module 6 - cengage learning · web viewthe difference between simple and compound interest is next....

TRANSCRIPT

Module 6Time Value of Money

Interest–Overview

Interest is the cost a lender charges for using money. It is calculated as follows:

I = P x R x NwhereI = Amount of simple interestP = Principal amountR = Interest rateN = Time in number of periods

Note the following:1. R, the interest rate, is normally expressed in terms per year. Hence, if interest is calculated in periods less than a year, appropriate adjustments must be made. 2. Interest is always calculated based on the beginning balance of the principal amount for any period.

Simple interest means that interest accrues only on the principal. Compound interest means that interest accrues on the entire amount owed at a time, which may include both the principal and the interest accrued from previous periods. The difference between simple and compound interest is next.

Simple and Compound Interest Calculations

ExampleAssume that $1,000 was borrowed on January 1, 2002, at the rate of 10% per annum. (Note: Annum means one year.) Calculate the total interest and the total amount owed as of December 31, 2003, assuming (1) simple interest and (2) compound interest.

1. Simple interest is calculated for two years as follows:$1,000 x 0.10 x 2 = $200The total amount owed at the end of two years = $1,200 ($1,000 principal + $200 interest).

2. Compound interest is calculated as follows:Interest for the first year = $1,000 x 0.10 x 1 = $100.Thus, the total amount owed at the end of the first year = $1,100 ($1,000 principal + $100 interest for the first year).Interest for the second year must be calculated on the total amount owed at the beginning of the second year, which is $1,100.Thus, interest for the second year = $1,100 x 0.10 x 1 = $110.Hence, total interest for the two years = $210 ($100 for the first year + $110 for the second year).Total amount owed at the end of two years = $1,210 ($1,000 principal + $210 compound interest for two years).

Note the difference between simple and compound interest preceding example. For the second year, when calculating simple interest, we ignore the fact that an additional $100 (the interest for

the first year) is also owed at the beginning of the second year. This additional $100 is not ignored in calculating compound interest. Thus, compound interest implies “interest on the interest.”

What are the simple interest and compound interest for three years if the initial amount borrowed is $1,000 and the interest rate is 10% per annum?Simple interest is calculated as follows$1,000 x 0.10 x 3 = $300Thus, the total amount owed at the of three years = $1,300 ($1,000 principal + $300 interest for three years).

Compound interest is calculated as follows:Amount owed at the end of the first year = $1,100 ($1,000 principal + $100 interest for one year).Amount owed at the end of the second year = $1,210 ($1,100 owed at the beginning of the second year + $110 interest on this $1,100 for one year).Amount owed at the end of the third year = $1,331 ($1,210 owed at the beginning of the third year + $121 interest on this $1,210 for one year).

In general, when using compound interest, the amount owed at the end of N periods when the rate of interest is R and the principal amount is P is calculated using the following formula:

A = P(1 + R)N where A = the total amount owed at the end of N periods.

Future Value and Present Value

Future value of a single sum = P(1 + R)N

whereP = Principal amountR = Rate of interestN = Time in number of periods

Future value calculations project value to the future using compound interest. In contrast, present value calculations project value from the future to the present using compound interest. For example, we calculated earlier that if we borrow $1,000 now at 10% per annum, the total amount owed at the end of two years will be $1,210. This can be restated as follows:The future value is $1,210 two periods from now when the interest rate is 10% per annum and the principal amount now is $1,000.The present value now of receiving $1,210 two periods from now is $1,000, when the rate of interest is 10% per annum.

Present value is calculated as follows:Present value of a single sum = P/(1 + R)N

whereP = Principal amountR = Rate of interestN = Time in number of periods

Most textbooks provide present value and future value tables. They are presented at he end of this module for 6%, 8%, 10%, and 12%. In addition, programmable financial calculators can be used to calculate present and future value numbers.

The rate of interest used in present value calculations is also referred to as the discount rate.

Annuities

Annuities involve a series of cash flows over a period of time. Receipt (or payment) of a constant amount each period for a number of periods is an annuity. For example, home mortgage payments are an annuity. Similarly, lottery payments constitute an annuity (e.g., a $1 million winner receives $50,000 per year [before taxes] for 20 years).

