multi asset study

TRANSCRIPT

Welcome to the first in a series of research papers setting out the

findings of our proprietary in-depth analysis of multi-asset portfolios.

For the first time, this analysis includes the performance of funds run

by fiduciary managers, as well as those of investment managers.

Multi Asset Study

Multi Asset Study 2

Through the series, we outline a wide range of issues investors

should consider, aiming to provide readers with a framework for

selecting and assessing multi-asset managers. We explore the

behaviour of these funds, delving beyond headline risk and return

numbers to understand “how” returns have been generated.

To set the groundwork we introduce a new way of breaking down performance in

multi-asset portfolios. This new approach allows us to identify the key drivers behind

managers’ performances and use this to re-set investor expectations for performance

going forward.

Three key questions

• Is there a “style” of multi-asset investing that works better across all

market environments?

• Do multi-asset investments provide a low governance way to quickly

capture opportunities?

• Do multi-asset investments provide any material access to the

illiquidity premium?

The most important consideration when selecting or deciding to retain an investment is

whether that investment is fulfilling the role it was chosen for in the context of the wider

strategy. This bigger-picture assessment should not be overlooked in favour of more

detailed fund analysis.

However, by using the tools and framework provided through

this series, investors will benefit from a clearer view of how a

manager fits into their strategy and when they are not fulfilling

their role. This paper focuses on the key observations and

conclusions from our work and is supplemented by a detailed

paper which goes into depth on the underlying analysis.

The detailed study explores 25 multi-asset portfolios,

including pooled “diversified growth” funds offered by

asset managers, and “central” growth portfolios offered

by fiduciary managers.

The analysis and conclusions are based primarily on

an independent, wide-ranging survey of multi-asset

providers coordinated by Barnett Waddingham. This data

goes beyond headline risk and return figures, additionally

exploring portfolio attributes such as allocations, liquidity

profile and portfolio construction considerations.

Multi Asset Study 3

Under the banner of “multi-asset strategies”, there are a

wide range of nuanced sub-strategies and different ways

of implementing and accessing returns. Where available,

performance attribution provided by multi-asset managers

can help investors understand which asset classes have

contributed to returns. However, this only answers the

superficial question, “Where was the return generated?”

A new way to think about return generation

01

Multi Asset Study 4

We want to answer a subtly different question: “How did my

manager generate returns?” For example, was it through

active decisions or general market trends? Was it because

they adopt a high risk strategy?

Whilst the universe of asset classes is seemingly ever-expanding

and increasingly complex, we believe there continue to be

the same four fundamental sources of return that have always

existed.

It is important to understand that there isn’t a one-to-one

translation from an asset class-based performance attribution to

the sources of return set out above.

For example, an equity fund could be passively

implemented, in which case this could be

categorised as “owning”. For an active fund, there

is an element of skill, often referred to as “alpha”,

which is expected to contribute to returns.

As you will see from this series, analysing returns using this

model provides us with a much clearer picture of how multi-

asset managers generate their returns, which in turn allows

us to more easily draw out key conclusions about multi-asset

investing and will enable investors to better appoint funds that fit

in with their wider portfolio.

Skill: active decisions to allocate assets in assets which then increase in

value over time

e.g. stock selection, style tilts, dynamic asset allocation,

macroeconomic positioning

Lending: money to a third party and, as compensation for associated

risk, receive interest payments over time

e.g. government bonds, corporate bonds

Structural price premia: notably illiquidity (a premium compensating

for locking up assets for an extended period of time) or complexity

(influencing demand-side pricing)

e.g. private equity, private debt

Owning: an asset that increases in value, realised upon sale of the asset

e.g. equities, property, infrastructure

Multi Asset Study 5

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

20%

18%

16%

14%

12%

10%

8%

6%

4%

2%

0%

The results in a single chart: How each manager has generated returns (2019)

There is wide variation in the balance of the sources of return across providers. What’s more, there is a strong and predictable link between a manager’s style and the broad

balance observed. For example, those multi-asset managers with an “absolute return” portfolio construction approach were generally less reliant on “owning” and “lending”

sources, i.e. those whose contribution is most closely linked to market returns. This link between portfolio construction and observable results means that, in general terms,

investors can be more sure of how a manager will perform in different market conditions. For example, during rising equity markets, it is unsurprising that those with an

absolute return focus, i.e. largely reliant on skill, were amongst the lower returning strategies (i.e. those on the left hand side above).

