monthly market review and forecast...amidst global growth concern and rising geopolitical tension,...

TRANSCRIPT

MONTHLY MARKET REVIEW AND FORECAST FOR DECEMBER 2019

TRUSTFUND PENSIONS LTD RESEARCH

J A N U A R Y 2 0 2 0

MACROS | EQUITIES| BONDS | MONEY MARKET | ALTERNATIVE INVESTMENTS

Outline

Confidential. Copyright © Trustfund Pensions Ltd

Equity market

Domestic Macro Review

Fixed Income Market

Outlook

Global Economy

GLOBAL MARKETEased Trade Tension and Stronger Economic data allayed Global growth concerns

INVESTMENT RESEARCHTRUSTFUND PENSIONS LIMITED

Amidst global growth concern and rising geopolitical tension, the news of an imminent phase one

trade agreement and stronger macros supported positive sentiment in the global market space.

Thus, US S&P 500 gained 2.9% in December to push the year-to-date return to 28.9%. This is

attributable to strong performance from Healthcare, Tech, Energy and Utilities, while the

consumer and industrial stocks thinned the overall return.

In Europe, clearer BREXIT and easing trade tension saw both UK’s FTSE 100 (+2.7% MTD &

+12.1% YTD) German’s DAX index (+0.1% MTD & +25.5% YTD) in the green zone. The

Conservatives’ won December election and PM’s refreshed promise of a new Brexit deal boosted

market performance.

Also in Asia, both CSI 300 (+7% MTD, +36% YTD) and Japan’s Nikkei 225 (+1.6% MTD, 18.2%

YTD) reported solid performance after Donald Trump commented that the Trade Agreement with

China is in its completion stage.

We expect the final signing of the Trade Agreement in January, geopolitical updates and release

of macroeconomic fundamentals to be major factors in Q1-2020.

Confidential. Copyright © Trustfund Pensions Ltd

28.9%

12.1%

25.5%

18.2%

36.1%

2.9% 2.7%0.1%

1.6%

7.0%

S&P 500 FTSE 100 DAX NIKKEI 225 CSI 300

GLOBAL EQUITY RETURN (%)2019-Ytd Return December Return

Commodities

Best Performed 2019 Return Least Performed 2019 ReturnBrent Crude 22.7% UK Natural Gas -49.12%

