moneymarketrkp.doc

DESCRIPTION

1TRANSCRIPT

MONEY MARKET:

CLASS NOTE For

PGDM/MMS, Simsr, Mumbai

Prof. Dr. R.K.Pattnaik

Learning Objective

To explain the concepts, operations and policy implications.

The emphasis is on Indian perspectives

Subjects to be covered

Meaning and importance of money market Monetary base and Money supplyProcedure of monetary policyTransmission MechanismInstrumentsParticipantsEvolutionIssues

Emphasis on call money market, CBLO and market RepoCommercial Paper and Certificate of Deposits

Critical evaluation of LAF

Empirical analysis with help of market data.

Monetary Policy Framework

Objectives

Twin objectives of “maintaining price stability” and “ensuring availability of adequate credit to productive sectors of the economy to support growth” continue to govern the stance of monetary policy, though the relative emphasis on these objectives has varied depending on the importance of maintaining an appropriate balance.

Reflecting the increasing development of financial market and greater liberalisation, use of broad money as an intermediate target has been de-emphasised and a multiple indicator approach has been adopted. Emphasis has been put on development of multiple instruments to transmit liquidity and interest rate signals in the short-term in a flexible and bi-directional manner. Increase of the interlink age between various segments of the financial market including money, government security and forex markets.

Instruments

Move from direct instruments (such as, administered interest rates, reserve requirements, selective credit control) to indirect instruments (such as, open market operations, purchase and repurchase of government securities) for the conduct of monetary policy.

Introduction of Liquidity Adjustment Facility (LAF), which operates through repo and reverse repo auctions, effectively provide a corridor for short-term interest rate. LAF has emerged as the tool for both liquidity management and also as a signaling devise for interstate in the overnight market. Use of open market operations to deal with overall market liquidity situation especially those emanating from capital flows.

Introduction of Market Stabilization Scheme (MSS) as an additional instrument to deal with enduring capital inflows without affecting short-term liquidity management role of LAF.

Developmental Measures

Discontinuation of automatic monetisation through an agreement between the Governmentand the Reserve Bank. Rationalisation of Treasury Bill market. Introduction of delivery versus payment system and deepening of inter-bank repo market. Introduction of Primary Dealers in the government securities market to play the role ofmarket maker. Amendment of Securities Contracts Regulation Act (SCRA), to create the regulatoryframework. Deepening of government securities market by making the interest rates on such securities market related. Introduction of auction of government securities. Development of a risk-free credible yield curve in the government securities market as a benchmark for related markets. Development of pure inter-bank call money market. Non-bank participants to participate inother money market

instruments. Introduction of automated screen-based trading in government securities through Negotiated Dealing System (NDS). Setting up of risk-free payments and system in government securities through Clearing Corporation of India Limited (CCIL). Phased introduction of Real Time Gross Settlement (RTGS) System. Deepening of forex market and increased autonomy of Authorised Dealers.

Institutional Measures

Setting up of Technical Advisory Committee on Monetary Policy with outside experts to review macroeconomic and monetary developments and advise the Reserve Bank on the stance of monetary policy. Creation of a separate Financial Market Department within the RBI.

Base Money and Broad Money_ M0 and M3

Difference between Monetary Management ( Monetary targeting through elasticity of demand for money, output growth and Inflation) and Liquidity management( Transmission of monetary policy to real sector through policy rate changes, {repo } following multiple indicator approach

Money Market Instruments for Liquidity Management

The Reserve Bank has been making efforts to develop a repo market outside the LAF for bank and non bank participants, so as to provide a stable collateralised funding alternative with a view to promoting smooth transformation of the call/notice money market into a pure inter-bank market and for deepening the underlying Government securities market. Thus, the following new instruments have been introduced.

CALL/NOTICE MONEY MARKET OPERATIONS IN INDIA

The money market is a market for short-term financial assets that are close substitutes of money. The most important feature of a money market instrument is that it is liquid and can be turned over quickly at low cost and provides an avenue for equilibrating the short-term surplus funds of lenders and the requirements of borrowers. The call/notice money market forms an important segment of the Indian money market. Under call money market, funds are transacted on overnight basis and under notice money market, funds are transacted for the period between 2 days and 14 days.

Banks borrow in this money market for the following propose. • To fill the gaps or temporary mismatches in funds • To meet the CRR & SLR Mandatory requirements as stipulated by the Central bank • To meet sudden demand for funds arising out of large outflows Thus call money usually serves the role of equilibrating the short-term liquidity position of banks

Participants

Participants in call/notice money market currently include banks, Primary Dealers (PDs), development finance institutions, insurance companies and select mutual funds. Of these, banks and PDs can operate both as borrowers and lenders in the market. But non-bank institutions (such as all-India FIs, select Insurance Companies or Mutual Funds), which have been given specific permission to operate in call/notice money market can, however, operate as lenders only. No new non-bank institutions are permitted to operate (i.e., lend) in the call/notice money market with effect from May 5, 2001. In case any eligible institution has genuine difficulty in deploying its excess liquidity, RBI may consider providing temporary permission to lend a higher amount in call/notice money market for a specific period on a case-by-case basis. Effective from Aug 06, 2005 non-bank participants except Primary Dealers are to discontinue participate, to make the call money market pure inter-bank market. Prudential norms of RBI Lending of scheduled commercial banks, on a fortnightly average basis, should not exceed 25 per cent of their capital fund. However, banks are allowed to lend a maximum of 50% on any day, during a fortnight. Borrowings by scheduled commercial banks should not exceed 100 per cent of their capital fund or 2 per cent of aggregate deposits, whichever is higher. However, banks are allowed to borrow a maximum of 125 per cent of their capital fund on any day, during a fortnight. Interest Rate Eligible participants are free to decide on interest rates in call/notice money market.

Collateralised Borrowing and Lending Obligation (CBLO)

Developed by the Clearing Corporation of India Limited (CCIL) and introduced on January 20, 2003, it is a

discounted instrument available in electronic book entry form for the maturity period ranging from one day to ninety

days (can be made available up to one year as per RBI guidelines).

In order to enable the market participants to borrow and lend funds, CCIL provides the Dealing System through Indian

Financial Network (INFINET), a closed user group to the Members of the Negotiated Dealing System (NDS) who

maintain Current account with RBI and through Internet for other entities who do not maintain Current account with

RBI.

Membership (including Associate Membership) of CBLO segment is extended to banks, financial institutions,

insurance companies, mutual funds, primary dealers, NBFCs, non-Government Provident Funds, Corporates, etc.

Eligible securities are Central Government securities including Treasury Bills. Borrowing limits for members is fixed

by CCIL at the beginning of the day taking into account the securities deposited by borrowers in their CSGL account

with CCIL. The securities are subjected to necessary hair-cut after marking them to market.

Auction market is available only to NDS Members for overnight borrowing and settlement on T+0 basis. At the end of

the Auction market session, CCIL initiates auction matching process based on Uniform Yield principle. CCIL assumes

the role of the central counter party through the process of innovation and guarantees settlement of transactions in

CBLO.

Automated value-free transfer of securities between market participants and the CCIL was introduced during 2004-05.

Members can reckon unencumbered securities for SLR calculations. The operations in CBLO are exempted from cash

reserve requirement (CRR).

