morgan stanley ceo unplugged 010308 -...

TRANSCRIPT

Morgan Stanley CEOs UnpluggedJanuary 3, 2008

Matthew Emmens, CEOShire plc

2

Introduction

Strategy on track

Excellent third quarter results

Strong product sales reflecting good results and successful product launches across all areas of our business

Upgrading revenue growth guidance to at least 30% (previous guidance: at least 25%)

3

How the Shire strategy is working

6 launches in past two years: FOSRENOL, ELAPRASE, DAYTRANA, LIALDA, VYVANSE, DYNEPO

100% track record of approvals or “approvables” in past four years

Strong intellectual property for key growth driving products

Focus on orphan drugs and specialist products fulfilling unmet needs

Global expansion into new markets (South America, Russia, Mexico, Australia, Japan)

Revenue growth

2006 = 12%

2007 latest published guidance recently upgraded to at least 30%

4

Strong market exclusivity for growth drivers

2012

2016

2018

2020

2023

2012

2010

2012

2013

2009

2000 2005 2010 2015 2020 2025

DYNEPO

ELAPRASE*

FOSRENOL

LIALDA^

VYVANSE

Patent Life Regulatory Exclusivity

^ Currently difficult generic approval pathway for locally acting drugs*Orphan Drug

EU 2017

VYVANSE – Launch update

6

VYVANSE is positioned as a new class of ADHD medication not just a replacement to AXR

7

Key attributes to support VYVANSE as an NCE in a new class

The first Pro-drug Stimulant

Consistent time to maximum concentration of d-amphetamine from patient to patient

Significant efficacy throughout the day, even at 6:00 PM

Adverse event profile that is mild to moderate in severity and incidence decreases over time

Significantly lower abuse related liking effect than an equivalent oral dose of d-amphetamine

5

8

05000

1000015000200002500030000350004000045000

6-Jul20-Jul

3-Aug17-Aug

31-Aug14-Sep

28-Sep12-Oct

26-Oct9-Nov

23-Nov7-Dec

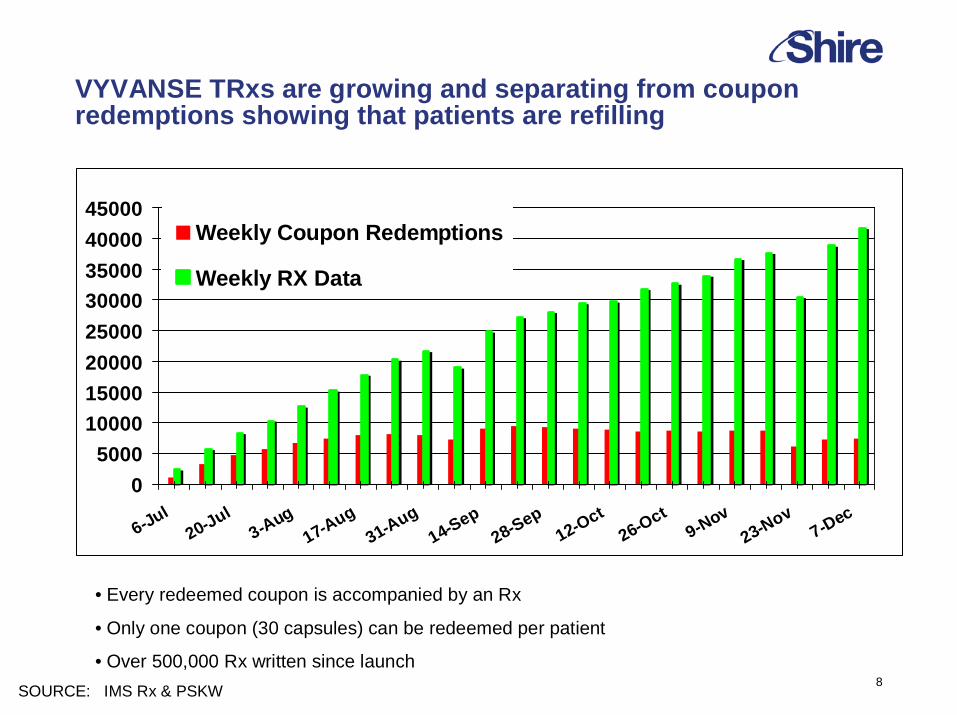

Weekly Coupon Redemptions

Weekly RX Data

SOURCE: IMS Rx & PSKW

• Every redeemed coupon is accompanied by an Rx

• Only one coupon (30 capsules) can be redeemed per patient

• Over 500,000 Rx written since launch

VYVANSE TRxs are growing and separating from coupon redemptions showing that patients are refilling

