monitoring and measuring intangibles using value maps: some examples

TRANSCRIPT

Monitoring and measuringintangibles using value maps:

some examplesShital Jhunjhunwala

Institute of Public Enterprise, Osmania University, Hyderabad, India

Abstract

Purpose – The purpose of this paper is to provide an integrated approach to understand and monitorthose intangible assets (IAs) that are the key value drivers of an organization. With the help of threedifferent examples, it attempts to examine the cause-and-effect relationship among differentintangibles and map them to organizational success.

Design/methodology/approach – System thinking approach using examples from three differentindustries.

Findings – The paper finds that the success of any organization depends on a network of interrelatedIAs that affect each other and the crux is to ensure that each of these is performing as desired. The useof a causal model clearly demonstrates the cause-and-effect relationships between key variables andultimate objectives, and helps companies identify which intangibles need to be constantly monitoredusing suitable indicators to achieve the desired goals.

Research limitations/implications – The models have not been verified in practice.

Practical implications – Useful for organizations to monitor and measure intangibles by linkingthem to their objective of maximizing shareholder value. The indicators illustrated can be used to trackthe performance of intangibles.

Originality/value – Three industry specific original generic models are presented that will be usefulto managers and consultants as a basis for identifying and mapping key intangibles (value drivers) totheir organization goals.

Keywords Intangible assets, Value analysis, Knowledge mapping, Shareholder value analysis

Paper type Conceptual paper

IntroductionThe industrial age characterized by enormous manufacturing facilities brought to theforefront of management attention and concerted their effort in managing, measuringand reporting tangible assets like buildings, plant, equipment, and machinery. Theinformation and knowledge age that we live in, with all its complexities and dynamicbehaviour has shifted the focus to intangible assets (IAs). It is well-accepted that brandvalue for a fast-moving consumer goods or employee skills for a software company arethe key assets of the organization and not the buildings or computers or any otherphysical asset they own. IAs have become the indisputable value drivers to success.

Organizations are thus, wanting to closely track their IAs. While traditionalaccounting systems were apt for measuring and reporting tangible assets,organizations today are at loss as to how to monitor the performance of IAs. Tomonitor, first intangibles need to be measured and reported. There are no globallyaccepted methods of doing this. Balance score card, intellectual capital report and IAmonitor are some of the tools that are gaining acceptance. They, however, measureindividual assets and fail to provide a holistic picture.

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1469-1930.htm

Monitoring andmeasuringintangibles

211

Journal of Intellectual CapitalVol. 10 No. 2, 2009

pp. 211-223q Emerald Group Publishing Limited

1469-1930DOI 10.1108/14691930910952623

The performance of each intangible is linked to others (Figure 1). Human capital(Chen et al., 2004) can convert knowledge into market value only with the support ofthe other three: structural, innovation and customer capitals. Human capital, in turn, isa determining factor of structural capital. “Furthermore, structural and human capitalenable enterprises to form, develop, and use innovation capital [. . .] On the other hand,innovation can give an impetus to growth of customer capital” by developing newproducts to meet customer demands. The promotion of customer capital relies onsupport from human, structural and innovative capital. Customer capital ultimatelygets converted into market value.

Value creation takes place depending on how intangibles interact. There is thus aneed to understand the causal relationship among the intangibles to be able to measureand monitor them so as to steer them towards the firm’s success.

The proponents of system thinking as a tool to study intangiblesLiterature surveySystem thinking and system dynamics (www.systemdynamics.org/) propounded byJay W. Forrester is a methodology for studying and managing complex feedbacksystems, such as one finds in business and other social systems. Feedback refers to thesituation of X affecting Y and Y in turn affecting X perhaps through a chain ofcause-and-effect. One cannot study the link between X and Y and, independently, thelink between Y and X and predict how the system will behave. System thinking usesthe causal loop mapping techniques to understand the relationship among differentvariables in a system. The use of causal diagrams to understand, monitor and measureintangibles has been suggested in different bodies of work.

Ittner and Larker (2003) suggested identifying and measuring those critical(intangible) factors that have a huge impact on the companies using a value drivermap. They used the fish and bone diagrams to study the interrelation betweenintangibles. Survey of 297 senior executives in 157 US manufacturing and servicecompanies indicates that companies make little effort to identify non-financial(intangible) performance and demonstrated a cause-and-effect link betweenimprovements in those non-financial parameters on cash flow profit or stock price.

