motilal oswal india conference - ashok leyland 7 al/cfo/6/8/07 global investments ashok leyland...

TRANSCRIPT

3rd Annual Bear Stearns and Motilal Oswal INDIA Conference

K SridharanChief Financial Officer

August 2007

2

2

AL/CFO/6/8/07

Presentation outline

Hinduja Group profile

Economy / Commercial Vehicle Industry (CV)

Performance

Products

Plans and Priorities

12345

3

3

AL/CFO/6/8/07

Hinduja Group Profile1

4

4

AL/CFO/6/8/07

The Hinduja Group

5

5

AL/CFO/6/8/07

The Hinduja Group Profile

The Group was established in 1914 in Mumbai

Entered Middle East in 1919 to grow trading initiatives

Presence in more than 25 countries and operates across the globe

Entered India for significant business activities in 1987

Employs over 30,000 personnel worldwide

6

6

AL/CFO/6/8/07

Global InvestmentsMedia &

Entertainment

IT/ITES

AutomotiveBanking & Finance

Real Estate

Energy & Chemicals

7

7

AL/CFO/6/8/07

Global Investments

Ashok LeylandSecond Largest Commercial Vehicle manufacturer in India with turnover > USD 2 Bn.Operating in CV Truck & Bus segmentsEmploying over 12,000 peopleISO / TS 16949 certificate – representing International quality standards specific to Auto industryExports to over 30 countries in Asia, the Middle East, AfricaListed on Mumbai and National Stock Exchange and in London Stock ExchangeUnbroken profit and dividend track record

Automotive

8

8

AL/CFO/6/8/07

Economy / CV Industry2

9

9

AL/CFO/6/8/07

Commercial Vehicle (CV) Industry

FY07 growth propelled by

Buoyant Economy

Freight generating sectors register robust growth

Continued focus on Infrastructure development .

Enforcement of rated payload regime.

Growth rates for CV Industry remained healthy at over 33%

IIP : 11.5%Agriculture: 0.9%

Exports: 20.8%CMIE July’07

10

10

AL/CFO/6/8/07

M&HCV TIV: Bus and Truck

Sixth year of consecutive growth

Bus

Truck

Source: SIAM

2869216814 19970 24591 25638 28127

246857

7318595741

136804172868 179345

'01-02 '02-03 '03-04 '04-05 '05-06 '06-07

89 999

115 711

161 395

198 506207 472

275 549

CAGR 25%

11

11

AL/CFO/6/8/07

Market Segment and growth

Growing segments: > 16.2 T GVW and < 3.5 T GVW

AL has significant presence in > 16T vehicles

12

12

AL/CFO/6/8/07

Freight Rates movement

13

13

AL/CFO/6/8/07

Increase in Truck operator profitability post SC ban

14

14

AL/CFO/6/8/07

Future growth drivers

Continued Economic Growth

Impetus to Development by States through

SEZ

Industries in rural areas

All above areas not connected by railways

Logistics management by organised sector for JIT

Development of vehicles suited for long haul , hitherto dominated by railways

Increase in Railway coverage to benefit Road sector

FY08 EstimatesIIP : 9.1%

Agriculture:2.6%Exports: 28.0%

CMIE July’07

15

15

AL/CFO/6/8/07

Future growth drivers contd..

NHAI projects – extension to rural areas

Implementation of ban on overloading by all States

Ban on trucks which are > 15 year old –Phased introduction by all States

If ban on overloading extended to bus segment, minimum growth potential around 30 to 40%

