mobile payments - how is it done?

TRANSCRIPT

1

Mobile Payments

2

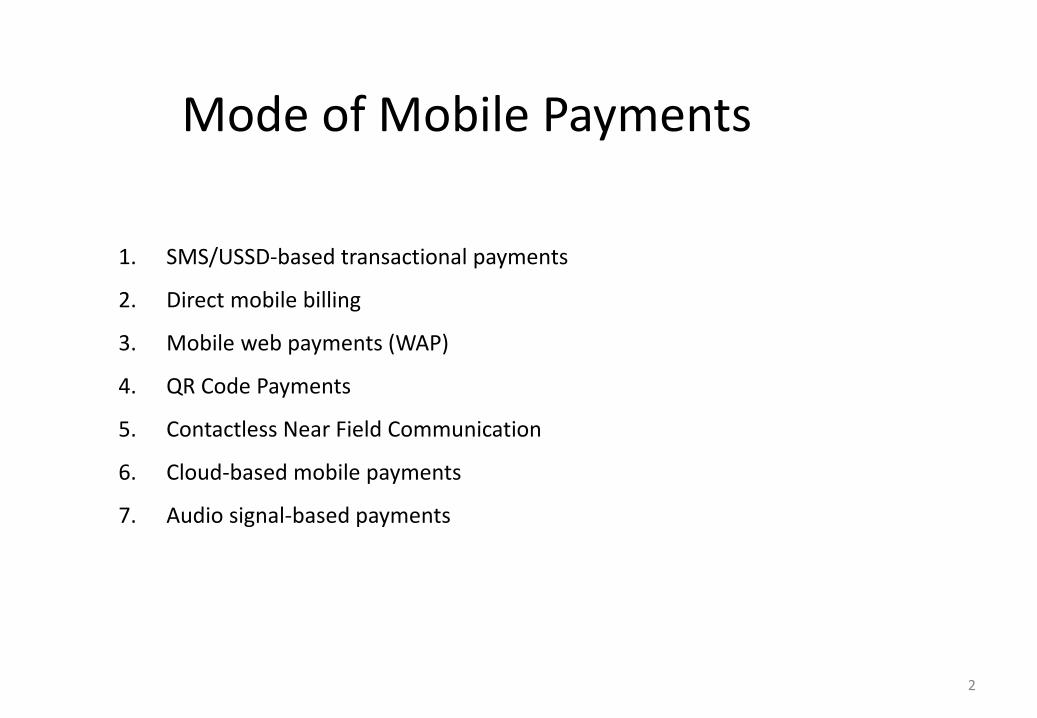

Mode of Mobile Payments

1. SMS/USSD-based transactional payments

2. Direct mobile billing

3. Mobile web payments (WAP)

4. QR Code Payments

5. Contactless Near Field Communication

6. Cloud-based mobile payments

7. Audio signal-based payments

3

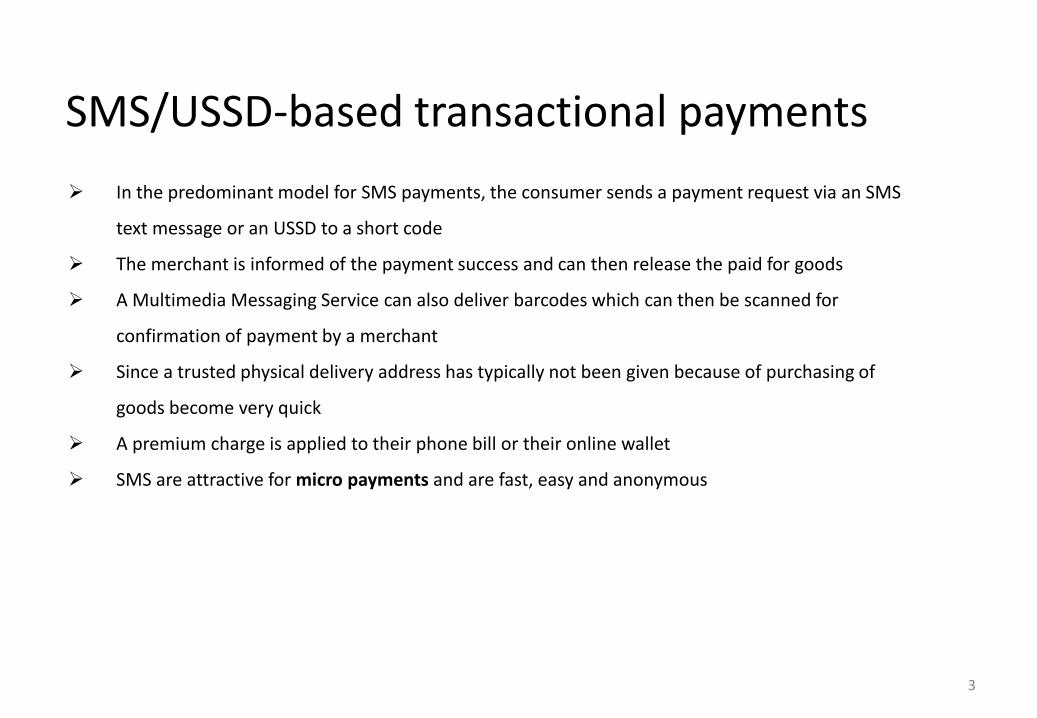

SMS/USSD-based transactional payments

In the predominant model for SMS payments, the consumer sends a payment request via an SMS

text message or an USSD to a short code

The merchant is informed of the payment success and can then release the paid for goods

A Multimedia Messaging Service can also deliver barcodes which can then be scanned for

confirmation of payment by a merchant

Since a trusted physical delivery address has typically not been given because of purchasing of

goods become very quick

A premium charge is applied to their phone bill or their online wallet

SMS are attractive for micro payments and are fast, easy and anonymous

4

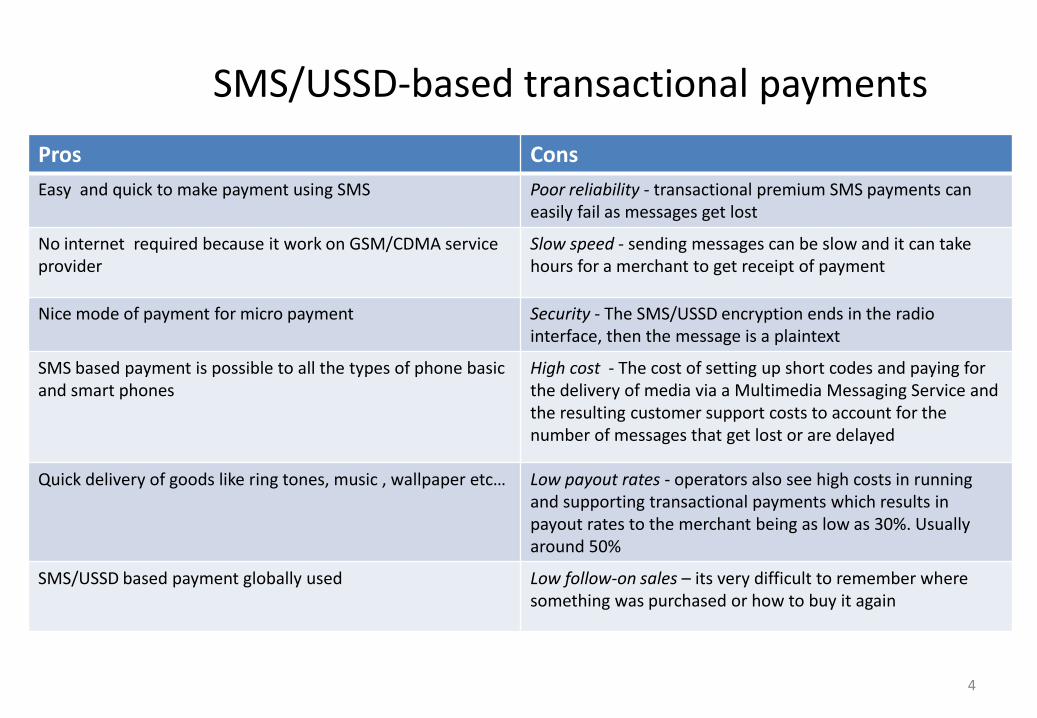

SMS/USSD-based transactional payments

Pros Cons

Easy and quick to make payment using SMS Poor reliability - transactional premium SMS payments can easily fail as messages get lost

