mr project article

TRANSCRIPT

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 1/20

www.palgrave-journals.com/fsm/

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–94

INTRODUCTIONThis study defines Internet banking (IB) as

‘Web-Based Banking’, whereby bank

account holders can interact with and obtain

a bank’s financial services (both informational

and transactional) in a virtual environmentusing any device connected to the Internet.

Internet Banking is a business model through

Correspondence: Ali Hussein Saleh Zolait

Faculty of Business and Accountancy, University of Malaya,

50603 Kuala Lumpur, Malaysia

E-mails: [email protected]; [email protected]

which a bank integrates both offline (bricks)

and online (clicks) presences (Bricks-and-

clicks).1 According to Cyree et al ,1 there are

two general business models used to provide

IB: ‘bricks and clicks’ and ‘Internet-primary’

banks. The ‘bricks and clicks’ model utilizestraditional brick and mortar offices,

supplemented by the Internet, similar to a

firm with a physical market presence, such as

Barnes and Noble, also operating a website

in which products can be purchased.1 Banks

utilize the web networks to provide

customers with information on their financial

Original Article

An examination of the factors

influencing Yemeni Bank users’behavioural intention to useInternet banking servicesReceived (in revised form): 24th February 2010

Ali Hussein Saleh Zolaitis Visiting Research Fellow and Lecturer of MIS in the Faculty of Business and Accountancy at the University of Malaya. His research

interests are management information systems (MIS), diffusion of innovation, security, and e-commerce application and performance.

ABSTRACT The purpose of this study was to examine the potential prominent factorsrelating to the adoption and use of the financial services of Internet banking (IB). The

study was carried out using a self-administered survey involving a convenience sample

of 369 Yemeni bank customers. The survey revealed that the overall prominent predictors

include Relative Advantage / Compatibility, User’s Informational-Based Readiness, Attitude,

Observability, Technology Facilitating Condition, Perceived Behavioural Control and

Self-efficacy. The model accounted for 75 per cent of the variation of an individual’s

behavioural intention to use IB. In addition, it was also discovered that a majority of the

respondents are innovators and early adopters of IB. Yet, the adoption of IB financial

service is still relatively low.

Journal of Financial Services Marketing (2010) 15, 76–94. doi:10.1057/fsm.2010.1

Keywords: financial services; Internet banking; adoption factors; diffusion of innovation

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 2/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–94 77

Factors influencing Yemeni Bank users’ BI to use IB services

services, replace transactions conducted

in branch offices and assist the bank’s

management to execute internal

administration. In addition, IB eliminates the

need to build new branches, eliminating

the overhead expenses of conventional banks

and service customers more efficiently.According to Mattila et al. 2 and Dandapani

et al. 49 IB services can provide timely,

speedy, accurate and convenient banking

opportunities round the clock. In addition,

customers can benefit from new banking

services such as paying bills online, finding

mortgages or auto loans, applying for credit

cards and locating the nearest ATM or

branch office. For the banks, IB offers them

many opportunities such as an additional

delivery channel, low-cost banking, profitablebanking, quality banking, and allows them to

sell products customized to individual

needs.3 – 4

IB broadens the geographical reach of

banks and can help to build and retain

additional customers.4

IB has appeared as the trend in banking,

nowadays, and emerged as one of the

payment models required to enable pure

e-commerce models to occur in online

business, rather than traditional banking.

There is a clear need to study the factors thatinfluence customers’ intention to adopt IB so

that banks can better formulate their

marketing strategies to increase IB usage in

the future. It is also important to note that

nations around the world need to get

connected and join the global networked

community.5 On the other hand, banking is

an information-intensive business4 in which

information technology (IT) is increasingly

becoming an invaluable and powerful tool

driving development, supporting growth,promoting innovation and enhancing

competitiveness.5 Furthermore, emerging IT

offers opportunities for developing nations to

leapfrog the earlier stages of development.5

Therefore, according to Cheng et al ,6 bankers

should accentuate the full functionality of

their systems to cater to the different banking

needs of the users efficiently. Moreover,

understanding the benefits of IB adoption

will encourage banks to develop new

products and services to fully utilize the

Internet’s capabilities.6 IB is widespread in

developed countries, but not yet in some

countries such as the Republic of Yemen.For instance, research on the factors that

identify and influence the adoption of IB has

not yet been studied academically in non-

western and developing countries such as the

Republic of Yemen. In the light of stiff

competition among banks in Yemen, the

banks themselves are now competing to gain

a larger market share and to use advanced

technologies to retain customers in the future.

The Theory of Planned Behaviour (TPB)

was developed as an extension of the theoryof reasoned action (TRA) to justify

conditions in which individuals do not have

complete control over their behaviour.7 This

theory posits that behaviour is determined by

the intention to perform the behaviour. In

TPB, there are three constructs that

determine the user ’s intention, which are

attitude, Subjective Norms (SN) and

Perceived Behavioural Control (PBC).

The TPB has been used to study the

adoption of different information systems

such as spreadsheets,8 computer resourcecentres9 and electronic brokerages by

Battacherjee10 and negotiation support

systems by Lim et al. 11 This study is of

value as it extends the TPB and Extended

Theory of Planned Behaviour (ETPB)12

by incorporating user readiness and

examines its impact on an individual’s

intention to adopt IB. From a theoretical

perspective, the findings will help and

expand the understanding of the constructs

that affect technology adoption. It alsoconfirms the multidimensionality of user

readiness and its role in the adoption of IB.

From a practical perspective, the findings can

help banks that have plans to offer IB

services to make informed decisions about

the actions they can take to increase their

chances of success.

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 3/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–9478

Zolait

From the above discussion, the benefits of

IB are numerous for both the customers and

banks. Banks all over the world have been

offering their financial services via the

Internet to their customers. The adoption

rate among customers, however, varies from

country to country, as too do the reasonswhy individuals use IB. Therefore, there is a

need to study IB adoption in Yemen as there

are only a few studies examining the

adoption of IB in developing countries

specifically those in the Arab world and

Yemen. Empirical studies conducted in this

area are mainly either from the western or

Asian developed contexts.2 – 4,13 Yemen is

different from other countries as their IT

usage level is low.14 In addition, there is a

lack of government policies regardingonline activities compared to other countries

around the world. As mentioned earlier,

the factors influencing IB adoption vary

among customers. Many have studied this

occurrence using TAM, TPB, and ETPB.

This study adapted both the TPB and

ETPB models and incorporated user

readiness as a factor influencing IB adoption.

The following section describes the

framework adopted.

FACTORS INFLUENCING THEINTENTION TO USE IBThe development of this study’s conceptual

framework is based on TPB, which is an

extension of TRA.7 This theory posits that

behaviour is determined by the intention to

perform the behaviour. There are three

constructs that determine the user ’s intention,

which are attitude, norms and PBC. TPB

has been used in several studies in the field

of information systems.8,9,11,15

This studyextends TPB to account for User ’s

Informational-Based Readiness (UIBR) in

studying acceptance predictors. It is argued

by Zolait et al 16 that when a customer

gains awareness, knowledge, prior experience

and exposure to related products of

innovation, those factors may contribute to

predicting the behavioural intention to adopt

the technology.16

Behavioural intention to use IBMeasuring individuals’ behavioural intentions

is core to the theories of adoption, which are

used to study adoption in the InformationSystems field. Researchers have used the

post-implementation phase as the basis for

analysing a user ’s behaviour towards

technology acceptance; in particular, those

who worked on the TAM model as cited by

Mathieson.8 Users’ willingness to adopt is an

important means not only of understanding

the diffusion steps but also of validating the

timing for the decision makers regarding

when they should accept or reject the

proposed innovation.

17

Ajzen and Fishbein

18

defined intention as the individual’s location

on a subjective probability dimension

involving a relationship between the

individual and some action. An individual’s

intention, according to Ajzen,7 is the central

factor in TRA and TPB. It is a function of

three determinants. These determinants are

attitude towards the behaviour, the SN and

PBC.