Market Repo

To broaden the repo market, the Reserve Bank enabled non-banking financial companies, mutual funds, housing

finance companies and insurance companies not holding SGL accounts to undertake repo transactions with effect from

March 3, 2003. These entities were permitted to access the repo market through their ‘gilt accounts’ maintained with

the custodians. Subsequently, non-scheduled urban co-operative banks and listed companies with gilt accounts with

scheduled commercial banks were allowed to participate. Necessary precautions were built into the system to ensure

‘delivery versus payment’ (DvP) and transparency, while restricting the repos to Government securities only. Rollover

of repo transactions in Government securities was facilitated with the enabling of DvPIII mode of settlement in

Government securities which involves settlement of securities and fundson a net basis, effective April 2, 2004. This

provided significant flexibility to market participantsin managing their collateral. CBLO and market repo helped in

aligning short-term money market rates to the LAF corridor. Mutual funds and insurance companies are generally the

main supplier of funds while banks, primary dealers and corporates are the major borrowers in the repo market

outside the LAF.

Liquidity Adjustment Facility

As part of the financial sector reforms launched in mid-1991, India began to move away from direct instruments of

monetary control to indirect ones. The transition of this kind involves considerable efforts to develop markets,

institutions and practices. In order to facilitate such transition, India developed a Liquidity Adjustment Facility (LAF)

in phases considering country-specific features of the Indian financial system. LAF is based on repo / reverse repo

operations by the central bank.

In 1998 the Committee on Banking Sector Reforms (Narasimham Committee II) recommended the introduction of a

Liquidity Adjustment Facility (LAF) under which the Reserve Bank would conduct auctions periodically, if not

necessarily daily. The Reserve Bank could reset its Repo and Reverse Reports which would in a sense provide a

reasonable corridor for the call money market. In pursuance of these recommendations, a major change in the

operating procedure became possible in April 1999through the introduction of an Interim Liquidity Adjustment

Facility (ILAF) under which repos and reverse repos were formalised. With the introduction of ILAF, the general

refinance facility was withdrawn and replaced by a collateralised lending facility (CLF) up to 0.25 per cent of the

fortnightly average outstanding of aggregate deposits in 1997-98 for two weeks at the Bank Rate.

Additional collateralised lending facility (ACLF) for an equivalent amount of CLF was made available at the Bank

Rate plus 2 per cent. CLF and ACLF availed for periods beyond two weeks were subjected to a penal rate of 2 per cent

for an additional two week period. Export Credit refinance for scheduled commercial banks was retained and

continued to be provided at the bank rate. Liquidity support to PDs against collateral of government securities at the

bank rate was also provided for. ILAF was expected to promote stability of money market and ensure that the interest

rates move within a reasonable range.

The transition from ILAF to a full-fledged LAF began in June 2000 and was undertaken in three stages. In the first

stage beginning June 5, 2000, LAF was formally introduced and the Additional CLF andlevel II support to PDs was

replaced by variable rate repo auctions with same day settlement. In the second stage, beginning May 2001 CLF and

level I liquidity support for banks and PDs was also replaced by variable rate repo auctions. Some minimum liquidity

support to PDs was continued but at interest rate linked to variable rate in the daily repos auctions as determined by

RBI from time to time. In April 2003, the multiplicity of rates at which liquidity was being absorbed/injected under

back-stop facility was rationalised and the back-stop interest rate was fixed at the reverse repo cut-off rate at the

regular LAF auctions on that day. In case of no reverse repo in the LAF auctions, back-stop rate was fixed at 2.0

percentage point above the repo cut-off rate. It was also announced that on days when no repo/reverse repo bids are

received/accepted, back-stop rate would be decided by the Reserve Bank on an ad-hoc basis.

A revised LAF scheme was operationalised effective March 29, 2004 under which the reverse repo rate was reduced to

6.0 per cent and aligned with bank rate. Normal facility and backstop facility was merged into a single facility and

made available at a single rate. The third stage of full fledged LAF had begun with the full computerisation of Public

Debt Office (PDO) and introduction of RTGS marked a big step forward in this phase. Repo operations today are

mainly through electronic transfers. Fixed rate auctions have been reintroduced since April 2004. The possibility of

operating at different times of the same day is now close to getting materialised. In that sense we have very nearly

completed the transition to operating a full-fledged LAF.

With the introduction of Second LAF (SLAF) from November 28, 2005 market participants now have a second window

to fine-tune the management of liquidity. In past, LAF operations were conducted in the forenoon between 9.30 a.m.

and 10.30 a.m. SLAF is conducted by receiving bids between 3.00 p.m. and3.45 p.m. The salient features of SLAF are

the same as those of LAF and the settlement for both is conducted separately and on gross basis. The introduction of

LAF has been a process and the Indian experience shows that phased rather than a big bang approach is required for

reforms in the financial sector and in monetary management.

Based on the recommendations of the Working Group on Operating Procedures of

Monetary Policy (Chairman: Shri DeepakMohanty), the Reserve Bank in its Monetary

Policy Statement for 2011-12 effected the following changes to the operating procedure

of monetary policy: (i) the weighted average overnight call money rate has become the

operating target of monetary policy; (ii) the repo rate has become the only independently

varying policy rate; (iii) the reverse repo rate, pegged at 100 bps below the repo rate,

provides the lower bound to the corridor of overnight interest rate and (iv) a new

Marginal Standing Facility (MSF) has been instituted at 100 bps above the repo rate that

provides the upper bound to the corridor. Banks can borrow overnight from the MSF up

to one per cent of their respective net demand and time liabilities (NDTL). The new

operating procedure became operational in May 2011 Based

COMMERCIAL PAPER

Features

Commercial Paper (CP) is an unsecured money market instrument issued in the form of a promissory note. It was introduced in India in 1990 with a view to enabling highly rated corporate borrowers/ to diversify their sources of short-term borrowings and to provide an additional instrument to investors.

CP can be issued for maturities between a minimum of 15 days and a maximum up to

one year from the date of issue. CP can be issued in denominations of Rs.5 lakh or multiples

thereof. CP can be issued in denominations of Rs.5 lakh or multiples thereof.

CP can be issued either in the form of a promissory note (Schedule I) or in a dematerialised

form through any of the depositories approved by and registered with SEBI. Banks, FIs, PDs

and SDs are directed to hold CP only in dematerialised form.

CP will be issued at a discount to face value as may be determined by the issuer. CP will be

issued at a discount to face value as may be determined by the issuer. No issuer shall have the

issue of Commercial Paper underwritten or co-accepted No issuer shall have the issue of

Commercial Paper underwritten or co-accepted

CP being a `stand alone’ product, it would not be obligatory in any manner on the part of banks and FIs to provide stand-by facility to the issuers of CP.

Eligibility to Issue CP

Corporates, primary dealers (PDs) and the All-India Financial Institutions (FIs) are eligible to

issue CP.

. A corporate would be eligible to issue CP provided –

a. the tangible net worth of the company, as per the latest audited balance sheet, is not less than Rs. 4 crore

b. company has been sanctioned working capital limit by bank/s or all-India financial institution/s; and

c. the borrowal account of the company is classified as a Standard Asset by the financing bank/s/ institution/s.

