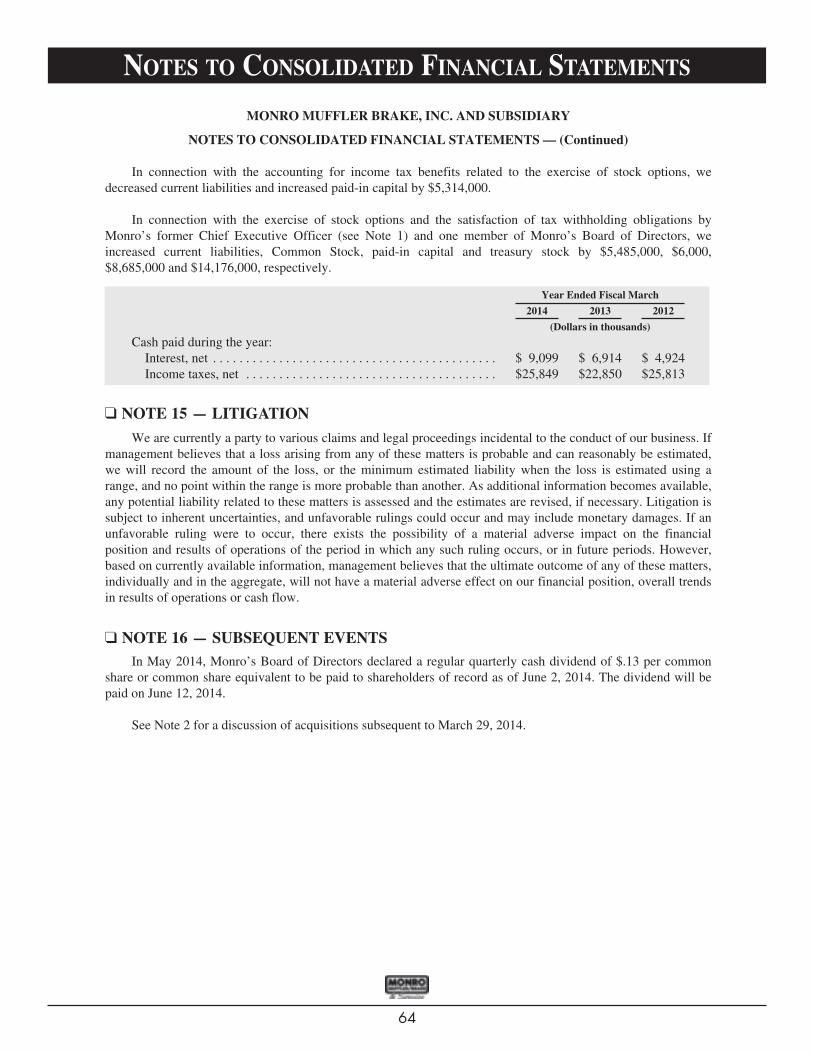

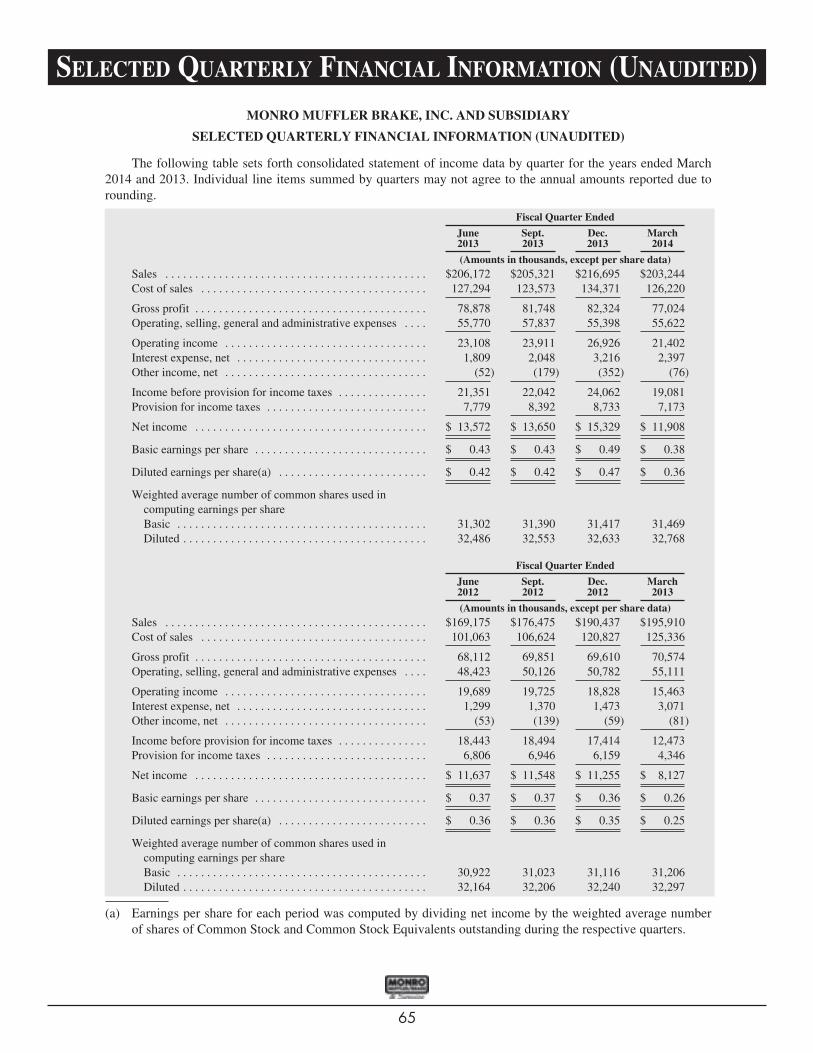

monro muffler brake, inc. · tire city • tire • carl king ony tire se tire craven y ... monro...

TRANSCRIPT

Autotire • Carl King Tire • Colony Tire • Courthouse Tire • Craven • Curry Auto Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer

Tire Co. • Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge •

Vespia Tire • Autotire • Carl King Tire • Colony Tire • Courthouse Tire • Craven • Curry Auto Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel

• Kramer Tire Co. • Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley

Forge • Vespia Tire • Autotire • Carl King Tire • Colony Tire • Courthouse Tire • Craven • Curry Auto Service • Enger Tire • Frasier • Import Export • Ken Towery

• Kimmel • Kramer Tire Co. • Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse

• Valley Forge • Vespia Tire • Autotire • MONRO • Colony Tire • Courthouse Tire • Craven • Curry Auto Service • Enger Tire • Frasier • Import Export • MONRO •

MRTIRE • TREAD QUARTERS • AUTOTIRE • Midwest • Midwest • MRTIRE • TREAD QUARTERS • AUTOTIRE • TIRE WAREHOUSE • Speedy • Terry’s Tire Town • Tire Barn • Tire

King • Tire Warehouse • TIRE WAREHOUSE • TIRE BARN • KEN TOWERY’S • CURRY’S • Colony Tire • TIRE BARN • KEN TOWERY’S • Curry Auto Service • Enger Tire • Frasier •

Import Export • Ken Towery • Kimmel • CURRY’S • Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire

King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire • Carl King Tire • Colony Tire • Courthouse Tire • Craven • Curry Auto Service • Enger Tire • Frasier

• Import Export • Ken Towery • Kimmel • Kramer Tire Co. • Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn

• Tire King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire • Carl King Tire • Colony Tire • Courthouse Tire • Craven • Curry Auto Service • Enger Tire •

Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire Co. • Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town

• Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire • Carl King Tire • Colony Tire • Courthouse Tire • Craven • Curry Auto Service •

Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire Co. • Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s

Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire • Carl King Tire • Colony Tire • Courthouse Tire • Craven • Curry Auto

Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire Co. • Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone • Speedy •

Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire • Carl King Tire • Colony Tire • Courthouse Tire • Craven • Curry

Auto Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire Co. • Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone •

Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire • Carl King Tire • Colony Tire • Courthouse Tire • Craven

• Curry Auto Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire Co. • Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S

Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire • Carl King Tire • Colony Tire • Courthouse

Tire • Craven • Curry Auto Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire Co. • Midwest • Mr. Tire • ProCare • Rice Tire • Roc

City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire • Carl King Tire • Colony Tire •

Courthouse Tire • Craven • Curry Auto Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire Co. • Midwest • Mr. Tire • ProCare • Rice

Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire • Carl King Tire • Colony

Tire • Courthouse Tire • Craven • Curry Auto Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire Co. • Midwest • Mr. Tire • ProCare

• Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire • Carl King Tire •

Colony Tire • Courthouse Tire • Craven • Curry Auto Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire Co. • Midwest • Mr. Tire

• ProCare • Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire • Carl

King Tire • Colony Tire • Courthouse Tire • Craven • Curry Auto Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire Co. • Midwest •

Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia Tire • Autotire

• Carl King Tire • Colony Tire • Courthouse Tire • Craven • Curry Auto Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire Co. •

Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia Tire •

Autotire • Carl King Tire • Colony Tire • Courthouse Tire • Craven • Curry Auto Service • Enger Tire • Frasier • Import Export • Ken Towery • Kimmel • Kramer Tire

Co. • Midwest • Mr. Tire • ProCare • Rice Tire • Roc City • S&S Firestone • Speedy • Terry’s Tire Town • Tire Barn • Tire King • Tire Warehouse • Valley Forge • Vespia

Monro Muffler Brake, Inc.2014 AnnuAl RepoRt

GrowinG Competitive AdvAntAGe

Monro Muffler Brake, Inc.200 Holleder Parkway

Rochester, New York 14615www.monro.com

1016834_Monro Annual Report_2014.indd 2 6/27/14 8:29 AM

ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS

Monro Muffler Brake, Inc., headquartered in Rochester, New York, is a chain of company-owned and operated stores in the United States. Our stores provide a broad array of services with either an undercar repair emphasis or a tire sale and service emphasis. >

Undercare services encompass:

• Brake systems• Steering systems• Exhaust systems• Drive train systems• Suspension systems• Wheel alignments

In addition, the stores provide many routine maintenance services, including or involving:• Oil changes• Tires sales and service• Air conditioning systems (in select stores)• Heating and cooling system flush and fills• Transmission flush and fills• Minor tune-ups• Batteries, alternators and starters• Belt and hose installations• State inspections• Scheduled maintenance

As of March 29, 2014, the company had 953 company-operated stores in New York, Pennsylvania, Ohio, Connecticut, Maine, Massachusetts, West Virginia, Virginia, Maryland, Vermont, New Hampshire, New Jersey, North Carolina, South Carolina, Indiana, Rhode Island, Delaware, Illinois, Kentucky, Tennessee, Wisconsin and Missouri.

Monro Muffler Brake, Inc., a category leader in the Northeast and Great Lakes, desires to be the dominant auto service provider in the markets it serves by:

• Providing consumers and businesses with superior value via a quality job at a fair price with superior convenience and customer service

• Being a rewarding place for dedicated, motivated employees to work

• Providing superior returns to shareholders

> Because you need to TRUST who’s working on your car.

