mission impossible of effective bank regulation

TRANSCRIPT

MISSION IMPOSSIBLE OF MISSION IMPOSSIBLE OF EFFECTIVE BANK REGULATIONEFFECTIVE BANK REGULATION

Dr. Petr TeplýCharles University in Prague, Czech Republic

University of Economics in Prague, Czech Republic

The University of AucklandAuckland, New Zealand

2 September 2011

AgendaAgenda

Introduction1.

Bank reg. & supervision in the CR3.

Theoretical background2.

Bank reg. & supervision in the CR3.

Basel I/II/III capital accords4.

Regulation after the crisis5.

2

Conclusion6.

Mission impossible of effective bank regulation2 September 2011

PresenterPresenter –– Dr. Dr. PetrPetr TeplTeplýý

2000 – JKU in Linz, Austria

2006 – University of Otago, New Zealand

2006 – State University of New York, New Paltz, USA

2009 – Ph.D. in Finance, Charles University, Czech Rep.

� Research interests: banking, finance, risk management,

Education

3

� (Co)author of over 60 articles and 10 books

� Guest lectures in New Zealand, Turkey, USA

� Presentations at Harvard University, State University of New York, China, Dubai, India, London, India, Nepal, Singapore etc.

� Research interests: banking, finance, risk management, financial stability, public finance, RIA

Job experience 2001-2005 CSOB Bank, Czech Rep.

2006 Spencer Clarke, New York, USA

2007+ EEIP, a.s., Czech Rep.

IntroductionIntroduction to The to The CzechCzech RepublicRepublic (1/2)(1/2)

4

IntroductionIntroduction to The to The CzechCzech RepublicRepublic (2/2)(2/2)

Three Main Czech Three Main Czech IconIconss

Czech TOP Sports Czech TOP Sports

Czech Beer

5

Czech TOP Sports Czech TOP Sports ((wowo)men)men

Petra

KVITOVA

� CUNI = public university founded in 1348

� now 17 faculties, 51,000 students, 7,500 employees, 300 accredited degree programms and 660 study disciplines

� My affiliation: Department of Finance and Capital Markets/Institute of Economic Studies/Faculty of Social Sciences

6

Sciences

Source: Academic Ranking of World Universities – 2011, http://www.shanghairanking.com/ARWU2011.html#

1) To provide my view on financialmarkets´ regulation in both theoryand practice

2) To focus on banking regulation Basel I,

1.1. IntroductionIntroduction

ThreeThree aimsaims ofof the the presentationpresentation

7

2) To focus on banking regulation Basel I, Basel II and Basel III

3) To welcome comments from the opposite side of the globe ☺

AgendaAgenda

Introduction1.

Bank reg. & supervision in the CR3.

Theoretical background2.

Bank reg. & supervision in the CR3.

Basel I/II/III capital accords4.

Regulation after the crisis5.

8

Conclusion6.

Mission impossible of effective bank regulation2 September 2011

2. Background of regulation2. Background of regulation

GlobalGlobal politicalpolitical governancegovernance --> politicians > politicians “pretend” regulation efforts but in fact they “pretend” regulation efforts but in fact they do not want to regulate so much...do not want to regulate so much...

Source: Petr Teply (2010)

......weakweak regulation regulation –– one caone cause use ofof the the globalglobal crisiscrisis

Flawedincentives

Failed risk management

Weak regulation and supervision

High“risky“ profits

1. Microeconomic causes

2. Background of regulation2. Background of regulation

10

Internationalimbalances

Long period of low real interest

ratesAsset bubles

2. Macroeconomic causes

Source: Petr Teply based on various sources

3 .Psychological effects

2. Background of regulation2. Background of regulation

Similarities of financial and nuclear Similarities of financial and nuclear criscriseess

1) Black swan events for complex systems (it would be very expensive to cover them)

2) Cross-border nature (global coverage -antinuclear regulation in Europe)

11Source: Petr Teplý based on Zachmann (2011)

3) Privatisation of profits, & socialisation of losses (failed risk mitigation)

4) Regulators failed to prevent the risk

5) Strong lobby

2. Background of regulation2. Background of regulation

Taxpayers did, do and will always cry!!!Taxpayers did, do and will always cry!!!

