n ationwide service;small town integrity tm

TRANSCRIPT

There are two parts to an HSA...

What is a Health SavingsAccount (HSA)?

Nationwide Service ; Small Town IntegrityTM

*Actual tax savings will vary by state and tax bracket. This table is provided as an example of possible tax savings. Additional tax savingsavailable on tax-deferred earnings.

Nationwide Service ; Small Town IntegrityTM

ALSO KNOWN A S M S A BANKT M

Example of ContributionTax Savings

$2,600 (Max. Annual Contribution)

$858Possible Annual Savings

Single Coverage Family Coverage

$5,150 (Max. Annual Contribution)

$1,442 (28% Federal Tax Bracket)*

$257 (5% State Tax)*

$728 (28%Federal Tax Bracket)*

$130 (5% State Tax)*

$1,699Possible Annual Savings

Part 1:Qualifying High

Deductible Health Plan(HDHP)

Part 2:Health Savings Account

(HSA)

High Deductible HealthPlan

An HDHP is designed to coverfor serious events, while you

pay for small and routineexpenses until your deductible

is met.

Health Savings AccountAn HSA is a tax exempt account

in which you accumulate savings to pay for minor and routine medical expenses that

make up your deductible or arenot coverd by your plan. An

HSA allows you to enjoy uniquetax benefits and affordable health

premiums without risking your protection.

Benefits of an HSAContributions: • Can be made by account holder, third party on behalf of

account holder, and/or by employer.• Can be made up to 100% of annual deductible with maximum

limits determined by the IRS each year.• Catch-up contributions are generally available to individuals,

and their spouses, who are between the age of 55 and 65.

Tax Benefits: • Contributions can be made pre-tax through a Cafeteria Plan

or as an above the line tax-deduction.• Interest and/or earnings on the assets grow tax-deferred.• Distributions are tax-free if used for qualified medical

expenses.

Allowable Distributions: • Money saved in an HSA can be used for qualified medical

expenses. (See IRS Publication 502). • HSA funds can also be used to pay COBRA or other medical

insurance premiums during periods of unemployment or temporary layoff while collecting unemployment compensation.

• At age 65, unused HSA money can be withdrawn for non-medical reasons without penalty (ordinary income taxapplies).

Eligibility RequirementsTo qualify for an HSA : (1) You must be covered by a HDHP.(2) You cannot be covered by a health plan other than a HDHP.(3) You are not enrolled in Medicare. (4) You may not be claimed as a dependent on another person’s

tax return.

How to open an HSA1) Obtain Coverage.Before you can open a Health Savings Account, you must have aqualifying high deductible health plan. Inquire with your insur-ance representative about obtaining coverage.

2) Complete all HSA Bank formsYou can obtain the proper forms from your insurance representative or by visiting our website www.hsabank.com. Forassistance, contact your insurance representative or an HSABank Personal Banker (800) 357-6246. Be sure to sign all forms.

3) Mail the forms and your checkMail all completed forms and your check(s) to the address listedon your application. Your check, payable to HSA Bank, shouldcover your initial deposit, the account opening fee, and the costof your checks (if requested).

HSA BankTM

211 N. Wisconsin DriveHowards Grove, WI 53083-1118

Phone: (800) 357-6246 • Fax: (920) 565-5283E-mail: [email protected] • Internet: www.hsabank.com

HSA BankTM and MSA BankTM are tradenames and trademarksowned and used by State Bank of Howards Grove.

Health Savings Accounts,or HSAsHSAs are the latest news in affordablehealth care. HSAs combine a qualifiedHigh Deductible Health Plan (HDHP)with a Health Savings Account. The HighDeductible Health Plan covers serious illness and injury, while the HealthSavings Account covers small expensesuntil the deductible is met. HSAs offer away to set aside funds to pay for todayand tomorrow’s medical expenses.

Why do HSAs spellaffordable health care?HSAs provide you with tax savings bothwhen you contribute the funds and whenyou use the funds. Annual contributionsreduce your taxable income and yourqualified medical expenses are nevertaxed. All of the money you set aside inyour HSA grows tax-deferred until age65, when you can withdraw funds for anynon-medical purpose at ordinary tax rates,or tax-free when used for medical expenses.