The two types of annuities are ordinary annuity and annuity due. If the first payment of an annuity is received at the end of the first period, that is an ordinary annuity. Thus, an ordinary annuity makes the last payment at the end of the last period. If the first payment of an annuity is received at the beginning of the first period, it is an annuity due. Thus, an annuity due makes the last payment at the beginning of the last period.

We can calculate the present value or future value of an annuity. Most textbooks also include tables for annuities (– present and future value, ordinary annuity and annuity due). In addition, calculators can be used to calculate annuity values.

Deferred Annuities

The word deferred means postponed. A deferred annuity makes the first payment at a specified time in the future. Assume that you will receive $1,000 per year each year for three years, beginning six years from now –a deferred annuity.

The present or future value of a deferred annuity can also be calculated using tables or the calculator. First, we assume that the payments begin in the current period and continue until they actually stop. We can calculate the present value of this assumed (longer) period. Next we subtract from this the value of the annuity for the extra periods (in which we really do not have a payment). The analogy is as follows. 4 + 5 + 6 = (1 + 2 + 3 + 4 + 5 + 6) – (1 +2 + 3) See the following example.

ExampleYou will receive $1,000 per year each year for three years beginning six years from now. What is the present value of this deferred annuity, assuming an interest rate of 8% per annum?

Step 1: Calculate when the last payment will be received. The first payment is six years from now (that is, at the beginning of year 7 if today is the beginning of year 1), and there are three payments will be made. Hence, the last payment will be made at the start of year 9.

Step 2: Calculate the present value of an annuity assuming payments from this period up to the last actual payment period.

In this example, we calculate the present value of an annuity of $1,000 for nine years at 8% per annum. Note that the payments are received at the beginning of the period, so this is an annuity due. Also note that this does not actually happen (because the actual payments begin only at the beginning of year 7), but we pretend that this happens in this step to make the calculations easy.Using the table given with this module, we see that the present value of an annuity due for nine years at 8% per period is 6.75. Thus, the total present value of the annuity in this case is $6,750 ($1,000 x 6.75).

Step 3: Calculate the present value of the payments that actually are not received.In the preceding example, payments are not received for the first six periods. The present value of an annuity due for six periods at 8% per annum is 5.00. Thus, the total present value of the annuity of payments that are not actually received is $5,000 ($1,000 x 5.00).

Step 4: Subtract the present value of the payments that actually are not received to get the present value of the deferred annuity.Present value of the actual payments to be received = $1,750 ($6,750 – $5,000).

Comparison of Options

Sometimes we must compare an option to receive an immediate payment with an option to receive payment (or an annuity of payments) in the future. In such instances, which option should we choose?

In general, we prefer the option that gives us more money (or costs less). However, to ensure a fair comparison, we need a level playing field. This means that all options must be at the same level; that is, we must compare either all available options using the total present value of the options or the future value of all available options at a given time in the future.

For example, assume that we have won the lottery and have two options: Receive $100,000 a year for 10 years beginning today or receive $650,000 right now. Which option do we prefer if the interest rate (discount rate) is 10% per year?

Option 1 is an annuity due.The present value of an annuity due for 10 years at 10% (from the attached table) is 6.75.Thus, the total present value of the annuity we will receive is $675,000 ($100,000 x 6.75).

Option 2 is a single sum of $650,000 now. In this case, the present value also is $650,000 (because you are getting the amount at the present).

Comparing options 1 and 2 using their total present values, we find that option 1 has a higher present value. Hence, option 1 is preferable.

If the amount we will get now is more than $675,000, then the immediate payment option is better. For example, if the choice is between getting $100,000 a year for 10 years and getting $700,000 right now, the better choice is to take the $700,000 right now.

Note that such calculations and comparisons depend on the interest rate used. For example, if the relevant interest rate is 8%, the present value of the annuity is $725,000, so getting the

annuity is preferable to getting $700,000 right now. If the interest rate is 8%, the immediate payment must be more than $725,000 to be better than the annuity.

Glossary

Annuity is a series of cash flows over a period of time.

Compound interest accrues on the entire amount owed at a time, which may include both the principal and the interest accrued from previous periods.

Deferred annuity makes the first payment at a specified time in the future.

Discount rate is the interest rate used for present value calculations.

Future value projects value to the future using compound interest.

Interest is the cost a lender charges for using money.

Present value projects value from the future to the present using compound interest.

Simple interest accrues only on the principal.

