mutual of america 2011 annual report -...

TRANSCRIPT

3

Mu

tu

AL

of

AM

er

ICA

2011 a

nn

ua

l repo

rt MutuAL of AMerICA 2 01 1 a n n ua l r eport

Table of Contents

Letter from the Chairman,

President and Chief Executive Officer 2

Featured Clients 6

Board of Directors 26

Financial and Corporate Information 29

*While these ratings do not apply to the safety or investment performance of the Separate Account investment alternatives available under Mutual of

America’s products, they do reflect Mutual of America’s ability to fulfill its General Account obligations, which include its obligations under the Interest

Accumulation Account, annuity purchase rate guarantees and annuity benefit payouts, as well as life insurance and disability income payments. Third-

party ratings are subject to change. For the complete reports, please visit mutualofamerica.com/ratings.

A+ (Superior) A.M. BeSt (as of February 2011)*“The rating reflects Mutual of America Life Insurance Company’s prominent market position in the small to medium-size not-for-profit annuity and pension sectors, conservative investment management approach, strong absolute and risk-adjusted capitalization, and strong asset/liability management.”

AA– (Very Strong) StAndArd & Poor’S® (as of October 2011)*“Mutual of America’s salaried sales force, based in regional field offices strategically located in major cities across the country, focuses on building long-term relationships with its customer base. ... We believe cultivating and maintaining these strong relationships, while requiring higher levels of investment, continues to differentiate Mutual of America through high-touch customer service.”

AA– (Very Strong) fitch (as of November 2011)* “Mutual of America’s rating continues to be based on the company’s extremely strong balance sheet fundamentals.”

2011 Selected Financial Data

December 31 ($ in Millions) 2011 2010 % Change

Premiums* 1,552.8 1,674.9 (7.3)%

Net Income 46.5 16.8 176.8

General Account Assets 7,604.6 7,190.4 5.8

Separate Account Assets 5,899.9 6,471.4 (8.8)

Total Assets 13,504.5 13,661.8 (1.2)

Total Surplus (including Asset Valuation Reserve) 895.5 872.9 2.6

Surplus Ratio** 11.8% 12.1%

mutual oF america

* Decline primarily due to 2010’s results including approximately $100 million from the one-time successful

acquisition of five very large Thrift plans.

** Total Surplus as a percentage of General Account Assets

Here and around the world, 2011 was a year of tremendous economic uncertainty and market volatility. The global economy is still grappling with the aftereffects of the investment and lending practices that led to the financial crisis of 2008. While there have been hints recently of a slow economic recovery at home, the future remains uncertain for the millions of Americans who have lost their jobs and their homes over the last three years.

Mutual of America has served the retirement savings needs of Americans for over 65 years during all kinds of economic markets and cycles. Our prudent, long-term approach to investing and managing our Company has prepared us to weather the recent economic turbulence successfully. When global markets experienced extreme volatility following Standard & Poor’s® downgrade of the United

Letter from Thomas J. Moran

Chairman, President and

Chief Executive Officer

States’ long-term credit rating in August, Mutual of America was once again well served by our high quality portfolio and very strong surplus position. At the close of 2011, our total surplus stands at $895.5 million, and our surplus ratio is over 11%—clear measures of our ongoing ability to meet our obligations to our customers.

The strong ratings we again received from the major independent rating agencies in 2011 reflect the financial strength of Mutual of America’s General Account and the Company’s prudent General Account investment policies.1 Our General Account investment strategy of maintaining high quality assets with excellent liquidity, strong capital adequacy and a proper matching of assets and liabilities places Mutual of America among the strongest of all life insurance companies in the United States today. Both Standard & Poor’s® and Fitch Ratings affirmed

Mutual of America’s AA- (Very Strong) rating and have a stable outlook on the Company. In addition, A.M. Best affirmed our financial strength rating of A+.

Our financial strength allows us to invest in enhancements to our products and services that offer real value to our customers. Many companies make online service the principal way they do business, cutting staff to improve their bottom line. While we continue to enhance and expand our online capabilities, we have also invested in our onsite services, adding staff in all of our Regional Offices, including Participant Account Representatives to help participants become better informed about saving for retirement.

When markets are as volatile as they have been, it is not uncommon for individuals to respond by

making short-term decisions that can become long-term investment mistakes. Participant Account Representatives meet with employees in groups and one-on-one to help them understand the saving and investment choices available under the retirement plan. These educational efforts, supported by the extensive educational materials we make available online and in print, help our customers understand how to create a retirement savings strategy that reflects their goals and time horizon, rather than simply reacting to short-term market fluctuations.

As you will read in this Annual Report, our customers are extraordinarily pleased with the onsite, individual service our representatives provide at both the plan administrator and participant level. Employers understand that it’s not enough to provide a retirement plan; their

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 3

Total Assets (In Billions)

General Account Separate Account

2010

$7.191 $6.471 $13.662

2011

$7.605 $5.899 $13.504

good of society. These are Mutual of America’s founding values—the spirit of America that we celebrate and embrace.

Each of us is responsible for helping to create a better future. I have complete confidence in America’s values and strength—not just to set right our economy, but to keep our commitment to future generations. At Mutual of America, we will continue to do our part to help ensure that Americans are financially prepared for the future.

Thomas J. MoranChairman, President and

Chief Executive Officer

employees need sound investment choices and investment education to make well-informed decisions for their financial future. Employers and employees alike continue to put their trust in us, confident in our long history of stability, prudence and commitment to their well-being.

This year has been a time for reflection as we marked the 10th anniversary of the 9/11 attack. We will always remember September 11, 2001, as a time of sorrow overcome by the love we have for our country. 2011 has also been a year of great challenges. While some have focused on the divisions within our society, I see much that unites us. This country remains unique in the hope and opportunity it offers its people and for the values we share—service, strength, leadership and innovation, trust and a willingness to care and work for the greater

“Individuals need sound investment choices and investment education to make well-informed decisions for their financial future.”

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 5

Brian Severin

Senior Field Vice President

Mutual of America

Los Angeles Regional Office

Gus Valdespino

President and CEO

Valley Presbyterian Hospital

Van Nuys, California

“Mutual of America has been a phenomenal partner for us.”

In these challenging economic times, employers who can help their employees’ efforts to achieve a more secure financial footing and to build towards a solid retirement will see greater job satisfaction, dedication and loyalty—the building blocks of successful organizations.

“Mutual of America has been a phenomenal partner for us—it’s almost as if their representatives have become an extension of our human resource department,” says Gus Valdespino, President and CEO of Valley Presbyterian Hospital in Van Nuys, C.A. “They’ve met with every employee—not just in groups, but individually—to explain the features of the retirement plan and the importance of contributing. As a result of their efforts, there’s a lot more confidence in the retirement plan and in the administration; participation has spiked; morale is through the roof. From a satisfied, confident group of employees, I get a more satisfied patient at the hospital.”

Mutual of America’s teams of trained, salaried representatives work within reach of all of our customers, providing the personal, one-on-one service that distinguishes our Company. Our Participant Account Representatives,

serviceGus Valdespino and Brian Severin

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 7

working from each of our 36 Regional Offices, educate individuals about the importance of financial preparedness and help them take steps to achieve it. They meet with employees in groups and individually to answer their questions, walk them through the enrollment process and provide the information that will help them devise a savings strategy tailored to their particular goals and circumstances. And when those goals and circumstances change, we’re there to educate them on how to best achieve their future financial security.

Our onsite approach to education provides opportunities for learning for employees from all levels and backgrounds within an organization— from younger workers who are looking to become more financially literate, to individuals who are ready to make decisions about their life in retirement.

Our representatives help employees make lasting changes in the way they manage their finances, giving rise to a greater sense of personal and financial well-being. By offering our quality retirement products, with their carefully chosen and competitive investment alternatives, online financial tools and individual support, organizations demonstrate their commitment to their employees’ future, helping to build and retain a dedicated, energized group of employees.

“ They’ve met with every employee—not just in groups, but individually.”

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 8

“Brian always has a good story to put everyone at ease.” —Gus

James Fergusson

Senior Field Vice President

Mutual of America

Southfield Regional Office

Karen Schrock, M.S.

President and CEO

Adult Well-Being Services

Detroit, Michigan

“These are challenging times to run a nonprofit.”

Many Americans wouldn’t be saving at all if it weren’t for their workplace retirement plans. Yet when individuals are focused on meeting daily expenses, they often neglect to plan for their future. Mutual of America works closely with employers to ensure they have a plan in place that meets the needs of their organization and their employees.

“These are challenging times to run a nonprofit,” says Karen Schrock, executive director of Adult Well-Being Services (AWBS) in Detroit, Michigan. “Detroit has been hit hard by the collapse of both the auto industry and the housing market. Cutbacks in government spending have had a big effect. I’m constantly on the road negotiating contracts for our organization. I rely on Mutual of America’s remarkable service to help me improve our employees’ chances to achieve financial security in these insecure times.”