No internet required because it work on GSM/CDMA serviceprovider

Slow speed - sending messages can be slow and it can take hours for a merchant to get receipt of payment

Nice mode of payment for micro payment Security - The SMS/USSD encryption ends in the radio interface, then the message is a plaintext

SMS based payment is possible to all the types of phone basic and smart phones

High cost - The cost of setting up short codes and paying for the delivery of media via a Multimedia Messaging Service and the resulting customer support costs to account for the number of messages that get lost or are delayed

Quick delivery of goods like ring tones, music , wallpaper etc… Low payout rates - operators also see high costs in running and supporting transactional payments which results in payout rates to the merchant being as low as 30%. Usually around 50%

SMS/USSD based payment globally used Low follow-on sales – its very difficult to remember where something was purchased or how to buy it again

5

SMS/USSD-based transactional payments

SMS Gateway

GPRS Gateway

Mobile Service Processing

Mobile Network

Customer

SBS/USSD

Digital goods return

6

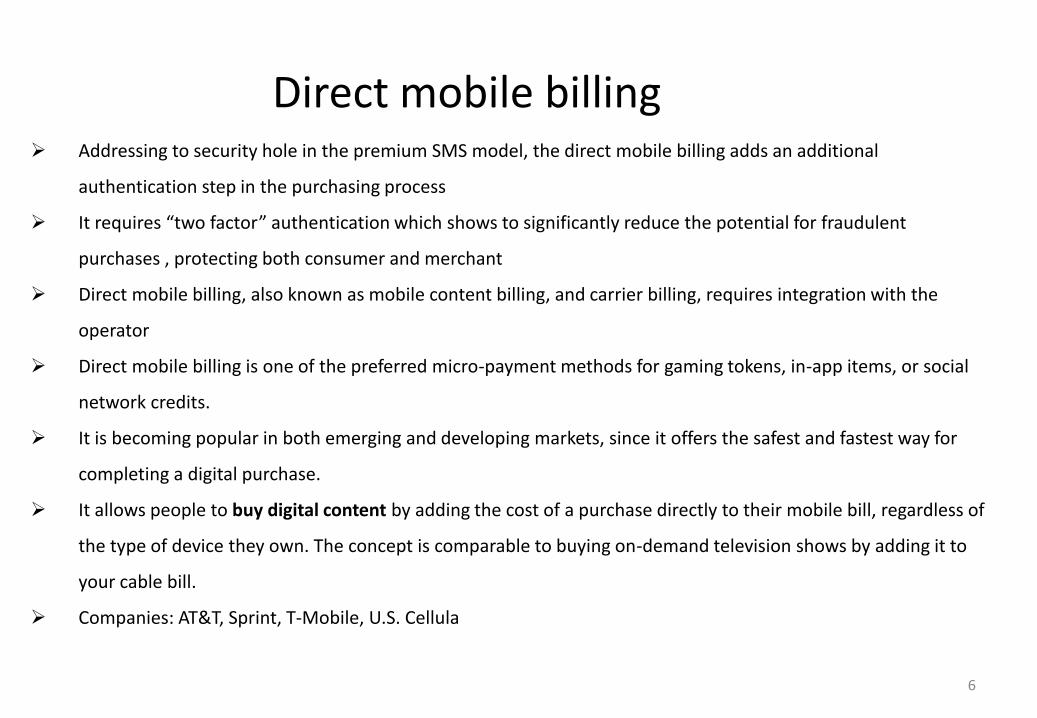

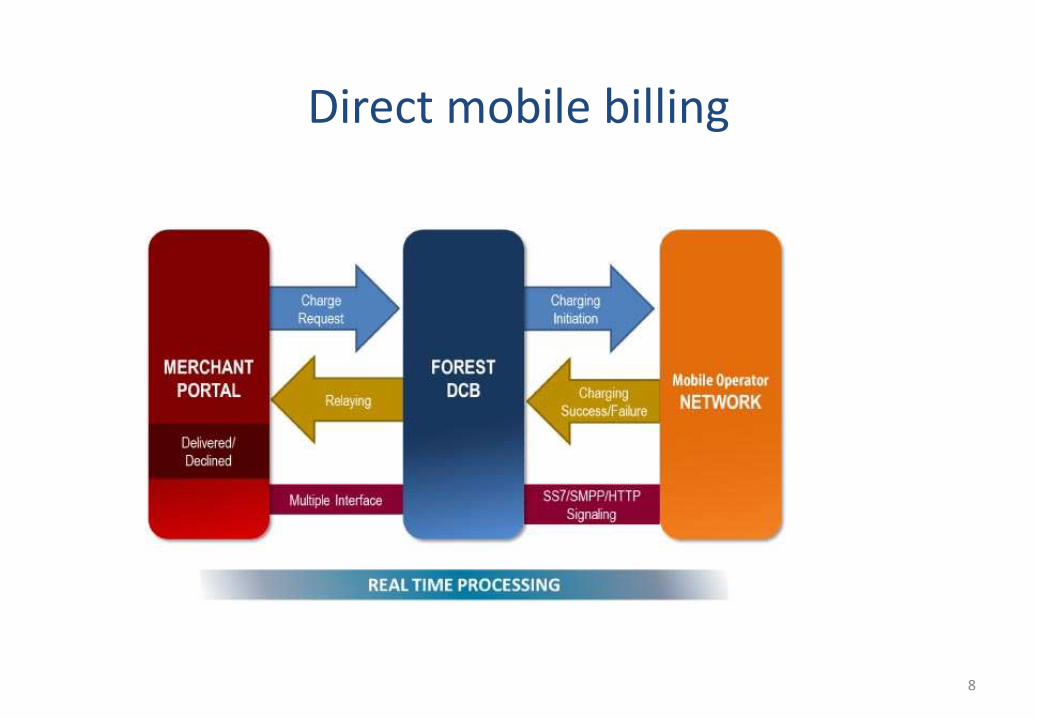

Direct mobile billing Addressing to security hole in the premium SMS model, the direct mobile billing adds an additional

authentication step in the purchasing process

It requires “two factor” authentication which shows to significantly reduce the potential for fraudulent

purchases , protecting both consumer and merchant

Direct mobile billing, also known as mobile content billing, and carrier billing, requires integration with the

operator

Direct mobile billing is one of the preferred micro-payment methods for gaming tokens, in-app items, or social

network credits.

It is becoming popular in both emerging and developing markets, since it offers the safest and fastest way for

completing a digital purchase.

It allows people to buy digital content by adding the cost of a purchase directly to their mobile bill, regardless of

the type of device they own. The concept is comparable to buying on-demand television shows by adding it to

your cable bill.

