m&v part 4: m&v plan review. 4-2 m&v plan review Ø femp documents f m&v overview...

TRANSCRIPT

M&V Part 4: M&V Part 4: M&V Plan M&V Plan

ReviewReview

4-2

M&V Plan ReviewM&V Plan Review

FEMP DocumentsM&V Overview Checklist (Phase 2)Final M&V Plan Checklist (Phase 3)

Risk & Responsibility Allocation Option A and Stipulation

Detailed Guidelines

Options B / C / D

4-3

Phase 2: Project DevelopmentPhase 2: Project Development

Contractor Responsibilities Develop M&V approach

(M&V Overview). Explain and justify approach.

Agency Responsibilities Review M&V approach and provide

feedback.

Phase 1 Phase 2 Phase 3 Phase 4

4-4

M&V Overview ChecklistM&V Overview Checklist

The following items should be described: Project site and measures. What savings will be claimed. M&V approach for each measure. Baseline equipment and conditions. Proposed equipment and conditions. Annual measurement and verification activities.

Phase 1 Phase 2 Phase 3 Phase 4

4-5

Phase 3: Negotiation and AwardPhase 3: Negotiation and Award

Contractor Responsibilities Perform Detailed Energy Survey (DES) and

document baseline information. Modify M&V plan to satisfy agency needs

and desires.

Agency Responsibilities Review and Approve M&V Plan. Witness and observe DES.

Phase 1 Phase 2 Phase 3 Phase 4

4-6

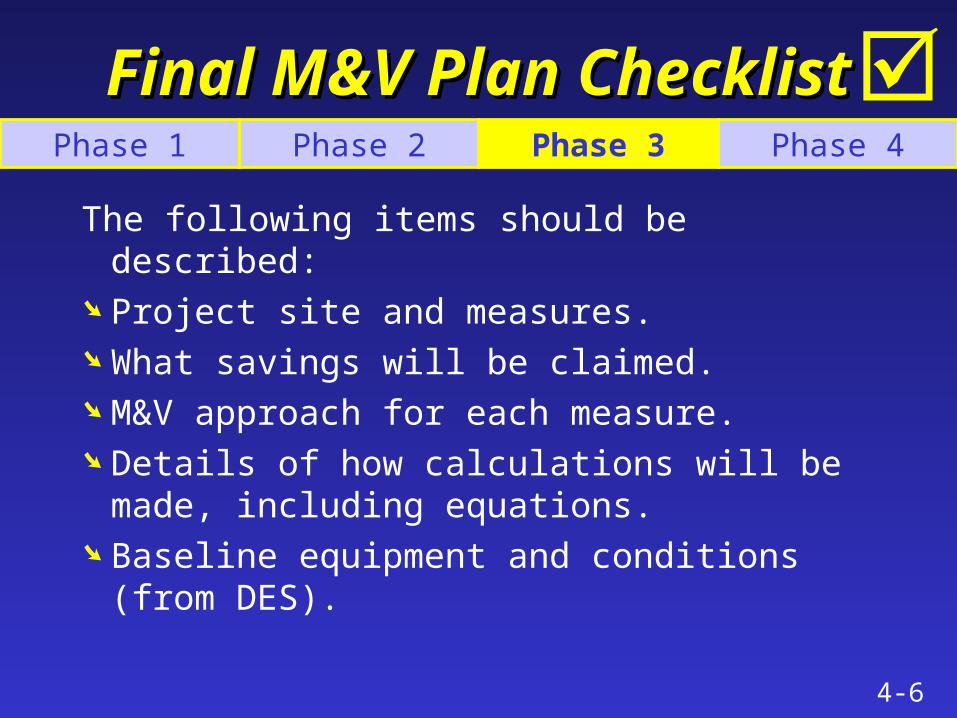

Final M&V Plan ChecklistFinal M&V Plan Checklist

The following items should be described: Project site and measures. What savings will be claimed. M&V approach for each measure. Details of how calculations will be made,

including equations. Baseline equipment and conditions (from

DES).