Credit Ratings

All eligible participants shall obtain the credit rating for issuance of Commercial Paper either

from Credit Rating Information Services of India Ltd. (CRISIL) or the Investment Information

and Credit Rating Agency of India Ltd. (ICRA) or the Credit Analysis and Research Ltd. (CARE)

or the FITCH Ratings India Pvt. Ltd. or such other credit rating agency (CRA) as may be

specified by the Reserve Bank of India from time to time, for the purpose.

The minimum credit rating shall be P-2 of CRISIL or such equivalent rating by other agencies

The issuers shall ensure at the time of issuance of CP that the rating so obtained is current and has not fallen due for review and the maturity date of the CP should not go beyond the date up to which the credit rating of the issuer is valid.

LIMITS

The aggregate amount of CP from an issuer shall be within the limit as approved by its Board of Directors or the quantum indicated by the Credit Rating Agency for the specified rating, whichever is lower.

As regards FIs, they can issue CP within the overall umbrella limit fixed by the RBI i.e., issue of CP together with other instruments viz., term money borrowings, term deposits, certificates of deposit and inter-corporate deposits should not exceed 100 per cent of its net owned funds, as per the latest audited balance sheet.

Individuals, banking companies, other corporate bodies registered or incorporated in India and unincorporated bodies, Non-Resident Indians (NRIs) and Foreign Institutional Investors (FIIs) etc. can invest in CPs. However, amount invested by single investor should not be less than Rs.5 lakh (face value).

However, investment by FIIs would be within the limits set for their investments by Securities

and Exchange Board of India (SEBI.

Guarantee for credit Enhancement

Non-bank entities including corporates can provide unconditional and irrevocable guarantee for credit enhancement for CP issue provided :

a. the issuer fulfils the eligibility criteria prescribed for issuance of CP;

b. the guarantor has a credit rating at least one notch higher than the issuer by an approved credit rating agency and

c. the offer document for CP properly discloses: the net worth of the guarantor company, the names of the companies to which the guarantor has issued similar guarantees, the extent of the guarantees offered by the guarantor company, and the conditions under which the guarantee will be invoked.

Role and responsibilities of the Issuer/Issuing and Paying Agent and Credit Rating Agency

Issuer:

a. Every issuer must appoint an IPA for issuance of CP.

b. The issuer should disclose to the potential investors its financial position as per the standard market practice.

c. After the exchange of deal confirmation between the investor and the issuer, issuing company shall issue physical certificates to the investor or arrange for crediting the CP to the investor's account with a depository.

Investors shall be given a copy of IPA certificate to the effect that the issuer has a valid agreement with the IPA and documents are in order (Schedule III).

Issuing and Paying Agent

a. IPA would ensure that issuer has the minimum credit rating as stipulated by the RBI and amount mobilised through issuance of CP is within the quantum indicated by CRA for the specified rating.

b. IPA has to verify all the documents submitted by the issuer viz., copy of board resolution, signatures of authorised executants (when CP in physical form) and issue a certificate that documents are in order. It should also certify that it has a valid agreement with the issuer (Schedule III).

c. Certified copies of original documents verified by the IPA should be held in the custody of IPA.

Credit Rating Agency

a. Code of Conduct prescribed by the SEBI for CRAs for undertaking rating of capital market instruments shall be applicable to them (CRAs) for rating CP.

b. Further, the credit rating agency have the discretion to determine the validity period of the rating depending upon its perception about the strength of the issuer. Accordingly, CRA shall at the time of rating, clearly indicate the date when the rating is due for review.

c. While the CRAs can decide the validity period of credit rating, CRAs would have to closely monitor the rating assigned to issuers vis-a-vis their track record at regular intervals and would be required to make its revision in the ratings public through its publications and website

.

Certificate of Deposits

Certificates of Deposit (CDs) is a negotiable money market instrument and issued in

dematerialised form or as a Usance Promissory Note, for funds deposited at a bank

or other eligible financial institution for a specified time period.

Eligibility

CDs can be issued by (i) scheduled commercial banks excluding Regional

Rural Banks (RRBs) and Local Area Banks (LABs); and (ii) select all-India Financial

Institutions that have been permitted by RBI to raise short-term resources within the

umbrella limit fixed by RBI.

Aggregate Amount

Banks have the freedom to issue CDs depending on their requirements.

An FI may issue CDs within the overall umbrella limit fixed by RBI, i.e., issue

of CD together with other instruments, viz., term money, term deposits, commercial

papers and inter-corporate deposits should not exceed 100 per cent of its net owned

funds, as per the latest audited balance sheet.

Minimum Size of Issue and Denominations

Minimum amount of a CD should be Rs.1 lakh, i.e., the minimum deposit that

could be accepted from a single subscriber should not be less than Rs. 1 lakh and in

the multiples of Rs. 1 lakh thereafter.

Who can Subscribe

CDs can be issued to individuals, corporations, companies, trusts, funds,

associations, etc. Non-Resident Indians (NRIs) may also subscribe to CDs, but only

on non-repatriable basis which should be clearly stated on the Certificate. Such CDs

cannot be endorsed to another NRI in the secondary market.

Maturity

The maturity period of CDs issued by banks should be not less than 7 days

and not more than one year.

The FIs can issue CDs for a period not less than 1 year and not exceeding 3

years from the date of issue.

Discount/Coupon Rate CDs may be issued at a discount on face value. Banks/FIs are also allowed

to issue CDs on floating rate basis provided the methodology of compiling the

floating rate is objective, transparent and market-based. The issuing bank/FI is free

to determine the discount/coupon rate. The interest rate on floating rate CDs would

have to be reset periodically in accordance with a pre-determined formula that

indicates the spread over a transparent benchmark.

Reserve Requirements Banks have to maintain the appropriate reserve requirements, i.e., cash

reserve ratio (CRR) and statutory liquidity ratio (SLR), on the issue price of the CDs.

Transferability

Physical CDs are freely transferable by endorsement and delivery. Dematted

CDs can be transferred as per the procedure applicable to other demat securities.

There is no lock-in period for the CDs. Loans/Buy-backs. Banks/FIs cannot grant

loans against CDs. Furthermore, they cannot buybacktheir own CDs before maturity.