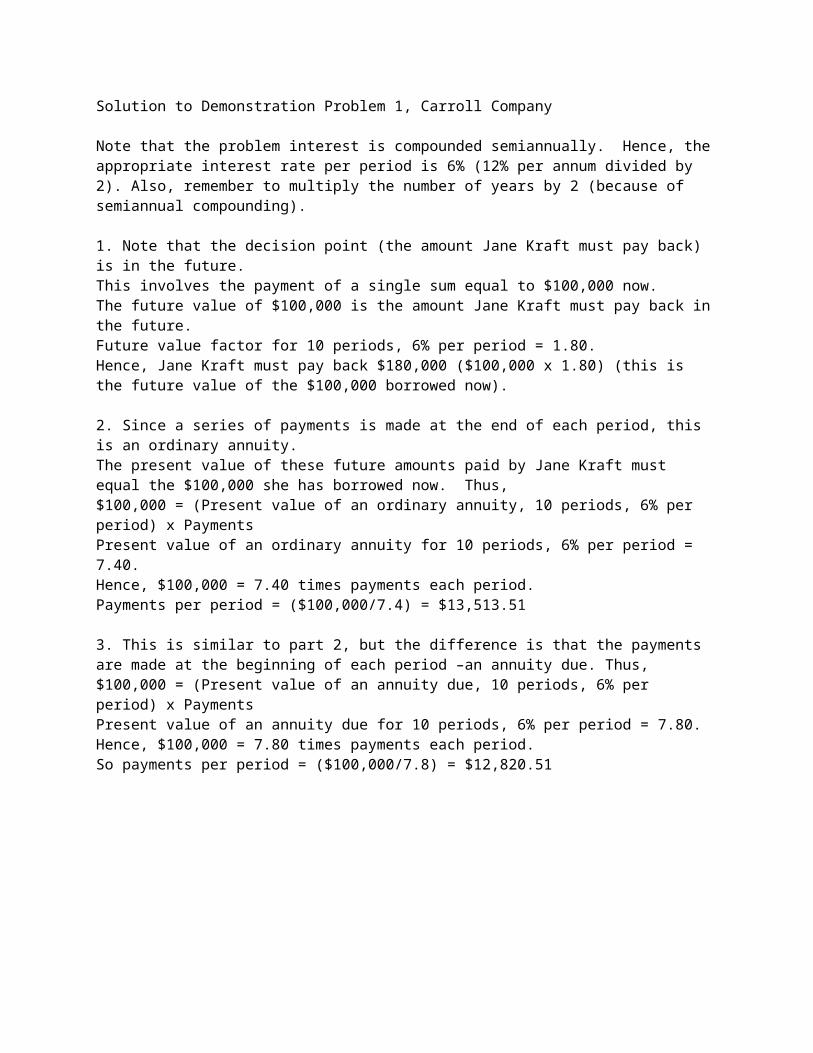

Demonstration Problem 1Carroll Company

Carroll Company loaned $100,000 to Jane Kraft, its president. The interest rate is 12% per annum and will be compounded semiannually. Calculate the appropriate amount to be paid under each of the three separate scenarios: 1. Repayment of the entire loan after five years. 2. Payment of an equal sum at the end of each period.3. Payment of an equal sum at the beginning of each period.

Solution to Demonstration Problem 1, Carroll Company

Note that the problem interest is compounded semiannually. Hence, the appropriate interest rate per period is 6% (12% per annum divided by 2). Also, remember to multiply the number of years by 2 (because of semiannual compounding).

1. Note that the decision point (the amount Jane Kraft must pay back) is in the future.This involves the payment of a single sum equal to $100,000 now. The future value of $100,000 is the amount Jane Kraft must pay back in the future.Future value factor for 10 periods, 6% per period = 1.80.Hence, Jane Kraft must pay back $180,000 ($100,000 x 1.80) (this is the future value of the $100,000 borrowed now).