Rice 31.6% Manganese -20.39%

Palm Oil 52.3% Wheat -7.13%

Iron Ore 28.4% Zinc -14.90%

Rubber 18.0% Steel -8.06%

-4.6%

-4.9%

-6.0%

-8.1%

-8.6%

-9.7%

-14.6%

-19.6%

Botswana

Jordan

Malaysia

Oman

Mongolia

Ghana

Nigeria

Lebanon

Equity Laggards of 2019

13.9%

19.1%

22.0%

23.9%

26.4%

28.9%

30.4%

49.5%

Israel

Canada

Belgium

Netherlands

France

S&P 500

New Zealand

Greece

Equity Advancers of 2019

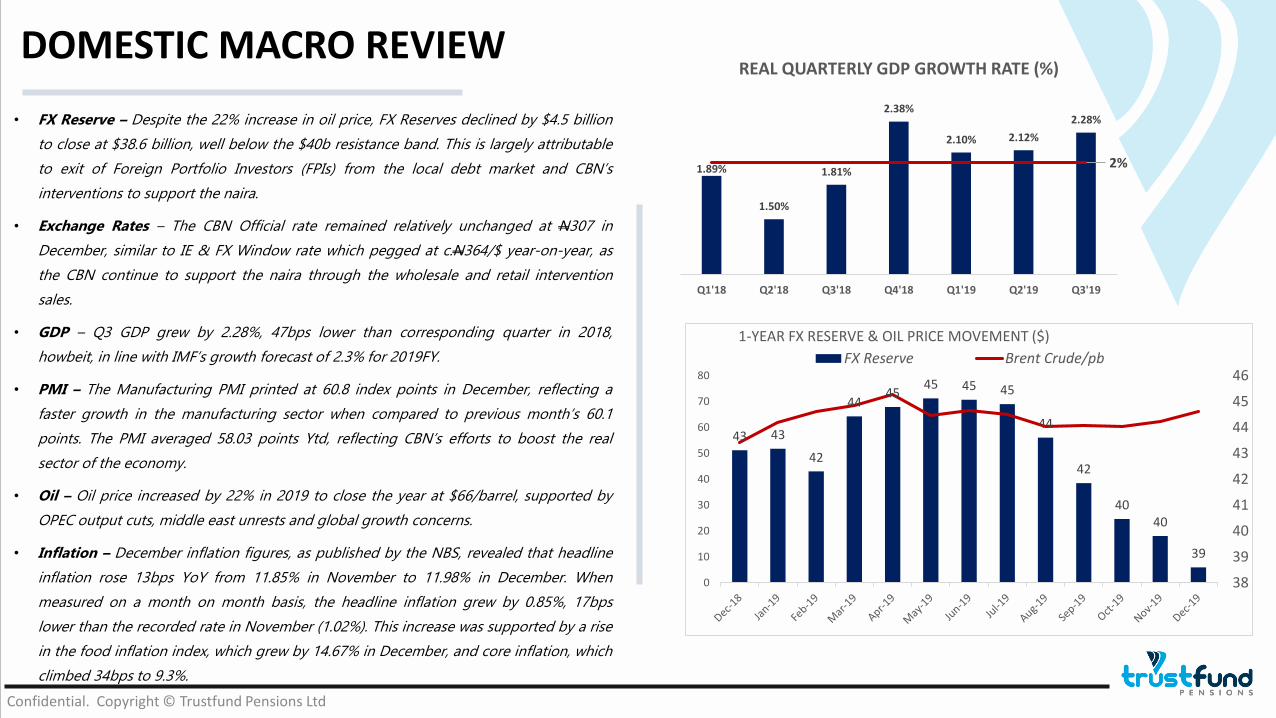

• FX Reserve – Despite the 22% increase in oil price, FX Reserves declined by $4.5 billion

to close at $38.6 billion, well below the $40b resistance band. This is largely attributable

to exit of Foreign Portfolio Investors (FPIs) from the local debt market and CBN’s

interventions to support the naira.

• Exchange Rates – The CBN Official rate remained relatively unchanged at N307 in

December, similar to IE & FX Window rate which pegged at c.N364/$ year-on-year, as

the CBN continue to support the naira through the wholesale and retail intervention

sales.

• GDP – Q3 GDP grew by 2.28%, 47bps lower than corresponding quarter in 2018,

howbeit, in line with IMF’s growth forecast of 2.3% for 2019FY.

• PMI – The Manufacturing PMI printed at 60.8 index points in December, reflecting a

faster growth in the manufacturing sector when compared to previous month’s 60.1

points. The PMI averaged 58.03 points Ytd, reflecting CBN’s efforts to boost the real

sector of the economy.

• Oil – Oil price increased by 22% in 2019 to close the year at $66/barrel, supported by

OPEC output cuts, middle east unrests and global growth concerns.

• Inflation – December inflation figures, as published by the NBS, revealed that headline

inflation rose 13bps YoY from 11.85% in November to 11.98% in December. When

measured on a month on month basis, the headline inflation grew by 0.85%, 17bps

lower than the recorded rate in November (1.02%). This increase was supported by a rise

in the food inflation index, which grew by 14.67% in December, and core inflation, which

climbed 34bps to 9.3%.

Source: Bloomberg/TFPResearchConfidential. Copyright © Trustfund Pensions Ltd

1.89%

1.50%

1.81%

2.38%

2.10% 2.12%

2.28%

2%

Q1'18 Q2'18 Q3'18 Q4'18 Q1'19 Q2'19 Q3'19

REAL QUARTERLY GDP GROWTH RATE (%)

43 43

42

4445

45 45 45

44

42

4040

39

38

39

40

41

42

43

44

45

46

0

10

20

30

40

50

60

70

80

1-YEAR FX RESERVE & OIL PRICE MOVEMENT ($)

FX Reserve Brent Crude/pb

DOMESTIC MACRO REVIEW

EQUITY MARKETWhat happened in December?

