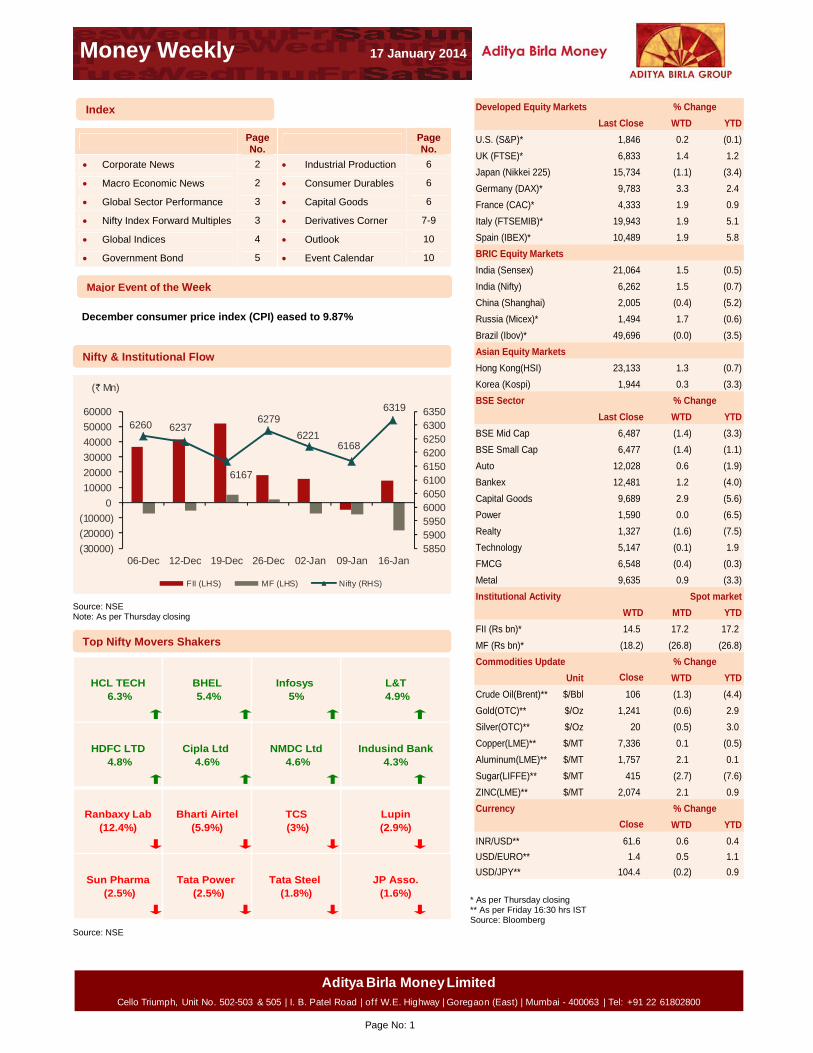

money weekly 17 january 2014

TRANSCRIPT

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 1

Page No.

Page No.

Corporate News 2 Industrial Production 6

Macro Economic News 2 Consumer Durables 6

Global Sector Performance 3 Capital Goods 6

Nifty Index Forward Multiples 3 Derivatives Corner 7-9

Global Indices 4 Outlook 10

Government Bond 5 Event Calendar 10

December consumer price index (CPI) eased to 9.87%

6260 6237

6167

6279

62216168

6319

58505900595060006050610061506200625063006350

(30000)

(20000)

(10000)

0

10000

20000

30000

40000

50000

60000

06-Dec 12-Dec 19-Dec 26-Dec 02-Jan 09-Jan 16-Jan

(` Mn)

FII (LHS) MF (LHS) Nifty (RHS) Source: NSE Note: As per Thursday closing

HCL TECH 6.3%

BHEL 5.4%

Infosys 5%

L&T 4.9%

HDFC LTD 4.8%

Cipla Ltd 4.6%

NMDC Ltd 4.6%

Indusind Bank4.3%

Ranbaxy Lab(12.4%)

Bharti Airtel(5.9%)

TCS (3%)

Lupin(2.9%)

Sun Pharma (2.5%)

Tata Power (2.5%)

Tata Steel (1.8%)

JP Asso.(1.6%)

Source: NSE

Developed Equity Markets

WTD YTD

U.S. (S&P)* 1,846 0.2 (0.1)

UK (FTSE)* 6,833 1.4 1.2

Japan (Nikkei 225) 15,734 (1.1) (3.4)

Germany (DAX)* 9,783 3.3 2.4

France (CAC)* 4,333 1.9 0.9

Italy (FTSEMIB)* 19,943 1.9 5.1

Spain (IBEX)* 10,489 1.9 5.8

BRIC Equity Markets

India (Sensex) 21,064 1.5 (0.5)

India (Nifty) 6,262 1.5 (0.7)

China (Shanghai) 2,005 (0.4) (5.2)

Russia (Micex)* 1,494 1.7 (0.6)

Brazil (Ibov)* 49,696 (0.0) (3.5)

Asian Equity Markets

Hong Kong(HSI) 23,133 1.3 (0.7)

Korea (Kospi) 1,944 0.3 (3.3)

BSE Sector

WTD YTD

BSE Mid Cap 6,487 (1.4) (3.3)

BSE Small Cap 6,477 (1.4) (1.1)

Auto 12,028 0.6 (1.9)