9

10,045 patients started on VYVANSE have enrolled and completed baseline surveys

At baseline, 84% had used a prescription for ADHD prior to VYVANSE

N = 10,045 Source: VYVANSE New Start Patient Experience program

16%

39%14%

6%

11%4% 10% No Prior

Adderall XRConcertaDaytranaFocalin XRStratteraOther

VYVANSE patients reported coming from ADDERALL XR and other brands

10

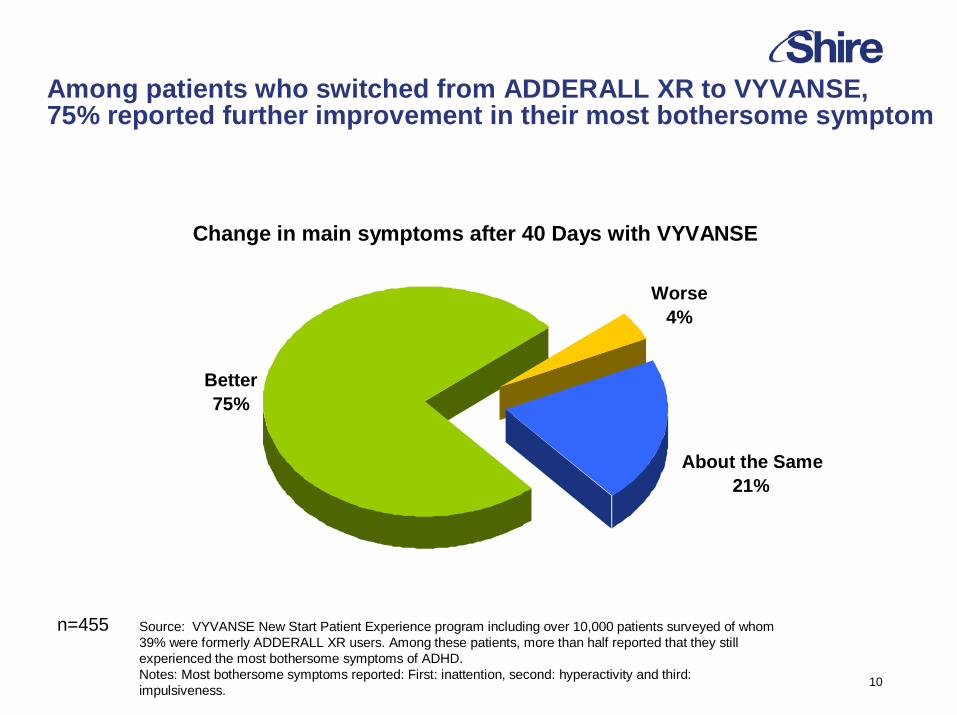

n=455 Source: VYVANSE New Start Patient Experience program including over 10,000 patients surveyed of whom 39% were formerly ADDERALL XR users. Among these patients, more than half reported that they still experienced the most bothersome symptoms of ADHD. Notes: Most bothersome symptoms reported: First: inattention, second: hyperactivity and third: impulsiveness.

Change in main symptoms after 40 Days with VYVANSE

Worse4%

About the Same21%

Better75%

Among patients who switched from ADDERALL XR to VYVANSE, 75% reported further improvement in their most bothersome symptom

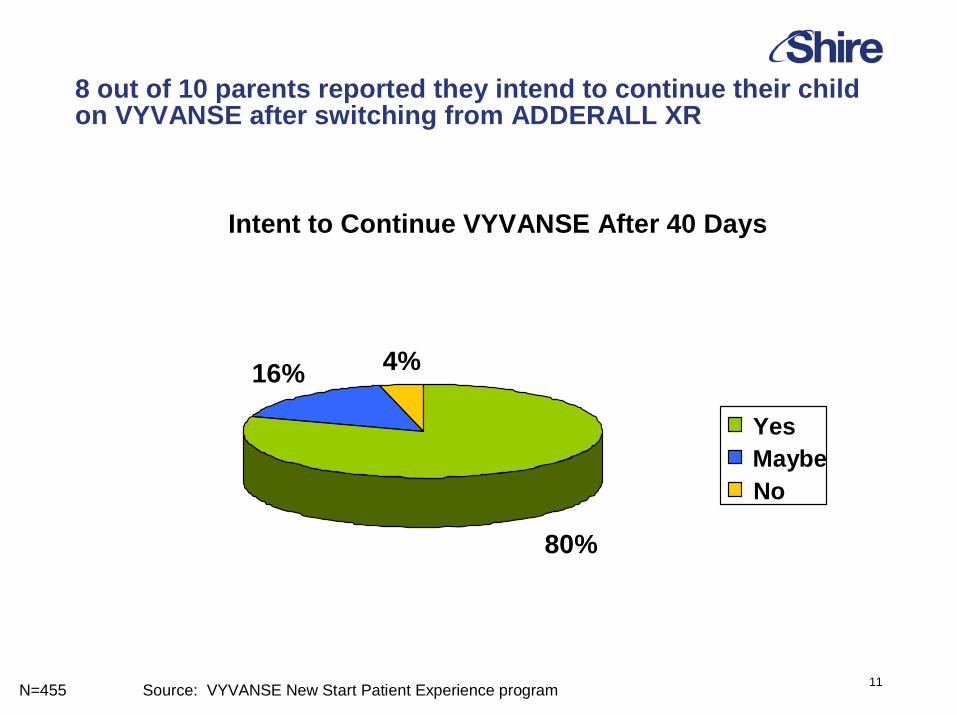

11N=455 Source: VYVANSE New Start Patient Experience program

Intent to Continue VYVANSE After 40 Days

80%

16% 4%

YesMaybeNo

8 out of 10 parents reported they intend to continue their childon VYVANSE after switching from ADDERALL XR