Information about the existence of

innovations, according to Rogers,19 flows

through social systems to the potentialadopters, which is then processed by the

adopters to form perceptions about the

innovation, such as characteristics, and

perceptions in relation to other contextual

factors, which then serve as a determinant

of innovation adoption behaviour. On the

basis of Rogers’ definition, there are four

main elements existing in the diffusion of

innovation (DOI) process: (1) the characteristics

of innovation; (2) the communication

channels used to communicate the benefitsof the innovation; (3) the time elapsed since

the introduction of the innovation; and

(4) the social system in which the innovation

is to diffuse. This study categorizes the factors

influencing the users’ intentions to use IB

into three types, namely direct, indirect and

readiness factors. These factors will be

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 4/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–94 79

Factors influencing Yemeni Bank users’ BI to use IB services

elaborated and discussed in the following

sections.

Direct antecedents of intention The three variables that are used in TPB as

antecedents of the Intention construct are

attitude, SN and PBC.7,8,18,20 Ajzen7,21 pointed out that most studies concerned with

the prediction of behaviour from attitudinal

variables were conducted in the framework

of TPB. To a certain extent, TPB is a

predecessor of TRA.18 Attitude is

characterized as a person’s inclination to

exhibit a certain response towards a concept

or object. Ajzen and Fishbein18 pointed out

that ‘The attitudinal component refers to the

person’s attitude towards performing the

behaviour under consideration’. Similarly,Rogers19 refers to individuals forming a

favourable or unfavourable attitude towards

an innovation, but with much concern on

the attitude formation, which is equivalent to

persuasion. The main outcome of the

persuasion stage in the innovation-decision

process is either a favourable or an

unfavourable attitude towards the innovation.

Subjective norms comprise the second

component of intention in both the TRA

and TPB models. They deal with the

influence of the social environment. Norms,according to Rogers,19 are established

behavioural patterns for members of the

social system, which tell an individual what

behaviour is expected. Mathieson8 defined

SN as ‘the individual’s perception of social

pressure to perform the behaviour.

PBC, according to TPB, is the third

antecedent of intention. Doll and Ajzen20

posited that when the behaviour or situation,

affords a person complete control over

behavioural performance, intention aloneshould be sufficient to predict behaviour, as

specified in TRA. According to Ajzen,7 PBC

refers to an individual’s perception of the

ease or difficulty of performing the behaviour

of interest. Similarly, Mathieson’s8 definition

of PBC ‘is the individual’s perception of his

or her control over performance of the

behaviour ’. Mathieson8 demonstrated that

behavioural control influences the intention

to use an information system. A positive

relationship between PBC and intentions is

also found in Taylor and Todd’s9 study,

which examines users in a computer

resources centre. In the context of IB, Tanand Teo13 demonstrated that the intention

to adopt IB services could be predicted by

PBC factors.

Indirect antecedents of intention The three direct antecedents discussed above,

according to Ajzen and Fishbein,18 are

themselves determined by multiple salient

behavioural beliefs towards the behaviour.

For instance, according to Taylor and

Todd,

9,15

although attitude directly influencesbehavioural intention, attitude itself is

determined by multiple salient behavioural

beliefs. Along these lines, Rogers19 suggested

five attributes that are assumed to have an

effect on the rate of the adoption of an

innovation. They are (1) relative

advantage, (2) compatibility, (3) complexity,

(4) trialability and (5) observability. With

respect to those five innovation attributes,

Kautz and Larsen22 argue that the more

favourable an individual’s perceptions of

these attributes, the higher are the chancesof a successful adoption of an innovation.

Subjective norm itself is determined by

multiple salient behavioural beliefs based on

personal referents towards the behaviour.

Bearden et al 23 and Karahanna et al 24

categorized social influence (normative belief)

into two types, which are informational-

based influence and normative influence.

This study examines the effect of two types

of salient normative beliefs, the personal and

media salient beliefs. Rogers19

pointed outthat information about an innovation can be

actively sought by individuals once they are

aware that the innovation exists and also

when they know those sources or channels

that can provide further information about

the innovation. Rogers19 noted that the

importance of different channels or

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 5/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–9480

Zolait

information sources about the innovation

is determined by their availability to the

potential adopter. Battacherjee10

demonstrated that SN is determined by

interpersonal influence (for example, word of

mouth). The mass media are often the most

rapid and efficient means of informing anaudience of potential adopters about the

existence of an innovation, that is, to create

awareness-knowledge.19 Furthermore, the

expected effects of mass media channels were

generalized by Rogers19 as relatively more

important at the knowledge stage of the

innovation-decision process.

According to Ajzen and Fishbein18 and

Taylor and Todd,9 although PBC directly

influences behavioural intention, PBC itself is

determined by multiple salient control beliefstowards the behaviour. The formal PBC

determinants in the ETPB are self-efficacy

(SE), the technology facilitating condition

and the resource facilitating condition. TPB

was extended (ETPB) to enable prediction of

behaviours that an individual may not be

able to perform at will. Thus, ETPB

incorporated perceptions of control over

performance of the behaviour as an

additional predictor (Ajzen).7 The following

sections will elaborate those determinants in

further detail.9 SE reflects a more complex process

involving the construction and orchestration

of adaptive performance to fit changing

circumstances.25 Recent studies (of IS) have

provided empirical support for the

relationship between SE and outcome

expectations. For instance, Hartzel26 showed

that computer SE is an important

determinant of an individual’s decision for

software adoption and use. The facilitating

conditions (FC) construct was originallyviewed as an external control related to the

environment.9,27 Therefore, understanding

the anticipated influence of FC is important

in studying human behaviour in IS and

especially in studies such as the ‘adoption of

IB’. FC originally have two dimensions:

resource factors (such as the time and money

needed) and technology factors regarding

compatibility issues that may constrain

usage.9 Early studies of IB adoption look

into factors that influence its adoption. For

example, Tan and Teo’s13 framework

investigates FC within two dimensions.

The two dimensions are the availability of government support and the availability

of technology support.

User ’ s Informational-based Readiness Factor The user ’s readiness for IB is a proposed

construct developed to take account of the

informational aspects related to the user ’s

behavioural intention that may affect an

adopters’ decision to accept or reject the

introduced innovation. The framework inthis study proposes four dimensions of the

‘User ’s Informational-Based Readiness’

construct. These exogenous variables are

‘awareness’,19,28 ‘knowledge’,19,28

‘experience’29 and ‘exposure’.30 Some of

these attributes are examined as a single

variable in the emerging field of IB. For

instance, Chang’s30 study undertook the

exposure attribute, whereas Karjaluoto et al 29

sought consumers’ experiences. The way this

study utilizes these attributes differs from

the previous studies in that it integrates thetwo attributes with a further two attributes

that are not yet studied widely in the field of

IB. The study defines UIBR as the potential

adopters’ assessment of their awareness,

knowledge, experience and exposure to the

related technologies available or recommended

by referents, which reflect their informational

abilities to adopt or reject the innovation. In

previous research, Dickerson and Gentry 31

indicated that adopters of home computers

are likely to be more active informationsearchers and have more previous experience

in the use of computers and other related

technologies. In Finland, Karjaluoto et al 29

found that attitude towards IB and actual

behaviour were influenced by prior

experience of computers and technology as

well as attitudes towards computers.

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 6/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–94 81

Factors influencing Yemeni Bank users’ BI to use IB services

Furthermore, Sarel and Marmorstein32 noted

that prior experience with computers and

technology seems to be a key correlate of

early adoption. Similarly, Black et al 33

concluded that previous computer experience

is the main factor positively influencing the

adoption of e-banking services. Some authors(for example, Taylor and Todd15 ) point out

that exposure to and experience of related

products may increase perceived

compatibility.

METHODOLOGYThis study relies on the ‘Hypothetic-

Deductive methods’ in which a set of

quantitative approach rules are employed.

According to Sekaran,34 the hypothetico-

deductive method is a scientific methodwhereby researchers should establish testable

hypotheses and then try to falsify them,

rather than trying to confirm them directly

by accumulating favourable evidence. The

questionnaire was the instrument used for

data collection and the major items of the

survey were adapted from the prior

literature review as shown in Appendix D.