Figure 1.

Customercapital

Structuralcapital

Humancapital

Source: Chen et al. (2004)

Innovationcapital

JIC10,2

212

Jack (n.d.) suggested the use of value mapping for measuring IAs. Valuing mappinguses value maps to visually communicate desired value outcomes, arising from valueneeds and associated strategy, as well as value drivers, the things that impact on thedesired value outcomes. It starts with a review of stakeholders needs called value needassessment with a clear use and worth within a given time scale. It uses predictivevalue outcome maps to obtain desired value outcomes. Value drivers that havegreatest value in deriving these values are identified. Performance measures are thendeveloped that capture the performance of both the value drivers and the valueoutcomes. Value outcome maps and measures for these predictive value outcomes arethen produced.

The value þ activity-based approach (Bygdas et al., 2004) for measuring IAsfocuses on the dynamic aspects of value creation, visualizing important and complexknowledge processes based on three phases of modeling, measuring and action.The modeling phase begins with a mapping and description of the company’s criticalvalue processes, the activities in those and a description of how they are interrelated. Inthe measuring phase, the resources required for each activity is mapped. For eachactivity there is a mapping of what intellectual (critical and necessary) resources areneeded to give sufficient quality and frequency of the activities.

The MERITUM Guidelines were developed by the Measuring Intangibles toUnderstand and Improve Innovation Management – MERITUM (2001) Project, aconsortium comprising researchers from six European countries (Denmark, France,Finland, Norway, Spain, and Sweden). It recommends linking intangible activities withlong-term strategy. Intangible resources are identified and activities that are like toaffect these resources as well as intangible activities and their impact on crucialintangible resources. As a result of the identification process a causal network ofintangibles emerges which are measured using indicators.

Kaplan and Norton (2004) strategy maps is by far the most well-known use ofsystem thinking in monitoring and measuring IAs. The strategy map provides aframework for linking IAs to shareholder value creation through four interrelatedprospective – financial, customer, internal processes, and learning and growth. Itpresents a way to systematically measure the alignment of the company’s human,information and organizational capital – without which even the best strategy cannotsucceed.

The causal relationship and value mapping: some examplesThe goal of all companies is to enhance share holder value. The key value drivers toachieve this goal are different for different companies based on their vision, mission,long and short-term goals and the strategy they adopt to achieve them. Value iscreated when organizations successful respond to market conditions by making themost of internal resources and capabilities (Marr et al., 2004). Thus, managers needto understand the key resources and drivers of value in the organization. Moreor less, however, the key value drivers, in other words intangibles that drive acompany to success would be common within an industry. For instance, employeeskill and talent is undoubtedly the key value driver for a software company.A generic kind of model with the key success variables is thus being presented forthree different industries for a better understanding of how intangibles ultimatelylead to creating shareholder value.

Monitoring andmeasuringintangibles

213

Hotel industryThe model (Figure 2) depicts the key variables that need to perform satisfactorily for aluxury holiday hotel to be successful. Success of a hotel is measured by its occupancyrate which is dependent on its reputation (an IA) and location advantage (IA) like onthe sea beach or in the centre of the city. Location advantage, good ambience (IA),a spread of well-layout (IA) facilities like swimming pools, multiple restaurants, etc.quality services (IA) whether at the reception, or of the food in the restaurant, or ofhousekeeping or even at the billing counter and the courtesy and helpfulness attitude(IA) of the employees lead to customer satisfaction (IA), which coupled with brand (IA)of the chain enhance reputation (IA) of the hotel. Quality services can be achieved onlyif the operational processes are well-designed (IA) and well-trained motivatedworkforce (IA) ensure the efficiency of the processes (IA). It is the responsibility of themanagement (IA) to select and recruit the right kind of people and provide training andmotivation to them.