Bankex 12,481 1.2 (4.0)

Capital Goods 9,689 2.9 (5.6)

Power 1,590 0.0 (6.5)

Realty 1,327 (1.6) (7.5)

Technology 5,147 (0.1) 1.9

FMCG 6,548 (0.4) (0.3)

Metal 9,635 0.9 (3.3)

Institutional Activity

WTD MTD YTD

FII (Rs bn)* 14.5 17.2 17.2

MF (Rs bn)* (18.2) (26.8) (26.8)

Commodities Update

Unit Close WTD YTD

Crude Oil(Brent)** $/Bbl 106 (1.3) (4.4)

Gold(OTC)** $/Oz 1,241 (0.6) 2.9

Silver(OTC)** $/Oz 20 (0.5) 3.0

Copper(LME)** $/MT 7,336 0.1 (0.5)

Aluminum(LME)** $/MT 1,757 2.1 0.1

Sugar(LIFFE)** $/MT 415 (2.7) (7.6)

ZINC(LME)** $/MT 2,074 2.1 0.9

Currency

Close WTD YTD

INR/USD** 61.6 0.6 0.4

USD/EURO** 1.4 0.5 1.1

USD/JPY** 104.4 (0.2) 0.9

% Change

% Change

Last Close

% Change

Last Close

Spot market

% Change

* As per Thursday closing ** As per Friday 16:30 hrs IST Source: Bloomberg

Top Nifty Movers Shakers

Index

Nifty & Institutional Flow

Major Event of the Week

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 2

Coal India declares interim dividend of Rs 29/share; Record date – 20th Jan14; Implied dividend yield of ~10% - Post this event,

the overhang of FPO will get removed and going forward, the street will start discounting FY15E/FY16E numbers – Positive in

medium to long term for Coal India; Will also have positive sentimental impact on all cash rich PSU companies in short term

Coal India has approved a special dividend of Rs 29/share (on FV of Rs 10/share) for the current financial year, which would fetch Rs

164.8 bn to government exchequer and help meet its disinvestment target of Rs 400 bn. Beside, government would also get dividend

distribution tax of Rs 31.1 bn from CIL and its subsidiaries. Thus government would get Rs 195.9 bn from CIL and its subsidiaries by way of

dividend and its tax. This dividend would be disbursed on and from January 25, 2014 to those shareholders who are holding the CIL shares

on January 20, 2014.

In short term, this event will lead to upmove in stock price of Coal India. Once, the dividend is paid, the overhand of FPO on its stock price

will get removed and going forward, the street will start discounting FY15E/FY16E numbers. With many environmental clearances in place,

the stock may give CAGR return of 10-15% over FY14-FY16E period.

TCS announces 3Q results; PAT above street estimates. Accumulate from medium to long term perspective.

TCS’s revenues jumped 32.5% YoY to Rs.212.9bn slightly below street estimates, however the company’s profits jumped 50.3% YoY to

Rs.53.3bn which was above street estimates. Operating margins stood at 29.7% for the quarter, and the company said it would be able to

maintain its margin in 27-29% range. The company said it had invested 70bps of its operating margins during the quarter into sales. Overall

the results are positive and we recommend investors to accumulate the stock from medium to long term.

Crude oil slumps on Iran nuclear deal with West – Brent and WTI falls to $106.7/barrel and $91.7/barrel respectively – Positive in

medium term for ONGC, OIL India, BPCL, HPCL and IOC

Brent and WTI has corrected to $ 106.7/barrel and $ 91.7/barrel respectively. This is led by reaction to weekend reports that Iran agreed on

a multilateral plan that would curb Tehran's nuclear ambitions in a deal that could end sanctions on the Middle East country and allow it to

resume exports and add to global supply. Talks among the U.S., Russia, China, Britain, Germany, France and Iran ended in agreement on

a six-month deal that will limit advancements in Iran's nuclear program in exchange for easing economic sanctions against Tehran starting

20th Jan14. In November, Iran pledged to eliminate its stocks of 20% enriched uranium within 6 months and limit the enrichment of

uranium to 5%. Trade sanctions slapped on Iran due to its alleged nuclear ambitions have taken out more than 1 million barrels of oil per

day from the global market over the past two years. We believe this news to be positive in medium term for ONGC, OIL India, BPCL, HPCL

and IOC.

Domestic International

IIP for the month of Nov13 shrinks 2.1%

India’s industrial production shrunk for the second month

running at -2.1% in November, reducing the prospects improved

growth in the third quarter October-December this financial year.

Manufacturing accounting for 76% of the industrial production

faring badly contracting 3.5%. Capital goods, seen as a

barometer for investment, too, was not encouraging at it grew by

a mere 0.3% in November. White goods in particular in

consumer goods too had a poor showing. Industrial output for

the first eight months for the present financial year (April-

November) shrunk 0.2% against 0.9% in year ago period.

Government defers Rs 150 bn bond issue to contain fiscal

deficit

The government's cash register is ringing again, raising the

hope that the fiscal slide would have begun to get arrested in

December and the government would achieve its fiscal deficit

target for the year. The finance ministry deferred a planned Rs

150 bn bond auction to raise funds in view of its comfortable

cash position because of robust direct tax collections in

December and anticipation of large dividend flows.