Government support to infrastructure financing would maintain growth momentum

16

16

AL/CFO/6/8/07

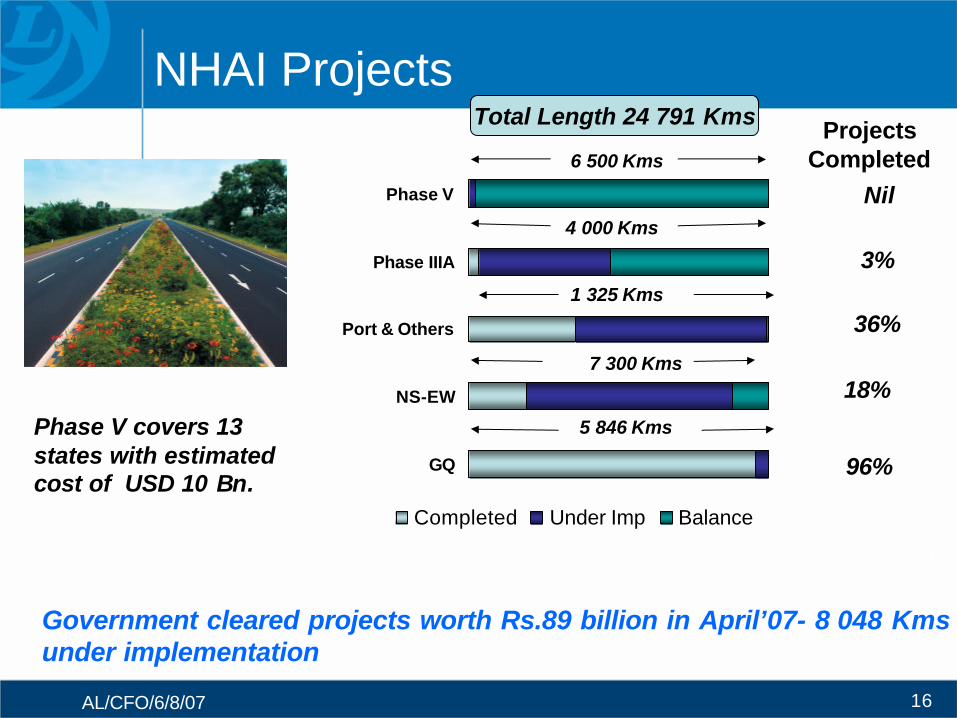

NHAI Projects

Government cleared projects worth Rs.89 billion in April’07- 8 048 Kmsunder implementation

GQ

NS-EW

Port & Others

Phase IIIA

Phase V

Completed Under Imp Balance

6 500 Kms

4 000 Kms

1 325 Kms

7 300 Kms

5 846 KmsPhase V covers 13 states with estimated cost of USD 10 Bn.

Total Length 24 791 Kms Projects Completed

3%

36%

18%

96%

Nil

17

17

AL/CFO/6/8/07

Current scenarioUncertainty in interest rates – Operators deferring purchasesContinued availability of freightRepayment track record of operators – no concern for NBFCsSecond hand vehicle market being strong. Prices are remunerativeSentiments likely to change for better beyond Oct’07Competition from other new entrants: MAN, Navistar, DCX, AMWMarket likely to be dominated by domestic players –Product offerings and price war likely to intensify

18

18

AL/CFO/6/8/07

CV Growth projection

Growth rate projections by leading research / rating agencies

CRISIL : CAGR at 6-8% (FY08-FY12)Fitch : 8 to 10 % in FY08HSBC : 6 %Motilal Oswal: > 8% in FY08UBS : Likely to increase from H2

TIV growth to be around 5% to 6% in FY08

19

19

AL/CFO/6/8/07

Performance3

20

20

AL/CFO/6/8/07

M & HCV: TIV and MS

Year Bus Truck TotalFY07TIV 28,692 246,857 275,549 AL 11,673 65,063 76,736 MS % 40.7% 26.4% 27.8%FY06TIV 28,127 179,345 207,472 AL 13,409 42,614 56,023 MS % 47.7% 23.8% 27.0%FY 05TIV 25,638 172,868 198,506 AL 10,469 37,137 47,606 MS % 40.8% 21.5% 24.0%

Source:SIAM

21

21

AL/CFO/6/8/07

Break-up of Sales

(30)5 4687 838Spares incl Defence(Rs million)

238 9047 261Engines

3583 09461 655Total vehicles

246 0254 879Exports

3677 06956 776Total

5365 06242 608Trucks

(15)12 00714 168 Buses

Domestic

% Inc (Dec)