Phase 1 Phase 2 Phase 3 Phase 4

4-7

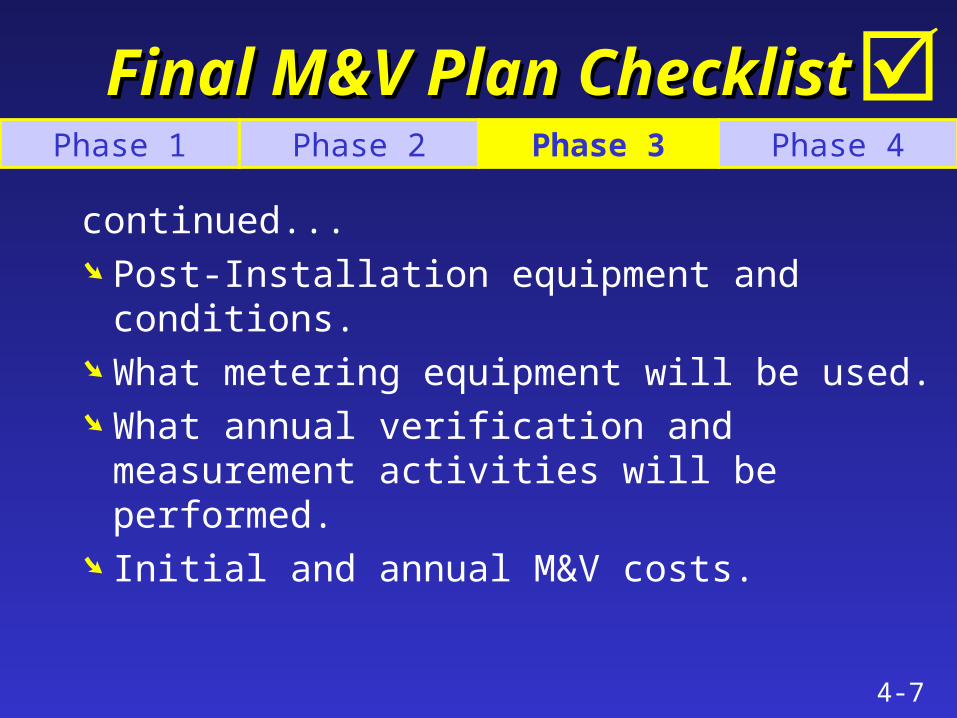

Final M&V Plan ChecklistFinal M&V Plan Checklist

continued... Post-Installation equipment and conditions. What metering equipment will be used. What annual verification and measurement

activities will be performed. Initial and annual M&V costs.