2. Background of regulation2. Background of regulation

How to save the financial sector? In theoryHow to save the financial sector? In theory

13Source: Oliver Wyman (2009)

How to save the financial sector? In praxisHow to save the financial sector? In praxis2. Background of regulation2. Background of regulation

Source: Oliver Wyman (2009)

The regulatory squeeze on The regulatory squeeze on banking, but…banking, but…

2. Background of regulation2. Background of regulation

15Source: Petr Teplý based on Oliver Wyman (2011)

2. Background 2. Background ofof regulationregulation

Lucan’s viLucan’s vicciousious circle of rcircle of regulategulationion

Innovation

ExpansionMotivation

16

Expansion

CrisisRegulation

Motivation

Source: Petr Teplý based on Ján Lučan (2011)/ Legal aspects of financial markets

2. Background 2. Background ofof regulationregulation

““MAC“ MAC“ questionsquestions regulatoryregulatory conceptconcept� Materiality

� Are activities of a newly regulated entity material and significant? Does this future regulated entity play a significant role on the relevant market

� Accountibility� Is the entity accountable, can the regulator easily described and

17

� Is the entity accountable, can the regulator easily described and defined it?

� Credibility� How successful were similar regulations? Does any applicable best-practice regulation exist??

Does this particular regulation make sense?

What about regulation of hedge funds and privateequity???

Source: Petr Teplý (2010): The importance of MAC questions in regulation

2. Background of regulation2. Background of regulation

Global materiality of HF and PE???Global materiality of HF and PE???

18

2. Background 2. Background ofof regulationregulation

AlternativeAlternative ““rregulationegulation““ of hedge fundsof hedge funds

19Source: Šinka ,Teplý (2011): The (non)sense of hedge fund regulation in the light of a MAC questions regulatory concept

2. Background of regulation2. Background of regulation

ChalChalllengeenge to regulation of world financial to regulation of world financial marketsmarkets –– howhow to do to do itit??????

20Source: Clifford Chance (2010)

2. Background of regulation2. Background of regulation

(Re)(Re)regulationregulation??

Regulation is needed but Regulation is needed but HOW ???HOW ???

21

TheThe ddevil is in evil is in the detail!the detail!

2. Background of regulation2. Background of regulation

Mission impossible Mission impossible ofof effective effective regulationregulation!!

We also know that under-regulation can unleash disaster observed ex-post only!

We know that excessive regulation involve costs, but what are they?

22Source: Petr Teplý based on Cooley, Walter (2010)

Recurring financial crises

Optimum regulation = the art of balancing the immeasurable against the unknowable

2. Background of regulation2. Background of regulation

Do Do youyou believebelieve in in economiceconomic andand//ororregulatoryregulatory capitalcapital??????

23Source: Petr Teplý based on Vejdovec (2011)

� Loosers (bail-outed or bankrupted banks fromTOP 50 world banks) posted higher economic capital thanWinners (healthy banks)

� In theory economic capital should reflect real risks!!!!

LoosersWinners

2. Background of regulation2. Background of regulation

MicroMicro vs. macroprudential vs. macroprudential regulationregulation

1) Microprudential regulation (bank-level) should help raise the resilience of individual banking institutions to periods of stress.

2) Macroprudential regulation (system

24

2) Macroprudential regulation (systemlevel) should diminish system wide risks that can build up across the banking sector as well as the procyclical amplification of these risks over time.