U.S. posts smallest job gains in three years - Just 74,000

positions added in December; unemployment rate falls to

6.7%

The United States added just 74,000 jobs in December to mark the

smallest gain in three years, a disappointing number likely

influenced by poor weather. The unemployment rate fell three ticks

last month to 6.7%, the first time it’s dropped below 7% in 60

months. The decline mainly occurred because more people

dropped out of the labor force. Some 347,000 Americans stopped

looking for work last month and the size of the labor force actually

shrank in 2013, a sour note in a year where the economy added a

robust 2.19 million jobs. The U.S. has created at least 2 million

jobs for three straight years, though the unemployment rate still

remains abnormally high by historical standards.

U.K. Inflation hits target for first time since 2009

U.K. inflation hit the Bank of England's 2% target for the first time

in more than than four years in December, suggesting that prices

were not bloated by robust economic recovery. Consumer prices

rose 2% YoY, the slowest since November 2009. The rate was

forecast to remain stable at 2.1%.

Source: Economic Times, Business Line, Business Standard, Times of India, DNA Money, Mint, Financial Express, Bloomberg

Top Corporate News during the week

Macro Economy & Other News

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 3

Global Sectoral Performance

DevelopedIndex value

Index Return

TechnologyBasic

MaterialsFinancials Telecom Industrials Utilities

Oil & Gas

Health Care

Consumer Goods

% % % % % % % % %

US DOW 16417 -0.12 3.07 0.08 -0.28 1.65 0.3 ---- -1.79 1.06 -0.36

UK FTSE 6832 1.37 -0.26 6.34 1.14 0.33 2.08 -0.65 1.6 4.22 1.73

GERMANY DAX 9783 3.27 -1.67 2.39 4.59 1.67 1.71 7.04 ---- 1.09 2.61

FRANCE CAC 4333 1.94 1.42 1.88 1.93 4.81 4.67 1 0.59 0.48 3.21

JAPAN NIKKEI 15734 -1.12 -0.58 -0.1 -1.17 0.39 -0.22 -0.69 1.19 -1.22 0.72

BRIC

BRAZIL BOVESPA 49697 0.00 ---- 1 0.96 3.26 3.4 -0.36 -0.65 2.01 -0.07

RUSSIA MICEX 1495 1.73 ---- ---- ---- ---- ---- ---- ---- ---- ----

INDIA NIFTY 6262 1.46 6.05 1.38 2.14 -4.26 1.41 -0.81 2.81 -1.56 1.35

CHINA SANGHAI 2005 -0.41 0.47 0.62 -0.8 -0.92 -0.21 0.63 0.83 -0.61 0.77

Asian

HONG KONG H S I 23133 1.26 5.2 -1.6 0.64 -0.25 0.39 1.28 1.07 ---- -0.9

KOREA KOSPI 1944 0.31 0.7 1.09 -1.42 -0.29 -0.02 -2.02 0.09 0.98 2.05

SINGAPORE STRAITS 3147 0.11 ---- ---- -0.35 -1.24 2.53 ---- -1.7 ---- -1.55

TAIWAN TWSE 8596 0.78 3.33 0.23 0.09 0.23 1.86 0.53 -2.22 -0.21 -0.52 Source: Bloomberg, ABML Research Note: As per Friday 16:30 hrs IST

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

Mar-07 Nov-07 Jun-08 Jan-09 Sep-09 Apr-10 Nov-10 Jul-11 Feb-12 Sep-12 Apr-13 Dec-13

1Yr Forward P/E

+2 SD

+1 SD

Mean: 15.0

-1 SD

-2 SD

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Mar-07 Nov-07 Aug-08 Apr-09 Dec-09 Aug-10 Apr-11 Dec-11 Aug-12 Apr-13 Dec-13

1Yr Forward P/B

+2 SD

+1 SD

Mean: 2.5

-1 SD

-2 SD

Source: NSE, ABML Research

Nifty Relative Valuation Metrics (1 Year Forward)

Global Equity Indices & Sectoral Performance

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 4

-5%

0%

5%

10%

15%

20%

0.0

5.0

10.0

15.0

20.0

25.0

BrazilBOVESPA

RussiaMicex

IndiaNifty*

ChinaSHCOMP

USDowJ

Germany DAX

FranceCAC

UKFTSE

JapanNIKKEI*

Hong KongHis-

SingaporeStraits

TaiwanTWSE

PE CY12 PE CY13 EPS % Change

PE FY13* PE FY14*PE FY13* PE FY14*

Source: Bloomberg, ABML Research Note: As per Friday 16:30 hrs IST

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

BrazilBOVESPA

RussiaMicex

IndiaNifty*

ChinaSHCOMP

USDowJ

Germany DAX

FranceCAC

UKFTSE

JapanNIKKEI*

Hong KongHis-

SingaporeStraits

TaiwanTWSE

(%)