Effective date 31 December 2019. 21 of 25 managers surveyed provided sufficient data for inclusion in this section.

Multi Asset Study 5

Private Markets

Stock selection and other skill

DAA

Credit (lending)

Diversifying markets

Equity

Total return over 2019

Only a small number of providers were able to isolate the value

added through dynamic asset allocation in a meaningful way

CO

NT

RIB

UT

ION

TO

OV

ERA

LL R

ETU

RN

AB

SOLU

TE

RET

UR

N

Multi Asset Study 6

Using the framework set out above and data provided

by the managers we start to unravel the performance of

multi-asset investments. In the first instance, we focus on

answering the following questions:

• Is there a “style” of multi-asset investing that works

better across all market environments?

• Does multi-asset investing provide a low governance

way to quickly capture opportunities?

• Does multi-asset investing provide any material access

to the illiquidity premium?

Tackling three fundamental questions

02

Multi Asset Study 7

What does a style tell us about performance?We have been advising clients on multi-asset funds for over

25 years and a conversation we return to time and time again

is whether there is a particular style of multi-asset investing

that is best.

Do dynamic funds perform better than static ones? Do funds run by fiduciary managers

perform better than those run by investment managers? Do portfolios with high

exposures to market risks perform better than those with a more absolute-return style?

The list goes on.

The short answer is, no. There is no single approach that

consistently outperforms.

The charts overleaf illustrate how the best and worst performing managers in each year

performed in the subsequent year. For example, we can see that, 38% of the managers

with top-quartile performance in 2018 generated returns in the bottom-quartile the

following year. Similarly, 25% of the worst performing managers in 2018 were

amongst the best performing managers of 2019.

As well as showing that there is not a single approach that

consistently outperforms, this analysis suggests that investors

need to be patient. One year’s “poor” performance shouldn’t

make you nervous as an investor as long as the manager has

performed in line with what you would expect given their style.

Multi Asset Study 8

38%

13%

13%

38%

75%

0%

13%

13%

25%

25%

13%

38%

25%

0%

38%

38%

2015 2016 2017 2018 2019

PERFORMANCE RESULTS OF TOP QUARTILE MANAGERS FOLLOWING EACH YEAR

Bottom Quartile

Third Quartile

Second Quartile

Top Quartile

Sources: Fund managers; Barnett Waddingham LLP

25%

0%

50%

25%

0%

25%

13%

63%

25%

25%

25%

25%

25%

50%

25%

0%

2015 2016 2017 2018 2019

PERFORMANCE RESULTS OF BOTTOM QUARTILE MANAGERS FOLLOWING EACH YEAR

Bottom Quartile

Third Quartile

Second Quartile

Top Quartile

Sources: Fund managers; Barnett Waddingham LLP

Multi Asset Study 9

9%

8%

7%

6%

5%

4%

3%

2%

1%

0%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Ret

urn

ove

r th

ree

year

s to

31

Dec

emb

er 2

019

(% p

.a.)

Average equity allocation over three years to 31 December 2019

Effective date 31 December 2019. 21 of 25 managers surveyed provided sufficient data for inclusion in this section.