Source: BIS (2011)

2. Background of regulation2. Background of regulation

1) Encourages innovation andefficiency

2) Provides transparency

3) Ensure safety and soundness

4 4 pillarspillars ofof effectiveeffective regulatoryregulatory architecturearchitecture

25Source: Petr Teplý based on Cooley, Walter (2010)

3) Ensure safety and soundness

4) Promote competitveness in globalmarkets

o…good in theory but both Basel I and II failedto meet its objectives and a similar story expected for Basel III as discussed below

2. Background of regulation2. Background of regulation

5Gs of effective regulation5Gs of effective regulation

1) Guarantee of strong supervisor (powerful and independent )

2) Guarantee of international coordination

3) Guarantee of risk coverage (simple and easy ratios of capital, liquidity, shocks absorption etc.)

26Source: Petr Teplý based on Dewatripont, Rochet & Tirole (2010)

ratios of capital, liquidity, shocks absorption etc.)

4) Guarantee of crisis mgmt (crisis resolution, bankruptcy law, recapitalisation etc.)

5) Guarantee of personal responsibility

Is it all of this achievable? Just a salami tactic...

-> Mission impossible of effective regulation!

2. Background of regulation2. Background of regulation

HowHow shouldshould the the regulatorregulator reactreact on on underpricingunderpricing//mismispricingpricing risk???risk???

27Source: Mejstřík, Teplý (2011)

AgendaAgenda

Introduction1.

Bank reg. & supervision in the CR3.

Theoretical background2.

Bank reg. & supervision in the CR3.

Basel I/II/III capital accords4.

Regulation after the crisis5.

28

Conclusion6.

Mission impossible of effective bank regulation2 September 2011

3. Bank3. Bank reg. & supervision in the CRreg. & supervision in the CR

Passive financial Passive financial regreg.. and supervisionand supervision in 1990sin 1990s

� Inexperienced staff

� Liberal licensing policy

�Regulation and supervision only for banks

�Regulatory Failure of Basel I for the Czech

29

�Regulatory Failure of Basel I for the Czech environment

� For instance, flat 20% risk weights forcredits to any OECD member countrybank, including weak Czech/domestic banks collapsed later

3. Bank3. Bank reg. & supervision in the CRreg. & supervision in the CR

Supervision on consolidated basisSupervision on consolidated basis

30Source: Petr Teplý (2006)

3. Bank3. Bank reg. & supervision in the CRreg. & supervision in the CR

Triple Supervision of Triple Supervision of CeskCeskaa sporitelnasporitelna

31Source: Petr Teplý (2006)

2. Bank reg. & supervision in the CR2. Bank reg. & supervision in the CR

No stronger regulation No stronger regulation neededneeded duringduring the the crisiscrisis

32Source: CNB (2010)

� Deposits exceed loans by 30%, highest value in the EU

� Very low share of FX loans in corporate sector (20%), almost no FX loans drawn by households

� No need to help banks with liquidity, no loans from international institutions needed

AgendaAgenda

Introduction1.

Bank reg. & supervision in the CR3.

Theoretical background2.

Bank reg. & supervision in the CR3.

Basel I/II/III capital accords4.

Regulation after the crisis5.

33

Conclusion6.

Mission impossible of effective bank regulation2 September 2011

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

RisksRisks “covered”“covered”underunder BasellBasell I I && IIII && IIIIII

1988 Basel I

1996 Market risk

2007

Basel II

2010

Basel III

34

Credit riskCredit & market risk

Credit & market & operational risk

Credit & market &

operational & liquidity risk

Basel IMarket risk Basel II Basel III

Source: Petr Teplý (2010)

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

DecreasingDecreasing capitalcapital ratio ratio duedue to to BaselBasel II

35

Source: Klinger (2011) based on Bank of England (2010)

o Banks want to minimize their capital -> challenge for regulators! But strong lobby....

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Strong lobby and conflict of interests Strong lobby and conflict of interests ––what about ethics?what about ethics?

� FormerTOP employess of regulatory bodies and centralbanks joined lobby groups such as the IIF!!!

� USD 2.8 bn = reported federal lobbying expenses in the US for 1999-2008 (+ USD 1bn in campaign contributions!)