The scale adopted was a 7-point Likert

scale, ranging from 1 (strongly disagree)

to 7 (strongly agree). There are many

tools to measure behaviour, and ‘manyresearchers prefer to use a Likert-type

scale because it is very easy to analyze

statistically’.35 Likert scales, according to

Neuman,36 are ‘summative-rating or

additive scales because a person’s score

on the scale is computed by summing

the number of responses the person gives’

(p. 207). Owing to the difficulty in

obtaining a comprehensive and up-to-date

sample from the banks, convenience

sampling was used.One thousand questionnaires were self-

administered to the 14 banks in Sana’a,

Yemen. Fifty forms were assigned to each

of the 14 locations and the remaining 300

questionnaires were self-administered to bank

customers in a few industrial companies such

as Yemen Petroleum Company. This was

carried out, as these respondents are not able

to go to the banks during office hours

because of work restrictions. Six hundred

and twenty-three responses were received,

achieving a response rate of 62 per cent; of

these, 369 were satisfactorily complete and

useable for analysis with 254 having beenreturned incomplete. Thus, the gross

response rate of the research survey was

36.9 per cent.

A path-analysis approach, using the

Ordinary Least-Squares method (OLS), was

performed to test the proposed model37

facilitating testing of the cause and effect

among variables, as well as estimating the

direct and indirect effects of the variables

and understanding the magnitude and

direction of the relationships among themodel variables. The SPSS program and

multivariate techniques of Multiple Linear

Regression were used as a means of testing

the validity of the information obtained via

the procedures of data analysis.

ANALYSIS AND RESEARCHRESULTSPath analysis, according to Bryman and

Cramer,38 is an extension of multiple

regression procedures. It was developed as a

method for studying the direct and indirecteffects of variables hypothesized as causes of

variables treated as effects.39 Path analysis and

path coefficient are among the oldest terms

in causal analysis, where standardized s are

usually employed as estimates of causal

effects.37 The aim of path analysis is to

provide quantitative estimates of the causal

connections between sets of variables.

According to Bryman and Cramer,38 a direct

effect occurs when a variable has an effect on

another variable without a third variableintervening between them. An indirect effect

occurs when there is a third intervening

variable through which two variables are

connected. Along these lines, Pedhazur 39

points out that multiple regression analysis

can be viewed as a special case of path

analysis. Following Pedhazur ’s39 guidelines,

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 7/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–9482

Zolait

the constructs in this study can be interpreted

as loadings in factor analysis, whereas the

paths can be interpreted as standardized beta

weights in regression analysis. In order to

illustrate the study further, path diagrams and

path coefficients are utilized. The path

diagram, according to Pedhazur,39 is veryuseful for displaying graphically the

hypothesized pattern of causal relations

among a set of variables. In line with

Bryman and Cramer,38 the arrows indicate

expected causal connections between

variables. Thus, in the diagram presented in

Figure 1, the study used upper case letters

and numerical figures to represent variables

in the model. Letters such as ‘I ’ refer to the

variable Intention, ‘R ’ User Informational-

Based Readiness, ‘ A ’ Attitude, ‘N ’ SubjectiveNorm and ‘C ’ Perceived Behavioural

Control. Meanwhile, numbers like ‘1’ refer

to the variable Relative Advantage/

Compatibility, ‘2’ Ease of use, ‘3’

Observability, ‘4’ Trialability, ‘5’ Personal

Norm, ‘6’ Mass Media Norm, ‘7’ Technology

Facilitating Condition, ‘8’ Resource

Facilitating Condition, ‘9’ Government

Support and ‘10’ Self-Efficacy.

In studying causal connections, the

researcher has to distinguish between

exogenous and endogenous variables.40 Therefore, all the variables represented by

numerical figures are examples of exogenous

variables, whereas those represented by

letters, with the exception of ‘R ’, are

endogenous variables. In Pedhazur ’s words:39

An exogenous variable is one whose

variation is assumed to be determined by

causes outside the hypothesized model.

Therefore, no attempt is made to explain

the variability of an exogenous variable

or its relations with other exogenousvariables. An endogenous variable …

is one whose variation is explained by

exogenous or other endogenous variables

in the model. (p. 770)

On the basis of this distinction of variables in

the path analysis, it is implied that variables

could be dependent and independent in the

same model. Kerlinger and Pedhazur 40

highlight some assumptions underlying the

application of path analysis as follows:

1. The relationships among the variables in

the model are linear, additive and causal.2. Residuals are not correlated with variables

preceding them in the model.

3. There is a one-way causal flow in the

system.

4. Variables are measured on an interval

scale (7-point Likert scale).

This study checks for the aforementioned

assumption required for using the application

of path analysis and there is no violation. In

addition, both the simple and multiple linear regressions employed in this study were

helpful in explaining the predictive power of

independent variables in direct relation. The

arrows in Figure 1 were drawn from the

independent variable (exogenous) to the

dependent variable (endogenous) . For instance,

the variable ‘attitude’ denoted by A is

conceived to be dependent on variables 1, 2,

3, 4 and variable R . Similarly, variable N is

conceived to be dependent on variables 5

and 6 and variable C is conceived to be

dependent on variables 7, 8, 9 and 10.Consequently, variable I is conceived to be

dependent on A , N , C and R . The diagram

in Figure 1 represents the a priori model.

As shown in the a priori model, variables

with a numerical symbol from one to 10,

including the variable R , are exogenous

variables, whereas the variables in uppercase

letters (I , A , N and C ) are endogenous

variables. Furthermore, an endogenous

variable treated as a dependent variable in

one set of variables may also be conceived asan independent variable in relation to other

variables.40 Along these lines, the path

coefficient indicates the direct effect of

variables taken as a cause of a variable

taken as an effect. The variable 1 is

exogenous and is, therefore, represented

by a residual (e 1 ).

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 8/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–94 83

Factors influencing Yemeni Bank users’ BI to use IB services

Testing the full effects model toidentify significance pathsAccording to Kerlinger and Pedhazur,40 a set

of equations referred to as a recursive model

(p. 376)37 are required to assess the full

effects model and identify significant paths.

Recursive models, according to Cohen and

Cohen,37 can be estimated by ordinary

regression equations. In testing thehypotheses, this study performed a series

of multiple regressions to derive the

various path coefficients for the full effects

model and to identify significance paths

(Appendix A). A path analytic approach

using the OLS technique, which was utilized

to test the proposed model as recommended

by Cohen and Cohen37 is shown in

Figure 2. The relationships among the

variables in the recursive model are depicted

in a series equations as follows:

X e11

=

X e22

=

X e33

=

X e44

=

X e55

=

X e66

=

X e77

=

X e88

=

X e99

=

X e10 10=

XR e R

=

XA PA X PA X PA X

PA X PARXR e A

= + +

+ + +

1 1 2 2 3 3

4 4

XN PN X PN X e N

= + +5 5 6 6

XC PC X PC X PC X

PC X eC

= + +

+ +

7 7 8 8 9 9

10 10

XI PI X PIRXR PIAXA PA X

PI X PN X PINXN PI X

PI X P

= + + +

+ + + +

+ +

1 1 2 2

3 3 5 5 6 6

7 7 I I X PI X

PICXC PCI X e I

8 8 9 9

10 10

+

+ + +

The notions PA 1X 1, PN 5X 5, PC 7X 7,

PIAXA and so on denote a specific path

(1)(1)

(2)(2)

(3)(3)

(4)(4)

Variables Key

I: Intention,

R: User Informational Based Readiness

A: Attitude

N: Subjective Norm

C: Perceived Behavioural Control

1: Relative Advantage/Compatibility

2: Ease of use

3: Observability

4: Trialability5: Personal Norm

6: Mass Media Norm

7: Technology Facilitating Condition

8: Resource Facilitating Condition

9: Government Support

10: Self-Efficacy

Unverified direct effect

β AR

eI

eR

e5

eC

e6

e8

e7

e9

e10

e3

e4

e1

e2

β I P

β I R

β I N

β C10

β C9

β C8

C7

β IA

β N5

β N 6

β A3

β A4

β A1

β A2

I

5

2

N

A

C

9

8

10

7

3

6

1

4

R

eN

eA

Figure 1: A priori model (conceptual framework).

