monthly updates | february, 2017 rights, chit funds, “nidhi” companies etc. recent changes in...

TRANSCRIPT

Monthly Updates | February, 2017

01- DIRECT TAXES

Income Tax Pg.3

International Tax Pg.7

02- INDIRECT TAXES

Customs Pg.14

Service Tax Pg.19

MVAT Pg.20

Excise Pg.21

03- MCA UPDATES Pg. 24

04- UPCOMING DUE DATES Pg. 26

05- CONTACT Pg. 31

CO

NT

EN

T

For Private Circulations Only 3 The Update – February, 2017, SGCO & Co. LLP

INCOME TAX Circular No. 35/2016 Applicability of TDS provisions of section 194I of the Act on lump sum lease premium paid for acquisition of long term lease The CBDT has issued Circular No. 35/2016 dated 13.10.2016 clarifying that lump sum lease premium or one-time upfront lease charges, which are not adjustable against periodic rent, paid or payable for acquisition of long-term leasehold rights over land or any other property are not payments in the nature of rent within the meaning of section 194I of the Act. Therefore, such payments are not liable for TDS u/s. 194I of the Act.

----------------------------------------------------- Circular No. 32/2016 Enquiry or investigation in respect of document / evidence relating to Income Declaration Scheme, 2016 found during the course of search u/s. 132 or survey u/s. 133A of the Act The CBDT has issued Circular No. 32/2016 dated 01.09.2016 clarifying that wherever in the course of search or survey, any document is found as a proof for having already filed a declaration under Income Declaration Scheme, including acknowledgment issued by the Income Tax

Department for having filed a declaration, no enquiry would be made by the Income Tax Department in respect of sources of undisclosed income or investment in movable or immovable property declared in a valid declaration made in accordance with the provisions of the scheme. ----------------------------------------------------------------- JUDICIAL RULINGS S. 34 of the Evidence Act: Entries in loose papers / sheets are irrelevant and inadmissible as evidence Facts: • Raids were conducted on the premises of

Aditya Birla Group Industries and Sahara India Group. It led to recovery of incriminating documents and unaccounted cash.

• The documents retrieved were not in the form of regular books of account and were only random sheets and loose papers.

• Common Cause (A Registered Society) had filed a writ petition before the Hon’ble Supreme Court to constitute Special Investigation Team (SIT) and direct investigation against the various functionaries / officers and further monitor the same.

Held: • Loose sheets of papers are wholly irrelevant

to constitute evidence, with respect to the

For Private Circulations Only 4 The Update – February, 2017, SGCO & Co. LLP

transactions mentioned therein being of no evidentiary value.

• There has to be some relevant and admissible evidence and some cogent reason, which is prima facie reliable and that too, supported by some other circumstances pointing out that the particular third person against whom the allegations have been levelled was in fact involved in the matter or he has done some act during that period, which may have co-relations with the random entries.

Common Cause vs. UOI (Supreme Court) 1WP No. 505 of 2015

--------------------------------------------- S. 2(22)(e): Taxation of Deemed dividend in the hands of recipient Facts: • The assessee is a HUF and had received

advance from a company in which Karta of the HUF had subscribed for shares representing 37.12% of the total shareholding of the company.

• The A.O. added the said advance as deemed dividend on the ground that the assessee was both the registered shareholder of the company and also the beneficial owner of the shares, holding more than 10% of voting power.

• The CIT(A) affirmed the said addition on the ground that the provisions of section 2(22)(e) of the Act is attracted if the shareholder is a beneficial shareholder.

• The Hon’ble ITAT deleted the said addition by holding that HUF cannot be a registered shareholder or a beneficial shareholder to

attract provisions of section 2(22)(e) of the Act.

• The Hon’ble HC reversed the decision of the Hon’ble ITAT by observing that the Karta is a member of HUF which had taken loan from the company.

Held: • Since the Karta of HUF was entitled to not

less than 20% of the income of HUF, provisions of section 2(22)(e) of the Act get attracted.

• As per the provisions of section 2(22)(e) of the Act, once the payment is received by the HUF and shareholder is a member of the said HUF and he has substantial interest in the HUF, the payment made to the HUF shall constitute deemed dividend.

Gopal and Sons (HUF) vs. CIT (Supreme Court) Appeal No. 12274 of 2016 ----------------------------------------------------------------- S. 28/29: All expenditure after “setting up” is deductible business expenditure even if the business has not Facts: • The assessee is an asset management

company. During the year under consideration it had shown business loss of Rs. 1.17 crores.

• The A.O. disallowed the business loss on the ground that setting up of business was not supported by any evidence.

• The CIT(A) confirmed the said disallowance on the ground that no evidence was furnished to prove that any activities of managing the investments or funds have been carried on.

For Private Circulations Only 5 The Update – February, 2017, SGCO & Co. LLP

• The Hon’ble ITAT allowed the business loss by stating that the balance sheet and profit and loss account including Director’s report, clearly depicts that the company has taken steps for commencing business of venture capital fund and employed necessary personnel for the purpose of running its business.

Held: The Hon’ble HC held that all expenses incurred during the interim period between setting up of business and commencement of business would be permissible deductions. CIT vs. Axis Pvt. Equity Ltd. (Bom HC) ITA No. 1204 of 2014

--------------------------------------------- S. 54EC: Investment in specified bonds from the amounts received as an advance is eligible for deduction, irrelevant of the fact that investment is made prior to the transfer of the asset ITA No 1009 of 2014 Facts: • The assessee had invested Rs. 50 lakhs,

from the advance received under the agreement to sale, in bond of Rural Electrification Corporation Ltd.

• The A.O. and CIT(A) denied the benefit of section 54EC of the Act to the assessee as the amounts were invested in the bonds prior to the sale of the property.

• The Hon’ble ITAT allowed the benefit of section 54EC of the Act to the assessee on the investment in bonds on receipt of advance as per the agreement of sale.

Held The earnest money received on sale of asset, when invested in specified bonds u/s. 54EC of the Act, is entitled to the benefit of section 54EC of the Act even when the investment was made prior to the date of sale of property CIT vs. Mr. Subhash Vinayak Supnekar (Bom HC) ITA No 1009 of 2014 ----------------------------------------------------------------- S. 69C: Purchases treated as bogus based on the information obtained from the Sales Tax Department Facts: • The assessee was engaged in business as

civil contractor. The assessee had submitted copies of purchase invoices, bank statement reflecting payment made through banking channels, ledger extracts, site wise stock register and site wise goods inward register, to ascertain the genuineness of purchases.

• The A.O. treated such purchases as unexplained expenditure on the ground of non-submission of delivery challans and lorry receipts; non-attendance of parties in response to notice u/s. 133(6) of the Act; non-production of parties by the assessee and by placing reliance on the statements made before the Sales Tax Department.

• The CIT(A) allowed the appeal in favour of the assessee by placing reliance on the decision of the Bombay High Court in the case of Nikunj Eximp Enterprises Pvt. Ltd. (372 ITR 619).

For Private Circulations Only 6 The Update – February, 2017, SGCO & Co. LLP

Held:

The Hon’ble ITAT decided the matter in favour of the assessee as follows: • Without corresponding purchases, sales

could not be effected. • Addition cannot be made by merely relying

on information obtained from the Sales Tax

Department, statements / affidavits of third parties and without affording any opportunity of cross examination.