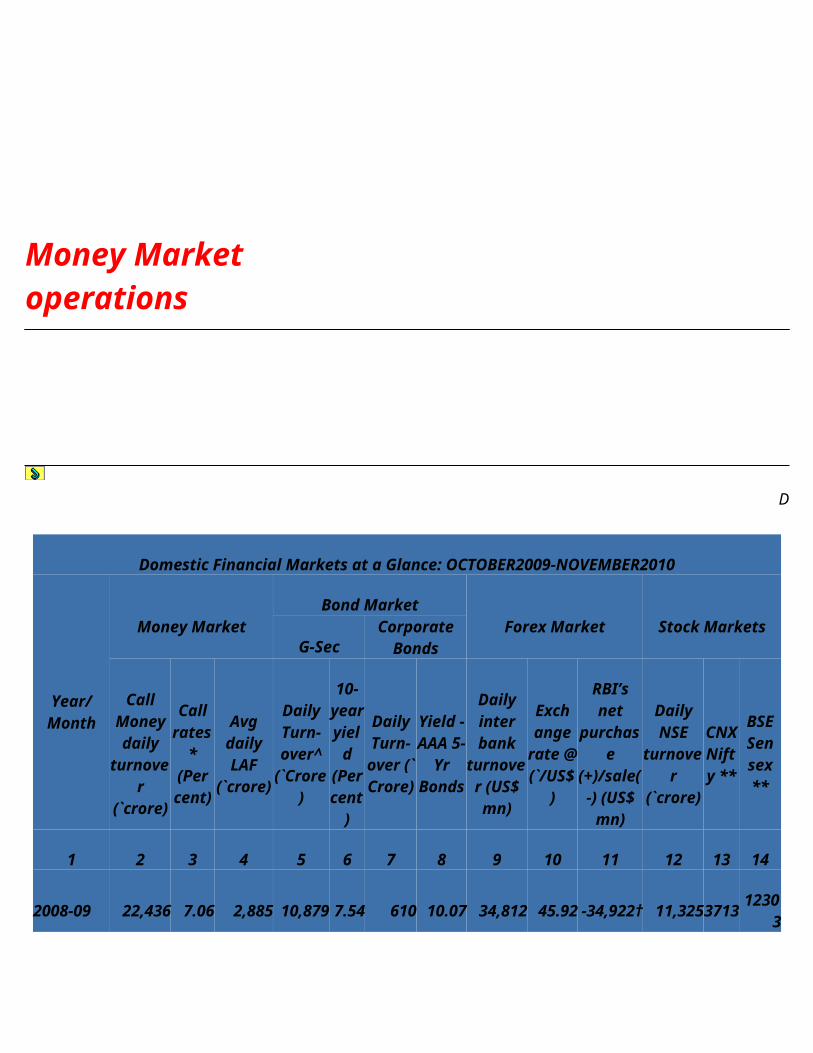

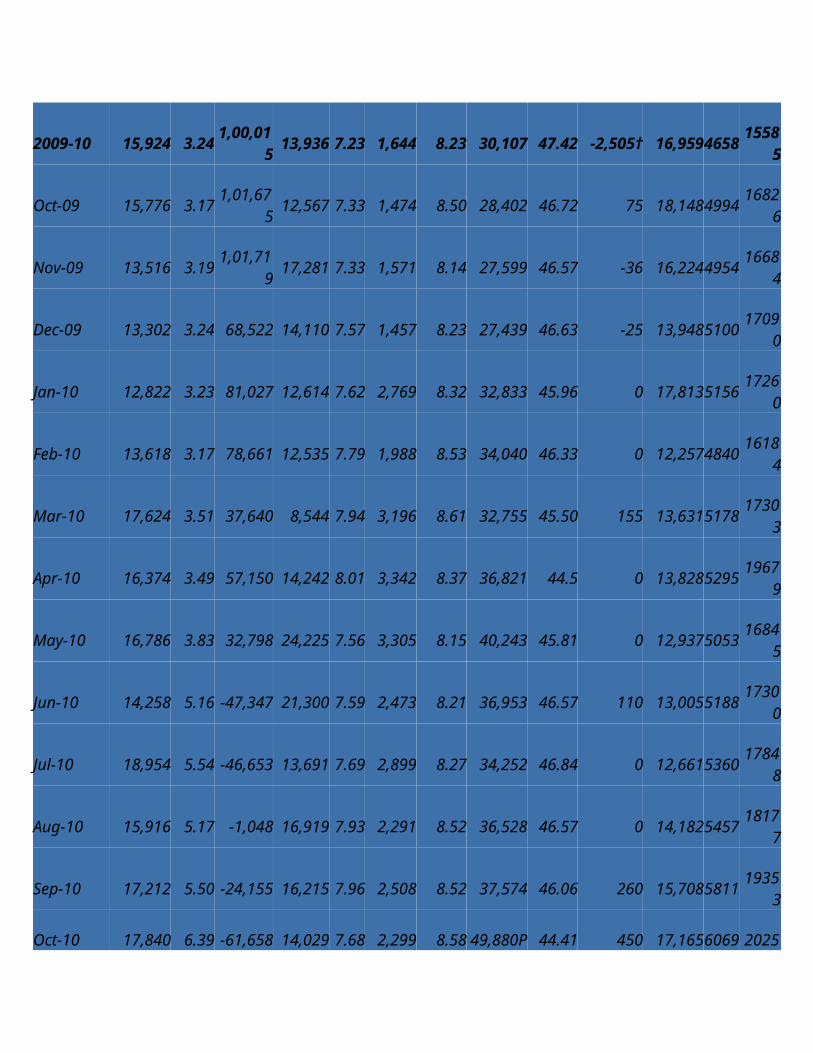

Money Market operations

D

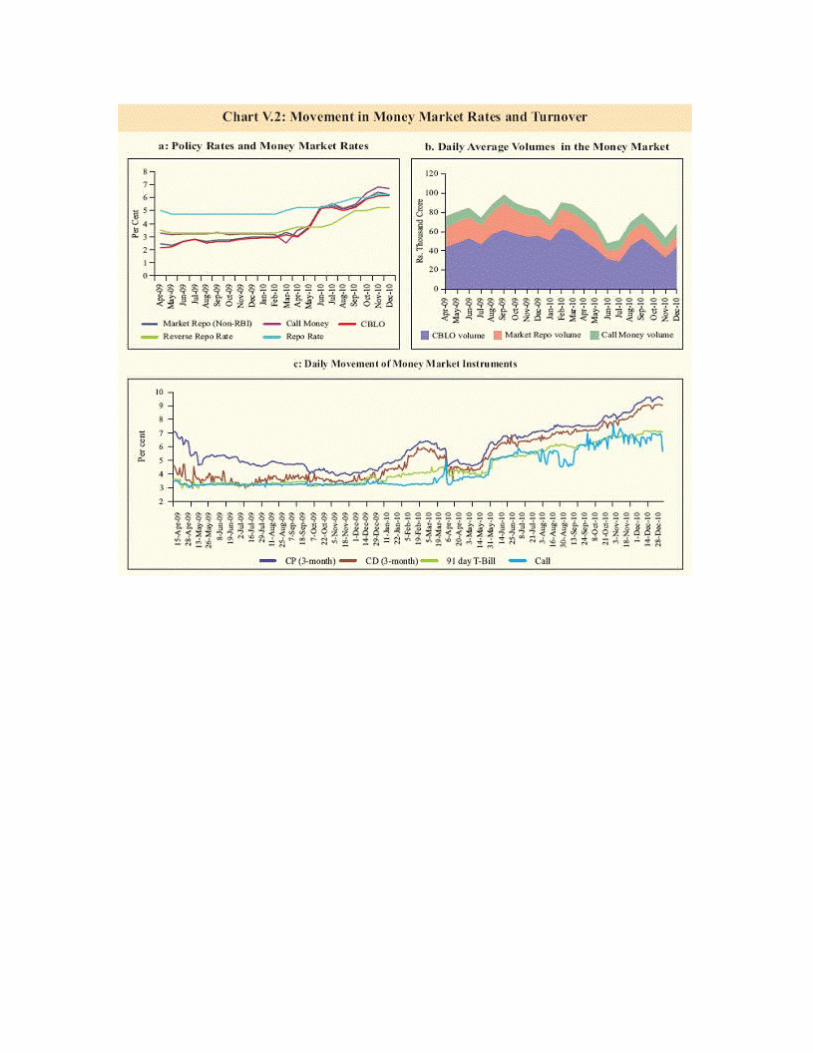

Domestic Financial Markets at a Glance: OCTOBER2009-NOVEMBER2010

Year/ Month

Money MarketBond Market

Forex Market Stock MarketsG-Sec

Corporate Bonds

Call Money daily

turnover (`crore)