12

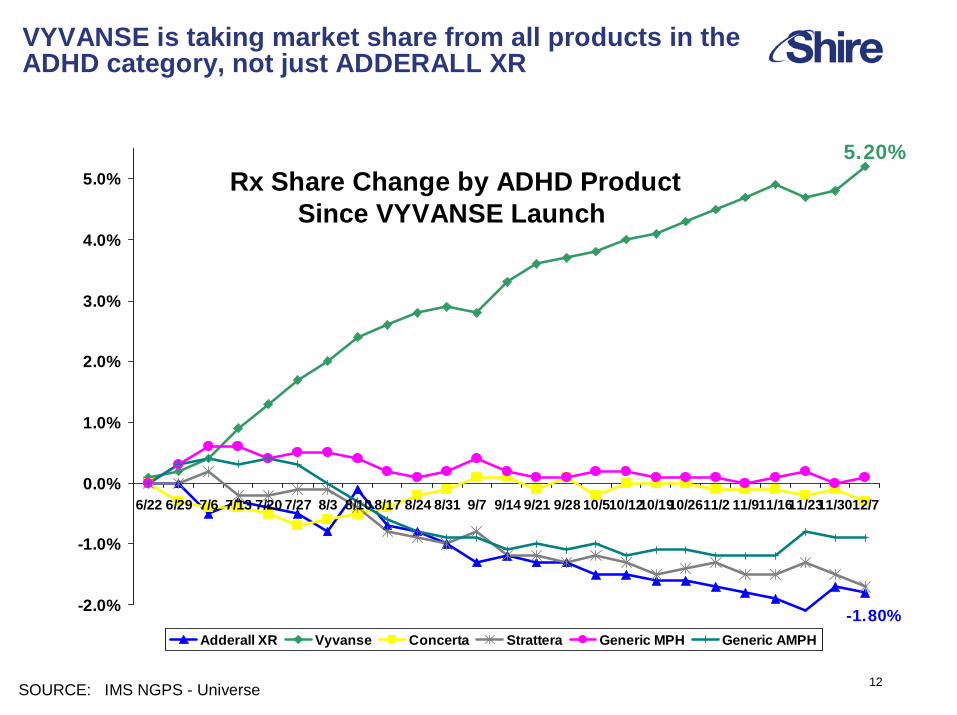

-1.80%

5.20%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6/22 6/29 7/6 7/13 7/20 7/27 8/3 8/10 8/17 8/24 8/31 9/7 9/14 9/21 9/28 10/510/1210/1910/2611/2 11/911/1611/2311/3012/7

Adderall XR Vyvanse Concerta Strattera Generic MPH Generic AMPH

SOURCE: IMS NGPS - Universe

VYVANSE is taking market share from all products in the ADHD category, not just ADDERALL XR