ACIT vs. Shri Mahesh K. Shah (ITAT Mumbai) ITA No. 5194/Mum/2014 -----------------------------------------------------

For Private Circulations Only 7 The Update –February, 2017, SGCO & Co. LLP

FEMA & INTERNATIONAL TAXATION

FOREIGN DIRECT INVESTMENT

Foreign Direct Investment (FDI) in India needs

to be undertaken in accordance with the FDI

policy formulated by the Government of India.

FDI upto 100% is permitted in most sectors.

There are however sector-specific caps on

foreign equity investment in certain sectors like

insurance, pension, defense, banking, basic

and cellular telecommunications services, civil

aviation, retail trading etc.

FDI can be made through two routes viz.

Automatic route: A foreign investor does not

need the approval of the government or RBI to

make investment in India

Approval route: Proposed investments that do

not qualify for the automatic route must be

submitted to the Foreign Investment

Promotion Board (FIPB) Investment in certain

sectors is prohibited even under approval

route for e.g. lotteries, gambling, betting

including casinos, manufacturing of cigarettes,

construction of farm houses, atomic energy,

railway operations (other than “railway

infrastructure”), trading in transferable

development rights, chit funds, “Nidhi”

companies etc.

Recent changes in FDI

Government has enhanced / liberalized FDI in

various sectors, subject to conditions. The Key

changes are highlighted below:

FDI in insurance, pension, asset reconstruction,

e-commerce, construction development

projects, defence, broadcasting, banking,

plantation, civil aviation, credit information,

satellites, financial services, food products and,

“Other Financial Services” enhanced /

liberalized subject to conditions.

FDI in “Other Financial Services” has been

permitted under automatic route if such

services are regulated by any financial sector

regulator viz. RBI, SEBI, IRDA, PFRDA, NHB etc.

Minimum capitalization norms specified for

NBFCs has been removed subject to meeting

the capitalisation norms specified by the

concerned Regulator. FDI in unregulated

“Other Financial Services”, will be permitted

under Government approval route.

FDI is also permitted under the automatic route

(as against earlier Government approval route)

in LLPs operating in sectors/ activities where

100% FDI is allowed under automatic route and

there are no FDI-linked performance

conditions.

To simplify the procedures for Indian

Companies to attract foreign investments, the

distinction between different types of foreign

For Private Circulations Only 8 The Update –February, 2017, SGCO & Co. LLP

investments i.e. FDI / FPI / FII / QFI / NRI etc.,

have been done away with and replaced with

composite caps

Investment by NRI in shares / convertible

debentures on non-repatriation basis is

deemed to be domestic investment at par with

the investment made by residents

Eligible foreign investors have been permitted

to make investment under automatic route in

units of AIF, REIT, as against approval route

Purchase or sale of shares of Indian company

between resident and nonresident for

payment on deferred basis allowed

Indian company engaged in a sector covered

under automatic route permitted to issue

shares to non-resident by way of swap of

shares under automatic route

FPIs allowed to invest in unlisted non-

convertible debentures irrespective of the

sector in which the issuing company operates

JUDICIAL RULINGS

Where under an agreement with foreign

company for carrying out research, assessee

made payment to foreign company for

purchase of equipments and appliances but

no research activity had taken place, said

payment could not be treated as royalty liable

to TDS

Facts of the Case:

The assessee-company engaged in the business

of generation of power entered into an

agreement with a Norway based company for

the purpose of carrying out research work

related to extraction of electric energy from

tidal waves.

The assessee made a payment of certain

amount for purchase of equipments and

appliances for the purpose of research.

The Assessing Officer treated the said amount

as payment in the nature of royalty.

On appeal, the Commissioner also confirmed

the order of the Assessing Officer on the

ground that since the payment was made

under an agreement for carrying out research

activities on behalf of assessee, the payment

must be treated as royalty.

On second appeal

Held:

Payment is made for acquiring certain

equipments and appliances for the purpose of

research.

The stand of the revenue authorities is that

since the payment was made under an

agreement which was aimed at carrying out

research activities on behalf of the assessee,

the payment must be treated as royalty.

While examining taxability of income in the

hands of the recipient, embedded in foreign

remittance, all that is required to be seen is

whether or not that particular income is

taxable in India.

In the present case, the payment is made for

purchase of equipments and appliances and

these equipments and appliances under the

agreement belonged to the assessee and

clearly, therefore, the income embedded in

these payments is not eligible to tax in India in

absence of permanent establishment of the

foreign company in India.

It is true that the contract for the purpose of

which these equipments and appliances were

purchased, relates to a taxable activity, i.e.,

royalty, it is equally correct that no such

taxable event, i.e., carrying out of research

For Private Circulations Only 9 The Update –February, 2017, SGCO & Co. LLP

activity has taken place during the course of

this transaction.

In this view of the matter, authorities below

were completely in error in holding that the

income embedded in the remittance of NOK

7,50,000 which was beyond any dispute or

controversy for the purpose of purchase of

equipments and appliances for research, was

not taxable in India.

Therefore, the orders of the authorities are

reversed and it was held that the assessee was

not liable to deduct any tax from this payment.

Since the impugned tax had cancelled

withholding liability itself, all other points such

as grossing up or invocation of section 206AA

or even interest liability under section 201(1A)

were not more than academic.

In favour of Assessee.

Aatash Power (P.) Ltd V. Income Tax Officer,

International Taxation-II, Ahmedabad [2017]

78 taxmann.com 202 Ahmedabad-Trib-

TRANSFER PRICING

Difference in turnover is not a valid criteria to

exclude a concern from list of comparable so

long as it is otherwise functionally

comparable

Facts of the Case:

The Assessee, (partnership firm) was engaged

in the business of cutting and polishing of

diamonds.

Transfer pricing Officer (TPO) examined the

international transactions of import and export

of diamonds with the Associated Enterprises

(AE) and benchmarked the same by selecting

the Transactional Net Margin (TNM) method as

the most appropriate method.

TPO selected 15 companies, which were

comparable to the assessee and determined

their mean profit margin at 11.02 per cent

Assessee's margin was 6.82 per cent, and the

TPO made an adjustment in order to compute

the Arm’s Length Price of the Transaction

Dispute Resolution Panel (DRP) passed an

order giving certain directions to the Assessing

Officer in order to finalize the assessment.

One of the directions given the DRP was to the

effect that a comparable named “Anshumi

Commercials Ltd” was not included in the final

set of comparables by the TPO, and the same

shall be included as a comparable.

Held:

In the given context, the said concern

(Anshumi) has been directed to be included on

the ground that it is functionally comparable

with the assessee.

The contention of the revenue seeking to

reverse the finding of the DRP to include

Anshumi in the final set of comparable was

misconceived.

TPO had excluded it from the final set of

comparables on the ground that the said

concern was 'not found functionally

comparable'.

The objection of the TPO with regard to the

functional comparability was not accepted by

the DRP, who in turn held it to be functionally

comparable.

The total sales of Anushni was only Rs. 79.80

lakhs, whereas that of the assessee was Rs.

33.32 crores. Difference in turnover is not a

valid criteria to exclude a concern from the list

of comparable so long as it is otherwise

functionally comparable.

For Private Circulations Only 10 The Update –February, 2017, SGCO & Co. LLP

As per the revenue, turnover is a deciding

factor in considering whether a concern is

comparable or not. The relevant characteristics

of a concern in any uncontrolled transaction

between independent enterprises must be

sufficiently comparable with the tested

transactions if the two are to be placed in

similar situation.