Companies: AT&T, Sprint, T-Mobile, U.S. Cellula

7

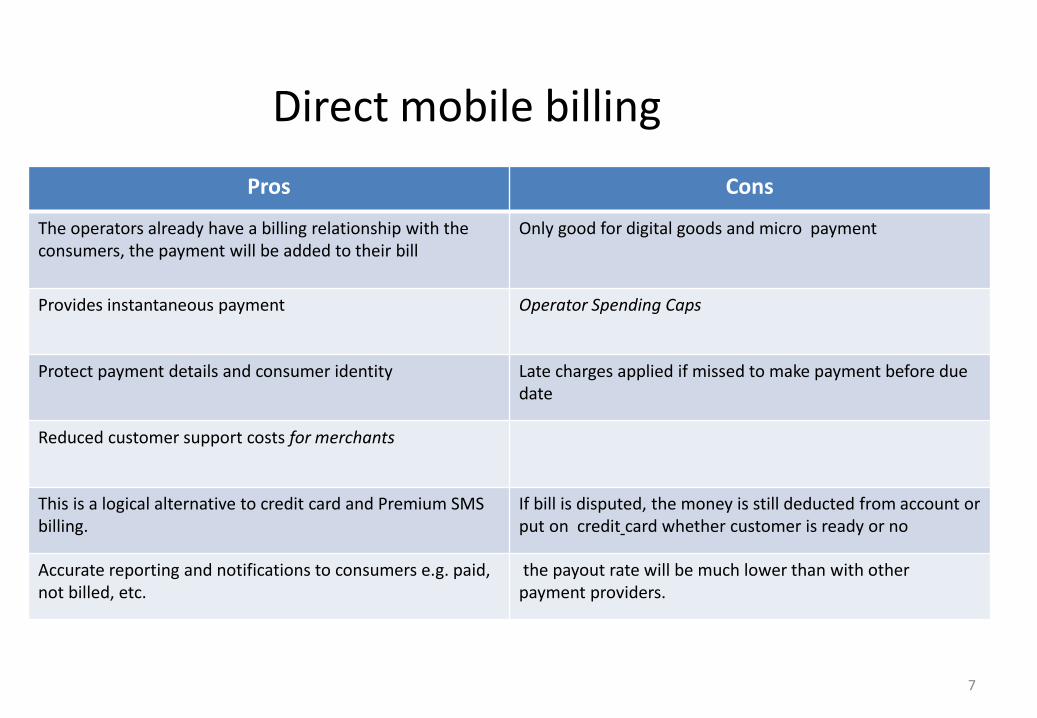

Direct mobile billing

Pros Cons

The operators already have a billing relationship with the consumers, the payment will be added to their bill

Only good for digital goods and micro payment

Provides instantaneous payment Operator Spending Caps

Protect payment details and consumer identity Late charges applied if missed to make payment before due date

Reduced customer support costs for merchants

This is a logical alternative to credit card and Premium SMS billing.

If bill is disputed, the money is still deducted from account or put on credit card whether customer is ready or no

Accurate reporting and notifications to consumers e.g. paid, not billed, etc.

the payout rate will be much lower than with other payment providers.

8

Direct mobile billing

9

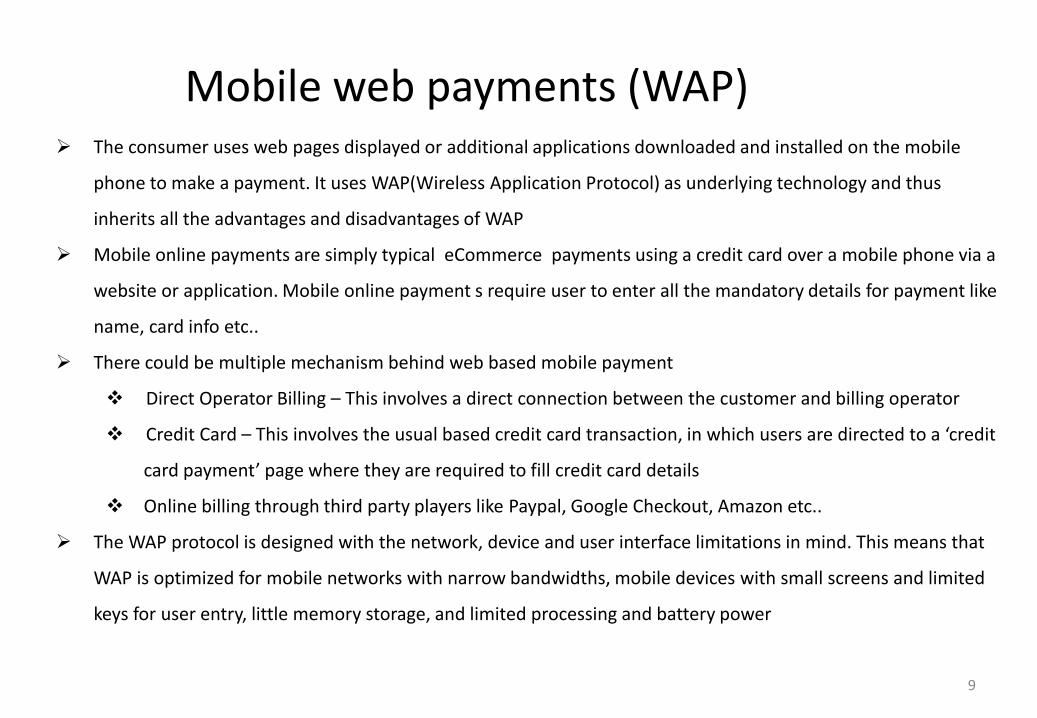

Mobile web payments (WAP) The consumer uses web pages displayed or additional applications downloaded and installed on the mobile

phone to make a payment. It uses WAP(Wireless Application Protocol) as underlying technology and thus

inherits all the advantages and disadvantages of WAP

Mobile online payments are simply typical eCommerce payments using a credit card over a mobile phone via a

website or application. Mobile online payment s require user to enter all the mandatory details for payment like

name, card info etc..

There could be multiple mechanism behind web based mobile payment

Direct Operator Billing – This involves a direct connection between the customer and billing operator

Credit Card – This involves the usual based credit card transaction, in which users are directed to a ‘credit

card payment’ page where they are required to fill credit card details

Online billing through third party players like Paypal, Google Checkout, Amazon etc..

The WAP protocol is designed with the network, device and user interface limitations in mind. This means that

WAP is optimized for mobile networks with narrow bandwidths, mobile devices with small screens and limited

keys for user entry, little memory storage, and limited processing and battery power

10

Mobile web payments (WAP)