2. Since a series of payments is made at the end of each period, this is an ordinary annuity.The present value of these future amounts paid by Jane Kraft must equal the $100,000 she has borrowed now. Thus, $100,000 = (Present value of an ordinary annuity, 10 periods, 6% per period) x PaymentsPresent value of an ordinary annuity for 10 periods, 6% per period = 7.40.Hence, $100,000 = 7.40 times payments each period.Payments per period = ($100,000/7.4) = $13,513.51

3. This is similar to part 2, but the difference is that the payments are made at the beginning of each period –an annuity due. Thus, $100,000 = (Present value of an annuity due, 10 periods, 6% per period) x PaymentsPresent value of an annuity due for 10 periods, 6% per period = 7.80.Hence, $100,000 = 7.80 times payments each period.So payments per period = ($100,000/7.8) = $12,820.51

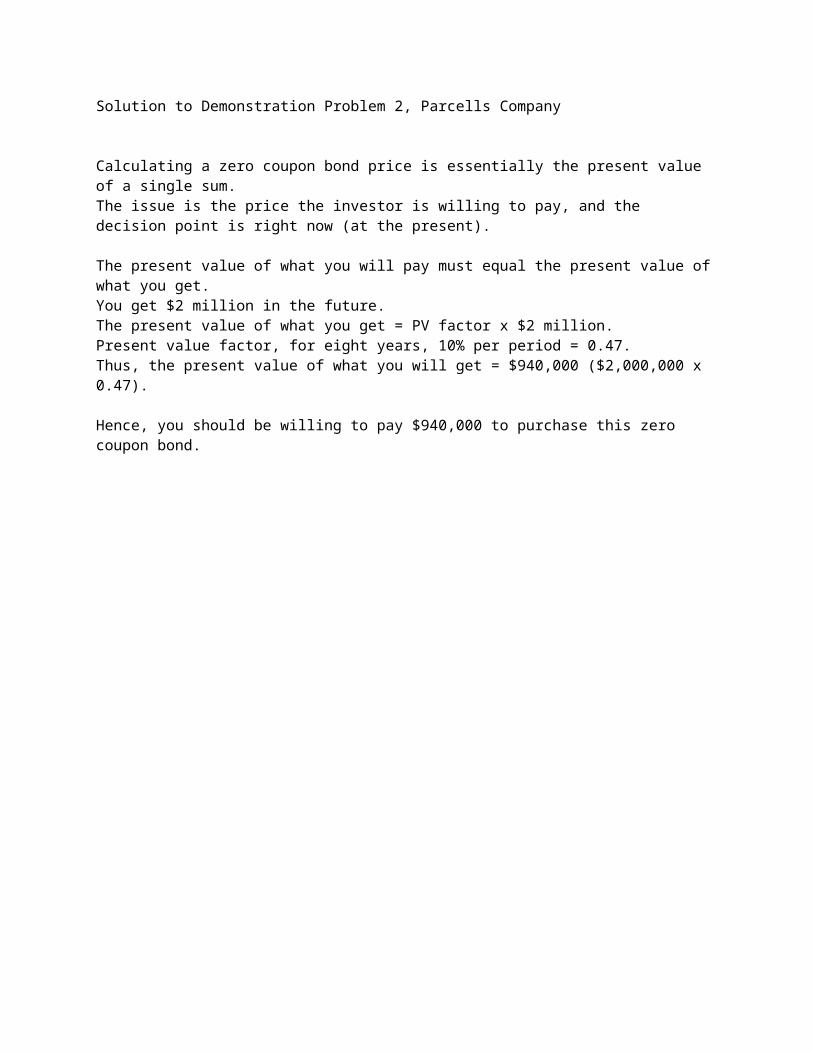

Demonstration Problem 2Parcells Company

A zero coupon bond pays no interest during its life. The bond investor pays some amount to the company, and the company then pays back the investor the specified amount (face value) of the bond at the end of the specified period. Assume that Parcells Company has offered you a zero coupon bond that will pay $2 million at the end of eight years. If your interest rate used for discounting is 10% per annum, what price will you be willing to pay to purchase the bond now?

Solution to Demonstration Problem 2, Parcells Company

Calculating a zero coupon bond price is essentially the present value of a single sum.The issue is the price the investor is willing to pay, and the decision point is right now (at the present).

The present value of what you will pay must equal the present value of what you get. You get $2 million in the future.The present value of what you get = PV factor x $2 million.Present value factor, for eight years, 10% per period = 0.47.Thus, the present value of what you will get = $940,000 ($2,000,000 x 0.47).

Hence, you should be willing to pay $940,000 to purchase this zero coupon bond.