Call rates* (Per cent)

Avg daily LAF

(`crore)

Daily Turn- over^

(`Crore)

10- year yield (Per cent)

Daily Turn- over (` Crore)

Yield - AAA 5-

Yr Bonds

Daily inter bank

turnover (US$ mn)

Exch ange

rate @ (`/US$)

RBI’s net purchase (+)/sale(-

) (US$ mn)

Daily NSE

turnover (`crore)

CNX Nifty

**

BSE Sen

sex **

1 2 3 4 5 6 7 8 9 10 11 12 13 14

2008-09 22,436 7.06 2,885 10,879 7.54 610 10.07 34,812 45.92 -34,922† 11,325 3713 12303

2009-10 15,924 3.24 1,00,015 13,936 7.23 1,644 8.23 30,107 47.42 -2,505† 16,959 4658 15585

Oct-09 15,776 3.17 1,01,675 12,567 7.33 1,474 8.50 28,402 46.72 75 18,148 4994 16826

Nov-09 13,516 3.19 1,01,719 17,281 7.33 1,571 8.14 27,599 46.57 -36 16,224 4954 16684

Dec-09 13,302 3.24 68,522 14,110 7.57 1,457 8.23 27,439 46.63 -25 13,948 5100 17090

Jan-10 12,822 3.23 81,027 12,614 7.62 2,769 8.32 32,833 45.96 0 17,813 5156 17260

Feb-10 13,618 3.17 78,661 12,535 7.79 1,988 8.53 34,040 46.33 0 12,257 4840 16184

Mar-10 17,624 3.51 37,640 8,544 7.94 3,196 8.61 32,755 45.50 155 13,631 5178 17303

Apr-10 16,374 3.49 57,150 14,242 8.01 3,342 8.37 36,821 44.5 0 13,828 5295 19679

May-10 16,786 3.83 32,798 24,225 7.56 3,305 8.15 40,243 45.81 0 12,937 5053 16845

Jun-10 14,258 5.16 -47,347 21,300 7.59 2,473 8.21 36,953 46.57 110 13,005 5188 17300

Jul-10 18,954 5.54 -46,653 13,691 7.69 2,899 8.27 34,252 46.84 0 12,661 5360 17848

Aug-10 15,916 5.17 -1,048 16,919 7.93 2,291 8.52 36,528 46.57 0 14,182 5457 18177

Sep-10 17,212 5.50 -24,155 16,215 7.96 2,508 8.52 37,574 46.06 260 15,708 5811 19353

Oct-10 17,840 6.39 -61,658 14,029 7.68 2,299 8.58 49,880P 44.41 450 17,165 6069 20250

Nov-10 17,730 6.81 -99,311 10,193 8.03 1,843 8.64 44,104P 45.02 870 17,333 6055 20126

Dec-10 18,872 6.67-

1,20,4959,849 8.03 1,723 8.89 34,894P 45.16

-13,440 5971 19228

* : Average of daily weighted call money rates. ^: Average of daily outright turnover in Central Government dated securities @: Average of closing rates. **: Average of daily closing indices. † : Cumulative for the financial year.NSE: National Stock Exchange of India Limited. P: Provisional - : Not available.Note : In col 4 (-)ve indicates injection of liquidity while (+)ve indicates absorption of liquidity.

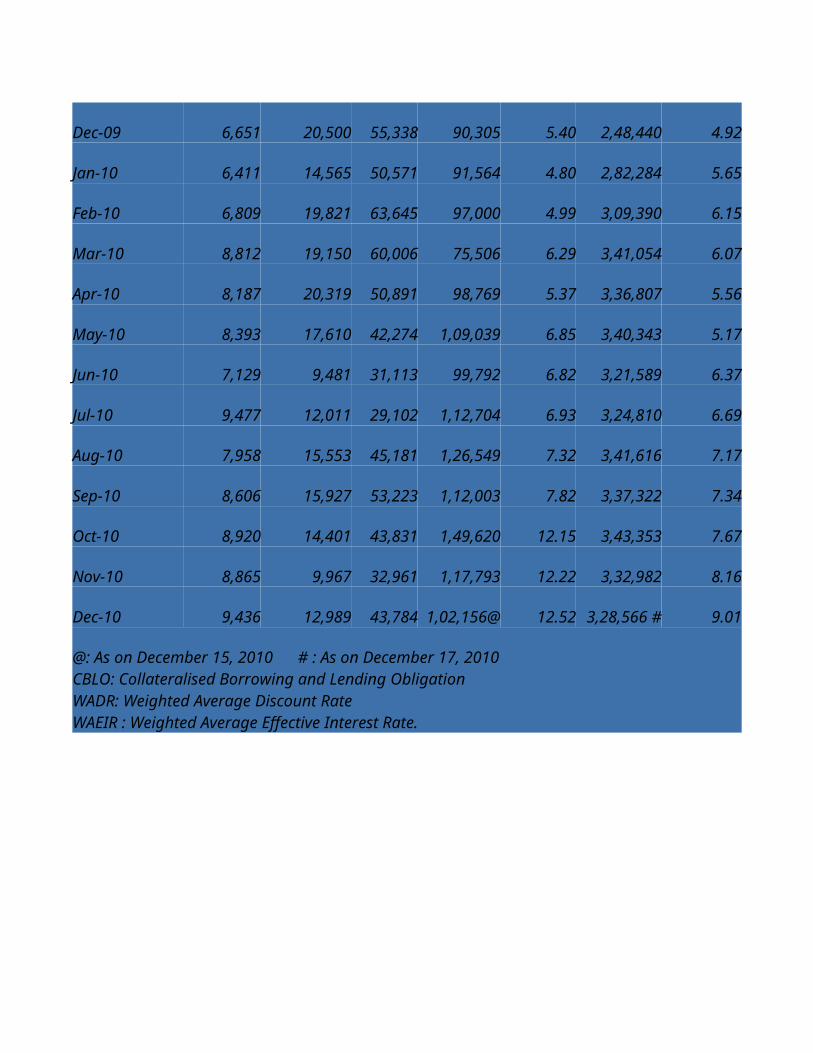

Activity in Money Market Segments: Sepetmber2009- December 2010

:(` Crore)

Year/Month

Average Daily Volume (One leg) Commercial Paper Certificates of Deposit

Call Money Market Repo CBLO OutstandingWADR (%) OutstandingWAEIR

(%)