Hence, Stand of the revenue seeking exclusion

of Anshumi was untenable.

Assistant Commissioner of Income Tax

16(2) v. Golawala Diamonds [2017] 78

taxmann.com 82 (Mumbai- Trib)

Assessee not precluded from changing MAM

during assessment proceeding, on

subsequent data availability

Facts of the Case:

The Assessee Company is engaged in the

business of manufacturing and selling

pigments, dye stuff, and pesticides.

During the assessment year 2005-06, the

assessee entered into international

transactions with Dainippon Ink & Chemicals

Inc, Japan (DIC) (AE) and thus reference was

made to the Transfer Pricing Officer (TPO).

The international transactions entered into by

the assessee with its AE are as under:

Purchase of raw material

Sale of finished goods

Commission paid

The assessee selected Cost plus Method (CPM)

as most appropriate method for benchmarking

its international transactions. The assessee

made certain adjustments, to the cost and

sales price to arrive at Arm’s Length Price (ALP).

The TPO rejected the adjustments made by the

assessee in respect of unrelated parties while

arriving at ALP. The TPO made upward

adjustment of Rs. 5,58,02,100/- in assessee’s

income. On the basis of the order of TPO, the

Assessing Officer passed assessment order by

making addition Rs. 5,58,02,100/- in the

income returned by the assessee.

Against the assessment order the assessee

preferred the appeal before this CIT (A). The

assesse during first appellate proceeding re-

computed ALP by adopting CUP as most

appropriate method.

The CIT (A) sought remand report from the A.O.

on change of method for computing ALP. On

the basis of remand report and the submission

of assessee, the CIT (A) accepted CUP method

applied by the assessee as the most

appropriate method for determining ALP.

The Revenue filed an appeal by stating that CIT

(A) had erred in holding that the assessee can

change its admitted position to save itself from

the disadvantage.

The revenue submitted that the assessee has

changed method of determining ALP only after

the TPO has rejected adjustments made by the

assessee and made upward adjustment in the

international transaction.

Assessee argued that it had entered into

international transactions with its AE . In TP

study, the assessee applied CPM as most

appropriate method on the basis of

information available. The assessee made

certain adjustments on cost side as well as on

income side with uncontrolled transactions to

make it comparable with the controlled

transaction. At the time of TP study, the details

were not available with the assessee so that

the assessee could apply CUP method.

Subsequently, when the assessee got the

For Private Circulations Only 11 The Update –February, 2017, SGCO & Co. LLP

details, the assessee furnished re-computed

ALP by applying CUP before TPO.

The assessee stated that it had furnished the

same details before the First Appellate

Authority. The Commissioner of Income Tax

(Appeals) sought remand report from the AO.

In the remand report A.O accepted that CUP

method can be applied in the instant case.

However, the A.O objected for applying CUP

method merely on the ground that in TP study,

the assessee had applied CPM and the assessee

cannot be allowed to change the method of

determining ALP at subsequent stage.

Assessee also stated that the provision of Act

and the Rules made there under envisage that

most appropriate method should be adopted

in determining ALP.

The assessee also placed reliance on the

decision of Mumbai Bench of Tribunal in the

case Mattel Toys1 and in the case of M/s

Chemtex Global Engineering Pvt. Ltd2

Held:

ITAT observed that when CIT (A) sought

remand report from the A.O regarding merits

of applications of CUP method, the A.O.

accepted in principle that CUP method can be

applied.

ITAT stated that any of the methods given in

section 92C (1) of the Act, may be selected as

the most appropriate method, provided it gives

the best estimate of the arm’s length price. In

evaluating, whether the method is best suited,

following factors are to be kept in mind:

1 Mattel Toys1 (I) Pvt Ltd v/s. DCIT reported as

30 ITR (Trib) 283

The nature and class of international

transaction

Degree of comparability between

controlled and uncontrolled transaction.

The class or classes of AE’s entering into

transactions & functions performed by

them

Reliability of data and assumptions the

extent of reliable adjustments that can

be made to factor the differences

between the transactions being

compared.

ITAT also stated that if at the time of TP study,

the details are not available with the assessee

to apply CUP method, there is no restriction on

the assessee for re-computing ALP by applying

CUP, if during the course of assessment

proceedings the relevant data comes in

possession of the assessee. The endeavor

should be to apply the most appropriate

method which would give closest result. There

is no bar under the Act or Rules made there

under which restricts the assessee to change

the method of determining ALP. However, it

should be kept in mind that the change of

method should be for bonafide reasons and

not in an arbitrary manner just to circumvent

adjustment proposed by the TPO.

Sudarshan Chemical Industries

Limited [TS-1078-ITAT-2016(PUN)-TP]

Characterization as market research

service provider over ITES-provider.

2 ACIT v/s M/s Chemtex Global Engineering

Pvt. Ltd2 in ITA No. 3590/Mum/2010 in A.Y.

2004-05

For Private Circulations Only 12 The Update –February, 2017, SGCO & Co. LLP

Facts of the Case:

The assessee is a company incorporated under

the provisions of Companies Act, 1956 and is

engaged in rendering market research services

for its customers.

During AY 2009-10, assessee provided market

research services to its AEs and benchmarked

it with the margin (operating profit/total

revenue) earned from rendering market

research services to non-associated

enterprises as an internal Transaction Net

Margin Method (TNMM) comparable.

Similarly, assessee also availed market

research services from its AEs and added value

to it by way of further analysis and rendered

final services to third parties.

Assessee compared the profitability from such

transactions to the profitability in case of

comparable uncontrolled transactions which

did not involve receiving of any services from

AEs.

During assessment proceedings, AO referred

the matter to TPO who held that TP study

report undertaken by assessee was not

appropriate. The primary area of difference

between the assessee and the TPO was in

characterizing the transactions undertaken

with AEs.

TPO considered activities undertaken by

assessee as Information Technology Enabled

Services (ITES) as against assessee’s

characterization of the services as market

research services which it claimed were clearly

distinct and in contrast to an ITE service

provider.

In appeal, DRP appreciated assessee’s stand on

the basis of records available and certain

documents furnished as additional evidence by

assessee. DRP upheld assessee’s

characterization as a market research service

provider and accepted the benchmarking

analysis using internal TNMM as comparable.

DRP directed that no addition was required on

the stated value of international transactions.

Aggrieved, Revenue filed an appeal before

Mumbai ITAT.

Before ITAT, Revenue submitted that

substantial chunk of work carried out by the

assessee involved data processing with the

help of computers; therefore, the overall

services were akin to those carried out by an

ITES provider. Revenue also pointed out that

for AY 2008-09 DRP had concurred with TPO’s

stand that activities of assessee could be

characterized as an ITES provider.

Held:

ITAT explained that market research service

provider would mean a person who is engaged

in conducting market research in any manner,

either in relation to any product, service or

utility and including all allied research services

which would be customized to a particular

situation.

ITAT further added that in common parlance,

market research is understood as referring to

collecting, collating and analyzing of

information or data consisting of a particular

subject which may be a product, service,

geographical area, industry, etc.

ITAT opined that DRP had succinctly brought

out the various stages that are involved in the

market research process which are in contrast

to ITES which is primarily understood as an

activity whereby certain processes are

outsourced, which are enabled with the help of

information technology.