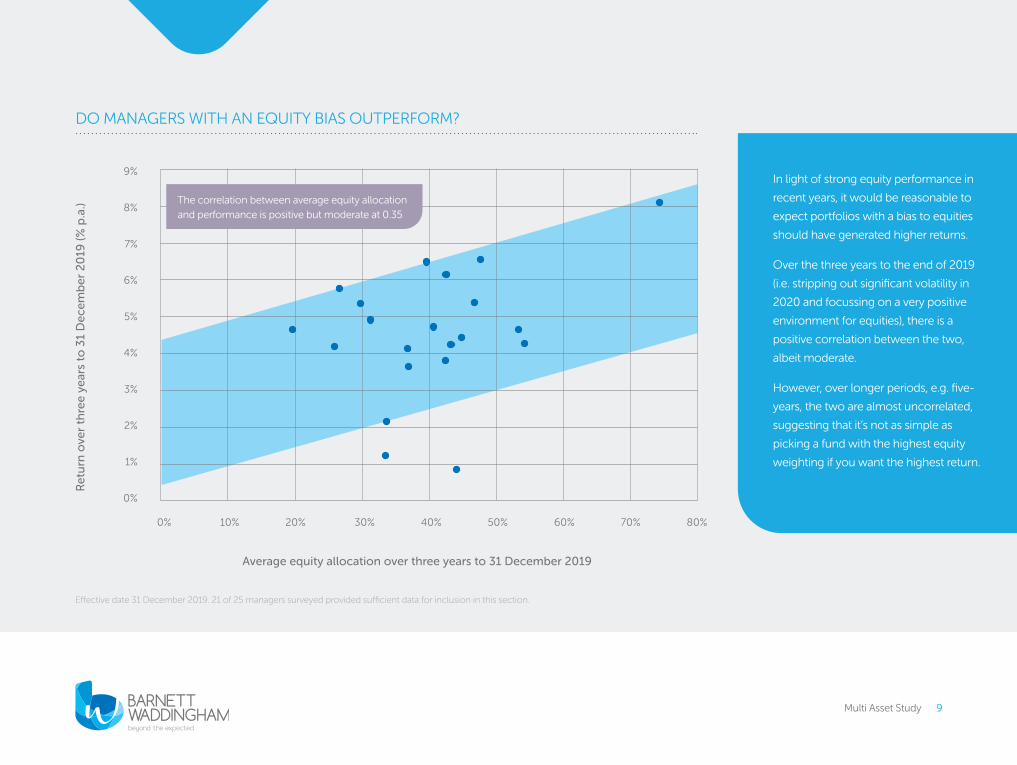

In light of strong equity performance in

recent years, it would be reasonable to

expect portfolios with a bias to equities

should have generated higher returns.

Over the three years to the end of 2019

(i.e. stripping out significant volatility in

2020 and focussing on a very positive

environment for equities), there is a

positive correlation between the two,

albeit moderate.

However, over longer periods, e.g. five-

years, the two are almost uncorrelated,

suggesting that it’s not as simple as

picking a fund with the highest equity

weighting if you want the highest return.

DO MANAGERS WITH AN EQUITY BIAS OUTPERFORM?

The correlation between average equity allocation

and performance is positive but moderate at 0.35

Multi Asset Study 10

The analysis broadly supports what we instinctively expected,

that the best style varies with market conditions. For example:

Crucially, we did not find one provider observably changed their

approach to perform strongly across all market environments.

This is perhaps the most important point in this paper: Multi-

asset managers will very rarely deviate from their DNA and so in

selecting the manager you are choosing your source of returns.

We do not think this is a bad thing – managers should stick to

where they feel they have a competitive advantage. However,

it means it is vital for investors to fully understand the DNA

of the multi-asset manager they are investing in and, if using

this manager as a subset of their portfolio, whether this DNA

complements the rest of the portfolio.

“This is perhaps the most important

point in this paper: Multi-asset

managers will very rarely deviate

from their DNA and so in selecting

the manager you are choosing

your source of returns.”

When market returns are strongly

positive, the opportunity to add

significant value from “skill” is

materially lessened…

In contrast, when market returns are

strongly negative, those with higher

reliance on skill typically have lower

levels of market exposure…

In volatile markets, there is more

potential to add value through skill

(e.g. stock picking or dynamic asset

allocation) and the contribution of

“skill” should be expected to

be higher…

… and funds with higher market

exposures (i.e. “owning” and

“lending”) tend to perform better

… and funds with lower reliance

on owning or lending are better

protected from falling prices

in general

… but whether this contribution

is positive or negative in absolute

terms is difficult to generalise

and results vary on a fund-by-

fund basis

Multi Asset Study 11Multi Asset Study 11

WHAT DOES IT MEAN TO BE DYNAMIC?

Effective date 31 December 2019. 19 of 25 managers surveyed provided sufficient data for inclusion in this section.

60%

50%

40%

30%

20%

10%

0%

60%

50%

40%

30%

20%

10%

0%

Average

AverageAverage allocation to equities over 5 years

Average allocation to fixed income over 5 years

1The majority of managers chose “2-5 year” when asked for the time horizon over

which top-level asset allocation decisions are made.