What is the advantage toan HSA?When compared to other consumer-drivenhealth care options, an HSA provides themost flexible and long-term investmentopportunities to consumers. Unlike mostconsumer-driven health care options;HSAs roll over from year to year, themoney belongs to the individual and isportable if employment changes, availability is not limited by employersize, and funds can be used for non-medical purposes after age 65 (ordinarytax applies).

Just askWhen you discuss a health plan for an HSAwith your health plan representative, let themknow that you’d like HSA Bank to act asyour HSA custodian. Or call HSA Bank at800-357-6246 for more information abouthow you can maximize your health careadvantage with an HSA.

HSA BankTM

HSA Bank is located just one hour north ofMilwaukee, Wisconsin and draws its rootsfrom providing a full-range of banking andinvestment products and services for individuals and businesses in the local community since 1913 as State Bank ofHowards Grove.

HSA Bank has provided dedicated MedicalSavings Account administration servicessince 1997 and has extended the same levelof commitment to Health Savings Accountssince January 1, 2004. HSA Bank is currently a leading financial institution providing Health Savings AccountAdministration in all 50 states andWashington DC.

HSA BankP.O. Box 939Sheboygan, WI 53082-0939Telephone: 920-565-5252Toll Free: 800-357-6246Fax: 920-565-5283

E-Mail:[email protected]

Web site:www.hsabank.com

August 2004

HealthConsidering a

SavingsAccount?See how an HSASee how an HSA

can maximizecan maximizeyour health care your health care

advantadvantage.age.

Nationwide Service ; Small Town IntegrityTM

Lower feesSome banks charge more infees to establish your HealthSavings Account than you’llearn back in interest. Thiserodes, or sometimes eliminates, any cost savingsadvantage. HSA Bank’smonthly fees and one-time

account set-up fee are usually half of what other custodians charge.

Additionally, HSA Bank will waive your monthly fee when youmaintain a balance of $3,000 or more in the account.

Informative website PLUS Internet BankingHSA Bank knows you need convenient and reliable informationand resources. The HSA Bank website provides valuable information about HSAs including: eligibility, account opening,legislative details, application forms, account access and muchmore. Check out the HSA Bank website or sign-up for internetbanking at: www.hsabank.com.

Peace of mindAs a Federal Deposit Insurance Corporation (FDIC) insuredfinancial institution, HSA Bank ensures that money in your HSAis safe and secure.With Bankline, our toll-free 24-hour automated telephone banking service, you can verify your account balance or otheractivity any time—at no charge! Just call Bankline toll-free at(800) 565-3512, or locally at (920) 565-3962. Your monthly statements will serve as your receipt for any contributions made.

Customer ServiceHSA Bank understands that you mayhave questions or concerns about youraccount or HSAs. Our dedicatedPersonal Bankers are available toll-freeat (800) 357-6246, Monday throughFriday, from 7A.M. to 7P.M., CST, toanswer any of your questions. DedicatedSpanish-speaking representatives are alsoavailable toll-free at 866-357-6232,8A.M. to 5P.M., CST.

Member FDIC InsuredHSA BankTM is a tradename and trademark

owned and used by State Bank of Howards Grove.

Now you havea choiceWhile many companies offer to act ascustodian or trustee of your HealthSavings Account by administeringdeposits and withdrawals to youraccount, HSA BankTM (State Bank ofHowards Grove) offers a safe and morecost-effective alternative. By selectingHSA Bank as your trustee, you maximizeyour benefits and cost savings.

Higher interest ratesHSA Bank offers higher interest rates on its HSAsthan most banks offer on traditional savings ormoney market accounts. Your account also has lowbalance requirements to earn the higher rates ofinterest. You can check our current rates at:www.hsabank.com.