For Private Circulations Only 13 The Update –February, 2017, SGCO & Co. LLP

ITAT also stated that the illustrative list of IT

enabled products/services as explained in

CBDT Circular No. SO 890(E) dated 26.9.2000

clearly explain that ITES involve routine human

tasks which are carried out more and more by

use of technology on the part of human

resources and that predominant use of

technology is involved to achieve the desired

output.

In light of this, ITAT opined that,” In contrast, if

we were to compare such like services with the

activities of a market research service provider,

it would be evident that in market research,

output is the product of collecting, collating

and analysing of information/data, which may

involve use of technology, whereas in the case

of ITE services, rendering of services is

primarily driven by use of technology on the

part of human resources.”

ITAT also referred to distinction made by DRP

between market research agency and an IT-

enabled service provider under the Service Tax

Rules to show that the two were incomparable.

ITAT also noted that assessee’s name was

included in the list of concerns which are

engaged in the business of market research

services communicated by Market Research

Society of India (MRSI), a trade association of

market research entities which was furnished

by assessee before DRP.

Accordingly, ITAT held that DRP was justified in

concluding that market research services

undertaken by assessee cannot be compared

with ITES.

ITAT noted that same dispute of

characterization as adjudicated for AY 2009-10

was raised for AY 2008-09. Accordingly, ITAT

held that the decision for AY 2009-10 would

apply mutatis mutandis for AY 2008-09.

Synovate India Pvt Ltd [TS-898-ITAT-

2016(Mum)-TP]

For Private Circulations Only 14 The Update –February, 2017, SGCO & Co. LLP

CUSTOMS

Notifications –Non-Tariff

Tariff Notification in respect of Fixation of

Tariff Value of Edible Oils, Brass Scrap, Poppy

Seeds, Areca Nut, Gold and Silver: -

Table 1

Sr.

No.

Chapter/he

ading/sub-

heading/ta

riff item

Description

of Goods

Tariff

Value

(US $)

(1) (2) (3) (4)

1 1511 10 00 Crude Palm

Oil

814

2 1511 90 10 RBD Palm Oil 819

3 1511 90 90 Others- Palm

Oil

817

4 1511 10 00 Crude

Palmolein

820

5 1511 90 20 RBD

Palmolein

823

6 1511 90 90 Others-

Palmolein

822

7 1507 10 00 Crude Soya

bean Oil

847

8 7404 00 22 Brass Scrap (

all grades)

3247

9 1207 91 00 Poppy seeds 2625

Table-2

Sr.

No.

Chapter/hea

ding/sub-

heading/tari

ff item

Descripti

on of

Goods

Tariff

Value (US

$)

(1) (2) (3) (4)

1 71 or 98 Gold 400 per 10

grams

2 71 or 98 Silver 583 per

kilogram

Table-3

For Private Circulations Only 15 The Update –February, 2017, SGCO & Co. LLP

Sr.

No.

Chapter/hea

ding/sub-

heading/ta

riff item

Descripti

on of

Goods

Tariff Value

(US $ per

metric tonne)

(1) (2) (3) (4)

1 080280 Areca

Nuts

2594

Customs Notification No. 08/2017-Customs (N.T)

Dated 31st January, 2017 & 11/2017 dated 15th

February 2017.

------------------------------------------------------------

Exchange rate to be consider for Import/Export

of Goods, shall be effective from 3rd February,

2017

Schedule I

Sr.

No.

Foreign

Currency

Rate of exchange of

100 units of foreign

currency equivalent to

Indian rupees

(1) (2) (3)

(a) (b)

(For

Importe

d Goods)

(For Export

Goods)

1 Australian

Dollar

52.60 50.80

2 Bahrain

Dinar

184.05 171.75

3 Canadian

Dollar

52.10 50.50

4 Danish

Krone

9.75 9.40

5 EURO 72.45 69.95

6 Hong Kong

Dollar

8.75 8.50

7 Kuwait

Dinar

226.90 212.30

8 New

Zealan

d Dollar

49.35 47.50

9 Norwegian

Kroner

8.20 7.90

10 Pound

Sterling

85.00 82.05

11 Singapore

Dollar

47.95 46.50

12 South

African

Rand

5.35 5.00

13 Saudi

Arabian

Riyal

18.45 17.30

14 Swedish

Kroner

7.65 7.40

15 Swiss Franc 67.85 65.70

16 UAE

Dirham

18.85 17.65

17 US Dollar 67.85 66.15

For Private Circulations Only 16 The Update –February, 2017, SGCO & Co. LLP

18 Chinese

Yuan

9.95 9.60

19 Qatari

Riyal

18.95 17.90

Schedule II

Sr.

No

.

Foreign

Currenc

y

Rate of exchange

of 100 units of

foreign currency

equivalent to

Indian rupees

(1) (2) (3)

(a) (b)

(For

Importe

d

Goods)

(For

Expor

t

Good

s)

1. Japanes

e Yen

59.85 57.90

2. Kenya

Shilling

66.90 62.55

Customs Notification No. 09/2017-Customs (N.T)

dated 02nd February, 2017 & 12/2017 dated 16th

February, 2017

------------------------------------------------------------

Notifications –Anti Dumping Duty

CBEC seeks to extend the levy of anti-dumping

duty, imposed on Hot Rolled products of alloy or

non-alloy steel originating in or exported from

China PR, Japan, Korea RP, Russia, Brazil and

Indonesia, vide notification No. 44/2016-Customs

(ADD), dated the 08.08.2016, to a period of 8

months i.e. further period of 2 months.

Customs Notification No. 05/2017-Customs

(ADD) Dated 7th February, 2017

--------------------------------------------------------

Seeks to extend the levy of anti-dumping duty,

imposed on Cold Rolled Flat Products of alloy or

non-alloy steel originating in or exported from

China PR, Japan, Korea RP and Ukraine vide

notification No. 45/2016-Customs (ADD), dated

the 17.08.2016, to a period of 8 months i.e. further

period of 2 months.

Customs Notification No. 06/2017-Customs

(ADD) Dated 7th February, 2017

--------------------------------------------------------

CBEC seeks to extend the levy of anti-dumping

duty on imports of Hot rolled products of alloy or

non-alloy steel originating in, or exported from

Peoples Republic of China, Japan, Korea, Russia,

Brazil and Indonesia for a period of eight months

i.e. up to and inclusive of the 8th September, 2017.

Extension of anti-dumping duty on Seamless

tubes, pipes & hollow profiles of iron, alloy or

non-alloy steel (other than cast iron and stainless

steel), wheather hot finished or cold drawn or

cold rolled of an external diameter not exceeding

355.6mm or 14” OD falling

CBEC seeks to impose definitive anti-dumping on

all imports of Seamless tubes, pipes & hollow

For Private Circulations Only 17 The Update –February, 2017, SGCO & Co. LLP

profiles of iron, alloy or non-alloy steel (other

than cast iron and stainless steel), wheather hot

finished or cold drawn or cold rolled of an

external diameter not exceeding 355.6mm or 14”

OD falling under heading 7304 of the First

schedule to the Customs Tariff Act, 1975,

originating in or exported from China PR.

