model questions on general banking - bankubeutn.inbankubeutn.in/downloads/offr_prmn_mtls1.pdf ·...

TRANSCRIPT

1 “Profitability, Asset Quality, Capital Optimization and Efficiency”

Staff College, Bengaluru

Fast Track Promotion RDOs - 2016

Model Questions on

General Banking

This is purely a voluntary effort and compilation made by

Mr. U Sethupitchai, Chief Manager (Faculty), Staff College, Bangalore

All the Best!!!!!!

2 “Profitability, Asset Quality, Capital Optimization and Efficiency”

For fast track Promotions

Recollected Questions for the month of January 2016

1. Current Ratio is 1.33.1, Current Assets is 100, what will be the amount of Current Liability

2. For creation of Equitable Mortgage on Agricultural Land, property is to be located at : a) Any Notified area

b) In Cantonment area

c) In Metro Cities

d) Anywhere in India

3. A financial product, which is driving its value from another financial product, is called _____

a) Forward Contract

b) Swap

c) Deriative

d) Currency futures

4. The legal liability to file charges with ROC in case of lending to a Company is that of _______

5. What increases a capital of a person

a) Profit

b) Loss

c) Depreciation

d) Sale of an asset

6. To reduce its foreign currency risks in case of overdue Export bill, bank should do

a) Forward Contract

b) Option Contract

c) Swap

d) Crystalization

7. The appraisal of Deferred Payment Guarantee is same as that of

a) Demand Loan

b) OD

c) Term Loan

d) CC

8. Projected Turnover is Rs.400 lacs, margin by promoter is Rs.20 lacs. What is maximum bank finance as per Annual Projected Turnover Method: 80 Lakhs.

9. Garnishee Order is not applicable to:

a) Savings

b) Current

c) FD

3 “Profitability, Asset Quality, Capital Optimization and Efficiency”

d) CC/OD

10. Under OTS, the compromise amount is calculated after taking in______

11. If Break Even Point is high, it can be construed that the margin of safety is____

12. On which one of the following assets, depreciation is applied on Straight Line Method:

13. What is the limitation period when Govt. wants to take legal action for recovery of its dues.

14. Public Debt Office (PDO) is an _____

15. When a farmer in addition to agriculture is engaged in rearing of farm stock, it is called________

16. Bharatiya Mahila Bank is a

a) Nationalized bank

b) Gramin Bank

c) Public Sector Bank

d) Private Bank

17. Minimum and maximum period for FCNR(B) accounts

18. In which currency, FCNR(B) can be opened :

19. Deferred Payment Guarantee is _________

20. What is the date for final implementation of Basel III ?

21. Safe custody of Articles comes under which Act:

22. CGTSME cover eligible for loan upto:

23. OD in PMJDY account upto:

24. Debt Swap meaning:

25. Shortfall in PS Advance target, amount to be deposited in:

26. For standing instructions, the relation between bank and customers is:

27. If in Garnishee Order no amount is mentioned, what should the bank do?

28. Long duration crop means a crop with harvest season of :

29. Provision on secured Sub-Standard Loan:

30. Loan to MSME without collateral :

31. CGTSME set by :

32. Maximum amount of claim that can filed by Lok Adalat

33. Eligible amount of suit in DRT

34. Time Limit for registration of equitable mortage with CERSAI;

35. Full form of USSD:

36. A housing loan in metro area will be classified as Priority Sector, provided maximum amount of loan is upto _____ and maximum cost of house is up to _____

37. Bank is not required to produce original book of records but true copy can be submitted when court has demanded as per which Act:

38. Outstanding in a CC account is Rs2.00 lacs. One of the partner died and the operations were continued in the account by the bank inspite of notice of the death given to the bank. Later 2.50 lakh deposited and 1 lakh was withdrawn ? What is the liability of legal heirs of the deceased partner?

4 “Profitability, Asset Quality, Capital Optimization and Efficiency”

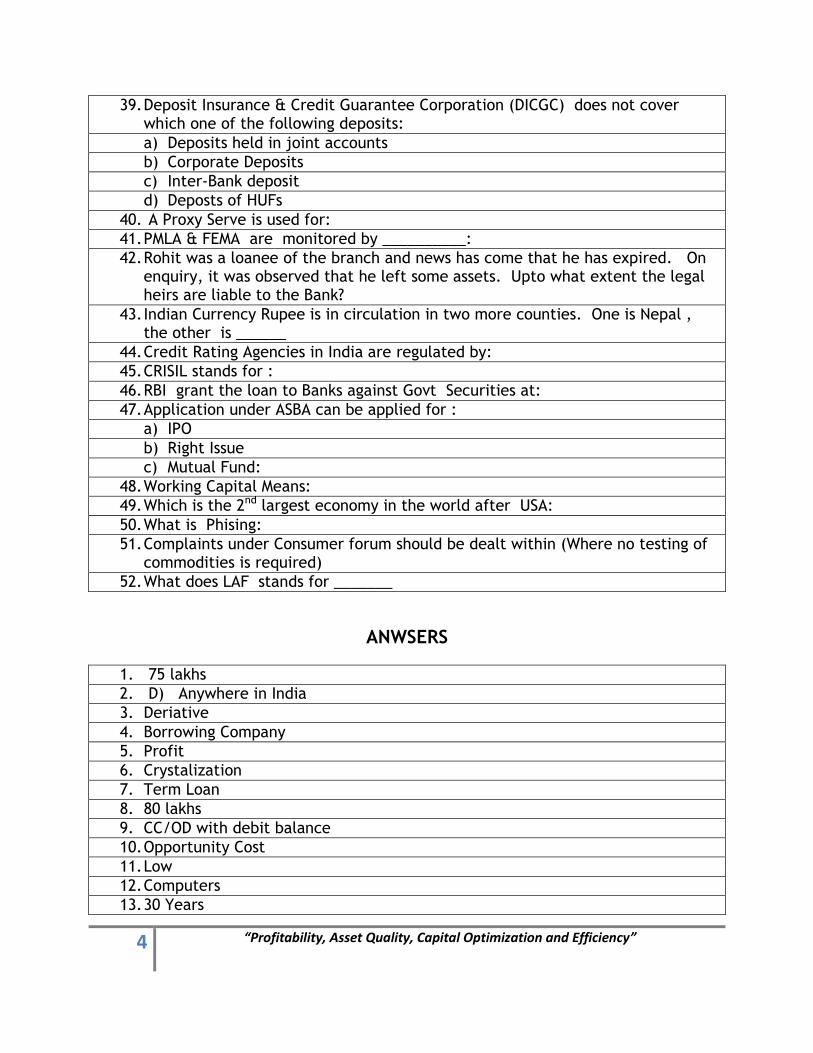

39. Deposit Insurance & Credit Guarantee Corporation (DICGC) does not cover which one of the following deposits:

a) Deposits held in joint accounts

b) Corporate Deposits

c) Inter-Bank deposit

d) Deposts of HUFs

40. A Proxy Serve is used for:

41. PMLA & FEMA are monitored by __________:

42. Rohit was a loanee of the branch and news has come that he has expired. On enquiry, it was observed that he left some assets. Upto what extent the legal heirs are liable to the Bank?

43. Indian Currency Rupee is in circulation in two more counties. One is Nepal , the other is ______

44. Credit Rating Agencies in India are regulated by:

45. CRISIL stands for :

46. RBI grant the loan to Banks against Govt Securities at:

47. Application under ASBA can be applied for :

a) IPO

b) Right Issue

c) Mutual Fund:

48. Working Capital Means:

49. Which is the 2nd largest economy in the world after USA:

50. What is Phising:

51. Complaints under Consumer forum should be dealt within (Where no testing of commodities is required)

52. What does LAF stands for _______

ANWSERS

1. 75 lakhs

2. D) Anywhere in India

3. Deriative

4. Borrowing Company

5. Profit

6. Crystalization

7. Term Loan

8. 80 lakhs

9. CC/OD with debit balance

10. Opportunity Cost

11. Low

12. Computers

13. 30 Years

5 “Profitability, Asset Quality, Capital Optimization and Efficiency”

14. Autonomous body and Investment Banker to Central Govt

15. Mixed Farming

16. Public Sector Bank

17. 1 year and 5 year

18. In any freely convertible foreign currency

19. Guarantee issued when payment by applicant of guarantee is to be made in installments over a period of time.

20. 31.03.2019

21. Indian Contract Act

22. Rs.100.00 Lac

23. Rs.5,0000\-.

24. To extend finance to farmers for repayment of loan taken from non-institution lenders.

25. RIDF

26. Agent and Principal

27. Full amount to be attached

28. More than 12 months

29. 15% of outstanding

30. Rs.10.00 lac

31. Govt of India and SIDBI

32. Rs20.00 lac and above Rs20 lac in Lok Adalat formed by DRT

33. Rs10.00 Lac & above

34. 30 days from date of deposit of the title deeds.