For many multi-asset managers, being dynamic does

not mean taking advantage of short-term opportunities

in the way that we discuss in the next section. Instead, it

means adjusting the portfolio to reflect their outlooks for

the various asset classes over the medium-term (usually

around three years)1.

The chart to the left shows the minimum, maximum and

average allocation to equities and fixed income of each

manager over the last five years.

It shows that in some cases managers have used the

freedoms within their mandates to make significant

alterations to the composition of their portfolios.

We suggest investors:

Check your definition of dynamic matches that of

your manager(s)

Understand how “dynamic” your manager’s

allocation has been based on the manager’s

definition and, crucially, why (there may be a

good reason for a static allocation)

How comfortable are you with how active the manager

has been in changing the allocation and their explanation

for this?

Multi Asset Study 12

Capturing opportunitiesMany multi-asset managers have the freedom to invest

across a plethora of asset classes ranging from traditional

assets, like listed equities and bonds, to very niche investment

ideas. Across the 25 providers surveyed, over 250 distinct

asset class names and labels were cited by the managers.

Often, this leads to an assumption that the managers will make use of this freedom to

change the composition of the portfolio frequently as opportunities arise. For many

investors, this expectation that the manager will be able to move quickly to capture

opportunities is a key reason for investing in a multi-asset portfolio, as most trustee

boards believe they do not have the expertise or time to do this themselves.

As the chart on page 5 illustrates, our analysis of how managers generated their returns

showed that there were very few managers where dynamic asset allocation made a

material contribution to performance.

However, perhaps even more importantly, we found it very hard to extract exactly

how dynamic managers are and, crucially, how much that dynamism adds to returns,

from the data provided. In fact, managers themselves were rarely able to answer these

questions. This raises an issue for investors: if you are going to invest in a portfolio that

professes to generate returns primarily through dynamic asset allocation, how do you

monitor this and assess manager performance if they can’t do that?

As investors, when deciding how much to allocate to a fund that

claims to be dynamic, you need to ask yourself the following,

“How comfortable are you with not being able to assess the

contribution this makes to the level of return?” and potentially

taper your allocation accordingly. The reliance on manager

skill – of which dynamic asset allocation is one part – should be

considered at a whole portfolio level.

How comfortable are you, given the make up of the rest of

your portfolio, to accept that the value of this element

cannot be assessed?

How much of the manager’s performance is attributable

to manager skill?

How dynamic does the manager claim to be?

Can they offer recent examples of dynamic trades?

How good at it are they? Can they provide a list of

short-term trades that have done well or badly

Multi Asset Study 13

A key takeaway from the last two sections is that

once you understand the nature of your multi-

asset investment, there aren’t too many surprises

with regard to how each of the providers’ returns

have been generated, at least relative to their

peers. From this, you can extrapolate how your

chosen fund might be expected to perform in

different economic scenarios.

This is crucial in assessing their continued

and ongoing value within a portfolio. Poor

performance by itself is rarely a good reason for

changing investments, but poor performance

relative to expectations, can be a leading indicator

of difficulties ahead.

Key Takeaway

Multi Asset Study 14

Across the multi-asset portfolios surveyed, the average allocation to assets with less than

annual liquidity was less than 3% in the years 2014-2019. However there was significant

variation between managers, with the maximum allocation to these assets being 31%

and the minimum 0%.

Illiquidity in multi-asset portfoliosThe final question we address is the extent to which multi-asset

portfolios generate returns through an illiquidity premium.

The vast majority of our clients, DB and DC pension funds,

endowments and charities, have a long time horizon and can

therefore allocate assets to illiquid investments. Do multi-asset

portfolios provide an effective way to access such investments?

Do such funds have a meaningful exposure? How much has this

contributed to returns?

As shown by the chart to the right, multi-asset managers

generate only a very small amount of their returns from the

illiquidity premium. In fact, only 3 managers across the 25

managers we surveyed generated more than 5% of their returns

through an illiquidity premium.

The lesson for investors here is, if you believe in the illiquidity

premium and want to access it, you should not assume a single

multi-asset portfolio will do this for you. Instead, you may need

to consider a specific allocation to illiquid assets. This may be

through a specialist fund or, if you are pursuing the fiduciary

route, ensuring this is built into scheme-specific mandate

parameters, which is likely to be outside their core offering.