P/BV CY12 P/BV CY13 Dividend Yield CY13

PE FY13* PE FY14*PE FY13* PE FY14*

Source: Bloomberg, ABML Research Note: As per Friday 16:30 hrs IST

5%

7%

9%

11%

13%

15%

17%

19%

21%

BrazilBOVESPA

RussiaMicex

IndiaNifty*

ChinaSHCOMP

USDowJ

Germany DAX

FranceCAC

UKFTSE

JapanNIKKEI*

Hong KongHis-

SingaporeStraits

TaiwanTWSE

RoE

CY12 CY13 FY13* FY14*FY13* FY14*

Source: Bloomberg, ABML Research Note: As per Friday 16:30 hrs IST

Global Indices Forward P/BV

Global Indices RoE

Global Indices Forward P/E

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 5

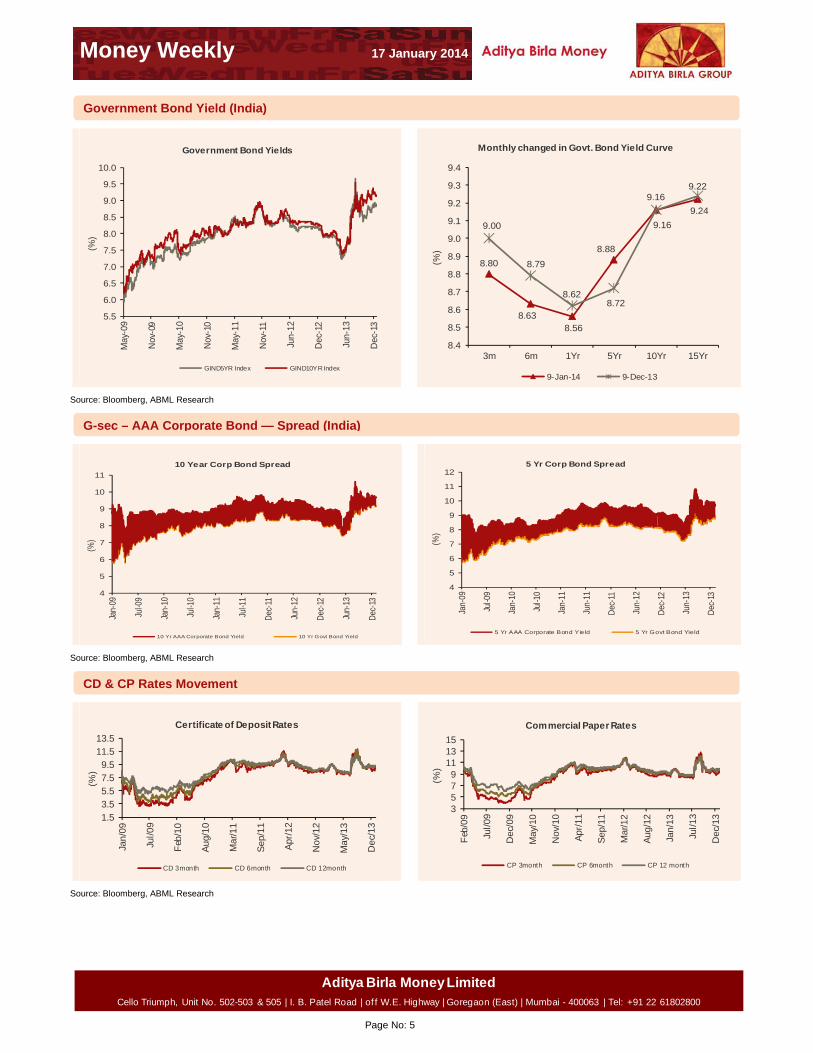

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

May

-09

Nov

-09

May

-10

Nov

-10

May

-11

Nov

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

(%)

Government Bond Yields

GIND5YR Index GIND10YR Index

8.80

8.638.56

8.88

9.169.22

9.00

8.79

8.62 8.72

9.16

9.24

8.4

8.5

8.6

8.7

8.8

8.9

9.0

9.1

9.2

9.3

9.4

3m 6m 1Yr 5Yr 10Yr 15Yr

(%)

Monthly changed in Govt. Bond Yield Curve

9-Jan-14 9-Dec-13

Source: Bloomberg, ABML Research

4

5

6

7

8

9

10

11

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

(%)

10 Year Corp Bond Spread

10 Yr AAA Corporate Bond Yield 10 Yr Govt Bond Yield

4

5

6

7

8

9

10

11

12Ja

n-09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

(%)

5 Yr Corp Bond Spread

5 Yr AAA Corporate Bond Yield 5 Yr Govt Bond Yield

Source: Bloomberg, ABML Research

1.53.55.57.59.5

11.513.5

Jan/

09

Jul/0

9

Feb

/10

Aug

/10

Mar

/11

Sep

/11

Apr

/12

Nov

/12

May

/13

Dec

/13

(%)

Certificate of Deposit Rates

CD 3month CD 6month CD 12month

3579

111315

Feb

/09

Jul/0

9

Dec

/09

May

/10

Nov

/10

Apr

/11

Sep

/11

Mar

/12

Aug

/12

Jan/

13

Jul/1

3

Dec

/13

(%)

Commercial Paper Rates

CP 3month CP 6month CP 12 month

Source: Bloomberg, ABML Research

CD & CP Rates Movement

G-sec – AAA Corporate Bond — Spread (India)

Government Bond Yield (India)

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 6

16

6 179

182

176

194

167

166

165 17

1

165

166

169

162

140150160170180190200

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Index of Industrial Production

(3)

8

2 (3)

10

(14)

(0) (1)4

(4)

1 2 (4)

-1 -1

21 4

1 -3

-2

3

02

-2 -2 (6)

(3)

-

3

6

(20) (15) (10) (5) - 5

10 15

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

MoM (%) (LHS) YoY (%) (RHS)