AWBS relied on Mutual of America to help increase enrollment in its plan and encourage employees to save. Our team of local representatives met with AWBS employees at their ten locations

leadershipKaren Schrock and James Fergusson

M u t u a l o f a M e r i c a 2 0 1 1 a n n u a l r e p o r t • p a g e 1 1

throughout Detroit to explain the provisions of the plan, the advantages of tax-deferred investing and the interest and investment options available to them. As a result, participation rose from 50% to 90%.

In addition to helping with employee enrollment, our representatives provide comprehensive administrative support to help employers meet their fiduciary responsibilities and keep their plans in compliance with ever-changing government regulations. Our comprehensive plan services eliminate the need for third-party administrators and include the preparation of plan documents, online recordkeeping, communications and educational materials, and an online Form 5500 and nondiscrimination testing platform for certain plans. We also work extensively with 403(b) clients to provide them with information they need to successfully comply with new audit requirements.

The plans we offer are competitively priced. And, unlike many of our competitors, we don’t charge start-up fees, conversion fees, commissions or any surrender or withdrawal fees.2 For small and mid-size organizations, our exceptional personal service and competitive fees are invaluable, allowing employers to focus on their mission while doing all they can to help their employees save for retirement.

“ I rely on Mutual of America’s remarkable service to help me improve our employees’ chances to achieve financial security in these insecure times.”

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 1 2

“I really enjoy my time with Jay. He cares about our people.” —Karen

Melisa Beauchesne

Participant Account Representative

Mutual of America

Rochester Regional Office

Chris Greene

Eastern Market Manager

Ray Sands Glass

Rochester, New York

“I worry about losing money in the market.”

The market volatility of the last few years has scared many individuals away from investing—particularly younger employees, who are building careers in one of the rockiest economic environments our country has ever known. “I have family members delaying retirement because of the hit their retirement savings took recently,” says Chris Greene, sales manager at Ray Sands Glass in Rochester, N.Y. “I worry about losing money in the market. I don’t want to work till I’m 70.”

Chris’s fears are understandable. But at 35, shying away from equity investments may be as risky in the long term as investing too aggressively may be for someone nearing retirement.

From our prudent investment philosophy to our dedication to personal service, our mission is to help individuals like Chris devise a strategy to build and preserve assets for a financially secure future. Our group annuity contracts make available an Interest Accumulation Account, as well as 35 Separate Account investment funds that offer suitable choices for individuals of every age and risk tolerance level—whether they prefer to actively manage their retirement plan portfolio or to take a less active role by choosing investment alternatives managed by an investment professional.

We favor funds that offer consistent performance over the long term as the most appropriate way for individuals to build their retirement savings.

trustChris Greene and Melisa Beauchesne

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 1 5

Each of our investment funds is carefully screened and consistently monitored to ensure that it does not bear such a high degree of risk that it is unsuitable for retirement investing.

Participants who prefer not to construct their own mix of investments can select our target-date Retirement Funds, Allocation Funds and several other balanced funds. Those who wish to avoid market risk entirely can opt for the Interest Accumulation Account of our General Account, which credits a specified, competitive rate of interest along with a guarantee of principal.3

The range and quality of our investment offerings and our emphasis on personal service go hand in hand. All of the investment options available through our products offer opportunities for growth, but there is no one-size-fits-all approach to financing one’s future. That’s why it’s so valuable to have a trusted Mutual of America representative to help explain these options, particularly when markets are volatile.

Luckily, Chris can turn to Melisa Beauchesne, our Participant Account Representative in Rochester, New York, who is helping him become a more confident, secure and disciplined investor. “It’s good to know I can ask Melisa for the five-minute rundown—‘What’s happening now? Am I still on track?’ I have another account I’m rolling into Mutual of America. The other company sends me material, but I never read it. With Melisa, I have someone I can go to and get answers to my questions.”

“ I don’t know much about investing, so it’s good to know I can ask Melisa for the five-minute rundown.”

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 1 6

“I have a lot of confidence in Mutual of America.” —Chris

Lea Starr

Associate Account Executive

Mutual of America

Dallas Regional Office

Kelley Kim

Senior Accountant

The Gibraltar Group, Inc.

Dallas, Texas

“I love Mutual’s website.”

With individuals increasingly responsible for making their own investment decisions for retirement, financial literacy is critical. Our website gives individuals the tools to learn about investing and effortlessly manage their retirement accounts whenever they find the time. For busy parents with full-time jobs, like Kelley Kim, that might be at midnight.

“I like to do research on my own,” says Kelley Kim, an accountant at Gibraltar Group. “I love Mutual’s website; I can go online anytime and check how the market is doing, how my investments are doing and change my investments if I want to. And when I have questions, I can call Lea and get answers.”

Our customers appreciate the clearly displayed account information and easy navigation that mutualofamerica.com affords. They can go online to transfer assets and change their allocations; learn about the objectives of the funds available through our annuity contracts; track fund performance over 1-, 3-, 5- and 10-year periods; check their personal rate of return and year-to-date contributions as well as estimate their future financial needs with our online calculators.

innovationKelley Kim and Lea Starr

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 1 9

For plans that permit their participants to take loans, participants can apply for a loan online and monitor payment activity at their convenience. Those who wish to save more, or transfer or roll over assets from another plan, can apply online for a Mutual of America IRA, including our new Inherited IRA. Also new this year, participants can schedule automatic contributions to an IRA or FPA from external accounts.

Studies show that financial literacy has an important effect on financial preparedness in retirement.4 Our website is one part of our comprehensive approach to education, which takes into account individual preferences in the ways people want their information and frame their choices. We’re helping individuals take control of their personal finances to ensure they’re prepared for retirement.

“I’ve seen from my parents what it means to retire without any savings, so I make saving for retirement my first priority,” says Kelley. “I’m very far from having enough saved. But I know what to do and how to do it. With Mutual of America, I have a plan and a way to get there.”

“ I can go online anytime and check how the market is doing, how my investments are doing and change my investments if I want to.”

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 2 0

“With Mutual of America, I have a plan and a way to get there.” —Kelley

the nation

al 9.11 f lag

Mutual of America’s founding mission to provide retirement plan services to nonprofit organizations has always been a source of pride for us. In helping people who dedicate their lives to helping others, we see ourselves as part of a tradition of service, responsibility and caring that makes our country strong.

Our commitment to nonprofits goes beyond providing quality retirement plans. In 2011, virtually every Mutual of America employee participated in charitable events and voluntary giving, both individually and with coworkers in bike-a-thons, marathons, bake sales and toy drives. The Company supports their efforts through matching contributions, grants and gifts to hundreds of charitable organizations.

Since 1996, the Mutual of America Community Partnership Award has honored the contributions that nonprofit organizations, in partnership with public, private and other social sector organizations, make to society. In 2011 and hereafter, the award bestowed on the national award winner will be named the Governor Hugh L. Carey Award, in honor of the late governor of New York, a long-standing member of the Mutual of America Foundation Community Partnership Award Selection Committee, who helped guide the selection of Community Partnership Award recipients.

caringCommunity Building

The winner of the 2011 Governor Hugh L. Carey Award is College Possible, a highly successful partnership in Minnesota that helps economically disadvantaged high school students navigate the college admissions process and continues to work with them in college. In addition, nine other remarkable partnerships were honored for their outstanding service to their communities.

A strong democracy is built on the open exchange of ideas. To that end, we continue to support the award-winning weekly Public Broadcasting System (PBS) series Religion and Ethics Newsweekly, as well as the PBS newsmagazine Need to Know.

Service to our customers and to the larger community in which we live are the values that have kept our Company strong since our founding in 1945 and continue to guide us going forward. Mutual of America’s advertising campaign, The Spirit of America, reflects our country’s proud heritage and our commitment to do our utmost to help Americans achieve a financially secure future.

Destroyed in the

aftermath of the World

Trade Center attacks

on September 11, The

National 9/11 flag is a

testament to service,

sacrifice and our

country’s ability to

overcome historic

challenges by working

together. With the

support of Mutual of

America and other

companies and

individuals, The

National 9/11 flag has

travelled across

America, where local

service heroes stitched

it back to its original

13-stripe format, using

pieces of retired

American flags from all

50 states. At each stop

on its journey, the

flag has brought

communities together

to pay tribute to our

military veterans, first

responders, educators,

volunteer service

leaders and those who

lost loved ones on 9/11.

The National 9/11 flag

will become a part of

the permanent

collection of the

National September 11

Memorial Museum

being built at the

World Trade Center.

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 2 5

thomas J. moranChairman, President and Chief Executive Officer Mutual of AmericaNew York, New York

elie WieselAndrew W. Mellon Professor in the Humanities Boston University Boston, Massachusetts

Founder, The Elie Wiesel Foundation for Humanity; Nobel Laureate New York, New York

roselyn P. epps, m.D.Medical and Public Health Consultant Washington, D.C.

robert J. mcGuire,

esq.CounselNew York, New York

roger B. Porter,

Ph.D.IBM Professor of Business and Government Harvard UniversityCambridge, Massachusetts

General

Dennis J. reimerU.S. Army (Retired);National Security ConsultantArlington, Virginia

Peter J. PowersChairman and Chief Executive Officer Powers Global Strategies, LLCNew York, New York

Senator

connie mackPartner Liberty Partners Group Washington, D.C.