INVESTMENT RESEARCHTRUSTFUND PENSIONS LIMITED

Confidential. Copyright © Trustfund Pensions Ltd

The Nigerian Equities market closed modestly bearish in December owing to slow start to usual Santa Claus rally.

Thus, the apex index dipped by 60bps to close at 26,842.07, well below the annual average of 28,900 index points. Market Capitalization closed at N12.96

trillion, 11% higher than year-open.

The top performing stocks based on weighting are NESTLE +8.9%, SEPLAT +19.7%, NB +15.6%, UNILEVER +36.7%, STANBIC +7.5%, ACCESS +8% and

WAPCO 9.3%. While losses from MTNN -12.5%, UNION -14.3%, CCNN -9.5% (Now BUACEMENT), GUARANTY -2.5%, FBNH -8.2% and bellwether

DANGCEM -0.6% drove the bourse southward.

Market valuation remains attractive at P/E ratio 7.08 and Dividend Yield at 6.12%, hence, we expect investors to continue to take profit on stocks that have

witnessed rally in the past sessions, while others will find appropriate entry price amidst paucity of attractive investible outlets in the fixed income space.

-2.8%

3.8%

-2.1%

-6.1%

6.5%

-3.5%

-7.5%-0.7%

0.4%

-4.6%

2.4%

-0.6%

26.8k

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

26k

27k

28k

29k

30k

31k

32k

Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19

ASI Monthly Return for 2019% Monthly Return ASI Average

2019 EQUITY MARKET WRAPEQUITY: The bears dominated market activities as ASI lost 14.6%

www.free-powerpoint-templates-design.com

W H A T I M P A C T E D T H E M A R K E T

18.9%

-16.3%

35.4%

47.2%

-16.1%

-17.4%

-6.2%

42.3%

-17.8%

-14.6%

NIGERIAN STOCK MARKET 10-YR HISTORICAL RETURN (%)

-14.6% -10.6% -13.1%

-20.8%

-13.1%

Mainboard Banking Industrialgoods

Consumergoods

Oil&Gas

Sector Performance in 2019 (%)

*Banking sector emerged as the best performing sector,

supported by strong earnings (fees and investment

income).

*Consumer goods sector performed below the

mainboard index due to poor corporate results from

manufacturing stocks.

Market Movers in 2019

*Below stocks were selected based

on the impact of individual stock’s

price movement on the main

index.

INVESTMENT RESEARCHTRUSTFUND PENSIONS LIMITED

• ASI closed negative for the second consecutive year.

✓ Weakened operating conditions and global growth concerns.

✓ Paucity of investment opportunities and lack of coordinated fiscal

measures to boost the real sector.

✓ US/China trade dispute and Moody’s report which downgraded

African banks from stable to Negative largely impacted the

decisions of foreign investors.

✓ Mixed Corporate Earnings released for Q1,Q2 &Q3 2019, with

Banking stocks posting better results.

✓ The adjournment of AGF’s case against MTN Nigeria, a case which

have been delaying the Telecom market leader’s move to launch

an IPO

News that marginally lifted market mood

✓ Listing of MTN Nigeria, Airtel Africa and SAHCO stocks in the

Nigeria’s stock exchange.

✓ The ban of local individuals and corporates from participating in

the OMO instruments and the subsequent paucity of investible

outlets in the fixed income space. Though the impact on the local

bourse was below expectation as investors’ risk tolerance waned.

✓ Global central banks rate cuts which saw most CBs across the

globe cut MPR up to 200bps on average. Nigeria’s CBN cut its

rate by 50bps

Delisted stocks

✓ Olam completed the acquisition of 100% interest in DANGFLOUR,

firmed at N120 billion amounting to N24/share, hence, and

subsequently delisted. Other delisted stocks are Diamond bank,

GNI, NEWREST, FIRST ALUM, Skye bank and Fortis MFB.