� IMF (2011): 3x higher probability for loosing fin. regulation!

36

� IMF (2011): 3x higher probability for loosing fin. regulation!

3. 3. BaselBasel I/II/III I/II/III capitalcapital accordsaccords

Two Two keykey objectives of Basel Iobjectives of Basel I

1) To assure the stability (“safety and soundness“) of the international banking system

2) To eliminate distortions to competitors arising from the fact that some countries

37Source: Dewatripont, Rochet & Tirole (2010)

arising from the fact that some countries (such as Japan) granted and implicit guaranteed of unlimited support to their banks in the event of failure

33. Basel I/II/III capital accords. Basel I/II/III capital accords

ResultResult ofof Basel IBasel I: : regulatoryregulatory arbitragearbitrage

1) Banks moved towards the riskier, higher-yielding assets within a given risk bucket, for example fromAmerican to Korean government bonds

Banks shifted assets off the balance sheet

38

2) Banks shifted assets off the balance sheet-> securitization

Basel IBasel I Lower capital!!!Lower capital!!!

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

BothBoth keykey objectives of Basel Iobjectives of Basel I failedfailed!!

1) Higher instability of the international banking system –lower capital!!!

The regulation

39

2) The regulationfavoured biginternational banks, i.e. it loweredoverall competition

33. Basel I/II/III capital accords. Basel I/II/III capital accords

ThreeThree keykey objectives of Basel Iobjectives of Basel III

1) The Accord should continue to promote safety and soundness in the financial system and, as such, the new framework should at least maintain the current overall level of capital in the system;

40

capital in the system;

2) The Accord should continue to enhance competitive equality;

3) The Accord should constitute a more comprehensive approach to addressing risks.

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

All threeAll three keykey objectives of Basel IIobjectives of Basel II failedfailed!!!!!!

1) Higher instability and lower capital later fueled global crisis

2) The regulation favored big international banks,

41

big international banks, i.e. it lowered overall competition

3) Internal banks models with poor assumptions (VAR etc.)/advanced internal ratings based approach (A-IRB)

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Basel II Basel II –– lower risk weight for mortgages!lower risk weight for mortgages!

42Source: Petr Teplý (2006)

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

SixSix oopen pen iissuesssues and and cchallengeshallenges ofof BasellBasell IIII

1) High Regulator’s Responsibility (lack of capacities)

2) “Adverse” Asymmetric Information (lack of adequate data)

3) A Weak Form of the Efficient Market

Hypothesis (reliance on the past events, lack of foresight)

4) Mitigation of Credit Risk (importance of collateral and

43

4) Mitigation of Credit Risk (importance of collateral and appropriate valuation)

5) No European Lender of Last Resort (poor crisis mgmt)

6) Concentration Risk (concentration on mortgages etc.)

This critique was presented by PetrTeplý at Massey University in 2006 - all these issues

materalized during the global crisis!!!!

Source: Petr Teplý´s presentation at Massey University in New Zealand (2006)

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Critique Critique of Basel II (of Basel II (TeplTeplýý et al, 200et al, 20077))

1) tendency towards procyclicity;

2) lack of the explicit implementation of other risks (e.g. systemic or liquidity);

3) an excessive use of external ratings;

44Source: Teplý et al. (2007)

3) an excessive use of external ratings;

4) an excessive and unequal prescriptionof the document (Pillar I vs. Pillar II vs. Pillar III);

5) difficult quantification of operational risk (NINJA loans, predatory lending etc.)