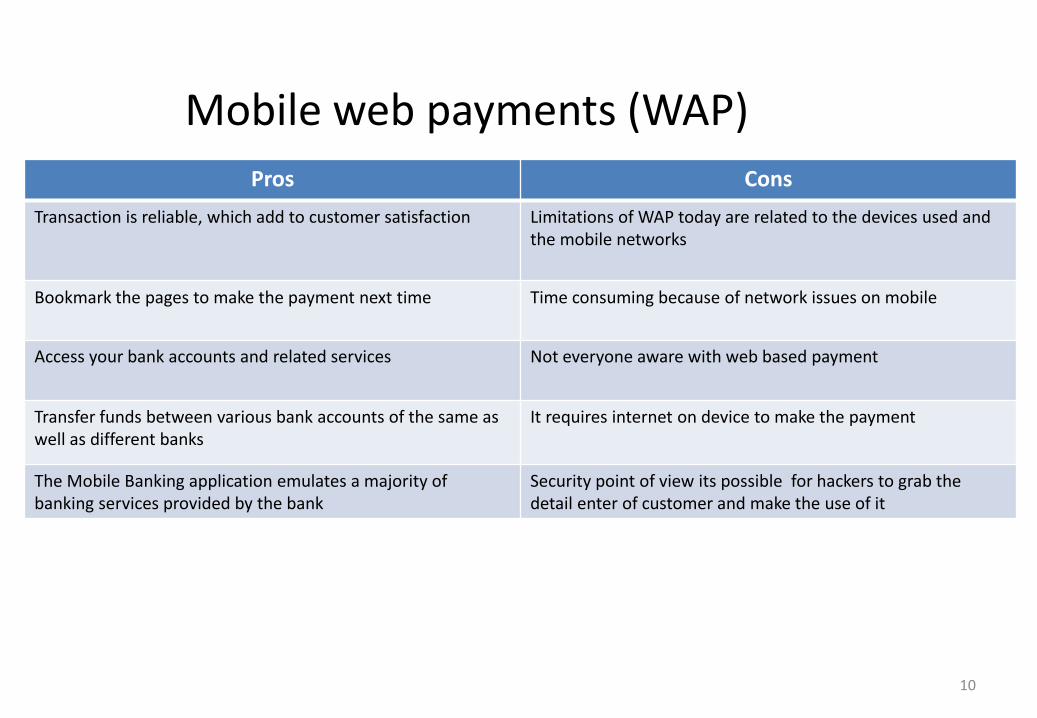

Pros Cons

Transaction is reliable, which add to customer satisfaction Limitations of WAP today are related to the devices used and the mobile networks

Bookmark the pages to make the payment next time Time consuming because of network issues on mobile

Access your bank accounts and related services Not everyone aware with web based payment

Transfer funds between various bank accounts of the same as well as different banks

It requires internet on device to make the payment

The Mobile Banking application emulates a majority of banking services provided by the bank

Security point of view its possible for hackers to grab the detail enter of customer and make the use of it

11

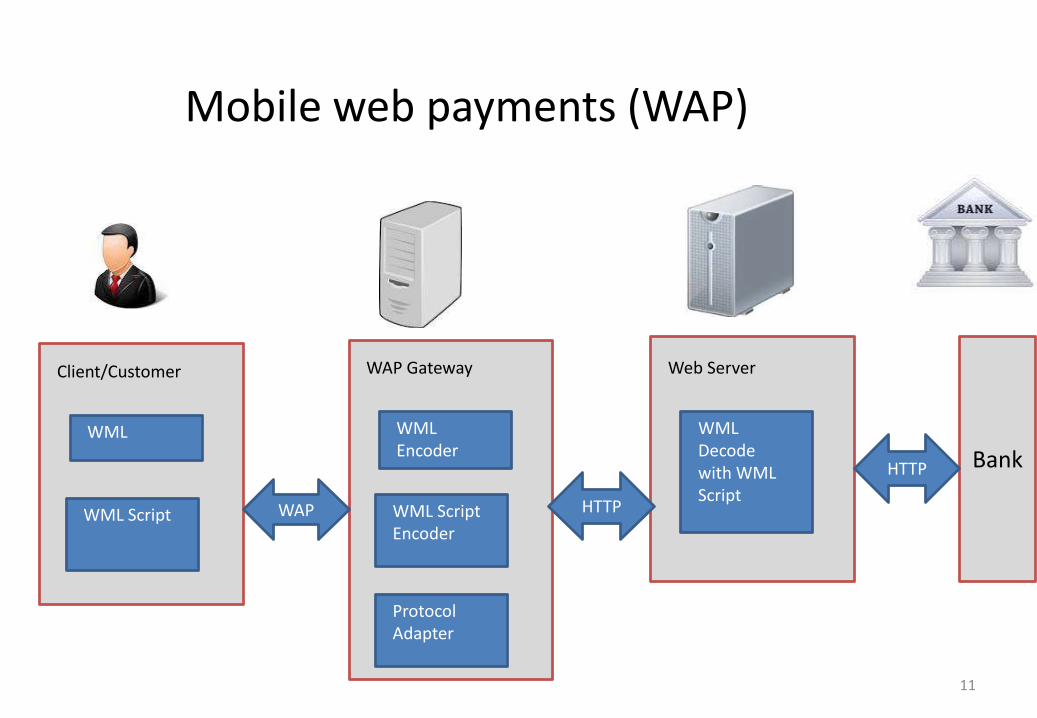

Mobile web payments (WAP)

Client/Customer

WML

WML Script

WAP Gateway

WML Encoder

WML Script Encoder

Web Server

WML Decode with WML Script

Protocol Adapter

WAP HTTP

BankHTTP

12

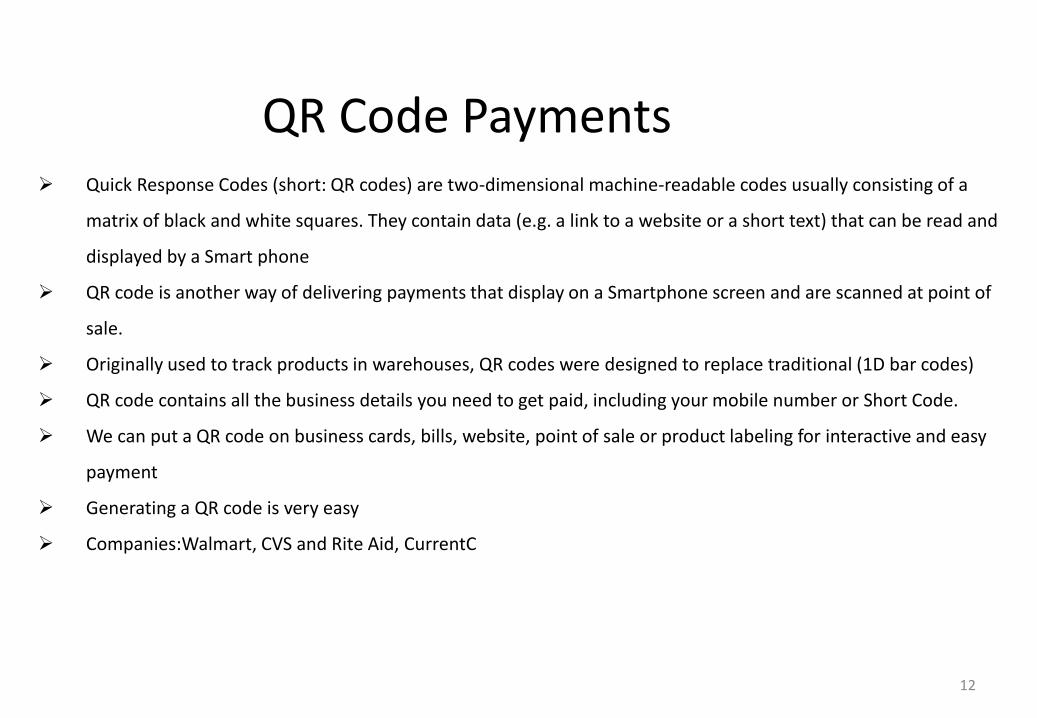

QR Code Payments Quick Response Codes (short: QR codes) are two-dimensional machine-readable codes usually consisting of a

matrix of black and white squares. They contain data (e.g. a link to a website or a short text) that can be read and

displayed by a Smart phone

QR code is another way of delivering payments that display on a Smartphone screen and are scanned at point of

sale.

Originally used to track products in warehouses, QR codes were designed to replace traditional (1D bar codes)

QR code contains all the business details you need to get paid, including your mobile number or Short Code.