35. Unstructured Supplementary Service Data.

36. Rs28 lac : Rs35 lac

37. Bankers Book Evidence Act

38. Nil as per Claytons rule

39. Inter Bank Deposits

40. To provide security against unauthorized users

41. Enforcement Directorate.

42. Legal Heirs are liable for the liabilities upto the assets inherited by them

43. Bhutan

44. RBI

45. Credit Rating Information Services of India Ltd

46. Repo Rate

47. All of these

48. Current Assets

49. China

50. To steal the customers personal/confidential date like Bank a\c number, Credit Card Number, PIN or Password over internet & access their accounts

51. 90 days

52. Liquidity Adjustment Facility

6 “Profitability, Asset Quality, Capital Optimization and Efficiency”

RECOLLECTED QUESTIONS – October 2015

1. Present Repo Rate: Reverse Repo: Bank Rate CRR SLR

2. Banker customer relationship in Safe Custody:

3. Protection available to materially altered cheque under which Section of N.I Act;

4. TDS deduction on interest more than 20,000/- under which Act:

5. Payment in due course under which act:

6. EEFC A\c can be of which type:

7. Educational loan for vocational purpose in India:

8. Housing loan under priority sector more than 10 lac population:

9. CRR decided by:

10. In JLG number of group members:

11. Loans for co-operative society under Priority Sector:

12. ATM dispense/non-dispense claim to be settled within______ days.

13. Under Ombudsman scheme, the customer has to give acceptance of the award within____ days.

14. Operational Risk:

15. In case of RTI, information related to life and liberty has to be provided within:

16. KYC updation for low risk customer has to be done:

17. Protection to the Collecting bank is available under which Sec of NI Act:

18. What is a Promissory Note ?

19. CC/OD/ A\c out of order for a period of ____ to become NPA:

20. Age limit in Prime Ministers Jeevan Jyoti Yojana:

21. How much NRI can remit from his NRO a/c:

22. Eligibility criteria for DRI in terms of income limit:

23. Interest subvention for exporter is upto:

24. No objection certificate from Agri:

25. Age limit staff housing loan:

26. Full form of IFRS:

27. Small value remittance in forex:

28. NBFC with assets size of Rs.500 Crore and registered with RBI can take action under:

29. For referring cases to Lok Adalat, the cut-off limit is:

30. In CMLC C stand for:

31. Position of bank if stop payment cheque is paid:

32. FD period for FCNR(B)

33. Bank has served the possession notice under Sarfeasi. The borrower has raised any query. The bank has to reply within:

7 “Profitability, Asset Quality, Capital Optimization and Efficiency”

34. NPAT - 100, Tax – 40, Depreciation – 50, Interest – 50, Instalment -75 What is DSCR:

35. Short Duration and long duration crop – who fixes:

36. Notice period to borrower before sale of assets in Sarfaesi:

37. Under Ombudsman scheme, the authority for appeal is:

38. ICAAP full form:

39. Current Assets 600, Long Term sources – 600, Total Assets-1000, What is NWC and Current Ratio

40. Marginal standing facility rate:

41. As per new PS guidelines Food & Agro processing will form part of:

42. CRISIL

43. Expand CRILC

44. What is Accrual Concept:

45. Difference between export and import:

46. Full form of CARE:

47. A\c will be NPA if not reviewed within how many months:

48. Premium in Prime Minister Suraksha Bima Yojana :

49. Target for Weaker Section under Priority Sector:

50. Under BASEL-II, what is the Risk Weightage on the Loans and advances given to Staff of the bank secured by Mortgage/superannuation benefits:

51. For assessing Fund Based Working Capital limit for SSI upto _______ Turnover method is followed under Nayak Committee:

52. What is the minimum education qualification required for an entrepreneur for a manufacturing project of Rs.10 Lakhs to be considered under PMEGP?

53. What is the minimum amount of Award that can be given by an Ombudsman under RBI’s

Ombudsman scheme?

54. Within how many days of filing a complaint with the bank, the complainant can approach the Ombudsman scheme?

55. Investment Fluctuation Reserve is calculated on which type of capital:

56. Investment Fluctuation Reserve is calculated on which type of security?

57. Right of foreclosure is available in which type of mortgage?

58. Double Dip Recession:

59. What is nature of Banker’s Lien?

60. Gold is pledged with bank as security for a Bank Guarantee by a borrower. Bank Guarantee stands expired . Whether a temporary overdraft availed by the borrower which is overdue can be got adjusted by selling the Gold held as security for issue of guarantee:

61. Which of the following is Intangible Assets:

a) Stock

b) Book debt more than 6 month old

c) Goodwill

ANSWERS

8 “Profitability, Asset Quality, Capital Optimization and Efficiency”

1. Repo: 6.75% Rev Rep: 5.75% Bank Rate: 7.75 CRR 4% : SLR 21.5%

2. Bailee- Bailor

3. Section 89 of the NI Act

4. Income Tax Act

5. Sec 10 of N.I. Act

6. Current Account

7. Max 1.50 lac

8. Rs.28 lacs with unit cost not exceeding Rs.35 lacs.

9. RBI

10. 4 to 10

11. 5 crore

12. 7 days

13. 1 month

14. Internal failure of system and procedure

15. 48 hours

16. Once in 10 years

17. Sec 131 of N.I. Act

18. Unconditional promise to pay

19. 90 days

20. 18-50

21. One million dollars per financial year

22. 18,000 & 24,0000

23. 3% subject to the condition that the floor rate is not less than 7%

24. Dispensed with – not required now

25. 70 years

26. International Financial Reporting Standard

27. $ 25,000 per financial year

28. Sarfaesi

29. Upto 20 lacs. More than 20 lacs Lok Adalat set up under DRT

30. CMLV Cambodia Myanamar, Laos & Vietnam

31. Not a payment in due course as per Sec 10 of N I Act

32. Min 1 and Max 5 years

33. 15 days

34. 200/125 = 1.6

35. Agri Deptt of the Govt

36. 30 days

37. Dy. Gov RBI

38. Internal Capital Adequacy Assessment Process

39. CR 1.5 : 1 NWC = 200

40. 7.75 %

41. Ancillary activity under agriculture

42. Credit Rating Information Services of India Ltd.

43. Central Repository Services of India Ltd

44. Mercantile. It means when the amt becomes due you recognize and take it to P & L account irrespective of the fact that the amount has not been recovered.

45. Balance of Trade

46. Credit Analysis and Research Limited

9 “Profitability, Asset Quality, Capital Optimization and Efficiency”

47. 6 month

48. Rs.12 per year and claim available is Rs.2 lac in case of accidental death only.

49. 10% of ANBC or 25% of total PS advances

50. 20%

51. Rs. 5 crore.

52. No educational qualification required.

53. Rs. 10 lacs

54. One year from the date of the receipt of the reply from the bank. If no reply Received then it is one year and one month.

55. Tier I Capital

56. Available for Sale Category and Held for Trading Category.

57. Mortgage by conditional sale.

58. The economy is partially in the recovery mode but it again slips down toward recession

59. It is implied pledge because Banker can dispose-off the goods after giving notice to the borrower.

60. Yes, because Bankers lien is a general lien and is an implied pledge. Further, the Gold was deposited in the ordinary course of business.

61. Goodwill.

RECOLLECTED QUESTIONS- September 2015

1. Mudra Bank full form:

2. NITI full form

3. General insurance works on

4. Limit for sending remittances to Nepal by NEFT

5. In case of a cheque, when the amount written in words and figures differ, which will hold good

As per law:

6. When remittance done to currency chest, counting in front of banks officials will be done for

Denomination of

7. Hindi Pakhwara (Hindi Fortnight) celebrated from ?

8. How many members from Lok Sabha are there in the official language Parliamentary committee.

9. Official language applicable to all States and Union Territories except.

10. Who decides Savings Bank Rate:

11. Shares transferred in electronic form:

12. Calculation of interest in loan account:

13. Business correspondent in bank are for banking business:

14. Mutual fund Market regulated by

15. No collateral up to the loan amt in NRLM – Aajivika:

16. Stand by L\c is like:

17. Duty of confirming bank:

18. What is “Pari Passu” means :

19. Maximum loan amount covered under CGTMSE:

10 “Profitability, Asset Quality, Capital Optimization and Efficiency”

20. Agri clinic maximum loan limit for individual

21. Unspent foreign currency can be retained upto :

22. DSCR is for evaluating:

23. Current Ratio used for evaluating:

24. Debt Securitisation Company means:

25. Minimum Education qualification for PMEGP :

26. Variable cost:

27. Break Even Point:

28. Special crossing banker protection Section:

29. Imports regulator:

30. Max foreign currency for business trip:

31. What is Noting:

32. Current Account operated by finance director dies. Cheque signed by him:

33. CRR is based on which act:

34. KCC accident death claim:

35. Certificate of Incorporation is:

36. Banker customer relationship in standing instruction :

37. Abbreviation for UCPDC:

38. FCNR(B) account type:

39. Blue revolution refers:

40. RTI:

41. CC account credit not enough to meet interest:

42. Which is the function of ALCO:

43. What is the time limitation for execution of decree:

44. Time limit to sue incase of cheque return unpaid:

45. Meaning of accrual concept:

46. Collecting Bank protection under which act:

47. Period of KYC updation on low risk customers:

48. Maximum amount of Tax Saver FDR:

49. Rajeev Rin Yojana how much maximum loan without collateral security:

50. Balance of trade:

51. CIN in case of a company indicates:

52. Partnership firm not registered then what:

53. Classification of NPA in consortium advances:

54. SARFAESI proceeding in a consortium advance will be implemented if ___ of creditors due agree

55. CTPS stands for

56. Right of Subrogation:

57. Maximum time for export crystalisation:

58. HUF cannot be partner in a Partnership firm:

59. Partners liability in a Partnership firm:

60. In a joint account Rohit is an agent (POA holder). On death of one of the Principal, Whether cheque signed by the agent will be paid or not:

61. Position of the minor on attaining the majority:

62. EEFC a\c can be opened as :

63. RBI gives credit to bank on which rate:

64. Insurance amount in PMJDY :

11 “Profitability, Asset Quality, Capital Optimization and Efficiency”

65. If in a Guarantee issued is silent, what will be the limitation period:

66. May I help you counter on how much staff:

67. Customer day in branch:

68. Security Officer visit for high risk branches:

69. Negative lien means:

70. Full form of CGTSME:

71. When Letter of Administration issued:

72. Cut-off amount in DRT:

ANSWERS

1. Micro Units Development Refinance Agency

2. National Institution for Transforming India ( Chairman Prime Minister: Dy Chairman Arvind Panagariya

3. Principle of utmost faith

4. Rs.50,000\- per transaction

5. Cheque will be paid as per amount written in words – Sec 18 of N I Act In practice bank will return

6. Rs500 and Rs1000 notes

7. 15th Sept

8. 20 Members from Lok Sabha (out of 30 members committee of Parliament – 10 from Rajya Sabha

9. Tamil Nadu

10. Bank – ALCO committee

11. Dematerialization

12. Monthly

13. Bank is the Principal and correspondent is the Agent

14. SEBI

15. Upto 10 lacs

16. Bank Guarantee

17. Only to verify the genuineness of L\C

18. Sharing in the ratio of outstanding

19. Rs1 cr Fund based + non fund based

20. 20 lac

21. 180 days

22. Term Loan repayment – surplus generating capacity

23. Liquidity position

12 “Profitability, Asset Quality, Capital Optimization and Efficiency”

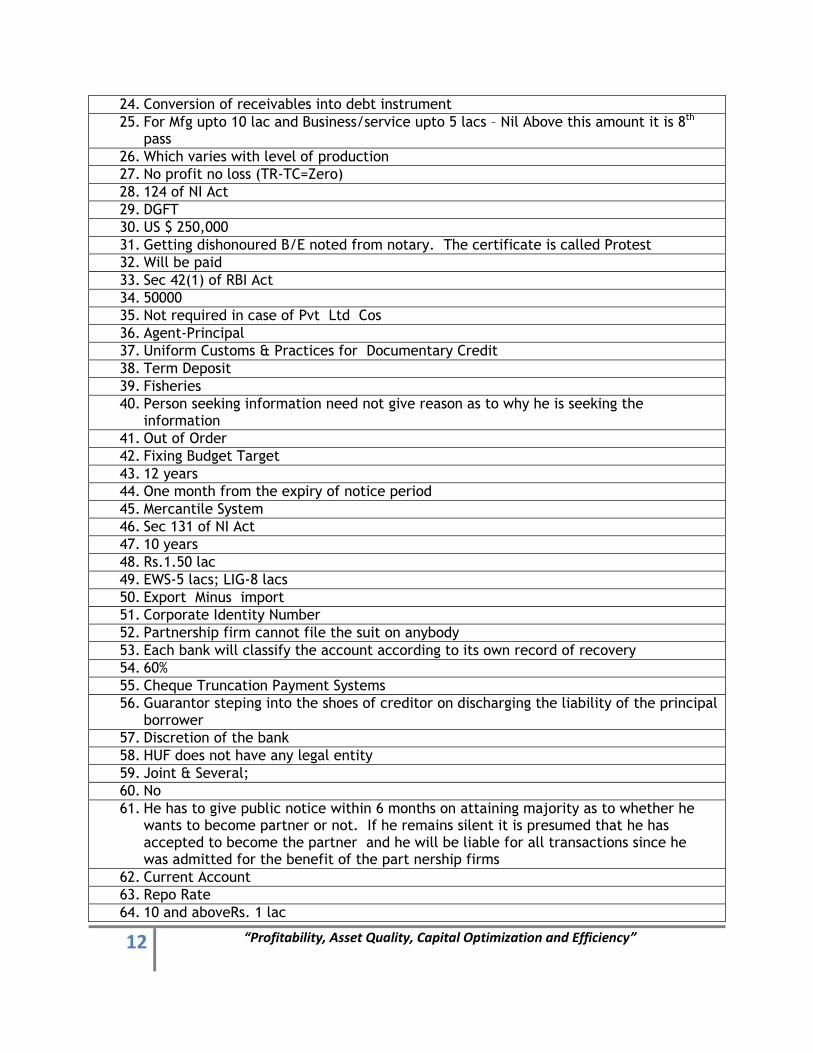

24. Conversion of receivables into debt instrument

25. For Mfg upto 10 lac and Business/service upto 5 lacs – Nil Above this amount it is 8th pass

26. Which varies with level of production

27. No profit no loss (TR-TC=Zero)

28. 124 of NI Act

29. DGFT

30. US $ 250,000

31. Getting dishonoured B/E noted from notary. The certificate is called Protest

32. Will be paid

33. Sec 42(1) of RBI Act

34. 50000

35. Not required in case of Pvt Ltd Cos

36. Agent-Principal

37. Uniform Customs & Practices for Documentary Credit

38. Term Deposit

39. Fisheries

40. Person seeking information need not give reason as to why he is seeking the information

41. Out of Order

42. Fixing Budget Target

43. 12 years

44. One month from the expiry of notice period

45. Mercantile System

46. Sec 131 of NI Act

47. 10 years

48. Rs.1.50 lac

49. EWS-5 lacs; LIG-8 lacs

50. Export Minus import

51. Corporate Identity Number

52. Partnership firm cannot file the suit on anybody

53. Each bank will classify the account according to its own record of recovery

54. 60%

55. Cheque Truncation Payment Systems

56. Guarantor steping into the shoes of creditor on discharging the liability of the principal borrower

57. Discretion of the bank

58. HUF does not have any legal entity

59. Joint & Several;

60. No

61. He has to give public notice within 6 months on attaining majority as to whether he wants to become partner or not. If he remains silent it is presumed that he has accepted to become the partner and he will be liable for all transactions since he was admitted for the benefit of the part nership firms

62. Current Account

63. Repo Rate

64. 10 and aboveRs. 1 lac

13 “Profitability, Asset Quality, Capital Optimization and Efficiency”

65. 3 years and in case of Govt Guarantee it is 30 years

66. 10 and above

67. 15th of every month

68. Once in a quarter

69. Undertaking given by the Co not to create subsequent charge till the currency of bank borrowings

70. Credit Guarantee Fund Trust For Micro & Small Enterprises

71. Intestate

72. 10 lac and above

RECOLLECTED QUESTIONS: AUG 2015

1. Maximum Indian currency that can be take n abroad by residents other than Nepal & Bhutan

2. FCNR(B) account can be opened in which all currencies:

3. NRE can be opened for a minimum and maximum period of:

4. When cheque is wrongly returned , the banker is liable to:

5. As per Right to Information Act(RTI) , in how much time the information to be provided to the Person seeking the information:

6. Loan granted for short duration crops will be NPA if overdue for

7. Minimum and Maximum amount that can be deposited in PPF account is ____

8. DICGC insurance is not available to the following:

9. Official Language Act pertains to which year:

10. Hindi was accepted as official Languages on ____

11. The Present Bank Rate is:

12. Interest Subvention for Agriculture:

13. ____ prohibits payment of term deposits or notice deposits in cash if the amount involved. Principal plus interest is Rs.20,000.00\- or more

14. For setting up of White Label ATMs the corporate body net worth must be ____:

15. ATM failed transactions are to be resolved within a maximum period of ____ :

16. In National Electronic Funds Transfer (NEFT) , the minimum and maximum amount is :

17. Financial inclusion aims at _____:

18. For ultra Small Branches a designated Officer will visit the village on a prefixed date and time every ____ with laptop and will be connected to Bank’s center server (CBS)

14 “Profitability, Asset Quality, Capital Optimization and Efficiency”

19. Loans to farmers up to____ against pledge/hypothecation of agriculture produce for a period not exceeding 12 months.

20. Maximum credit for Service Enterprises under PMEGP is ____ :

21. Interest subvention of 1% will be available on housing loans up to Rs _____ to individuals for Construction/purchase of a new house or extension of an existing house, provided the cost of Construction / price of the new house / extension does not exceed 25 lakh.

22. Banker Customer relationship dor deposits:

23. For takeover of accounts from other Banks, the account copies of all the borrower accounts With the present bankers/financial institution shall be obtained at least for the last

24. An account become NPA, if regular credit limits have not been reviewed within _____ from due date:

25. In case of Educational Loan, no collateral security is to be obtained upto:

26. Income ceiling for assistance for project under PMEGP is _______

27. Basel II has how many pillars _____

28. CDR Scheme will not apply to accounts involving ______________

29. Subordinated debt instruments together with all other instruments of Tier II capital are to be limited to _____ of Tier I:

30. FIR is required to be filed in case where the counterfeit notes found are ______ in a single transaction and acknowledgment is to be obtained from the concerned police authorities.