% in Industrial Production

Source: Bloomberg, ABML Research

301

274

285

290 31

1

277

254 27

6

278

257

271 29

6

237

100

200

300

400

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Consumer Durables Index

11

(10) (9)

4 2

7

(11) (8)

9

1

(7)

5 9

(20)

17

1

-8-1 -3

-5-10

-18

-10

-10 -8 -11-12

-21 -25-20-15-10-505101520

(25) (20) (15) (10) (5) - 5

10 15

Oct

-12

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

MoM (%) (LHS) YoY (%) (RHS)

% in Consumer Durables Index

Source: Bloomberg, ABML Research

138 17

2

176

165

168

156

144

146

144

138

143

137

141

0

50

100

150

200

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Consumer Non Durables Index

2

24

3

(6)

1

(7)

(8)

2

(1)(4)

3

(4)

3 (2)

(0)

5 3

7

11

4 6

7 5

12

2 2

(3) - 3 6 9 12 15

(10)

-

10

20

30

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

MoM (%) (LHS) YoY (%) (RHS)

% in Consumer Non Durables Index

Source: Bloomberg, ABML Research

235 261

251 28

6 343

207

219

220 27

1

245

232

247

236

0

100

200

300

400

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Capital Goods Index

(2)

11

(4)

14 20

(40)

6 0

24

(10) (5)6

(4)

(9)

(1)

(2)

9 10 (0)(4)

(7)

16

(2)(7)

2 0

-10

0

10

20

(45) (30) (15)

- 15 30

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

MoM (%) (LHS) YoY (%) (RHS)

% in Capital Goods Index

Source: Bloomberg, ABML Research

Capital Goods

Consumer Non Durables

Consumer Durables

Index of Industrial Production

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 7

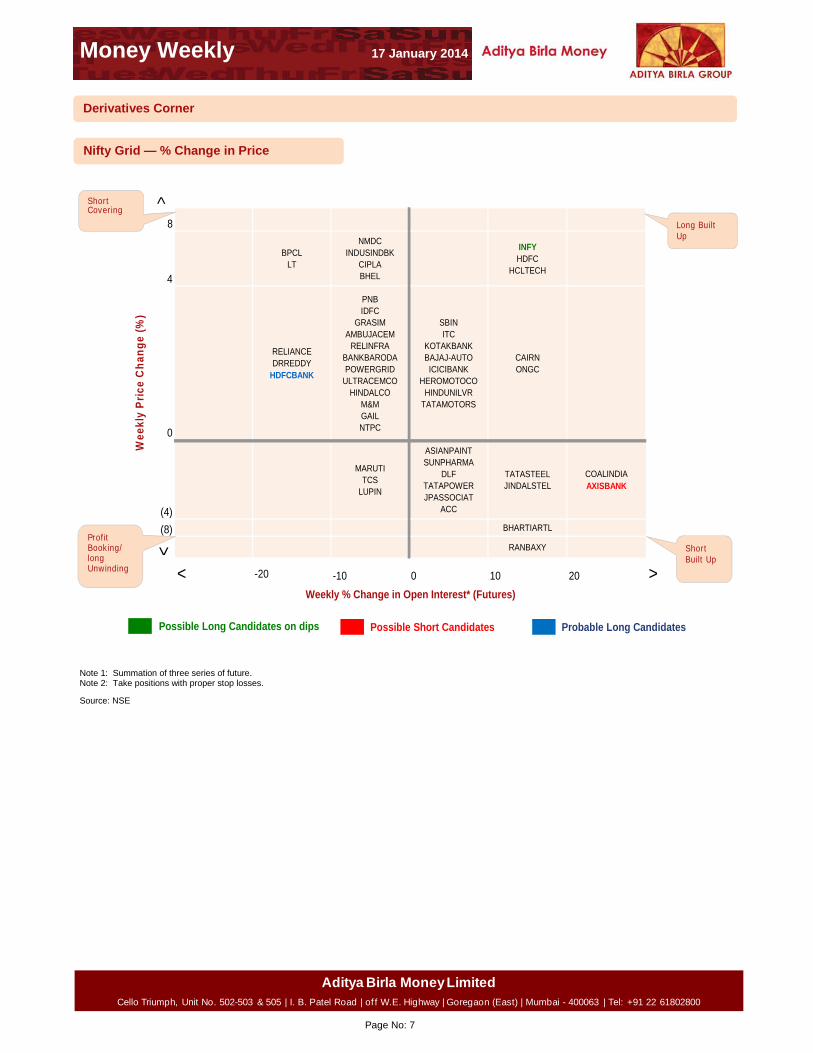

<

8

4

BPCLLT

NMDCINDUSINDBK

CIPLABHEL

INFYHDFC

HCLTECH

0

RELIANCEDRREDDY

HDFCBANK

PNBIDFC

GRASIMAMBUJACEM

RELINFRABANKBARODAPOWERGRID

ULTRACEMCOHINDALCO

M&MGAILNTPC

SBINITC

KOTAKBANKBAJAJ-AUTO

ICICIBANKHEROMOTOCO

HINDUNILVRTATAMOTORS

CAIRNONGC

(4)

MARUTITCS

LUPIN

ASIANPAINTSUNPHARMA

DLFTATAPOWERJPASSOCIAT

ACC

TATASTEELJINDALSTEL

COALINDIAAXISBANK

(8) BHARTIARTL

< RANBAXY

< -20 -10 0 10 20 >

Wee

kly

Pri

ce

Ch

ang

e (

%)

Weekly % Change in Open Interest* (Futures)

Short Covering

Long Built Up

Possible Long Candidates on dips Possible Short Candidates Probable Long Candidates

Profit Booking/long Unwinding

Short Built Up

Note 1: Summation of three series of future. Note 2: Take positions with proper stop losses.