We can put a QR code on business cards, bills, website, point of sale or product labeling for interactive and easy

payment

Generating a QR code is very easy

Companies:Walmart, CVS and Rite Aid, CurrentC

13

QR Code Payments

Pros Cons

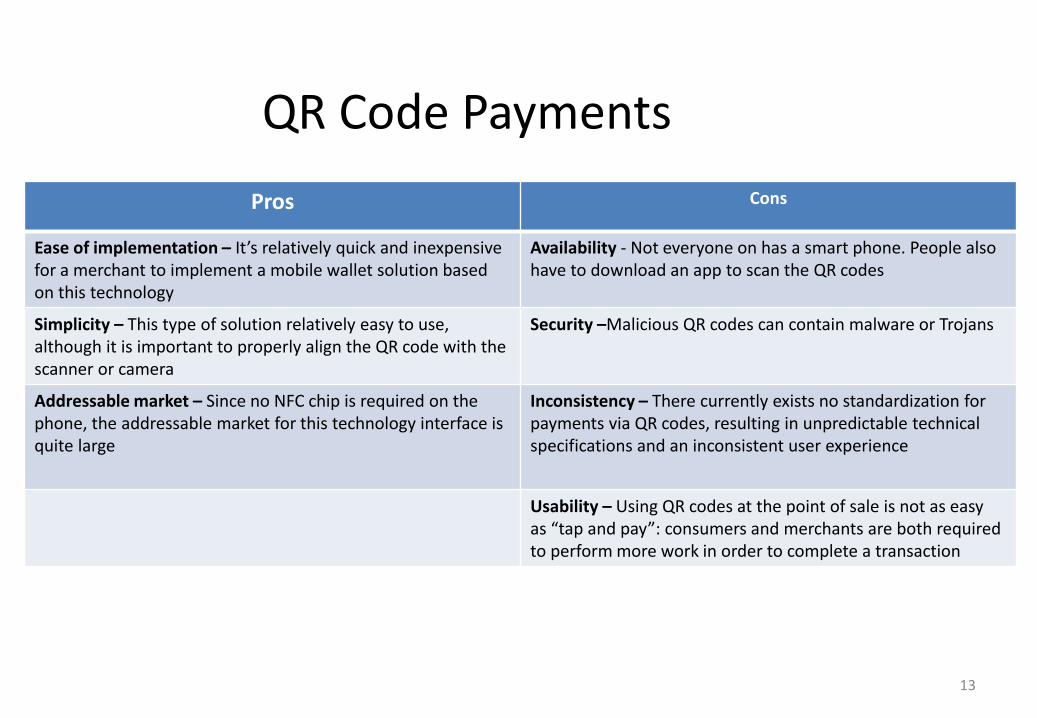

Ease of implementation – It’s relatively quick and inexpensive for a merchant to implement a mobile wallet solution based on this technology

Availability - Not everyone on has a smart phone. People also have to download an app to scan the QR codes

Simplicity – This type of solution relatively easy to use, although it is important to properly align the QR code with the scanner or camera

Security –Malicious QR codes can contain malware or Trojans

Addressable market – Since no NFC chip is required on the phone, the addressable market for this technology interface is quite large

Inconsistency – There currently exists no standardization for payments via QR codes, resulting in unpredictable technical specifications and an inconsistent user experience

Usability – Using QR codes at the point of sale is not as easy as “tap and pay”: consumers and merchants are both required to perform more work in order to complete a transaction

14

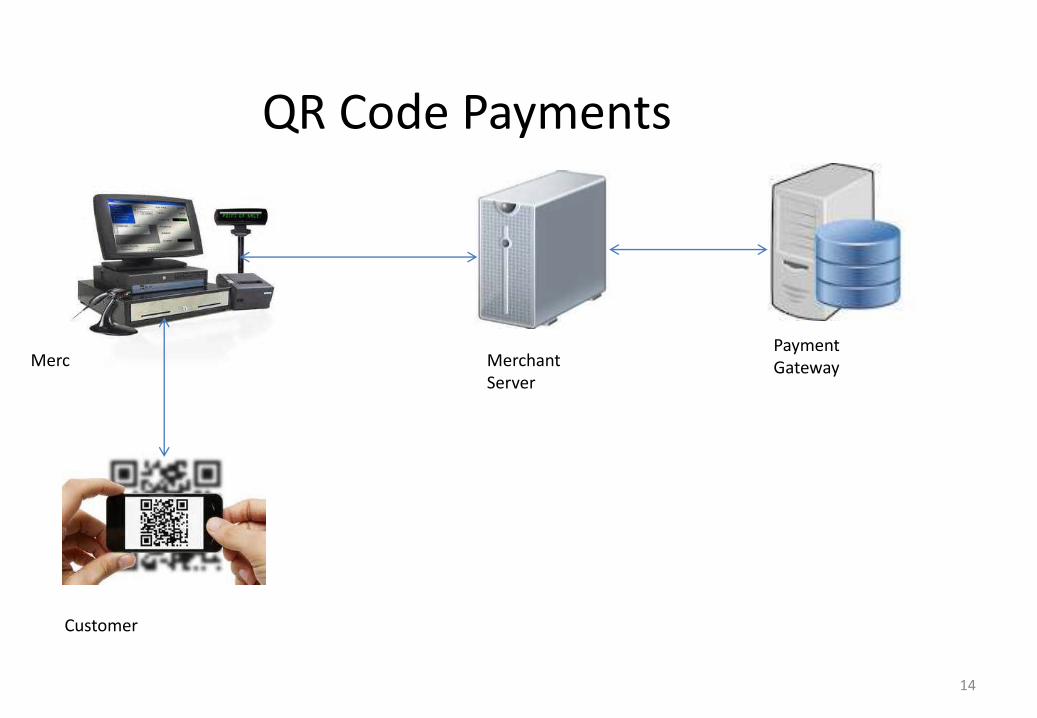

QR Code Payments

Merchant

Customer

Merchant Server

Payment Gateway

15

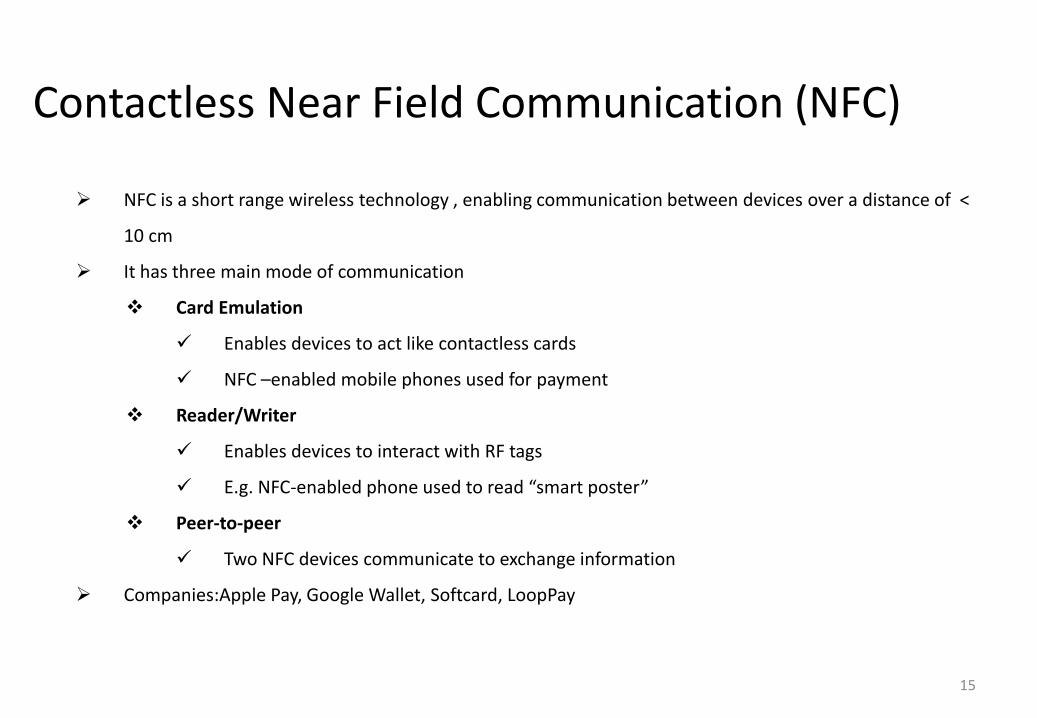

Contactless Near Field Communication (NFC)