FY07FY06

22

22

AL/CFO/6/8/07

Growth in other Business segments

Exports grew by 24% in FY 07 with a sale of 6,025 vehiclesEngines

Volumes grew 23%

Leyparts saw record sales at Rs. 3288 Mio, growing 26%Drop in overall Parts turnover due to deferral of supplies to ArmyFocus on Fully Built solutions: 10 % of sale volume

23

23

AL/CFO/6/8/07

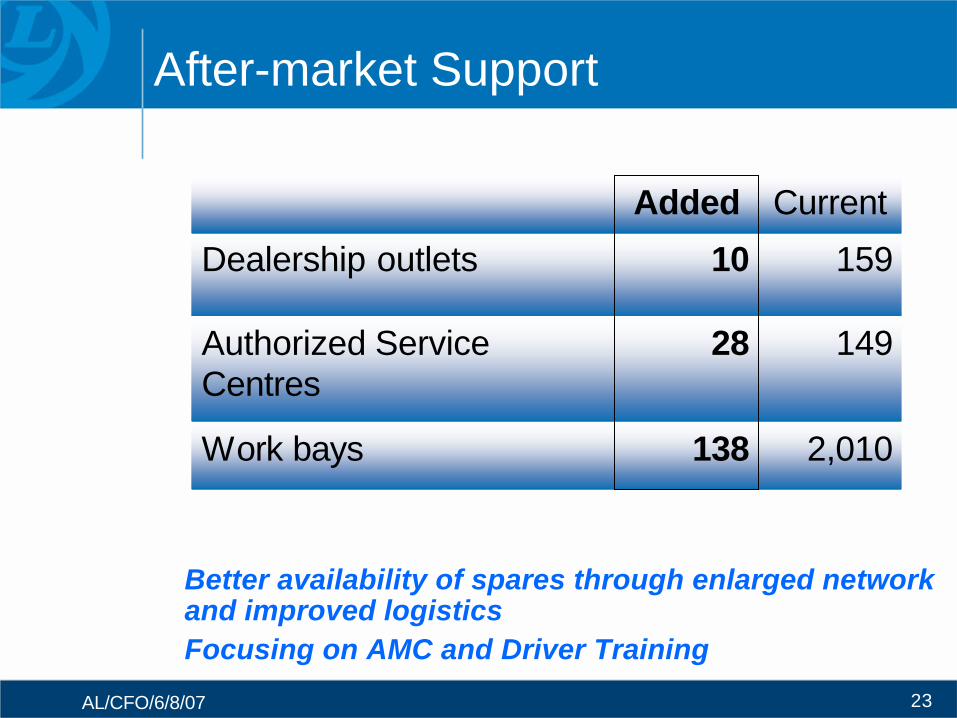

After-market Support

2,010138Work bays

15910Dealership outlets

14928Authorized Service Centres

CurrentAdded

Better availability of spares through enlarged network and improved logisticsFocusing on AMC and Driver Training

24

24

AL/CFO/6/8/07

Financial Performance in FY07Rs million

FY06 % FY07 % % GrowthNet Sales / Income from Operations 52,477 100.0 71,682 100.0 37 Expenditure

Raw Material consumption 37,690 71.8 53,391 74.5 42 Staff cost 4,039 7.7 4,807 6.7 19 Other expenditure 5,347 10.2 6,457 9.0 (163)

Gross Operating Margin 5,401 10.3 7,027 9.8 30 Depreciation 1,260 2.4 1,506 2.1 19 Net Profit after Tax 3,273 6.2 4,413 6.2 35 Basic Earnings Per Share (FV of Re1 per share)

2.74 3.38 24

Pressure on marginsImpact of Commodity prices , CMVR regulation, Emission standardsCost increase partially mitigated through:

Pricing action – April 06 : 2 %; Nov’06:1.5 % VAT benefit for last qtr (Rs.10,000 per veh)

25

25

AL/CFO/6/8/07

Performance Highlights – 5 Years

23.420.239.961.429.5EPS Growth %

2.74

0.2

18

5.3

21.2

FY06

1.63

0.5

21

5.2

17.6

FY04

2.28

0.3

14

5.7

18.6

FY05

3.38

0.3

17

5.5

24.7

FY07

1.01EPS (In Rs.)