Phase 1 Phase 2 Phase 3 Phase 4

4-8

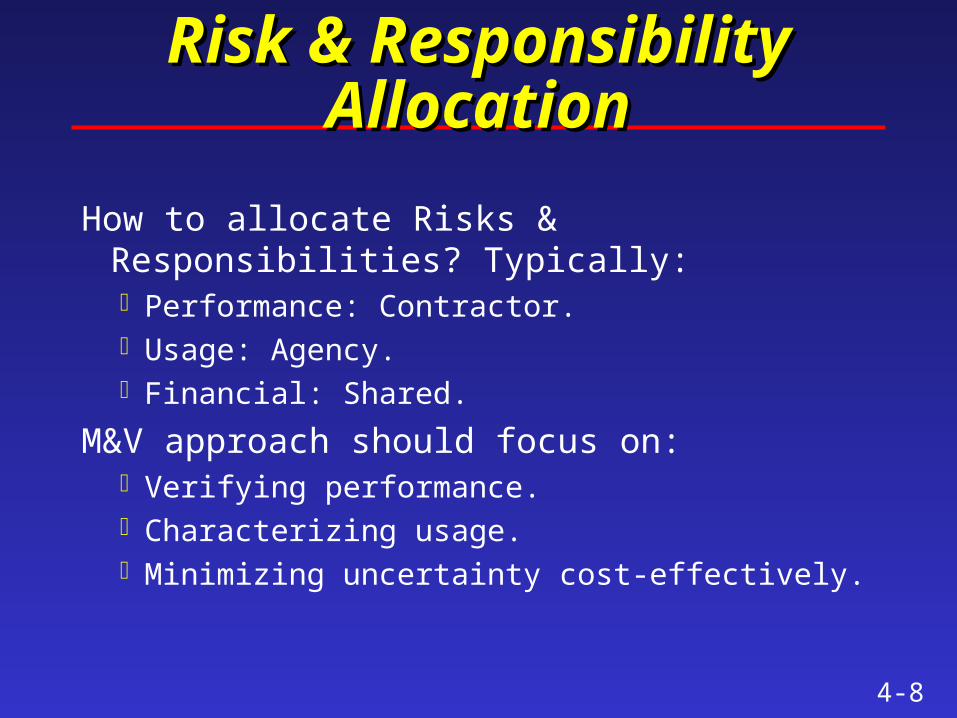

Risk & Responsibility AllocationRisk & Responsibility Allocation

How to allocate Risks & Responsibilities? Typically:Performance: Contractor.Usage: Agency.Financial: Shared.

M&V approach should focus on:Verifying performance.Characterizing usage.Minimizing uncertainty cost-effectively.

4-9

Cost EffectivenessCost Effectiveness

Need to balance M&V rigor with project risk.Measure things that need measuring.Consider required precision.

Law of Diminishing Returns applies. Typically, initial M&V costs will be 3% to

15% of the capital cost; annual M&V costs will be 3 – 15% of the savings.

4-10

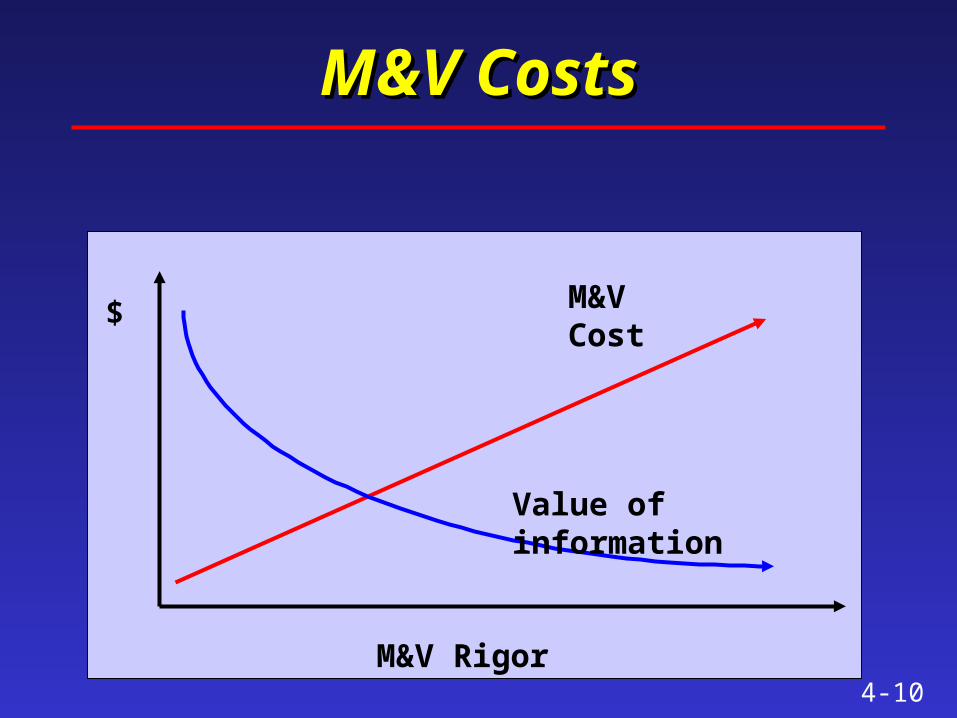

M&V CostsM&V Costs

M&V Rigor

M&V Cost

Value of information

$

4-11

Western Region SuperESPCWestern Region SuperESPC

Annual M&V Costs and Annual Savings

Cost, % = -3E-07 * Savings + 12%

R2 = 0.40

0%

5%

10%

15%

$0 $200,000 $400,000Annual Savings

Rel

ativ

e M

&V

Cos

t

No strong relationship between M&V costs and savings!