Chairman Emeritus H. Lee Moffitt Cancer Center & Research InstituteTampa, Florida

earle H. Harbison, Jr.Chairman Harbison Corporation St. Louis, Missouri

Kimberly casianoPresident Kimberly Casiano & Associates Inc.San Juan, Puerto Rico

clifford l.

alexander, Jr.President Alexander & Associates, Inc. Washington, D.C.

John r. GreedSenior Executive Vice President and Chief Financial OfficerMutual of AmericaNew York, New York

Mutual of AmericaBoard of Directors

laSalle D. leffall,

Jr., m.D.Charles R. Drew Professor of Surgery Howard University College of Medicine Washington, D.C.

Frances r. HesselbeinPresident and Chief Executive Officer The Frances Hesselbein Leadership Institute New York, New York

maurine a. HaverPresident Haver Analytics, Inc.New York, New York

Patrick a. BurnsConsultant to the Board of Mutual of AmericaBronxville, New York

Election of Directors

Mutual of America policyholders and contract holders are entitled to participate in the election of Directors. The election is held each year on a designated working day in April. In 2012 the election of Directors is scheduled for Thursday, April 26, 2012, between 10:00 a.m. and 4:00 p.m., at the Home Office, 320 Park Avenue, New York, NY 10022. At each election, approximately one-third of the Directors are elected for terms of three years.

Each policyholder and contract holder whose policy or contract has been in force for one year prior to the date of election is entitled to one vote per person to be cast in person, by mail or by proxy. Pursuant to Section 4210 of the New York Insurance Law, groups of policyholders or contract holders have the right to nominate one or more independent tickets not less than five months prior to the date of each election. Mail ballots may be obtained by writing to the Corporate Secretary at Mutual of America’s Home Office address, no later than 60 days prior to the date of election.

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 2 7

mutual oF america caPital manaGement

corPoration

Mutual of AmericaBoards of Directors

amir learChairman and Chief Executive Officer Mutual of America Capital Management Corp. New York, New York

theresa a. BischoffChief Executive Officer (Past) American Red Cross in Greater New York New York, New York

noreen culhaneExecutive Vice President (Past) New York Stock Exchange New York, New York

robert X. chandlerDevelopment Director (Past) Archdiocese of Boston Boston, Massachusetts

nathaniel a. DavisManaging Director RANND Advisors Oakton, Virginia

robert c. GoldenExecutive Vice President of Corporate Operations (Past)Prudential Financial, Inc.Newark, New Jersey

christopher c. QuickVice Chairman, Global Wealth and Investment Management (Past) Bank of America New York, New York

James e. QuinnPresident (Past) Tiffany & CompanyNew York, New York

alfred e. Smith iVChairman of the Board (Past) Saint Vincent Catholic Medical CentersNew York, New York

John J. StackChairman and Chief Executive Officer (Past) Ceska Sporitelna Prague, Czech Republic

John r. GreedChairman of the Board President and Chief Executive Officer Mutual of America Investment Corporation and Mutual of America Institutional Funds, Inc.New York, New York

carolyn n. DolanFounding principal and Portfolio ManagerSamson Capital Advisors, Inc. New York, New York

Kevin m. KearneyPartner Wingate, Kearney & Cullen Brooklyn, New York

laSalle D. leffall iiiPresident and Founder, LDL Financial, LLC Washington, D.C.

John W. SibalPresident and Chief Executive Officer Eustis Commercial Mortgage Corporation New Orleans, Louisiana

margaret m. SmythVice President, Finance and Chief Financial Officer (Past) Hamilton Sundstrand Windsor Locks, Connecticut

William e. WhistonChief Financial Officer, Archdiocese of New YorkNew York, New York

Patrick J. Waide, Jr.President (Past), Drucker Foundation New York, New York

mutual oF america inVeStment corPoration

mutual oF america inStitutional FunDS, inc.

Statement by Management 30

Consolidated Statutory Statements of Financial Condition 3 1

Consolidated Statutory Statements of Operations and Surplus 32

Consolidated Statutory Statements of Cash Flows 33

Notes to Consolidated Statutory Financial Statements 34

Report of Independent Registered Public Accounting Firm 54

Officers 55

Regional Offices 57

Financial anD corPorate inFormation

M u T u A l o f A M e R I C A 2 0 1 1 A N N u A l R e P o R T • P A G e 2 9

Statement by management

Management is responsible for the integrity of the accompanying consolidated statutory financial statements. In meeting this responsibility, management maintains systems of internal controls designed to provide reasonable assurance that assets are safeguarded and that transactions are executed in accordance with appropriate authorization and are properly recorded. These systems include an organizational structure that appropriately provides for delegation of authority and division of responsibility, the communication and enforcement of accounting and business policies and procedures and the utilization of an internal audit program that requires responsive action to audit findings.

The accompanying consolidated financial statements have been prepared by management in conformity with statutory accounting principles prescribed or permitted by the New York State Department of Financial Ser-vices. Such practices differ from U.S. generally accepted accounting principles (GAAP).

Since the New York State Department of Financial Services recognizes only statutory accounting practices for determining and reporting financial condition and results of operations of insurance companies, and no consideration is given to GAAP financial information, the accompanying consolidated statutory financial state-ments present the Company’s consolidated financial position and results of operations in conformity with statu-tory accounting practices prescribed or permitted by the New York State Department of Financial Services. The significant variances between such practices and GAAP are described in Note 9 to the consolidated statutory financial statements, which is included on pages 52-53.

The accompanying consolidated statutory financial statements for the years ending December 31, 2011 and 2010 have been audited by KPMG LLP, and their opinion, which states that the accompanying consolidated statutory financial statements are fairly presented in conformity with accounting practices prescribed or permitted by the New York State Department of Financial Services, is included on page 54. Their audits were performed in accor-dance with the standards of the Public Company Accounting Oversight Board (United States).

The Board of Directors has appointed an Audit Committee composed solely of directors who are not officers or employees. The committee meets regularly with management, the Executive Vice President and Internal Au-ditor and the independent registered public accounting firm to review audit scope and results, the adequacy of internal controls and accounting and financial reporting matters. The Audit Committee also reviews the services performed by the independent registered public accounting firm and related fee arrangements and recommends their appointment to the Board of Directors. The independent registered public accounting firm and the Execu-tive Vice President and Internal Auditor have direct access to the Committee.

M u t u a l o f a M e r i c a 2 0 1 1 a n n u a l r e p o r t • p a g e 3 1

2011 2010

ASSETSGeneral Account assets Bonds and notes $ 6,997,640,298 $ 6,572,702,783 Common stocks 44,784,304 41,444,347 Cash and short-term investments 7,127,969 18,104,455 Guaranteed funds transferable 30,338,989 35,970,904 Mortgage loans 1,262,625 1,773,231 Real estate 253,146,871 255,071,606 Policy loans 101,251,111 96,584,804 Investment income accrued 86,554,296 87,714,814 Deferred federal income taxes 64,330,201 61,500,402 Other assets 18,175,759 19,474,812

Total General Account assets 7,604,612,423 7,190,342,158

Separate Account assets 5,899,846,871 6,471,430,662

TOTAL ASSETS $13,504,459,294 $13,661,772,820

LIABILITIES AND SURPLUSGeneral Account liabilities Insurance and annuity reserves $ 6,434,183,841 $ 6,088,492,384 Other contract holders liabilities and reserves 11,705,941 10,669,244 Interest maintenance reserve 121,021,902 109,488,765 Other liabilities 142,160,266 108,749,682

Total General Account liabilities before asset valuation reserve 6,709,071,950 6,317,400,075

Separate Account reserves and other liabilities 5,899,846,871 6,471,430,662

Total liabilities before asset valuation reserve 12,608,918,821 12,788,830,737

Asset valuation reserve 49,398,157 38,294,357

Total liabilities 12,658,316,978 12,827,125,094

SURPLUS Assigned surplus 1,150,000 1,150,000 Unassigned surplus 844,992,316 833,497,726

Total surplus 846,142,316 834,647,726

TOTAL LIABILITIES AND SURPLUS $13,504,459,294 $13,661,772,820

See accompanying notes to consolidated statutory financial statements.