31. Which of the following is withdrawn by RBI:

a) EFT

b) NEFT

c) RTGS

d) ECS

e) ABB

32. In Basic Savings Bank Deposit Account in all their accounts taken together and the total credit in all the accounts taken together is not expected to exceed _____ in a year has been simplified to enable those belonging to low income groups without documents of identity and proof of residence to open bank accounts.

33. Central Registry of Securitization Asset Reconstruction and Security Interest of India (CERSAI) Is a government company licensed under Section 25 of the Companies Act has been incorporated to operate and maintain the Central Registry under the provisions of ______

34. _____ is a money market instrument, which enables collateralized short term borrowing through Govt Securities:

35. While disposing-off the request under RTI Act, PIO is required to mention clearly the time limit of _____ and addr ess of the Appellate Authority to the complainant .

36. Education Loan under priority sector for study abroad is upto :

37. In Joint Liability Group (JLG) , per member can be granted maximum amount upto ____ under priority sector:

38. The extent of coverage in CGTMSE scheme for credit facility upto 5 lacs to micro

15 “Profitability, Asset Quality, Capital Optimization and Efficiency”

enterprises is ____________

39. Limitation of demand Promissory Note is ______:

40. As per RBI guidelines, Base Rate is to be reviewed by bank on ______:

41. Family income of borrower for DRI in urban areas:

42. Provisions in case of accounts classified in Doubtful category for 12 months to 3 years is _____

43. Bank can sell NPA after it has remained in books for:

44. FCNR(B) can be opened in :

45. RBI has permitted release of foreign exchange not exceeding upto ______ in one financial year for one or more private visits (except Nepal & Bhutan)

46. Crystallisation means:

47. When no time or date is mentioned on bill of exchange, then it will be payable :

48. When cheque is dishonoured, notice is to be sent by payee to the drawer within

49. Periodicity of official language meetings:

50. The Audited Balance Sheet for the latest financial year is to be obtained within _____ to finalise credit rating and re-fix interest accordingly:

51. For Speed clearing, no charges should be levied for cheques upto _______

ANSWERS

1) Rs25,000.00

2) All freely convertible currencies

3) 1 year and 10 years

4) Drawer

5) 30 days

6) 2 cropping seasons

7) Minimum Rs.500\- & Maximum Rs.1.50 lacs

8) Deposits above Rs1.00 lacs

9) 1963

10) 14:09:1949

11) 8.25%

12) 2% and also additional 3% for prompt payment borrowers

13) Income Tax Act,1961

14) 100 crores

15) 7 Working Days

16) 1 Lakh

17) There is no cap on minimum and maximum amount

18) Week

16 “Profitability, Asset Quality, Capital Optimization and Efficiency”

19) Rs.50 lac

20) Rs500.00 lac

21) 15 lakh

22) Debtor – creditor

23) 12 months

24) 180 days

25) Rs.7.50 lacs

26) There will be no income ceiling

27) 3

28) Only one financial institution or one bank and outstanding exposure is less than Rs10 Cr

29) 100%

30) Five pieces and above

31) EFT

32) 1,00,000\-

33) SARFAESI Act 2002

34) Repo Rate

35) 30 days

36) Rs.10 lacs

37) Rs50,000 per person and incase of Group, maximum upto 5 lacs

38) 85% of the amount of claim

39) Three years

40) Quarterly basis

41) Rs24,000\- ( Rural Rs.18,000)

42) 40% (but in deficit portion it is 100%)

43) No lock in period now

44) Term deposit only

45) USD 10,000

46) Converting foreign liability into rupee liability (delinking foreign elements from bill and Converting to INR

47) On demand

48) 30 days

49) Quarterly

50) 6 months

51) 1 lakh

Recollected Questions for the month of June 2015

1. Tangible Net Worth (T N W) is calculated as :

2. When an MSE unit is showing signs of sickness, the unit is said to be in the ______

3. While extending to NBFC-MFIs, the percentage of Qualifying Assets should be:

4. Internal Rate of Return is arrived at a point where future cash flows on Net Present Value basis should be:

5. What is the cut-off date for RKBY during Khariff Season in case of Loanee Farmers

6. For a loan more than Rs.1 crore to NGO-MFI/NBFC/MFI:

7. Debt Securitization refers to:

17 “Profitability, Asset Quality, Capital Optimization and Efficiency”

8. IMPS:

9. National Financial Switch of IDRBT (now with National Payment Corp of India)

10. Advantages of Cluster based finance to MSMEs:

11. Revaluation Reserve discounting factor to be taken to which capital:

12. For the purpose of Medical expenses abroad the maximum amount that can be allowed is:

13. Sales above Breakeven point is :

14. Export trade is regulated by the Directorate General of Foreign Trade

15. The _____ has replaced the existing GR form used for declaration of export of goods at Non-EDI ports. The procedure relating to the exports of goods through EDI ports will remain the same and SDF form will be applicable hitherto.

16. Interest Subsidy Scheme for Housing the Urban Poor (ISHUP). The scheme will provide a subsidized loan for 15-20 years for a maximum amount of _____ for a EWS individual for as house

17. For Housing Loans, maximum amount of EMI that can be permitted for salaried class, is to be taken as ____ of net salary.

18. In Model Educational Loan Scheme (IBA) repayment of the loan starts after ____ from the date of completion of course.

19. For setting up White Label ATMs the corporate body net worth must be _____

20. ATM failed transactions are to be resolved within a maximum period of _____

21. For Speed clearing, no charges should be levied for cheques up to ______

22. For Ultra Small Branches a designated officer will visit the village on a prefixed date and time every ____ with laptop and will be connected to Bank’s Central Server (CBS)

23. Why International Financial Reporting System (IFRS) should be implemented

24. Market Risk is monitored by:

25. What is the purpose of Disaster Recovery Plan:

26. What is the time period of crediting proceeds of outstation cheques presented in Speed Clearing

27. While doing Project Appraisal, sensitivity analysis is useful for:

28. Market Risk is monitored by:

29. Lorry Receipts issued by Transport Operators approved by IBA are preferred. The reason is the Transport Operators will take care of

30. What is the definition of Quick Mortality:

31. What is the target in DRI scheme for women:

32. While doing Risk Rating, an asset is downgraded from A+ rating to A rating What type of risk is involved:

33. The extent of coverage under CGTSME for Micro units upto Rs5. Lacs:

34. Up to what loan amount banks need to lend under Consortium finance?

Rs 5 Cr/Rs10Cr/Rs.20 Cr/Rs50CR

35. What should be annual income of a BPL family to be eligible for getting interest subvention under educational loan?

36. Cluster based approach is applicable

a) Priority Credit advance

b) SME

c) SHG

37. What is Hybrid debt instrument?

18 “Profitability, Asset Quality, Capital Optimization and Efficiency”

a) Debenture

b) Bond

c) Preference Shares

d) Convertible Bonds

38. Implied authority of a partner does not allow ____ singly?

39. When guarantor on payment of all dues to principal debtor, he gets which rights as that of creditor?

a) Subrogation

b) Lien

c) Assignment

d) Pledge

40. Rating of Bank is carried by RBI on CAMELS criteria, what do “C” stands for ?

41. Banks is not required to produce original book of records but true copy can be submitted when court has demanded as per which act ? a) Civil Procedure code b) Registration Act

c) B R Act

d) RBI act

e) Banker Books Evidence Act

42. To improve Current Ratio of 2:1 what has to be done? a) Recover cash from Receivables b) Cash Sales

c) Decrease the Bills payables

43. Whether “WILL” has to be registered?

44. Which of the following does not come under Tier II capital ? a) Capital Reserves b) Undisclosed Reserves

c) Revaluation Reserves

d) Cumulative perpetual shares

45. Which of the following can purchase NPA ?

a) ARC

b) Banks

c) Financial Institutions

d) NBFC

e) All of the above

46. Nominee can claim payment when:

47. A foreign tourist who is in India and is having USD 5,0000\- wants to open a\c. Which type of deposit account he can open

48. Monetary ceiling for case filing at Lok Adalat is

49. For MSE units, no collateral security/third party guarantee is to be taken for loans upto Rs._____

50. Cheque issued without balance what penalty:

51. Which is the latest recovery channel made available to the banks for speedy recovery of NPAs backed by security:

52. What is the latest RBI directives for issuing DD for amount of Rs.20,000 and above

53. As per the moratorium guidelines, the repayment of education loan should start from :

19 “Profitability, Asset Quality, Capital Optimization and Efficiency”