4-12

Selection MatrixSelection Matrix

Simple M&V

More Rigorous

Uncertainty: High Low

Component Level A B

Whole Facility C D

Warning: This is a gross generalization!

4-13

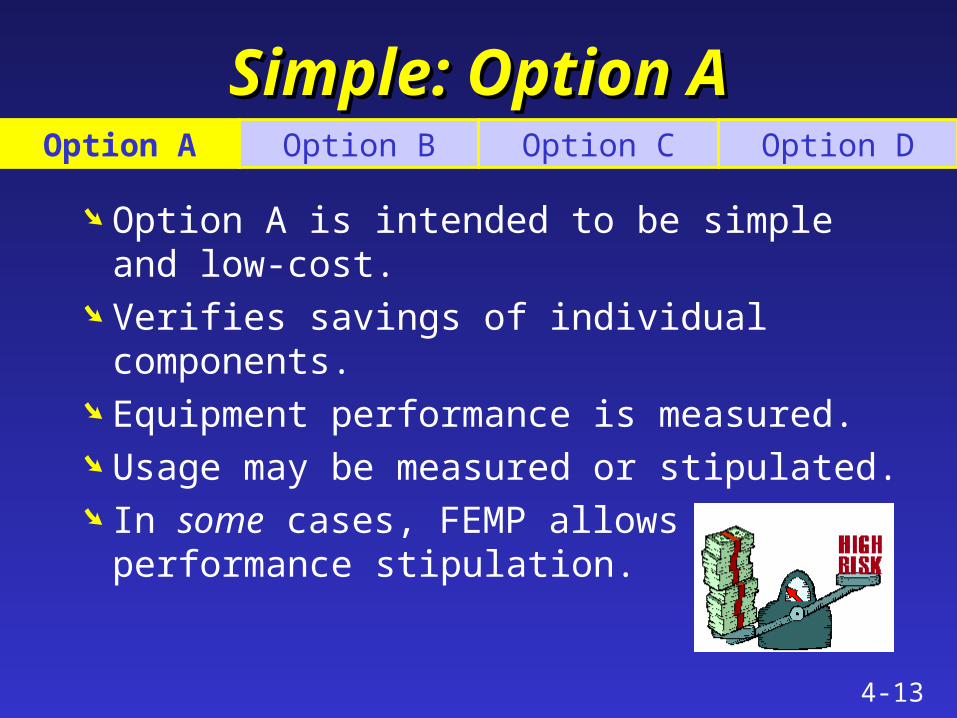

Simple: Option ASimple: Option A

Option A is intended to be simple and low-cost.

Verifies savings of individual components. Equipment performance is measured. Usage may be measured or stipulated. In some cases, FEMP allows

performance stipulation.

Option A Option B Option C Option D

4-14

Option A and StipulationOption A and Stipulation

Not ‘stipulated savings’!

Stipulations shift risk to agency.OK for usage.Not OK for performance (some

exceptions).

Option A Option B Option C Option D

4-15

Option A GuidelinesOption A Guidelines

Option A most common in SuperESPC. Potential for misapplication. Discusses how to use Option A. Discusses how to apply stipulations.

See Detailed Guidelines For FEMP M&V Option A (2002)