Source: NSE

Derivatives Corner

Nifty Grid — % Change in Price

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 8

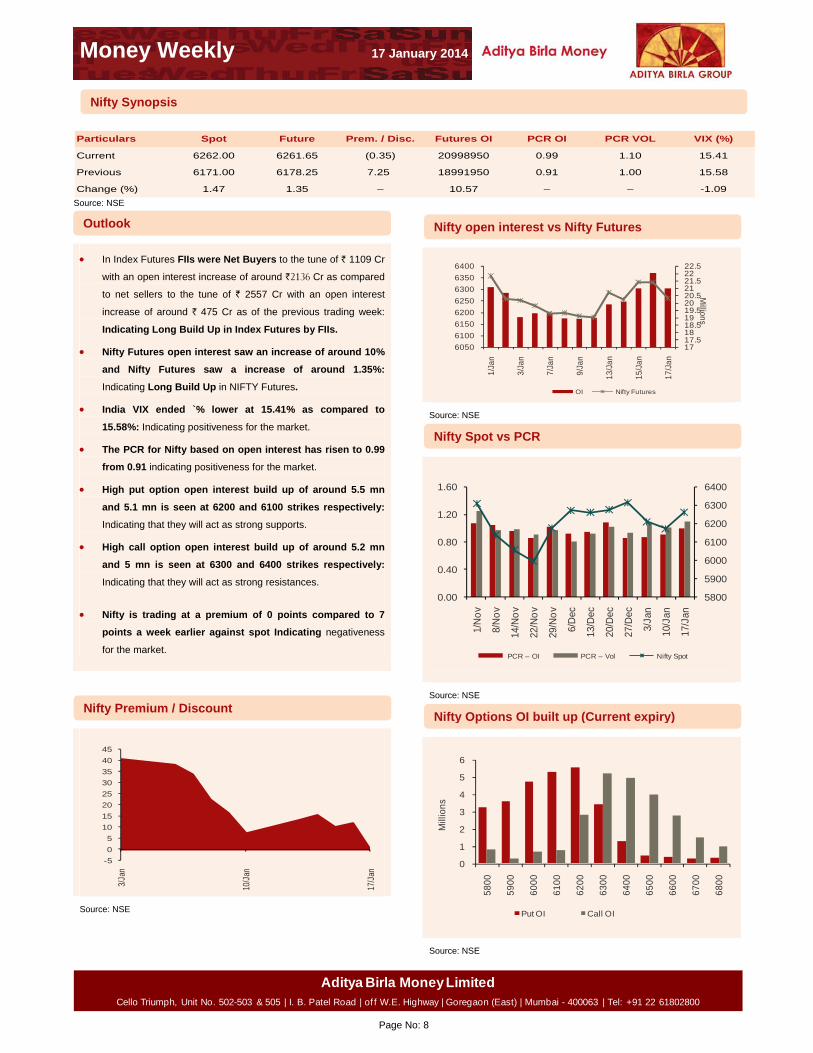

Particulars Spot Future Prem. / Disc. Futures OI PCR OI PCR VOL VIX (%)

Current 6262.00 6261.65 (0.35) 20998950 0.99 1.10 15.41

Previous 6171.00 6178.25 7.25 18991950 0.91 1.00 15.58

Change (%) 1.47 1.35 – 10.57 – – -1.09

Source: NSE

In Index Futures FIIs were Net Buyers to the tune of ` 1109 Cr

with an open interest increase of around `2136 Cr as compared

to net sellers to the tune of ` 2557 Cr with an open interest

increase of around ` 475 Cr as of the previous trading week:

Indicating Long Build Up in Index Futures by FIIs.

Nifty Futures open interest saw an increase of around 10%

and Nifty Futures saw a increase of around 1.35%:

Indicating Long Build Up in NIFTY Futures.

India VIX ended `% lower at 15.41% as compared to

15.58%: Indicating positiveness for the market.

The PCR for Nifty based on open interest has risen to 0.99

from 0.91 indicating positiveness for the market.

High put option open interest build up of around 5.5 mn

and 5.1 mn is seen at 6200 and 6100 strikes respectively:

Indicating that they will act as strong supports.

High call option open interest build up of around 5.2 mn

and 5 mn is seen at 6300 and 6400 strikes respectively:

Indicating that they will act as strong resistances.

Nifty is trading at a premium of 0 points compared to 7

points a week earlier against spot Indicating negativeness

for the market.

