more business with ira's keller williams blue bell jan 19

TRANSCRIPT

Build Wealth….

Your WayThrough Self-Directed Retirement Plans

Investing In Traditional & Non-Traditional Assets Using Self-Directed Retirement Plans (IRAs/401Ks)

Keller Williams - Blue Bell, PA January 2012

More Business with IRAs

Disclosure

CAMA Self-Directed IRAs, LLC, does not provide investment advice or endorsements.

All information and materials contained are provided for educational purposes only. All parties are encouraged to consult with their attorneys, accountants and financial advisors before entering into any type of investments.

Too Good to Be True?• Increase sales and commissions• Additional tools few others use• New clients you already know• Little or no cost to you• Bypass bank loan problems• Use your expertise to grow your wealth and

your clients wealth

Agenda• What is Self-Direction?• Types of Assets or Investments Allowed• Plan Types & Why People Use It• Step By Step Summary• IRS Rules and Regulations• The Role of CAMA• Who Can Use Self-Direction?• What to do next? Push back?

What is a “Self-Directed” IRA?

An IRA in which the IRA owner directs all investments in the account. There is no legal distinction between a “self-directed IRA” and any other IRA except with a truly self-directed IRA the account agreement allows the broadest possible spectrum of investments.

Statement Comparison

Assets:

CashFidelity Freedom FundFidelity Growth Fund

Assets:

CashReal Estate

Secured Notes

Allowable Investments

• Real Estate• Precious Metals• Notes/Mortgages• Private Placements• Other

Allowable Assets & Investments

Real Estate • Single family and multi-unit homes

• Apartments

• Condominiums

• Commercial Property

• Improved or un-improved land

• Leveraged and un-leveraged property

• Foreign property investments

Real Estate

Allowable Assets & Investments

Precious Metals • Gold

• Silver

• Palladium

• Certain coins and bullion

(see restrictions)

Precious Metals

Allowable Assets & Investments

Loans & Notes • Mortgages

• Promissory Notes

• Trust Deeds

• Leases

• Convertible Notes

• Discounted Notes

• Secured/Unsecured Notes

• Short-term/Long-term Notes

Loans/Notes

Allowable Assets & Investments

Private Placements • LLC’s

• LP’s

• Trusts

• Corporations (S-Corp prohibited)

• Joint Ventures

• Investment Clubs

• Structured Settlements

• Hedge Funds

Other Allowable Assets• Tax Liens

• Commodities/futures

• Securities, certificates of deposits, stocks, bonds

• Mutual funds

• Oil & gas rights

• Contracts of sale

• Accounts receivable financing

• Auto/commercial paper

• Other – Boat, car, trailer, sports tickets, etc.

• Anything the IRS does not prohibit

Collectibles & Life Insurance• Any Work of Art• Any Rug or Antique• Any Metal or Gem• Any Stamp or Coin• Any Alcoholic Beverage

*Exception • US Government Minted Gold Or Silver Eagle, Gold and

Palladium Bullion

Prohibited Investments

More sales

How can I profit NOW?

How can I profit NOW?

Create your own private financing source

Partnering with OPI

How can I profit NOW?

Raising investment capital

How can I profit NOW?

There are TRILLIONS of dollars in retirement accounts!

How can I profit NOW?

At every gathering there are MILLIONS of dollars available for investment.

How can I profit NOW?

Spread the knowledge about self-directed plans, then help them invest their money!

How can I profit NOW?

Types of Plans That Can Be Self-Directed

Plans That Can Be Self-Directed

IRAs Retirement Plans

Other Accounts

Roth IRA & Traditional

401KsPre & Post Tax

HSA (Health Savings Accounts)

SEP & SIMPLE Defined Contribution

ESA (Educational Savings Accounts)

Spousal & Custodial

Defined Benefit = Tax Free

Types of Self-Directed PlansTax Deferred

• Traditional IRA• Spousal IRA• Simplified Employee

Pension (SEP)• Savings Incentive Match

for Employees of small employers (SIMPLE)

• Defined Benefit Plan• Defined Contribution

Tax Free

• Roth IRA

• Health Savings Account

(HSA)

• Roth like 401k (2006)

• Coverdell (Educational)

“Invest in what you know, understand and can control” Vs. Using “Hope” as your strategy.