0.8Debt : Equity

26Debtors (Days)

3.7Inventory Turns (Times)

11.7R O C E (%)

FY03

Control on Assets employedAll round improvements Y-O-Y

26

26

AL/CFO/6/8/07

Break-up of Sales in Q1FY08

461 4641 000Spares incl Defence (Rs million)

552 7041 740Engines

718 16317 040Total vehicles

151 4241 244Exports

616 73915 796Total

(15)12 22914 328Trucks

2074 5101 468Buses

Domestic

% Inc (Dec)

Q1FY08Q1FY07

Outperformed TIV growth: Volume improved by 6% against negative growth in TIV 3%

27

27

AL/CFO/6/8/07

Financials in Q1FY08

Rs million

Q1FY07 % Q1FY08 % %

Growth Net Sales / Income from operations 14,239 100.0 16,211 100.0 14 Expenditure

Raw Materials consumption 10,445 73.4 11,670 72.0 12 Staff cost 1,291 9.1 1,391 8.6 8 Other expenditure 1,316 9.2 1,408 8.7 7

Gross operating margin 1,187 8.3 1,743 10.8 47 Depreciation 328 2.3 413 2.5 26 Net profit after Tax 692 4.9 882 5.4 28 Basic earnings per share (Rs.) - not annualised

0.55 0.67 21

Margin improvement through better mix and volumes

28

28

AL/CFO/6/8/07

Products4

29

29

AL/CFO/6/8/07

DIESEL

FRONT ENGINE

REAR ENGINE

NORMAL FLOOR - 7m to 12m

SEMI LOW FLOOR

VESTIBULE BUS

DOUBLE DECKER

SINGLE STEP

NO STEP

CNG FRONT ENGINE

REAR ENGINE

NORMAL FLOOR

SINGLE STEP

NO STEP

Bus Matrix

Low Floor options available

30

30

AL/CFO/6/8/07

Trucks - Matrix

HAULAGE4 x 2

6 x 2, 6 x 4

8 x 2

TRACTORS4 x 2

6 x 4

TIPPERS4 x 2

6 x 4

8 x 4

31

31

AL/CFO/6/8/07

Engine development

AL is developing fuel efficient Euro IV compliant engine with support of AVL AustriaIndia may introduce Euro IV in 2010 in major 11 cities and extend to pan India few years thereafterAL offers Euro III compliant vehicles now even though it is mandatory only in 11 citiesCollaboration with Hino motors and ZF Germany in last two decades was successfulAL currently holds IPR for Euro II / III “H”seriesengines

32

32

AL/CFO/6/8/07

Plans and Priorities5

33

33

AL/CFO/6/8/07

Plans and Priorities

Product launches – Focus on Fully Built SolutionsEngine development – Euro IV emission standardsCapacity build upDe-risking – Focus on Engine / Defence / Export marketsCost Management initiatives through employee involvementSpreading Global footprint

34

34

AL/CFO/6/8/07

Capex / Capacity plans

50 000New plant in Uttarkhand (by Mar 2010)

50 000Expansion in existing plants by Dec’07

Capex outlay planned at Rs 40 Billion over 3 years including Product Development / Technology upgradation

1 84 000Total Capacity over next 3 years

84 000Capacity enhancement Plan over 3 years

Capacity on Board

Veh. P.a.

35

35

AL/CFO/6/8/07

Increasing Capacities

Uttarkhand

Integrated manufacturing plant for 50,000 vehicles per annum

Layouts made for lean manufacturing and automation

Production start up : phase 1 by 2nd half of FY09; Full capacity production by March FY10

Fiscal incentives will pay for cost of the project

36

36

AL/CFO/6/8/07

Defence, Exports, Engines and Spare Parts contributing 18% of revenue.Engines Business

Strategy in place to trade on enginesTrading engines to match the in-house volumes by FY 11Engine business to double to 5% of Sale Revenue