ConvenienceHSA Bank offers a variety of contribution andwithdrawal methods to provide you with quick andeasy access to your account. Contributions—You can make contributions eitherby check or by electronic transfer from your personalchecking account. Contributions made by checkshould be sent with a contribution form or depositticket. Electronic transfers can be done through On-Demand Transfer. On-Demand Transfer allows you toset up one-time or recurring contributions from yourpersonal computer. For employer contributionoptions, please visit www.hsabank.com or call (800) 357-6246 for details. Withdrawals—Our HSA Bank debit card makespaying for health care quick and easy. Just presentyour HSA Bank debit card for payment of services toany provider who accepts Debit MasterCard®. Tomake sure you receive any network discounts associated with your health plan, wait to pay theprovider until you have received an explanation ofbenefits (EOB). The cost of these health care serviceswill be automatically deducted from your HealthSavings Account. If you prefer, HSA Bank also provides a supply of checks, for a nominal fee, toaccess your account. If you pay your expenses out-of-pocket, you also have the option to submit awithdrawal form and HSA Bank will send you a distribution check.

How to applyWant to open an HSA Bank Health Savings Account?Just follow these three easy steps and you’re on your way tomore affordable health care! A packet of the necessary formscan be provided through your health plan representative or byvisiting our website at: www.hsabank.com.

1) Verify eligibility & health plan coverage.Once you have verified your eligibility and obtained qualifying health plan coverage, you will be eligible for anHSA. You are eligible for an HSA if:

1. You are covered under a qualifying High Deductible Health Plan(HDHP). Inquire with your health plan representative about obtaining coverage.

2. You are not covered under any other health plan than the HDHP.3. You are not enrolled in Medicare (typically age 65).4. You cannot be claimed as a dependent on another person’s tax return.

2) Complete all HSA Bank formsYou can obtain the proper application and eligibility formsfrom your health plan representative or by visiting the HSABank website. Use the Online Access form in your accountwelcome kit to sign up for Internet Banking and On-DemandTransfer. Other HSA Forms are available on the HSA Bankwebsite at www.hsabank.com.

For assistance in completing these forms, please contact anHSA Bank Personal Banker at (800) 357-6246. Be sure tosign all forms.

3) Mail the forms and your checkMail all completed forms to the address found on the application form. Your check, payable to HSA Bank, shouldcover your initial deposit, the account opening fee, and thecost of your checks, if requested. Please call our HSA BankPersonal Bankers at 800-357-6246 or visit our website foradditional information.

Once your account has been opened, you will receive a welcome kit in 8-12 business days with your account numberand other important account information.

Group Plans?If you are enrolling through your employer, the enrollmentprocess decribed above may vary. Please contact your benefits administrator for enrollment details.