The more the employee satisfaction (IA) and motivation, the better will be theirbehaviour and attitude towards customers and towards work leading to highercustomer satisfaction, which in turn will increase reputation of the hotel and therebyincrease occupancy rate ultimately creating shareholder value. Satisfied shareholders

Figure 2.Hotel industry

Shareholdervalue creation

Sustained profitability(occupancy rate)

Customerstatisfaction

ReputationLocationaladvantage

++

Chain brand

Employee behaviourand attitude

+

Assembled, productiveemployee workforce

Top managerialhuman resources

Employeesatisfaction

Training

Appropriate selection andrecruitment policy and

procedure

+

+

+

Investments

Facilities

+

+

+

+

Architectural andinterior desingning

Note: Variables in italic are intangible and underlined variables are the key intangibles

Layout of facilitiesand ambience Quality of service (reception,

restaurants, room service,housekeeping, etc)

Processefficiency

++

+

++

+

++

+

+

+

+

+

+

JIC10,2

214

will then reappoint the top management whose performance has created wealth forthem. If they are dissatisfied they will replace them.

Software (support) industryCustomer retention, customer acquisition, and expanding business from existingcustomer are the key intangibles for sustained profits creating shareholder value for acompany providing software support to its clients (Figure 3).

This is possible only through high levels of customer satisfaction (IA) whichdepends on quality service (IA) – timely delivery of objective without hamperingproduction. Satisfied customers, not only, means customer retention (IA) and newbusiness from them but also builds the companies reputation attracting new customers(IA). Top management (IA) need to design effective and efficient processes (IA) andhave a team of highly skilled, trained and motivated technical workforce with theappropriated competency (IA) available to provide quality services.

Figure 3.Software (support)

industry

Shareholder valuecreation

Sustainedprofitability

Expansion of businessof existing customers

Customer (new)acquisition

+

Reputation

Quality service (timely deliveryof service object withouthampering production)

+

+

Assembled, productivetechnical workforce

Top managerialhuman resources

Skilled,talented and trainedmarketing human

resourses

Training

Note: Variables in italics are intangible and underlined variables are the key intangibles

Appropriate selection andrecruitment policy and

proccedure

+ +

+

Employeesatifaction

Productive marketingworkforce

+

+

Marketingstrategy

Customersatifaction

+

+

Processefficiency

Customerretention +

+

+

+

+

+

+

Skilled, talented andtrained technical human

resourse

+

+

Competency mapping (ofskill set matrix with service

requirements)

+

+

+

+

Monitoring andmeasuringintangibles

215

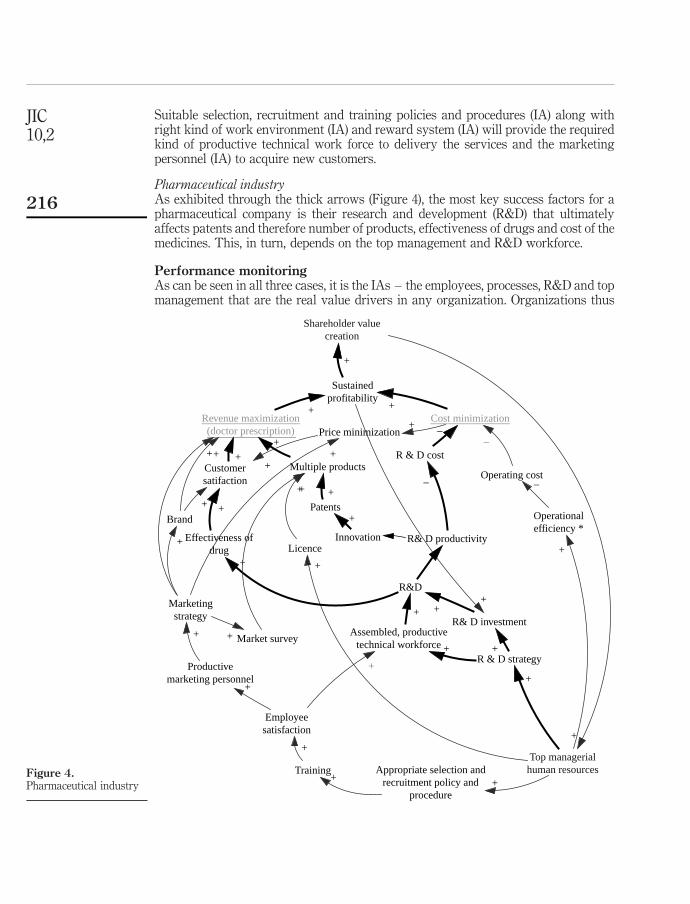

Suitable selection, recruitment and training policies and procedures (IA) along withright kind of work environment (IA) and reward system (IA) will provide the requiredkind of productive technical work force to delivery the services and the marketingpersonnel (IA) to acquire new customers.