Customs Notification No. 07/2017-Customs

(ADD) Dated 17th February, 2017

----------------------------------------------------------

DGFT

Public Notice

Product description of the following in the MEIS

Schedules i.e Table 2 of Appendix 3B has been

corrected so as to make it in line with ITC (HS) w.e.f

01.04.2015.

ITC (HS)

Code

Exsisting

description

Corrected

Description

12119022 Senna Leaves

and Pads

Senna Leaves and

Pods

48045100 Krft

Papr/Paprbord

Weing/225G/M

2 Unblchd

Other kraft paper

and paperboard

weighing 255

g/m2 or more :

Unbleached.

64039990 Lthr Sandals

With Othr Sole

Other

DGFT Public Notice No. 55/ 2015-2020 dated 30

January, 2017

----------------------------------------------------------

New Sub Para 5.03 (c ) (i) has been added providing

that application for amendment in the list of

import item (s) including addition(s)/deletion(s)

may be filed with RA concerned provided that

authorization is valid for import. Applicant has to

provide justification for such amendment along

with fresh nexus certificate from (CEC).

Similarly para 5.03 (c ) (ii) has been added

providing that application for amendment in the

list of export item (s) including addition

(s)/deletion(s) may be filed with RA concerned

provided that Export obligation period of the

authorization is valid and CG has nexus with

original export product. Applicant has to provide

justification for such amendment along with fresh

nexus certificate from (CEC).

Para 5.10(d)(ii) has been amended to provide that

unit not registered with central excise can provide

proof of having dispatch the goods from

authorization holder’s factory/premises to

ultimate exporter /port of export in the form of

Invoice duly incorporating the relevant EPCG

authorization number & date at the time of

dispatch.

DGFT Public Notice No. 56/ 2015-2020 dated 06

February, 2017

----------------------------------------------------------

4 Pre-shipment Inspection agency (PSIA’s) have

been approved under the heading “New PSIA’s

recognized in terms of FTP 2015-20” in Appendix

2G. Instruments have been approved for such

PSIA’s. Also Additional instrument has been

approved for existing PSIA’s.

DGFT Public Notice No. 57/ 2015-2020 dated 10

February, 2017

----------------------------------------------------------

Sub Para (b) & (c) of para 3.06 has been replaced

with the following two tables.

For Private Circulations Only 18 The Update –February, 2017, SGCO & Co. LLP

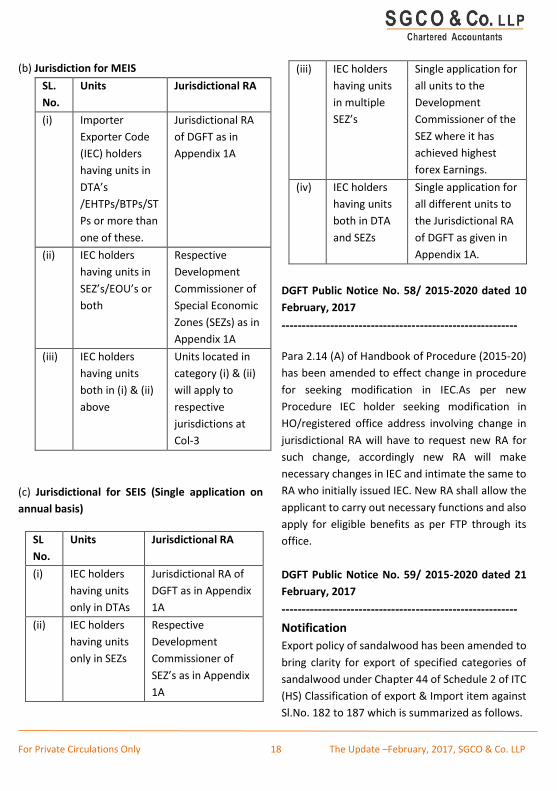

(b) Jurisdiction for MEIS

SL.

No.

Units Jurisdictional RA

(i) Importer

Exporter Code

(IEC) holders

having units in

DTA’s

/EHTPs/BTPs/ST

Ps or more than

one of these.

Jurisdictional RA

of DGFT as in

Appendix 1A

(ii) IEC holders

having units in

SEZ’s/EOU’s or

both

Respective

Development

Commissioner of

Special Economic

Zones (SEZs) as in

Appendix 1A

(iii) IEC holders

having units

both in (i) & (ii)

above

Units located in

category (i) & (ii)

will apply to

respective

jurisdictions at

Col-3

(c) Jurisdictional for SEIS (Single application on

annual basis)

SL

No.

Units Jurisdictional RA

(i) IEC holders

having units

only in DTAs

Jurisdictional RA of

DGFT as in Appendix

1A

(ii) IEC holders

having units

only in SEZs

Respective

Development

Commissioner of

SEZ’s as in Appendix

1A

(iii) IEC holders

having units

in multiple

SEZ’s

Single application for

all units to the

Development

Commissioner of the

SEZ where it has

achieved highest

forex Earnings.

(iv) IEC holders

having units

both in DTA

and SEZs

Single application for

all different units to

the Jurisdictional RA

of DGFT as given in

Appendix 1A.

DGFT Public Notice No. 58/ 2015-2020 dated 10

February, 2017

----------------------------------------------------------

Para 2.14 (A) of Handbook of Procedure (2015-20)

has been amended to effect change in procedure

for seeking modification in IEC.As per new

Procedure IEC holder seeking modification in

HO/registered office address involving change in

jurisdictional RA will have to request new RA for

such change, accordingly new RA will make

necessary changes in IEC and intimate the same to

RA who initially issued IEC. New RA shall allow the

applicant to carry out necessary functions and also

apply for eligible benefits as per FTP through its

office.

DGFT Public Notice No. 59/ 2015-2020 dated 21

February, 2017

----------------------------------------------------------

Notification

Export policy of sandalwood has been amended to

bring clarity for export of specified categories of

sandalwood under Chapter 44 of Schedule 2 of ITC

(HS) Classification of export & Import item against

Sl.No. 182 to 187 which is summarized as follows.

For Private Circulations Only 19 The Update –February, 2017, SGCO & Co. LLP

Restriction under the following item description

against Sl No. 183 & 184 has been deleted.

Finished Handicraft products of

‘Sandalwood’ & Other Species.

Machine Finished Sandalwood Products.

Also ‘Other forms of sandalwood’ has been made

exhaustive and specified in the tariff code itself

under Sl No.187.

Notification No. 37/ 2015-2020 dated 27 January,

2017

----------------------------------------------------------

Category MS007 in the Export Licensing note of

Table A of Schedule2 of ITC(HS) classification of

Export and Import items has been amended to

exclude “Soft Skinned Vehicles” i.e the vehicles

which are neither armoured nor intended to be

modified as an armoured vehicle in the future from

the list of military ground vehicles and components

designed or modified for military use. Hence, NOC

is not to be obtained for soft skinned vehicles from

department of Defence production for export

purposes.

Notification No. 38/ 2015-2020 dated 17

February, 2017

----------------------------------------------------------

The exporter of cut and polished diamonds (each

of 0.25 carat and above) with annual turnover of

Rs.5 crores for each of the last 3 years with re-

import facility at zero duty within 3 months from

the date of export mentioned under para 4.44 has

been extended to the authorized offices and

agencies in India of laboratories mentioned under

paragraph 4.74 of handbook of procedures 2015-

2020.