COnSOLIDateD StatUtORy StatementS OF FInanCIaL COnDItIOn

December 31, 2011 and 2010

COnSOLIDateD StatUtORy StatementS OF OPeRatIOnS anD SURPLUS

For the years ended December 31, 2011 and 2010

2011 2010

INCOME Premium and annuity considerations $1,538,892,743 $1,661,747,896 Life and disability insurance premiums 13,886,053 13,146,574

Total considerations and premiums 1,552,778,796 1,674,894,470

Separate Account investment and administrative fees 65,094,291 53,150,823 Net investment income 377,268,689 375,784,317 Other, net 6,246,114 7,275,271

Total income 2,001,387,890 2,111,104,881

DEDUCTIONS Change in insurance annuity reserves (89,458,988) 399,572,896 Annuity and surrender benefits 1,800,587,572 1,448,781,003 Death and disability benefits 10,712,145 12,315,225 Operating expenses 233,615,612 233,793,473

Total deductions 1,955,456,341 2,094,462,597

Net gain before dividends 45,931,549 16,642,284

Dividends to contract holders and policyholders (63,478) (143,091)

Net gain from operations 45,868,071 16,499,193

Federal income tax (expense) (3,588,525) (623,249)

Net realized capital gains 4,180,014 876,550

Net income 46,459,560 16,752,494

Surplus Transactions Change in: Asset valuation reserve (11,103,800) 1,701,164 Unrealized capital (losses), net (6,332,697) (4,890,964) Non-admitted assets and other, net 14,903,373 11,859,376 Minimum pension liability (38,169,000) 4,601,000 Net deferred income tax asset 2,348,842 2,954,915 Incremental increase in net deferred income tax asset 3,388,312 4,764,918

Net change in surplus 11,494,590 37,742,903 Surplus Beginning of year 834,647,726 796,904,823

End of year $ 846,142,316 $ 834,647,726

See accompanying notes to consolidated statutory financial statements.

M u t u a l o f a M e r i c a 2 0 1 1 a n n u a l r e p o r t • p a g e 3 3

COnSOLIDateD StatUtORy StatementS OF CaSH FLOWS

For the years ended December 31, 2011 and 2010

2011 2010

CASH FLOWS FROM OPERATIONS Premium and other income collected $ 1,552,787,943 $ 1,674,909,131 Net investment income 370,030,699 353,598,789 Separate Account investment and administrative fees 70,195,255 53,150,823 Benefit payments (1,814,145,531) (1,469,601,467) Net transfers (to) from separate accounts 462,476,673 (74,254,959) Investment and operating expenses paid (192,926,103) (222,272,452) Other, net — 7,466,620 Dividends paid to policyholders (152,837) (308,858)

Net cash from operations 448,266,099 322,687,627

CASH FLOWS FROM INVESTMENTSProceeds from investments sold, matured or repaid: Bonds 1,887,900,195 2,359,564,118 Common stock 5,974,389 48,843,683 Mortgage loans 510,606 470,320 Real estate 8,643,974 8,481,638 Other invested assets 5,631,915 5,652,805 Other 2,033,693 2,014,554

Total 1,910,694,772 2,425,027,118

Costs of investment acquired: Bonds (2,314,295,326) (2,638,243,543) Common stock (6,468,153) (1,876,746) Real estate (6,719,237) (3,990,940) Other - (2,591,494)

Total (2,327,482,716) (2,646,702,723)

Net change in policy loans (4,669,206) (5,177,650)

Net cash used in investment activity (421,457,150) (226,853,255)

CASH FLOW FROM FINANCING AND OTHER SOURCES Net withdrawals on deposit-type contracts (41,144,669) (101,428,940) Other cash applied 3,359,234 8,294,304

Net cash applied from financing and others sources (37,785,435) (93,134,636)

Net change in cash, cash equivalents and short-term investments (10,976,486) 2,699,736

Cash, cash equivalents and short-term investments: Beginning of year 18,104,455 15,404,719

End of year $ 7,127,969 $ 18,104,455

See accompanying notes to consolidated statutory financial statements.

nOteS tO COnSOLIDateD StatUtORy FInanCIaL StatementS

December 31, 2011 and 2010

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

PrinciPles of consolidation

The accompanying financial statements include the consolidated accounts of Mutual of America Life Insurance Company (“Mutual of America”) and its wholly owned subsidiaries (collectively referred to as the “Company”), as permitted by the New York State Department of Financial Services (formerly known as the State of New York Insurance Department). Significant intercompany balances and transactions have been eliminated in consolidation.

nature of oPerations

Mutual of America provides retirement and employee benefit plans in the small to medium-size company mar-ket, principally to employees in the not-for-profit social health and welfare field. In recent years, the Company has expanded to include for-profit organizations in the small to medium-size company market. The insurance company in the group is licensed in all 50 states and the District of Columbia. Sales operations are conducted primarily through a network of regional offices staffed by salaried consultants.

Basis of Presentation

The accompanying financial statements are presented in conformity with statutory accounting practices pre-scribed or permitted by the New York State Department of Financial Services (“New York Department”). Such practices differ from U.S. generally accepted accounting principles (“GAAP”). The significant variances between such practices and GAAP are described in Note 9. The ability of the Company to fulfill its obligations to contract holders and policyholders is of primary concern to insurance regulatory authorities.

The National Association of Insurance Commissioners (“NAIC”) has codified statutory accounting principles (“Codification”). The New York Department issued Regulation No. 172 (“Regulation No. 172”), which adopted Codification, with certain significant modifications, as the prescribed basis of accounting for its domestic insur-ers. Periodically, the New York Department amends Regulation No. 172 for revisions in the prescribed basis of accounting. All changes required by New York Regulation No. 172, as amended through December 31, 2011, are reflected in the accompanying consolidated statutory financial statements.

During 2010, Regulation No. 172 was amended to adopt the accounting change and new disclosure require-ments set forth in Statement of Statutory Accounting Principles No. 100 titled “Fair Value Measurements” (“SSAP No. 100”) under which the criteria used to determine the fair value of certain types of investment securities was changed. As a result of this change, the Company recorded an $11.7 million unrealized loss to adjust the carrying value of four loan-backed securities in its portfolio to their estimated current fair value. These bonds had an adjusted book value of $27.5 million prior to the recognition of this unrealized loss. SSAP No. 100 also established the valuation hierarchy for measuring fair value and established disclosure require-ments about fair value. At December 31, 2011 and 2010, the Company elected to disclose the inputs used to determine fair value for all of its assets that are considered financial instruments and not just those financial instruments required to be reported at fair value in the Statement of Financial Condition as required under SSAP No. 100.

M u t u a l o f a M e r i c a 2 0 1 1 a n n u a l r e p o r t • p a g e 3 5

The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent liabilities at the date of the finan-cial statements, and the reported amounts of income and deductions during the reporting period. Actual results could differ from these estimates.

asset Valuations

Bonds, Notes and Short-Term Investments — Investment valuations are prescribed by the NAIC. Bonds, which include asset-backed and mortgage-backed investments qualifying for amortization, and notes, are stated at amortized cost. Amortization of bond premium or discount is calculated using the constant yield interest method taking into consideration specified interest and principal provisions over the life of the bond. Short-term investments are stated at cost, which approximates fair value, and consist of highly liquid investments purchased with maturities of one year or less. Bond, note and short-term investment transactions are recorded on a trade date basis. The fair value of bonds and notes is based upon quoted market prices provided by an in-dependent pricing organization. If quoted market prices are unavailable or an inactive market for the security currently exists, fair value is estimated using internal valuation models and techniques or based upon quoted market prices for comparable investments. At December 31, 2011, there were five securities with a fair value of $26.9 million for which no quoted market prices were available. As such, the Company used internal valuation models and techniques to determine the fair value of these securities. The Company recorded an unrealized loss of $5.1 million during 2011 to adjust the carrying value of these five securities, which were required to be reported at the lower of amortized cost or fair value, to their current fair value at December 31, 2011. At December 31, 2010, there were several securities with a fair value of $38.2 million that were valued using this methodology. Bonds, where the NAIC rating has fallen to class six and the fair value is below amortized cost, are carried at the lower of amortized cost or fair value.

On December 31, 2011, the rating of one asset-backed security with a book value of $12.0 million was lowered to an NAIC class six, which requires that the security be reported at the lower of amortized cost or fair value. While the results of the valuation testing determined that this security did not have an other than temporary credit impairment, a $7.7 million interest-rate related loss was recorded to adjust this security to its estimated fair value at December 31, 2011 and was accounted for as a realized capital loss charged to the Interest Maintenance Reserve (“IMR”). Given the current inactivity for this security, its fair value was estimated using internal valuation models and techniques.

Losses that are considered to be other than temporary are recognized in net income when incurred. All bonds are subjected to the Company’s quarterly review process for identifying other than temporary impairments. This impairment identification process utilizes a screening procedure that includes all bonds in default or not in good standing, as well as bonds with a fair value that is less than 80% of their cost for a continuous six-month period. The Company writes down bonds that it deems to have an other than temporary impairment after considering a wide range of factors, including, but not limited to, the extent to which cost exceeds fair value, the duration of that market decline, an analysis of the discounted estimated future cash flows for asset-backed and mortgage-backed securities, an analysis of the financial health and specific prospects for the issuer, the likeli-hood that the Company will be able to collect all amounts due according to the contractual terms of the debt security in effect at the date of acquisition, consideration as to whether the decline in value is due to general

nOteS tO COnSOLIDateD StatUtORy FInanCIaL StatementS

December 31, 2011 and 2010

changes in interest rates and credit spreads and the Company’s intent and ability to retain its investment in the issuer for a period of time sufficient to allow for any anticipated recovery in fair value. Effective January 1, 2010, if an impairment is determined to be other than temporary, a realized capital loss equal to the entire difference between the amortized cost of the bond and its fair value is recorded and a new cost basis for the bond is estab-lished. Credit-related other-than-temporary impairment losses are recorded as realized capital losses included in net income (and through the asset valuation reserve), whereas interest-related other-than-temporary impair-ment losses are recorded in the IMR.