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

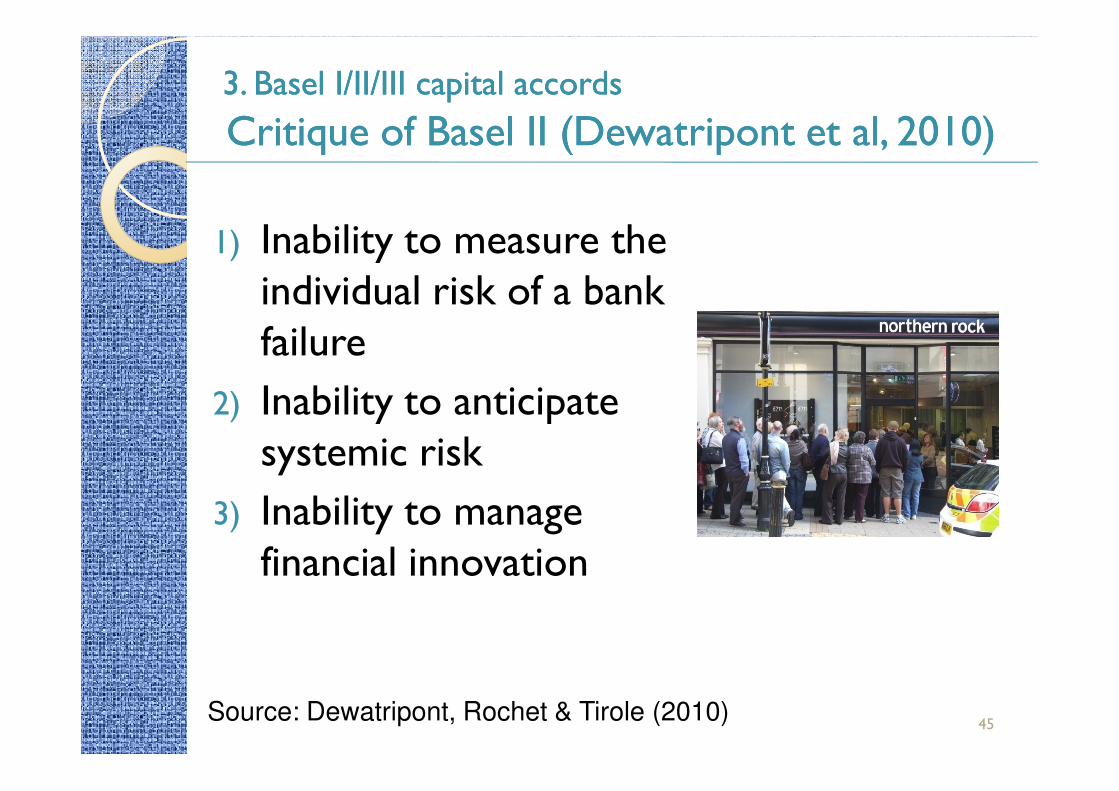

Critique Critique of Basel II (of Basel II (DewatripontDewatripont et al, 2010)et al, 2010)

1) Inability to measure the individual risk of a bank failure

2) Inability to anticipate

45Source: Dewatripont, Rochet & Tirole (2010)

2) Inability to anticipate systemic risk

3) Inability to manage financial innovation

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Basel II Basel II –– fundamentally fundamentally flawedflawed processprocess

Supply

side

Basel II

Failure

Poor institutional framework

BIS proposal = nontransparent process

46Source: Petr Teplý based on Lall (2011)

Demand

side

Failure

� Neo-proceduralists (W.Mattli & N.Woods)

� …and temporal contextualization (R. Lall)

RegulationFirst movers/big int.banks (data...)

BIS proposal = “tailored “ for big int.banks

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Parallels of Basel II and antismoking committeeParallels of Basel II and antismoking committee

Tobacco companies provide (asymmetric)information…

47

…to a non-transparent committee deciding on….

…smoking ban!

What´s expected result of this process????

Source: Petr Teplý (2011)

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Go Go forforViceroysViceroys//BaselBasel IIII+III+IV+ V...+III+IV+ V...!!