Key Benefit of Having a Self-Directed IRA/401K

Account Comparison

$50,000

$50,000

$50,000

$129,687$110,589

$98,358

$336,375

$235,462$193,484

$872,470

$610,729

$380,613

$2,262,963

$1,584,074

$748,723

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

Start 10 yr 20 yr 30 yr 40 yr

Tax-Free Tax-Deferred Taxable

Types of MoneyTypes of Money You Make Taxes

W2 – Salaries, 1099

$60,000Fed: 0—35%State: 0—10%Local: 0—4%SS/Med – 7.65% (you) + 7.65% (employer) = 15.3%

Passive – Rent, Royalties, Interest, Dividends and Capital Gains $75,000

0—49%

Tax Deferred – Traditional, etc. $100,000*0% - taxed when taken

Tax Free – Roth, HSA, ESA $100,0000%

IRS Rules and Regulations

Prohibited Transactions & Disqualified Persons

Disqualified People / Parties

Business Entities

owned 50% or more

by a “Related

Party”

Parents

You

Kids Spouse

Spouse

Spouse

Fiduciary “F”(includes IRA Owner)

Member of F’s Family

Corporation “C” if F owns

(directly or indirectly)50% or more of vote or

value of stock

Partnership “P” if F owns

(directly or indirectly)50% or more of capital or profits interest in P

Trust or Estate “T” if F owns

(directly or indirectly)50% or more of

Beneficial interest in T

10% or more

partner or joint

venture with CF’s Spouse

F’s Ancestor

F’s LinealDescendant “LD”

LD’s Spouse

Officer or Director of C

Highly Compensated Employee of C (10%

or more of wages)

10% or more shareholder of C

Person with management

or administrative functions of P

Highly Compensated Employee of P

(10% or more of wages)

10% or more partner of P

Trustee of T

Highly Compensated Employee of T (10%

or more of wages)