Common and Preferred Stocks — At December 31, 2011 and 2010, common stocks include $34.8 million and $34.5 million, respectively, invested in a sponsored series of mutual funds for institutional investors. The Decem-ber 31, 2011 and 2010, amounts also include $3.3 million, in each year, invested in an actively managed Mid-Cap Growth equity portfolio. Common stocks in good standing are stated at fair value. Fair value is determined by reference to valuations quoted by an independent pricing organization. Unrealized gains and losses are recorded directly to unassigned surplus. Preferred stock is carried at cost. During 2010, the preferred stock owned by the Company was called by its issuer and redeemed at par. A loss of $.1 million was recognized on this transaction.

Losses that are considered to be other than temporary are recognized in net income when incurred. All equity investments are subjected to the Company’s quarterly review process for identifying other-than-temporary impairments. This impairment identification process utilizes a screening procedure that includes all common stock issuers not in good standing, as well as common stocks where the fair value is less than 80% of their cost for a continuous six-month period. The Company writes down common stocks that it deems to have an other-than-temporary impairment after considering a wide range of factors, including, but not limited to, the extent to which cost exceeds fair value, the duration of that market decline, an analysis of the financial health and specific prospects for the issuer and the Company’s intent and ability to retain its investment for a period of time sufficient to allow for any anticipated recovery in fair value in the short-term. The Company also considers other qualitative and quantitative factors in its evaluation of other-than-temporary impairments.

Guaranteed Funds Transferable — Guaranteed funds transferable consists of funds held with a former rein-surer and is stated at the total principal amount of future guaranteed transfers to Mutual of America, net of a $1.5 million unrealized loss that was recorded as a direct reduction to unassigned surplus. No additional losses were recorded on this investment during 2011 and 2010.

Mortgage Loans — Mortgage loans are carried at amortized indebtedness. Impairments of individual loans that are considered other than temporary are recognized in net income when incurred. There were no impairment losses incurred during 2011 and 2010.

Real Estate — Real estate, which is classified as Company-occupied property, is carried at cost, including capital improvements, net of accumulated depreciation of $148.8 million and $140.2 million at December 31, 2011 and 2010, respectively, and is depreciated on a straight-line basis over 39 years. Tenant improvements on real estate investments are depreciated over the shorter of the lease term or the estimated life of the improvement.

M u t u a l o f a M e r i c a 2 0 1 1 a n n u a l r e p o r t • p a g e 3 7

Policy Loans — Policy loans are stated at the unpaid principal balance of the loan. There were no losses recog-nized during 2011 and 2010.

Other Assets — Certain other assets, such as net deferred income tax assets not expected to be realized within three years, furniture and fixtures and prepaid expenses, are considered “nonadmitted assets” and are excluded from the consolidated statutory statements of financial condition.

insurance and annuity reserVes

Reserves for annuity contracts are computed on the net single premium method and represent the estimated present value of future retirement benefits. These reserves, which were $.9 billion at both December 31, 2011 and 2010, are based on mortality and interest rate assumptions (ranging predominately from 5.00% to 6.50% at both December 31, 2011 and 2010), which meet or exceed statutory requirements and are not subject to discretionary withdrawal.

Reserves for contractual funds not yet used for the purchase of annuities are accumulated at various credited interest rates that, during 2011 and 2010, averaged 2.50% and 2.90%, respectively, and are deemed sufficient to provide for contractual surrender values for these funds. These reserves, which were $5.4 billion and $5.0 billion at December 31, 2011 and 2010, respectively, are subject to discretionary withdrawal at book value.

Reserves for guaranteed investment contracts, which were $39.2 million and $33.0 million at December 31, 2011 and 2010, respectively, are accumulated at various guaranteed interest rates, which during 2011 and 2010 aver-aged 2.21% and 5.63%, respectively, and meet statutory requirements. Reserves for life and disability insurance are based on mortality, morbidity and interest rate assumptions, which meet statutory requirements.

interest Maintenance and asset Valuation reserVes

Realized gains and losses, including certain other-than-temporary impairment losses, net of applicable taxes, arising from changes in interest rates are accumulated in the IMR and are amortized into net investment in-come over the estimated remaining life of the investment sold. All other realized gains and losses are reported in the consolidated statements of operations.

An Asset Valuation Reserve (“AVR”), applying to the specific risk characteristics of all invested asset catego-ries excluding cash, policy loans and investment income accrued, has been established based on a statutory formula. Realized and unrealized gains and losses, including other-than-temporary impairment losses arising from changes in the creditworthiness of the issuer, are included in the appropriate subcomponent of the AVR. Changes in the AVR are recorded directly to unassigned surplus.

seParate account oPerations

Variable annuity considerations and certain variable life insurance premiums may be allocated at participants’ discretion among investment funds in Separate Accounts. Separate Account funds invest in mutual funds, in-cluding funds managed by Mutual of America Capital Management Corporation, a wholly owned subsidiary (the “Adviser”), and other funds managed by outside investment advisers. All net realized and unrealized capital gains in the Separate Accounts, which reflect investment performance of the mutual funds in which they invest, accrue directly to participants (net of administrative and other Separate Account charges) and are not reflected

nOteS tO COnSOLIDateD StatUtORy FInanCIaL StatementS

December 31, 2011 and 2010

in the Company’s Consolidated Statutory Statements of Operations and Surplus. Certain administrative and other charges are assessed as a percentage of Separate Account assets and vary based upon the average size of the participant’s equity in the Separate Accounts and the level of administrative services provided. In 2011 and 2010, such charges were equal to approximately 1.04% and .91%, respectively, of total average Separate Account assets. Separate Account charges and investment advisory fees paid to the Adviser are included in the Consoli-dated Statutory Statement of Operations and Surplus. Investments held in the Separate Accounts are stated at fair value and are not available to satisfy liabilities of the General Account. Participants’ corresponding equity in the Separate Accounts is reported as liabilities in the accompanying statements. Premiums and benefits re-lated to the Separate Accounts are combined with the General Account in the accompanying statements. Net operating gains and losses are offset by changes to reserve liabilities in the respective Separate Accounts. These reserves, which were approximately $5.9 billion and $6.5 billion at December 31, 2011 and 2010, respectively, are subject to discretionary withdrawal at fair value.

PreMiuMs and annuity considerations

All annuity considerations derived from voluntary retirement-savings-type plans and defined benefit plans, which represents the vast majority of the Company’s annual premiums, are recognized as income when received. In-surance premiums and annuity considerations derived solely from defined contribution plans are recognized as income when due. Group life and disability insurance premiums are recognized as income over the contract period.

inVestMent incoMe and exPenses

General Account investment income is reported as earned and is presented net of related investment expenses. Operating expenses, including acquisition costs for new business, are charged to operations as incurred.

diVidends

Dividends are based on formulas and scales approved by the Board of Directors and are accrued currently for payment subsequent to plan anniversary dates.

Certain 2010 amounts included in the accompanying consolidated statutory financial statements have been reclassified to conform to the 2011 presentation.

2. INVESTMENTS

Valuation

The statement and fair values of investments in fixed maturity securities (bonds and notes) at December 31, 2011 and 2010, are shown on the next page. Excluding U.S. government and government agency investments, the Company is not exposed to any significant concentration of credit risk.