54. Business correspondent is:

55. Mulbery Crop Loan without margin can be upto:

56. Net working capital means:

57. Virus refers to:

58. In Basel II, Pillar I covers which types of risks

59. For Agri business centre, outer project cost limit for individual is:

60. What is the time period for crediting proceeds of outstation cheques presented in Speed Clearing

61. In an Exchange Quotation, the rate is mentioned as USD 60.61/63. What is Selling Rate:

ANSWERS

1. Total paid up capital + Reserves – Intangible Assets.

2. Handholding stage of MSEs

3. Minimum 85%

4. Zero

5. November

6. 10% Collateral in the form of Bank Deposits

7. Conversion of receivables into debt instruments

8. Immediate Payment Service – Mobile to account

9. ATM network

10. Risk Mitigation

11. 55% & Tier II Capital

12. USD 100,000 or as per the question from the Hospital abroad whichever is high

13. Margin of Safety

14. (DGFT)

15. (EDF)

16. 1. Lakh

17. 50%

18. 24 months

19. 100 Crores

20. 7 Working days

21. 1 lakh

22. Week

23. For comparision of financials of companies operating in two different international jurisdictions

24. Bank for International Settlements

25. Alternate Server installed for smooth functioning of systems in case of failure of Main Server.

26. 48 hours

20 “Profitability, Asset Quality, Capital Optimization and Efficiency”

27. Viability and sustainability of project

28. Bank for International Settlements

29. Carriers Risk

30. Account becoming NPA with in 12 months from the date of first disbursement

31. No Target for women

32. Credit Risk

33. 85% with maximum amount of claim upto Rs4.25 lacs

34. No limit now

35. Rs4.50 lac

36. SME

37. Convertible Bonds

38. Settle a dispute relating to the business of the firm thru arbitration

39. Subrogation

40. Capital Adequacy

41. Banker Books Evidence Act

42. Decrease the Bills payables

43. Not required

44. Capital Reserves

45. All of the above

46. Only after the death of depositor as a trustee of legal heir

47. NRO for a maximum period of 6 months

48. Max Rs.20 lakhs (Above Rs 20 lac for Lok Adalat under DRT)

49. Rs 10 lakhs. (For Good track record unit upto Rs25 lacs)

50. No penalty (Only on dishonor, Court Proceedings)

51. Action can be taken under SARFAESI

52. It should Account Payee only

53. 12 months on completion of course or 6 months after getting job, whichever is earlier

54. Agent of Banker

55. Rs.1 lac

56. Current assets minus current liabilities

57. Program which infects the system

58. Credit Risk, Market Risk, Operational Risk

59. Rs20 lacs

60. 48 hours

61. 60.63

Questions on New Priority Sector Guidelines (W E F 23.04.2015)

1.The Reserve Bank has revised Priority Sector lending guidelines w.e.f. 23-4-2015, on

21 “Profitability, Asset Quality, Capital Optimization and Efficiency”

the basis of Internal Working Group headed by:

a) Mr. Lily Vadera

b) Mr. M.V. Nair

c) Dr. Urjit Patel

d) Mr. C.S. Murthy committee

2) As per the revised guidelines, bank loans up to a limit of Rs.____ Crores per borrower for building social infrastructure for activities namely schools, health care facilities, drinking water and sanitation facilities in Tier II to Tier VI centres.

a) 3

b) 5

c) 8

d) 10

3) Bank loans up to a limit of Rs._____ crore to borrowers for purposes like solar based power generators, biomass based power generators, wind mills, micro-hydel plants and for non-conventional energy based public utilities viz. street lighting systems, and remote village electrification. For individual households, the loan limit will be Rs. ____ lakh per borrower. a) 10 ; 5

b) 15; 10 c) 20 ; 15 d) 25 ; 15

4) As per the revised guidelines, housing loans to individuals up to Rs________ lakh in metropolitan centres (with population of ten lakh and above) and loans up to Rs. _____ lakh in other centres for purchase / construction of a dwelling unit per family provided the overall cost of the dwelling unit in the metropolitan centre and at other centres should not exceed Rs.____ lac & Rs.____ lakh respectively.

a) 20;15;25; 20 b) 28; 20; 35, 25 c) 25; 20;30;35 d) 30; 25; 35; 30

5) Micro (Manufacturing) Enterprises are those having original investment in plant and machinery up to _____ a) Rs.25 lakh b) Rs 30 lakh c) Rs 35 lacs d) Rs 40 lacs

6) As per revised guidelines, Net bank credit for priority sector is calculated as bank credit in India minus (1) bills rediscounted with RBI or other approved Fls (2) Net NPA provisions (3) Interest receivable on loans: a) 1 to 3 all

22 “Profitability, Asset Quality, Capital Optimization and Efficiency”

b) 1 & 2 only c) 2 only d) 1 only

7) As per revised guidelines, loans to individuals other than farmers can be sanctioned upto Rs _____ to prepay their debt to non- institutional lenders. a) 25,000 b) 50,000 c) 1 lac d) no limit

8) Small (Manufacturing) Enterprises are those engaged in the manufacture, processing or preservation of goods and whose investment in plant and machinery [original cost excluding land and building) does not exceed

a) Rs 1 crore

b) Rs 2 crore

c) Rs 2.5 crore

d) Rs. 5 crore

9) Micro (Service) Enterprises are those enterprises engaged in providing 1 rendering of services and whose investment in equipment (original cost excluding land and building and furniture, fittings) does not exceed _____

a) Rs. 10 lacs

b) Rs 20 lacs

c) Rs 30 lacs

d) Rs 40 lacs

10) Small (Service) Enterprises are enterprises engaged in providing / rendering of services and whose investment in equipment (original cost excluding Land and Building and furniture, fittings and other items not directly related to the service rendered) does not exceed _______

a) Rs 1 crore

b) Rs 2 crore

c) Rs 2.5 crore

d) Rs. 5 crore

11) Bank loans to Housing Finance Companies (HFCs), approved by NHB for their refinance, for on lending for the purpose of purchase / construction / reconstruction of individual dwelling units or for slum clearance and rehabilitation of slum dwellers, will be classified as priority sector provided _____ , •

a) Maximum loan per borrower does not exceed Rs.10 lac. b) Maximum loan per borrower does not exceed Rs.20 lac.

c) The overall eligibility under PS loans to HFC is restricted to 5% of the individual banks total PS lending on an going basis

d) Both (a) and (c)

23 “Profitability, Asset Quality, Capital Optimization and Efficiency”

12) Bank loans to Micro and Small Enterprises (MSE)engaged in providing or rendering of services will be eligible for classification as direct finance to MSE Sector under priority sector up to an aggregate loan limit of Rs.cr, per borrower / unit provided they satisfy the investment criteria for equipment as defined under MSMED Act, 2006. a) 2 b) 5 c) 7.5 d) 10 e)15

13)Bank loans to any Governmental agency for construction of dwelling units

or for slum clearance and rehabilitation of slum dwellers will be treated as

prioritysector provided the amount of loan does not exceed ______ per dwelling

unit.

a) Rs. 5 lac

b) Rs. 10 lac

c) Rs. 15 lac

d)Rs.20lac

14) Under Priority sector, the loans can sanctioned by banks up to Rs .____ for

solar based power generators, biomass based power generators, wind mills, micro-

hydel plants and for non-conventional energy based public utilizes viz. street

lighting systems, and remote village electrification:

a) Rs.1 or

b) Rs. 5 cr

c) Rs.15 cr

d)Rs.20cr

15) Loans for Food and Agro-processing up to an aggregate sanctioned limit of Rs.

___ crore per borrower from the banking system.

a) 25

b) 50

c) 75

d)100

16) The loans sanctioned by banks for housing projects exclusively for the purpose of

construction of houses for economically weaker sections and low income groups, the

total cost of which does not exceed Rs.___- lakh per dwelling unit. For the

purpose of identifying the economically weaker sections and low income groups,

the family income limit of Rs. ____ lakh per annum, irrespective of the location, is

24 “Profitability, Asset Quality, Capital Optimization and Efficiency”

prescribed.

a) 5; 1

b) 10; 2

c) 15; 5

d)20;10

17) The eligibility under priority sector loans to HFCs is restricted to ____ percent of

the individual bank's total priority sector lending, on an ongoing basis. The maturity

of bank loans should be co-terminus with average maturity of loans extended by

HFCs. Banks should maintain necessary borrower-wise details of the underlying

portfolio.

a) Five

b) Ten

c) Fifteen

d)Twenty

18) Loans to distressed persons other than farmers already included not exceeding

___ per borrower to prepay their debt to non-institutional lenders;

a) Rs.100,000

b) Rs.200,000

c) Rs.300,000

d) Rs.400,000

19) Individual Women beneficiary up to____ per borrower is covered under

weaker section:

a) Rs, 1 lakh

b) Rs. 2 lakh

c) Rs. 3 lakh

d) Rs. 5 lakh

20) Foreign Banks with less than 20 Branches to achieve ___ percent of ANBC or

Credit Equivalent Amount of Off-Balance Sheet Exposure, whichever is higher to

be achieved in a phased manner by____

a) 40; 2020

b) 32; 2020

c) 40; 2022

d) 32; 2022

21) Within the 18% target for agriculture, a target of ____ % of ANBC or CEOBE,

whichever is higher is prescribed for Small and Marginal Farmers, to be achieved in a

phased manner i.e., ___ % by March 2016 & ____ % by March 2017.