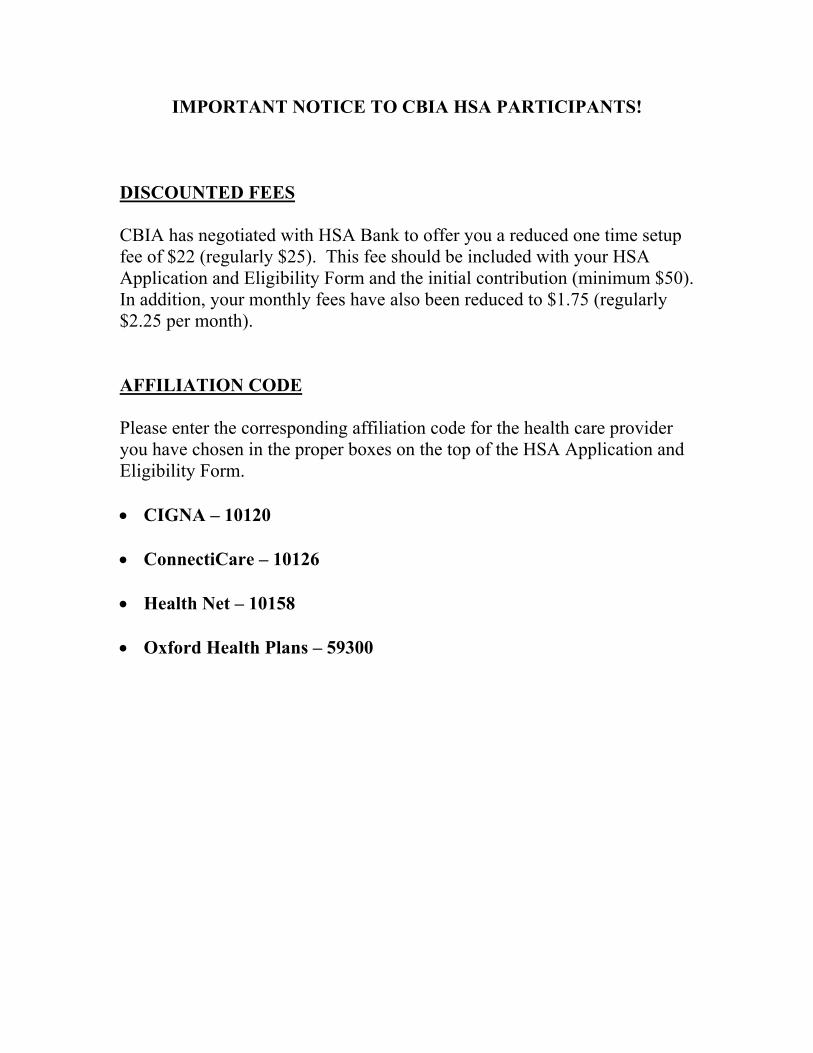

IMPORTANT NOTICE TO CBIA HSA PARTICIPANTS!

DISCOUNTED FEES

CBIA has negotiated with HSA Bank to offer you a reduced one time setupfee of $22 (regularly $25). This fee should be included with your HSAApplication and Eligibility Form and the initial contribution (minimum $50).In addition, your monthly fees have also been reduced to $1.75 (regularly$2.25 per month).

AFFILIATION CODE

Please enter the corresponding affiliation code for the health care provideryou have chosen in the proper boxes on the top of the HSA Application andEligibility Form.

• CIGNA – 10120

• ConnectiCare – 10126

• Health Net – 10158

• Oxford Health Plans – 59300

My employer wishes to have access to my HSA Bank account information inorder to facilitate direct deposit of employer contributions to my account. I, asnamed above, authorize my employer to obtain my account information; for thesole purpose of facilitating direct contributions to my account. I hold harmlessand indemnify the Bank against any claims against or losses Bank may sufferarising out of Bank reliance on this authorization and release Bank from allliability arising form such reliance. This authorization remains in full force andeffect until Bank receives written notice of revocation and has had a reasonabletime to act upon such notice.

HEALTH SAVINGS ACCOUNTAPPLICATION AND ELIGIBILITY FORM

Note: To help the government fight the funding of terrorism and money laundering activities, Federal law requires all financial institutions to obtain,verify and record information that identifies each person who opens an account. What this means to you: When you open an account we will ask foryour name, street address, date of birth and other information that will allow us to identify you. We may request a copy of your driver's license orother identifying documents.

Initial Contribution Source and Amount

Accountholder and/or Third Party Deposit

Employer Contribution

Employee Pre-Tax through Section 125 Plan

Type of Initial DepositRegular-Year of Contribution

Rollover/Transfer

Internal Use:

StreetAddress

Fed ID #

For Insurance Agents ONLY

Preferred Mailing Method Street Address PO Box

Driver's License State ID Passport

Social Security # Birth Date

Please fill in all boxes (MM DD YYYY) (IE: 01 01 2005)Personal Information:

Form of IdentificationID#

Instructions: All fields must be completed. For assistance, call 800-357-6246. (Para unformulario en Español por favor contactar 866-357-6232). Return this Application with a check to:

AIN #

CodeIn. Ong.

- Please check one

* Set-up Fee $25.00 for handwritten applications (ex. ) or$22.00 for machine-readable applications (ex. ). Visit www.hsabank.comor see your healthcare representative for a PDF file you can complete using a computer.

H S A

HSAAE031505

Amt. ($) .Amt. ($) .

Total "Above the Line" Deductions (after tax)

Pre-tax Deduction

HSA Bank™ is a division of Webster Bank, N.A.

HSA Bank™, P.O. Box 939, Sheboygan, WI 53082-0939

(Required)

(Required)

Purchases made with either the debit MasterCard® or HSA Bank checks will be reported by the Bank as "normal distributions" and should only be used for qualified medicalexpenses.I understand I am responsible for any IRS penalties. I understand that I should submit an HSA withdrawal form for any non-qualifying or non-medical transactionat a cost of $4.00 per occurrence. I understand the bank will issue me a check. I understand I must pay a monthly fee of $2.25 for this account. The fee is waived each monthfor accounts that maintain a balance greater than $3,000 during the entire month period.