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 9/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–9484

Zolait

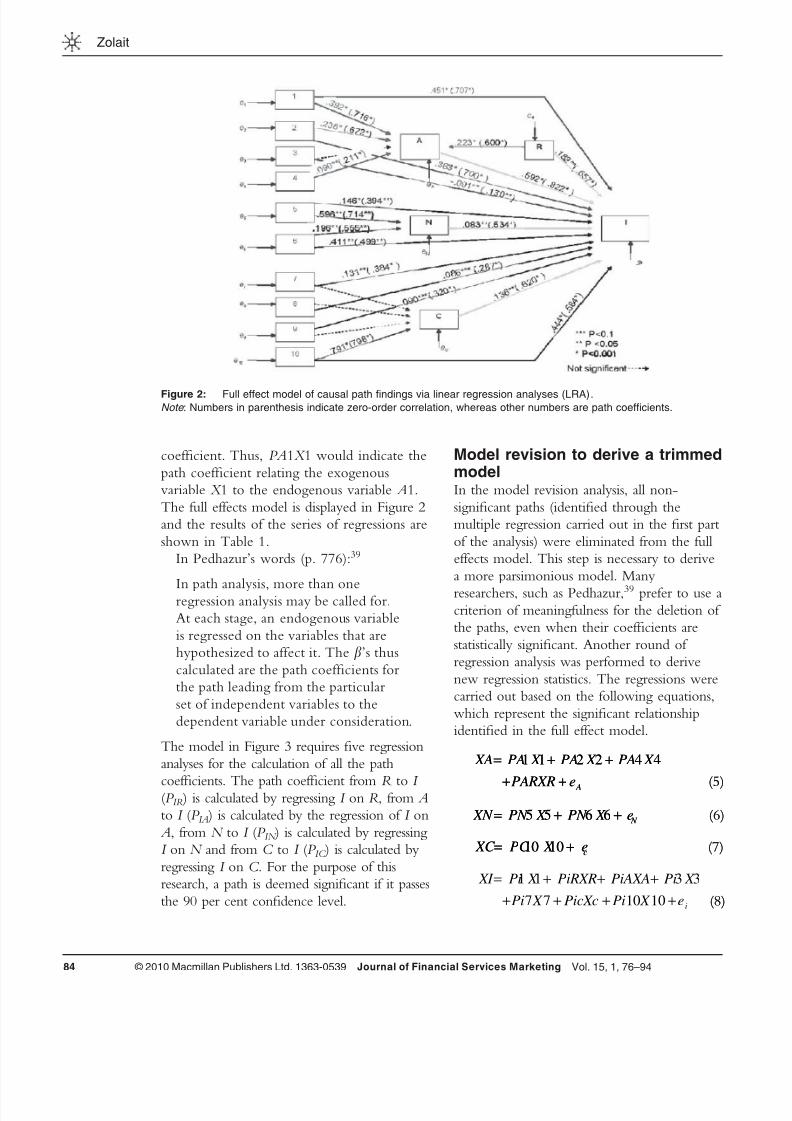

coefficient. Thus, PA 1X 1 would indicate the

path coefficient relating the exogenous

variable X 1 to the endogenous variable A 1.

The full effects model is displayed in Figure 2

and the results of the series of regressions are

shown in Table 1.

In Pedhazur ’s words (p. 776):39

In path analysis, more than oneregression analysis may be called for.

At each stage, an endogenous variable

is regressed on the variables that are

hypothesized to affect it. The ’s thus

calculated are the path coefficients for

the path leading from the particular

set of independent variables to the

dependent variable under consideration.

The model in Figure 3 requires five regression

analyses for the calculation of all the path

coefficients. The path coefficient from R to I (P IR ) is calculated by regressing I on R , from A

to I (P IA ) is calculated by the regression of I on

A , from N to I (P IN ) is calculated by regressing

I on N and from C to I (P IC ) is calculated by

regressing I on C . For the purpose of this

research, a path is deemed significant if it passes

the 90 per cent confidence level.

Model revision to derive a trimmedmodelIn the model revision analysis, all non-

significant paths (identified through the

multiple regression carried out in the first part

of the analysis) were eliminated from the full

effects model. This step is necessary to derive

a more parsimonious model. Many

researchers, such as Pedhazur,39 prefer to use acriterion of meaningfulness for the deletion of

the paths, even when their coefficients are

statistically significant. Another round of

regression analysis was performed to derive

new regression statistics. The regressions were

carried out based on the following equations,

which represent the significant relationship

identified in the full effect model.

XI Pi X PiRXR PiAXA Pi X

Pi X PicXc Pi X ei

= + + +

+ + + +

1 1 3 3

7 7 10 10

XA PA X PA X PA X

PARXR e A

= + +

+ +

1 1 2 2 4 4 XA PA X PA X PA X

PARXR e A

= + +

+ +

1 1 2 2 4 4

(5)(5)

XN PN X PN X e N

= + +5 5 6 6 XN PN X PN X e N

= + +5 5 6 6 (6)(6)

XC PC X ec

= +10 10 XC PC X ec

= +10 10 (7)(7)

(8)(8)

Figure 2: Full effect model of causal path findings via linear regression analyses (LRA).Note : Numbers in parenthesis indicate zero-order correlation, whereas other numbers are path coefficients.

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 10/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–94 85

Factors influencing Yemeni Bank users’ BI to use IB services

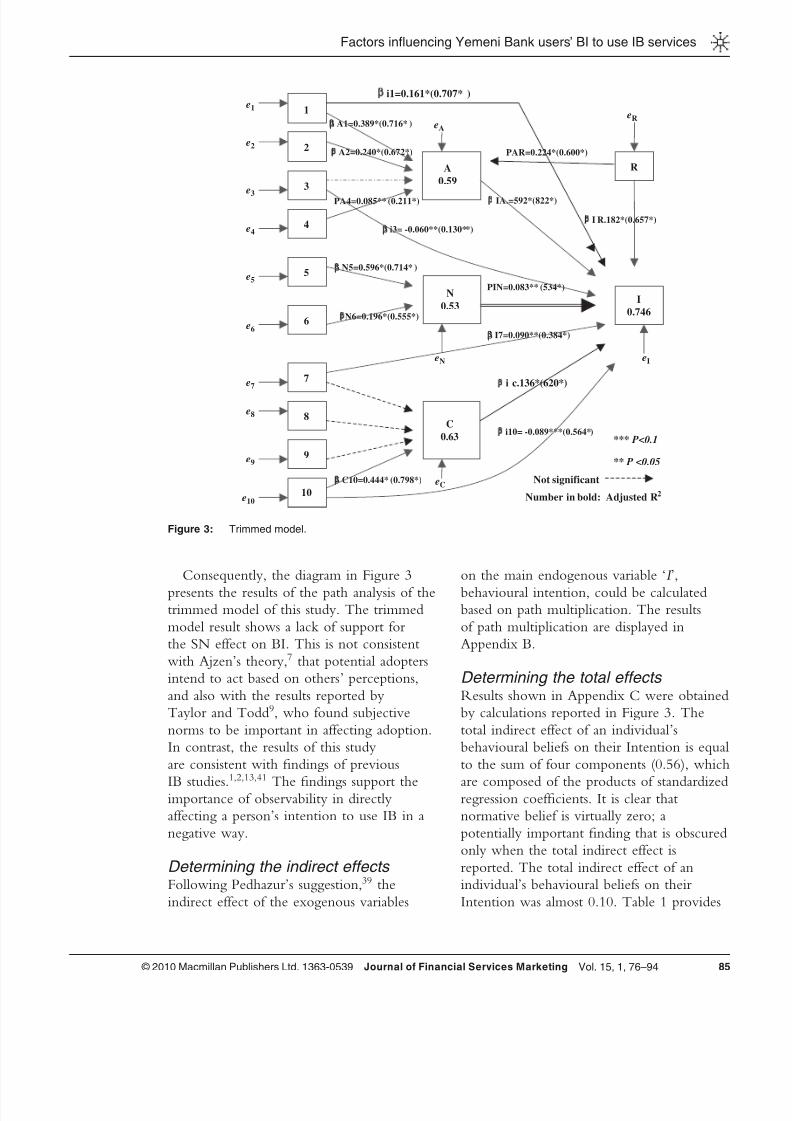

Consequently, the diagram in Figure 3

presents the results of the path analysis of thetrimmed model of this study. The trimmed

model result shows a lack of support for

the SN effect on BI. This is not consistent

with Ajzen’s theory,7 that potential adopters

intend to act based on others’ perceptions,

and also with the results reported by

Taylor and Todd9 , who found subjective

norms to be important in affecting adoption.