1016834_Monro Annual Report_2014.indd 3 6/27/14 8:29 AM

ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS

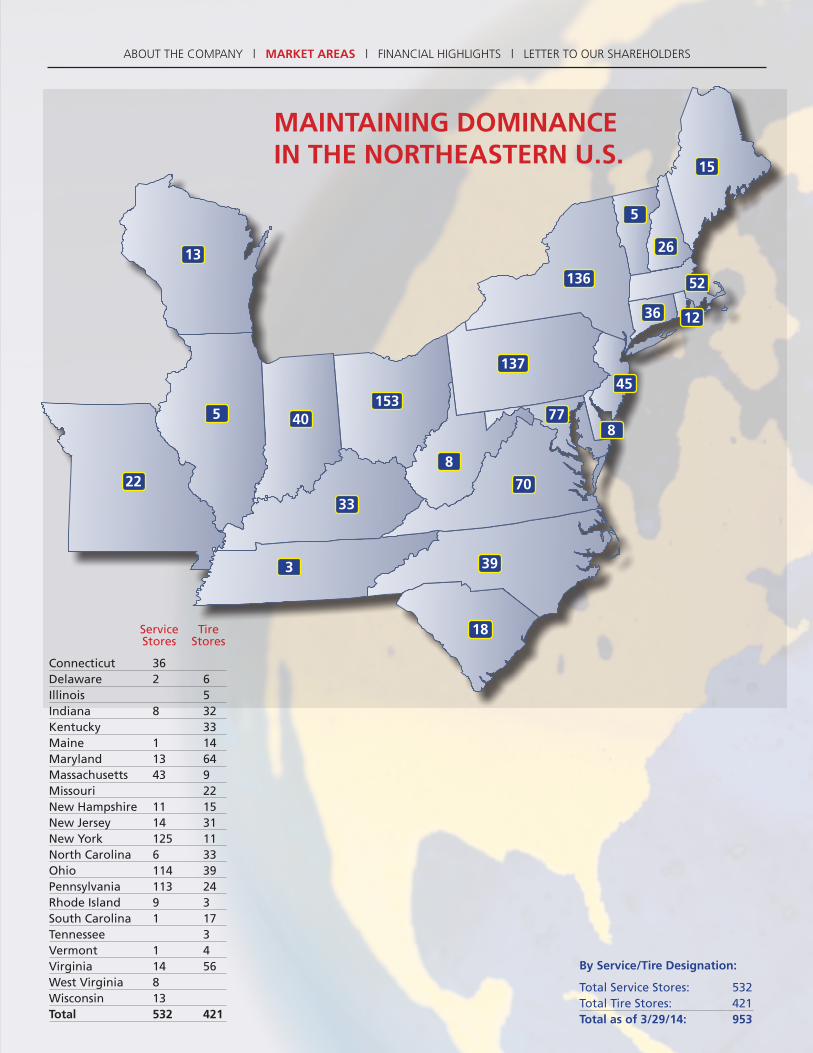

By Service/Tire Designation:

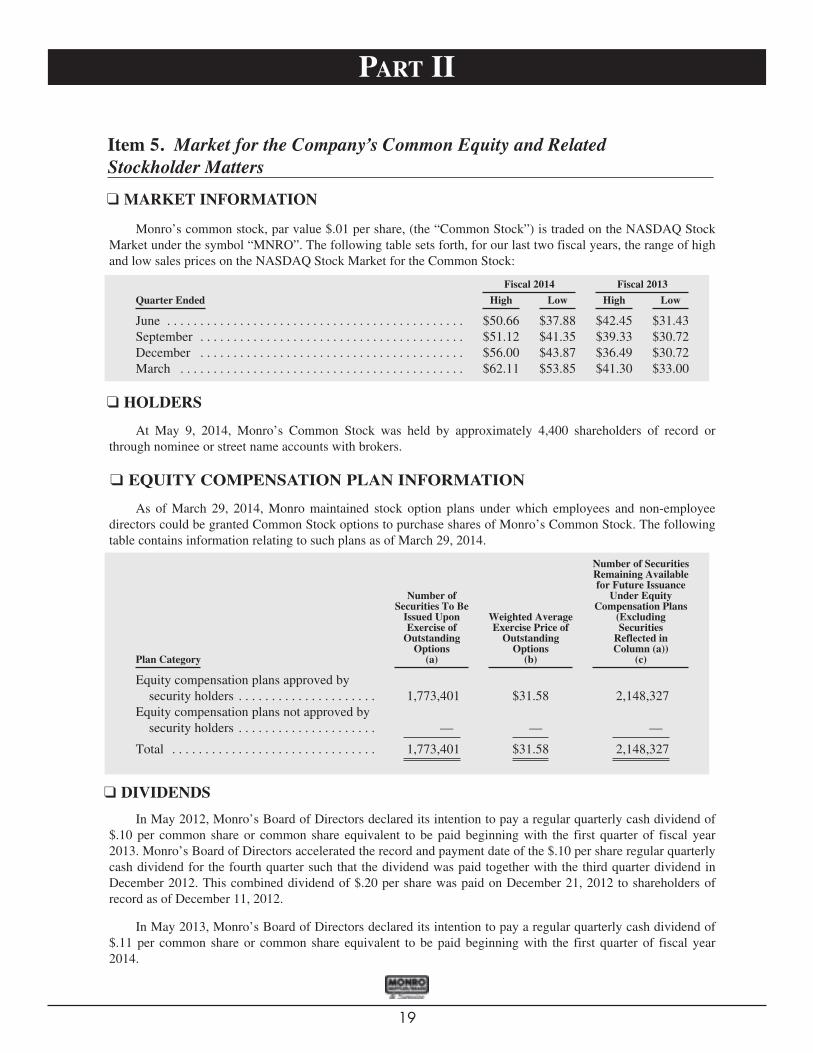

Total Service Stores: 532Total Tire Stores: 421Total as of 3/29/14: 953

MAiNTAiNiNg DOMiNANCE iN THE NORTHEASTERN U.S.

153405

13

22

33

3 39

18

70

8

778

45

36 12

52

26

5

15

137

136

Service Tire Stores Stores

Connecticut 36Delaware 2 6Illinois 5Indiana 8 32Kentucky 33Maine 1 14Maryland 13 64Massachusetts 43 9Missouri 22New Hampshire 11 15New Jersey 14 31New York 125 11North Carolina 6 33Ohio 114 39Pennsylvania 113 24Rhode Island 9 3South Carolina 1 17Tennessee 3Vermont 1 4Virginia 14 56West Virginia 8Wisconsin 13Total 532 421

1016834_Monro Annual Report_2014.indd 4 6/27/14 10:45 AM

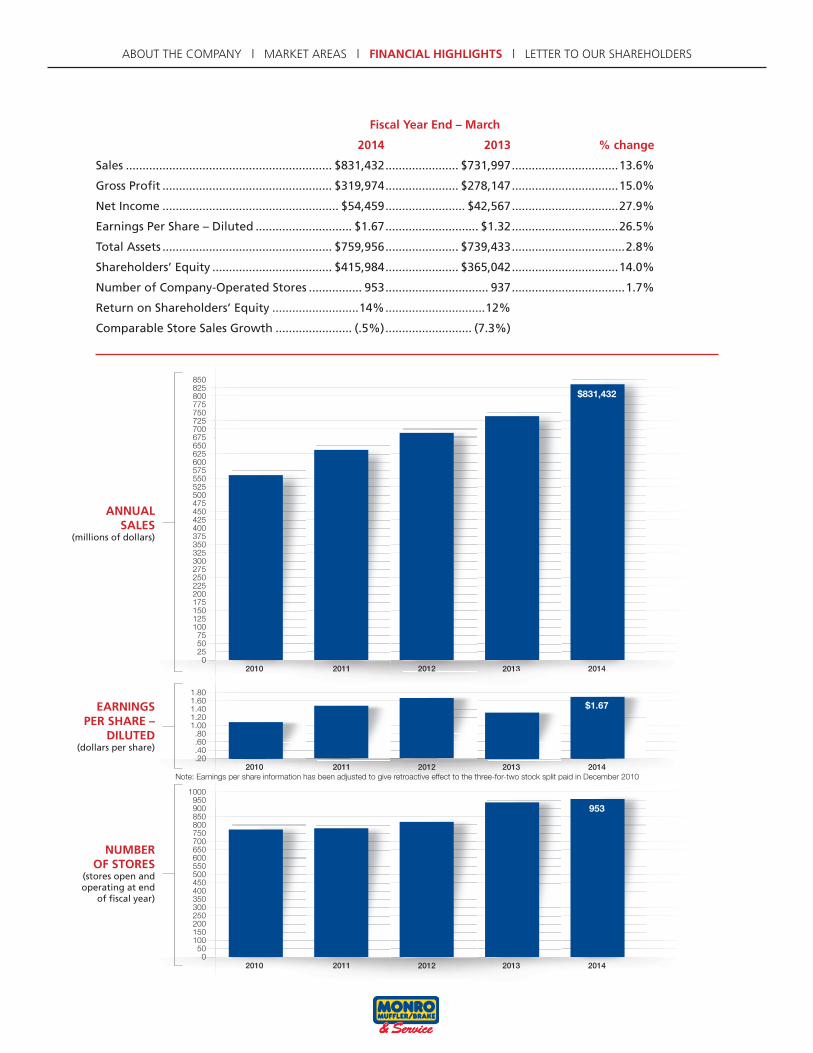

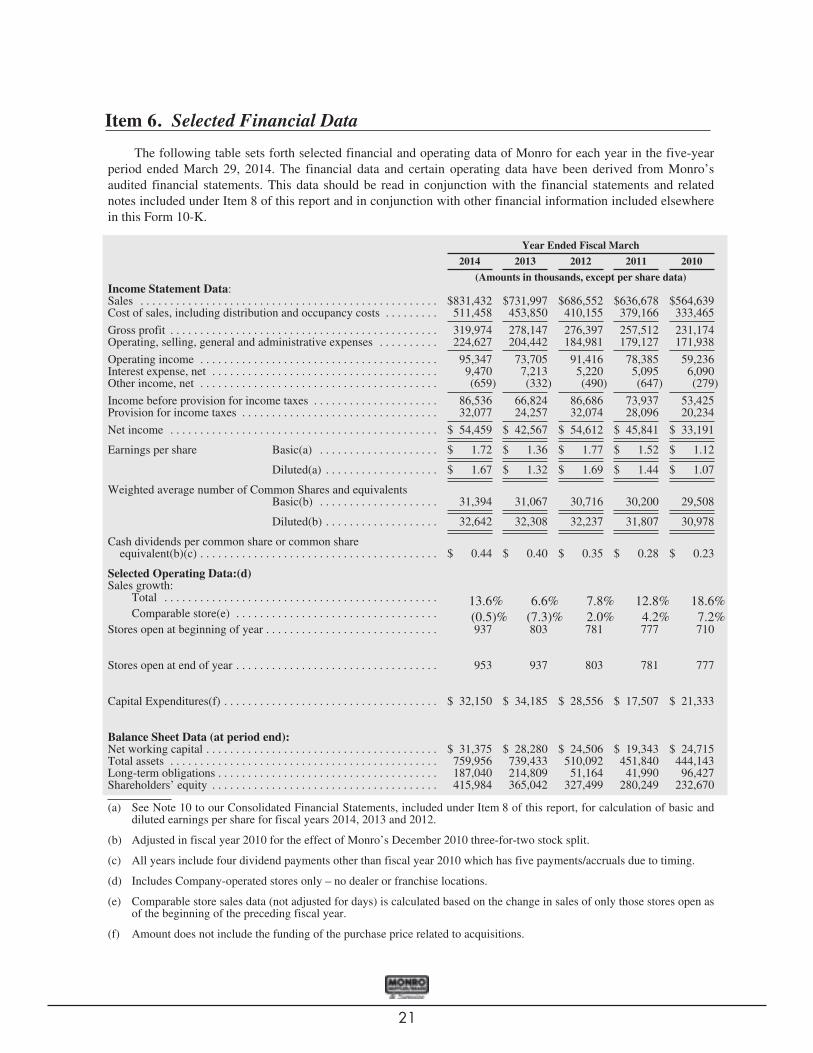

Fiscal Year End – March

2014 2013 % change

Sales .............................................................. $831,432 ...................... $731,997 ................................13.6%