Rx Share Change by ADHD ProductSince VYVANSE Launch

13

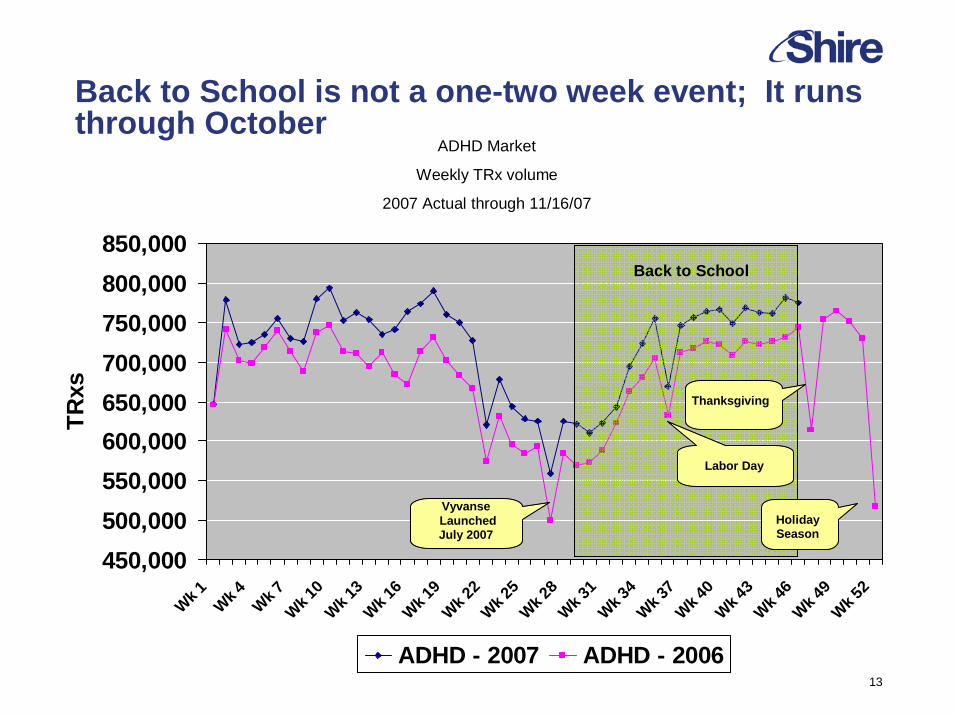

450,000500,000550,000600,000650,000700,000750,000800,000850,000

Wk 1 Wk 4 Wk 7Wk 1

0Wk 1

3Wk 1

6Wk 1

9Wk 2

2Wk 2

5Wk 2

8Wk 3

1Wk 3

4Wk 3

7Wk 4

0Wk 4

3Wk 4

6Wk 4

9Wk 5

2TR

xs

ADHD - 2007 ADHD - 2006

VyvanseLaunched July 2007

Labor Day

Holiday Season

ADHD Market

Weekly TRx volume

2007 Actual through 11/16/07

Back to School

Thanksgiving

Back to School is not a one-two week event; It runs through October

14

Managed Care update

Coverage is progressing as planned:

6-9 month post-launch review period on adding new products to formulary is common

Early success – 3 of top 6 targeted MCO’s have added VYVANSE with preferred status

Negotiations with numerous plans are progressing

Parity with ADDERALL XR formulary status expected by 18 months

15

VYVANSE Summary

VYVANSE rapid launch uptake – 5.2% market share as of week 12/7/07

Tracking in line with the industry’s best successor molecule launches

Patients starting on coupons are refilling Rxs

Back to school is not a one-two week event, but lasts a few months

Physicians and Patients are providing very positive feedback on their clinical experience with VYVANSE

Managed Care coverage is progressing as planned

VYVANSE has tremendous growth potential beyond 2009

Very strong IP

Europe

Potential for other indications

SOURCE: IMS NGPS – as at November 16, 2007

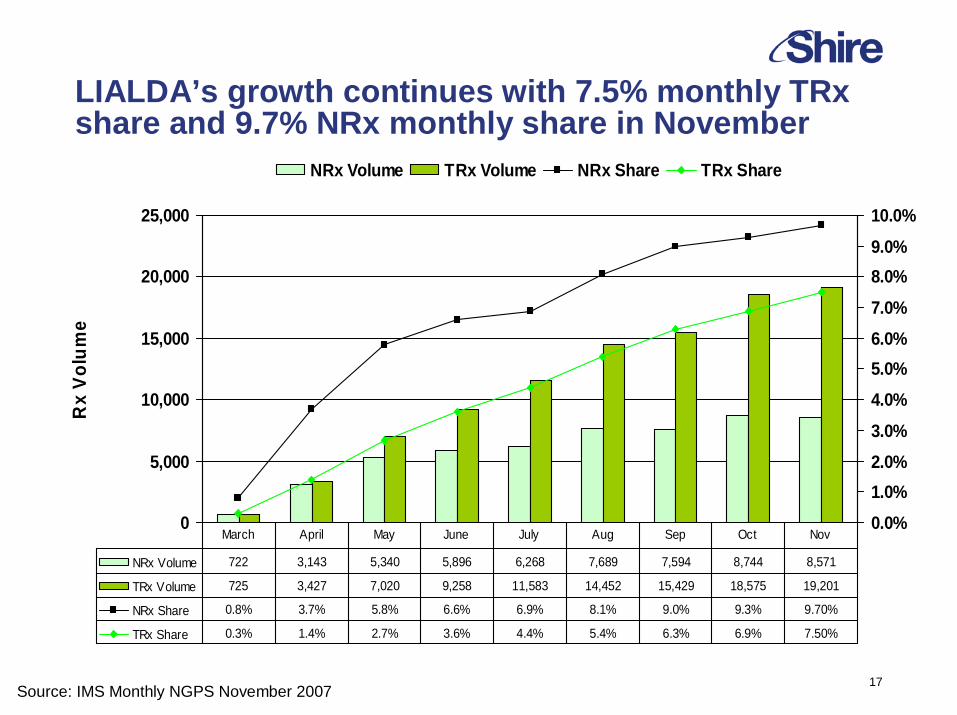

LIALDA – Launch update

17

0

5,000

10,000

15,000

20,000

25,000

Rx

Volu

me

0.0%1.0%2.0%3.0%

4.0%5.0%6.0%7.0%

8.0%9.0%

10.0%

NRx Volume TRx Volume NRx Share TRx Share

NRx Volume 722 3,143 5,340 5,896 6,268 7,689 7,594 8,744 8,571

TRx Volume 725 3,427 7,020 9,258 11,583 14,452 15,429 18,575 19,201

NRx Share 0.8% 3.7% 5.8% 6.6% 6.9% 8.1% 9.0% 9.3% 9.70%

TRx Share 0.3% 1.4% 2.7% 3.6% 4.4% 5.4% 6.3% 6.9% 7.50%

March April May June July Aug Sep Oct Nov

Source: IMS Monthly NGPS November 2007

LIALDA’s growth continues with 7.5% monthly TRxshare and 9.7% NRx monthly share in November