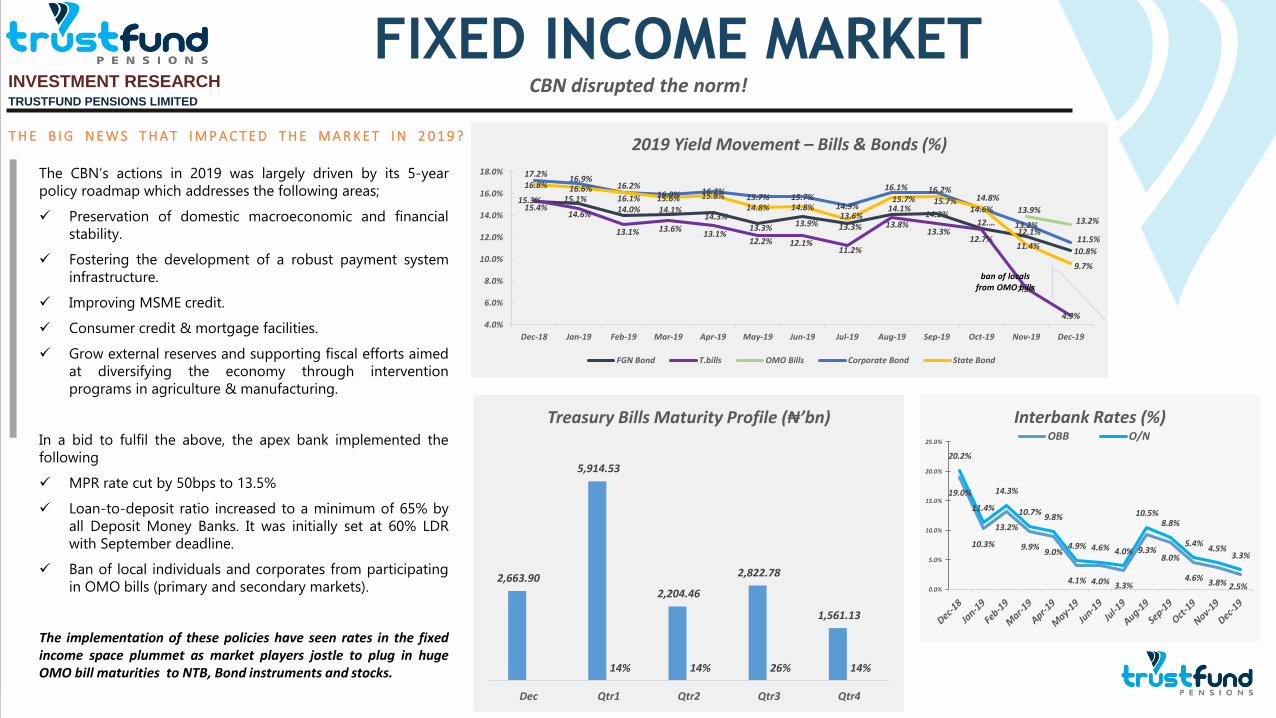

FIXED INCOME MARKETINVESTMENT RESEARCHTRUSTFUND PENSIONS LIMITED

Coming into the month of December, the effects of the CBN’s mandate on domestic players and their participation in the OMO bills market was quite apparent on the

market’s performance in December. As a result, market players were seen to have channeled most of their liquidity on short dated investments, i.e. money market

instruments and NTBs. The graph below illustrates;

Confidential. Copyright © Trustfund Pensions Ltd

3.332.50 2.50 2.50 2.50 2.50

4.503.79

2.50

7.007.50

8.75

0

2

4

6

8

10

O/N OBB CALL 1M 3M 6M

Money Market Rates (%)

DECEMBER NOVEMBER

Money Market – The drastic decline in money market rates between the months of November and December

is most evident in the 625bps depreciation in the interest rates on six-month fixed deposit placements, from

8.75% in November, to 2.50% in December. Likewise, the 129bps MoM decrease in interbank rates from 3.79%

to 2.50% reinforces the notion that market participants were heavily engaged in the short end of the fixed

income space.