Gross Profit ................................................... $319,974 ...................... $278,147 ................................15.0%

Net Income ..................................................... $54,459 ........................ $42,567 ................................27.9%

Earnings Per Share – Diluted ............................. $1.67 ............................ $1.32 ................................26.5%

Total Assets ................................................... $759,956 ...................... $739,433 ..................................2.8%

Shareholders’ Equity .................................... $415,984 ...................... $365,042 ................................14.0%

Number of Company-Operated Stores ................ 953 ............................... 937 ..................................1.7%

Return on Shareholders’ Equity ..........................14% ..............................12%

Comparable Store Sales Growth ....................... (.5%) .......................... (7.3%)

8508258007757507257006756506256005755505255004754504254003753503253002752502252001751501251007550250

2010 2011 2012 2013 20142013

$831,432

1000950900850800750700650600550500450400350300250200150100500

2010 20112010 2012 2013 20142011 2012 2013 2014

953

1.801.601.401.201.00.80.60.40.20

2010 2011 2012 2013 2014

$1.67

ANNUALSALES

(millions of dollars)

EARNiNgSPER SHARE –

DiLUTED(dollars per share)

NUMBEROF STORES

(stores open and operating at end

of fiscal year)

ABOUT THE COMPANY | MARKET AREAS | FiNANCiAL HigHLigHTS | LETTER TO OUR SHAREHOLDERS ABOUT THE COMPANY | MARKET AREAS | FiNANCiAL HigHLigHTS | LETTER TO OUR SHAREHOLDERS

Note: Earnings per share information has been adjusted to give retroactive effect to the three-for-two stock split paid in December 2010

1016834_Monro Annual Report_2014.indd 5 6/27/14 10:45 AM

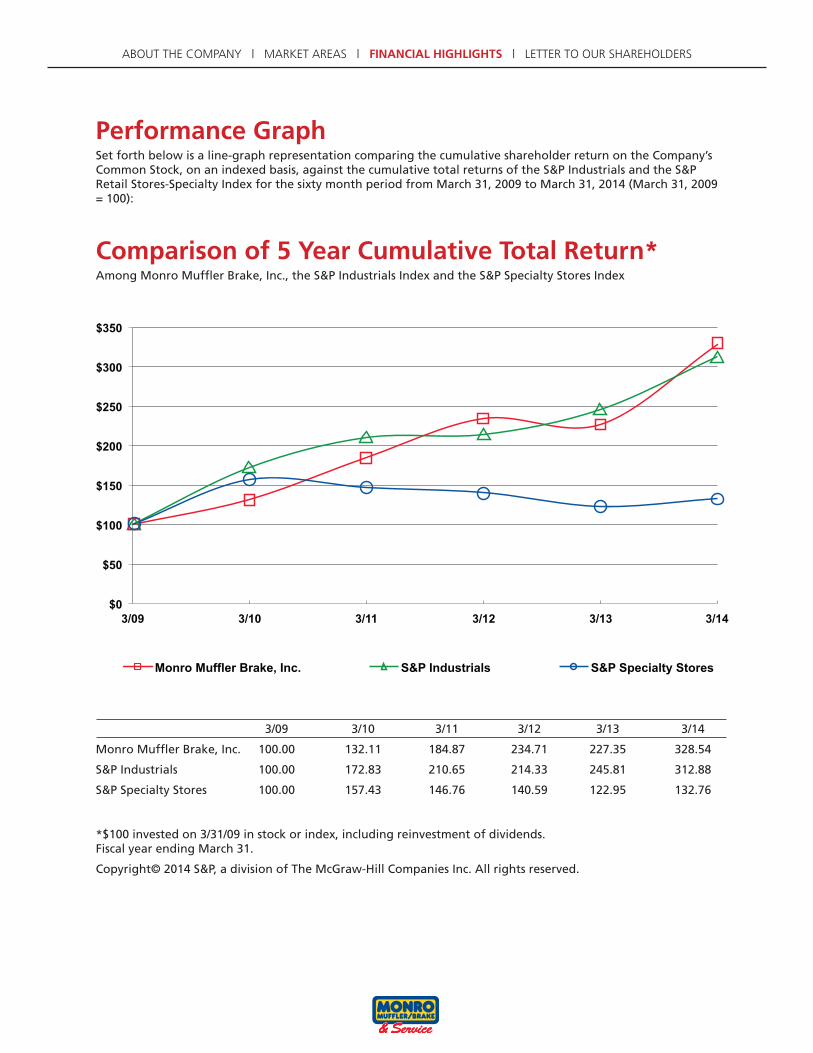

Performance graphSet forth below is a line-graph representation comparing the cumulative shareholder return on the Company’s Common Stock, on an indexed basis, against the cumulative total returns of the S&P Industrials and the S&P Retail Stores-Specialty Index for the sixty month period from March 31, 2009 to March 31, 2014 (March 31, 2009 = 100):

Comparison of 5 Year Cumulative Total Return*Among Monro Muffler Brake, Inc., the S&P Industrials Index and the S&P Specialty Stores Index

3/09 3/10 3/11 3/12 3/13 3/14

Monro Muffler Brake, Inc. 100.00 132.11 184.87 234.71 227.35 328.54

S&P Industrials 100.00 172.83 210.65 214.33 245.81 312.88

S&P Specialty Stores 100.00 157.43 146.76 140.59 122.95 132.76

*$100 invested on 3/31/09 in stock or index, including reinvestment of dividends. Fiscal year ending March 31.

Copyright© 2014 S&P, a division of The McGraw-Hill Companies Inc. All rights reserved.

Graph produced by Research Data Group, Inc. 4/7/2014

$0

$50

$100

$150

$200

$250

$300

$350

3/09 3/10 3/11 3/12 3/13 3/14

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN* Among Monro Muffler Brake, Inc., the S&P Industrials Index, and the S&P Specialty Stores Index

Monro Muffler Brake, Inc. S&P Industrials S&P Specialty Stores

*$100 invested on 3/31/09 in stock or index, including reinvestment of dividends. Fiscal year ending March 31.

Copyright© 2014 S&P, a division of The McGraw-Hill Companies Inc. All rights reserved.

ABOUT THE COMPANY | MARKET AREAS | FiNANCiAL HigHLigHTS | LETTER TO OUR SHAREHOLDERS ABOUT THE COMPANY | MARKET AREAS | FiNANCiAL HigHLigHTS | LETTER TO OUR SHAREHOLDERS

1016834_Monro Annual Report_2014.indd 6 6/27/14 10:45 AM

To Monro Muffler Brake, inc. Shareholders:

In fiscal 2014, we continued to leverage our competitive advantages to outperform the automotive service industry, delivering record sales and 27% earnings growth, while completing several acquisitions to drive future growth. We successfully increased traffic, expanded gross margins through lower product costs, carefully managed operating expenses, and drove strong sales and earnings contributions from recent acquisitions. These results, which are a testament to Monro’s unique business model and our team’s consistent execution of our strategy, contributed to a 42% increase in the Company’s stock price during fiscal 2014.

The continued growth of our business, along with our team’s hard work throughout fiscal 2014, has allowed us to extend our competitive advantages, further differentiating Monro from chains and independent operators, while also positioning us to attract automotive dealer customers. More specifically, our Company-owned and operated store network, service and tire store brand strategy, store density combined with geographic expansion in contiguous markets, low-cost operating model, Company-owned distribution network, effective direct marketing programs and the TRUST we have established with our customers uniquely position Monro to serve the ever-aging vehicle fleet and be the service provider of choice when consumers can no longer defer major repairs.

Fiscal 2014: growing Profitability

The Company’s strategy is focused on continuously improving our competitive position to grow sales and our industry-leading operating margins. In fiscal 2014, we achieved record sales of $831.4 million, representing year-over-year growth of $99.4 million, or 14%, over fiscal 2013. Robust sales from acquisitions completed in fiscal years 2013 and 2014 enabled us to overcome a .5% decrease in comparable store sales in a difficult consumer environment, as customers deferred purchases and traded down from higher cost automotive maintenance and repair purchases.

Despite the difficult macroeconomic environment, we serviced more customers as a result of 1% increases in comparable store oil change and tire units, demonstrating that our position as a trusted service provider remains strong and we are maintaining market share. Comparable store sales also increased approximately 1% for brakes, exhaust and shocks, offset by lower comparable store sales in maintenance service and tires. Comparable store tire unit sales were up approxi-mately 1%, however, comparable store tire sales in dollars declined 1% due primarily to consumers continuing to trade down from higher priced tires to more value-oriented options. While this reduced our reported overall comparable store

sales by approximately 1% in fiscal 2014 – importantly, we were able to grow tire margins and gross profit dol-lars during the year, outperforming the competition.

Gross profit for fiscal 2014 increased to $320.0 million, or 38.5% of sales, as compared with $278.1 million, or 38.0% of sales, for fiscal 2013. The increase as a percentage of sales was due to reduced product costs – particularly tires, payroll control and leverage of fixed distribution and occupancy costs, which more than offset a sales mix shift to the lower margin tire category reflecting the higher tire sales mix of our recent acquisitions. Because tires are our largest product category, we have extraordinary focus on identifying cost savings opportunities –including taking advantage of our 25% growth in units in fiscal 2014 to

shift our buying to manufacturers offering the best costs. We also continue to take advantage of more significant declines in the cost of direct import private label tires compared to branded tires. In fact, we saw the mix of direct imports increase to 32% of total tire units sold for fiscal 2014 versus mid-20s in fiscal 2013, and mid-teens three years ago. We expect that we will get to a 40% mix of direct import tires in fiscal 2015, further improving our margins.

ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS

1016834_Monro Annual Report_2014.indd 7 6/27/14 10:45 AM

Operating expenses for fiscal 2014 were $224.6 million, or 27.0% of sales, as compared with $204.4 million, or 27.9% of sales, for fiscal 2013. The year-over-year decrease in operating expenses as a percentage of sales reflects our ongoing focused cost control and leverage of our expense structure on higher sales. For the year, we reduced operating expenses by approximately $2.2 million, excluding the increase in operating expenses related to the stores acquired in fiscal 2014 and 2013.

In fiscal 2014, we generated significant earnings growth despite slightly negative comparable store sales, due to lower product costs, our company-owned distribution network, improvements in the performance of recent acquisitions and disciplined cost control. Net income for fiscal 2014 increased 28% to $54.5 million from $42.6 million in the prior year. Diluted earnings per share increased 27% to $1.67, as compared to diluted earnings per share of $1.32 in fiscal 2013, outpacing the competition.

growing Competitive Advantage

Coming off a year of significant acquisitions in fiscal 2013 which added to the strength and scale of our business, in fiscal 2014, we leveraged and extended our competitive advantages to outperform the automotive service industry. We believe our competitive advantages include our company-owned and operated store network, two-brand strategy, store density combined with geographic expansion in contiguous markets, low cost operating model, Company-owned distribution network, effective direct marketing programs and the TRUST we have established with our customers. In addition, Monro continues to be the low-cost operator in our industry, and our cost control initiatives and increasing scale have further extended our cost advantage.