In contrast, the results of this study

are consistent with findings of previous

IB studies.1,2,13,41

The findings support theimportance of observability in directly

affecting a person’s intention to use IB in a

negative way.

Determining the indirect effects Following Pedhazur ’s suggestion,39 the

indirect effect of the exogenous variables

on the main endogenous variable ‘I ’,

behavioural intention, could be calculatedbased on path multiplication. The results

of path multiplication are displayed in

Appendix B.

Determining the total effects Results shown in Appendix C were obtained

by calculations reported in Figure 3. The

total indirect effect of an individual’s

behavioural beliefs on their Intention is equal

to the sum of four components (0.56), which

are composed of the products of standardizedregression coefficients. It is clear that

normative belief is virtually zero; a

potentially important finding that is obscured

only when the total indirect effect is

reported. The total indirect effect of an

individual’s behavioural beliefs on their

Intention was almost 0.10. Table 1 provides

PA4=0.085** (0.211*)

PAR=0.224*(0.600*)

PIN=0.083** (534*)

β I7=0.090**(0.384*)

Not significant

β i10= -0.089***(0.564*)

β i c.136*(620*)

eN eI

eR

e5

eC

e6

e8

e7

e9

e10

e3

e4

e1

e2

β I R.182*(0.657*)

β C10=0.444* (0.798*)

β IA.=592*(822*)

β N5=0.596*(0.714* )

βN6=0.196*(0.555*)

β i3= -0.060**(0.130**)

β A1=0.389*(0.716* )

β A2=0.240*(0.672*)

I

0.746

5

2

N

0.53

A

0.59

C

0.63

9

8

10

7

3

6

1

4

R

eA

β i1=0.161*(0.707* )

*** P<0.1

** P <0.05

Number in bold: Adjusted R2

Figure 3: Trimmed model.

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 11/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–9486

Zolait

T a b l e

1 :

S u m m a r y a s s e s s m e n t o f r e s e a r c h h y p o t h e s e s

A n a l y s i s t e c h n i q u e s

C r i t e r i o n ( D V )

H y p o t h e s e s

P r e d i c t o r s ( I V )

S t a t i s t i c t e s t

R e s u l t s

t

S i g .

B e

t a

M u l t i p l e r e g r e s s i o n + F A

B e h a v i o u r a l

i n t e n t i o n ( B I )

H 1 , H 2

H 1 a

A t t i t u d e

1 7 . 8 0

0 . 0 0 0 * * *

0 . 6 5

3

S u p p o r t e d

H 1 b

S u b j e

c t i v e n o r m

2 . 8 5

0 . 0 0 4 * *

0 . 0 9

7

S u p p o r t e d

H 1 c

P B C

6 . 1 3

0 . 0 0 0 * * *

0 . 2 0

7

S u p p o r t e d

F a c t o r a n a l y s i s

H 3

H 4

B e h a

v i o u r a l b e l i e f s

—

—

—

S u p p o r t e d

H 5

N o r m

a t i v e b e l i e f s

—

—

—

S u p p o r t e d

H 6

C o n t r o l b e l i e f s

—

—

—

S u p p o r t e d

F a c t o r a n a l y s i s + M R

A t t i t u d e

H 4

H 4 a

R e l a t

i v e A d v a n t a g e / C o m p a t i b i l i t y

8 . 7 6 4

0 . 0 0 0 * * *

0 . 4 6

6

S u p p o r t e d

H 4 b

O b s e

r v a b i l i t y

− 0 . 6 2 7

0 . 5 3 1

− 0 . 0 2

6

R e j e c t e d

H 4 c

E a s e

o f u s e

6 . 2 3 0

0 . 0 0 0 * * *

0 . 3 2

5

S u p p o r t e d

H 4 d

T r i a l a

b i l i t y

1 . 6 5 3

0 . 0 9 9 *

0 . 0 6

8

R e j e c t e d

M R + F a c t o r a n a l y s i s

S u b j e c t i v e

n o r m ( S N )

H 5

H 5 a

P e r s o

n a l ( P R )

1 3 . 3 3

0 . 0 0 0 * * *

0 . 5 9

6

S u p p o r t e d

H 5 b

M e d i a ( M M )

4 . 4 0

0 . 0 0 0 * * *

0 . 1 9

6

S u p p o r t e d

H i e r a r c h i c a l r e g r e s s i o n +

F a c t o r a n a l y s i s

P B C H 6

H 6 a

F a c i l i t a t i n g t e c h n o l o g y ( F T )

5 . 5 5 5

0 . 0 0 0 * * *

0 . 1 0

9

( a )

H 6 b

F a c i l i t a t i n g r e s o u r c e ( F R )

3 . 8 1 5

0 . 0 0 0 * * *

0 . 6 6

2

( a )

H 6 c

G o v e

r n m e n t s u p p o r t G O V S P

2 . 3 4 7

0 . 0 1 9 * *

0 . 0 1

6

( a )

H 6 d

S e l f - e

f fi c a c y ( S E )

2 1 . 1 8 1

0 . 0 0 0 * * *

0 . 7 9

1

S u p p o r t e d ( b )

B e h a v i o u r a l

i n t e n t i o n ( B I )

H 7 a

A w a r e n e s s ( A W )

5 . 4 8 1

0 . 0 0 0 * * *

0 . 2 4

4

S u p p o r t e d

H 7 b

K n o w

l e d g e ( K W )

7 . 2 8 4

0 . 0 0 0 * * *

0 . 2 9

8

S u p p o r t e d

H 7 c

E x p e r i e n c e ( E X T )

7 . 4 3 4

0 . 0 0 0 * * *

0 . 3 6

3

S u p p o r t e d

H 7 d

E x p o s u r e ( E X P O S )

4 . 7 1 9

0 . 0 0 0 * * *

0 . 2 2

4

S u p p o r t e d

S t e p w i s e r e g r e s s i o n

B e h a v i o u r a l

i n t e n t i o n ( B I )

H 8 a

A t t i t u d e ( A T T )

1 5 . 7 6 3

0 . 0 0 0 * * *

0 . 5 9

2

S u p p o r t e d

H 8 b

U s e r ’ s i n f o r m a t i o n a l b a s e d r e a d i n e s s ( U I B R )

4 . 8 8 0

0 . 0 0 0 * * *

0 . 1 8

2

S u p p o r t e d

H 8 c

P B C

( P B C )

3 . 7 1 2

0 . 0 0 0 * * *

0 . 1 3

6

S u p p o r t e d

H 8 d

S u b j e

c t i v e n o r m s ( S N )

2 . 5 5 0

0 . 0 1 1 * *

0 . 0 8

3

S u p p o r t e d

* * * P < 0 . 0

0 1 ,

* * P < 0 . 0

5 ,

* P < 0 . 1 .

( a ) M a r g i n a l p o s i t i v e a n d

s i g n i fi c a n t r e l a t i o n s h i p s .

( b ) S i g n i fi c a n t a t P < 0 . 0

0 1 .

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 12/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–94 87

Factors influencing Yemeni Bank users’ BI to use IB services

a summary of the entire results of the

hypotheses testing. It shows that 22 out of

the 24 main and sub-hypotheses were

supported. There are two hypotheses that

were rejected, and three that exhibited

marginal positive and significant relationships.

CONCLUSIONSThe findings of this study indicate that the

majority of the respondents are innovators

and early adopters of IB. In addition, the

relative advantages combined with

compatibility represent the IB attributes that

are of most interest to Yemeni bank

customers followed by ease of use (EOU).

The influence of both personal and media

referents shows up as a prominent

determinant of the SN. SE is a prominentdeterminant of PBC, whereas FC of

technology, resources and government

support are marginal predictors. Although

customers perceived that the Relative

Advantage/Compatibility and EOU are

significant and important attributes of IB, the

extent of actual usage of IB by the bank

customers in Yemen is still not strong. The

finding on the observability attribute of

conducting IB could lead one to conclude

that this innovation’s attribute is an undesired

attribute for IB, which negatively affects thecustomers’ intention to adopt IB. It was

noted that customers’ intention to adopt IB

will be influenced by both personal and

media norms.