Notification No. 39/ 2015-2020 dated 22

February, 2017

----------------------------------------------------------

Para 4.34 (i) has been amended to provide that

replenishment of precious metal (Gold, Silver and

platinum) shall be allowed only if it is used in the

manufacture of dutiable goods in the factory/unit,

where exported Gems and jewellery products

were manufactured .It is subject to condition that

Cenvat credit on such input has been availed and

products are exported availing rebate.

Sale/Transfer of such duty free precious metal

inputs shall not be allowed.

Notification No. 40/ 2015-2020 dated 23

February, 2017

----------------------------------------------------------

SERVICE TAX

Notification

In exercise of the powers conferred by section 11C

of the Central Excise Act, 1944 (1of 1944) read with

section 83 of the Finance Act, 1994 (32 of 1994),

the Central Government hereby directs that

Service Tax payable under section 66B of the

Finance Act, 1994 for the period 1 July 2012 to 31

March 2015 on Services provided by operators of

Common Effluent Treatment plan by way of

treatment of effluent is no longer required to be

paid.

Notification No. 8/ 2017 dated 20 February, 2017

----------------------------------------------------------

Circular

As per Section 66C of the Finance Act, 1994 read

with Rule 10 of the Place of Provision of Services

Rules, 2012, Service Tax will not be leviable on

services by way of transportation of goods by a

vessel from a place outside India to the customs

stations in India with respect to only such goods

which are intended to be trans-shipped to some

other Country in accordance to provisions of the

Customs Act, 1962.

For Private Circulations Only 20 The Update –February, 2017, SGCO & Co. LLP

Circular No. 204/2/ 2017 dated 16 February, 2017

----------------------------------------------------------

MVAT

Circulars

Improved functionality of new registration and

amendment / cancellation of registration

certificate:

To integrate and align the improved system with

SAP based platform, Maharashtra Sales Tax

Department (MSTD) now wished to provide

added features. This includes features like

1. Integration of Payment Gateway for payment

of fees or deposit or both alongwith

application for new registration;

2. Online facility of application for amendment

or cancellation of registration certificate.

Further, procedures in regard to implementation

of the above amendments have also been

explained in detail.

Detailed circular can be viewed for your reference

at

http://mahavat.gov.in/Mahavat/MyFold/KNOWLE

DGE%20CENTER/TRADE%20CIRCULARS/DateWise

/KNOW_TRADEC_DW_MVAT/KNOW_TRADEC_D

W_MVAT_02_02_17_0_9_27PM.pdf

Trade Circular 4T of 2017 Dated 02 February 2017.

----------------------------------------------------------

As we aware that one of the biggest taxation

reforms in India - Goods and Services Tax (GST), is

all set to be implemented by 1 July 2017 as aimed

by the present governed. In this regard, one of the

step was to enroll the existing dealers registered

under various Act to GST. Enrolment/Registration

under GST has been made open by various States.

Existing taxpayers were liable to enroll under GST

system portal. In connection to above,

Maharashtra state had started enrollment under

GST in various phases for the dealers registered

under MVAT. Phase I was open from 14th

November, 2016 for the dealers registered prior to

31st August, 2015. Phase II was also made open for

the dealers registered after 31st August, 2015.

In the said process, it was required for the dealer

to collect provisional login credentials and based

on such details get itself registered on the GST

portal. Now, if any active dealer from Phase 1 and

Phase 2, who has not collected Provisional Id from

MSTD and have not activated their account on GST

Portal on or before 06-03-2017 then it would be

assumed by MSTD that the dealer is not willing to

enroll for GST for any reason and his Provisional Id

and Access Token presently available with MSTD as

well as in GSTN will be disabled/deleted

permanently. Accordingly, such dealers will not be

eligible for the benefits of transitional Provisions

under the GST Act.

The process for getting enrollment for Phase III

dealers i.e. dealers who were not covered in Phase

1 or Phase 2, for creation of Provisional Id, with

GSTN is expected to start soon. Whereas dealers

from Phase 1 and Phase 2 who have noticed that

their Provisional Ids has been generated on

Incorrect PAN, and accordingly they have applied

for and amended the PANs in registration database

of MSTD. The process of generation and

distribution of fresh Provisional Ids for all such

dealers is under consideration. Fresh Provisional

Ids for these dealers will be issued in Phase 4 and

subsequent phases.

Further, it is necessary for every dealer to submit

the provisional registration application either

through Digital Signed Certificate (DSC) or e-Sign.

For Private Circulations Only 21 The Update –February, 2017, SGCO & Co. LLP

Accordingly, it is proposed that last date for

submitting signed application on GST Portal is 31

March 2017.

Detailed circular can be viewed for your reference

at -

http://mahavat.gov.in/Mahavat/MyFold/KNOWLE

DGE%20CENTER/TRADE%20CIRCULARS/DateWise

/KNOW_TRADEC_DW_MVAT/KNOW_TRADEC_D

W_MVAT_02_28_17_0_11_26PM.pdf

Trade Circular 5T of 2017 Dated 27 February 2017.

----------------------------------------------------------

Other Updates:

1. Facility to view and Print challan / Get Status

for MSTD users and Dealers is made available

from new SAP system

2. Date of Computerized Desk Audit (CDA) for F.Y.

2013-14 is extended up to 28.02.2017.

3. Functionality to upload Returns for the third

quarter (October to December) of 2016 has not

started yet by MSTD. It will be made available

shortly.

----------------------------------------------------------

EXCISE

Circular

Clarification has been bought in relation to

classification of articles of paper and printing

industry with respect to railway/bus/other

tickets/passes, railway ticket rolls and bus ticket

rolls, mark sheets/certificate, OMR sheets/Answer

books with OMR, Answer booklets, inland letter

cards, passbooks, applications forms, paper outer

strip seal, Railway receipt and practical notebook.

Circular No. 1052/01/2017-CX dated 23-02-2017

JUDICIAL RULINGS

Ownership is not the criteria for allowing the

Cenvat credit on capital goods, the only criteria is

that the capital goods should be installed in the

factory of the assesse and used in the

manufacture of final product.

Facts:

The Appellant imported capital goods which

got damaged in transit. However, the

machine was received in the factory premises

of the appellant.

Insurance claim was made, but the insurance

claim did not include the Counter Vailing Duty

(“CVD”) paid on the said capital goods.

Insurance claim was settled after survey

without deducting the salvage amount.

Appellant Company proposed the Insurance

Company for redemption of the capital goods

on payment of Rs. 12 Lakhs.

Capital Goods were retained, installed and put

to use by the Appellant Company.

Accordingly, the appellant Company have

taken Cenvat Credit of the CVD.

The Department denied the Cenvat Credit on

the ground that machine was received in

damaged condition and insurance was

claimed.

After claiming the insurance, the machine did

not belong to the appellant and it is owned by

the New India Insurance Company.

For Private Circulations Only 22 The Update –February, 2017, SGCO & Co. LLP

Subsequently, the Appellant repurchased the

capital goods, hence the credit is not

admissible on the same.

The Order passed by the Adjudicating officer

was agitated by the appellant before

Commissioner (Appeals).

The Commissioner (Appeals) also confirmed

the demand and therefore the appellant has

filed an appeal before CESTAT.

Both the parties made additional submission

before the CESTAT.

The Appellant stated that credit was availed of

CVD paid on the machine even though the

machine was damaged. Insurance Claim was

made subsequently after repairing the same.

The Machine was used in the factory premises

of the Appellant.