25 “Profitability, Asset Quality, Capital Optimization and Efficiency”

a) 6; 5; 6

b) 8; 7; 8

c) 5 ; 6; 5

d)7;8;7

22) As per the revised guidelines Agriculture target for Scheduled Commercial Banks

is ___ % of ANBC or CEOBE whichever is higher.

a) 12

b)15

c)18

d)20

23) As per the revised guidelines, Micro Enterprises target for Scheduled

Commercial Banks is % ___ of ANBC or CEOBE, whichever is higher to be achieved in

a phased

Manner i.e .___ % by March 2016 & ___ % by March 2017.

a) 5 ; 4 ; 5

b) 6 ; 5; 6

c) 7.5; 7; 7.5

d) 7; 8 ; 7

24) The Total Priority Sector target of 40% for foreign banks with less than __

branches has to be achieved in a phased manner as under: 2015-16 -

32%; 2016-17 -34%; 2017-18 -36%; 2018-19 -38%; 2019-20 - 40%.

a)15

b)18

c) 20

d) 22

25) As per the revised guidelines, the distinction between direct and indirect

agriculture has been dispensed with. Instead the lending to agriculture sector has

been re-defined to include three categories. Which of the following is not part of

the categories?

a)Farm Credit (which will include short-term crop loans and medium / long-term

credit to farmers);

b) Agriculture Infrastructure

c) Ancillary Activities.

d) Non Farm Credit

26) As per the revised guidelines, loans to Corporate farmers, farmers' producer

organizations / companies of individual farmers, partnership firms and co-operatives

of

26 “Profitability, Asset Quality, Capital Optimization and Efficiency”

farmers directly engaged in Agriculture and Allied Activities, viz., dairy, fishery,

animal husbandry, poultry, bee-keeping ,sericulture upto an aggregate limit of Rs.

___ cr per borrower.

a) 2

b) 3

c) 5

d) 10

27) As per the revised guidelines, the Export target for foreign banks with 20

branches and above, would be classified as priority sector to the extent of

incremental

export credit over corresponding date of the preceding year, up to _____

percent of ANBC or CEOBE, whichever is higher, effective from April

1,____ :

a) 2; 2016

b) 2; 2017

c) 5; 2016

d) 5; 2017

28) As per the revised guidelines, the Export target for foreign banks with less than

20 branches will be allowed up to __ % of ANBC or CEOBE whichever is higher.

a) 12

b) 20

c) 32

d) 40

29) As per the revised guidelines, loans to individuals for educational purposes

including vocational courses upto Rs. ___ lakh irrespective of the sanctioned

amount will be considered as eligible for priority sector.

a) 10

b) 15

c) 20

d) 25

30) As per ,the revised guidelines issued by RBI which are operational w.e.f April

23, 2015, there are 8 categories under Priority Sector. Which of the following pair is

not part of the category:

a) Agriculture; Micro, Small and Medium Entt.;

b) Export Credit; Education; Housing;

27 “Profitability, Asset Quality, Capital Optimization and Efficiency”

c) Social Infrastructure; Renewable Energy; Others.

d) Agriculture Infrastructure; Retail trade; Financial inclusion

31) As housing loans which are backed by long term bonds are exempted from ANBC,

banks should either include such housing loans to individuals up to Rs. ___

lakh in

metropolitan centres and Rs.___ lakh in other centres under priority sector or

take benefit of exemption from ANBC, but not both.

a) 30; 20

b) 25; 30

c) 28; 20

d) 28; 25

32) Loans for repairs to damaged dwelling units of families up to Rs.__ lakh in

metropolitan centres and up to Rs. __lakh in other centres are eligible to be covered

under priority sector.

a) 3; 1

b) 5; 2

c) 5; 3

d) 7.5; 5

33)Bank credit to MFIs extended for on-lending to individuals and also to

members of SHGs I JLGs will be eligible for categorisation as priority sector

advance under respective categories viz., Agriculture, Micro, Small and Medium

Enterprises, and 'Others', as indirect finance, provided not less than __ percent

of total assets of MFI(other than cash, balances with banks and financial

institutions, government securities and money market instruments) are in the

nature of "qualifying assets". In addition, aggregate amount of loan, extended for

income generating activity, should be not less than ___ percent of the total loans

given by MFIs.

a) 75 ; 50

b) 80; 50

c) 85; 50

d) 90 ; 60

34) As per the revised guidelines, under Agriculture infrastructure, loans for

construction of storage facilities (warehouses, market yards, godowns and silos)

including cold storage units / cold storage chains designed to store agriculture

produce / products, irrespective of their location ,Soil conservation and watershed

development; Plant tissue culture and agri-biotechnology, seed production,

28 “Profitability, Asset Quality, Capital Optimization and Efficiency”

production of bio-pesticides, bio-fertilizer, and vermi composting – an aggregate

sanctioned limit of Rs. ____crone per borrower from the banking system, will apply.

a) 100

b) 70

c) 50

d) 25

35) All loans to units in the Khadi and Village Industries Sector (KVI) will be eligible

for classification under the sub-target of __ percent / ___ percent prescribed

for Micro Enterprises under priority sector.

a) 5 ; 7

b) 5 ; 10

c) 7; 7.5

d) 7.5 ; 10

36) As per the revised guidelines, the Export target for domestic banks, would be

classified as priority sector to the extent of incremental export credit over

corresponding date of the preceding year, up to __ % of ANBC or CEOBE,

whichever is higher, effective from April 1, 2015 subject to a sanctioned limit of

Rs.___ crore per borrower to units having turnover of up to Rs. ___ crore.

a) 2;50;75

b)2;25;100

c) 2;50;105

d) 5;50;100

37) A "qualifying asset" shall mean a loan disbursed by MFI, which satisfies the

stipulated criteria. Which of the following is not a part of the criteria?

a) The loan is to be extended to a borrower whose household annual income in rural

areas does not exceed Rs.1,00,000/-while for non-rural areas it should not exceed

Rs.1,60,000/-.

b) Loan does not exceed Rs.60,000/- in the first cycle and Rs. 100,000/- in the

subsequent cycles.

c) Total indebtedness of the borrower does not exceed Rs. 1,00,000/-;

d) Tenure of loan is not less than 24 months when loan amount exceeds

Rs.15,000/- with right to borrower of prepayment without penalty.

e) None of the above.

38) For bank credit to Micro Finance institutions, interest cap on individual loans will

be the average Base Rate of five largest commercial banks by assets multiplied by

29 “Profitability, Asset Quality, Capital Optimization and Efficiency”

per ___ annum or cost of funds plus margin cap, whichever is less.

The average of the Base Rate shall be advised by RBI Further, only three components

are to be included in pricing of loans viz., namely a processing fee not exceeding

1 percent of the gross loan amount; the interest charge and the insurance premium.

a) 2.50

b) 2.75

c) 3.0

d) 3.5

39) For bank credit to Micro Finance Institutions the margin cap should not exceed

_____% for MFIs having loan portfolio exceeding Rs.___ crore and ___ percent for

others. a) 10;50;10

b)10;100;12

c) 10;100;15

d) 15;100;20

40) Loans upto Rs ___ crore to Producer Companies setup exclusively by only small

and marginal farmers under Part IXA of Companies Act, 1956 for agricultural and

allied activities is covered under indirect finance to agriculture.

a) 2

b) 5

c) 7. 5

d) 10

41) Under revised Priority sector guidelines, loans up to Rs ____ crore can be

sanctioned to Co-operative societies of farmers for disposing of the produce of

members.

a) 2

b) 5

c) 7.5

d) 10

42) As per revised Priority sector guidelines, loans to individuals can be

sanctioned up to Rs. ___ lakh in metropolitan centres with population above

ten lakh and Rs. __lakh in other centres for purchase /construction of a

dwelling unit per family excluding loans sanctioned to bank's own employees.

a) 25;10

b) 28;35

c) 28;10

30 “Profitability, Asset Quality, Capital Optimization and Efficiency”

d) 28;20

43) RBI has issued guidelines as per which loans for repairs to the damaged dwelling

units of families can be sanctioned up to Rs. ___ lakh in rural and semi-urban areas

and upto Rs. ____ lakh in urban and metropolitan areas.

a)1;3

b) 2;3

c) 2; 5

d) 3:5

44) As per revised Priority sector guidelines, loans, not exceeding Rs. ___ per

borrower can be sanctioned directly by banks to individuals and their SHG/JLG,

provided the borrower's household annual income in rural areas does not exceed Rs.