1 2 3 4 5 6 7 8

Sep-09 8,059 27,978 62,388 79,228 5.04 2,16,691 5.30

Oct-09 7,888 23,444 58,313 98,835 5.06 2,27,227 4.70

Nov-09 6,758 22,529 54,875 1,03,915 5.17 2,45,101 4.86

Dec-09 6,651 20,500 55,338 90,305 5.40 2,48,440 4.92

Jan-10 6,411 14,565 50,571 91,564 4.80 2,82,284 5.65

Feb-10 6,809 19,821 63,645 97,000 4.99 3,09,390 6.15

Mar-10 8,812 19,150 60,006 75,506 6.29 3,41,054 6.07

Apr-10 8,187 20,319 50,891 98,769 5.37 3,36,807 5.56

May-10 8,393 17,610 42,274 1,09,039 6.85 3,40,343 5.17

Jun-10 7,129 9,481 31,113 99,792 6.82 3,21,589 6.37

Jul-10 9,477 12,011 29,102 1,12,704 6.93 3,24,810 6.69

Aug-10 7,958 15,553 45,181 1,26,549 7.32 3,41,616 7.17

Sep-10 8,606 15,927 53,223 1,12,003 7.82 3,37,322 7.34

Oct-10 8,920 14,401 43,831 1,49,620 12.15 3,43,353 7.67

Nov-10 8,865 9,967 32,961 1,17,793 12.22 3,32,982 8.16

Dec-10 9,436 12,989 43,784 1,02,156@ 12.52 3,28,566 # 9.01

@: As on December 15, 2010 # : As on December 17, 2010CBLO: Collateralised Borrowing and Lending ObligationWADR: Weighted Average Discount RateWAEIR : Weighted Average Effective Interest Rate.

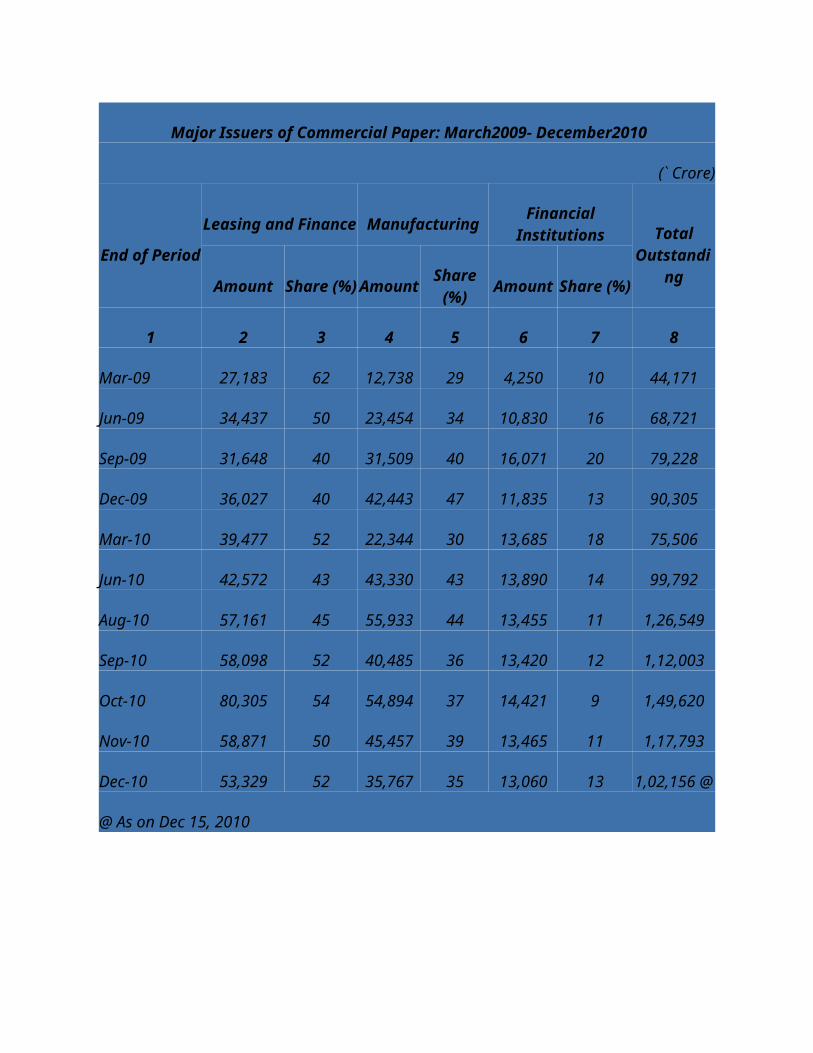

Major Issuers of Commercial Paper: March2009- December2010

(` Crore)

End of PeriodLeasing and Finance Manufacturing

Financial Institutions Total

OutstandingAmount Share (%) Amount Share (%) Amount Share (%)