HSA Account Options:Please read Power of Attorney section for spousal or third party access to your HSA.

Affiliation

I am interested in receiving an Investment Application. (Non FDIC Insured: Stocks, Bonds, and Mutual Fund Options)

Make Check Payable to HSA Bank

Amt. ($) .

Amt. ($) .

Contact your employer to utilize this option

($) .

If email address is provided, HSA Bank will send an email confirmation following account opening. All accounts will also receive a Welcome Kit bymail within 2 weeks of account opening.

Total Initial Contribution Amount(Indicate amount on part C of Instructions section above)

A. Set-up Fee (See Instructions)* $

D. Total Amount Enclosed $C. Initial Contribution (Min. $50) $B. Check Order ($12.75, if requested) $

Payroll Deductions Contact your employer to utilize this option

Payroll Deductions

PO Box City

State Zip

(Please attach transfer/rollover form)

(Required)

Monthly Per Payroll

Home # Bus. #

I would like 1 free debit MasterCard issued in my name for my account.

Broker Dealer

I would like to be enrolled in internet banking. (Email address required above for this option)

I would like to order 50 non-duplicate checks, including 10 deposit tickets, at a cost of $12.75. (Indicate amount on part B of Instructions section above)

My employer is not authorized to facilitate deposits to my account.

Employer Consent

Group

First Name MI Last Name

Account holder certification- I certify that: (1) I am or effective * will be covered by a single or family

qualified High Deductible Health Plan (HDHP), with a deductible of , (2) I certify that I am not

covered by a health plan, other than a HDHP, which provides any of the same benefits as the HDHP, (3) I am not enrolled in Medicare,

and (4) I may not be claimed as a dependent on another person's tax return.

Authorized Signer / Power of Attorney (POA) (Optional): Authorized Signer / POA signature required below.Since regulations require that only one individual own a Health Savings Account, the Accountholder may want his/her spouse and/or another third party throughpower of attorney to write checks or use his/her debit card. I (account holder) hereby designate the following individual as additional authorized signer on myHealth Savings Account.

By signing this Application and per the HSA Account options selected, I am requesting that the Bank issue to my spouse or other authorized third party, asindicated above, a separate debit MasterCard to allow them access to my Health Savings Account and to add their name to my HSA Bank check order tofacilitate access to my Health Savings Account.

Signatures Important: Please read before signing.I understand the eligibility requirements for the type of HSA deposit I am making and I state that I do or effective the date above qualified to make thedeposit. HSA Bank is hereby appointed to serve as custodian of my Health Savings Account. I have received a copy of the Application, HSA CustodialAgreement and Fee Schedule as they may be amended from time to time. I also agree to the Bank's agreements, rules and regulations, and disclosuresapplicable to this account and any additional accounts that I establish with the Bank in the future as an individual, custodian or single trustee; this mastersignature card agreement governing additional account will remain in effect as long as I continuously maintain at least one covered account with the Bank.Within seven (7) calendar days from the date I open this HSA I may revoke the authorization by mailing or delivering a written notice to HSA Bank (set-upfee non-refundable).

I assume complete responsibility for:1. Determining that I am eligible for an HSA each year I make a contribution. 2. Ensuring that all contributions I make are within the limits set forth bythe tax laws. (Go to www.hsabank.com, click on contribution calculator for help.) 3. The tax consequences of any contribution (including rollovercontributions) and distributions.

T.I.N. BACKUP WITHHOLDING CERTIFICATION (Cross out item two (2) if subject to backup withholding)Under penalties of perjury, I certify that (1) The number shown on this form is my correct taxpayer identification number (T.I.N.)(or I am waitingfor a number to be issued to me), (2) I am not subject to backup withholding because: (a) I am exempt from backup withholding, or (b) I have notbeen notified by the Internal Revenue Service that I am subject to backup withholding as a result of a failure to report all interest and dividends,or (c) the IRS has notified me that I am no longer subject to backup withholding, and (3) I am a U.S. person (including a U.S. resident alien).The Internal Revenue Service does not require your consent to any provision of this document other than the certifications required to avoidbackup withholding.

Accountholder Signature Date

Authorized Signer / POA Signature Date

Signature of Witness Date

I would like a second FREE debit MasterCard® issued, for the POA listed above, for my account to be used for normal distributions only.