Treasury Bills – The NTB space was not spared either as continued demand pressures on these scarce

instruments led average discounted rates on these instruments to finish 226bps lower MoM, thus settling at

4.76% from 7.02%.

It can also be agreed that the PMAs conducted last month also influenced the direction of yields at the

secondary market. In December, a total of N52bn worth of the 91DTM, 182DTM and 364DTM bills were offered

and eventually sold at average stop rates of 4.50%, 5.60% and 6.19% respectively. However, these auctions were

not enough to mop-up the excess liquidity as only about 13% of the total demand for these instruments (over

N392bn) were absorbed, hence further straining yield levels on NTBs overall. A plausible explanation to these

trends could be the fact that most investors positioned in short term instruments, in the hope that the CBN

would reverse the directive restricting domestic players from participating in OMO activities by the end of the

year. This short-term positioning would then enable investors take advantage of the anticipated reversal by

locking in on higher rates at the OMO bills market. However, this was not the case as the directive, which was

believed to have been issued by the apex bank in other to cushion its ever-growing balance sheet, still stands.

5.82

3.93

5.88

7.10 7.007.50

0.00

2.00

4.00

6.00

8.00

3M 6M 1 YR

Secondary Market NTB Rates (%)

DECEMBER NOVEMBER

FIXED INCOME MARKETINVESTMENT RESEARCHTRUSTFUND PENSIONS LIMITED

Nevertheless, average yields on benchmark bonds finished the month

129bps lower at 10.76% from 12.05% in November. This indicates that

despite the fact that investors were seen to have played mostly in the

short end of the fixed income space, long tenured instruments were

also actively traded. This is as a result of investors seeking double digit

yields, given the current situation of yields at the short end of the

spectrum, amidst limited investment outlets. In addition, the outcome

of the bond auction conducted in December further influenced the

direction of yields in the secondary market as stop rates of the

instruments on offer closed lower than at the previous auction, with a

larger volume of instruments being (N264.38bn in December,

compared to N157.924bn in November).

Confidential. Copyright © Trustfund Pensions Ltd

MARKET OUTLOOK

In the coming month, the DMO is scheduled to conduct a bond auction in which the 12.75% FGN APR 2023, 14.55% FGN APR 2029, 14.80% FGN APR 2049 bond

instruments will be re-opened and auctioned. We expect the results of this auction to drive the direction of bond yields in January. We also expect high subscription levels

at this auction, given the current paucity of instruments in the fixed income space. As such, we anticipate yields on these instruments tapering in the coming month.

Furthermore, the slim chance of a reversal on the CBN’s OMO activity restriction on local corporates and individuals supports our expectation of yield declines in the

secondary bond and NTB spaces. In addition, we foresee money market rates hovering at current levels, with slight declines as investors seek out other investment outlets

offering more attractive yields. All these expectations are barring any CBN interventions and liquidity shocks to the system.

10.94

12.18 12.2012.60

12.8513.31

8.20

10.30

11.2811.63

11.96

12.89

2Y 5Y 7Y 10Y 20Y 30Y

SECONDARY BOND MARKET YIELDS (%)

NOVEMBER DECEMBER

FIXED INCOME MARKETCBN disrupted the norm!

T H E B I G N E W S T H A T I M P A C T E D T H E M A R K E T I N 2 0 1 9 ?

INVESTMENT RESEARCHTRUSTFUND PENSIONS LIMITED

The CBN’s actions in 2019 was largely driven by its 5-year

policy roadmap which addresses the following areas;

✓ Preservation of domestic macroeconomic and financial

stability.

✓ Fostering the development of a robust payment system

infrastructure.

✓ Improving MSME credit.