NFC is a short range wireless technology , enabling communication between devices over a distance of <

10 cm

It has three main mode of communication

Card Emulation

Enables devices to act like contactless cards

NFC –enabled mobile phones used for payment

Reader/Writer

Enables devices to interact with RF tags

E.g. NFC-enabled phone used to read “smart poster”

Peer-to-peer

Two NFC devices communicate to exchange information

Companies:Apple Pay, Google Wallet, Softcard, LoopPay

16

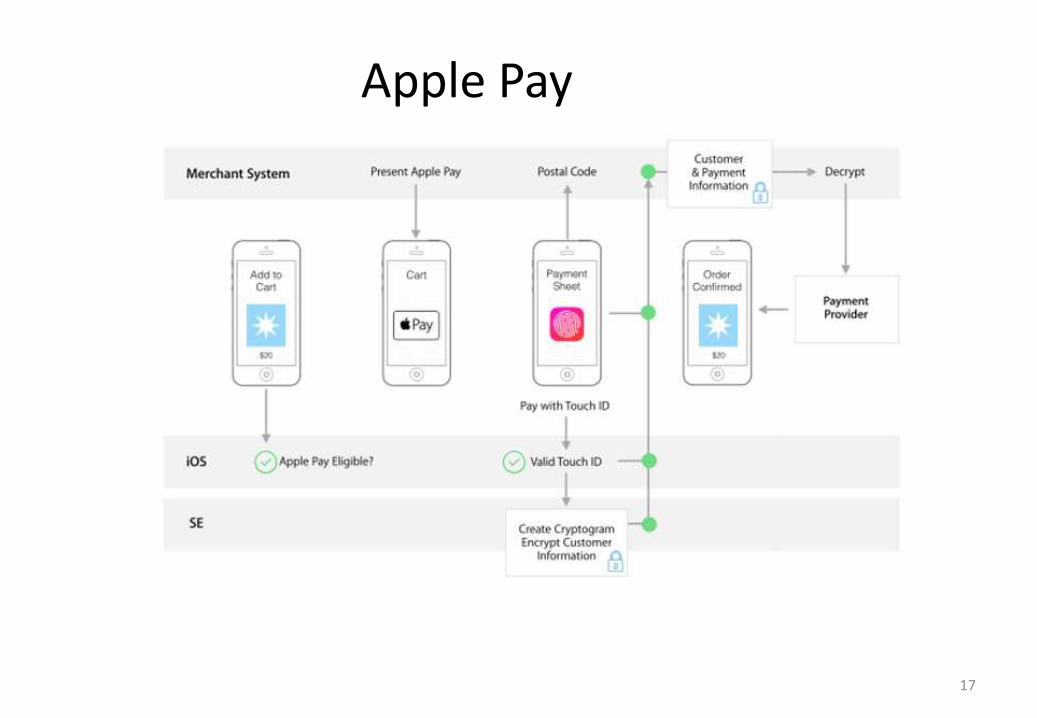

Apple Pay Apple Pay is a mobile payment service that lets certain Apple mobile devices make payments at retail and online

checkout

It lets Apple devices wirelessly communicate with point of sale systems using a near field communication (NFC)

antenna, a "dedicated chip that stores encrypted payment information" (known as the Secure Element), and

Apple's Touch ID and Passbook

Passbook is use to store credit or debit cards while registering it for payment

It keeps customer payment information private from the retailer, and creates a "dynamic security code generated

for each transaction“

iPhone users authenticate by holding their fingerprint to the phone's Touch ID sensor

To keep transactions secure, Apple uses a method known as "tokenization," preventing actual credit card

numbers from being sent over the air. Card numbers are not stored on the device, instead, a unique Device

Account Number is created, encrypted and stored in the Secure Element (SE) of the device

User's payment information, and credit card numbers and data are never uploaded to iCloud or Apple's servers

Apple utilizes Device Account Numbers, a user's credit card number is never shared with merchants or

transmitted with payments

17

Apple Pay

18

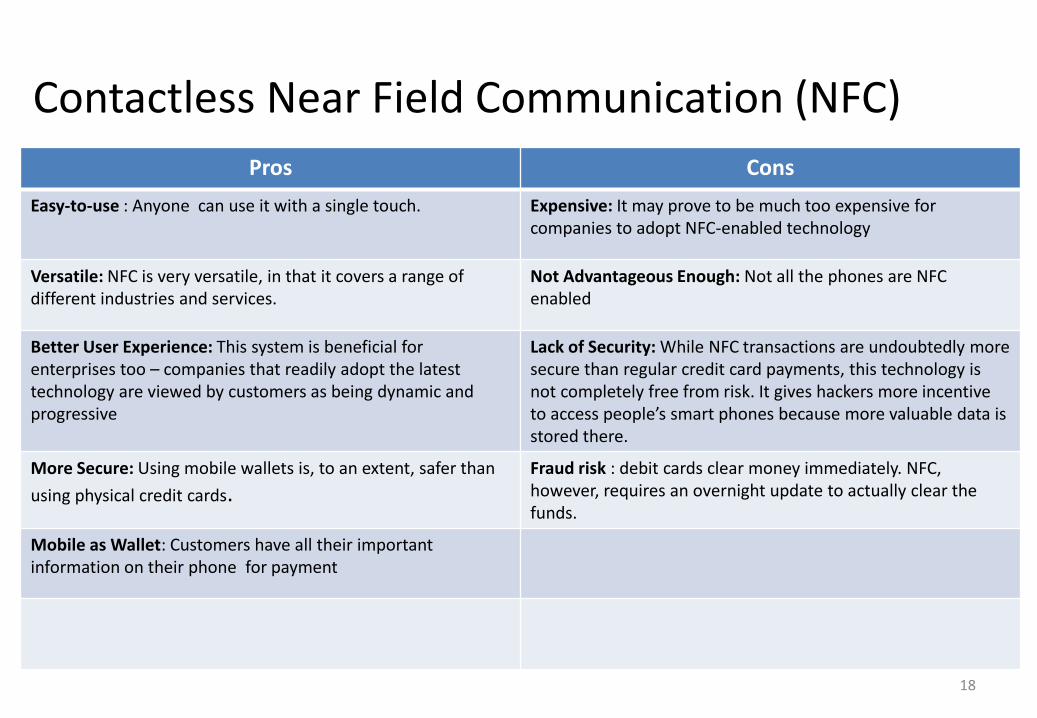

Contactless Near Field Communication (NFC)

Pros Cons

Easy-to-use : Anyone can use it with a single touch. Expensive: It may prove to be much too expensive for companies to adopt NFC-enabled technology

Versatile: NFC is very versatile, in that it covers a range of different industries and services.

Not Advantageous Enough: Not all the phones are NFC enabled

Better User Experience: This system is beneficial for enterprises too – companies that readily adopt the latest technology are viewed by customers as being dynamic and progressive

Lack of Security: While NFC transactions are undoubtedly more secure than regular credit card payments, this technology is not completely free from risk. It gives hackers more incentive to access people’s smart phones because more valuable data is stored there.

More Secure: Using mobile wallets is, to an extent, safer than

using physical credit cards.Fraud risk : debit cards clear money immediately. NFC, however, requires an overnight update to actually clear the funds.