Pharmaceutical industryAs exhibited through the thick arrows (Figure 4), the most key success factors for apharmaceutical company is their research and development (R&D) that ultimatelyaffects patents and therefore number of products, effectiveness of drugs and cost of themedicines. This, in turn, depends on the top management and R&D workforce.

Performance monitoringAs can be seen in all three cases, it is the IAs – the employees, processes, R&D and topmanagement that are the real value drivers in any organization. Organizations thus

Figure 4.Pharmaceutical industry

Shareholder valuecreation

Sustainedprofitability

R & D cost

Cost minimizationRevenue maximization(doctor prescription)

++

Operating cost

Price minimization

R& D productivity

+

–

R & D strategy

Assembled, productivetechnical workforce

Top managerialhuman resources

Employeesatisfaction

Training Appropriate selection andrecruitment policy and

procedure

+ +

+

Productivemarketing personnel

Marketingstrategy

+

+

+

+

–

–

+

Brand

Customersatifaction

Effectiveness ofdrug

+

+ +

++

Multiple products

+

Patents

LicenceInnovation

R&D

R& D investment

+

+

+

+

+

+

+

+

+

+

+

Market survey+

+

Operationalefficiency *

–

+

+

+

+

JIC10,2

216

need to layout their value driver maps (causal model) and identify the key intangiblesthat need to be tracked. The causal network of intangibles provides not only a preciserepresentation of the organization’s current critical IAs but also those that need to bedeveloped in future to meet its strategic objectives. Once the cause-and-effectrelationship is established there is a need to validate the same. We need to assess theusefulness of the measure? In our hotel example, large turnover of sweepers cannot beconsidered in the same light as large turnover of cooks. So which employees’satisfactions are more important have to be identified. Each parameter then needs to bemeasured using a valid and reliable measurement technique. To meet the goals desiredperformance targets are set. Suitable remedial actions can be taken if variables in valuechain are not up to the mark so as to improve future performance. Consistentperformance of the key variables will ultimately lead to the organizations creatingshareholders wealth.

MeasurementOnce critical intangibles have been identified and causal relationship established, thefirm needs to define specific set of indicator for each intangible. Indicators should befeasible, i.e. easy to measure. The effort and cost of measurement should not be so highas to set-off any benefit derived thereby. Indicators must be understandable andbeneficial to the user. The user must know how to improve the measure. Indicator to beuseful must be consistent, comparable, relevant, and reliable (adopted from Statementof Financial Accounting Concepts (CON) 2: Qualitative Characteristics of AccountingInformation, FASB):

(1) Comparable. The characteristic of comparability allows the users to assessthe similarities and differences either among different companies for thesame time period or for the same company over different time periods.Comparisons are usually made on the basis of quantifiable measurements ofa common characteristic. Therefore, to be comparable, the measurements usedmust be reliable with respect to the common characteristic. Non-comparabilitycan result from the use of different inputs, procedures, or systems ofclassification.

(2) Consistent. The characteristic of consistency also contributes to indicatorusefulness. Consistency requires the use of the same principles in measurementfrom one period to another. Consistency does not insure comparability.Non-comparability can also arise when the data measurements lackrepresentational faithfulness.

(3) Relevant. An indicator is relevant if it makes a difference to the user in his/herability to improve performance and create value. To be relevant, it must betimely: although timeliness alone will not make an indicator relevant, indicatorsmust be timely to be relevant. It must be available before it loses its ability toinfluence the users’ actions.

(4) Reliable. Indicators are a reflection of the firm’s activities. To be reliable, theymust be verifiable, neutral, and a truthful representation:. Verifiability means that several independent measures will obtain the same

result. A measure that can be repeated with the same result (consensus) isdesirable because it serves to detect and reduce measurer bias. The direct

Monitoring andmeasuringintangibles

217

verification of a measure would serve to minimize measurer bias andmeasurement bias. The verification of the procedures used to obtain themeasure would minimize measurer bias only. Finally, verifiability does notguarantee representational faithfulness or relevance.