10% or more beneficial interest

owner of T

10% or more

partner or joint

venture with P

10% or more

partner or joint

venture with T

IRA

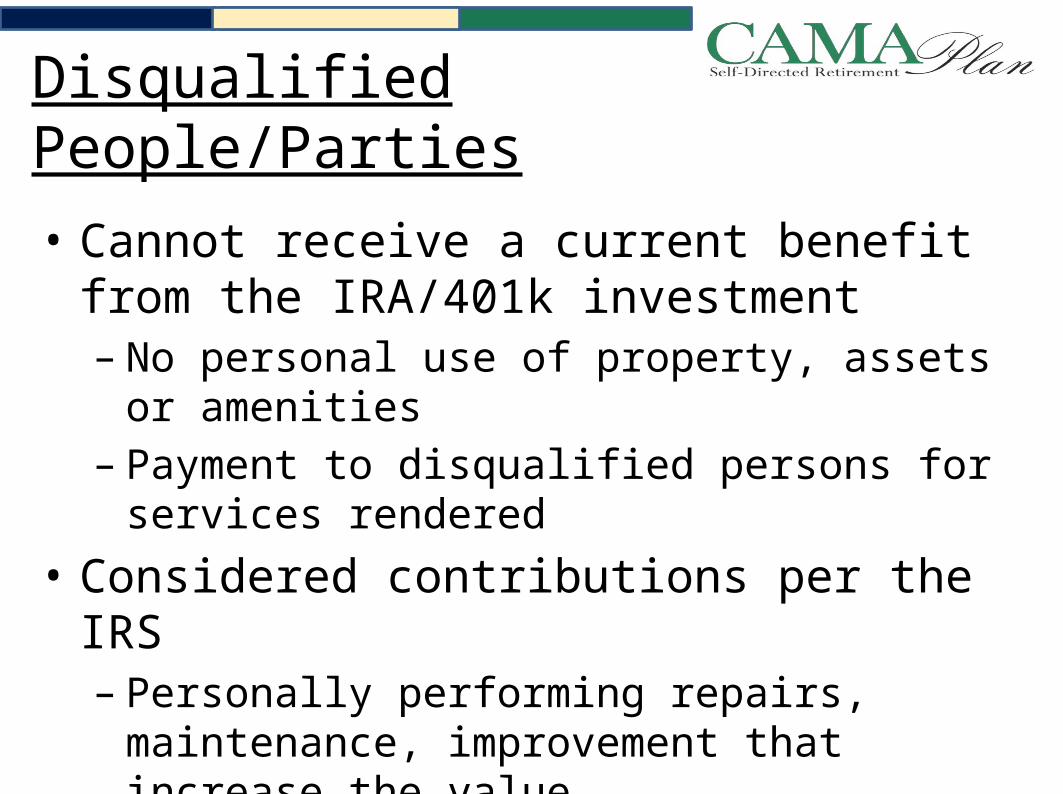

Disqualified People/Parties

• Cannot receive a current benefit from the IRA/401k investment– No personal use of property, assets or amenities– Payment to disqualified persons for services rendered

• Considered contributions per the IRS– Personally performing repairs, maintenance,

improvement that increase the value – Pay for services from any account other than IRA

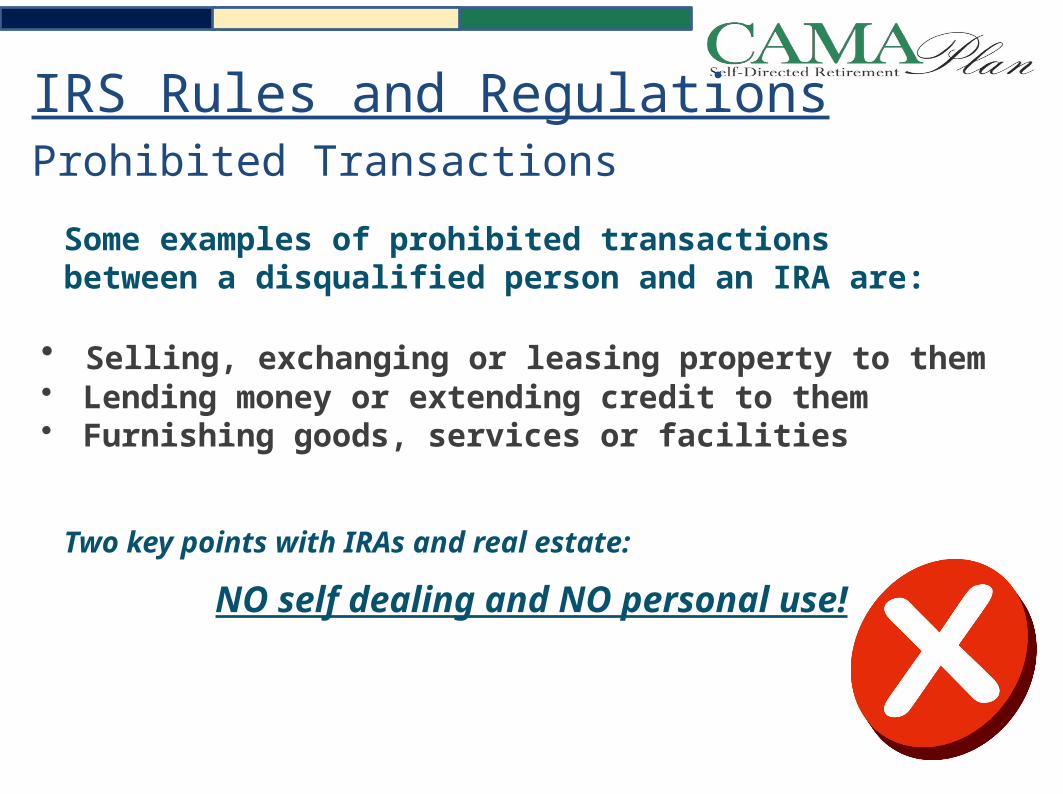

Some examples of prohibited transactions between a disqualified person and an IRA are:

• Selling, exchanging or leasing property to them• Lending money or extending credit to them • Furnishing goods, services or facilities

Two key points with IRAs and real estate:

NO self dealing and NO personal use!

IRS Rules and RegulationsProhibited Transactions

What Does CAMA SDIRA Do?• The IRS requires you to use a neutral 3rd party to open a self-

directed IRA – we provide that service.• No investment advice or products to sell.• We specialize in the legal (IRS-approved) use of tax-free and

tax-deferred retirement and savings plans for traditional and non-traditional investments.