There isn’t necessarily a single off-the-shelf solution. This is vital

for an investor tasked with building an investment portfolio.

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

LIQUIDITY IN CORE MULTI-ASSET PORTFOLIOS

2014 2015 2016 2017 2018 2019

>3 year lock-up

>1-3 year lock-up Quarterly

Annual Monthly

Weekly

Multi Asset Study 15

Performance versus

targets versus expectations

In the early days of diversified growth funds, many investors invested on

the understanding that these funds would generate equity-like returns

with significantly lower volatility. Given the runaway performance of

equities in what was the longest equity bull-run in recent history, this

expectation left many investors disappointed with their multi-asset

allocations over the decade to 31 December 2019. But how has the

performance of these funds compared to their actual stated targets?

The chart to the left illustrates the returns produced by a range of DGFs

and FM growth portfolios over the five years to the end of 2019,

highlighting whether they have out, or underperformed their

individually stated targets.

Why does this matter? Whilst this may not do much to ease the

frustrations of investors that have missed out on equity-like performance

over the last five years, it should help investors assessing whether there

continues to be a role for multi-asset investments going forward. We take

from this that these portfolios are not a replacement for equities – and

will not keep pace with equities when equities are outperforming almost

everybody’s expectations but, on the whole, you should expect them to

meet their stated targets. Once again, the key is to know what to expect

from your multi-asset allocation – both in terms of the level of return and

how they will generate it – so that there are no surprises.

0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

Outperforming (against individually stated benchmark)

Absolute return (5 yrs to 31 December 2019), % p.a.

Underperforming (against individually stated benchmark)

Benchmark performance

Effective date 31 December 2019. 24 of 25 managers surveyed provided

sufficient data for inclusion in this section.

Multi Asset Study 15

By using this new framework to analyse how multi-

asset managers have generated returns, we are able

to draw the following conclusions.

We encourage investors to apply this framework in

assessing the how their multi-asset managers fit into

their overall strategy and whether their managers are

successfully fulfilling that role.

Conclusion

Multi-asset investing has a place but investors should

understand how a manager generates returns and establish

their expectations around that. Whilst they, may all carry one

label, there is a significant variation in how the managers

generate returns. Managers rarely deviate from their chosen

style. Therefore, when selecting a manager you, the investor,

are choosing your sources of returns.

01

There is not one style that is likely to systematically

outperform. By understanding the return drivers underlying

the manager’s portfolios, investors will understand when

the managers can be expected to perform well and when

the fund may encounter problems. Be patient and don’t be

surprised when managers then perform in line with

these expectations.

02

Whichever options you chose, it is unlikely to provide you

with meaningful exposure to the illiquidity premium. If you

believe that this is something that can add value, you

need to get it elsewhere.

03

Multi Asset Study 16

Multi Asset Study 17Multi Asset Study 17

We found that only a few multi-asset managers were

able to quantify the value added through dynamic

asset allocation. Where responses were received, the

methodology also varied between providers.

In our next paper, we explore the challenges of

assessing this type of skill, particularly in trying to

compare multi-asset strategies which operate in

fundamentally different ways.

What’s next

03

Please contact your Barnett Waddingham consultant if you would like to discuss any of the above topics in more detail.

Alternatively get in touch via the following:

[email protected] 0333 11 11 222

www.barnett-waddingham.co.uk

Barnett Waddingham LLP is a body corporate with members to whom we refer as “partners”. A list of members can be inspected at the registered office. Barnett Waddingham LLP (OC307678), BW SIPP LLP (OC322417), and Barnett Waddingham Actuaries and Consultants Limited (06498431) are registered in England and Wales with their registered office at 2 London Wall Place, London, EC2Y 5AU. Barnett Waddingham LLP is authorised and regulated by the Financial Conduct Authority. BW SIPP LLP is authorised and regulated by the Financial Conduct Authority. Barnett Waddingham Actuaries and Consultants Limited is licensed by the Institute and Faculty of Actuaries in respect of a range of investment business activities.

Multi Asset Study 186007245

SARAH LOCHLUNDPrincipal and Senior

Investment Consultant

DAN WOODER Associate and Investment Consultant