-5

0

5

10

15

20

25

30

35

40

45

3/Ja

n

10/J

an

17/J

an

Source: NSE

1717.51818.51919.52020.52121.52222.5

6050

6100

6150

6200

6250

6300

6350

6400

1/Ja

n

3/Ja

n

7/Ja

n

9/Ja

n

13/J

an

15/J

an

17/J

an

Millions

OI Nifty Futures

Source: NSE

5800

5900

6000

6100

6200

6300

6400

0.00

0.40

0.80

1.20

1.601/

No

v

8/N

ov

14/N

ov

22/N

ov

29/N

ov

6/D

ec

13/D

ec

20/D

ec

27/D

ec

3/Ja

n

10/J

an

17/J

an

PCR – OI PCR – Vol Nifty Spot

Source: NSE

0

1

2

3

4

5

6

5800

5900

6000

6100

6200

6300

6400

6500

6600

6700

6800

Mill

ions

Put OI Call OI

Source: NSE

Nifty Premium / Discount Nifty Options OI built up (Current expiry)

Nifty Spot vs PCR

Nifty open interest vs Nifty Futures Outlook

Nifty Synopsis

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 9

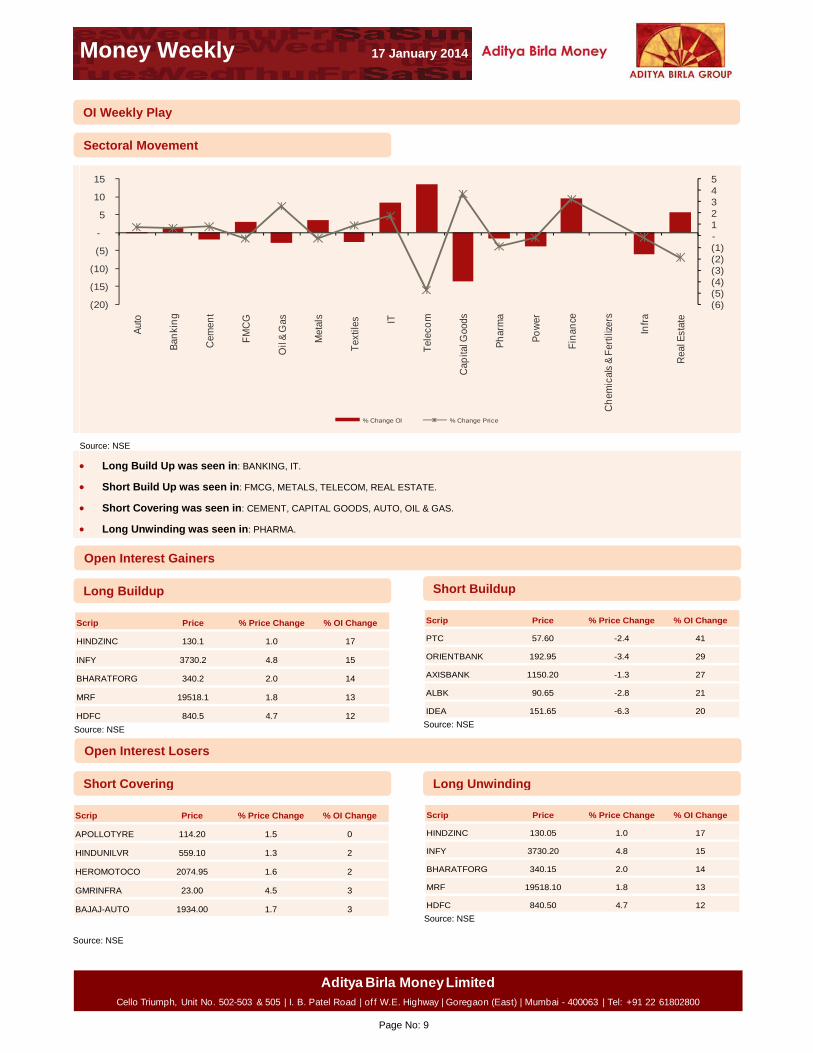

(6)(5)(4)(3)(2)(1)-1 2 3 4 5

(20)

(15)

(10)

(5)

-

5

10

15

Aut

o

Ban

kin

g

Cem

ent

FM

CG

Oil

& G

as

Met

als

Tex

tiles

IT

Tel

eco

m

Cap

ital G

oods

Ph

arm

a

Po

wer

Fin

ance

Ch

emic

als

& F

ertil

izer

s

Infr

a

Rea

l Est

ate

% Change OI % Change Price

Source: NSE

Long Build Up was seen in: BANKING, IT.

Short Build Up was seen in: FMCG, METALS, TELECOM, REAL ESTATE.

Short Covering was seen in: CEMENT, CAPITAL GOODS, AUTO, OIL & GAS.

Long Unwinding was seen in: PHARMA.

Scrip Price % Price Change % OI Change

HINDZINC 130.1 1.0 17

INFY 3730.2 4.8 15

BHARATFORG 340.2 2.0 14

MRF 19518.1 1.8 13

HDFC 840.5 4.7 12

Source: NSE

Scrip Price % Price Change % OI Change

PTC 57.60 -2.4 41

ORIENTBANK 192.95 -3.4 29

AXISBANK 1150.20 -1.3 27

ALBK 90.65 -2.8 21

IDEA 151.65 -6.3 20

Source: NSE

Scrip Price % Price Change % OI Change

APOLLOTYRE 114.20 1.5 0

HINDUNILVR 559.10 1.3 2

HEROMOTOCO 2074.95 1.6 2

GMRINFRA 23.00 4.5 3

BAJAJ-AUTO 1934.00 1.7 3

Source: NSE

Scrip Price % Price Change % OI Change

HINDZINC 130.05 1.0 17

INFY 3730.20 4.8 15

BHARATFORG 340.15 2.0 14

MRF 19518.10 1.8 13

HDFC 840.50 4.7 12

Source: NSE

OI Weekly Play

Long Unwinding

Open Interest Gainers

Open Interest Losers

Short Covering

Short BuildupLong Buildup

Sectoral Movement

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 10

Result season kicked off to a decent start with most of the companies reporting results in line with the analyst estimates. CPI and

WPI pleasantly surprised on the positive side with both falling more than expected on back of softening food inflation. However the

week was volatile with the markets gyrating wildly. Nifty closed 90 points higher.