• Relieve the administrative burdens associated with transactions.

• Keep records of all transactions and report to the IRS.• Part of your professional advisory team.

Who Can Use Self-Direction?

Does she care about an IRA or ESA or HSA?

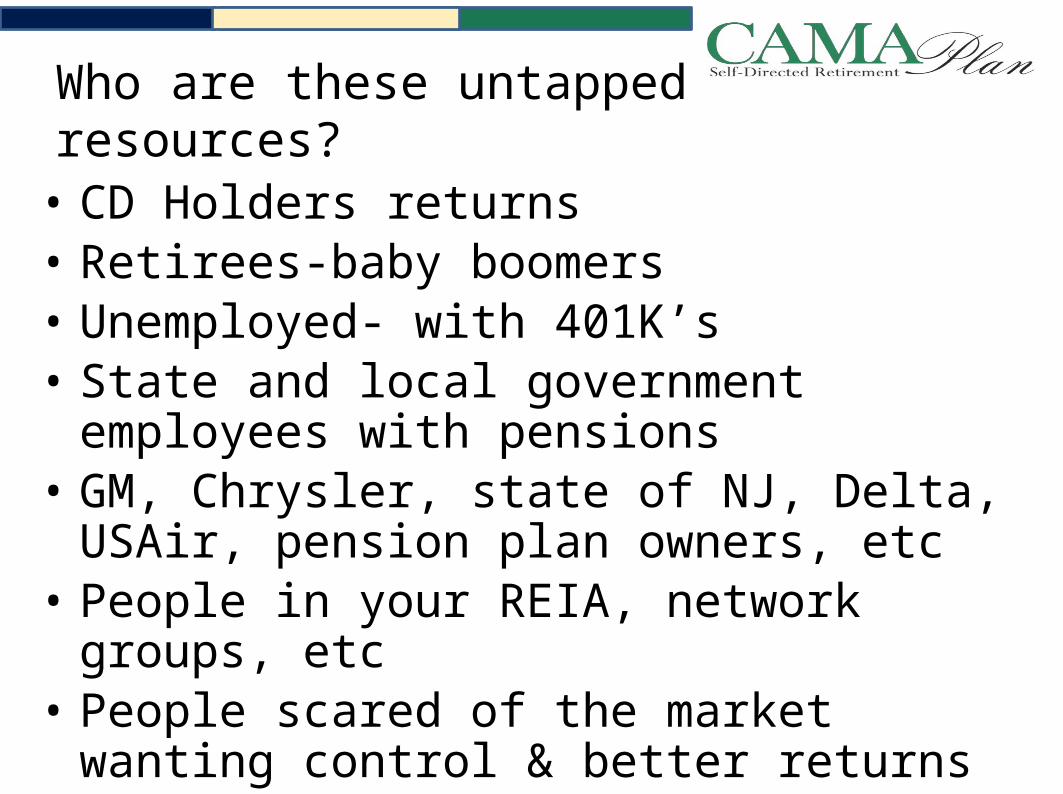

Who are these untapped resources?

• CD Holders returns• Retirees-baby boomers• Unemployed- with 401K’s• State and local government employees with

pensions• GM, Chrysler, state of NJ, Delta, USAir, pension

plan owners, etc • People in your REIA, network groups, etc• People scared of the market wanting control &

better returns

What Next? (Free)• Talk to investors – let them know• Add information to your collateral material • Link to CAMA SDIRA website • Publish article in your newsletter – ask me for one• Put SDIRA collateral material in your office• Set-up a class with your investors• Give me your contact information and receive

newsletter you can forward to clients.

What Next? (Minimal Cost)

• Attend webinars, workshops, seminars – see attached

• Invite your clients to attend classes.• Read books on the subject – see attached• Open an account ($50 one time)

Additional Reading

Books• How to Purchase Real Estate with Your IRA/401K and

Pay Little or No Taxes - Hubert Bromma• We Buy Houses Sometimes - Michele Gorman and

Mark Halpern• How Not To Go Broke At 102 - Adriane Berg• Real Estate Investment Using Self Directed IRAs an

Other Retirement Plans - Dyches Boddiford Quincy Long, George Yeiter

Additional Reading

Court Cases– James H. Swanson, et ux. v. Commissioner, 106 TC 76, Code Sec(s)

4975; 7430 - LLC’s and checkbook control– Tax Court & Board of Tax Appeals Memorandum Decisions Joseph R.