1 2 3 4 5 6 7 8

Mar-09 27,183 62 12,738 29 4,250 10 44,171

Jun-09 34,437 50 23,454 34 10,830 16 68,721

Sep-09 31,648 40 31,509 40 16,071 20 79,228

Dec-09 36,027 40 42,443 47 11,835 13 90,305

Mar-10 39,477 52 22,344 30 13,685 18 75,506

Jun-10 42,572 43 43,330 43 13,890 14 99,792

Aug-10 57,161 45 55,933 44 13,455 11 1,26,549

Sep-10 58,098 52 40,485 36 13,420 12 1,12,003

Oct-10 80,305 54 54,894 37 14,421 9 1,49,620

Nov-10 58,871 50 45,457 39 13,465 11 1,17,793

Dec-10 53,329 52 35,767 35 13,060 13 1,02,156 @

@ As on Dec 15, 2010

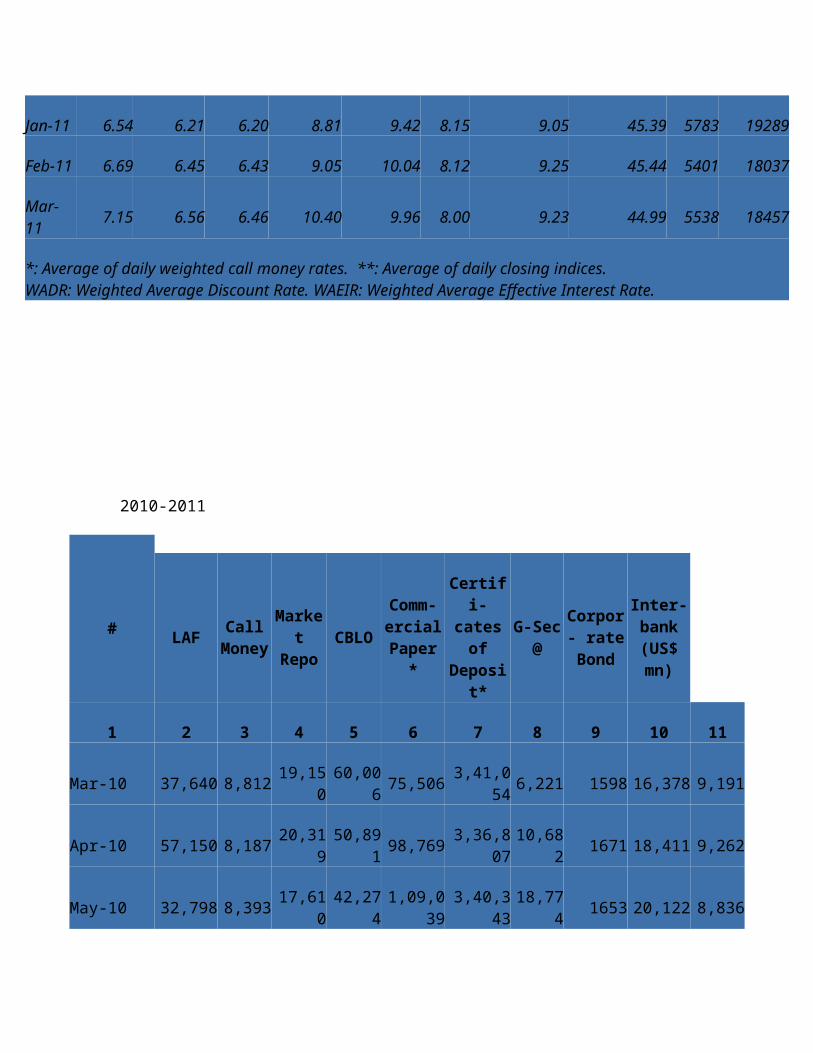

Table V.2 : Rates in Domestic Financial Markets

Money Market Bond Market Forex MarketStock Market

Indices

Call Rate* (Per cent)

Market Repo Rate

(Non-LAF) (Per

cent)

CBLO Rate (Per

cent)

Comm- ercial Paper WADR

(Per cent)

Certifi- cates of Deposit WAEIR

(Per cent)

G-Sec 10-year yield (Per cent)

Corporate Bonds Yield -

AAA 5-Yr bond (Per

cent)

Exchange Rate (`/US$)

CNX Nifty

**

BSE Sensex **

1 2 3 4 5 6 7 8 9 10 11

Mar-10 3.51 3.32 3.15 6.29 6.07 7.94 8.61 45.50 5178 17303

Apr-10 3.49 3.04 2.95 5.37 5.56 8.01 8.37 44.50 5295 19679

May-10 3.83 3.79 3.67 6.85 5.17 7.56 8.15 45.81 5053 16845

Jun-10 5.16 5.29 5.21 6.82 6.37 7.59 8.21 46.57 5188 17300

Jul-10 5.54 5.37 5.25 6.93 6.69 7.69 8.27 46.84 5360 17848

Aug-10 5.17 5.12 5.01 7.32 7.17 7.93 8.52 46.57 5457 18177

Sep-10 5.50 5.35 5.24 7.82 7.34 7.96 8.52 46.06 5811 19353

Oct-10 6.39 5.96 5.88 12.15 7.67 7.68 8.58 44.41 6069 20250

Nov-10 6.81 6.42 6.14 12.22 8.16 8.03 8.64 45.02 6055 20126

Dec-10 6.67 6.27 6.20 10.10 9.15 8.03 8.89 45.16 5971 19228

Jan-11 6.54 6.21 6.20 8.81 9.42 8.15 9.05 45.39 5783 19289

Feb-11 6.69 6.45 6.43 9.05 10.04 8.12 9.25 45.44 5401 18037

Mar-11 7.15 6.56 6.46 10.40 9.96 8.00 9.23 44.99 5538 18457

*: Average of daily weighted call money rates. **: Average of daily closing indices.WADR: Weighted Average Discount Rate. WAEIR: Weighted Average Effective Interest Rate.

2010-2011

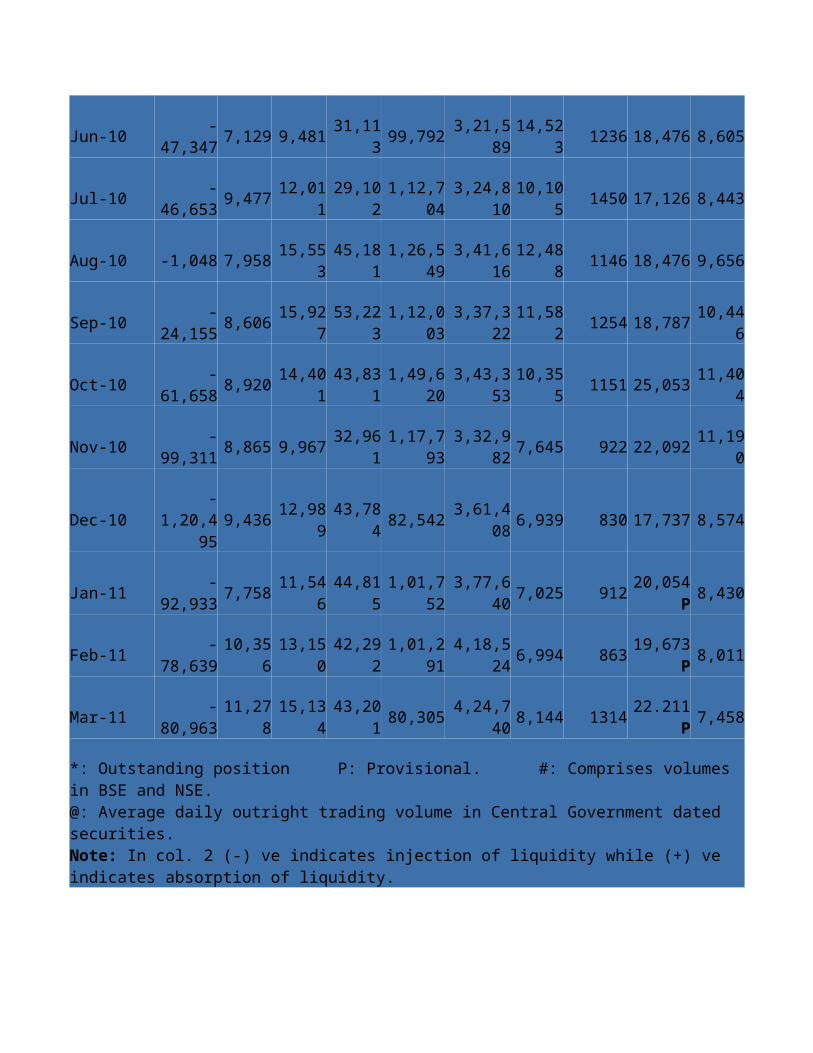

#LAF

Call Money

Market Repo

CBLOComm- ercial

Paper *

Certifi- cates of

Deposit*

G-Sec @

Corpor- rate

Bond

Inter-bank (US$ mn)