The Appellant further submits that even

though the ownership does not remain with

the appellant for time being the same

machine was used in the factory of the

appellant, therefore even though in the

intervening period the ownership was not of

appellant but the capital goods was lying in

the factory and subsequently used, hence

Cenvat credit cannot be denied. Reliance has

been placed on the judgement of M/s.

Mahadev Industries vs. CCE [2000 (115) ELT

452 (T)] and CCE vs. Modernova Plastyles P.

Ltd. 2015 (323) ELT 312 (Bom).

Further the Department contended that when

the ownership of the capital goods did not

remain with the appellant after taking claim

from insurance company they were not

entitled to take Cenvat credit. He submits that

as against the claim of Rs.2 crores, they have

repurchased the machine from the insurance

company only on an amount of Rs.12 lakhs

including sales tax. Therefore, for this reasons

also credit should not be allowed. He submits

that the ownership is important criteria for

allowing the credit. Reliance has been placed

in the case of CCE vs. Associated Cement Co.

Ltd. 2009 (236) ELT 240 (Kar.)

Held:

The CESTAT aft considering the submissions made

by both the parties and made the following

observations as follows:

After receipt of the capital goods, the

damaged machine was lying in the factory of

the appellant. Subsequently, the same

machine was used by the appellant. It is also

fact that appellant had not claimed the

insurance in respect of CVD amount.

Even though for intervening period, after

insurance claim, the ownership of the

machine transferred to the insurance

company and thereafter the appellant has

taken the ownership after making payment of

Rs.12 lakhs, the fact remains that the capital

goods remained in the factory of the

appellant subsequently installed and used by

them.

The ownership is not the criteria for allowing

the credit on capital goods. The only criteria is

that the capital goods should be installed in

the factory of the Appellant and used in the

manufacture of final product which is not in

dispute in the present case also. As regards

judgment relied by the Department in the

case of Associated Cement Co. Ltd. (supra), in

the said judgment the fact was that the capital

goods was sold by the assessee and the buyer

was using that machine for generation of

power and the power generated was being

supplied to the assessee.

For Private Circulations Only 23 The Update –February, 2017, SGCO & Co. LLP

In the present case the capital goods was

installed and used by the appellant, therefore,

the fact of the present case is entirely

different from Associated Cement Co. Ltd.'s

case.

Hence, the CENVAT Credit availed by the

Appellant is legally admissible and the

impugned order is set aside.

Tata Motors Limited vs. Commissioner of Central

Excise, Pune-I [2017-TIOL-603-CESTAT-MUM]

------------------------------------------------------------------

For Private Circulations Only 24 The Update –February, 2017, SGCO & Co. LLP

MCA UPDATES

Reference No- General Circular No.

01/2017:-

Section 391 of the Companies Act, 2013, states

that provision of Chapter XX shall apply to mutatis

mutandis for closure of the place of business of a

Foreign company in India as if it were a company

incorporated in India. These provisions have been

bought into force on 15th December, 2016.

Stakeholders sought clarification with regard to

scope of application of the said sub-section.

As per sub section (1) and sub section (2) of section

391 needs to be read harmoniously. Accordingly, it

is clarified that provisions of sub-section (2) of

Section 391 of the Companies Act, 2013 would

apply only in case of Foreign Company which has

issues prospectus or IDRs pursuant to provisions of

Chapter XXII of the Companies Act, 2013.

Dated 22nd February, 2017

NEW RULES OF THE GAME FOR CORPORATE

RESTRUCTURING, AMALGAMATION ETC.

UNDER NCLT

Government of India has recently notified

provisions of the Companies Act, 2013 (the 2013

Act) relating to merger, amalgamation, winding-up

etc., which will now be exercised by National

Company Law Tribunal (NCLT), a quasi-judicial

authority. NCLT is envisioned as a fast track

dedicated quasi-judicial forum for handling

matters arising under the 2013 Act, Insolvency and

Bankruptcy Code 2016 and other legislations.

Persons who can represent a case before NCLT

now includes professionals like Chartered

Accountants, Company Secretaries and Cost and

Management Accountants in addition to legal

practitioners. 11 benches of NCLT have been

constituted which will have jurisdiction over

various States / Union Territories of India. FDI can

be made through two routes viz. Automatic Route

& Approval Route

Illustrative matters requiring NCLT approval

Scheme of arrangement, merger, demerger

Reduction of capital including securities

premium

Conversion of public company into private

company

Re-opening of books of account and recasting

of financial statements

Consolidation or division of share capital

resulting in change in voting percentage of

shareholders

Change in financial year of company (other

than April-March)

Voluntary revision of financial statements or

Board’s Report

For Private Circulations Only 25 The Update –February, 2017, SGCO & Co. LLP

Compounding of offences

Approval of revival plan of delinquent

corporate debtor

Winding-up of companies / LLPs

HIGHLIGHTS OF CHANGES HAVING IMPLICATIONS

ON CORPORATE RESTRUCTURING SUCH AS

AMALGAMATION, DE-MERGER ETC.

Certificate from statutory auditor to be filed

with NCLT that the accounting treatment in

the Scheme is in accordance with Accounting

Standards;

Valuation to be done by a registered valuer.

Till registered valuer provisions are notified,

valuation by independent merchant banker

registered with SEBI or independent

practicing chartered accountant having

minimum experience of 10 years

Joint application for sanction of the Scheme

can be filed

Meeting of creditors may be dispensed with if

90% in value agree and confirm to the Scheme

through an affidavit

Purchase of equity shares of minority

shareholders by 90% shareholder (acquirer

and person acting in concert or any person or

group of persons)

Notice of shareholders’ / creditors’ meeting

should also be filed with Income tax

authorities, RBI, SEBI, CCI, stock exchanges

and other sectoral regulators/authorities

which are likely to be affected.

Objection to the scheme can be made only by

persons holding at least 10% of shareholding

or having outstanding debt of at least 5% of

total debt NCLT is expected to ease the

burden on the judiciary and speed-up the

process relating to reorganization of

companies.

For Private Circulations Only 26 The Update –February, 2017, SGCO & Co. LLP

For Private Circulations Only 27 The Update ‐ February, 2017, SGCO & Co. LLP

Upcoming Due Dates

March 2017

Income Tax 2nd ‐ Due date for furnishing of challan cum

statement in respect of tax deducted u/s 194‐IA in the month of January, 2017.

7th ‐ TDS/TCS payment for February 2017 15th ‐ Payment of fourth instalment of Advance

Tax for AY 2017‐18. 15th – Due date for furnishing of form 24G by an

office of the Govt where TDS for the month of February, 2017 has been paid without the production of challan.

15th ‐ Advance tax payment of whole amount of advance tax in respect of AY 2017‐18 for assesses covered under presumptive scheme of Section 44AD.

17th – Due date for furnishing of certificate of TDS to payee in respect of tax deducted u/s 194‐IA in the month of January, 2017

30th Due date for furnishing of challan cum statement in respect of tax deducted u/s 194‐IA in the month of February, 2017

31st ‐ Last date for declaration of undisclosed income under Pradhan Mantri Garib Kalyan Yojana, 2016.

31st Due date for payment of second instalment (i.e., 25% of tax, surcharge and penalty) under Income Declaration Scheme, 2016.