Our fiscal 2014 acquisitions built on the significant increase in store count we experienced in fiscal 2013, and increased our store density in Maryland, Kentucky and Delaware. Greater market density brings superior customer convenience, as well as lower cost of product, logistics and marketing on a per store and percentage of sales basis. We have the ability to share inventory across stores, increasing usage of parts supplied through our low-cost supply chain, reducing our overall inventory levels and increasing inventory turnover. Our systems facilitate this cost advantage as every store can see the inventory of the 14 closest stores, giving us 15 chances to source a part or tire from our supply chain instead of paying up to double that cost to source it from a local supplier. Overall, greater store density increases our efficiencies, leading to greater profitability…and a lasting competitive advantage.

Monro’s lower occupancy costs are another excellent example of the Company’s effectiveness at creating cost advantages in key areas of our business, enhancing profitability and maximizing cash flow to reinvest in the growth of the business. We own approximately 30% of our store locations, a greater percentage than most competitors, lowering the Company’s long-term occupancy costs. Additionally, Monro’s lease costs are generally lower than most competitors by 1% to 3% of sales. This real estate cost advantage is significant and will benefit Monro for many years to come.

In the past fiscal year, we also remained focused on making it easier for our store teams to meet customer needs while controlling payroll costs. We continued to successfully leverage technology embedded in our point-of-sale system to more efficiently staff our stores in line with customer traffic patterns. This system advantage, combined with our team’s ongoing superior store execution, has resulted in a 65% increase in company-wide labor productivity over the last 13 years. At the same time, we made investments in our owned warehousing and distribution systems to achieve both cost and service advantages for our increasing scale and high-density tire and service store presence.

Combined with our store density, our direct marketing approach has always positioned us strongly with our customers while allowing us to grow at a lower advertising cost to sales ratio than our competitors. With our expansion of digital marketing, we are targeting not only a continued cost advantage, but a sales generation advantage as well. To accomplish this, we share marketing cost and sales category learning across store formats and brands. Also, as customers move to

ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS

1016834_Monro Annual Report_2014.indd 8 6/27/14 10:45 AM

mobile technology, so have we. During fiscal 2014, we launched enhanced mobile websites and saw an average 25% increase in overall online sales activity (i.e. coupon prints, online appointments and phone calls to stores from website visits). The share of total website visits on mobile devices climbed to 32% in fiscal 2014 from approximately 10% as recently as fiscal 2012. With our acquisitions of strong brands, we are focused on improving individual brand positioning and messaging, with new websites and marketing database programs that will allow us to do so cost effectively.

At the same time that we effectively drive traffic to our stores at better costs than competitors, we also make sure to deliver a superior store experience with a robust customer satisfaction program. Our company-owned store model allows us to provide a greater level of consistency in the service experience, particularly compared to franchise operators. In the high-service, low-trust business of taking care of consumers’ vehicles, we are pleased that our satisfaction rating exceeds 95% in (1) explaining needed repairs to our customers, (2) completing those repairs right the first time and (3) completing those repairs on time.

growing Through Acquisitions

Market pressures on operators in our industry who do not have our competitive advantages continue to provide strong acquisition opportunities. More specifically, the choppy sales environment we experienced in fiscal 2014 contributed to our ability to complete three acquisitions at attractive prices during the year as well as reach our highest-ever level of signed non-disclosure agreements with potential acquisition targets heading into fiscal 2015.

During fiscal 2013 and 2014, we completed 11 acquisitions totaling 159 stores and 30% annualized sales growth. Nine of these acquisitions increased store density in existing markets while two allowed us to expand our geographic footprint in new contiguous markets, as we entered Wisconsin, Kentucky and Tennessee. The majority of these acquisitions were completed in fiscal 2013 and those stores contributed fiscal 2014 earnings per share ahead of our original estimates of $.15 to $.20 earnings per share.

Our ability to complete acquisitions at attractive prices is due to our superior experience in completing and integrating acquisitions, our two-store brand strategy and our financial strength. Importantly, these factors represent a distinct competitive advantage that underpins a key component of our growth strategy. Over the past 10 years, we have completed 24 acquisitions by applying highly developed internal processes and methods of working with sellers that allow us to complete deals more efficiently than others as opportunities arise, and to meet or exceed our operating plans post-transaction. In addition, any location redundancy that may make an acquisition target less attractive to others, in fact, benefits Monro as a result of our two-store brand strategy and the leverage we achieve through store density. Finally, our strong balance sheet, significant availability on our credit facility and borrowing rate of approximately 1.5% allow us to execute our acquisition strategy at a low cost.

Continuing Our Positive Momentum

In fiscal 2015, we will continue to focus on growing comparable store sales, driving increased customer traffic through oil changes and tires by capitalizing on our direct marketing improvements, expanding gross margins through lower product

ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS

1016834_Monro Annual Report_2014.indd 9 6/27/14 10:45 AM

costs and our low cost supply chain, and carefully managing operating expenses. At the same time, we will drive strong sales and earnings contributions from recent acquisitions, while also capitalizing on opportunities to complete additional acquisitions at attractive prices. We are optimistic that the harsh weather conditions experienced this past winter will continue to help drive sales through the spring and summer and should serve as a tailwind for the reversal of customers’ increased deferrals. Based primarily on the continued reduction of product costs we expect in fiscal 2015 and cost control measures that we have in place, including improvements in payroll and marketing efficiency, we expect to be able to deliver earnings growth after a 1% comparable store sales increase, a lower threshold than the 2% to 2.5% comparable store sales increase we have needed to achieve in prior years.

Given our expectation for a continued choppy sales environment in fiscal 2015, we see a greater opportunity for attractive acquisition opportunities in the marketplace than we have historically. We have already signed definitive agreements to acquire 21 stores generating approximately $16 million in annualized sales, which closed in the first quarter of fiscal 2015. Nineteen of the stores are located in Michigan, a new state for the Company, and the other stores fill in an existing market. These acquisitions provide additional upside because we purchased the real estate for 19 locations, which generally drives higher levels of profitability. Their sales represent approximately 2% of total Monro sales, adding to our 30% acquisition growth achieved in the 11 deals closed in fiscal 2013 and 2014.

On a broader note, the key industry trends that have driven our business over the last decade remain in place. There are 245 million cars on the road in the U.S. that are getting older and the number of service bays is declining. We expect consumers to continue to drive and maintain vehicles longer. This will continue to expand our “sweet spot” for age of vehicles serviced. In fiscal 2014, vehicles over 12 years old represented more than 20% of our traffic, up from mid-teens in fiscal 2010, and the average sales ticket for these vehicles is consistent with our overall average. We believe the Do-It-For-Me (DIFM) service sector will continue to take market share from the Do-It-Yourself (DIY) segment, as vehicle repairs are becoming increasingly complex, the population is aging and younger consumers have limited DIY capabilities. As is true for all retailers, if gas prices or economic developments reduce consumer spending power or confidence, our sales could be negatively impacted. However, we do have the advantage of providing products and services that are a “need” rather than a “want,” especially for aging vehicles. More than two years into an extended deferral cycle, we expect that consumers will begin to reduce their deferrals of higher ticket maintenance, repair and tire purchases and that their TRUST in Monro will bring them back into our stores when that work must be done. The last period we experienced extended customer deferrals – fiscal years 2007 and 2008 – were followed by our ability to generate average comparable store sales growth of 6% in fiscal years 2009 to 2011. Additionally, the increasing number of owners of target independent tire dealers who are at or nearing retirement age will continue to drive acquisition opportunities. We believe these key trends will continue to benefit our business going forward.

In summary, our long-term confidence in the business and outlook for our industry remain very positive. We will continue to leverage our growth and extend our many strategic advantages to increase both sales and profits. As a reflection of the Board’s continued confidence in our long-term strategic plan and financial prospects, we are pleased to have announced on May 22, 2014 that the Board of Directors approved an 18% increase in the Company’s cash dividend for the first quarter of fiscal 2015, to $.13 per share, representing an annual rate of $.52 per share, and the ninth consecutive annual increase in our dividend. This increase is a reflection of Monro’s financial strength and flexibility, which allows us to invest in continued growth while returning additional value directly to our shareholders. We believe we have a long runway of growth ahead of us.

As always, I also want to thank each of our 6,100 employees, who continue to work hard to execute our strategy and attract new customers while maintaining the trust of our loyal customers, bringing them back into our stores time and again by delivering an exceptional customer experience. We are honored to work on behalf of our stockholders, and thank you for your ongoing support.

Best Regards,

John W. Van Heel President and Chief Executive Officer

ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS ABOUT THE COMPANY | MARKET AREAS | FINANCIAL HIGHLIGHTS | LETTER TO OUR SHAREHOLDERS

1016834_Monro Annual Report_2014.indd 10 6/27/14 10:45 AM

This page intentionally left blank.

1016834_Monro Annual Report_2014.indd 11 6/27/14 10:45 AM

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K(MARK ONE)È ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934For Fiscal Year Ended March 29, 2014

OR‘ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934Commission File Number 0-19357

MONROMUFFLER BRAKE, INC.(Exact name of registrant as specified in its charter)

New York 16-0838627(State of incorporation) (I.R.S. Employer Identification No.)

200 Holleder Parkway,Rochester, New York 14615

(Address of principal executive offices) (Zip code)

Registrant’s telephone number, including area code:(585) 647-6400

Securities registered pursuant to Section 12(b) of the Act:Common Stock, par value $.01 per share

Name of each exchange on which registered: The NASDAQ Stock Market

Securities registered pursuant to Section 12(g) of the Act:NONE

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the SecuritiesAct. Yes È No ‘

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of theAct. Yes ‘ No È

Indicate by check mark if the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the SecuritiesExchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file suchreports), and (2) has been subject to such filing requirements for the past 90 days. Yes È No ‘

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, everyInteractive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months(or for such shorter period that the registrant was required to submit and post such files). Yes È No ‘

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, andwill not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by referencein Part III of this Form 10-K or any amendment to this Form 10-K. ‘

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or asmaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “small reporting company” inRule 12b-2 of the Exchange Act.Large Accelerated Filer È Accelerated Filer ‘ Non-Accelerated Filer ‘ Smaller Reporting Company ‘

(Do not check if a smaller reporting company)Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange

Act). Yes ‘ No ÈThe aggregate market value of the voting stock held by non-affiliates of the registrant, computed by reference to the closing

price as of the last business day of the registrant’s most recently completed second fiscal quarter, September 28, 2013, wasapproximately $1,386,400,000.

As of May 9, 2014, 31,510,479 shares of the registrant’s Common Stock, par value $.01 per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the registrant’s definitive proxy statement (to be filed pursuant to Regulation 14A) for the 2014 Annual Meeting ofShareholders (the “Proxy Statement”) are incorporated by reference into Part III hereof.

PART IFORM 10-K

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page i

1

PART IPART IItem 1. Business

GENERAL

Monro Muffler Brake, Inc. (“Monro”, the “Company”, “we”, “us”, or “our”) is a chain of 953 Company-operated stores (as of March 29, 2014), three franchised locations and 14 dealer-operated stores providingautomotive undercar repair and tire services in the United States. At March 29, 2014, Monro operated Companystores in 22 states, including New York, Pennsylvania, Ohio, Connecticut, Massachusetts, West Virginia,Virginia, Maryland, Vermont, New Hampshire, New Jersey, North Carolina, South Carolina, Indiana, RhodeIsland, Delaware, Maine, Illinois, Missouri, Wisconsin, Tennessee and Kentucky primarily under the names“Monro Muffler Brake & Service”, “Tread Quarters Discount Tire”, “Mr. Tire”, “Autotire Car Care Center”,“Tire Warehouse”, “Tire Barn Warehouse” and “Ken Towery’s Tire & Auto Care” (together, the “CompanyStores”). Company Stores typically are situated in high-visibility locations in suburban areas and small towns, aswell as in major metropolitan areas. Company Stores serviced approximately 5.3 million vehicles in fiscal 2014.(References herein to fiscal years are to the Company’s year ended fiscal March [e.g., references to “fiscal 2014”are to the Company’s fiscal year ended March 29, 2014].)