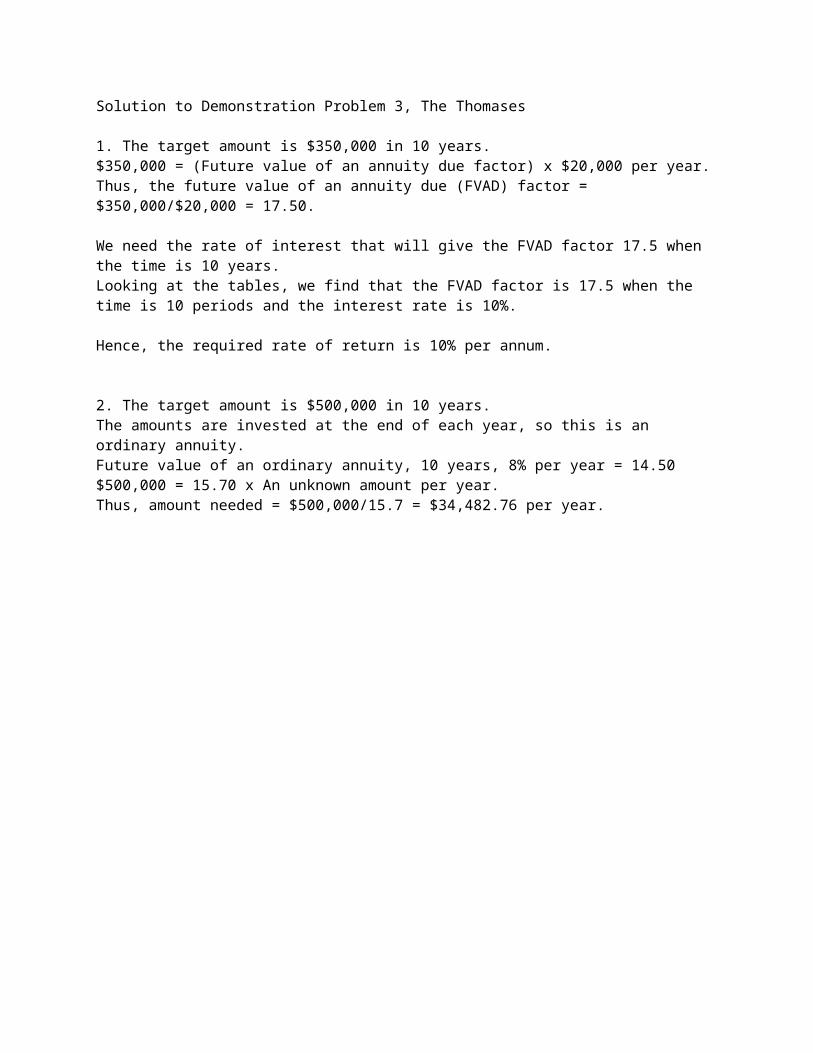

Demonstration Problem 3The Thomases

I. Sam and Pam Thomas want to establish two funds. 1. They want to start a fund for their newborn daughter. If they want to have $350,000 in the

fund in 10 years and can contribute $20,000 a year beginning today, what is the rate of return they must earn to achieve their goal?

2. They wish to have $500,000 in their retirement fund and plan to retire in 10 years. If they expect to earn 8% per year, what amount should they start investing each year, assuming that they invest at the end of each year?

Solution to Demonstration Problem 3, The Thomases

1. The target amount is $350,000 in 10 years.$350,000 = (Future value of an annuity due factor) x $20,000 per year.Thus, the future value of an annuity due (FVAD) factor = $350,000/$20,000 = 17.50.

We need the rate of interest that will give the FVAD factor 17.5 when the time is 10 years.Looking at the tables, we find that the FVAD factor is 17.5 when the time is 10 periods and the interest rate is 10%.

Hence, the required rate of return is 10% per annum.

2. The target amount is $500,000 in 10 years.The amounts are invested at the end of each year, so this is an ordinary annuity.Future value of an ordinary annuity, 10 years, 8% per year = 14.50$500,000 = 15.70 x An unknown amount per year.Thus, amount needed = $500,000/15.7 = $34,482.76 per year.