48

o Basel II failed to meet its objectives 1) promote safety and soundness in the financial system while maintaing

capital levels

2) enhance competitive equality

3) a more comprehensive approach to addressing risks – JUST OPPOSITE HAPPENED!!!

o…resulted from non-transparent regulator

FailureFailure ofof BaselBasel IIII3. Basel I/II/III capital accords3. Basel I/II/III capital accords

49

o…resulted from non-transparent regulator(BIS) supplied by asymmetric info by banks

o Basel II: Banks provided more (subprime) mortgages, used off-balance sheet vehicles and applied bad models -> Banks has fueled the global crisis

o The same story expected for Basel III!!!

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Basel Basel II II –– examplesexamples ofof lobbylobby´́s s successsuccess

50

Source: Klinger (2011) based on Lall (2010)

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

What can we expect fWhat can we expect frromom Basel Basel IIIIII??????

51

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

ThreeThree keykey objectives and targets of Basel Iobjectives and targets of Basel IIIII

Objectives

1) Improve the banking sector's ability to absorb shocks arising from financial and economic stress, whatever the source

2) Improve risk management and governance

52

2) Improve risk management and governance

3) Strengthen banks' transparency and disclosures. Targets

1) bank-level, or microprudential, regulation, which will help raise the resilience of individual banking institutions to periods of stress.

2) macroprudential, system wide risks that can build up across the banking sector as well as the procyclical

amplification of these risks over time.

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Do you believe the Basel Do you believe the Basel III objectives III objectives after clear failures of Basel I and Basel II?after clear failures of Basel I and Basel II?

53

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

BaselBasel III III proposalproposal ((DecemberDecember 2010) 2010)

1) requirements for higher quality, constituency and transparency of banks´ capital and risk management (calibration and delayed implementation period)

54Source: BIS (2010)

period)

2) introduction of new liquidity standards for internationally active banks

3) focus on systemic risk and interconnectedness (including procyclicityand regulation of OTC markets)

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Key components of Basel IIIKey components of Basel III

55Source: KPMG (2010)

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Basel III proposal (timing & implementation) Basel III proposal (timing & implementation)

56

Source: Klinger (2011) based on BCBS (2010) and McKinsey (2010)

3. Basel I/II/III capital accords3. Basel I/II/III capital accordsBasel III proposal (expected capital and Basel III proposal (expected capital and liquidity shortfalls) liquidity shortfalls)

57Source: McKinsey (2010)