M u t u a l o f a M e r i c a 2 0 1 1 a n n u a l r e p o r t • p a g e 3 9

Statement GrossUnrealized Fair

December31,2011(inmillions) Value Gains Losses Value

Fixed maturities:Mortgage- and asset-backed securities: Residential mortgage-backed securities $2,337.5 $143.9 $ .3 $2,481.1 Commercial mortgage-backed securities — — — — Other asset-backed securities 23.9 .3 .1 24.1 Total $2,361.4 $144.2 $ .4 $2,505.2

U.S. Treasury securities and obligations of U.S. government corporations and agencies 910.8 66.5 — 977.3 Obligations of states and political subdivisions 23.0 3.5 — 26.5 Debt securities issued by foreign governments 34.6 4.7 — 39.3 Corporate securities 3,670.8 235.0 15.0 3,890.8 Total $7,000.6 $453.9 $ 15.4 $7,439.1

Statement GrossUnrealized Fair

December31,2010(inmillions) Value Gains Losses Value

Fixed maturities: Mortgage- and asset-backed securities: Residential mortgage-backed securities $2,519.3 $113.3 $ 8.7 $2,623.9 Commercial mortgage-backed securities 2.5 — — 2.5 Other asset-backed securities 17.3 .2 .1 17.4 Total $2,539.1 $113.5 $ 8.8 $2,643.8

U.S. Treasury securities and obligations of U.S. government corporations and agencies 741.6 23.8 10.5 754.9 Obligations of states and political subdivisions 21.5 .8 — 22.3 Debt securities issued by foreign governments 34.2 4.4 .1 38.5 Corporate securities 3,250.4 202.9 18.1 3,435.2 Total $6,586.8 $345.4 $ 37.5 $6,894.7

The Company does not have any exposure to subprime mortgage loans, either through direct investment in such loans or through investments in residential mortgage-backed securities, collateralized debt obligations or other similar investment vehicles. Approximately 95% of the $2.5 billion invested in mortgage-backed securities were issued by Fannie Mae (“FNMA”), Freddie Mac (“FHLMC”) or Ginnie Mae (“GNMA”) and, as such, are 100% guaranteed by the U.S. government. The Company does have investments in publicly traded bonds of financial institutions. These financial institutions may have investments with subprime exposure. At December 31, 2011, the statement value and fair value of the Company’s bond investments in financial institutions totaled $891.8 million and $927.6 million, respectively. At December 31, 2010, the statement value and fair value of the Company’s bond investments in financial institutions totaled $564.3 and $595.6 million, respectively.

nOteS tO COnSOLIDateD StatUtORy FInanCIaL StatementS

December 31, 2011 and 2010

Short-term fixed maturity securities with a statement value and fair value of $3.0 million and $14.1 million at December 31, 2011 and 2010, respectively, are included in the above tables. At December 31, 2011 and 2010, the Company had $3.3 million (par value $3.4 million), respectively, of its long-term fixed maturity securities on deposit with various state regulatory agencies.

fair Value

The Company values its financial instruments at fair value. Fair value is an estimate of the price the Company would receive upon selling a security in an orderly arms-length transaction. Investments are categorized based on a three-level valuation hierarchy for measurement and disclosure of fair value. The valuation hierarchy is based upon the transparency of inputs used to measure fair value. The three levels are as follows:

Level 1 — quoted prices in active markets for identical securities.Level 2 — quoted prices for identical or similar assets in markets that are not active or other signifi-

cant observable inputs (including yield, quality, coupon rate, maturity, issue type, quoted prices for similar securities, prepayment speeds, trading characteristics, etc.).

Level 3 — significant unobservable inputs (including the assumptions in determining the fair value of investments).

The Company has determined the fair value inputs used to measure all of its assets that are considered financial instruments, which includes fixed maturity securities, common stocks, cash and short-term investments, mort-gage loans, policy loans, other invested assets and Separate Account funds whose net asset values are calculated on a daily basis. Cash, short-term investments, common stocks, investments in publicly traded mutual funds that are registered with the Securities and Exchange Commission and Separate Account assets were deter-mined to be Level 1. The vast majority of the Company’s fixed maturity securities (bonds and notes), and all of its policy loans, other invested assets and private-placement common stock were determined to be Level 2. Finally, certain fixed maturity securities, the guaranteed funds transferrable and mortgage loans representing less than 1% of the total, for which quoted market prices were unavailable or an inactive market for the security currently exists, were determined to be Level 3. The inputs used for valuing these securities are not necessarily an indication of the risk associated with investing in those securities.

The following tables provide fair value information at December 31, 2011 and 2010, about the Company’s assets that are considered financial instruments:

December31,2011FinancialInstrument Level1 Level2 Level3 Total

Bonds and notes $ — $7,409.3 $26.9 $ 7,436.2 Common stocks 42.3 2.5 — 44.8 Cash and short-term investments 7.1 — — 7.1 Guaranteed funds transferrable — — 30.3 30.3 Mortgage loans — — 1.3 1.3 Policy loans — 101.3 — 101.3 Separate Accounts assets 5,899.9 — — 5,899.9 Total $5,949.3 $7,513.1 $58.5 $13,520.9

M u t u a l o f a M e r i c a 2 0 1 1 a n n u a l r e p o r t • p a g e 4 1

December31,2010FinancialInstrument Level1 Level2 Level3 Total

Bonds and notes $ — $6,821.8 $58.8 $ 6,880.6 Common stocks 39.0 2.4 — 41.4Cash and short-term investments 18.1 — — 18.1 Guaranteed funds transferrable — — 36.0 36.0Mortgage loans — — 1.8 1.8 Policy loans — 96.6 — 96.6 Separate Accounts assets 6,471.4 — — 6,471.4 Total $6,528.5 $6,920.8 $96.6 $13,545.9

The book value of Level 3 securities declined from $96.6 million at December 31, 2010, to $58.5 million at De-cember 31, 2011, primarily as a result of the sale of two securities during the year that had an adjusted fair value of $16.6 million and $2.5 million, respectively. The company realized capital gains on these sales of $3.3 million and $2.5 million, respectively, which are included in net income in 2011. Furthermore, as previously discussed in Note 1, one additional security in this group, with an unadjusted book value of $12.0 million was determined to be an NAIC class six at December 31, 2011 and a $7.7 million adjustment to report this security at the lower of amortized cost or fair value was recorded. The fair value of the remaining securities classified as Level 3 decreased by $5.1 million in 2011 as a result of the redetermination of the fair value of these securities during the year. The guaranteed funds transferrable and the mortgage loan asset balances declined due to the receipt of scheduled principal payments during the year. There were no additional securities added to the Level 3 clas-sification during 2011.

In determining the fair value of Level 3 bonds and notes, the Company utilized expected cash flows provided by an independent valuation service together with discount rate and default factor assumptions commensurate with the current credit rating of such securities and consistent with those that would be used in pricing similar types of securities based upon market conditions that existed at December 31, 2011 and 2010.

unrealized Gains and losses

At December 31, 2011 and 2010, net unrealized (depreciation) appreciation reflected in surplus consisted of the following:

December31(inmillions) 2011 2010 Change

Equity securities (common and preferred stock) $ 7.6 $ 8.8 $ (1.2)Bonds and notes (16.8) (11.7) (5.1)Guaranteed funds transferable (1.5) (1.5) — Net unrealized (depreciation) appreciation $(10.7) $(4.4) $(6.3)

nOteS tO COnSOLIDateD StatUtORy FInanCIaL StatementS

December 31, 2011 and 2010

Net unrealized depreciation related to the Company’s bonds and equity securities increased by $6.3 million during the year as shown above. The net unrealized appreciation of $7.6 million related to equity securities at December 31, 2011, consists of $8.0 million of gross unrealized gains and $.4 million of gross unrealized losses, of which none of the unrealized losses are less than 12 months old. The net unrealized appreciation of $8.8 million related to equity securities at December 31, 2010, consisted of $8.9 million of gross unrealized gains and $.1 million of gross unreal-ized losses, of which $.1 million of the unrealized losses were greater than 12 months old.

During 2010, Regulation No. 172 was amended to adopt the accounting change and new disclosure require-ments set forth in SSAP No. 100 titled Fair Value Measurements, under which the criteria used to determine the fair value of certain types of investment securities was changed. As a result of this change in 2010, the Com-pany recorded an $11.7 million unrealized loss to adjust the carrying value of certain loan-backed securities in the portfolio to their estimated current fair value. These securities had an adjusted book value of $27.5 million prior to the recognition of this unrealized loss. At December 31, 2011, an additional unrealized loss of $5.1 mil-lion was recorded to adjust these securities to their estimated fair value. SSAP No. 100 also established the valuation hierarchy for measuring fair value and establishes disclosure requirements about fair value.

The following is an analysis of the fair values and gross unrealized losses as of December 31, 2011 and 2010, aggregated by fixed maturity category and length of time that the securities were in a continuous unrealized loss position. As shown in the table below, total gross unrealized losses as of December 31, 2011 and 2010, were $15.4 million and $37.5 million, respectively and the majority of such losses related to corporate and U.S. Trea-sury securities. These unrealized losses arise primarily from general changes in interest rates and credit spreads, which are still wider than historical norms, despite having narrowed considerably during 2011 and are not due to fundamental credit problems that exist with the specific issuers.

The tables that follow exclude $6.8 billion and $5.7 billion at December 31, 2011 and 2010, respectively, of fair value of fixed maturity securities in an unrealized gain position.