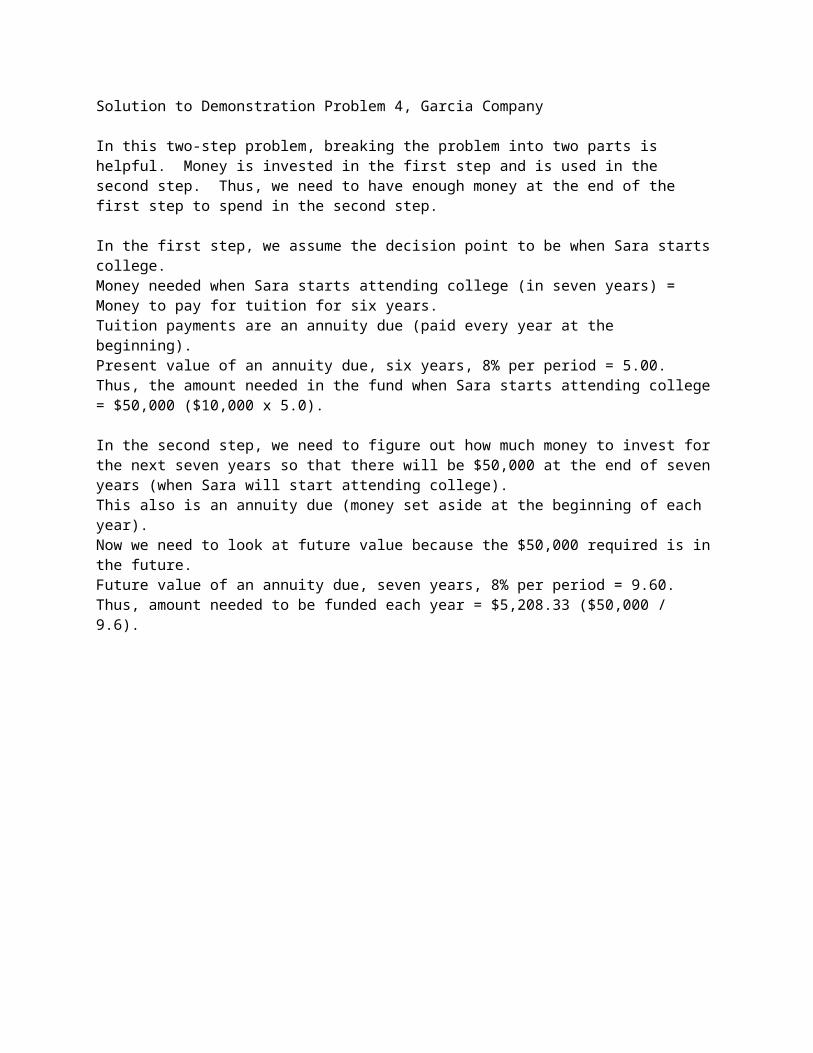

Demonstration Problem 4Garcia Company

Jim Garcia is setting aside money to send his daughter Sara to college. Sara believes college life is to be enjoyed and estimates that she will need six years to obtain her degree. Tuition and fees will be $10,000 per year, and Sara will start attending college seven years from now. How much money should Jim Garcia set aside for his daughter’s college tuition and fees if he will set aside the same amount each year beginning today and can expect to earn 8% per annum? (Assume that the entire amount of tuition and fees will be paid at the beginning of each year.)

Solution to Demonstration Problem 4, Garcia Company

In this two-step problem, breaking the problem into two parts is helpful. Money is invested in the first step and is used in the second step. Thus, we need to have enough money at the end of the first step to spend in the second step.

In the first step, we assume the decision point to be when Sara starts college.Money needed when Sara starts attending college (in seven years) = Money to pay for tuition for six years.Tuition payments are an annuity due (paid every year at the beginning).Present value of an annuity due, six years, 8% per period = 5.00.Thus, the amount needed in the fund when Sara starts attending college = $50,000 ($10,000 x 5.0).

In the second step, we need to figure out how much money to invest for the next seven years so that there will be $50,000 at the end of seven years (when Sara will start attending college).This also is an annuity due (money set aside at the beginning of each year).Now we need to look at future value because the $50,000 required is in the future.Future value of an annuity due, seven years, 8% per period = 9.60.Thus, amount needed to be funded each year = $5,208.33 ($50,000 / 9.6).

Practice Problem 1Swift Company

Susan Swift borrowed $500,000 from First National Bank to expand her factory. If the interest rate is 8% per year, calculate the amount she will have to pay the bank under each of the following separate assumptions. 1. Repayment of the entire loan after six years. 2. Payment of an equal sum at the end of each period for seven periods3. Payment of an equal sum at the beginning of each period for 10 periods.