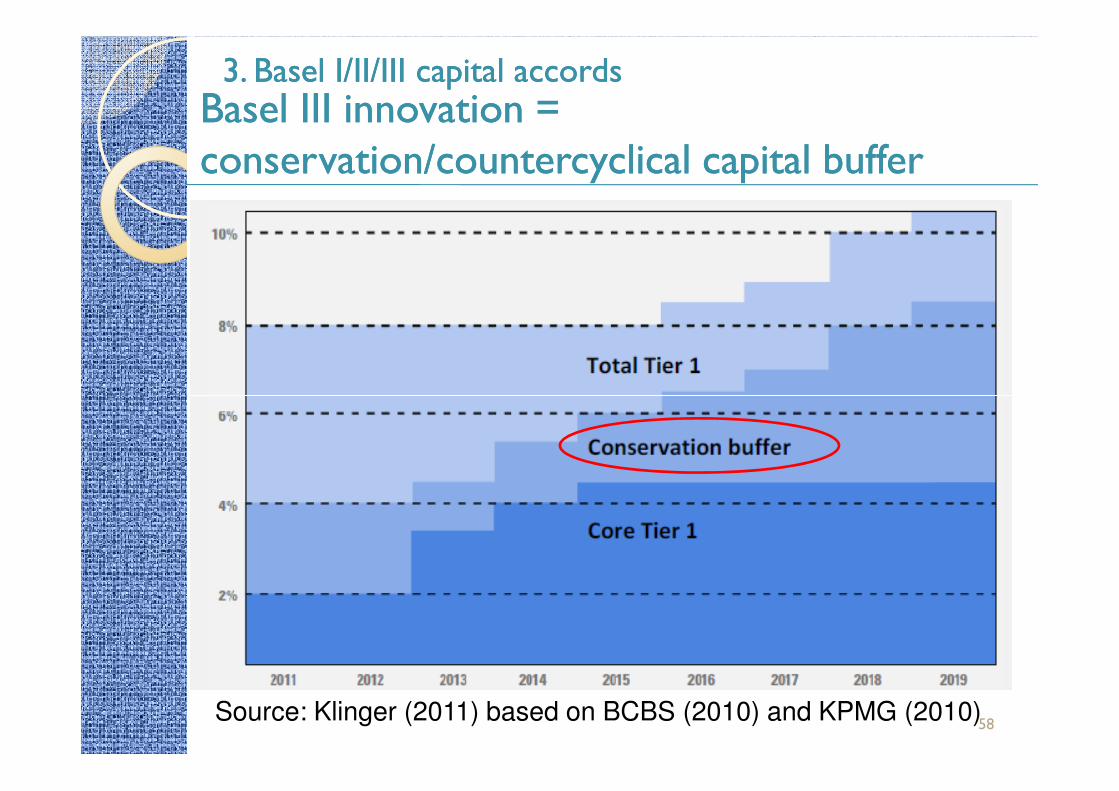

3. Basel I/II/III capital accords3. Basel I/II/III capital accordsBasel III innovation = Basel III innovation = conservation/countercyclicalconservation/countercyclical capital buffercapital buffer

58Source: Klinger (2011) based on BCBS (2010) and KPMG (2010)

� BCBS (2010) sets that the decision about imposition ofthe countercyclical buffer and its release is in hands of national authorities.

� To translate the credits/GDP ratio to the buffer, we follow the steps described in BCBS (2010c).

� First we calculate the actual ratio of credits to private

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

BaselBasel III: III: CountercyclicalCountercyclical bufferbuffer

59

� First we calculate the actual ratio of credits to private sector to the GDP. This ratio is then translated into trend using Hodrick-Prescott filter for Q1 1993 to Q1 2010. The actual level of buffer is derived from the gap between the ratio and its trend as

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

BaselBasel III: III: CountercyclicalCountercyclical bufferbuffer

� Calculation of risk weights under Basel II

� Calculation of risk weights under Basel III

60

� Regresion formula for Basel III:

� The parameter now stands for sensitivity of the Basel III risk weights to the business cycle. Comparing it to the Basel II sensitivity parameter provides us with the result to the question whether Basel III mitigates the procyclicality of the regulation.

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Comparison of risk weights and GDPComparison of risk weights and GDP((calculatedcalculated fromfrom nonnon--performingperforming loansloans ((NPLsNPLs))))

61

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Basel II and Basel III procyclicality for the Basel II and Basel III procyclicality for the household sector (as a % response to 1%household sector (as a % response to 1%change in business cycle)change in business cycle)

62Source: Authors’ calculations

2. Bank reg. & supervision in the CR2. Bank reg. & supervision in the CR

The CNB: BCBS The CNB: BCBS methodsmethods do not do not alwaysalways workwork!!

� HP filter-based calculation of the excessive credit indicator is not necessarily appropriate in

63

appropriate in certain cases

� In CEE: rapid credit expansion may mean convergence rather than excessive borrowing)

Source: Gersl, A., Seidler, J. (2011). Excessive credit growth policy as an indicator of financial (in)stability and its use in macroprudential policy,in CNB (2011): Financial stability report 2010/2011

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

PetrPetrTeplTeplýý in 202in 2021: 1: BaselBasel III III resultsresultsAll threeAll three keykey objectives of Basel IIIobjectives of Basel III failedfailed!!!!!!

1) Higher instability (financial crisis in 2016)

2) Failure of risk

64

2) Failure of risk management models(unrealistic stress testing in EU/US banks)

3) Lower banks´ transparency (highlysophisticated and non-transparent products in the field of insurance etc.)