Next week becomes important as lot of data is due from the global markets. Eurozone comes out with Consumer Confidence

report. BoJ announces it’s Monetary Policy statement and Industrial Production is due from Japan. Market awaits Chinese

economic data including factory output and investment growth which are expected to have slowed indicating world’s 2nd largest

economy is slowing. While US and Japan move into the thick of the result season, back home Asian Paints, Ultratech, Colgate,

HDFC, L& T and Cairn are some of the companies slated to announce the quarterly results.

Economy Monday 20 Jan Tuesday 21 Jan Wednesday 22 Jan Thursday 23 Jan Friday 24 Jan

Domestic

Global Japan: Industrial

Production MoM Nov F

(Prior 0.10%)

Industrial Production

YoY Nov F (Prior

5.00%)

Machine Tool Orders

YoY Dec F (Prior

28.00%)

China: GDP YoY 4Q

(Exp 7.60%, Prior

7.80%)

GDP SA QoQ 4Q (Exp

2.00%, Prior 2.20%).

Industrial Production

YoY Dec GDP YoY 4Q

(Exp 9.80%, Prior

10.00%)

HongKong: CPI

Composite YoY Dec (Exp

4.30%, Prior 4.30%)

US: MBA Mortgage

Applications 17-Jan

(Prior 11.90%)

UK: Jobless Claims

Change Dec (Exp -

34.0K, Prior -36.7K)

Bank of England

Minutes

US: Initial Jobless Claims

18-Jan (Exp 332K, Prior

326K)

Continuing Claims 11-Jan

(Prior 3030K)

China: HSBC/Markit

Flash Mfg PMI Jan (Exp

50.5, Prior 50.5)

EURO: ECB Current

Account SA Nov (Prior

21.8B)

PMI Manufacturing Jan A

(Exp 53.0, Prior 52.7)

Consumer Confidence

Jan A (Exp -13, Prior -

13.6)

Brazil: FGV Consumer

Confidence Jan (Prior

111.5)

Source: Bloomberg

Event Calendar

Outlook

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 11

Research Team

Vivek Mahajan Hemant Thukral

Head of Research Head – Derivatives Desk

022-61802820 022-61802870

[email protected] [email protected]

Fundamental Team Sunny Agrawal FMCG/Cement/Mid Caps 022-61802831 [email protected]

Shreyans Mehta Construction/Real Estate 022-61802829 [email protected]

Pradeep Parkar Database Analyst 022-61802839 [email protected]

Quantitative Team Sudeep Shah Technical Analyst 022-61802837 [email protected]

Advisory Support Suresh Gardas Advisory Desk 022-61802835 [email protected]

Mohan Jaiswal Executive – Research Support 022-61802838 [email protected]

ABML research is also accessible in Bloomberg at ABMR

Money Weekly 17 January 2014

Aditya Birla Money LimitedCello Triumph, Unit No. 502-503 & 505 | I. B. Patel Road | of f W.E. Highway | Goregaon (East) | Mumbai - 400063 | Tel: +91 22 61802800

Page No: 12

Disclaimer:

This document is not for public distribution and is meant solely for the personal information of the authorised recipient. No part of the information must be altered, transmitted, copied, distributed or reproduced in any form to any other person. Persons into whose possession this document may come are required to observe these restrictions. This document is for general information purposes only and does not constitute an investment advice or an offer to sell or solicitation of an offer to buy / sell any security and is not intended for distribution in countries where distribution of such material is subject to any licensing, registration or other legal requirements. The information, opinion, views contained in this document are as per prevailing conditions and are of the date of appearing on this material only and are subject to change. No reliance may be placed for any purpose whatsoever on the information contained in this document or on its completeness. Neither Aditya Birla Money Limited (ABML) nor any person connected with it accepts any liability or loss arising from the use of this document. The views and opinions expressed herein by the author in the document are his own and do not reflect the views of Aditya Birla Money Limited or any of its associate or group companies. The information set out herein may be subject to updating, completion, revision, verification and amendment and such information may change materially. Past performance is no guarantee and does not indicate or guide to future performance. Nothing in this document is intended to constitute legal, tax or investment advice, or an opinion regarding the appropriateness of any investment, or a solicitation of any type. The contents in this document are intended for general information purposes only. This document or information mentioned therefore should not form the basis of and should not be relied upon in connection with making any investment. The investment may not be suited to all the categories of investors. The recipients should therefore obtain your own professional, legal, tax and financial advice and assessment of their risk profile and financial condition before considering any decision. Aditya Birla Money Limited, its associate and group companies, its directors, associates, employees from time to time may have various interests / positions in any of the securities of the Company(ies) mentioned therein or be engaged in any other transactions involving such securities or otherwise in other securities of the companies / organisation mentioned in the document or may have other potential conflict of interest with respect of any recommendation and / related information and opinions.