Member FDIC

Second Debit Card Option

(Can be anyone other than a family member or the POA who has witnessedthe signing of this form)

Printed Name of Witness ____________________________________

Note: Authorized Signer / POA signature required below.

Member FDIC

Employer Information (For help, see your Insurance or Employer Representative.)Employer Name

Eligibility Requirements: REGULAR HSA

Y N

Your HSA account will be considered established for tax purposes as of your first date of eligibility under your HDHP, provided that you havesigned and dated the application for your HSA on or before that date. If we receive the application after your first date of eligibility under yourHDHP, your HSA account will be considered established as of the date you signed and dated this application. To receive tax favored treatment fordistributions from your HSA account, any qualified medical expenses must be incurred after the date that your HSA account is established.

Deductibleof HDHP

Spouse/Other First MI Last

Effective Date of HDHP

Federal ID #

(Required)

(Employer Only - Required)

(Required if POA is designated)

Rules and ConditionsAn HSA is a trust or custodial account owned by the account holder generally created to payqualifying medical expenses. Contributions can be made to your HSA by you, your employer,or a third party.

If you answered NO to the above, you are not eligible to establish a qualified HSA. Please visitwww.hsabank.com for a Non-Qualified HSA application. * Note: Your application will not be processed untilthe effective date above. Signatures Required Below

High Deductible Health Plan Guidelines for 2005

Minimum DeductibleMaximum Out of Pocket

Maximum Contribution

Single Coverage Family Coverage$1,000 $2,000$5,100 $10,200

Lesser of the annual deductible or:$2,650 $5,250

*Additional catch-up contribution is available for individuals 55 orolder and not enrolled in Medicare

HSA Bank™ is a division of Webster Bank, N.A.

Social Security # Birth Date

HEALTH SAVINGS ACCOUNTDESIGNATION OF BENEFICIARIESSTATE BANK OF HOWARDS GROVE

ALSO KNOWN AS MSA BANK™

Personal Information:

HSA Bank™ and MSA Bank™ are tradenames and trademarks owned and used by State Bank of Howards Grove.

Initial Beneficiary Designation : I designate the individual(s) or entity named below as my primary and/or contingent beneficiary(ies) ofthis HSA.Replace Beneficiary(ies): I designate the individual(s) or entity named below as my primary and/or contingent beneficiary(ies) of the accountnamed above and hereby revoke all prior beneficiary(ies) designations, if any, made by me.Add beneficiary(ies): I designate the individual(s) or entity named below as my primary and/or contingent beneficiary(ies) of the accountnamed above. This list supplements, but does not replace, the beneficiary(ies) previously designated by me on the date specified. (When addingbeneficiaries, if the share % of previously designated beneficiary(ies) changes, restate all beneficiary(ies) and the corresponding share % ifthe previous percentages are no longer correct.)

Designation Type: Please check one of the following options.

First Name MI Last Name

SocialSecurity #

BirthDate

Account #(If known)

Designation of BeneficiariesThe following individual(s) or entity shall be my primary and/or contingent beneficiary(ies). If neither primary nor contingent is indicated, the individualor entity will be deemed to be a primary beneficiary. If more than one primary beneficiary is designated and no distribution percentages are indicated, thebeneficiaries will be deemed to own equal share percentages in the account. Multiple contingent beneficiaries with no share percentage indicated will alsobe deemed to share equally. If primary or contingent beneficiary dies before me, his or her interest and the interest of his or her heirs shall terminatecompletely, and the percentage share of any remaining beneficiary(ies) shall be increased on a pro-rated basis. If no primary beneficiary(ies) survives me,the contingent beneficiary(ies) shall acquire the designated share of my account.

Name & Address Date of Birth Social Security # Relationship

Primary

Contingent

Share %

Primary orContingent

Primary

Contingent

This section should be reviewed if either the trust or the residence of the Account Holder is located in a community or marital property state and theAccount Holder is married. Due to important tax consequences of giving up one’s community property interest, individuals signing this section shouldconsult with a competent legal or tax advisor.

CURRENT MARITAL STATUS I am not married - I understand that if I become married in the future, I must complete a new Designation of Beneficiary form. I am married - I understand that if I chose to designate a primary beneficiary other than my spouse, my spouse must sign below.