. The characteristic of neutrality means that the indicator should be objectiveand unbiased and not attempt to influence behavior in a particular direction.This does not mean that the indicator should not influence behavior or that itshould affect everyone in the same way. It means that indicator should notfavor certain interest groups.

. The characteristic of representational faithfulness implies that indicatorsmust represent that which it is intended to represent. It should be truthfuland present the real situation that it represents. It should not be bias. Bias isthe tendency for a measure to be consistently too high or too low. Bias mayarise because the measurer does not use the measurement method properlyor because the measurement method does not represent what it purports torepresent.

The indicators may be general, comparing across firms and industries, say, employeeturnover ratio or advertisement expenses to sales or industry specific so that onlycomparison among companies within the same industry is possible, e.g. no. ofprofessors in different subjects in a business school, or even firm specific, the definitiondiffers from company to company and comparisons are hard to make or do not makesense, e.g. ratio of delay in report X and absentees of employee Y.

Indicators derive their data from either financial sources (revenue/R&Dexpenditure) or non-financial sources (number of defects in a batch) or may combineboth (average training expenses per employee category or telephone expenses percustomer, Table I):

The set of indicators (MERITUM Guidelines) used by the firm is a dynamic set. If they are tobe useful for management purposes, they should reflect changes and the learning effectsaccomplished by the organization. Simultaneously, if the company and its stake holders mustvisualize the dynamics of a situation, it may be necessary to make comparisons acrossperiods. Consequently, a core and stable set of indicators should be kept over a relatively longperiod of time.

Finally, the indicators must measure and monitor intangibles serving the process ofvalue creation.

ConclusionThe success of any organization, thus, depends on a network of interrelated IAs thataffect each other and the crux is to ensure that each of these is performing as desired.The use of a causal model clearly demonstrating the cause-and-effect relationshipsbetween key variables and ultimate objectives, help companies identify whichintangibles needed to be constantly monitored using suitable indicators to achieve thedesired goals. A study conducted by Wharton School and PricewaterhouseCoopers(Ittner and Larker, 2003) shows that companies that use causal models laying downcause-and-effect relationship between drivers of success and outcomes had “on average2.95% higher return on assets and 5.14% higher return on equity” than companies that

JIC10,2

218

Sou

rce

ofin

form

atio

nIn

tan

gib

leca

teg

ory

Fin

anci

alF

inan

cial

and

non

-fin

anci

al(R

s)N

on-fi

nan

cial

Hu

man

cap

ital

Tot

alem

plo

yee

exp

ense

sT

rain

ing

exp

ense

sT

rain

ing

exp

ense

/tot

alex

pen

ses

Tra

inin

gex

pen

se/a

dm

inis

trat

ive

exp

ense

s(%

)(S

N)

Tra

inin

gex

pen

ses/

tota

lem

plo

yee

exp

ense

Mar

ket

val

ue/

emp

loy

eeA

sset

s/em

plo

yee

Fix

edas

sets

/em

plo

yee

Inco

me/

emp

loy

eeV

alu

e-ad

ded

/em

plo

yee

Inv

oici

ng

/em

plo

yee

Tra

inin

gex

pen

ses/

emp

loy

ee

Lea

der

ship

ind

ex(%

)M

otiv

atio

nin

dex

(%)

Em

pow

erm

ent

ind

ex(r

esp

onsi

bil

ity

/au

thor

ity

)E

mp

loy

eesa

tisf

acti

onin

dex

No.

ofem

plo

yee

sE

ffici

ency

:ou

tpu

t/em

plo

yee

(un

its)