The predecessor to the Company was founded by Charles J. August in 1957 as a Midas Muffler franchise inRochester, New York, specializing in mufflers and exhaust systems. The Company was incorporated in the Stateof New York in 1959. In 1966, we discontinued our affiliation with Midas Muffler, and began to diversify into afull line of undercar repair services. An investor group led by Peter J. Solomon and Donald Glickman purchaseda controlling interest in the Company in July 1984. At that time, Monro operated 59 stores, located primarily inupstate New York, with approximately $21 million in sales in fiscal 1984. Since 1984, we have continued ourgrowth and have expanded our marketing area to include 22 additional states (including dealer locations).

In December 1998, Monro appointed Robert G. Gross as President and Chief Executive Officer, who beganfull-time responsibilities on January 1, 1999. Effective October 1, 2012, Mr. Gross assumed the role of ExecutiveChairman and John W. Van Heel was appointed Chief Executive Officer.

The Company’s principal executive offices are located at 200 Holleder Parkway, Rochester, New York14615, and our telephone number is (585) 647-6400.

Monro provides a broad range of services on passenger cars, light trucks and vans for brakes; mufflers andexhaust systems; and steering, drive train, suspension and wheel alignment. Monro also provides other productsand services, including tires and routine maintenance services, including state inspections. Monro specializes inthe repair and replacement of parts which must be periodically replaced as they wear out. Normal wear on theseparts generally is not covered by new car warranties. Monro typically does not perform under-the-hood repairservices except for oil change services, various “flush and fill” services and some minor tune-up services. Monrodoes not sell parts or accessories to the do-it-yourself market.

All of the Company’s stores, except Tire Warehouse and Tire Barn Warehouse stores, provide the servicesdescribed above. Tire Warehouse and Tire Barn Warehouse stores only sell tires and tire related services andalignments. However, a growing number of our stores are more specialized in tire replacement and service and,accordingly, have a higher mix of sales in the tire category. These stores are described below as tire stores,whereas the majority of our stores are described as service stores. (See additional discussion under “OperatingStrategy”.) At March 29, 2014, there were 532 stores designated as service stores and 421 as tire stores.

1

Item 1. Business� GENERAL

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page 1

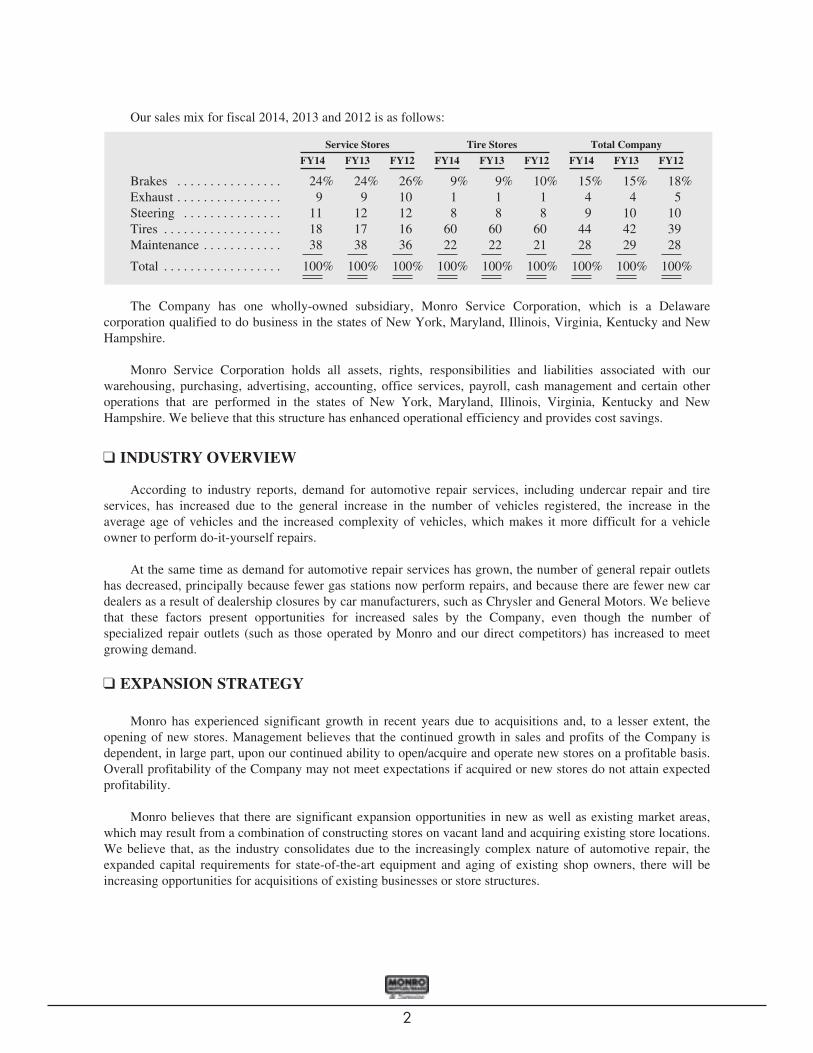

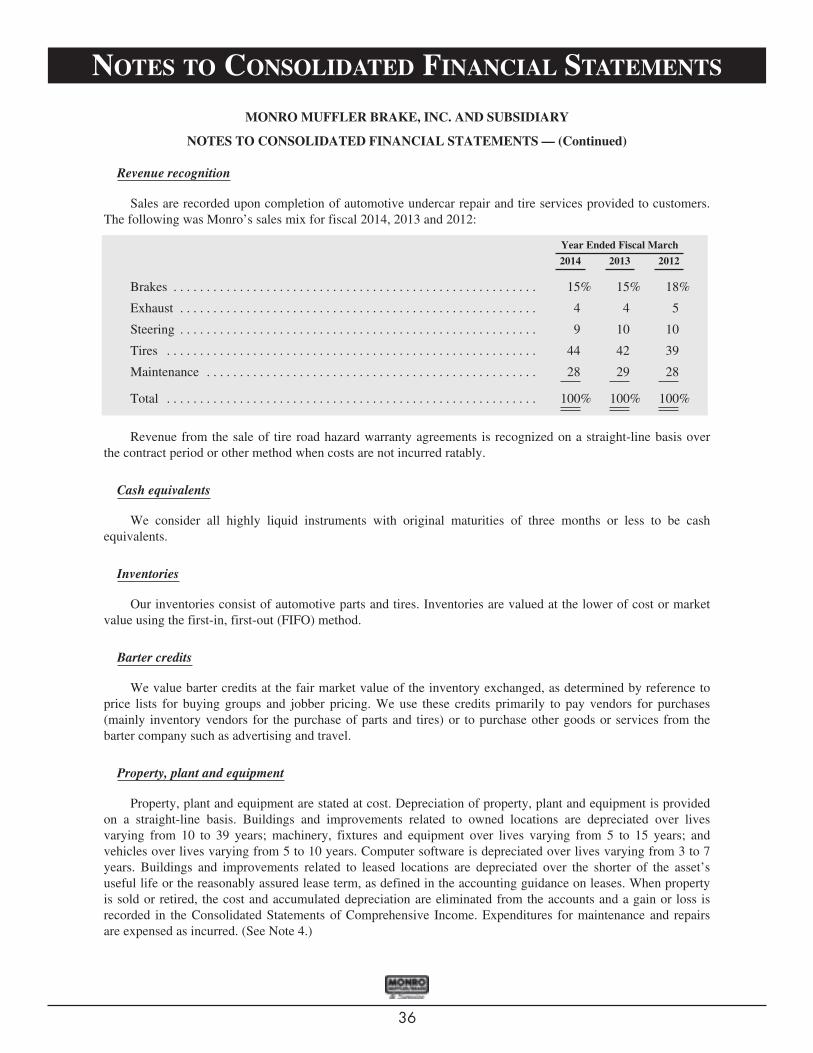

Our sales mix for fiscal 2014, 2013 and 2012 is as follows:

Service Stores Tire Stores Total Company

FY14 FY13 FY12 FY14 FY13 FY12 FY14 FY13 FY12

Brakes . . . . . . . . . . . . . . . . 24% 24% 26% 9% 9% 10% 15% 15% 18%Exhaust . . . . . . . . . . . . . . . . 9 9 10 1 1 1 4 4 5Steering . . . . . . . . . . . . . . . 11 12 12 8 8 8 9 10 10Tires . . . . . . . . . . . . . . . . . . 18 17 16 60 60 60 44 42 39Maintenance . . . . . . . . . . . . 38 38 36 22 22 21 28 29 28

Total . . . . . . . . . . . . . . . . . . 100% 100% 100% 100% 100% 100% 100% 100% 100%

The Company has one wholly-owned subsidiary, Monro Service Corporation, which is a Delawarecorporation qualified to do business in the states of New York, Maryland, Illinois, Virginia, Kentucky and NewHampshire.

Monro Service Corporation holds all assets, rights, responsibilities and liabilities associated with ourwarehousing, purchasing, advertising, accounting, office services, payroll, cash management and certain otheroperations that are performed in the states of New York, Maryland, Illinois, Virginia, Kentucky and NewHampshire. We believe that this structure has enhanced operational efficiency and provides cost savings.

INDUSTRY OVERVIEW

According to industry reports, demand for automotive repair services, including undercar repair and tireservices, has increased due to the general increase in the number of vehicles registered, the increase in theaverage age of vehicles and the increased complexity of vehicles, which makes it more difficult for a vehicleowner to perform do-it-yourself repairs.

At the same time as demand for automotive repair services has grown, the number of general repair outletshas decreased, principally because fewer gas stations now perform repairs, and because there are fewer new cardealers as a result of dealership closures by car manufacturers, such as Chrysler and General Motors. We believethat these factors present opportunities for increased sales by the Company, even though the number ofspecialized repair outlets (such as those operated by Monro and our direct competitors) has increased to meetgrowing demand.

EXPANSION STRATEGY

Monro has experienced significant growth in recent years due to acquisitions and, to a lesser extent, theopening of new stores. Management believes that the continued growth in sales and profits of the Company isdependent, in large part, upon our continued ability to open/acquire and operate new stores on a profitable basis.Overall profitability of the Company may not meet expectations if acquired or new stores do not attain expectedprofitability.

Monro believes that there are significant expansion opportunities in new as well as existing market areas,which may result from a combination of constructing stores on vacant land and acquiring existing store locations.We believe that, as the industry consolidates due to the increasingly complex nature of automotive repair, theexpanded capital requirements for state-of-the-art equipment and aging of existing shop owners, there will beincreasing opportunities for acquisitions of existing businesses or store structures.