18

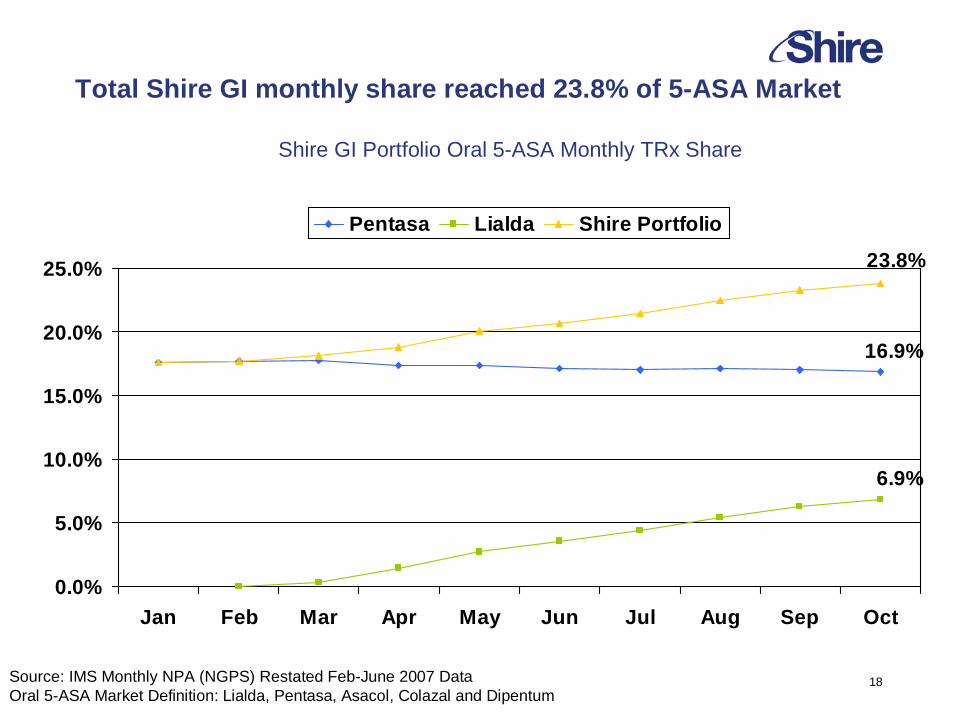

16.9%

6.9%

23.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Pentasa Lialda Shire Portfolio

Source: IMS Monthly NPA (NGPS) Restated Feb-June 2007 DataOral 5-ASA Market Definition: Lialda, Pentasa, Asacol, Colazal and Dipentum

Shire GI Portfolio Oral 5-ASA Monthly TRx Share

Total Shire GI monthly share reached 23.8% of 5-ASA Market

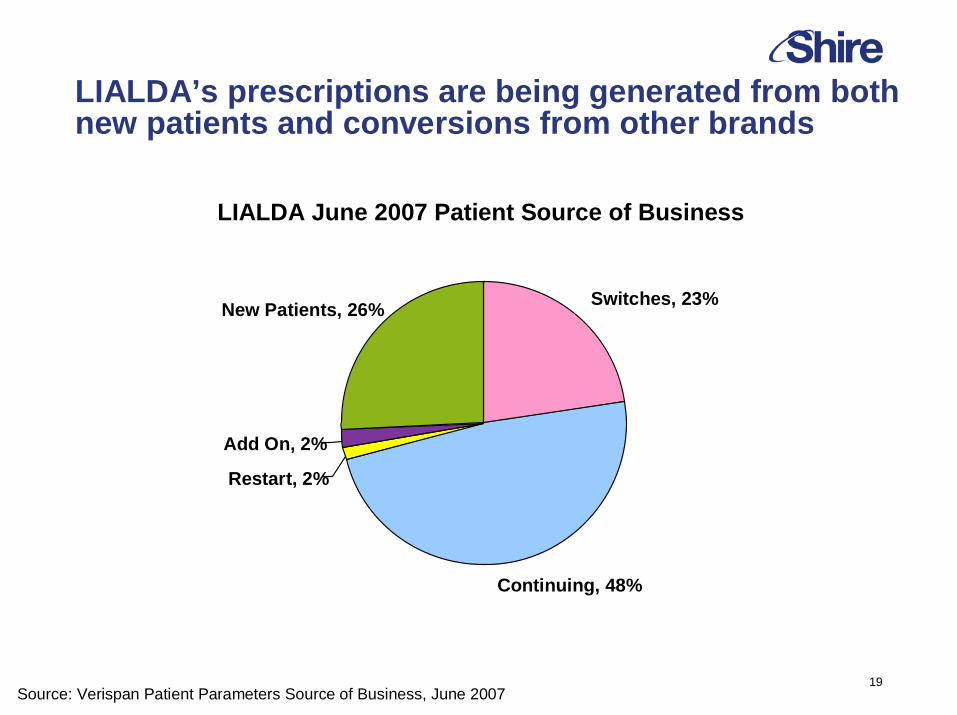

19Source: Verispan Patient Parameters Source of Business, June 2007

LIALDA June 2007 Patient Source of Business

Switches, 23%

Continuing, 48%

Restart, 2%

Add On, 2%

New Patients, 26%

LIALDA’s prescriptions are being generated from both new patients and conversions from other brands

Recent events

21

Expansion of Human Genetic Pipeline through in-licensing agreement with Amicus Therapeutics Inc.