Fair Unrealized Number Fair Unrealized Number Value Losses of Issues Value Losses of IssuesDecember 31, 2011 (in millions) Twelve Months or Less Twelve Months or Greater

Fixed maturities:Mortgage- and asset-backed securities: Residential mortgage-backed securities $ 28.2 $ .2 8 $ 9.1 $ .1 5 Commercial mortgage-backed securities — — — — — — Other asset-backed securities 1.1 — 1 6.4 .1 2 Total $ 29.3 $ .2 9 $ 15.5 $ .2 7

U.S. Treasury securities and obligations of U.S. government corporations and agencies 8.5 — 2 — — —Obligations of states and political subdivisions — — — — — —Debt securities issued by foreign governments — — — — — —Corporate securities 264.5 7.1 29 277.8 7.9 14 Total $302.3 $ 7.3 40 $ 293.3 $ 8.1 21

M u t u a l o f a M e r i c a 2 0 1 1 a n n u a l r e p o r t • p a g e 4 3

Fair Unrealized Number Fair Unrealized Number Value Losses of Issues Value Losses of IssuesDecember 31, 2010 (in millions) Twelve Months or Less Twelve Months or Greater

Fixed maturities:Mortgage- and asset-backed securities: Residential mortgage-backed securities $ 352.6 $ 8.6 34 $ 2.8 $ .1 3 Commercial mortgage-backed securities — — — — — — Other asset-backed securities 3.1 — 1 3.7 .1 2 Total $ 355.7 $ 8.6 35 $ 6.5 $ .2 5

U.S. Treasury securities and obligations of U.S. government corporations and agencies 245.9 10.5 6 — — —Obligations of states and political subdivisions — — — — — —Debt securities issued by foreign governments 2.0 — 1 1.5 .1 1Corporate securities 459.3 13.3 27 152.6 4.8 13 Total $1,062.9 $ 32.4 69 $ 160.6 $ 5.1 19

realized caPital Gains and losses

Net realized capital gains (losses) reflected in the statements of operations for the years ended December 31, 2011 and 2010, were as follows:

December31(inmillions) 2011 2010

Bonds and notes $ 3.3 $ —Equity securities (common and preferred stock) .9 .9 Net realized capital gains (losses) $ 4.2 $ .9

At December 31, 2011 and 2010, the book value and fair value of the Company’s mortgage-backed and asset-backed securities portfolio totaled $2.8 billion and $2.8 billion, and $3.0 billion and $2.9 billion, respectively, of which approximately 95% in both years are U.S. government agency guaranteed instruments. Investments in loan-backed and asset-backed securities are carried at amortized cost, except for those securities rated as class 6 by the NAIC, which are carried at lower of amortized cost or fair value.

Sales of investments in fixed maturity securities resulted in $30.8 million and $49.9 million of net interest rate related gains being accumulated in the IMR in 2011 and 2010, respectively, as follows:

December31(inmillions) 2011 2010

Fixed maturity securities Proceeds $1,971.4 $2,355.5 Gross realized gains 39.7 50.3 Gross realized losses (8.9) (.4)

nOteS tO COnSOLIDateD StatUtORy FInanCIaL StatementS

December 31, 2011 and 2010

During 2011 and 2010, $19.3 million and $16.3 million, respectively, of the IMR was amortized and included in net investment income.

Sales of investments in equity securities resulted in $.9 million of net capital gains in both 2011 and 2010 being recognized in net income as follows:

December31(inmillions) 2011 2010

Equity securities Proceeds $4.9 $35.8 Gross realized gains 1.1 1.0 Gross realized losses (.2) (.1)

Maturities

The statement and fair values of investments in fixed maturity securities by contractual maturity (except for mortgage-backed securities, which are stated at expected maturity) at December 31, 2011, are shown below. Expected maturities may differ from contractual maturities because borrowers may have the right to prepay obligations with or without prepayment penalties.

Statement FairDecember31,2011(inmillions) Value Value

Due in one year or less $ 399.1 $ 406.9Due after one year through five years 2,655.3 2,815.7Due after five years through 10 years 3,294.0 3,513.1Due after 10 years 652.2 703.4 Total $7,000.6 $7,439.1

3. GUARANTEED FUNDS TRANSFERABLE

In 1980, Mutual of America terminated a reinsurance arrangement and assumed direct ownership of funds held by John Hancock Mutual Life Insurance Company (“Hancock”), the former reinsurer, and direct liability for the contractual obligations to policyholders. The liability to such policyholders is included as insurance and annuity reserves in the consolidated statutory statements of financial condition. The principal amount of the funds held by the former reinsurer is guaranteed to earn at least 3.125% per year.

The guaranteed funds are transferable to Mutual of America over time through 2030 and are stated at the total principal amount of future guaranteed transfers to Mutual of America of $30.3 million and $36.0 million at December 31, 2011 and 2010, respectively. The actual interest and other allocated investment earnings related to this contract amounted to $1.5 million and $2.0 million in 2011 and 2010, respectively, and are included in net investment income.

M u t u a l o f a M e r i c a 2 0 1 1 a n n u a l r e p o r t • p a g e 4 5

4. REAL ESTATE

Real estate consists primarily of an office building that Mutual of America purchased for its corporate head-quarters. The Company occupies approximately one-third of this office building as its corporate headquar-ters and leases the remaining space. Depreciation expense was $8.6 million and $8.4 million in 2011 and 2010, respectively.

5. PENSION PLAN AND POSTRETIREMENT BENEFITS

Pension Benefit and other Benefit Plans

The Company has a qualified, noncontributory defined benefit pension plan covering virtually all employees. Benefits are generally based on years of service and final average earnings. The Company’s funding policy is to contribute annually, at a minimum, the amount necessary to satisfy the funding requirements under the Employee Retirement Income Security Act of 1974 (“ERISA”). The Company also maintains a nonqualified defined benefit pension that provides benefits to employees whose total compensation exceeds the maximum allowable compensation limits for qualified retirement plans under ERISA.

The Company has two defined benefit postretirement plans covering substantially all salaried employees. Post-retirement benefit plan expense required to be recorded under this plan was $4.7 million and $3.0 million in 2011 and 2010, respectively. Employees may become eligible for such benefits upon attainment of retirement age while in the employ of the Company and upon satisfaction of service requirements. One plan provides medical and dental benefits and the second plan provides life insurance benefits. The postretirement plans are contributory for those individuals who retire with less than 25 years of eligible service, with retiree contribu-tions adjusted annually, and contain other cost-sharing features, such as deductibles and coinsurance. All benefit plans are underwritten by Mutual of America.

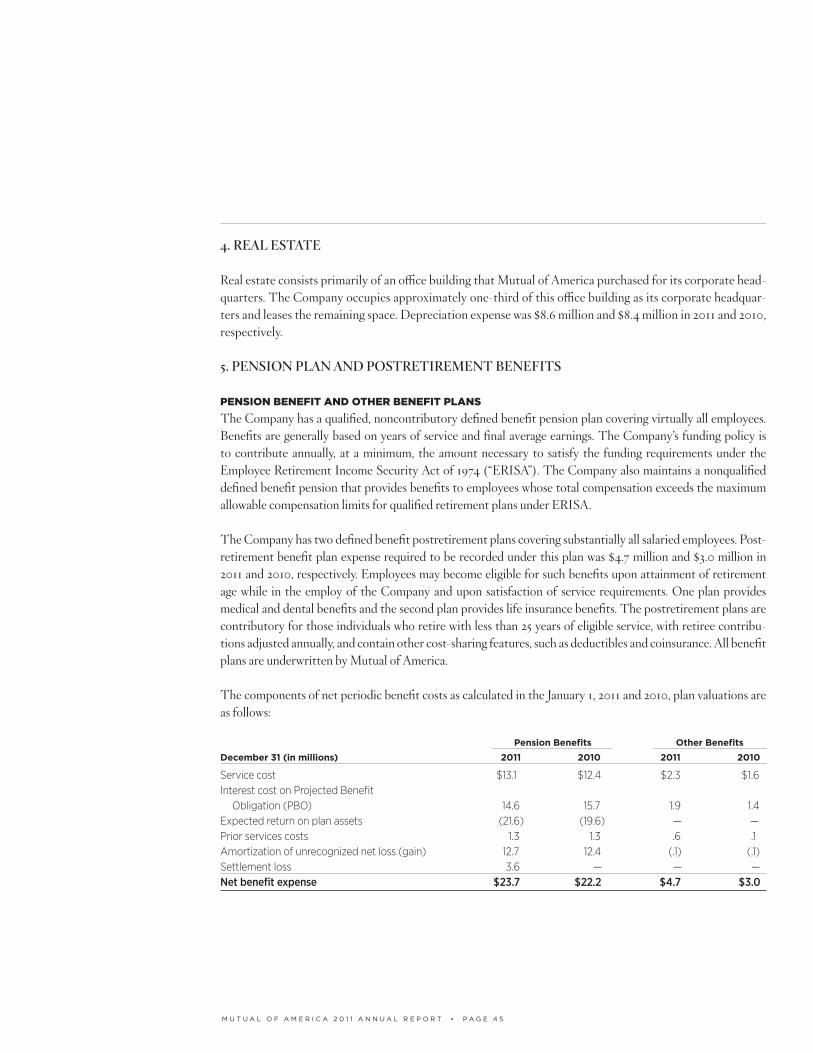

The components of net periodic benefit costs as calculated in the January 1, 2011 and 2010, plan valuations are as follows:

PensionBenefits OtherBenefits

December31(inmillions) 2011 2010 2011 2010

Service cost $ 13.1 $ 12.4 $ 2.3 $ 1.6Interest cost on Projected Benefit Obligation (PBO) 14.6 15.7 1.9 1.4Expected return on plan assets (21.6) (19.6) — —Prior services costs 1.3 1.3 .6 .1Amortization of unrecognized net loss (gain) 12.7 12.4 (.1) (.1)Settlement loss 3.6 — — —Net benefit expense $ 23.7 $ 22.2 $ 4.7 $ 3.0

nOteS tO COnSOLIDateD StatUtORy FInanCIaL StatementS

December 31, 2011 and 2010

During 2011 pension expense included a $3.6 million settlement loss, resulting from the level of lump-sum ben-efit payments made from the nonqualified plan during the year exceeding the plan’s interest and service costs. During 2010, there were no settlement losses recognized.