2

2

� INDUSTRY OVERVIEW

� EXPANSION STRATEGY

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page 2

3

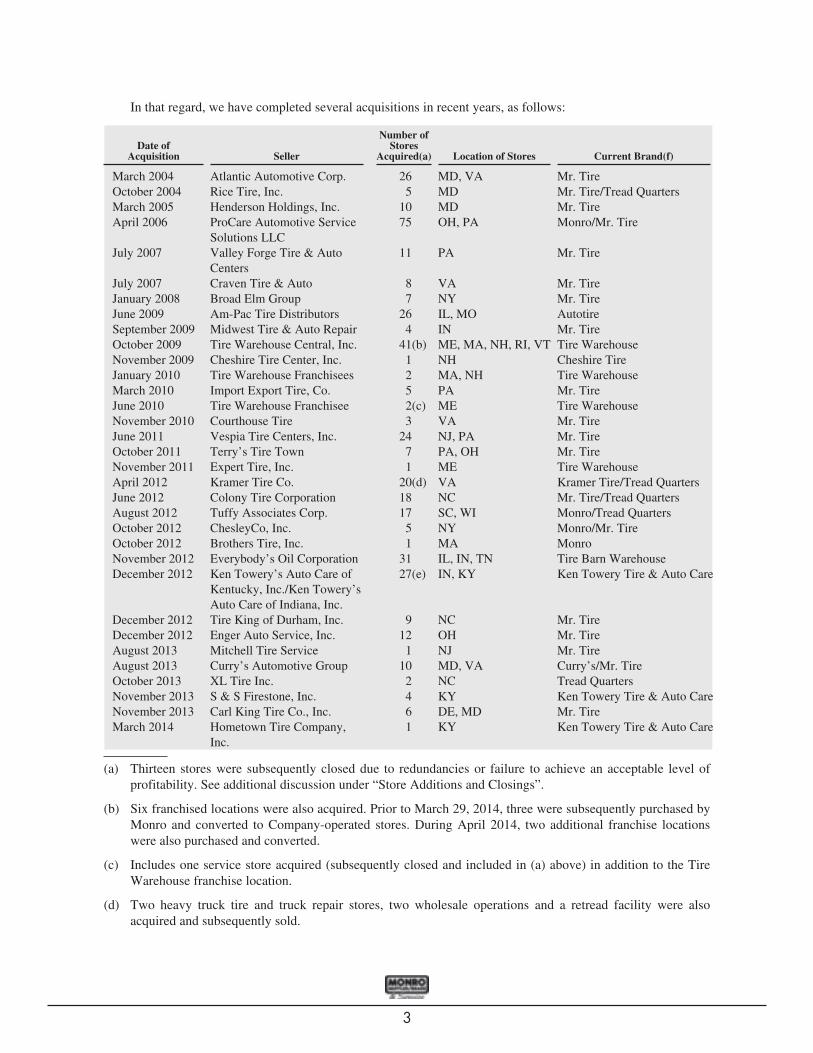

In that regard, we have completed several acquisitions in recent years, as follows:

Date ofAcquisition Seller

Number ofStores

Acquired(a) Location of Stores Current Brand(f)

March 2004 Atlantic Automotive Corp. 26 MD, VA Mr. TireOctober 2004 Rice Tire, Inc. 5 MD Mr. Tire/Tread QuartersMarch 2005 Henderson Holdings, Inc. 10 MD Mr. TireApril 2006 ProCare Automotive Service

Solutions LLC75 OH, PA Monro/Mr. Tire

July 2007 Valley Forge Tire & AutoCenters

11 PA Mr. Tire

July 2007 Craven Tire & Auto 8 VA Mr. TireJanuary 2008 Broad Elm Group 7 NY Mr. TireJune 2009 Am-Pac Tire Distributors 26 IL, MO AutotireSeptember 2009 Midwest Tire & Auto Repair 4 IN Mr. TireOctober 2009 Tire Warehouse Central, Inc. 41(b) ME, MA, NH, RI, VT Tire WarehouseNovember 2009 Cheshire Tire Center, Inc. 1 NH Cheshire TireJanuary 2010 Tire Warehouse Franchisees 2 MA, NH Tire WarehouseMarch 2010 Import Export Tire, Co. 5 PA Mr. TireJune 2010 Tire Warehouse Franchisee 2(c) ME Tire WarehouseNovember 2010 Courthouse Tire 3 VA Mr. TireJune 2011 Vespia Tire Centers, Inc. 24 NJ, PA Mr. TireOctober 2011 Terry’s Tire Town 7 PA, OH Mr. TireNovember 2011 Expert Tire, Inc. 1 ME Tire WarehouseApril 2012 Kramer Tire Co. 20(d) VA Kramer Tire/Tread QuartersJune 2012 Colony Tire Corporation 18 NC Mr. Tire/Tread QuartersAugust 2012 Tuffy Associates Corp. 17 SC, WI Monro/Tread QuartersOctober 2012 ChesleyCo, Inc. 5 NY Monro/Mr. TireOctober 2012 Brothers Tire, Inc. 1 MA MonroNovember 2012 Everybody’s Oil Corporation 31 IL, IN, TN Tire Barn WarehouseDecember 2012 Ken Towery’s Auto Care of

Kentucky, Inc./Ken Towery’sAuto Care of Indiana, Inc.

27(e) IN, KY Ken Towery Tire & Auto Care

December 2012 Tire King of Durham, Inc. 9 NC Mr. TireDecember 2012 Enger Auto Service, Inc. 12 OH Mr. TireAugust 2013 Mitchell Tire Service 1 NJ Mr. TireAugust 2013 Curry’s Automotive Group 10 MD, VA Curry’s/Mr. TireOctober 2013 XL Tire Inc. 2 NC Tread QuartersNovember 2013 S & S Firestone, Inc. 4 KY Ken Towery Tire & Auto CareNovember 2013 Carl King Tire Co., Inc. 6 DE, MD Mr. TireMarch 2014 Hometown Tire Company,

Inc.1 KY Ken Towery Tire & Auto Care

(a) Thirteen stores were subsequently closed due to redundancies or failure to achieve an acceptable level ofprofitability. See additional discussion under “Store Additions and Closings”.

(b) Six franchised locations were also acquired. Prior to March 29, 2014, three were subsequently purchased byMonro and converted to Company-operated stores. During April 2014, two additional franchise locationswere also purchased and converted.

(c) Includes one service store acquired (subsequently closed and included in (a) above) in addition to the TireWarehouse franchise location.

(d) Two heavy truck tire and truck repair stores, two wholesale operations and a retread facility were alsoacquired and subsequently sold.

3

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page 3

(e) One wholesale operation was also acquired and is operating under the America’s Best Tires name.

(f) In this table, “Monro” refers to the brand of “Monro Brake/Tires” or “Monro Muffler Brake & Service”, notthe corporation.

The total number of stores that we operate in BJ’s Wholesale Clubs is 34 at March 29, 2014.

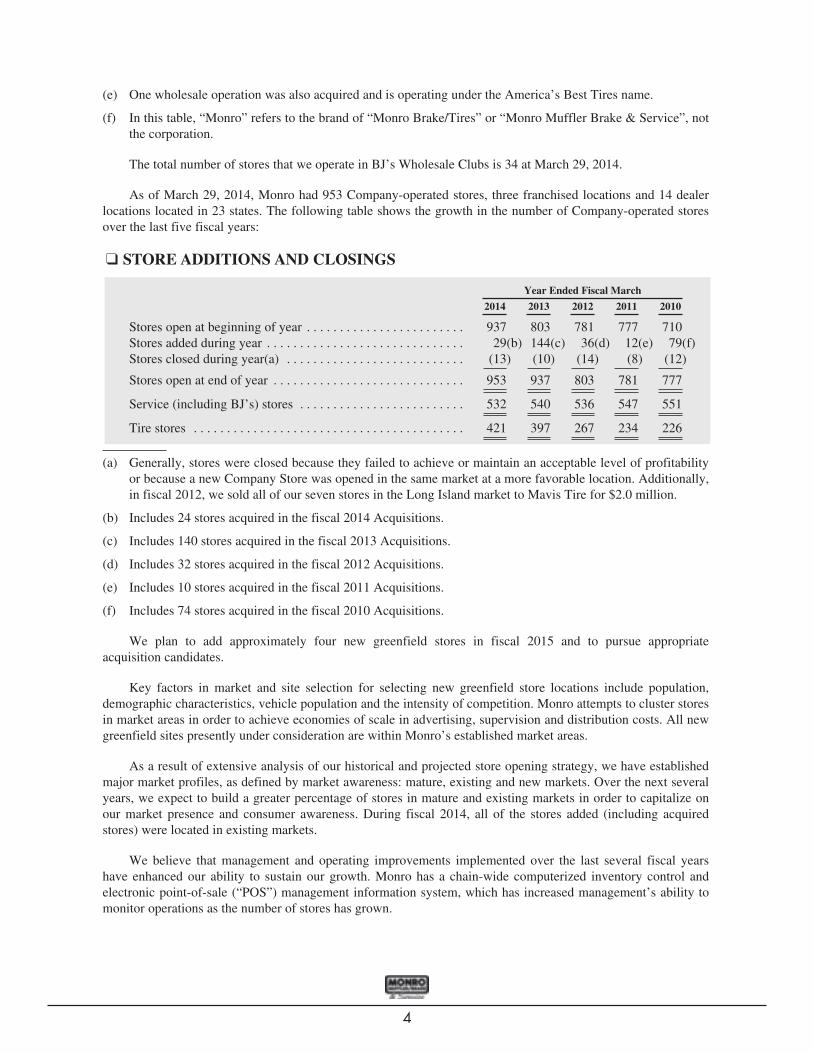

As of March 29, 2014, Monro had 953 Company-operated stores, three franchised locations and 14 dealerlocations located in 23 states. The following table shows the growth in the number of Company-operated storesover the last five fiscal years:

STORE ADDITIONS AND CLOSINGS

Year Ended Fiscal March

2014 2013 2012 2011 2010

Stores open at beginning of year . . . . . . . . . . . . . . . . . . . . . . . . 937 803 781 777 710Stores added during year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29(b) 144(c) 36(d) 12(e) 79(f)Stores closed during year(a) . . . . . . . . . . . . . . . . . . . . . . . . . . . (13) (10) (14) (8) (12)

Stores open at end of year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 953 937 803 781 777

Service (including BJ’s) stores . . . . . . . . . . . . . . . . . . . . . . . . . 532 540 536 547 551

Tire stores . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 421 397 267 234 226

(a) Generally, stores were closed because they failed to achieve or maintain an acceptable level of profitabilityor because a new Company Store was opened in the same market at a more favorable location. Additionally,in fiscal 2012, we sold all of our seven stores in the Long Island market to Mavis Tire for $2.0 million.

(b) Includes 24 stores acquired in the fiscal 2014 Acquisitions.

(c) Includes 140 stores acquired in the fiscal 2013 Acquisitions.

(d) Includes 32 stores acquired in the fiscal 2012 Acquisitions.

(e) Includes 10 stores acquired in the fiscal 2011 Acquisitions.

(f) Includes 74 stores acquired in the fiscal 2010 Acquisitions.

We plan to add approximately four new greenfield stores in fiscal 2015 and to pursue appropriateacquisition candidates.

Key factors in market and site selection for selecting new greenfield store locations include population,demographic characteristics, vehicle population and the intensity of competition. Monro attempts to cluster storesin market areas in order to achieve economies of scale in advertising, supervision and distribution costs. All newgreenfield sites presently under consideration are within Monro’s established market areas.

As a result of extensive analysis of our historical and projected store opening strategy, we have establishedmajor market profiles, as defined by market awareness: mature, existing and new markets. Over the next severalyears, we expect to build a greater percentage of stores in mature and existing markets in order to capitalize onour market presence and consumer awareness. During fiscal 2014, all of the stores added (including acquiredstores) were located in existing markets.

We believe that management and operating improvements implemented over the last several fiscal yearshave enhanced our ability to sustain our growth. Monro has a chain-wide computerized inventory control andelectronic point-of-sale (“POS”) management information system, which has increased management’s ability tomonitor operations as the number of stores has grown.