31st ‐ Belated Income/Wealth tax return AY16‐17 31st – Last date of filing return Income for AY

2015‐16 to avoid penalty u/s. 271F

MVAT/CST/PT 2nd ‐ MVAT/CST return for month ending Jan’ 17 21st ‐ MVAT/CST payment for month ending Feb’

17 21st ‐ WCT/ TDS payment for month of Feb’ 2017

if deducted 21st ‐ MVAT/CST monthly return for Feb’17 in case

where there is NIL VAT liability/refund cases

April 2017

Income Tax 7th ‐ TDS/TCS payment for March, 2017 14th ‐ Due date for furnishing of certificate

of TDS to payee in respect of tax deducted u/s 194‐IA in the month of February, 2017.

30th – Due date for furnishing of Form 24G by an office of the Govt where TDS for the month of March, 2017 has been paid without the production of challan.

30th Due date for deposit of Tax deducted by an assessee other than an office of the Govt. for the month of March, 2017

30th – Due date of e‐filing of a statement in Form No.61 containing particulars of Form No. 60 received during the period October1, 2016 to March 31, 2017.

MVAT/CST/PT 21st ‐ MVAT/CST payment for month / quarter

ending Mar’ 17 21st‐ WCT/ TDS payment for month of Mar’

2017 if deducted 21st ‐ MVAT/CST monthly return for Mar’17

in case where there is NIL VAT liability/refund cases.

For Private Circulations Only 28 The Update ‐ February, 2017, SGCO & Co. LLP

Upcoming Due Dates

March 2017

Income Tax 2nd ‐ Due date for furnishing of challan cum

statement in respect of tax deducted u/s 194‐IA in the month of January, 2017.

7th ‐ TDS/TCS payment for February 2017 15th ‐ Payment of fourth instalment of Advance

Tax for AY 2017‐18. 15th – Due date for furnishing of form 24G by an

office of the Govt where TDS for the month of February, 2017 has been paid without the production of challan.

15th ‐ Advance tax payment of whole amount of advance tax in respect of AY 2017‐18 for assesses covered under presumptive scheme of Section 44AD.

17th – Due date for furnishing of certificate of TDS to payee in respect of tax deducted u/s 194‐IA in the month of January, 2017

30th Due date for furnishing of challan cum statement in respect of tax deducted u/s 194‐IA in the month of February, 2017

31st ‐ Last date for declaration of undisclosed income under Pradhan Mantri Garib Kalyan Yojana, 2016.

31st Due date for payment of second instalment (i.e., 25% of tax, surcharge and penalty) under Income Declaration Scheme, 2016.

31st ‐ Belated Income/Wealth tax return AY16‐17 31st – Last date of filing return Income for AY

2015‐16 to avoid penalty u/s. 271F

MVAT/CST/PT 2nd ‐ MVAT/CST return for month ending Jan’ 17 21st ‐ MVAT/CST payment for month ending Feb’

17 21st ‐ WCT/ TDS payment for month of Feb’ 2017

if deducted 21st ‐ MVAT/CST monthly return for Feb’17 in case

where there is NIL VAT liability/refund cases

April 2017

Income Tax 7th ‐ TDS/TCS payment for March, 2017 14th ‐ Due date for furnishing of certificate

of TDS to payee in respect of tax deducted u/s 194‐IA in the month of February, 2017.

30th – Due date for furnishing of Form 24G by an office of the Govt where TDS for the month of March, 2017 has been paid without the production of challan.

30th Due date for deposit of Tax deducted by an assessee other than an office of the Govt. for the month of March, 2017

30th – Due date of e‐filing of a statement in Form No.61 containing particulars of Form No. 60 received during the period October1, 2016 to March 31, 2017.

MVAT/CST/PT 21st ‐ MVAT/CST payment for month / quarter

ending Mar’ 17 21st‐ WCT/ TDS payment for month of Mar’

2017 if deducted 21st ‐ MVAT/CST monthly return for Mar’17

in case where there is NIL VAT liability/refund cases.

For Private Circulations Only 29 The Update ‐ February, 2017, SGCO & Co. LLP

Upcoming Due Dates

March 2017

Income Tax 2nd ‐ Due date for furnishing of challan cum

statement in respect of tax deducted u/s 194‐IA in the month of January, 2017.

7th ‐ TDS/TCS payment for February 2017 15th ‐ Payment of fourth instalment of Advance

Tax for AY 2017‐18. 15th – Due date for furnishing of form 24G by an

office of the Govt where TDS for the month of February, 2017 has been paid without the production of challan.

15th ‐ Advance tax payment of whole amount of advance tax in respect of AY 2017‐18 for assesses covered under presumptive scheme of Section 44AD.

17th – Due date for furnishing of certificate of TDS to payee in respect of tax deducted u/s 194‐IA in the month of January, 2017

30th Due date for furnishing of challan cum statement in respect of tax deducted u/s 194‐IA in the month of February, 2017

31st ‐ Last date for declaration of undisclosed income under Pradhan Mantri Garib Kalyan Yojana, 2016.

31st Due date for payment of second instalment (i.e., 25% of tax, surcharge and penalty) under Income Declaration Scheme, 2016.

31st ‐ Belated Income/Wealth tax return AY16‐17 31st – Last date of filing return Income for AY

2015‐16 to avoid penalty u/s. 271F

MVAT/CST/PT 2nd ‐ MVAT/CST return for month ending Jan’ 17 21st ‐ MVAT/CST payment for month ending Feb’

17 21st ‐ WCT/ TDS payment for month of Feb’ 2017

if deducted 21st ‐ MVAT/CST monthly return for Feb’17 in case

where there is NIL VAT liability/refund cases

April 2017

Income Tax 7th ‐ TDS/TCS payment for March, 2017 14th ‐ Due date for furnishing of certificate

of TDS to payee in respect of tax deducted u/s 194‐IA in the month of February, 2017.

30th – Due date for furnishing of Form 24G by an office of the Govt where TDS for the month of March, 2017 has been paid without the production of challan.

30th Due date for deposit of Tax deducted by an assessee other than an office of the Govt. for the month of March, 2017

30th – Due date of e‐filing of a statement in Form No.61 containing particulars of Form No. 60 received during the period October1, 2016 to March 31, 2017.

MVAT/CST/PT 21st ‐ MVAT/CST payment for month / quarter

ending Mar’ 17 21st‐ WCT/ TDS payment for month of Mar’

2017 if deducted 21st ‐ MVAT/CST monthly return for Mar’17

in case where there is NIL VAT liability/refund cases.

For Private Circulations Only 31 The Update –March, 2017, SGCO & Co. LLP

M u m b a i

Disclaimer

This newsletter is prepared strictly for private circulation and personal use only. The newsletter is for general guidance on matters of interest only and does not constitute any professional advice from us. One should not act upon the information contained in this newsletter without obtaining specific professional advice. Further, no representation or warranty (expressed or implied) is given as to the accuracy or completeness of the information contained in this newsletter. This newsletter (and any extract from it) may not be copied, paraphrased, reproduced, or distributed in any manner or form, whether by photocopying, electronically, internet, within another document or otherwise, without the prior written consent of S G C O & Co

4A, Kaledonia-HDIL, 2nd Floor, Sahar Road, Near Andheri Station, Andheri (East), Mumbai - 400 069. India

Tel.: +91 22 6625 6363 Fax: +91 22 6625 6364 E-Mail: [email protected] Web: www.sgco.co.in