Acquisition of ex-US rights for:

AMIGAL ™, Fabry disease (Phase 2)

PLICERA ™, Gaucher disease (Phase 2)

AT2220, Pompe disease (Phase 1)

Financial terms of the license are geared to the successful development and commercialization of the products

$50m upfront and up to $390m of development and sales-based milestones and;

Royalties on net sales of the products, with tiered, double digit royalty rates

Oral therapies based on novel chaperone technology for Lysosomal Storage Disorders:

This technology has been applied to various defective enzymes as a result of improper folding.

Pharmacological chaperone technology uses small molecules that selectively bind to and stabilize proteins in cells. This leads to improved protein folding into its proper three-dimensional shape. The re-folded enzyme can then be trafficked to the specific location inthe cell to perform its intended biological function.

22

Concluding Remarks 2007 guidance upgraded as revenue growth accelerates

revenue growth to be at least 30% for 2007 (previous guidance: at least 25%)

Excellent Q3 results

Successful ongoing launches

Continuing to demonstrate our ability to execute

VYVANSE – enthusiastic response from physicians and caregivers

ELAPRASE – rapid uptake in US and EU

LIALDA – growth continues – 9.7% share of NRx as of week 12/7/07

FOSRENOL – strong start in Europe

DYNEPO – launched in Q1 2007, good reception

Good progress in strengthening our R&D pipeline

In-licensing agreement with Amicus Therapeutics Inc. 3 oral treatments for: Gaucher, Fabry and Pompe disease

JUVISTA license agreement with Renovo

Positive Phase 2 clinical trial results

SOURCE: IMS NGPS – as at November 2, 2007

Additional information and Back-up slides

24

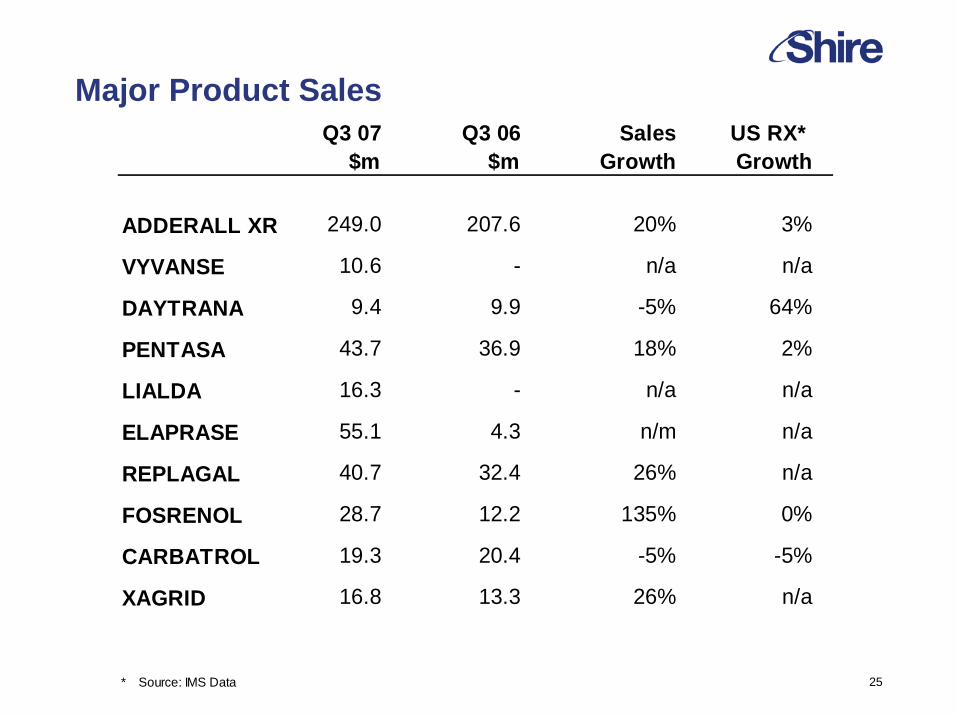

Q3 07 Q3 06 Growth$m $m %

Product Sales 543.1 386.2 41%

Royalties 61.9 60.4

Other Revenues 3.7 2.8

Total Revenues 608.7 449.4 35%

Q3 07 Q3 06 Growth$m $m %

Product Sales 77% 418.6 359.8 16% (excl. new launches)

ELAPRASE 55.1 4.3LIALDA 16.3 0.0FOSRENOL US 16.3 11.4FOSRENOL EU 23% 12.4 0.8VYVANSE 10.6 0.0DAYTRANA 9.4 9.9DYNEPO 4.4 0.0

Product Sales 100% 543.1 386.2 41%

Product Sales from New Launches (%)