Rollins v. Commissioner, TC Memo 2004-260 , Code Sec(s) 4975 - Control and ownership of LLC’s

• Adler Advisory Opinion Letter2000 - 10A ERISA Sec. 4975(c)(1) - Family ownership

• Investing in Entities - General guidelines -- call CAMA for an emailed version

Sessions to Attend

• Upcoming events - Webinars, Seminars, Meetings:

– Every Wed at Noon: Webinars on multiple subjects– Mon & Thu 9:00am – Office visit and information

exchange– Visit our website for other events recorded free

For you or your clients

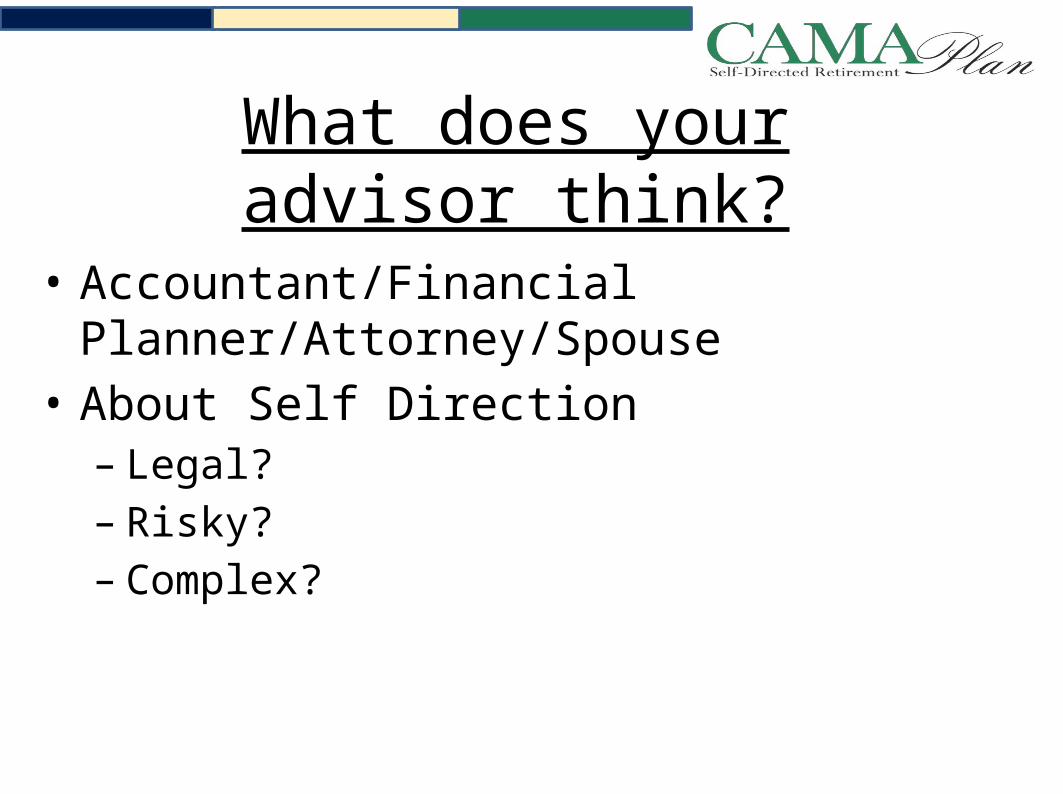

What does your advisor think?

• Accountant/Financial Planner/Attorney/Spouse• About Self Direction– Legal?– Risky?– Complex?

IRS Info for the Doubtful• Publications & Regulations– Prohibited Transactions - IRS Reg. Sect 4975, Pub 514– Unrelated Business Income Tax Pub 598– IRA’s Pub 590 and 5305– Retirement Plans Pub 560– Education Pub 970– Pub 969HSA, Form 8889– Form 990T

• Private Letter Rulings (www.camaplan.com)• Court Cases (www.camaplan.com)

Thank You!

Contact Information:Carl Fischer, Principaltoll free [email protected]

www.CAMAPlan.com-List of CAMA events and seminars.-Educational webinar recordings.