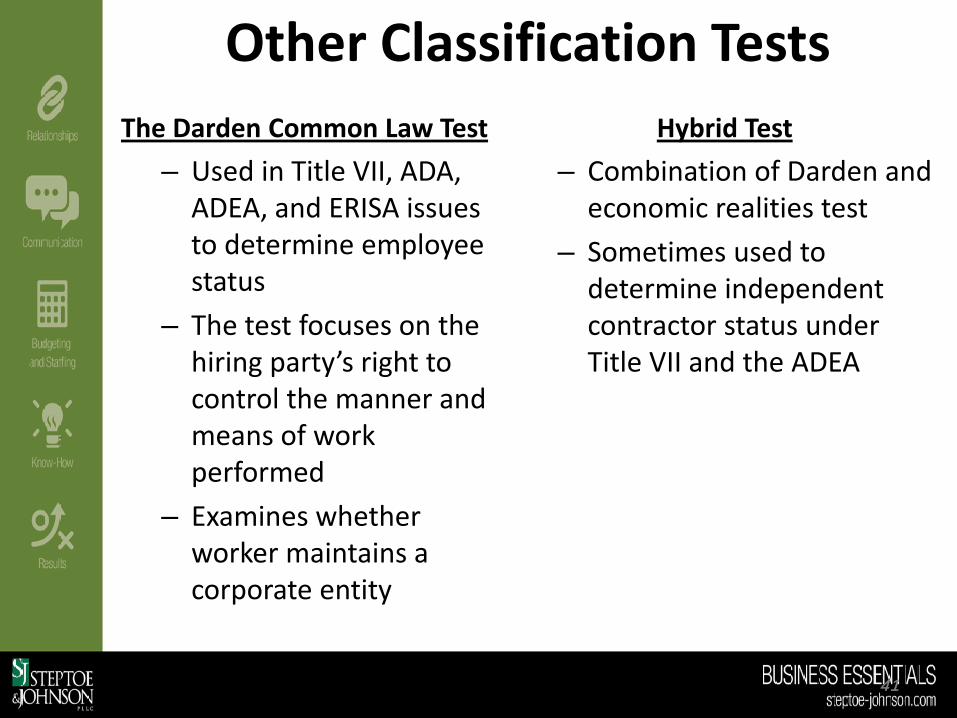

Other Classification Tests The Darden Common Law Test

– Used in Title VII, ADA, ADEA, and ERISA issues to determine employee status

– The test focuses on the hiring party’s right to control the manner and means of work performed

– Examines whether worker maintains a corporate entity

Hybrid Test – Combination of Darden and

economic realities test – Sometimes used to

determine independent contractor status under Title VII and the ADEA

41

State Law Tests

• Laws vary state to state regarding the classifications of workers

• Coordinated efforts between states and federal agencies

• Classification at state level may be pertinent for state law claims

42

Best Practices for Classification

Audit Workforce – Review existing worker

classifications under the framework examined

– Determine whether the relationships appear to be independent or reliant

– Focus on control and right to control

Train Personnel – Train employees with

authority to hire and classify under the tests

– Monitor relationships with independent contractors

– Monitor communications published to independent contractors

43

Recordkeeping

• Maintain copies of written agreements – Current, revised, and expired

• Maintain contractor’s Employer Identification Number • Record all payments made to the independent

contractor – Amounts – Dates – Method

• Copies of 1099-MISC – Including those returned by USPS

• All documents supporting independent contractor relationship

44

Mitigating Risks

Request IRS Audit – Utilized Form SS-8 – Six months or more for

determination – May be used under

Section 530 for safe harbor

– Be cautious that determination from IRS is conclusive

Review Contracts – Incorporate language

that ensures both parties understand the relationship

– Remove language that provides employer with the right to control method and means of work

45

Voluntary Classification Settlement Program

• VCSP offered by the IRS • Businesses may conduct

workforce audits and reclassify independent contractors as employees

• Reclassification results in a penalty fee paid to IRS, but it is a fraction of tax liability for most previous year

46

QUESTIONS?

This program has been accredited for 1 RL, RPL or CPL recertification credit(s) (CEU), and 0 CPL/ESA, and/or 0 Ethics credit(s) (CEU Ethics), for a total of 1 credit(s). (Number of credits accredited or claimed for 100% participation in this educational program). Add the recertification credits to your AAPL transcript within 30 days of attendance by following these instructions: 1. Go to “My Account” on www.landman.org 2. On the left, under Certifications, click “View and Add Continuing Education Credits.” 3. Click “Add Continuing Education Credit.” 4. Enter Component code in the pop-up window. Click “Apply.” 5. If you need to record partial attendance, please edit the “# of credits” field to reflect 1 credit per hour attended 6. Click “Save.”

AAPL CLE Component Code: SJ9171

Thank You!

Susan Llewellyn Deniker Member

304.933.8154 [email protected]

Zachary D. Bombatch Associate

724.749.3133 [email protected]

These materials are public information and have been prepared solely for educational purposes. These materials reflect only the personal views of the authors and are not individualized legal advice. It is understood that each case and/or matter is fact-specific, and that the appropriate solution in any case and/or matter will vary. Therefore, these materials may or may not be relevant to any particular situation. Thus, the authors and Steptoe & Johnson PLLC cannot be bound either philosophically or as representatives of their various present and future clients to the comments expressed in these materials. The presentation of these materials does not establish any form of attorney-client relationship with the authors or Steptoe & Johnson PLLC. While every attempt was made to ensure that these materials are accurate, errors or omissions may be contained therein, for which any liability is disclaimed.

Material Disclaimer