Solution to Practice Problem 1, Swift Company

1. Note that the decision point (the amount Swift will have to pay back) is in the future.Future value factor for six periods, 8% per period = 1.60.Swift must pay back $800,000 ($500,000 x 1.60).

2. Since there is a series of payments at the end of each period, this is an ordinary annuity.$500,000 = (Present value of an ordinary annuity, 7 periods, 8% per period) x PaymentsPresent value of an ordinary annuity for 7 periods, 8% per period = 5.20.Hence, $500,000 = 5.20 times payments each period.Therefore, payments per period = ($500,000/5.2) = $96,153.85

3. As there is a series of payments at the beginning of each period, this is an annuity due. $500,000 = (Present value of an annuity due, 10 periods, 8% per period) x PaymentsPresent value of an annuity due for 10 periods, 8% per period = 7.25.Hence, $500,000 = 7.25 times payments each period.Therefore, payments per period = ($500,000/7.25) = $68,965.52

Practice Problem 2Millionaires Company

Assume that you have won $1 million in the lotto. However, you find out that the full amount will be paid in equal installments over 10 years, beginning today. In addition, you discover that the federal and state taxes (which amount to 30 percent) will be withheld before you get the check from the lottery agency. You also discover that you have the option to take one lump payment right now. If the relevant discount rate is 10%, what is the amount of the prize money you will take to the bank under each option?

Solution to Practice Problem 2, Millionaires Company

The prize money of $1 million is given over 10 years.Hence, the prize money per year is $100,000 ($1 million divided by 10).From this, 30 percent will be withheld for taxes. Thus, taxes withheld each period = $30,000 ($100,000 x 0.30).The amount you take to the bank each period = $70,000 ($100,000 – $30,000).This is an annuity due (because the first payment is right now).The present value of an annuity due, 10 periods, 10% per period = 6.75.Thus, the prize money you receive by accepting one lump sum = $472,500 ($70,000 x 6.75).

Practice Problem 4Fox Company

Fox Company purchased a machine for $100,000. The company has agreed to pay the dealer over a period of years. 1. What amount must the company pay each period if it pays equal amounts semiannually for five years, beginning today? Assume that the applicable interest rate is 12% per year.2. What is the interest rate if the company pays $16,000 per year, at the end of each year, for nine years?

Solution to Practice Problem 3, Fox Company

1. $100,000 = Present value of an annuity due (PVAD) factor x Periodic paymentsSince payments are made semiannually, applicable interest rate is 6% per period, and the number of periods is 10.PVOA, for 10 periods, 6% per period = 7.80Hence, annual payments = $100,000/7.80 = $12,820.51

2. $100,000 = Present value of an ordinary annuity (PVOA) factor x $16,000PVOA factor = $100,000/$16,000 = 6.25From the tables, the PVOA factor is 6.25 for nine years at 8%.Hence, the applicable interest rate = 8%.

Practice Problem 4Rodriguez Company

Rodriguez Company is setting aside money to fund its pension fund. The fund will begin paying retirement benefits to employees nine years from now and will pay benefits of $300,000 a year at the start of each year for seven years. How much money should Rodriguez Company set aside at the end of each year of next nine years, to have enough money in the fund to pay the retirement benefits? Assume that the company expects to earn 10% per year on its investments.

Solution to Practice Problem 4, Rodriguez Company

Money needed at the start of the second stage (when benefits are paid) = $300,000 x Present value of an annuity due (PVAD) factor for seven years, 10% per year = $300,000 x 5.35 = $1,605,000

Therefore, $1,605,000 is needed nine years from now, and the company will fund this amount through an ordinary annuity (set aside money at the end of each year).$1,605,000 = (Amount to fund) x Future value of an ordinary annuity (FVOA) for nine years, 10% per year = (Amount to fund) x 13.6 Hence, amount to fund each year = $118,014.70

Homework Problem 1Tipper Company

Tipper Company wants to sell a parcel of land. It has received two offers as follows:1. Clarence Company will pay $60,000 at the end of each year for eight years.2. Steven Company will pay $70,000 at the beginning of each year for six years.If the relevant interest rate for Tipper Company is 12% per year, what is the present value of the two offers, and which offer should it accept?

Solution to Homework Problem 1, Tipper Company

1. Present value of offer from Clarence Company = $60,000 x PVOA, 8 years, 12% = $60,000 x 5.00= $300,000

2. Present value of offer from Steven Company = $70,000 x PVAD, 6 years, 12%= $70,000 x 4.60= $322,000

Tipper Company should accept the offer of Steven Company.