____ and for non rural areas it should not exceed Rs. ______

a) 50,000; 1,00,000; 1,60,000

b) 1 lac; 1,00,000;1,60,000

c) 2 lac; 60,000;1,00,000

d) 2 lac; 1,00,000;1,60,000

45) The amount of education loan that can be classified as priority sector is

restricted to

a) Education in India Rs.10 and education abroad Rs. 10 lac

b) Education in India Rs.20 and education abroad Rs. 10 lac

c) Education in India Rs.10 and education abroad Rs, 20 lac

d) Education in India Rs.20 and education abroad Rs. 20 lac

46) Loans to distressed persons can be granted for amount not exceeding Rs ____

per borrower to prepay their debt to non-institutional lenders.

a) 50,000

b) 75,000

c) I lac

d) 2 lac

47) Farmers with landholding of up to 1 hectare is considered as ____ Farmers

with a landholding of more than1 hectare but less than 2 hectares are considered as

______

a) Ultra Small Farmers; Micro Farmers

b) Oral Lessees; Ultra Small Farmers

c) Micro Farmers; Share croppers

d) Marginal Farmers; Small Farmers

31 “Profitability, Asset Quality, Capital Optimization and Efficiency”

48) As per RBI guidelines, the banks should not insist for collateral security from

Micro & Small (Mfg) with good track record units upto Rs. ___ lacs:

a) Two

b) Five

c) Ten

d)Twenty five

49) Priority Sector targets are linked to (a) adjusted net bank credit (b) credit

equivalent of off-balance sheet exposure (c) whichever is lower (d) whichever is

higher.

a) Only a

b) a and b both

c) a, b and c together

d) a, b and d together

50) Adjusted 'net bank credit (ANBC) is calculated as

a) Bank credit in India - Bills rediscounted with RBI or other approved Hs +

investment in non-SLR bonds in HIM categories- investments eligible to be treated as

priory sector.

b) Bank credit in India minus bills rediscounted with RBI and other approved

financial institutions = net bank credit + bonds / debentures in HTM categories +

other Investments eligible to be treated as priority sector + Outstanding Deposits

under RIDF and other eligible funds with NABARD, NHB and SOBI on account of

priority sector shortfall + outstanding PSLCs (-) issuance of long-term bonds for

infrastructure and affordable housing (-) eligible advances in India against the

incremental FCNR (8) I NRE deposits, qualifying for exemption from CRR / SLR

requirements.

c) Bank Credit in India minus bills rediscounted with RBI or other approved FIs +

Investment in non-SLR bonds in HTM categories minus investments eligible to be

treated as Priority Sector (-) eligible advances in India against the incremental FCNR

(8) / NRE deposits, qualifying for exemption from CRR / SLR requirements.

d) Bank credit in India minus bills rediscounted with RBI or other approved FIs minus

investment in non-SLR bonds in HIM categories + investments eligible to be treated

as priority sector + Outstanding Deposits under RIDF and other eligible funds with

NABARD, NHB and SIDE on account of priority sector shortfall + outstanding PSLCs.

51) Which of the following statement is correct?

a) Bank loans to only Micro and Small Enterprises, for both manufacturing and

service sectors are eligible to be classified under the priority sector.

b) Bank loans to Micro, Small and Medium Enterprises, for both manufacturing and

service sectors are eligible to be classified under the priority sector.

32 “Profitability, Asset Quality, Capital Optimization and Efficiency”

c) Bank loans to Micro, Small & Medium Enterprises, for only manufacturing sector

is eligible to be classified under the PS.

d) Bank loans to Micro and Small Enterprises, for manufacturing sector only is

eligible to be classified under the priority sector

52) As per the revised guidelines, Bank loans up to Rs. ___ crore per unit to Micro

and Small Services Enterprises and Rs. ___ crore to Medium Service Enterprises

engaged in providing or rendering of services and defined in terms of investment in

equipment under MSMED Act, 2006.

a) 3 ; 5

b) 5 ; 10

c) 7.5 ; 15

d) 10; 20

53) Which of the following statement regarding Rural Infrastructure

Development Fund (RIDF) is not correct:

a) Domestic banks deposit short fall in priority sector lending targets, or weaker

section lending or agriculture lending in RIDF.

b) RIDF corpus is estimated annually and for 2015-16 it is Rs. 25,000 crore.

c) Interest is Bank Rate less 2% to 4% and period of deposit for RDIF is determined by

RBI

d) Amount deposited in RIDF by banks is not eligible investment for priority sector

classification..

54) Micro (Service) Enterprises is defined as enterprise having investment in

equipment up to ____

a) Rs. 10 lakh

b) Rs 5 lakh

c) Rs 3 lakh

d) Rs 2 lacs

55) Domestic SCBs having shortfall in lending to Priority sector and I or Agriculture

sector target will be allocated amounts for contribution to ___ established with

NABARD.

a) RIDF

b) SEDF

c) NEF

d) Any of the above

33 “Profitability, Asset Quality, Capital Optimization and Efficiency”

56) Bank loans up to Rs ___ per unit to Micro and Small Enterprises engaged in

providing or rendering of services and defined in terms of investment in

equipment under MSMED Act, 2006.

a).150 lac

b) 200 lac

c) 250 lac

d) 500 lac

57) Priority Sector loan application should be disposed off in the following time

schedule:

a) 2 weeks for loan up to Rs.25000 and 5 weeks for loan above Rs.25,000

b) 2 weeks for loan up to Rs.25,000 and 4 weeks for loan above Rs.25,000

c) 2 weeks for loan upto Rs.25000 and 8 to 9 weeks for loan above Rs.25000

d) At discretion of banks

58) Loans for Food and Agro Processing Units are to be classified as:

a) Direct MSE advance

b) Direct agriculture advance

c) Agriculture advance

d) Indirect agriculture advance

59) Inter Bank Participation Certificates (IBPCs) bought by banks, on a _____ are

eligible for classification under respective categories of priority sector, provided

the underlying assets are eligible to be categorized under the respective categories

of priority sector and the banks fulfil the Reserve Bank of India guidelines on IBPCs.

a) Risk sharing basis

b) Credit basis

c) Profit sharing basis

d) None of these

60) Priority sector loans to Artisans, village and cottage industries where individual

credit limits do not exceed Rs._____ are covered under weaker section:

a) 50,000

b) 1 lac

c) 1.25 lac

d)1.50 lac

34 “Profitability, Asset Quality, Capital Optimization and Efficiency”

61) Overdrafts upto Rs.___ under Pradhan Mantrl Jan-Dhan Yojana (PMJDY)

accounts, provided the borrowers household annual income does not exceed Rs.

_____ for rural areas and Rs._____ for non-rural areas.

a) 5,000/-;100,0001-;1,60,000

b) 10,000/-; 100,000/-; 1,60,000

c) 5,000/-; 100,000/-; 1,80,000

d) 5,000/-; 100,000/-; 1,80,000

62) Scheduled Commercial Banks having any shortfall in lending to priority sector

shall be allocated amounts for contribution to the ____ established with NABARD

and other Funds with NABARD I NHS I SIDBI, as decided by the Reserve Bank from

time to time. For the year 2015-16, the shortfall in achieving priority sector target I

sub-targets will be assessed based on the position as on March 31, 2016.

a) Rural Infrastructure Development Fund (RIDF)

b) Small Enterprises Development Fund (SEDF)

c) Infrastructure Development Fund ( IDF)

d) Priority Sector Deficit Fund (PSDF)

64) As per Weaver Card Scheme, what is the maximum amount of loan that can be

granted to a beneficiary:

a) Rs.50,000

b) Rs.1,00,000

c) Rs.2,00,000

d) Rs.5,00,000

65) With respect to Joint Liability Group (JLG), which of the following is correct?

a) The group size is 4 -10 people.

b) The members may be availing loan singly/jointly.

c) The maximum credit facility to a member is Rs.50,000/- and to the Group is

Rs.5,00,000/-.

d) All the above

66) Under PMEGP Scheme what is margin requirement for General and Special

category beneficiaries?

a) Gen -15%, Spl - 5%

b) Gen - 5%, Spl - 5%

c) Gen.-10%, Spl - 5%

d) Gen -10%, Spl - 10%

67) As per revised guidelines, loans to individual women beneficiaries upto Rs ____

35 “Profitability, Asset Quality, Capital Optimization and Efficiency”

per borrower is covered under weaker section.

a) 25,000

b) 50,000

c) 1,00,000

d) 2,00,000

68) Swarnjayanti Gram Swarozgar Yojana (SGSY), has been renamed as

a) National Gram Swarozgar Yojana (NGSY).

b) Swarnjayanti Rural Livelihood Mission (SRLM)

c) National Rural Livelihood. Mission (NRLM)

d) National Rural Mission Yojana (NRMY)

69) When Business Correspondent has to update Current Account, Saving Fund

account:

a) Next working day

b) Within 2 days

c) Within 5 days.

d) Within 7 days

70) Under NRLM scheme, the second dose of loan will be repaid in ___

months:

a) 6-12

b) 12-24

c) 12-36

d) 24-36

71) Pursuant to the Government of India extending the scheme of 1% interest

subvention to housing loans up to Rs. ____ lakh where the cost of the house does not

exceed Rs. ___ lakh:

a) 5; 15

b) 10, 15

c) 15; 25

d) 20; 30

72) Under Janashree Bima Yojana the annual premium is Rs. ___ , of which Rs.