The changes in the PBO and plan assets are as follows:

PensionBenefits OtherBenefits

December31(inmillions) 2011 2010 2011 2010

Change in PBOPBO, beginning of year $ 292.3 $ 279.9 $ 37.2 $ 25.6 Service cost 13.1 12.4 2.3 1.6 Interest cost 14.6 15.7 1.9 1.4 Plan amendment — — — — Change in assumptions 12.1 10.9 2.6 3.2 Actuarial loss (gain) 11.0 (2.8) 4.0 8.1 Benefits and expenses paid (27.2) (23.8) (3.3) (2.7)PBO, end of year $315.9 $292.3 $44.7 $37.2

PensionBenefits OtherBenefits

December31(inmillions) 2011 2010 2011 2010

Change in Plan Assets Plan assets, beginning of year $ 215.8 $ 199.4 $ — $ — Employer contributions 10.0 13.6 — — Return on plan assets .1 26.6 — — Benefits and expenses paid (27.2) (23.8) — —Plan assets, end of year 198.7 215.8 — —Plan assets (lower than) PBO $(117.2) $ (76.5) $(44.7) $(37.2)

At December 31, 2011 and 2010, all of the pension plan assets are invested in several of the investment funds offered by the Company’s Separate Accounts and in the Company’s General Account, and consisted of ap-proximately 80% in equity investments and 20% in fixed-income investments. A distribution of plan assets by investment objective as of December 31, 2011 and 2010, is as follows:

($inmillions) 2011 2010

Fixed Income Funds $ 30.1 $ 28.7 Equity Funds: Index 88.6 86.6 Growth 25.4 28.3 Balanced 24.1 26.4 Total Level 1 Investments $ 168.2 $ 170.0 General Account 30.5 45.8 Total Plan Assets $198.7 $215.8

M u t u a l o f a M e r i c a 2 0 1 1 a n n u a l r e p o r t • p a g e 4 7

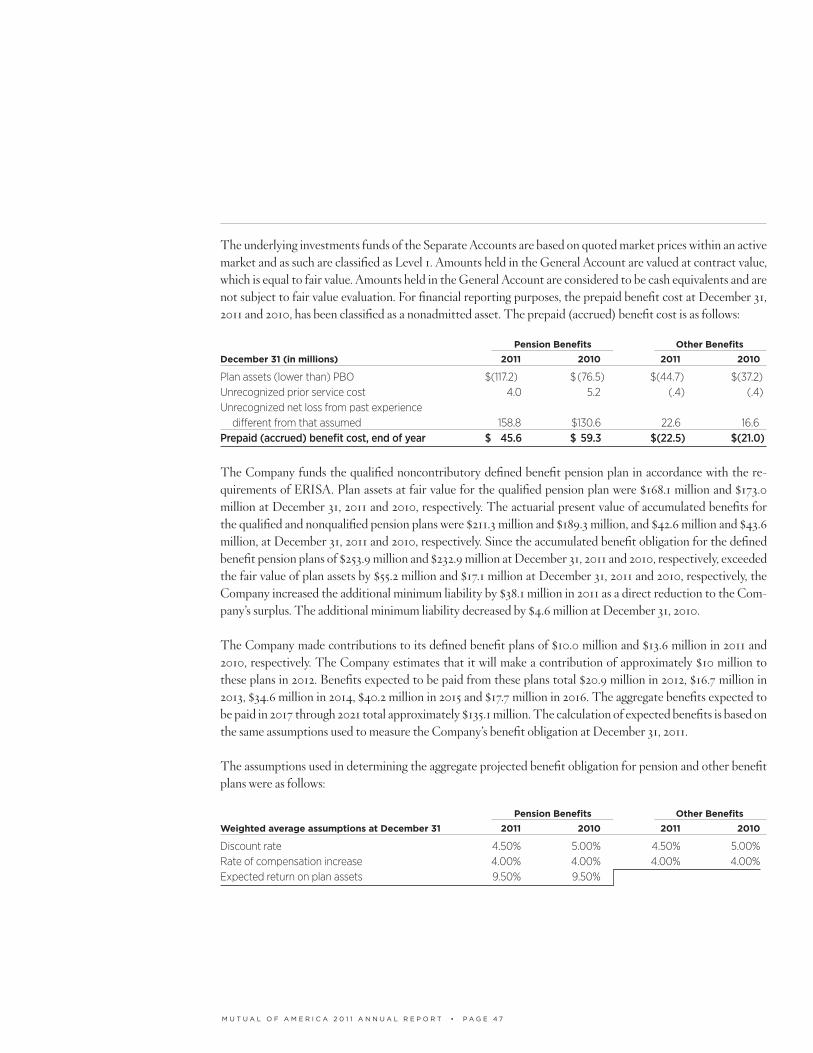

The underlying investments funds of the Separate Accounts are based on quoted market prices within an active market and as such are classified as Level 1. Amounts held in the General Account are valued at contract value, which is equal to fair value. Amounts held in the General Account are considered to be cash equivalents and are not subject to fair value evaluation. For financial reporting purposes, the prepaid benefit cost at December 31, 2011 and 2010, has been classified as a nonadmitted asset. The prepaid (accrued) benefit cost is as follows:

PensionBenefits OtherBenefits

December31(inmillions) 2011 2010 2011 2010

Plan assets (lower than) PBO $(117.2) $ (76.5) $(44.7) $(37.2)Unrecognized prior service cost 4.0 5.2 (.4) (.4)Unrecognized net loss from past experience different from that assumed 158.8 $130.6 22.6 16.6Prepaid (accrued) benefit cost, end of year $ 45.6 $ 59.3 $(22.5) $(21.0)

The Company funds the qualified noncontributory defined benefit pension plan in accordance with the re-quirements of ERISA. Plan assets at fair value for the qualified pension plan were $168.1 million and $173.0 million at December 31, 2011 and 2010, respectively. The actuarial present value of accumulated benefits for the qualified and nonqualified pension plans were $211.3 million and $189.3 million, and $42.6 million and $43.6 million, at December 31, 2011 and 2010, respectively. Since the accumulated benefit obligation for the defined benefit pension plans of $253.9 million and $232.9 million at December 31, 2011 and 2010, respectively, exceeded the fair value of plan assets by $55.2 million and $17.1 million at December 31, 2011 and 2010, respectively, the Company increased the additional minimum liability by $38.1 million in 2011 as a direct reduction to the Com-pany’s surplus. The additional minimum liability decreased by $4.6 million at December 31, 2010.

The Company made contributions to its defined benefit plans of $10.0 million and $13.6 million in 2011 and 2010, respectively. The Company estimates that it will make a contribution of approximately $10 million to these plans in 2012. Benefits expected to be paid from these plans total $20.9 million in 2012, $16.7 million in 2013, $34.6 million in 2014, $40.2 million in 2015 and $17.7 million in 2016. The aggregate benefits expected to be paid in 2017 through 2021 total approximately $135.1 million. The calculation of expected benefits is based on the same assumptions used to measure the Company’s benefit obligation at December 31, 2011.

The assumptions used in determining the aggregate projected benefit obligation for pension and other benefit plans were as follows:

PensionBenefits OtherBenefits

WeightedaverageassumptionsatDecember31 2011 2010 2011 2010

Discount rate 4.50% 5.00% 4.50% 5.00%Rate of compensation increase 4.00% 4.00% 4.00% 4.00%Expected return on plan assets 9.50% 9.50%

nOteS tO COnSOLIDateD StatUtORy FInanCIaL StatementS

December 31, 2011 and 2010

The Company’s overall expected long-term rate of return on plan assets was determined based upon the cur-rent projected benefit payout period and the current mix of plan investments, which generally consists of ap-proximately 80% in equity investments and 20% in fixed-income investments. The Company believes that this investment mix properly matches the plan’s benefit obligations. The equity component of the expected long-term rate of return was determined using a combination of the actual rate of return of equities (net of inflation) and an inflation-adjusted equity rate of return (assuming an inflation rate of 4%) based upon historical 30-year rolling averages (with the most recent five years more heavily weighted).