1 2 3 4 5 6 7 8 9 10 11

Mar-10 37,640 8,812 19,150 60,006 75,506 3,41,054 6,221 1598 16,378 9,191

Apr-10 57,150 8,187 20,319 50,891 98,769 3,36,807 10,682 1671 18,411 9,262

May-10 32,798 8,393 17,610 42,274 1,09,039 3,40,343 18,774 1653 20,122 8,836

Jun-10 -47,347 7,129 9,481 31,113 99,792 3,21,589 14,523 1236 18,476 8,605

Jul-10 -46,653 9,477 12,011 29,102 1,12,704 3,24,810 10,105 1450 17,126 8,443

Aug-10 -1,048 7,958 15,553 45,181 1,26,549 3,41,616 12,488 1146 18,476 9,656

Sep-10 -24,155 8,606 15,927 53,223 1,12,003 3,37,322 11,582 1254 18,787 10,446

Oct-10 -61,658 8,920 14,401 43,831 1,49,620 3,43,353 10,355 1151 25,053 11,404

Nov-10 -99,311 8,865 9,967 32,961 1,17,793 3,32,982 7,645 922 22,092 11,190

Dec-10 -1,20,495 9,436 12,989 43,784 82,542 3,61,408 6,939 830 17,737 8,574

Jan-11 -92,933 7,758 11,546 44,815 1,01,752 3,77,640 7,025 912 20,054 P 8,430

Feb-11 -78,639 10,356 13,150 42,292 1,01,291 4,18,524 6,994 863 19,673 P 8,011

Mar-11 -80,963 11,278 15,134 43,201 80,305 4,24,740 8,144 1314 22.211 P 7,458

*: Outstanding position P: Provisional. #: Comprises volumes in BSE and NSE.@: Average daily outright trading volume in Central Government dated securities.Note: In col. 2 (-) ve indicates injection of liquidity while (+) ve indicates absorption of liquidity.

Major Issuers of Commercial Paper: March 09-March11

(` crore)

End of Period

Leasing and Finance

ManufacturingFinancial

InstitutionsTotal

OutstandingAmount

Share (%)

AmountShare(%) Amount Share(%)

1 2 3 4 5 6 7 8

Mar-09 27,183 62 12,738 29 4,250 9 44,171

Jun-09 34,437 50 23,454 34 10,830 16 68,721

Sep-09 31,648 40 31,509 40 16,071 20 79,228

Dec-09 36,027 40 42,443 47 11,835 13 90,305

Mar-10 39,477 52 22,344 30 13,685 18 75,506

Jun-10 42,572 43 43330 43 13,890 14 99,792

Aug-10 57,161 45 55,933 44 13,455 11 1,26,549

Sep-10 58,098 52 40,485 36 13,420 12 1,12,003

Oct-10 80,306 54 54,894 37 14,420 9 1,49,620

Nov-10 58,871 50 45,457 39 13,465 11 1,17,793

Dec-10 49,282 60 24,960 30 8,300 10 82,542

Jan-11 55,591 55 35,601 35 10,560 10 1,01,752

Feb-11 51,339 51 40,262 39 9,690 10 1,01,291

Mar-11 46,350 58 22,695 28 11,260 14 80,305

2011-12(up to June)

Domestic Financial Markets at a Glance: March11-June11

Money Market Bond Market Forex Market

Stock Market Indices

Call Rate* (Per cent)

Market Repo Rate (Non-RBI)(Per cent)

CBLO Rate (Per cent)

Commercial Paper

WADR (Per cent)

Certificates of Deposit WAEIR

(Per cent)

G-Sec 10-year

yield@(Per cent)

Corporate Bonds Yield

AAA 5-Yr bond (Per

cent)

Exchange Rate@@ (`/US$)

CNX Nifty#

BSE Sensex#

1 2 3 4 5 6 7 8 9 10 11

Mar-10 3.51 3.32 3.15 6.29 6.07 7.94 8.61 45.50 5178 17303

Mar-11 7.15 6.56 6.46 10.40 9.96 8.00 9.23 44.99 5538 18457

Apr-11 6.58 5.55 5.63 8.62 8.66 8.05 9.25 44.37 5839 19450

May-11 7.15 7.05 6.94 9.49 9.30 8.31 9.48 44.90 5492 18325

Jun-11 7.38 7.30 7.06 10.15^ 9.61 8.28 9.63 44.85 5473 18229

*: Average of daily weighted call money borrowing rates. #: Average of daily closing indices. @: Average of daily FIMMDA closing rates. @@: Average of daily RBI reference rate. ^: As at mid-June 2011.WADR: Weighted Average Discount Rate. WAEIR: Weighted Average Effective Interest Rate.

Average Daily Volumes in Domestic Financial Markets : March11-June11

(` crore)

Money Market Bond Market Forex Market

Stock Market#

LAF Call Money

Market Repo

CBLO Commercial Paper*

Certificates of Deposit*

G-Sec@ Corporate Bond

Inter-bank (US$ mn)

1 2 3 4 5 6 7 8 9 10 11

Mar-10 37,640 8,812 19,150 60,006 75,506 3,41,054 6,621 1,598 16,082 9,191

Mar-11-

80,96311,278 15,134 43,201 80,305 4,24,740 8,144 1,314 22,211 7,276

Apr-11-

18,80913,383 14,448 56,160 1,24,991 4,47,354 6,928 1,053 25,793 8,277

May-11 - 10,973 15,897 40,925 1,21,221 4,33,287 7,356 691 24,167 6,668

54,643

Jun-11-

74,125 11,562 16,650 41,313 1,23,400^ 4,23,767 12,844 1,16819,099**

6,404

*: Outstanding position. @: Average daily outright trading volume in Central Government dated securities. #: Volumes in BSE and NSE. ^: As at mid-June 2011. **: Up to June 24, 2011. Note: In col. 2, (-) ve sign indicates injection of liquidity while (+) ve sign indicates absorption of liquidity.

Money Market Operations as on July 27, 2011

(Amount in ` crore, Rate in per cent)

MONEY MARKETS @Volume Wtd.Avg.Rate Range

(One Leg)A. Overnight Segment (I+II+III+IV)

75,412.26 7.99 6.25-8.15

I. Call Money 13,198.18 8.02 6.25-8.15

II. CBLO 48,844.00 7.98 7.75-8.13

III. Market Repo 13370.08 7.99 7.55-8.15

IV. Repo in Corporate Bond

0.00 - -

B. Term Segment

I. Notice Money**

77.00 7.69 6.50-8.00

II. Term Money@@

402.30 - 6.90-9.85

III. CBLO 0.00 - -

IV. Market Repo 25.00 7.00 7.00-7.00

V. Repo in Corporate Bond

0.00 - -

RBI OPERATIONSAmount

OutstandingRate

C. Liquidity Adjustment Facility

(i) Repo (1 day) 25,430.00 8.00

(ii) Reverse Repo

(1 day)0.00 7.00

D. Marginal Standing Facility # (1 day) 0.00 9.00E. Standing Liquidity Facility Availed from RBI 2,459.27 8.00 RESERVE POSITION @F. Cash Reserves Position of Scheduled Commercial Banks

(i) Cash balances with RBI as on

25/07/2011 370,994.46

(ii) Average daily cash reserve requirement for the fortnight ending

29/07/2011 350,798.00

@ Based on Provisional RBI / CCIL Data- Not Applicable / No Transaction

# As announced in the Monetary Policy for the year 2011-12, a new Marginal Standing Facility (MSF) has been introduced with effect from May 9, 2011.** Relates to uncollateralized transactions of 2 to 14 days tenor@@ Relates to uncollateralized transactions of 15 days to one year tenor

QUESTIONS

Briefly discuss various money market instruments and their importance.

With examples explain how LAF has evolved over time

Discuss the transmission mechanism of monetary policy through interest channel in the money market

Discuss briefly the CP market and how it has been helpful to non-bank participants like private corporate

The evolution CD as money market instruments