The test of generalizability of the results

conducted in this research used both statistical

tools (spilt sample, and Adjusted R 2 )42 and

the findings of previous research.42 The test

of generalizability could lead one to conclude

that SN is the weakest psychological

determinant of Intention in this study withrespect to the IB adoption in Yemen,

whereas it could lead one to conclude that

attitudes, readiness and PBC are prominent

direct predictors of IB. This study

has fulfilled both the objectives of the

research and supported TPB. The decrease

of awareness, knowledge, experience and

exposure in the adopter led to the decrease

of intention to use the IB service. As the

number of actual users of IB was very

limited at the time of this study, further

promotion is required to make customers

aware of the existence of IB. This research

has highlighted that UIBR is an importantfactor that must be considered in research

adoption. Although there have now been

quite a lot of papers on the adoption of IB,

this study contributes to the body of

knowledge by giving much focus on a new

integrated approach of user ’s readiness that

gives much concern/pays great attention to

investigating the user ’s informational and

psychological readiness to use technology.

In this study, we look into the adoption of

use and integration of both UIBR andpsychological readiness to accept IB services.

Furthermore, the study benefited from DOI,

which provides the widely applied concepts

of DOI by modelling the attributes of

innovation as part of attitudinal belief and

the communication channels as part of

normative belief.

The contribution of this study can be

viewed from two perspectives, that is

theoretical as well as managerial.

Subsequently, there are four theoretical

implications. First, the study empiricallyillustrated that SN acts as a second-order

formative structure, formed by two distinct

dimensions: (personal and media referents),

and accordingly, normative belief is viewed

as a two-dimensional construct, which allows

a more detailed examination of external

normative beliefs. Previous studies were

concerned only with the influence of

referents that rely on person-to-person

interaction (personal).

Second, this study provides anunderstanding of the nature and role of PBC

which, according to Pavlou and Fygenson,43

is still not well understood. Third, the

empirical data affirm that UIBR is a new

predictor of an individual’s behavioural

intention to use IB. Fourth, a formative

structure permits a more detailed prediction

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 13/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–9488

Zolait

of external, behavioural, normative and

control beliefs by allowing a distinct

prediction of (1) IB attributes as perceived

by the respondents and their role in the

prediction of an individual’s attitude in

formative structure, (2) personal and media

referents which, in turn, contribute to abetter prediction of SN and (3) SE and FC

(controllability), which lead to a better

prediction of PBC, and behavioural

intention.

In terms of the managerial contribution,

the study has shown that managers have to

be prepared to provide financial services via

the Internet, as there are customers who

prefer to conduct IB. In addition, offering IB

would also mean that Yemeni banks would

be able to expand their customer base.Furthermore, the study proved that personal

interaction is influential in shaping an

individual’s SN to adopt IB. Therefore,

banks should focus on personal referents to

increase the number of IB adopters among

their customers. In addition, the banks

should use MM as a channel of interaction

with individuals in their effort to increase IB

users.

Despite the various contributions, the

study has two main limitations. One is the

sample size. It was difficult to get bankcustomers to respond to the survey; hence,

the targeted sample of 1000 was not

achievable. A larger sample would enhance

the results statistically. Future studies should

incorporate more respondents. The second

limitation is the target population. The

study concentrated only on certain regions

in Yemen and, hence, may not be

representative of the entire Yemeni

population. Future studies should expand

to other regions as well as other MiddleEast countries. In addition, it is proposed

that comparative studies between developed

and developing countries and between

different regions of the world be

conducted using the framework used

in this study to further validate the existing

findings.

REFERENCES1 Cyree, k., Delcoure, N. and Dickens, R. (2009) An

examination of the performance and prospects for the

future of internet-primary banks. Journal of Economics and

Finance 33(2): 128 – 147.

2 Mattila, M., Karjaluoto, H. and Pento, T. (2003) Internet

banking adoption among mature customers: Early

majority or laggards. Journal of Services Marketing 17(5):

514 – 528.

3 Lu, M., Liu, C., Jing, J. and Huang, L. (2005) Internet

banking: Strategic responses to the accession of WTO by

Chinese banks. Industrial Management & Data System

105(4): 429 – 442.

4 Sahut, J. and Kucerova, Z. (2009) Enhanced internet

banking service quality with quality function deployment

approach. Journal of Internet Banking and Commerce ,

http://www.arraydev.com/commerce/jibc/0311-09.htm.

5 Kamel, S. (2009) The use of information technology to

transform the banking sector in developing nations.

Information Technology for Development 11(4): 305 – 312.

6 Cheng, T.C., Lam, D. Y. and Andy, C. Y. (2006)

Adoption of internet banking: An empirical study

in Hong Kong. Decision Support Systems 42(3):

1558 – 1572.

7 Ajzen, I. (1991) The theory of planned behaviour .

Organizational Behaviour and Human Decision Processes

50(2): 179 – 211.

8 Mathieson, K. (1991) Predicting user intention: Comparing

the technology acceptance model with the theory of planned

behaviour . Information Systems Research 2(3): 173 – 191.

9 Taylor , S. and Todd, P.A. (1995a) Understanding

information technology usage: A test of competing

model. Information Systems Research 6(2): 144 – 176.

10 Battacherjee, A. (2000) Acceptance of e-commerce

services: The case of electronic brokerages. IEEE

Transactions on Systems, Man and Cybernetics – Part A:

Systems and Humans 30(4): 411 – 420.

11 Lim, J., Gan, B. and Chang, T.-T. (2002) A survey onNSS adoption intention. Proceedings of the 35th Hawaii

International Conference on System Sciences; 7 – 10

January 2002, pp. 399 – 408, http://www.ieee.org/portal/

site, accessed 6 May 2004.

12 Shih, Y. and Fang, K. (2004) The use of a decomposed

theory of planned behaviour to study internet banking in

Taiwan. Internet Research 14(3): 213 – 223.

13 Tan, M. and Teo, T.S.H. (2000) Factors influencing the

adoption of internet banking. Journal for Association of

Information System 1(5): 1 – 42, http://portal.acm.org/

citation.cfm?id:374134.

14 ITU. (2009) International telecommunication union:

News related to ITU telecommunication/ICT statistics,

http://www.itu.int/ITU-D/ict/newslog/Internet+

Subscribers+Rise+36+In+2008+Yemen.aspx, accessed31 July 2009.

15 Taylor , S. and Todd, P. (1995b) Decomposition and

crossover effects in the theory of planned behaviour:

A study of consumer adoption intentions. International

Journal of Research in Marketing 12(2): 137 – 155.

16 Zolait, A.H., Mattila, M. and Sulaiman, A. (2009)

The effect of user’s informational-based readiness on

innovation acceptance. International Journal of Bank

Marketing 27(1): 76 – 100.

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 14/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–94 89

Factors influencing Yemeni Bank users’ BI to use IB services

17 Courter , E. (1999) Home banking missteps. Credit Union

Management 22(3): 10 – 12.

18 Ajzen, I. and Fishbein, M. (1980) Understanding Attitudes

and Predicting Social Behaviour . Englewood Cliffs, NJ:

Prentice-Hall.

19 Rogers, E.M. (1995) Diffusion of Innovations , 4th edn.

New York: Free Press, Collier Macmillan.

20 Doll, J. and Ajzen, I. (1992) Accessibility and stability

of predictors in the theory of planned behaviour . Journal of Personality and Social Psychology 63(5):

754 – 765.

21 Ajzen, I. (2001) Nature and operation of attitudes.

Annual Review of Psychology: Pro Quest Medical Library 52(1):

27 – 58.

22 Kautz, K. and Larsen, E. (2000) Diffusion theory and

practice: Disseminating quality management and software

process improvement innovations. Information Technology

& People 13(1): 11 – 26.

23 Bearden, W.O., Calcich, S.E., Netemeyer , R. and Teel,

J.E. (1986) An exploratory investigation of consumer

innovativeness and interpersonal influences. Advances in

Consumer Research 13(1): 77 – 82.

24 Karahanna, E., Straub, D.W. and Chervany, N.L. (1999)

Information technology adoption across time: A cross-

sectional comparison of pre-adoption and post-adoption

beliefs. MIS Quarterly 23(2): 183 – 213.