Homework Problem 2Stewart Company

Stewart Company is considering the purchase of a machine whose market value is $23,000. The manufacturer has agreed to let Stewart Company buy the machine by making six annual payments of $5,000 beginning today. What interest rate does the manufacturer use to finance this sale?

Solution to Homework Problem 2, Stewart Company

$23,000 = PVAD factor x $5,000.PVAD factor = $23,000/$5,000 = 4.60.From the table, the PVAD factor is 4.6 for six years, when the interest rate is 12%.Thus, the interest rate used by the manufacturer is 12%.

Homework Problem 3Salinas Company

Salinas Company purchased a truck for $40,000. The company has agreed to pay the dealer over a period of years. 1. What amount will the company pay each period if it pays equal amounts at the end of each year for six years? Assume that the applicable interest rate is 10% per year.2. What is the interest rate if the company pays $8,000 per year, at the end of each year, for eight years?

Solution to Homework Problem 3, Salinas Company

1. $40,000 = Present value of an ordinary annuity (PVOA) factor x Yearly paymentsPVOA, for six years, 10% = 4.35Hence, annual payments = $40,000/4.35 = $9,195.40

2. $40,000 = Present value of an ordinary annuity (PVOA) factor x $8,000PVOA factor = $40,000/$8,000 = 5.00From the tables, the PVOA factor is 5.00 for eight years at 12%.Hence, the applicable interest rate = 12%.

Homework Problem 4Laura Company

Laura Company is setting aside money to pay off its long-term bonds that become payable six years from now and involve payments of $200,000 each year for seven years. Laura Company intends to set aside money to invest at the end of each year for six years. The bond payments are due at the end of each year. Assuming that the money set aside is the same each year and that the investments are expected to earn 12% per year, how much should Laura Company set aside each year so that the fund will have enough money to pay the bonds?

Solution to Homework Problem 4, Laura Company

Money needed at the start of the second stage (when the bonds are paid) = $200,000 x Present value of an ordinary annuity (PVOA) factor for seven years, 10% per year = $200,000 x 4.50 = $900,000

The company will fund this amount through an ordinary annuity.$900,000 = (Amount to fund) x Future value of an ordinary annuity (FVOA) for six years, 12% per year = (Amount to fund) x 8.10Hence, amount to fund each year = $111,111.11 ($900,000/8.10)

Present and Future Values Table

Present and future values (rounded for ease of use)6% per period 8% per period

Number of periods Number of periods6 7 8 9 10 6 7 8 9 10

PVSS 0.70 0.67 0.63 0.60 0.56 0.63 0.58 0.54 0.50 0.46 PVOA 4.90 5.60 6.20 6.80 7.40 4.60 5.20 5.75 6.25 6.70PVAD 5.20 5.90 6.60 7.20 7.80 5.00 5.60 6.20 6.75 7.25FVSS 1.40 1.50 1.60 1.70 1.80 1.60 1.70 1.85 2.00 2.15FVOA 7.00 8.40 9.90 11.50 13.20 7.30 8.90 10.60 12.50 14.50FVAD 7.40 8.90 10.50 12.20 14.00 7.90 9.60 11.50 13.50 15.70Note:PVSS = Present value of a single sumPVOA = Present value of an ordinary annuityPVAD = Present value of an annuity dueFVSS = Future value of a single sumFVOA = Future value of an ordinary annuityFVAD = Future value of an annuity due

Present and future values (rounded for ease of use)10% per period 12% per period

Number of periods Number of periods6 7 8 9 10 6 7 8 9 10

PVSS 0.56 0.51 0.47 0.42 0.39 0.50 0.45 0.40 0.36 0.32PVOA 4.35 4.90 5.33 5.75 6.15 4.10 4.50 5.00 5.30 5.70PVAD 4.80 5.35 5.90 6.33 6.75 4.60 5.10 5.60 6.00 6.33FVSS 1.80 1.95 2.15 2.35 2.60 2.00 2.20 2.50 2.75 3.10FVOA 7.70 9.50 11.40 13.60 15.90 8.10 10.10 12.30 14.80 17.50FVAD 8.50 10.40 12.60 14.90 17.50 9.10 11.30 13.80 16.50 19.60