Defence – New vehicle applications to increase revenue share from Defence; Target to increase share of revenue above 10%Thrust markets identified in ASEAN, African countries using mix of European and Indian designWith availability of factory fitted cabins and vehicles with high power / weight ratio product offerings doubled to export market. Targeting to grow at 25% YoY. Volume to double in next 3 years and reach 15% of total sales

Non Cyclical business to grow

Share of non-cyclical revenue streams to reach 30%

37

37

AL/CFO/6/8/07

Cost Management Initiative Mission Gemba : A move focused on value addition in the shop floor through attitudinal alignment and process improvements resulted in through-put improvements across the company. Reflected in operating cost reduction by 100 bps

Employee productivity improvements reduce cost by 100 bps

Project YE : To bring about organizational transformation through empowering Young Executives

Improve : 1800 plus projects implemented by employee teams

Innovations: 7 Patents filed

Supply Chain Ownership Teams solved capacity constraint of suppliers and achieved 100% utilisation

38

38

AL/CFO/6/8/07

Spreading The Global FootprintAVIA in Czech Republic

Acquired AVIA TBU in FY07Vehicles are Euro IV compliant, sold in almost 17 countries in Europe; strong presence in Eastern European countries. Scope exists to improve margins through cost reduction and scale up operationsOrganisation rebuilding, alternate sourcing and value engineering programme for cost reduction on course Operations stabilised, currently at 2000 p.a. Efforts on Dealership development in existing markets being doubled

Ras Al Khaimah in UAE An integrated assembly plant with an investment of Rs. 380 Million to build 1000 buses p.a.Construction activities commenced.Operations to commence in Mar 2008

39

39

AL/CFO/6/8/07

D E F I A N C ED E F I A N C ETESTING & ENGINEERINGTESTING & ENGINEERING

Northwood Drive, Troy, USANorthwood Drive, Troy, USA

Spreading The Global Footprint contd..

40

40

AL/CFO/6/8/07

Company Overview

Providers of Component, System & Full Vehicle Product Development Support to the TransportationIndustry

Vehicle SystemsVehicle SystemsChassis Chassis Suspension/SteeringSuspension/SteeringCooling ModulesCooling ModulesBody StructureBody StructureInteriorInteriorBumpersBumpersPowertrainPowertrainExhaustExhaustElectricalElectrical

Vehicle TypesVehicle TypesCarCarLight TruckLight TruckHeavy TruckHeavy TruckOffOff--highwayhighwayBus/RecreationalBus/Recreational

41

41

AL/CFO/6/8/07

DiversificationJV with Alteams

A 50:50 JV with the Alteams Group, Finland to produce High Pressure Die Casting (HPDC) aluminum components pre-dominantly for telecommunications & automotive sectors

Target turnover of Rs. 6.5 billion in about 5 years, with total investment of Rs.3.35 billion

JV with Siemens VDOA 50:50 JV with Siemens VDO to design, develop and adapt infotronicproducts and services for the transportation sector

Through acquisitions / diversifications AL targets to:

Access new markets with new product designs manufactured cost effectively to add value to customers

Address with physical and intelligent part of future vehicles to remain at edge of technology innovations / offerings

42

42

AL/CFO/6/8/07

Value-added services for share-holders

Annual share-holders satisfaction surveyConducted for 6 years consecutively Responses are summarised and reviewed by the Share-holder/Investor Grievance Committee of the Board

Investor GuideSent to every share-holder every year since 1998

Annual ReportsDisclosures beyond mandatory requirements –contains useful information about Industry / Company

43

43

AL/CFO/6/8/07

Corporate Social ResponsibilityDisaster Management TrainingAlcohol De-addiction Centre at NamakkalComputer training to economically marginalized students in HosurSelf-Help Groups in HosurRoad Safety Road shows on Chennai Highway (GST Road)FunBus for physically challenged persons

44

44

AL/CFO/6/8/07

The Share-holding Pattern

FIIs18%

Resident Individuals / Trust / Clearing members

12%

FIs, Ins.Co, Banks,MFs

19%

LRLIH51%

45

45

AL/CFO/6/8/07

Thank you