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

WhyWhy Basel III Basel III willwill failfail……

Success Failure

65Source: Petr Teplý (2011)

3. Basel I/II/III capital accords3. Basel I/II/III capital accords

Direct and indirect impacts Direct and indirect impacts ofof BaselBasel III III on on Czech banks Czech banks

• Higher liquidity requirements • Higher capital requirements for counterparty risk

• Higher capital requirements for trade finance products

Directeffects

66Source: Petr Teplý based on the Czech Banking Association (2010)

finance products

• Lower banks´ profitability due to expected lower growth of the Czech economy

• Uncertain reaction on regulatory proposals of foreign parent banks

Indirecteffects

AgendaAgenda

Introduction1.

Bank reg. & supervision in the CR3.

Theoretical background2.

Bank reg. & supervision in the CR3.

Basel I/II/III capital accords4.

Regulation after the crisis5.

67

Conclusion6.

Mission impossible of effective bank regulation2 September 2011

55. . RegulationRegulation afterafter thethe crisiscrisis

Major crises and international Major crises and international financial regulatory initiativesfinancial regulatory initiatives

68Source: Breguel (2010)

5. Regulation after the crisis5. Regulation after the crisis

PrePre--crisiscrisis oversightoversight frameworkframework

69Source: Breugel (2009)

RRegulategulation ion andand macroeconomicsmacroeconomics5. Regulation after the crisis5. Regulation after the crisis

70Source: Oliver Wyman (2011)

5. Regulation after the crisis5. Regulation after the crisis

New New EuropeanEuropean SupervisorySupervisory FrameworkFramework

71Source:ESMA (2010)

5. Regulation after the crisis5. Regulation after the crisis

......implying high leverage of banks (2007)implying high leverage of banks (2007)

72

Source:BOE (2010)

5. Regulation after the crisis5. Regulation after the crisis

NationalizationNationalization ofof “Western““Western“banksbanks

Nationalization of banks in US, UK, GER, BEL, SUI …

Source: DB Reserach (2009)

5. Regulation after the crisis5. Regulation after the crisisGovernment bank interventions in % of GDP Government bank interventions in % of GDP (10/2008(10/2008 –– 0606//2009)2009)

74Zdroj: Breugel (2009)

55. . RegulationRegulation afterafter thethe crisiscrisis

FutureFuture regulatoryregulatory actionsactions

75Source: Oliver Wyman (2010)

AgendaAgenda

Introduction1.

Bank reg. & supervision in the CR3.

Theoretical background2.

Bank reg. & supervision in the CR3.

Basel I/II/III capital accords4.

Regulation after the crisis5.

76

Conclusion6.

Mission impossible of effective bank regulation2 September 2011

6.6. ConclusionConclusion

1) Regulation = challenge for both regulators and market players (+ “pretending” politicians & strong lobby)

2) MAC questions in regulation = a useful tool

3) Expected failure of Basel III (a similar fairy tale as

77

3) Expected failure of Basel III (a similar fairy tale as Basel I and II)

4) Regulator´s prescribed models cannot capture national specifics -> national discretion needed but what about market and regulatory competition?

5) 5Gs are not achievable -> recurring financial crises

-> Mission impossible of bank effective regulation!

UsefulUseful sourcessources

78

DiscussionDiscussion

TThanks for your attentionhanks for your attention..LetLet´́s discuss it now!s discuss it now!

79

ContactContact –– Petr TeplýPetr Teplý

Senior LecturerInstitute of Economic StudiesFaculty of Social SciencesCharles University

Senior LecturerBanking and Insurance Department Faculty of Finance and AccountingUniversity of Economics in Prague

80

Charles UniversityOpletalova 26110 00 PragueCzech RepublicE-mail: [email protected]

University of Economics in PragueWinston Churchill Square 4130 67 Prague Czech RepublicE-mail: [email protected]

http://ies.fsv.cuni.cz/en/staff/teply