___ is to be contributed by the artisan, Rs. ___ by the Govt. and Rs. ____ by LIC.

a) 100 ; 20 ; 40 ; 40

b) 100 ; 10 ; 45 ; 45

36 “Profitability, Asset Quality, Capital Optimization and Efficiency”

c) 200; 20 ;80 , 100

d) 200; 40 :60 , 100

73) Under National Rural Livelihood Mission (NRLM) scheme a women's self help

group consisting of members, coming together on the basis of mutual affinity is the

primary building block of the NRLM community institutional design. In case of special

SHGs i.e. groups in the difficult areas, groups with disabled persons, and groups

formed In remote tribal areas, this number may be a minimum of persons. The

mission will provide a continuous hand-holding support to the Institutions of

poor for a period of years till they come out of abject poverty.

a) 5-10; 3; 5-5

b) 7-10; 5; 3-8

c) 10-15; 5; 5-7

d) 15-20; 10; 7-10

74) Under NRLM scheme, the second dose covers ___ times of existing corpus and

proposed saving during the next twelve months or Rs. ___ whichever is higher.

a) 1-5, 50,000

b) 2-10, 1 lac

c) 5-10, 1 lac

d) 10-20, 5 lac

75) NRLM would provide a Revolving Fund (RF) support to SHGs in existence for a

minimum period of ____ months. Only such SHGs that have not received any RF

earlier will

be provided with RF, as corpus, with a minimum of Rs. ___ and up to a maximum of

Rs.______ per SHG.

a) 1 to 5; 5,000; 10,000

b) 3 to 6; 10,000; 15,000

c) 5 to 7; 12,000, 20,000

d) 7 to 10; 15,000, 25,000

76) Under Janashree Bima Yojana, in addition to the insurance cover, a scholarship

of Rs. ______ per quarter per child for the education of two children from 9th to

12th Standard is also provided under the Shlksha Sahyog Yojana.

a) 200

b) 300

c) 500

d) 600

37 “Profitability, Asset Quality, Capital Optimization and Efficiency”

77) State level bankers' committees (SLBCs) mandated to prepare a roadmap

covering all unbanked villages of population less than and notionally allot these

villages to banks for providing banking services, in a time-bound manner. While

preparing the roadmap for providing banking services in all unbanked villages with

population of less than 2000 through a combination of banking correspondent (BC)

and branches, it

should be ensured that there is a brick and mortar branch to provide support to a

cluster of BC units, i.e., about 8-10 BC units, at a reasonable distance of 3-4

kilometres.

a) 1000

b) 1500

c) 2000

d) 2500

ANSWER

1 A 2 B 3 B 4 B 5 A

6 D 7 C 8 D 9 A 10 B

11 D 12 B 13 B 14 C 15 D

16 B 17 A 18 A 19 A 20 A

21 B 22 C 23 C 24 C 25 0

26 A 27 B 28 C 29 A 30 D

31 C 32 B 33 C 34 A 35 C

36 B 37 E 38 B 39 B 40 B

41 B 42 D 43 C 44 A 45 A

46 C 47 D 48 D 49 D 50 B

51 B 52 B 53 0 54 A 55 A

56 D 57 D 58 C 59 A 60 B

61 A 62 A 63 C 64 C 65 D

66 C 67 C 68 C 69 A 70 B

71 C 72 D 73 C 74 C 75 B

76 B 77 C

38 “Profitability, Asset Quality, Capital Optimization and Efficiency”

For the month of May 2016

1. The extent of coverage under CGTMSE for Micro Unit s up to Rs.5 lacs is ______

2. Statutory Liquidity Ratio (SLR) defined in which section

3. Interest @ ____ is given by RBI on CRR balance maintained by banks

4. Cash Reserve Ratio is maintained as a percentage of

5. What should be annual income of a BPL family to be eligible for giving interest subvention under educational loan?

6. What is the Banker-Customer relationship in case of cheques sent for collection:

7. No bank can issue bearer draft/pay order as per which act:

8. If Net working Capital is 48 and Current Liabilities are 12, what is the Current Ratio

9. Cluster based approach is applicable for

a) Priority credit advance

b) SME

c) SHG

10. What is Hybrid debt instrument ?

a) Debenture

b) Bond

c) Preference shares

d) Convertible Bonds

11. Implied authority of a partner does not allow ____ singly?

12. What is the minimum and maximum period for FCNR (B)

13. What is a full form of MCLR

14. Full form of LRS

15. In case of equitable mortgage, deposit of title deeds has to be at _______

39 “Profitability, Asset Quality, Capital Optimization and Efficiency”

16. What is the % age of provision on Standard assets in case of Direct Agriculture and Direct MSE advances.

17. Bailment of goods for securing a repayment of loan is called

18. As per the revised guidelines, the withdrawal of all old Mahatma Gandhi pre-2005 series notes is _____

19. If ___ number of counterfeit notes are detected in single transaction, a consolidated report sent to police station:

20. In case of House Loan where loan amount is above Rs.75 lac, Loan to Value

Is 75% the risk weight is _______:

21. What is the risk weight in case of Staff loan secured by mortgage or superannuation benefits

22. Mortgage means:

23. What is the interest rate in case of Sovereign Gold Bond Scheme :

24. What is the premium in cas of PMFSY

25. What is the rate of TDS in case of Savings Bank deposit account as per Income Tax Act Section 80 TTA

26. What is the rate of TDS in case the customer does not submit PAC Card and 15G/H

27. Certificate of incorporation refers to:

28. Hypothecation is defined in:

29. Negative Line refers to

30. When guarantor on payment of all dues of principal debtor gets which rights as that of creditor?

a) Subrogation

b) Lien

c) Assignment

d) Pledge

31. Rating of Bank is carried by RBI on CAMELS criteria, what do “C” stands for ?

32. Bank is not required to produce original book of records but true copy can be submitted when court has demanded as per which act<

a) Civil Procedure code

b) Registration act

c) B R Act

d) RBI act

e) Banker Books of Evidence Act

33. To improve Current Ratio of 2:1, what has to be done?

a) Recover cash from Receivables b) Cash Sales

c) Decrease the Bills payables

34. Whether WILL has to be registered ?

35. Which of the following does not come under Tier II capital?

a) Capital reserves

b) Undisclosed reserves

40 “Profitability, Asset Quality, Capital Optimization and Efficiency”

c) Revaluation reserves

d) Cumulative Perpetual shares

36. Which of the following can purchase NPA?

a) ARC

b) Banks

c) Financial Institutions

d) NBFC

e) All of the above

37. Nominee can claim payment when

38. A foreign tourist who is in India and is having US$ 5,000 wants to open a/c. Which type of deposit account he can open

39. What is the target in DRI scheme for women:

40. Food & Processing industry up to what amount can be given under priority sector

41. Unspent Foreign Currency to be surrendered within:

42. Special Crossing – what is essential:

43. Locker Operation to be categories under High and Low risk in case of non-operation of such accounts for ____ and ____

44. Why International Financial Reporting System (IFRS) should be implemented

45. Agent dies – Cheque signed by him presented for payment :

46. Financial Director dies – Cheque signed by him presented for payment:

47. If Garnishee Order does not specify any amount, it will be applicable or not

48. As per LTV guidelines, what is the risk weight for housing loan up to 30 lakhs with L T V of 75% :

49. As per the Task Force committee headed by T K A Nair, the banks to achieve annual growth of ___ % in Micro enterprise accounts

50. NPA –D3 Category ( Beyond three years):

51. MSE single window ceiling of the amount with CGTMSE coverage

52. Banks undertake BEP analysis to assess:

53. Guarantee given by a minor:

54. NABARD undertakes supervision on which type of Bank:

ANSWERS

1. 85% with maximum amount of claim upto Rs4.25 lakhs

2. Section 24(2) of Banking Regulation Act

3. Nil

4. Net Demand and Time Liabilities (NDTL)

5. Rs4.50 lac

6. Agent and Principal

7. Sec 31 of Reserve Bank of India Act

8. 5:1 (Current assets 60: Current liability 12)

41 “Profitability, Asset Quality, Capital Optimization and Efficiency”

9. b) SME

10. d) Convertible Bonds

11. Settle a dispute relating to the business of the firm thru arbitration

12. 1 year and 5 years

13. Marginal cost of funds based lending rate

14. Liberalized Remittance Scheme

15. Any notified town notified by the State Govt

16. 0.25% of outstanding

17. Pledge

18. 30-06-2016

19. Less than 5

20. 75%

21. 20%

22. Transfer of interest in a specific immovable property

23. 2.75%

24. 1.5% Rabi 2% Khariff

25. TDS is not applicable in savings bank interest

26. @20%

27. Birth certificate for a company issued by ROC

28. Sec 2(n) of SARFAESI Act

29. Undertaking given by the company not to create any charge/not to get the assets encumbered to any other bank during the currency of bank borrowings

30. a) Subrogation

31. Capital Adequacy

32. e) Banker Books Evidence Act

33. Decrease the Bills Payables

34. Not required

35. Capital Reserves

36. e) All of the above

37. Only after the death of depositor as a trustee of legal heir

38. NRO for a maximum period of 6 months

39. No Target for women

40. Rs.100 crores

41. 180 days

42. Bank’s name must appear with or without two parallel lines

43. 1 year and 3 years respectively

44. For comparision of financials of companies operating in two different international jurisdictions.

45. Can be paid as for all acts of agent, principal is liable.

46. Can be paid as he is signing in representative capacity

47. Applicable and full amount in the a\c will be attached.

48. 35%

49. 10%p.a.

50. 100% Provision both on secured and unsecured

51. Rs.1 crore

52. Margin for safety

53. Cannot be ratified even when he becomes major

42 “Profitability, Asset Quality, Capital Optimization and Efficiency”

54. RRBs.