Av

erag

ew

ork

ing

hou

rsT

rain

ing

/em

plo

yee

(tim

e)In

form

atio

nte

chn

olog

y(I

T)

lite

racy

ofem

plo

yee

s(%

)A

ver

age

sati

sfac

tion

wit

hco

mp

eten

ced

evel

oped

Per

cen

tag

eof

wor

kfo

rce

wit

hy

earl

yjo

bro

tati

onA

ver

age

emp

loy

eere

ten

tion

Av

erag

ey

ears

inco

mp

any

Av

erag

eag

eof

emp

loy

ee(y

ears

)A

ver

age

edu

cati

onle

vel

Per

cen

tag

eof

emp

loy

ees

wit

hp

ost-

gra

du

ate,

gra

du

ate,

and

sch

ool

lev

elq

ual

ifica

tion

sA

ver

age

pro

fess

ion

alex

per

ien

ce(y

ears

)S

kil

led

/un

skil

led

Gra

du

ates

/tot

alP

ost-

gra

du

ates

/tot

alE

mp

loy

eetu

rnov

erE

xp

ert

turn

over

Man

ager

stu

rnov

erW

ork

ers

turn

over

Man

ager

s/w

ork

ers

Mal

e/fe

mal

eF

emal

em

anag

ers

(%)

(continued

)

Table I.Indicators for measuring

performanceof different IAs

Monitoring andmeasuringintangibles

219

Sou

rce

ofin

form

atio

nIn

tan

gib

leca

teg

ory

Fin

anci

alF

inan

cial

and

non

-fin

anci

al(R

s)N

on-fi

nan

cial

Cu

stom

er-r

elat

edS

ales

from

top

cust

omer

(Rs)

Sal

esfr

omto

pfi

ve

cust

omer

(Rs)

Sal

esfr

omto

pcu

stom

er/t

otal

sale

sS

ales

from

top

fiv

ecu

stom

er/t

otal

sale

s

Cu

stom

ersi

ze:

ann

ual

pu

rch

ase

per

cust

omer

Su

pp

ort

exp

ense

s/cu

stom

erS

erv

ices

exp

ense

s/cu

stom

er

Cu

stom

erti

me/

emp

loy

eeat

ten

dan

ce(%

)N

um

ber

ofac

cou

nts

Cu

stom

er/e

mp

loy

eeC

ust

omer

sco

nta

cted

(no.

)C

ust

omer

sco

nta

cted

(%)

Cu

stom

ers

vis

ited

(no.

)C

ust

omer

sv

isit

ed(%

)N

o.of

rep

eat

cust

omer

sR

ate

ofre

pea

tcu

stom

ers

(%)

Cu

stom

erd

ura

tion

ortu

rnov

erra

teA

ver

age

cust

omer

du

rati

on/l

oyal

tyti

me

Cu

stom

ers

vis

itin

gco

mp

any

(no.

)C

ust

omer

sv

isit

ing

web

site

Av

erag

eco

nta

cts

by

cust

omer

sD

ays

spen

tv

isit

ing

cust

omer

s(n

o.)

Dir

ect

com

mu

nic

atio

ns

tocu

stom

er(n

o.)

Cu

stom

erra

tin

gin

dex

Cu

stom

ersa

tisf

acti

onin

dex

No.

ofcu

stom

ers/

no.

ofem

plo

yee

sd

irec

tly

inv

olv

edA

nn

ual

pu

rch

ase

per

cust

omer

(no.

)C

ust

omer

slo

st(n

o.)

Cu

stom

erIT

lite

racy

rate

(%)

Imag

een

han

cin

gcu

stom

ers

Mar

ket

-rel

ated

Mar

ket

ing

exp

ense

s/to

tal

exp

ense

s(%

)S

ales

/mar

ket

ing

exp

ense

s(%

)In

ves

tmen

tin

dev

elop

ing

new

mar

ket

s(R

s)

Sal

es/c

ust

omer

Sal

es/n

ewcu

stom

ers

Sal

es/e

mp

loy

eeS

ales

/fro

nt-

lin

eem

plo

yee

sM

ark

etin

gex

pen

ses

cust

omer

Sal

es/e

mp

loy

eeM

ark

etin

gex

pen

ses/

pro

du

ctli

ne

Mar

ket

ing

exp

ense

s/p

rod

uct

Mar

ket

shar

e(%

)N

o.of

pro

du

cts

Pro

du

cts

sold

Pro

spec

tiv

ecu

stom

ers

vis

ited

orco

nta

cted

(no.