25 Gist, M.E. and Mitchell, T.R. (1992) Self-efficacy: A

theoretical analysis of its determinants and malleability.

Academy of Management: The Academy of Management

Review, Briarcliff Manor 17(2): 183 – 211.

26 Hartzel, K. (2003) How self-efficacy and gender issues

affect software adoption and use. Communications of the

ACM 46(9): 167 – 171.

27 Triandis, H.C. (1980) Values, attitudes, and interpersonal

behaviour . In: M.M. Page (ed.) Nebraska Symposium on

Motivation , 1979: Beliefs, Attitudes, Values Lincoln, NE:

University Nebraska Press, pp. 195 – 259.

28 Hall, G., George, A. and Rutherford, W. (1977)

Measuring stages of concern about the innovation: A

manual for use of the soc questionnaire. Research and

development centre for teacher education. Austin, TX:

Southwest Educational Development Laboratory (SEDL),

p. 104, http://www.eric.ed.gov/ERICDocs/data/

ericdocs2sql/content_storage_01/0000019b/80/33/88/f5

.pdf .

29 Karjaluoto, H., Mattila, M. and Pento, T. (2002) Factors

underlying attitude formation towards online banking in

Finland. International Journal of Bank Marketing 20(6):

261 – 272.

30 Chang, Y.T. (2004) Dynamics of banking technology

adoption: An application to internet banking. Warwick

Economic Research Papers. Coventry, UK: Department

of Economics, University of Warwick.

31 Dickerson, M.D. and Gentry, J.W. (1983) Characteristics

of adopters and non-adopters of home computers. Journal

of Consumer Research 10(2): 225 – 235.

32 Sarel, D. and Marmorstein, H. (2003) Marketing online

banking services: The voice of the customer . Journal of

Financial Services Marketing 8(2): 106 – 118.

33 Black, N. J., Lockett, A., Winklhofer , H. and Ennew, C.

(2001) The adoption of internet financial services: A

qualitative study. International Journal of Retail &

Distribution Management 29(8): 390 – 398.

34 Sekaran, U. (2003) Research Methods for Business: A Skill

Building Approach , 4th edn. New York: John Wiley &

Sons.

35 Jackson, S.L. (2006) Research Methods and Statistics: A

Critical Thinking Approach , 2nd edn. Belmont, CA:Wadsworth.

36 Neuman, W.L. (2006) Social Research Methods: Qualitative

and Quantitative Approach , 5th edn. Boston, MA: Allyn &

Bacon.

37 Cohen, J. and Cohen, P. (1983) Applied Multiple

Regression/Correlation Analysis for the Behavioural Sciences ,

2nd edn. New Jersey: Lawrence Erlbaum Associates.

38 Bryman, A. and Cramer , D. (2001) Quantitative Data

Analysis with SPSS Release 10 for Windows: A Guide for

Social Scientists. Philadelphia, PA: Taylor & Francis

Group; Routledge.

39 Pedhazur , E. J. (1997) Multiple Regression in Behavioural

Research: Explanation and Prediction , 3rd edn. Florida:

Thomson Learning.

40 Kerlinger , F.N. and Pedhazur , E. J. (1973) Multiple

Regression in Behavioural Research. New York: Holt,

Rinehart and Winston.

41 Liao, S., Yuan, P.S., Huaiqing, W. and Ada, C. (1999)

The adoption of virtual banking: An empirical study.

International Journal of Information Management 19(1):

63 – 74.

42 Hair , J.F., Black, W.C., Babin, B. J., Anderson, R.E. and

Tatham, R.L. (2006) Multivariate Data Analysis , 6th edn.

Upper Saddle River, NJ: Prentice Hall international.

43 Pavlou, P.A. and Fygenson, M. (2006) Understanding

and predicting electronic commerce adoption an

extension of the theory of planned behaviour . MIS

Quarterly 30(1): 115 – 143.

44 Venkatesh, V. and Davis, F.D. (2000) A theoretical

extension of the technology acceptance model: Four

longitudinal field studies. Management Science 45(2):

186 – 204.

45 Moore, G.C. and Benbasat, I. (1991) Development of an

instrument to measure the perceptions of adopting an

information technology innovation. Information Systems

Research 2(3): 192 – 222.

46 Laforet, S. and Li, X. (2005) Consumers’ attitudes

towards online and mobile banking in China. International

Journal of Bank Marketing 23(5): 362 – 380.

47 Pedersen, P.E. (2005) Adoption of mobile internet

services: An exploratory study of mobile commerce early

adopters. Journal of Organizational Computing & Electronic

Commerce 15(3): 203 – 222.

48 Lassar , W., Manolis, C. and Lassar , S.S. (2005) The

relationship between consumer innovativeness, personal

characteristics, and online banking adoption. International

Journal of Bank Marketing 23(2): 176 – 199.

49 Dandapani, K., Karels, G.V. and Lawrence, E.R. (2008)

Internet banking services and credit union performance.

Managerial Finance 34(6): 437 – 446.

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 15/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–9490

Zolait

APPENDIX ASee Table A1.

Table A1: Regression results: Predicting overall behavioural intention by psychological determinants and UIBR

Independent variable B t R 2 F p

DV1 – Behavioural intention (BI) — — 0.735 252.101 0.000Constant − 3.504 − 3.384 — — 0.001IV1 – Attitude (ATT) 0.790 15.763 — — 0.000IV2 – Readiness (UIBR) 0.101 4.880 — — 0.000IV3 – PBC (PBC) 0.128 3.712 — — 0.000IV4 – Subjective norms (SN) 0.064 2.550 — — 0.011

Model R R 2 Adj. R 2 F p

Summary table 1 0.822 0.676 0.675 764.538 0.0002 0.847 0.718 0.716 465.059 0.0003 0.854 0.730 0.728 329.006 0.0004 0.857 0.735 0.732 252.101 0.000

Independent variable B t R 2 F p

DV2 – Attitude (ATT) — — 0.562 234.693 0.000

Constant 6.380 8.361 — — 0.000IV1 – Relative advantage / compatibility(RAC)

0.247 9.600 — — 0.000

IV2 – Ease of use (EOU) 0.279 6.375 — — 0.007

Model R R 2 Adj. R 2 F P

Summary table 1 0.716 0.513 0.512 386.958 0.0002 0.750 0.562 0.559 234.693 0.000

Independent variable B T R 2 F P

DV3 – Subjective norms (SN) — — 0.535 210.169 0.000Constant 10.821 13.774 — — 0.000IV1 – Personal referent (PR) 0.078 13.334 — — 0.000IV2 – Media referent (MM) 0.047 4.396 — — 0.000

Model R R 2

Adj. R 2

F P Summary table 1 0.714 0.510 0.509 381.947 0.0002 0.731 0.535 0.532 210.169 0.000

Independent variable B T R 2 F P

DV3 – PBC (PBC) — — 0.192 28.906 0.000Constant 13.120 11.319 — — 0.000IV1 – Technology-facilitating condition

(TFC)0.070 5.555 — — 0.000

IV2 – Resource-facilitating condition(RFC)

0.051 3.815 — — 0.000

IV3 – Government support (GOVSP) 0.024 2.347 — — 0.019

Model R R 2 Adj. R 2 F P

Summary table 1 0.372 0.138 0.136 58.921 0.0002 0.424 0.180 0.175 40.111 0.0003 0.438 0.192 0.185 28.906 —

Independent variable B T R 2 F P

DV3 – PBC (PBC) — — 0.637 643.747 0.000Constant 8.033 12.498 — — 0.000IV1 – Self-efficacy (SE) 0.112 25.372 — — 0.000

P < 0.05.

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 16/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–94 91

Factors influencing Yemeni Bank users’ BI to use IB services

APPENDIX BSee Table B1.

APPENDIX CSee Table C1.

APPENDIX DSee Table D1.