Option A Option B Option C Option D

4-16

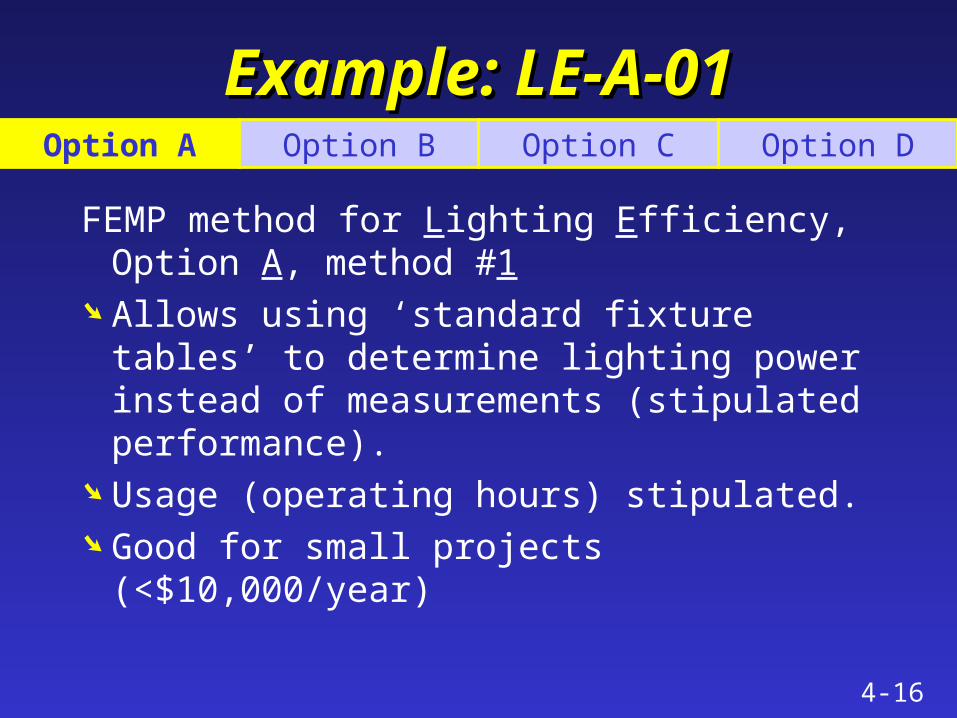

Example: LE-A-01Example: LE-A-01

FEMP method for Lighting Efficiency, Option A, method #1

Allows using ‘standard fixture tables’ to determine lighting power instead of measurements (stipulated performance).

Usage (operating hours) stipulated. Good for small projects (<$10,000/year)

Option A Option B Option C Option D

4-17

Stipulation RiskStipulation Risk

LE-A-01 allows stipulation of both usage and performance parameters.

If the stipulated values are wrong, the savings estimates will be wrong.

The agency assumes all risk, contrary to the intent of a performance contract.

Option A Option B Option C Option D

4-18

Stipulation ProblemStipulation ProblemOption A Option B Option C Option D

Lighting Retrofit Project

0

200,000

400,000

600,000

800,000

1,000,000

Jan-97 Jun-97 Dec-97 Jun-98 Dec-98 Jun-99 Dec-99 Jun-00

kWh

Actual Energy Consumption

Anticipated Energy Consumption

Baseline Post-Retrofit

Post-retofit energy use should have decreased 15%;actual energy use decreased by 10%.

4-19

Stipulation LessonsStipulation Lessons

Guaranteed savings $50,000; $24,000 observed in utility bill.

Poorly-defined baseline prevents adequate after-the-fact analysis.

Option C methods are not sufficiently accurate to support or reject savings claims.

Option A Option B Option C Option D

4-20

Example: LE-A-02Example: LE-A-02

FEMP method for Lighting Efficiency, Option A, method #2

Common fixture types measured using a statistically-valid number of measurements (3-6).

Operating hours usually stipulated, but can be measured.

Good for large projects (>$100,000/yr)

Option A Option B Option C Option D

4-21

Option A Risk AllocationOption A Risk Allocation

The contractor should measure performance since they control this.

The operating hours may be stipulated. Measuring the operating hours reduces uncertainty and risks to both parties.

The agency bears the risk of unrealized savings due to changing schedule or incorrect operating hours.

Option A Option B Option C Option D

4-22

More Rigorous: Option BMore Rigorous: Option B

Verifies at component level. Requires periodic performance

measurements- annual to hourly. Usage can be stipulated or measured.

Option A Option B Option C Option D

4-23

Option B Risk AllocationOption B Risk Allocation

Energy use and claimed savings will vary from year to year.

The contractor assumes all project risk (performance & usage) since savings are based on measured energy use.