4

4

� STORE ADDITIONS AND CLOSINGS

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page 4

5

We have customized the POS system to specific service and tire store requirements and deploy theappropriate version in each type of store. Being Windows-based, the system has simplified training of newemployees. Additionally, the system includes the following:

• Electronic mail and electronic cataloging, which allows store managers to electronically research thespecific parts needed for the make and model of the car being serviced;

• Electronic repair manuals that allow for instant access to a single source of accurate, up to date, originalequipment manufacturer-direct diagnosis, repair and maintenance information;

• Software which contains data that mirrors the scheduled maintenance requirements in vehicle owners’manuals, specifically by make, model, year and mileage for every major automobile brand. Managementbelieves that this software facilitates the presentation and sale of scheduled maintenance services tocustomers;

• Streamlining of estimating and other processes;

• Graphic catalogs;

• A feature which facilitates tire searches by size;

• Direct mail support;

• Appointment scheduling;

• Customer service history;

• A thermometer graphic which guides store managers on the profitability of each job;

• The ability to view inventory of up to the closest 14 stores or warehouse; and

• Expanded monitoring of price changes. This requires more specificity on the reason for a discount,which management believes helps to control discounting.

Enhancements will continue to be made to the POS system annually in an effort to increase efficiency,improve the quality and timeliness of store reporting and enable us to better serve our customers.

The financing to open a new greenfield service store location may be accomplished in one of three ways: astore lease for the land and building (in which case, land and building costs will be financed primarily by thelessor), a land lease with the building constructed by Monro (with building costs paid by Monro), or a landpurchase with the building constructed by Monro. In all three cases, for service stores, each new store also willrequire approximately $200,000 for equipment (including a POS system and a truck) and approximately $55,000in inventory. Because we generally do not extend credit to our customers, stores generate almost no receivablesand a new store’s actual net working capital investment is nominal. Total capital required to open a newgreenfield service store ranges, on average, from $350,000 to $950,000 depending on the location and which ofthe three financing methods is used. In general, tire stores are larger and have more service bays than Monro’straditional service stores and, as a result, construction costs are at the high end of the range of new storeconstruction costs. Total capital required to open a new greenfield tire (land and building leased) location costs,on average, approximately $600,000, including $225,000 for equipment and $150,000 for inventory. In instanceswhere Monro acquires an existing business, it may pay additional amounts for intangible assets such as customerlists, covenants not-to-compete, trade names and goodwill, but generally will pay less per bay for equipment andreal property.

5

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page 5

At March 29, 2014, we leased the land and/or the building at approximately 71% of our store locations andowned the land and building at the remaining locations. Monro’s policy is to situate new stores in the bestlocations, without regard to the form of ownership required to develop the locations.

New service and tire stores, (excluding acquired stores and BJ’s locations), have average sales ofapproximately $384,000 and $1,015,000, respectively, in their first 12 months of operation, or $64,000 and$145,000, respectively, per bay.

STORE OPERATIONS

Store Format

The typical format for a Monro store is a free-standing building consisting of a sales area, fully-equippedservice bays and a parts/tires storage area. In BJ’s locations, Monro and BJ’s both operate counters in the salesarea, while Monro operates the service bay area. Most service bays are equipped with above-ground electricvehicle lifts. Generally, each store is located within 25 miles of a “key” store which carries approximately doublethe inventory of a typical store and serves as a mini-distribution point for slower moving inventory for otherstores in its area. Individual store sizes, number of bays and stocking levels vary greatly, even within the serviceand tire store groups, and are dependent primarily on the availability of suitable store locations, population,demographics and intensity of competition among other factors (See additional discussion under “StoreAdditions and Closings”). A summary of average store data for service and tire stores is presented below:

AverageNumberof Bays

AverageSquareFeet

AverageInventory

AverageNumberof StockKeeping

Units (SKUs)

Service stores (excluding BJ’s and ProCare) . . . . . . . 6 4,400 $100,000 2,700Tire stores (excluding Tire Warehouse and Tire BarnWarehouse stores) . . . . . . . . . . . . . . . . . . . . . . . . . . 7 6,500 $145,000 1,400

Data for the acquired ProCare service stores has been excluded because the stores’ stock rooms are smallerthan those in typical service stores and therefore, they generally carry approximately half the amount ofinventory of a typical service store.

Data for the Tire Warehouse and Tire Barn Warehouse stores has been excluded because these locationsprimarily install new tires and wheels and many perform alignments. Additionally, most Tire Warehouse storeshave no indoor service bays. The store building houses a waiting room, storage area and an area to mount andbalance tires on the car’s wheels once the wheels and tires have been removed from the car. Removal of old tiresand wheels from, and installation of new tires and wheels on, customers’ cars are performed outdoors under acarport. A growing number of Tire Warehouse stores have an indoor bay to perform alignments. The averageinventory carried by the Tire Warehouse and Tire Barn Warehouse stores is $236,000 per store.

Stores generally are situated in high-visibility locations in suburban areas, major metropolitan areas or smalltowns and offer easy customer access. The typical store is open from 7:30 a.m. to 7:00 p.m. on Monday throughFriday and from 7:30 a.m. to 6:00 p.m. on Saturday. A majority of store locations are also open Sundays from9:00 a.m. to 5:00 p.m.

Inventory Control and Management Information System

All Company Stores communicate daily with the central office and warehouse by computerized inventorycontrol and electronic POS management information systems, which enable us to collect sales and operationaldata on a daily basis, to adjust store pricing to reflect local conditions and to control inventory on a near “real-

6

6

� STORE OPERATIONS

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page 6

time” basis. Additionally, each store has access, through the POS system, to the inventory carried by up to the 14stores or warehouse nearest to it. Management believes that this feature improves customer satisfaction and storeproductivity by reducing the time required to locate out-of-stock parts and tires. It also improves profitabilitybecause it reduces the amount of inventory which must be purchased outside Monro from local vendors.

Quality Control and Warranties

To maintain quality control, we conduct audits to rate our employees’ telephone sales manner and theaccuracy of pricing information given.

We have a customer survey program to monitor customer attitudes toward service quality, friendliness,speed of service, and several other factors for each store. Customer concerns are addressed by customer serviceand field management personnel.

Monro uses a “Double Check for Accuracy Program” as part of our routine store procedures. This qualityassurance program requires that a technician and supervisory-level employee (or in certain cases, anothertechnician in tire stores) independently inspect a customer’s vehicle, diagnose and document the necessaryrepairs, and agree on an estimate before presenting it to a customer. This process is formally documented on thewritten estimate by store personnel.

We are an active member of the Automotive Maintenance & Repair Association (AMRA). AMRA is anorganization of automotive retailers, wholesalers and manufacturers which was established as part of an industry-wide effort to address the ethics and business practices of companies in the automotive repair industry throughthe Motorist Assurance Program (MAP). Participating companies commit to improving consumer confidence andtrust in the automotive repair industry by adopting “Uniform Inspection Communication Standards” (“UICS”)established by MAP. These “UICS” are available in our stores and serve to provide consistent recommendationsto customers in the diagnosis and repair of a vehicle.

We offer limited warranties on substantially all of the products and services that we provide. We believethat these warranties are competitive with industry practices and serve as a marketing tool to increase repeatbusiness at our stores.

Store Personnel and Training

Monro supervises store operations primarily through our Divisional Vice Presidents who oversee ZoneManagers who, in turn, oversee Market Managers. The typical service store is staffed by a Store Manager andfour to six technicians, one of whom serves as the Assistant Manager. The typical tire store, except TireWarehouse stores, is staffed by a Store Manager, an Assistant Manager and/or Service Manager, and four to eighttechnicians. Larger volume service and tire stores may also have one or two sales people. The higher staffinglevel at many tire stores is necessary to support their higher sales volume. Tire Warehouse stores are generallystaffed by a Store Manager and two to four technicians, one of whom serves as the Assistant Manager. All StoreManagers receive a base salary and Assistant Managers receive either hourly or salaried compensation. Inaddition, Store Managers and Assistant Managers may receive other compensation based on their store’scustomer relations, gross profit, labor cost controls, safety, sales volume and other factors via a monthly orquarterly bonus based on performance in these areas.

We believe that the ability to recruit and retain qualified technicians is an important competitive factor inthe automotive repair industry, which has historically experienced a high turnover rate. We make a concertedeffort to recruit individuals who will have a long-term commitment to the Company and offer an hourly ratestructure and additional compensation based on productivity; a competitive benefits package including health,dental, life and disability insurance; a 401(k)/profit-sharing plan; as well as the opportunity to advance within theCompany. Many of our Store Managers and Market Managers started with the Company as technicians.

7

7

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page 7

Many of our new technicians join the Company in their early twenties as trainees or apprentices. As theyprogress, many are promoted to technician and eventually master technician, the latter requiring ASEcertification in both brakes and suspension. We offer a tool purchase program through which trainee technicianscan acquire their own set of tools. We also will reimburse technicians for the cost of ASE certificationregistration fees and test fees and encourage all technicians to become certified by providing a higher hourlywage rate following their certification.

Our training program provides multiple training sessions to both Store Managers and technicians in eachstore, each year.

Management training courses are developed and delivered by our dedicated training department andOperations management, and are supplemented with live and on-line vendor training courses. Managementtraining covers customer service, sales, human resources (counseling, recruiting, interviewing, etc.), leadership,scheduling, financial and operational areas, and is delivered on a regular basis. We believe that involvingOperations management in the development and delivery of these sessions results in more relevant andactionable training for Store Managers, and helps to improve overall performance and staff retention.

Our training department develops and coordinates technical training courses on critical areas of automotiverepair to Monro technicians (e.g. Antilock braking systems (“ABS”) brake repair, drivability, tire pressuremonitoring system (“TPMS”), etc.) and also conducts required technical training to maintain compliance withstate inspection licenses, where applicable, and AMRA/MAP accreditation. Additionally, our training departmentholds periodic field technical clinics for store personnel and coordinates technician attendance at technical clinicsoffered by our vendors. We have electronic repair manuals installed in all of our stores for daily reference. Wealso issue technical bulletins to all stores on innovative or complex repair processes, and maintain a centralizeddatabase for technical repair problems. In addition, Monro has established a telephone technical help line toprovide assistance to store personnel in resolving problems encountered while diagnosing and repairing vehicles.The help line is available during all hours of store operation. Monro also maintains an employee web page thatcontains many resources that are available for both managers and technicians to reference.

OPERATING STRATEGY

Monro’s operating strategy is to provide our customers with a wide range of dependable, high-qualityautomotive services at a competitive price by emphasizing the following key elements.

Products and Services

The typical store provides a full range of undercar repair services for brakes, steering, mufflers and exhaustsystems, drive train, suspension and wheel alignment, as well as tire replacement and service. These servicesapply to all makes and models of domestic and foreign cars, light trucks and vans. As a percentage of sales, theservice stores provide significantly more brake and exhaust service than tire stores, and tire stores providesubstantially more tire replacement and related services than service stores.

Stores generally provide many of the routine maintenance services (except engine diagnostic), whichautomobile manufacturers suggest or require in the vehicle owners’ manuals, and which fulfill manufacturers’requirements for new car warranty compliance. We offer “Scheduled Maintenance” services in our storeswhereby the aforementioned services are packaged and offered to consumers based upon the year, make, modeland mileage of each specific vehicle. Management believes that we are able to offer this service in a moreconvenient and cost competitive fashion than auto dealers can provide.

Included in maintenance services are oil change services, heating and cooling system “flush and fill”service, belt installation, fuel system service and a transmission “flush and fill” service. Additionally, most storesreplace and service batteries, starters and alternators. Stores in New York, West Virginia, New Hampshire,

8

8

� OPERATING STRATEGY

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page 8

Maryland, Rhode Island, Pennsylvania, North Carolina, Virginia, Missouri, Maine, Vermont and Wisconsinperform annual state inspections. Approximately 46% of our stores also offer air conditioning services.