Mobile as Wallet: Customers have all their important information on their phone for payment

19

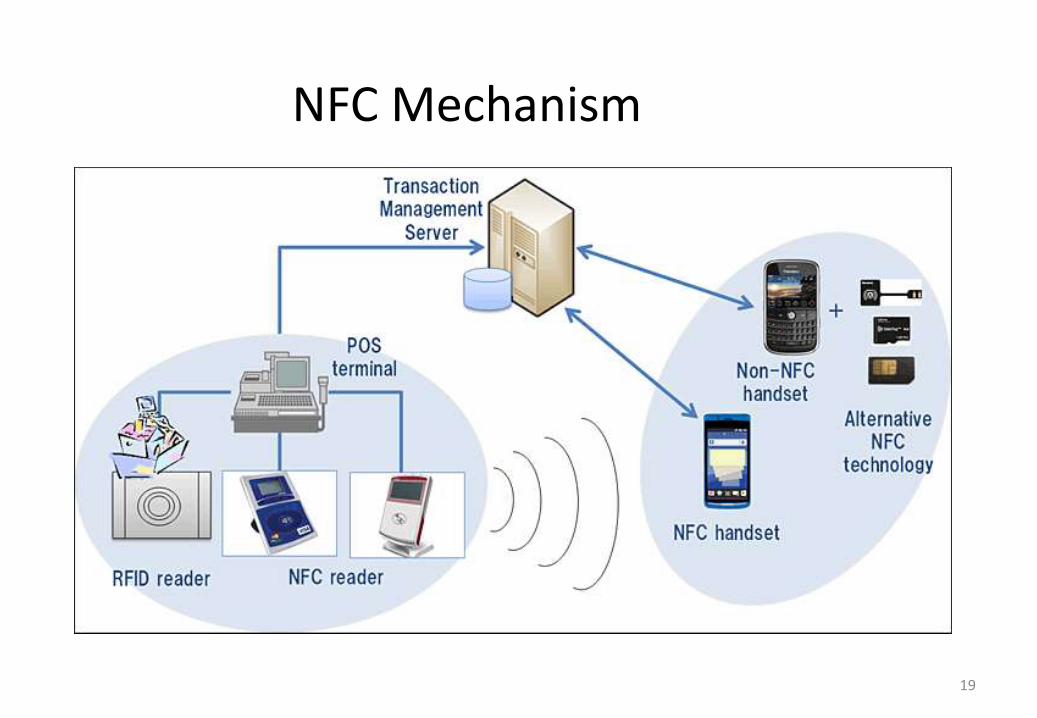

NFC Mechanism

20

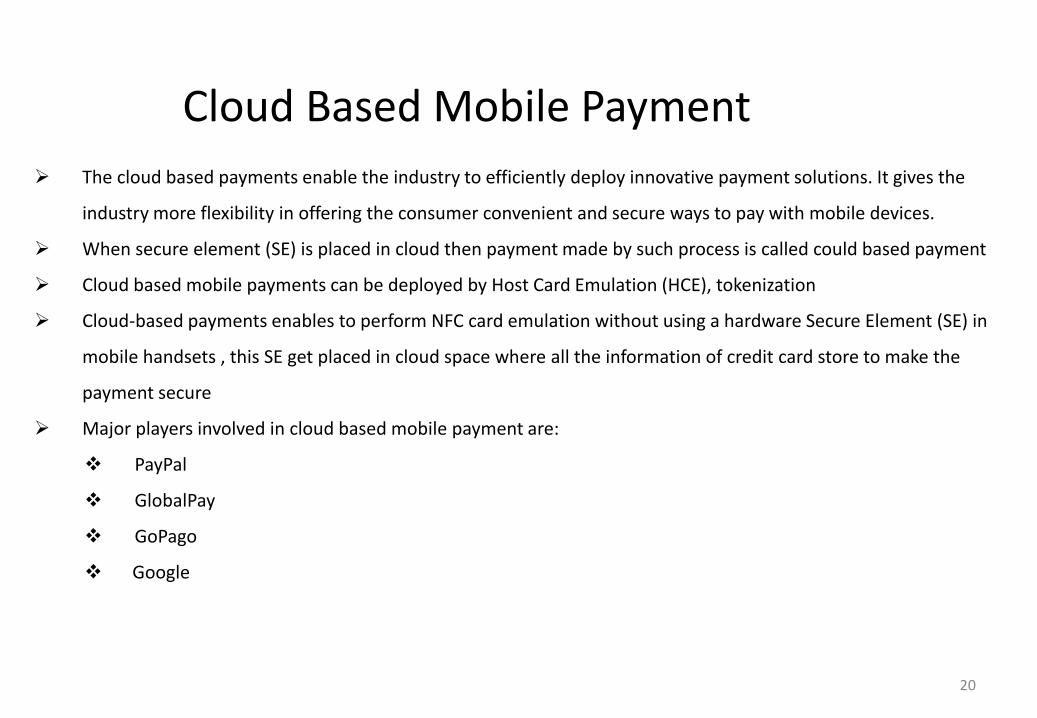

Cloud Based Mobile Payment

The cloud based payments enable the industry to efficiently deploy innovative payment solutions. It gives the

industry more flexibility in offering the consumer convenient and secure ways to pay with mobile devices.

When secure element (SE) is placed in cloud then payment made by such process is called could based payment

Cloud based mobile payments can be deployed by Host Card Emulation (HCE), tokenization

Cloud-based payments enables to perform NFC card emulation without using a hardware Secure Element (SE) in

mobile handsets , this SE get placed in cloud space where all the information of credit card store to make the

payment secure

Major players involved in cloud based mobile payment are:

PayPal

GlobalPay

GoPago

21

Cloud Based Mobile PaymentPros Cons

Easier to integration with third parties which includes mobile network operators, NFC device manufacturers and trusted service managers (MSMs)

One of the major concerns with cloud computing is the security of data. Often mobile users will provide sensitive information through the network, and if not protected, can lead to major damages in the case of a security breach.

Cardholders as well as financial institutions might find it easier to get their cards into this wallet as Secure Element (SE) is deployed in cloud which leads to lower cost as well

A wireless connection (via WiFi or 3G/4G) is required to deliver credentials from the cloud to the phone

The computing power of an SE in the cloud is higher than that on a mobile device

Storing information in the cloud could make your company vulnerable to external hack attacks and threats.

Storage capacity on a physical SE is limited. In the cloud, storage is scalable and can be expanded to meet individual requirements and to support any card, application and payment scheme

Credentials stored in the cloud can be available to any device, assuming the user is properly authenticated on the device. And the credentials stored in the cloud can be delivered from the phone to the POS via a variety of mechanisms, including NFC