Table B1: Path analysis indirect effects

Cause / effects Indirect paths Path coefficient

Behavioural belief / intention X1; XA; XI (0.389×0.592)=0.230288

X2; XA; XI (0.240×0.592)=0.14200X4; XA; XI (0.085×0.592)=0.05032XR; XA; XI (0.224×0.592)=0.132608

Normative belief / intention X5; XN; XI (0.596×0.083)=0.049468X6; XN; XI (0.196×0.083)=0.016268

Control belief / intention X10; XC; XI (0.798×0.124)=0.098952

Table C1: The total effects of behavioural belief, normative belief and control belief on the behavioural intention

Cause / effects Indirect effect Direct effect Total effect

Behavioural belief / intention + 0.230288 0.161 —+ 0.14200 − 0.060 —+ 0.05032 — —+ 0.132608 — —

Total 0.555216 0.10 0.655216

Normative belief / intention + 0.049468 — —+ 0.016268 — —

Total 0.065736 0.00 0.065736

Control belief / intention 0.098952 − 0.089 0.075688

Table D1: Questionnaire items in a 7-point Likert scale

Q. No. Items (in a 1– 7 Likert scale: Strongly disagree (1) and strongly agree (7))

Models references

Intention (I) INT1 Given the chance, I predict that I would use Internet banking (IB)

in the future to achieve my banking activities.Venkatesh and Davis;44

Mathieson;8 Shih and Fang12

INT2 I will strongly recommend others to use IB.INT3 My favourable intention would be to use (IB) rather than my

(traditional banking) for my banking practice.INT4 I plan to use IB.INT5 When I have access to the IB system, I intend to use it.

Attitude (A) ATT 1 In my opinion, using the IB services is a good idea.ATT 2 I think it is a wise idea for me to use the IB services.ATT 3 I like the idea of using the IB services.ATT 4 Using the IB services would be a pleasant experience.

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 17/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–9492

Zolait

Table D1: Continued

Q. No. Items (in a 1– 7 Likert scale: strongly disagree (1) and strongly agree (7))

Models references

Relative advantage (RA) RA1 If I were to use IB, it would enable me to accomplish my

tasks more quickly.Moore and Benbasat;45

Karahanna et al 24 RA2 If I were to use IB, the quality of my work would improve.

RA3 If I were to use IB, it would enhance my effectiveness on the job.RA4 If I were to use IB, it would make my job easier.RA5 Using IB gives me greater control over my work.

Complexity (PEOU) COX1 Learning to operate IB would be easy for me. Moore and Benbasat;45

Karahanna et al ;24 Tan and Teo13

COX2 Overall, if I were to use IB, it would be easy to use.COX3 It would be easy for me to become skilful at using IB.COX4 I believe that it is easy to get IB to do what I want it to do.COX5 If I were to use IB, it would be (not available) difficult to use.COX6 Using IB requires a lot of mental effort.

Compatibility (COMPT) COM1 If I were to use IB, it would be compatible with most aspects

of my work.Moore and Benbasat;45

Karahanna et al; 24

Tan and Teo13 COM2 If I were to use IB, it would fit my work style.COM3 If I were to use IB, it would fit well with the way I like to work.

Trialability (TR) TR1 Before deciding on whether or not to use IB, I want to be able to

use it on a trial basis.Moore and

Benbasat;45 Karahannaet al ;24 Tan and Teo13

TR2 Before deciding on whether or not to use IB, I want to be able toproperly try it out.

TR3 I want to be permitted to use IB, on a trial basis long enough tosee what it can do.

Observability (OBSRV): If the bank introduces IB service OBS1 I will use it when many use it. Karahanna et al 24 OBS2 I will use it when I have seen others using IB.

OBS3 I will use it as soon as I get to know about it.OBS4 I will use it if this service becomes popular.OBS5 I will wait until other customers start to use it.OBS6 I will use it when other people have successful experience

of using it.OBS7 If IB is unknown to me, I will not use it.

Subjective norm (SN) SN1 Most people, who are important to me would think that I should

use IB to get bank services.Taylor and Todd;15

Shih and Fang12 SN2 The people who influence my decisions would think that I should

use IB.SN3 Most people who are important to me would think that I should try

out the bank’s website to get access to the bank’s IB.SN4 The people who influence my decisions would think that I should try

out the bank’s website to get access to the bank.SN5 Most people who are important to me would think that using IB is a

good idea.SN6 Most people who are important to me would think I should use IB.

Perceived behavioural control PBC PBC1 I would be able to use IB. Taylor and Todd9 PBC2 I have the resources necessary to make use of IB.PBC3 I have the knowledge necessary to make use of IB.PBC4 I have the ability to make use of IB.PBC5 Using IB would be entirely within my control.

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 18/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–94 93

Factors influencing Yemeni Bank users’ BI to use IB services

Table D1: Continued

Q. No. Items (in a 1– 7 Likert scale: Strongly disagree (1) and strongly agree (7))

Models references

UIBR attribute Awareness

AW1 I do not even know what IB is. Hall et al 28 AW2 I am not concerned about IB.

AW3 I am completely occupied with other things.AW4 Although I do not know about IB, I am concerned about thingsin the area.

AW5 At this time, I am not interested in learning about IB.

Knowledge KW1 I have a very limited knowledge of IB. Hall et al 28 KW2 I would like to discuss the possibility of using IB.KW3 I would like to know what resources are available if I want decide to

adopt IB.KW4 I would like to know what the use of IB will require in the immediate

future. .KW5 I would like to know how this innovation is better than other banking

innovation.

Experience EXP1 I have a great deal of experience using the Internet. Laforet and Li;46 Karjaluoto

et al 29 EXP2 I have a great deal of experience using computers.EXP3 I have a great deal of experience using personal banking.

Exposure Expo1 I have seen advertisements recommending the use of IB. Chang30 Expo2 I have used IB before.Expo3 I have been exposed to a recommendation to use IB.

Normative influences (NB × MC) Personal reference

MCPER1 Peers / colleagues think that I should use IB and I will do whatpeer / colleagues suggest I do.

Taylor and Todd15

MCPER2 Peers / colleagues think that I should try out IB and I will do whatpeer / colleagues suggest I do.

MCPER3 Opinion leaders think that I should use IB and I will do what leaders

suggest I do.MCPER4 Opinion leaders think that I should try out IB and I will do whatleaders suggest I do.

MCPER5 Bank’s employees think that I should use IB and I will do what thebank’s people suggest I do.

MCPER6 Bank’s employees think I should try out IB and I will do what thebank’s people suggest I do.

Media reference MCMEDIA1 The media suggest using IB is a good idea and I will do what the

media suggest.Pedersen;47 Battacherjee10

MCMEDIA2 The media consistently recommend using IB services and I will dowhat the media suggest.

MCPRFS3 For my profession, it is advisable to use IB services and I will dowhat it suggests.

MCMEDIA4 I read / saw news reports that using IB is a good way of managingmy bank account and I will do what the media suggest.

Self-efficacy DSE1 I feel comfortable using IB on my own and for me this aspect is

important.Lassar et al 48

DSE2 I can easily operate IB from the bank’s website on my own and forme this aspect is important.

DSE3 I can use IB without others’ help and for me this aspect is important.

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 19/20

© 2010 Macmillan Publishers Ltd. 1363-0539 Journal of Financial Services Marketing Vol. 15, 1, 76–9494

Zolait

Table D1: continued

Q. No. Items (in a 1– 7 Likert scale: Strongly disagree (1) and strongly agree (7))

Models references

Government support FGS1 Government supports e-commerce. Tan and Teo13 FGS2 Government endorses e-commerce.FGS3 Setting up the facilities to enable e-commerce.

FGS4 Government promotes e-commerce.

Facilitating resources FR1 Facilitate computers for everyone to use IB services. Taylor and Todd9 FR2 Facilitate access to the Internet at low prices to make it affordable to

use IB.FR3 Facilitate IB availability then I would be able to use IB when I need it.FR4 I have the time to set up IB services.FR5 I have enough money to use IB services.

Facilitating technology conditions FT1 I have the computers, Internet access and applications needed to

use IB.Taylor and Todd;9

Shih and Fang12 FT2 Facilitate the bank’s IB transactional websites to use IB.FT3 Facilitate a good quality of Internet connection to use IB.FT4 Facilitate high quality of Internet wireless to use IB.

8/8/2019 Mr Project Article

http://slidepdf.com/reader/full/mr-project-article 20/20

Copyright of Journal of Financial Services Marketing is the property of Palgrave Macmillan Ltd. and its content

may not be copied or emailed to multiple sites or posted to a listserv without the copyright holder's express

written permission. However, users may print, download, or email articles for individual use.