I am the spouse of the above-named Account Holder. I acknowledge that I have received a fair and reasonable disclosure of my spouse’s property andfinancial obligations. Due to the important tax consequences of giving up my interest in this account, I have been advised to see a tax professional. Ihereby give the Account Holder any interest I have in the funds or property deposited in this account and consent to the beneficiary designation(s)indicated above. I assume full responsibility for any adverse consequences that may result. No tax or legal advice was given to me by the Custodian.

I understand that I may change or add beneficiaries at any time by completing and delivering the proper form to HSA Bank. HSA Bankhas provided no tax or legal advice to me regarding my beneficiary designation.

Primary

Contingent

Primary

Contingent

Primary

Contingent

Spousal Consent

Signature of Spouse Date Signature of Witness (Required) Date

Signature of Witness (Required) DateSignature of Account Holder Date

Signatures

Nationwide Service ; Small Town IntegrityTM

Monthly FeesMonthly Bank Account Fee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $2.25

Waived on balances of $3,000 or moreMonthly Brokerage Account Fee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1.25Distributions by CheckFifty (50) checks (including ten deposit tickets) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $12.75Check Transactions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . No chargeCheck images returned with monthly bank statement . . . . . . . . . . . . . . . . . . . . . . . . . No chargeDistributions by Debit CardDebit card (MasterCard)

Initial Card – two-year expiration. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . No charge2nd Initial Card – (for POA/Spousal use only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . No chargeTwo-year renewal per card . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $3.00Replacement of lost card per card . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $6.00Debit card point-of-sale purchase via signature. . . . . . . . . . . . . . . . . . . . . . . . . . . . No chargePer ATM withdrawal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1.50Per point-of-sale purchase using PIN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1.50

Distributions by Withdrawal FormProcess Withdrawal Form. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $4.00ContributionsContribution Form . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . No chargeOn-Demand-Transfer via www.msabank.com. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . No chargeDeposit Tickets (100). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $8.95Automatic Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . No chargeInternet BankingBalance inquiries, statement requests, download transactions . . . . . . . . . . . . . . . . . . No chargeContributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . No chargeOtherBankline (800-565-3512) balance, transaction inquiries, etc.. . . . . . . . . . . . . . . . . . . . No chargeClose Account Fee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $25.00Excess Contribution Distribution. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $20.00Deposited item returned unpaid to us . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $10.00Overdraft/NSF per item . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $20.00Wire transfer sent or received. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $15.00Stop Payment Requests per item. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $16.00Request copy of debit card transaction merchant receipt . . . . . . . . . . . . . . . . . . . . . . . . . $25.00Request copy of check or statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . $.50 per pg., $2.00 min.Check images . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . No chargeRequest copy of 1099, 5498, or year-end status . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $2.00Corrected IRS filing fee (non-bank error). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $10.00One-time Set-up FeesBank Account 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $25.00 1Brokerage Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . No chargeInterest Rate Tiers (see website for current rates)Less than $500.00 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Subject to change$500.00 or greater and less than $5,000.00. . . . . . . . . . . . . . . . . . . . . . . . . . . Subject to change$5,000.00 or greater and less than $15,000.00 . . . . . . . . . . . . . . . . . . . . . . . . Subject to change$15,000.00 or more . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Subject to changeMinimum Balance RequirementsRather than charge minimum balance fees, the bank will place a $25.00 hold on your bank balance ($100.00 hold if you have brokerage) to keep the account open. Thismeans that your “available” balance for check writing and debit card transactions will be$25.00 less (or $100.00 less) than your actual balance.

HSA BankTM

211 N. Wisconsin DriveHowards Grove, WI 53083-1118

Phone: (800)357-6246 • Fax: (920) 565-5283E-mail: [email protected] • Internet: www.msabank.com

HSA BankTM and MSA BankTM are tradenames and trademarksowned and used by State Bank of Howards Grove.

Member FDIC

Service Fees(Fees subject to change)

Effective January 2004Printed June 2004

1 Bank account set-up fee: The set-up fee will be reduced to $22.00 if the application is completed electronically, printed, signed, and mailed to HSA Bank. Contact your Insurance Agent to receive a PDFthat can be completed on a Personal Computer before being printed and signed.