13

1923

0

5

10

15

20

25

Q1 Q2 Q3

2007

%

Total Revenues

25

Q3 07 Q3 06 Sales US RX* $m $m Growth Growth

ADDERALL XR 249.0 207.6 20% 3%

VYVANSE 10.6 - n/a n/a

DAYTRANA 9.4 9.9 -5% 64%

PENTASA 43.7 36.9 18% 2%

LIALDA 16.3 - n/a n/a

ELAPRASE 55.1 4.3 n/m n/a

REPLAGAL 40.7 32.4 26% n/a

FOSRENOL 28.7 12.2 135% 0%

CARBATROL 19.3 20.4 -5% -5%

XAGRID 16.8 13.3 26% n/a

* Source: IMS Data

Major Product Sales

26

Sales deductions will trend towards a long term rate of approximately 28%.

Q2 deferred revenue sales 55.9 Add Q3 deferred sales 1.9 Less Q3 sales demand (20.9) Deferred revenue at 9/30/07 36.9

Q3TRx ('000)* $m Notes

Sales Demand 217 20.9 Price per TRx = 28.3 (tablets per TRx) x $3.41 (price per tablet)

Restocking 10.2

Underlying gross sales 31.1 100%

Sales coupons (12.3) 39%66%

Wholesaler discounts & rebates (8.2) 27%

Net Sales 10.6 34%

*per IMS

VYVANSE – Gross to Net Sales (Q3 2007)

27

DAYTRANA – Gross to Net Sales (Q3 2007)

Voluntary market withdrawal. This is a one off charge for Q3

Coupon expense to moderate at 10% in 2008.

Sales deductions are expected to trend towards a long term rate of approximately 25%.

Q3TRx ('000)* $m Notes

Sales Demand 183 21.7 Price per TRx = 29.8 (patches per TRx) x $3.98 (price per patch)

Destocking (0.1)

Underlying gross sales 21.6 100%

Sales coupons (3.9) 18%

Returns (4.0) 18% 56%

Wholesaler discounts and rebates (4.3) 20%

Net Sales 9.4 44%

*per IMS

28

Q3 07 Q3 06 Growth$m $m (%)

3TC 36.7 36.5 1% *

ZEFFIX 10.2 9.3 10% **

Other *** 15.0 14.6 3%

Total 61.9 60.4 2%

*Foreign exchange movements have contributed +4% to reported growth **Foreign exchange movements have contributed +6% to reported growth ***Includes REMINYL/RAZADYNE

Royalties

29

(on a non-GAAP basis)

Q3 07 Q3 06 YTD 07 FY 06

COGS 14% 14% 14% 13%

Gross margin 86% 86% 86% 87%

R&D 19% 19% 18% 20%

SG&A 46% 54% 47% 52%

Operating EBITDA (1) 21% 14% 22% 16%

Operating EBITDA margin (% Total Revenue) 29% 26% 31% 28%

This slide contains non GAAP financial measures. They exclude intangible asset amortization in respect of intellectual property charges, the accounting impact of share-based compensation and the effect of certain cash and non-cash items, both recurring and non-recurring, that Shire's management believes are not related to the core performance of Shire’s business.

(1) Excluding royalties

Financial Ratios (% of net product sales)

30

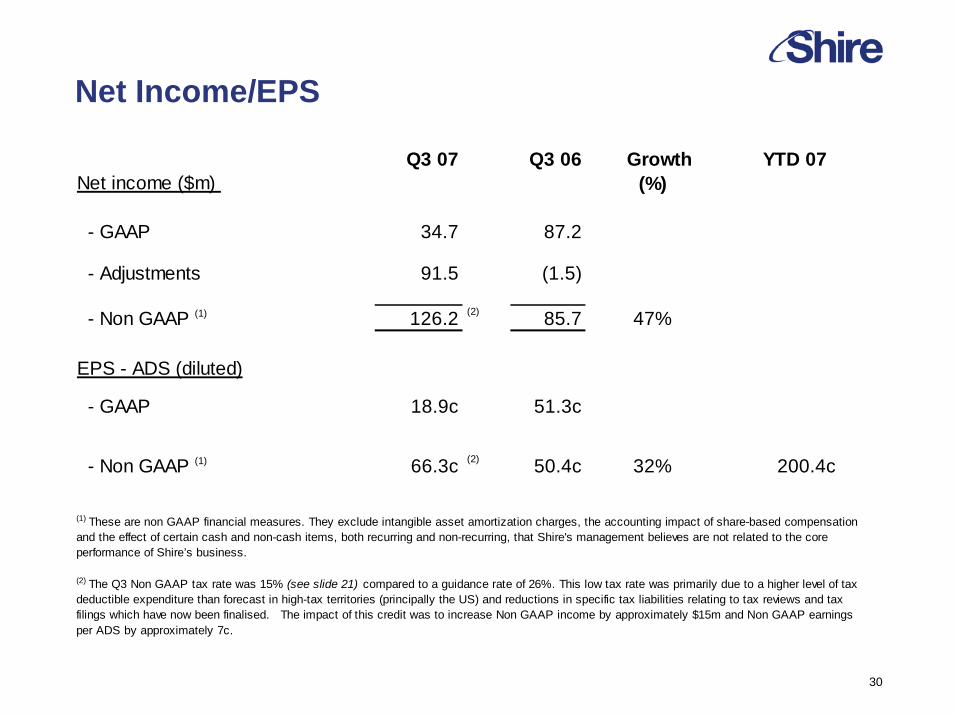

Net Income/EPS

Q3 07 Q3 06 Growth YTD 07Net income ($m) (%)