22

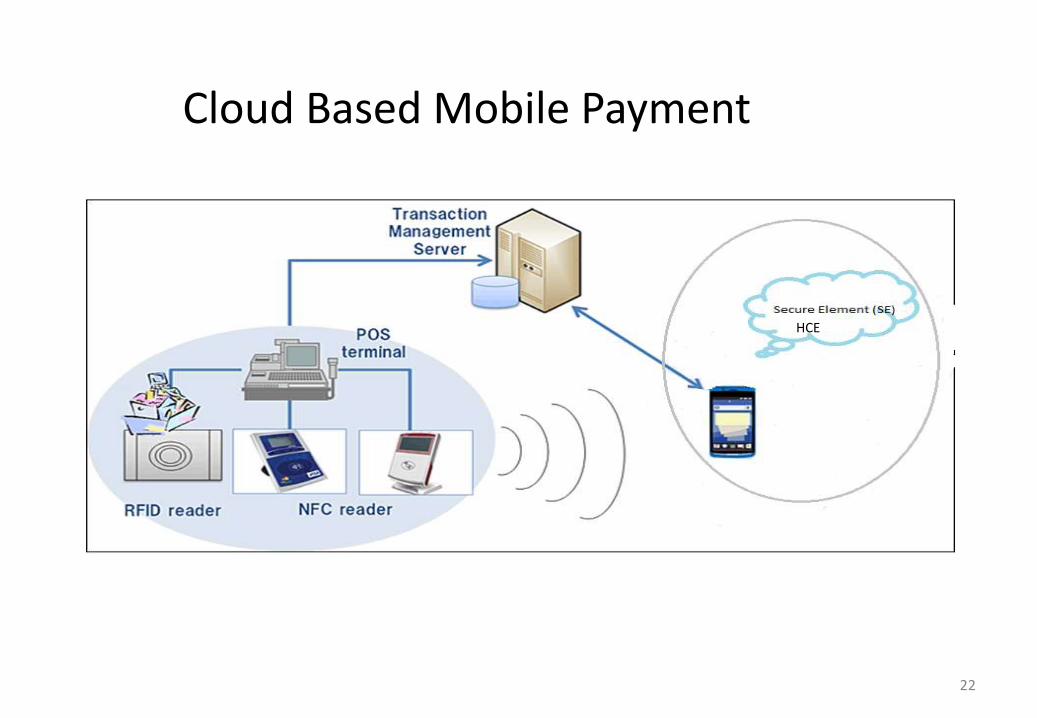

Cloud Based Mobile Payment

HCE

23

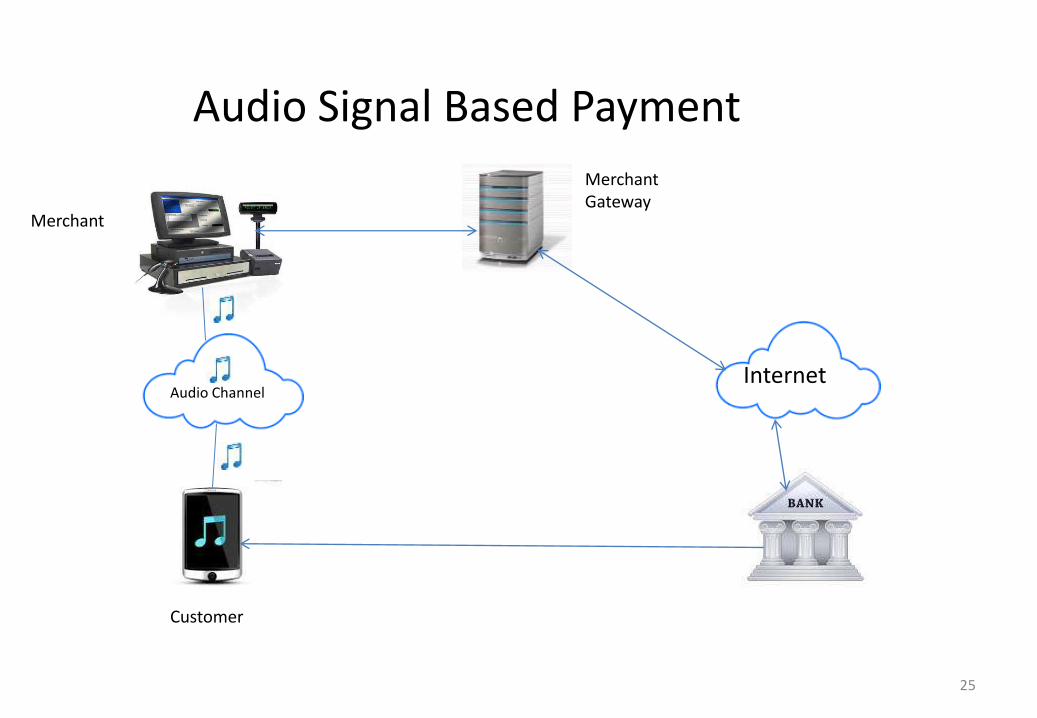

Audio Signal Based Payment The audio channel of the mobile phone is another wireless interface that is used to make payments.

Several companies have created technology to use the acoustic features of cell phones to support mobile

payments and other applications that are not chip-based

It uses different technologies like Near sound data transfer (NSDT), Data Over Voice and NFC 2.0 produce

audio signatures that the microphone of the cell phone can pick up to enable electronic transactions

Each time a client make a transaction, encrypted information is embedded in an audio one-time password

(OTP) that is sent to the payment server through the phone’s audio channel

Today, NSDT is primarily used for mobile banking transactions through the mobile money platform Tagpay.

It is also used to securely open doors and enable authentication on websites etc…

By using TagPay as an integrated solution, banks, microfinance organizations and other financial actors can

benefit from secure, convenient, and affordable mobile transactions

The NSDTTM technology built into the TagPay platform is widely recognized as the leading solution for

enabling mobile payments

Companies: Illiri sound API, Verifone (Way2ride), Edgetech , Alipay etc…

24

Audio Signal Based Payment

Pros Cons

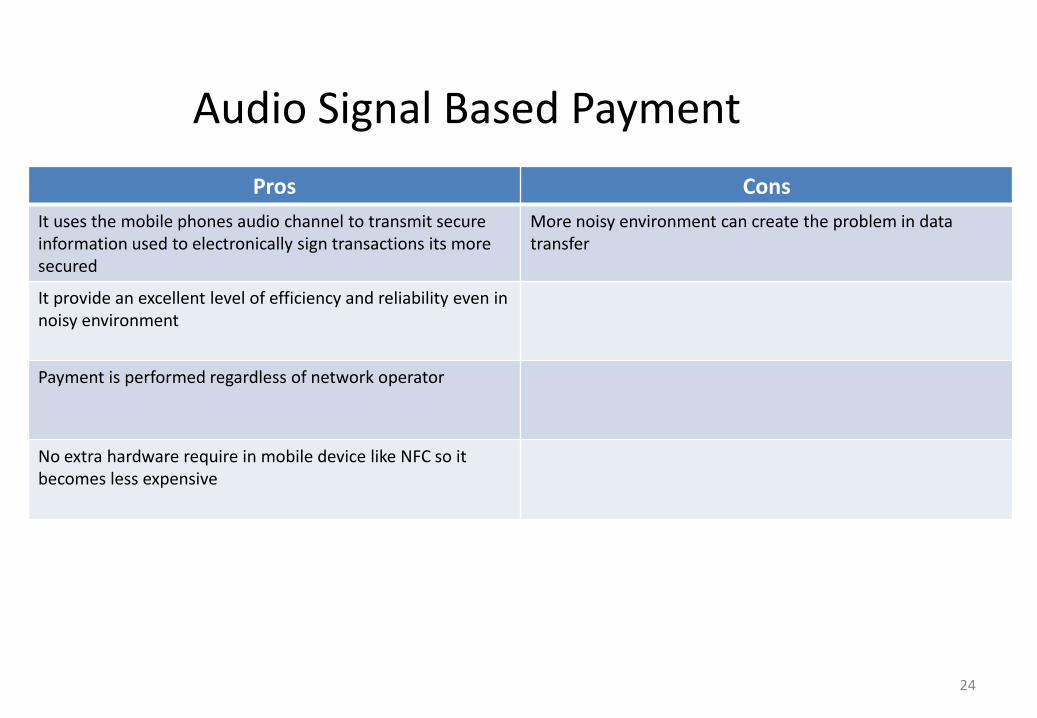

It uses the mobile phones audio channel to transmit secure information used to electronically sign transactions its more secured

More noisy environment can create the problem in data transfer

It provide an excellent level of efficiency and reliability even in noisy environment

Payment is performed regardless of network operator

No extra hardware require in mobile device like NFC so it becomes less expensive

25

Audio Signal Based Payment

Audio ChannelInternet

Customer

Merchant

Merchant Gateway