✓ Consumer credit & mortgage facilities.

✓ Grow external reserves and supporting fiscal efforts aimed

at diversifying the economy through intervention

programs in agriculture & manufacturing.

In a bid to fulfil the above, the apex bank implemented the

following

✓ MPR rate cut by 50bps to 13.5%

✓ Loan-to-deposit ratio increased to a minimum of 65% by

all Deposit Money Banks. It was initially set at 60% LDR

with September deadline.

✓ Ban of local individuals and corporates from participating

in OMO bills (primary and secondary markets).

The implementation of these policies have seen rates in the fixedincome space plummet as market players jostle to plug in hugeOMO bill maturities to NTB, Bond instruments and stocks.

19.0%

10.3%

13.2%

9.9%9.0%

4.1% 4.0% 3.3%

9.3%8.0%

4.6%3.8% 2.5%

20.2%

11.4%

14.3%

10.7%9.8%

4.9% 4.6% 4.0%

10.5%8.8%

5.4%4.5%

3.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Interbank Rates (%)OBB O/N

15.3% 15.1%14.0% 14.1%

14.3%13.3% 13.9% 13.3%

14.1%14.2%

12.…12.1%

10.8%

15.4%14.6%

13.1% 13.6%13.1%

12.2% 12.1%11.2%

13.8%13.3%

12.7%

7.3%

4.9%

13.9%13.2%

17.2%16.9%

16.1% 16.0% 16.2%15.7% 15.7%

14.9%

16.1% 16.2%

14.6%

13.2%

11.5%

16.8% 16.6% 16.2%

15.6% 15.8%

14.8% 14.8%13.6%

15.7% 15.7% 14.8%

11.4%

9.7%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19

2019 Yield Movement – Bills & Bonds (%)

FGN Bond T.bills OMO Bills Corporate Bond State Bond

ban of locals from OMO bills

2,663.90

5,914.53

2,204.46

2,822.78

1,561.13

14% 14% 26% 14%

Dec Qtr1 Qtr2 Qtr3 Qtr4

Treasury Bills Maturity Profile (₦’bn)

MARKET OUTLOOK AND STRATEGY

E Q U I T Y

INVESTMENT RESEARCHTRUSTFUND PENSIONS LIMITED

We expect market to be driven by;

✓ Market valuation which remains attractive at P/E ratio of 7.08x

and Dividend Yield at 6.12%.

✓ Expected T-bill maturities and paucity of attractive investible

outlet.

Hence, we will continue to take profit on stocks that have witnessed

significant rally in the past trading sessions, while identifying

appropriate entry points to take position in underpriced stocks with

strong fundamentals and history of dividend payment.

Nonetheless, we will remain cautious.

F I X E D I N C O M E

Given the quantum of maturity inflows expected in Q1-2020, we expect

rates to remain at current levels.

Bond – The extent of the CBN’s response to inflationary pressures, possible

capital flight and the size of government borrowing will likely determine

yield direction in Q1-20.

Treasury Bills – we expect yields to continue to trend lower as the CBN

restriction on OMO bills participation continue to push investors to T-bills

space.

Money Market – Rates are expected to remain compressed at 2% as the

CBN continues to pressure banks to loan to the real sector of the economy.

Following the recent policy directive by the CBN that restricts participation in primary market OMO auction by corporate and individual investors, local

institutional and individual investors are left with no choice than to combine or do either of the following 1.) channel their funds to primary and secondary

treasury bills, 2.) invest in Bank term deposits, 3.) increase appetite for corporate commercial papers or 4.) increase exposure to equities. we see the first

three cases as plausible and envisage buy pressure from local investors in the fixed income market over the near term following expected liquidity surfeit

in the system. While paucity of instruments in the fixed income market will boost activities in the Equity market.

We will be cautious on equity positions with focus on quality stocks, especially the financials with the potential to turn in attractive

dividend yield and capital appreciation.

copyright(c)Trustfund Pensions Limited

THANK YOU