- GAAP 34.7 87.2

- Adjustments 91.5 (1.5)

- Non GAAP (1) 126.2 (2) 85.7 47%

EPS - ADS (diluted)

- GAAP 18.9c 51.3c

- Non GAAP (1) 66.3c (2) 50.4c 32% 200.4c

(1) These are non GAAP financial measures. They exclude intangible asset amortization charges, the accounting impact of share-based compensation and the effect of certain cash and non-cash items, both recurring and non-recurring, that Shire's management believes are not related to the core performance of Shire’s business.

(2) The Q3 Non GAAP tax rate was 15% (see slide 21) compared to a guidance rate of 26%. This low tax rate was primarily due to a higher level of tax deductible expenditure than forecast in high-tax territories (principally the US) and reductions in specific tax liabilities relating to tax reviews and tax filings which have now been finalised. The impact of this credit was to increase Non GAAP income by approximately $15m and Non GAAP earnings per ADS by approximately 7c.

31

Q3 07 Q3 07 Q3 06 Q3 06$m cents/ADS $m cents/ADS

Net income for diluted EPS (ADS) 34.7 18.9c 87.2 51.3cCost of product sales fair value adjustment - - 6.7 3.9c

In-licensing payments 75.0 39.0c 30.5 18.3c

Gain on disposal of product rights (7.1) (3.6c) (63.0) (37.5c)

Legal settlement provision 27.0 13.8c - -

Intangible asset amortization 31.1 15.9c 14.6 8.7c

SFAS 123R effect 11.7 6.0c 9.1 5.4c

Taxes on above adjustments (46.2) (23.7c) 0.6 0.3c

Non GAAP net income / EPS (ADS) 126.2 66.3c 85.7 50.4c

EPS Reconciliation

32

Asset Sales

Cash flow – Q3 2007

Net cash outflow for Q3 2007 : -33

$ in millions

-61

+1

(2) Shire has a revolving credit facility of $1.2bn which was undrawn at 30 Sept 2007

Cash generation + 200

Fixed asset purchases

Other Financing

-30

Product Milestones-26

+8

Net tax/interest

Renovo-125

(1) Shire’s balance of cash and cash equivalents at 30 Sept 2007 includes $42m of restricted cash and is available to finance payments due to TKT dissenting shareholders (provision at 30 Sept 2007 of $473m)

Cash at 30/6/07 638

Cash outflow Q3 07 (33)

Cash at 30/9/07 (1) (2) 605

Convertible debt (1,100)

Net debt at 30/9/07 (495)

33

Q3 07 YTD 07 Updated Q2Actual Actual FY Guidance FY Guidance

Revenue growth 35% 32% > 30% > 25%

R&D - GAAP ($m) 180.7 363.7

Less SFAS 123R (3.3) (8.8) Noven - (5.9) Renovo (75.0) (75.0)

R&D - Non GAAP ($m) 102.4 274.0 $365m to $375m $340m to $360m

SG&A - GAAP ($m) 286.7 753.5 Less SFAS 123R (7.5) (22.7)

Legal settlement provision (27.0) (27.0)

SG&A - Non GAAP ($m) 252.2 703.8 $955m to $975m $930m to $960m

Updated FY 2007 Guidance

34

Q3 07 YTD 07 Updated Q2Actual Actual FY Guidance FY Guidance

D&A - GAAP ($m) 46.3 107.4 Less amortization (31.1) (64.0) Up 70% Up 80%

Depn - Non GAAP ($m) 15.2 43.4 Up 30% Up 20%

Tax charge (credit) - US GAAP (23.2) 43.9 Less non GAAP adjustments 46.2 63.5

Non GAAP Charge 23.0 107.4

Non GAAP-Income before tax 148.7 477.4

Effective Tax rate 15% 22% Low 20%'s 26%

Updated FY 2007 Guidance (cont.)

35

The study was a double-blind, placebo-controlled, 4-week study with forced dose escalation in 420 adult subjects aged 18 to 55 years with moderate to severe symptomatic ADHD

All VYVANSE doses (30, 50, or 70 mg/d) were highly effective compared with placebo, as shown by ADHD-RS-IV (the primary endpoint)

Significant improvements in ADHD symptoms were observed within the first week of treatment

Adverse event profile was similar to that seen with other ADHD trials in adults. A/Es were mild to moderate in severity and incidence decreased over time

VYVANSE did not worsen sleep quality5

VYVANSE demonstrated strong efficacy in Adults with ADHD in a very large Phase III study