We began a program in the third quarter of fiscal year 2007 to increase tire and tire related sales, such asalignments, in our service stores. The goal was to increase the overall sales of these stores by capturing tire andrelated sales from existing store traffic and eventually drive additional traffic and sales. The program involvesincreasing the specific sales training of store managers, expanding the tire merchandise selection in these stores,and raising the focus of store advertising in this category. This initiative, which is called “Black Gold”, has nowbeen rolled out to 263 of the Company’s service stores, primarily in markets where we also have tire stores,which allows for greater utilization of inventory.

The format of the Tire Warehouse and Tire Barn Warehouse stores, acquired in fiscal year 2010 and fiscalyear 2013, respectively, are slightly different from Monro’s typical service or tire stores (as described above) inthat, generally, over 94% of the stores’ sales involve tire services, including the mounting and balancing of tires,and the sale of road hazard warranties. All stores provide the installation of wiper blades. Currently, 25 TireWarehouse and 21 Tire Barn Warehouse stores perform alignments. In fiscal year 2015, Monro plans to expandthe number of Tire Warehouse and Tire Barn Warehouse stores offering alignment services to a total of 52stores.

Customer Satisfaction

Monro’s vision of being the dominant Auto Service provider in the markets we serve is supported by a set ofvalues displayed in each Company Store emphasizing TRUST:

• Total Customer Satisfaction

• Respect, Recognize and Reward (employees who are committed to these values)

• Unparalleled Quality and Integrity

• Superior Value and

• Teamwork

Also displayed in each Company Store are guiding principles in support of our commitment to customerservice: only present needed work; fix vehicles right the first time; complete vehicle service on time; and exceedthe customer’s expectations.

Additionally, each Company-operated store operates under the following set of customer satisfactionprinciples: free inspection of brakes, tires, shocks, front end and exhaust systems (as applicable); item-by-itemreview with customers of problem areas; free written estimates; written guarantees; drive-in service without anappointment; fair and reasonable prices; a 30-day best price guarantee; and repairs by professionally-trainedundercar and tire specialists. (See additional discussion under “Store Operations: Quality Control andWarranties”.)

Competitive Pricing, Advertising and Co-branding Initiatives

Monro seeks to set competitive prices for quality services and products. We support our pricing strategy byadvertising through direct mail coupon inserts and in-store promotional signage and displays. In addition, toincrease consumer awareness of the services we offer, Monro advertises through radio, yellow pages,newspapers, service reminders and digital marketing. Our digital marketing efforts include email marketing, paidsearch on all major search engines, search remarketing, and banner and mobile advertising. We also managesocial media profiles for all Monro brands on Twitter, Facebook and Foursquare.

9

9

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page 9

Our websites include www.Monro.com, www.MrTire.com, www.Tirewarehouse.net, www.Kentowery.com,www.TireBarn.com and www.Currysauto.com. These sites help customers search for store locations, printcoupons, make service appointments, shop for tires and access information on our services and products, as wellas car care tips.

Monro currently maintains mobile apps on the iPhone and Android platforms for the Monro, Mr. Tire andTire Warehouse brands. Our mobile apps enable customers to manage vehicle service records on their smartphones and access information, coupons and specials, as they do on our websites.

Centralized Control

Unlike many of our competitors, we operate, rather than franchise, most of our stores (except for the threeTire Warehouse franchises and 14 dealer locations). We believe that direct operation of stores enhances ourability to compete by providing centralized control of such areas of operations as service quality, storeappearance, promotional activity and pricing. A high level of competence is maintained throughout theCompany, as we require, as a condition of employment, that employees participate in periodic training programs,including sales, management, customer service and changes in automotive technology. Additionally, purchasing,distribution, merchandising, advertising, accounting and other store support functions are centralized primarily inMonro’s corporate headquarters in Rochester, New York, and are provided through our subsidiary, MonroService Corporation. The centralization of these functions results in efficiencies and gives management theability to closely monitor and control costs.

Comprehensive Training

We provide ongoing, comprehensive training to our store employees. We believe that such training providesa competitive advantage by enabling our technicians to provide quality service to our customers in all areas ofundercar repair and tire service. (See additional discussion under “Store Operations: Store Personnel andTraining”.)

PURCHASING AND DISTRIBUTION

Through our wholly-owned subsidiary Monro Service Corporation, we select and purchase tires, parts andsupplies for all Company-operated stores on a centralized basis through an automatic replenishment system.Although purchases outside the centralized system (“outside purchases”) are made when needed at the storelevel, these purchases are low by industry standards, and accounted for approximately 16% of all parts and tiresused in fiscal 2014.

Our ten largest vendors accounted for approximately 83% of our parts and tire purchases, with the largestvendor accounting for approximately 21% of total stocking purchases in fiscal 2014. In fiscal 2014 Monroimported approximately 28% of our parts and tire purchases. We purchase parts and tires from approximately100 vendors. Management believes that our relationships with vendors are excellent and that alternative sourcesof supply exist, at comparable cost, for substantially all parts used in our business. We routinely obtain bids fromvendors to ensure we are receiving competitive pricing and terms.

Most parts are shipped by vendors to our primary warehouse facility in Rochester, New York, and aredistributed to stores by the Monro-operated tractor/trailer fleet. The majority of tires are shipped to our storesdirectly by vendors pursuant to orders placed by our headquarters staff. During fiscal 2013, we completed anexpansion of our warehouse from 80,000 square feet to 135,000 square feet. Stores are replenished at leastmonthly from this warehouse, and such replenishment fills, on average, 95% of all items ordered by the stores’automatic POS-driven replenishment system. The Rochester warehouse stocks approximately 4,400 SKUs.Monro also operates warehouses in Maryland, Virginia, Illinois, New Hampshire and Kentucky. Thesewarehouses carry, on average, 1,200; 300; 1,200; 900 and 1,000 SKUs, respectively.

1

10

� PURCHASING AND DISTRIBUTION

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page 10

11

We enter into contracts with certain parts and tire suppliers, some of which require us to buy (at marketprices) up to 100% of our annual purchases of specific products. These agreements expire at various datesthrough July 2017. We believe these agreements provide us with high quality, branded merchandise at preferredpricing, along with strong marketing and training support.

COMPETITION

Monro competes in the retail automotive service and tire industry. This industry is generally highlycompetitive and fragmented, and the number, size and strength of competitors vary widely from region to region.We believe that competition in this industry is based on customer service and reputation, store location, nameawareness and price. Monro’s primary competitors include national and regional undercar, tire specialty andgeneral automotive service chains, both franchised and company-operated; car dealerships, mass merchandisers’operating service centers; and, to a lesser extent, gas stations, independent garages and Internet tire sellers.Monro considers TBC Corporation (operating under the NTB, Merchant’s Tire, Midas and Tire Kingdombrands), Firestone Complete Auto Care service stores and Meineke Discount Mufflers Inc. to be directcompetitors. In most of the new markets that we have entered, at least one competitor was already present. Inidentifying new markets, we analyze, among other factors, the intensity of competition. (See “ExpansionStrategy” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”.)

EMPLOYEES

As of March 29, 2014, Monro had 6,139 employees, of whom 5,779 were employed in the fieldorganization, 139 were employed at the warehouses, 185 were employed at our corporate headquarters and 36were employed in other offices. Monro’s employees are not members of any union. We believe that our relationswith our employees are good.

REGULATION

Monro stores new oil and recycled antifreeze and generates and/or handles used tires and automotive oils,antifreeze and certain solvents, which are disposed of by licensed third-party contractors. In certain states, asrequired, we also recycle oil filters. Thus, we are subject to a number of federal, state and local environmentallaws including the Comprehensive Environmental Response Compensation and Liability Act (“CERCLA”). Inaddition, the United States Environmental Protection Agency (the “EPA”), under the Resource Conservation andRecovery Act (“RCRA”), and various state and local environmental protection agencies regulate our handlingand disposal of waste. The EPA, under the Clean Air Act, also regulates the installation of catalytic converters byMonro and all other repair stores by periodically spot checking repair jobs, and has the power to fine businessesthat use improper procedures or materials. The EPA has the authority to impose sanctions, including civilpenalties up to $37,500 per violation (or up to $37,500 per day for certain willful violations or failures tocooperate with authorities), for violations of RCRA and the Clean Air Act.

We are subject to various laws and regulations concerning workplace safety, zoning and other mattersrelating to our business. We maintain programs to facilitate compliance with these laws and regulations. Webelieve that we are in substantial compliance with all applicable environmental and other laws and regulationsand that the cost of such compliance is not material to the Company.

Monro is environmentally conscious, and takes advantage of recycling opportunities at our offices,warehouses and stores. Cardboard, plastic shrink wrap and parts’ cores are returned to the warehouse by thestores on Monro stock trucks. There, they are accumulated for sale to recycling companies or returned to partsmanufacturers for credit.

1

� REGULATION

� EMPLOYEES

� COMPETITION

1016834_Monro Annual Report_BWText_2014.qx9_6.26.14 6/26/14 4:31 PM Page 11

12

SEASONALITY

Although our business is not highly seasonal, customers do purchase more undercar service during theperiod of March through October than the period of November through February, when miles driven tend to belower. In the tire stores, the better sales months are typically May through August, and October throughDecember. The slowest months are typically January through April and September. As a result, profitability istypically lower during slower sales months, or months where mix is more heavily weighted toward tires, which isa lower margin category. Additionally, since our stores are primarily located in the northeastern United States,profitability tends to be lower in the winter months when certain costs, such as utilities and snow plowing, aretypically higher.

COMPANY INFORMATION AND SEC FILINGS

Monro maintains a website at www.monro.com and makes its annual, quarterly and periodic Securities andExchange Commission (“SEC”) filings available through the Investor Information section of that website.Monro’s SEC filings are available through this website free of charge, via a direct link to the SEC website atwww.sec.gov. Monro’s filings with the SEC are also available to the public at the SEC Public Reference Room at100 F Street, N.E., Washington, D.C. 20549 or by calling the SEC at 1-800-SEC-0330.

Item 1A. Risk Factors

In addition to the risks discussed elsewhere in this annual report, the following are the important factors thatcould cause Monro’s actual results to differ materially from those projected in any forward looking statements:

We operate in the highly competitive automotive repair industry.

The automotive repair industry in which we operate is generally highly competitive and fragmented, and thenumber, size and strength of our competitors varies widely from region to region. We believe that competition inthe industry is based primarily on customer service, reputation, store location, name awareness and price. Ourprimary competitors include national and regional undercar, tire specialty and general automotive service chains,both franchised and company-operated, car dealerships, mass merchandisers’ operating service centers and, to alesser extent, gas stations, independent garages and Internet tire sellers. Some of our competitors have greaterfinancial resources, are more geographically diverse and have better name recognition than we do, which mightplace us at a competitive disadvantage to those competitors. Because we seek to offer competitive prices, if ourcompetitors reduce prices, we may be forced to reduce our prices, which could have a material adverse effect onour business, financial condition and results of operations. Further, our success within this industry also dependsupon our ability to respond in a timely manner to changes in customer demands for both products and services.We cannot assure that we, or any of our stores, will be able to compete effectively. If we are unable to competesuccessfully in new and existing markets, we may not achieve our projected revenue and profitability targets.

We are subject to seasonality and cycles in the general economy and customers’ use of vehicles, which mayimpact demand for our products and services.