The contractor would be wise to include in the M&V plan: limits on their exposuremethods of adjusting the baseline or usage

Option A Option B Option C Option D

4-24

Simple: Option CSimple: Option C

Regression method using existing utility meters.

Captures interactions between measures to find total savings.

Requires collecting and tracking information that affects energy use:weatheroccupancyproduction

Option A Option B Option C Option D

4-25

Option C Risk AllocationOption C Risk Allocation

The contractor may not find the savings if less than 15% of the baseline use.

The contractor bears all project risk. The agency bears the responsibility of

tracking changes that affect energy use. It may take 1 year to determine savings. Weather and other factors will influence

savings estimates.

Option A Option B Option C Option D

4-26

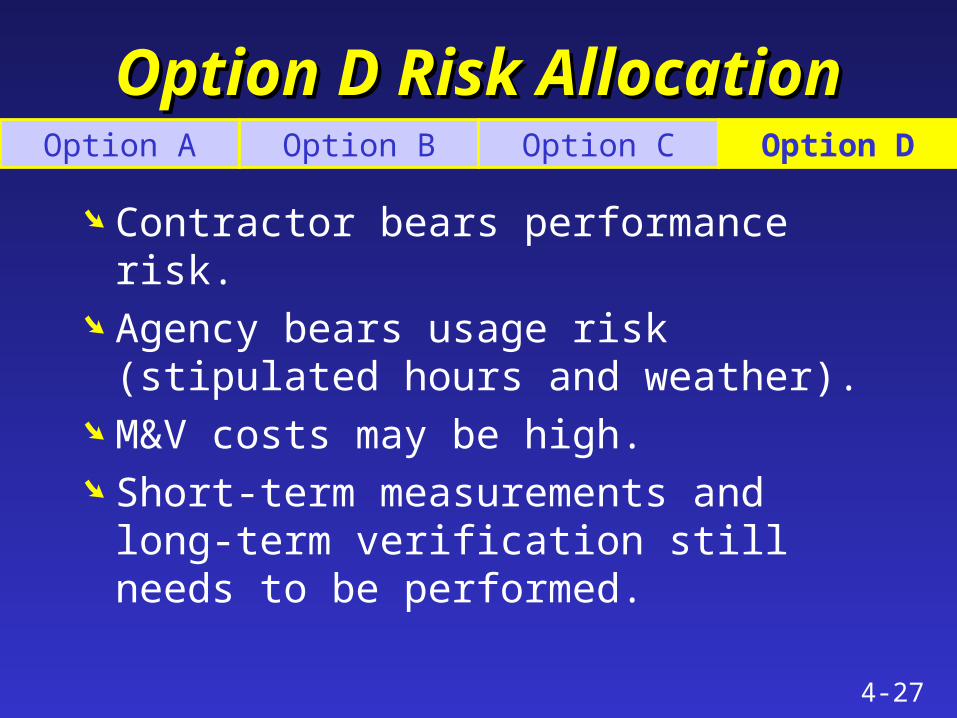

More Rigorous: Option DMore Rigorous: Option D

Computer simulation method of evaluating total building performance.

Requires calibration to be useful. Requires measurements to calibrate

model. Weather data usually ‘typical’, not real.

Option A Option B Option C Option D

4-27

Option D Risk AllocationOption D Risk Allocation

Contractor bears performance risk. Agency bears usage risk (stipulated

hours and weather). M&V costs may be high. Short-term measurements and long-

term verification still needs to be performed.

Option A Option B Option C Option D

4-28

ResultsResults

Option Usage Risk

Performance Risk

Uncertainty Cost

A agency contractor high low

B contractor contractor low high

C contractor contractor medium low

D agency contractor variable high

Option A Option B Option C Option D

Warning: These are gross generalizations!

It is possible to shift risks and changes costs.

4-29

Review & DiscussionReview & Discussion

Performance must be verified if guarantee is to have value.

Agency often assumes usage risk. Uncertainty is inherent in M&V. M&V costs need to be balanced against

project risks.

4-30

Review QuestionsReview Questions

How do we measure savings? When might an agency accept

performance risk?