)P

rosp

ecti

ve

cust

omer

sv

isit

edor

con

tact

ed(%

)P

oin

tsof

sale

(no.

)N

o.of

new

acco

un

tsA

ver

age

tim

efr

omcu

stom

erco

nta

ctto

sale

Rat

ioof

con

tact

tosa

les

clos

ed(continued

)

Table I.

JIC10,2

220

Sou

rce

ofin

form

atio

nIn

tan

gib

leca

teg

ory

Fin

anci

alF

inan

cial

and

non

-fin

anci

al(R

s)N

on-fi

nan

cial

Inn

ovat

ion

and

R&

DIn

com

efr

omn

ewb

usi

nes

sop

erat

ion

s(R

s)R

etu

rnon

net

asse

tsfr

oma

new

bu

sin

ess

oper

atio

n(R

s)R

even

ue

from

new

pat

ents

Net

rev

enu

efr

omn

ewp

aten

tsIn

ves

tmen

tin

R&

DR

&D

retu

rnon

inv

estm

ent

R&

Dex

pen

ses/

rev

enu

e(%

)R

&D

exp

ense

s/to

tal

exp

ense

s(%

)R

&D

inv

estm

ent

inb

asic

rese

arch

(%)

R&

Din

ves

tmen

tin

pro

du

ctre

sear

ch(%

)R

&D

inap

pli

edre

sear

ch(%

)R

&D

asse

ts/t

otal

asse

tsIn

ves

tmen

tin

com

pet

itiv

ein

tell

igen

cep

rog

ram

(Rs)

Com

pet

ency

dev

elop

men

tex

pen

ses/

emp

loy

ee(S

N)

Tra

inin

gex

pen

ses/

emp

loy

ee

Per

cen

tag

eof

new

pro

du

cts

reac

hin

gm

ark

etN

o.of

new

pro

du

cts

New

pro

du

cts

ind

evel

opm

ent

Av

erag

ees

tim

ated

age

ofp

rod

uct

sN

o.of

pat

ents

No.

ofn

ewp

aten

tsA

ver

age

age

ofp

aten

tsN

o.of

pat

ent

app

lica

tion

sR

&D

emp

loy

ees/

tota

lem

plo

yee

sT

rain

ing

hou

rs

Pro

cess

-rel

ated

Ad

min

istr

ativ

eex

pen

ses/

tota

lex

pen

ses

(%)

Ad

min

istr

ativ

eex

pen

ses/

tota

lre

ven

ue

(%)

Inv

estm

ent

inIT

/rev

enu

e(%

)

Ad

min

istr

ativ

eex

pen

ses/

emp

loy

ees

Ad

min

istr

ativ

eex

pen

ses/

cust

omer

ITex

pen

ses/

emp

loy

ee

Pro

du

ctiv

ity

Pro

cess

ing

tim

eA

ver

age

ord

erre

spon

seti

me

No.

ofer

rors

Per

cen

tag

eof

erro

rsto

outp

ut

Ou

tpu

t/em

plo

yee

Fu

nct

ion

poi

nt/

emp

loy

eeA

dm

inis

trat

ive

staf

f/to

tal

emp

loy

ees

(%)

Per

cen

tag

eof

crit

ical

pro

cess

esth

ath

ave

am

anu

alR

elat

ion

ship

and

coll

abor

atio

nIn

ves

tmen

tin

stra

teg

icp

artn

ersh

ipd

evel

opm

ent

(Rs)

Com

mon

trai

nin

gp

rog

ram

sof

com

pan

yan

dp

artn

ers

(Rs)

Com

mon

cust

omer

acti

vit

ies

wit

hco

mp

any

and

par

tner

sC

omp

any

pro

du

cts

orco

mp

onen

tsd

esig

ned

by

par

tner

sC

omm

ontr

ain

ing

pro

gra

ms

ofco

mp

any

and

par

tner

s(n

os)

Source:

Com

pli

edfr

omd

iffe

ren

tw

ork

san

dow

n

Table I.

Monitoring andmeasuringintangibles

221

do not use causal models. In a dynamic, complex, and competitive global businessenvironment that is a need to continuously refine the cause-and-effect diagram asrelationships undergo transformation changing the value drivers.

References

Bygdas, A.L., Royrvik, E. and Gjerde, B. (2004), “Integrative visualization and knowledgeenabled value creation: an activity based approach to intellectual capital”, Journal ofIntellectual Capital, Vol. 5 No. 4, pp. 540-55.

Chen, J., Zhu, Z. and Xie, H.Y. (2004), “Measuring intellectual capital: a new model and empiricalstudy”, Journal of Intellectual capital, Vol. 5 No. 1, pp. 196-212.

Ittner, C.D. and Larker, D.F. (2003), “Coming up short on non-financial performancemeasurement”, Harvard Business Review, November, pp. 88-95.

Jack, A. (n.d.), “Value mapping: a second generation performance measurement and performancemanagement solution”, available at: www.valuebasedmanagement.net/articles_jack_value_mapping_second_generation_performance_management.pdf

Kaplan, R.S. and Norton, D.P. (2004), “Measuring the strategic readiness of intangible assets”,Harvard Business Review, February, pp. 52-63.

Marr, B., Suchiuma, G. and Neely, A. (2004), “The dynamics of value creation: mapping yourintellectual performance drivers”, Journal of Intellectual Capital, Vol. 5 No. 2, pp. 312-25.

MERITUM (2001), Guidelines for Managing and Reporting on Intangibles, Programa TargetedSocio Economic Research – TSER, European Union, Brussels, available at: www.urjc.es/innotec/tools/MERITUM%20Guidelines.pdf

Further reading

Allen, D. (2001), “Hard currency”, Financial Management, Caspian Publishing, London,14719185, January.

Edvinsson, L. and Malone, M.S. (1997), Intellectual Capital, Harper Collins, New York, NY.

Epstein, B.J., Nach, R. and Bragg, S.M. (2006), GAAP 2006, Interpretations and Applications ofGenerally Accepted Accounting Principals, Wiley, New York, NY.

Foster, B.P. and Stout, W.D. (2003), “Valuing intangible assets”, CPA Journal, October, pp. 52-4.

Jhunjhunwala, S. (2005), “Does the market understand intangibles”, The CA Journal ICAI, July,pp. 123-7.

Jhunjhunwala, S. (2007), paper presented at National Conference on System Dynamics atInstitute of Public Enterprise, Hyderabad, June 28-29.

Lev, B. (2001), Intangibles, Management, Measurement and Reporting, Brookings InstitutionPress, Washington, DC.

Lev, B. (2004), “Sharpening the intangible edge”, Harvard Business Review, June, pp. 109-16.

Mard, J.M., Hichner, J.R., Hyden, S.D. and Zyla, M.L. (2002), Valuation for Financial Reporting –Intangible Assets, Goodwill and Impairment Analysis, SFAS 141 and 142, Wiley,New York, NY.

Richmond, B. (2001), Introduction to System Thinking, High Performance, Hanover, NH.

Sternman, J. (2000), Business Dynamics: Systems Thinking and Modeling for a Complex World,McGraw-Hill, New York, NY.

Ulrish, D. and Smallwood, N. (2004), “Capitalizing on capabilities”, Harvard Business Review,June, pp. 119-27, available at: www.iseesystems.com

JIC10,2

222

About the authorShital Jhunjhunwala is an Assistant Professor in the Institute of Public Enterprise, she is aFellow Member of the Institute of Chartered Accountants of India, a cost accountant andmanagement graduate from Indian Institute of Management – Calcutta. She has over five yearsof experience in accounting, auditing, and credit appraisal having worked in diverse sectorsincluding manufacturing, dot-com and financial services. She has been teaching and conductingresearch in the areas of cost and management accounting, investment planning, valuation,intangible assets, and corporate social responsibility. She has conducted managementdevelopment programs for senior executives and faculty development program in the area offinance and management. She has also conducted national level conferences. She has publishedarticles in reputed journals and presented papers in a number of international conferences. Shepresented a paper at an International Conference on Business and Information (BAI 2006) atSingapore in July 2006. She is a reviewer for Contemporary Management Review an internationaljournal of Academy of Taiwan Information Systems Research. Shital Jhunjhunwala can becontacted at: [email protected]

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints

Monitoring andmeasuringintangibles

223