HEALTH SAVINGS ACCOUNT CUSTODIAL AGREEMENT

The account holder whose name appears on the attached Application ("Depositor") is establishing a Health Savings Account ("HSA") under Section 223(a) of the Internal Revenue Code ("Code") exclusively for the purpose of paying or reimbursing qualified medical expenses of the Depositor and his or her spouse and dependents. The Depositor has assigned to the custodial account the sum indicated on the Application. The Depositor represents that, unless this account is used solely to make rollover contributions, he or she is eligible to contribute to this HSA; specifically, that he or she: (1) is (or as of the effective date as set forth in the Application will be) covered under a high deductible health plan ("HDHP"); is not also covered by any other health plan that is not an HDHP (with certain exceptions for plans providing preventative care and limited types of permitted insurance and permitted coverage); (3) is not enrolled in Medicare; and (4) cannot be claimed as a dependent on another person's tax return. The Depositor, by submitting the signed Application, and the Custodian, by acceptance of the application and delivery of account items to the Depositor for the Depositor's HSA, make the following agreement: ARTICLE I: The Custodian may accept additional cash contributions for the tax year made by or on behalf of the Depositor (by an employer, family member or any other person). No contributions will be accepted by the Custodian for the Depositor that exceed the maximum amount for family coverage plus the catch-up contribution. Contributions for any tax year may be made at any time before the deadline for filing the Depositor's federal income tax return for that year (without extensions). Rollover contributions from an HSA or an Archer Medical Savings Account (Archer MSA) need not be in cash and are not subject to the maximum annual contribution limit set forth in Article II.

ARTICLE II: For calendar year 2004, the maximum annual contribution limit for a Depositor with single coverage is the lesser of the amount of the HDHP deductible or $2,600. For calendar year 2004, the maximum annual contribution limit for a Depositor with family coverage is the lesser of the amount of the HDHP deductible or $5,150. These limits are subject to cost-of-living adjustments after 2004. Eligibility and contribution limits are determined on a month-to-month basis. Contributions to Archer MSAs or other HSAs count toward the maximum annual contribution limit to this HSA. For calendar year 2004, an additional $500 catch-up contribution may be made for a Depositor who is at least age 55 or older and not enrolled in Medicare. The catch-up contribution increases to $600 in 2005, $700 in 2006, $800 in 2007, $900 in 2008, and $1,000 in 2009 and later years. Contributions in excess of the maximum annual contribution limit (other than catch-up or rollover contributions) are subject to a 6% excise tax. This tax will apply each year in which an excess remains in your HSA.

ARTICLE III: It is the responsibility of the Depositor to determine whether contributions to this HSA have exceeded the maximum annual contribution limit described in Article II. If contributions to this HSA exceed the maximum annual contribution limit, the Depositor shall notify the Custodian that there exist excess contributions to the HSA. It is the responsibility of the Depositor to request the withdrawal of the excess contribution and any net income attributable to such excess contribution.

ARTICLE IV: The Depositor's interest in this custodial account is non-forfeitable.

ARTICLE V: No part of the custodial funds may be invested in life insurance contracts or in collectibles as defined in Code Section 408(m). The assets of this account may not be commingled with other property except in a common trust fund or common investment fund. Neither the Depositor nor the Custodian will engage in any prohibited transaction with respect to this account (such as borrowing or pledging the account or engaging in any other prohibited transaction as defined in Code Section 4975).

ARTICLE VI: Distributions of funds from this HSA may be made upon the direction of the Depositor. Distributions from this HSA that are used exclusively to pay or reimburse qualified medical expenses of the Depositor, his or her spouse, or dependents are tax-free. However, distributions that are not used for qualified medical expenses are included in the Depositor's gross income and are subject to an additional 10 percent tax on that amount. The additional 10 percent tax does not apply if the distribution is made after the Depositor's death, disability, or reaching age 65. The Custodian is not required to determine whether the distribution is for the payment or reimbursement of qualified medical expenses. Only the Depositor is responsible for substantiating that the distribution is for qualified medical expenses and must maintain records sufficient to show, if required, that the distribution is tax-free.

ARTICLE VII: If the Depositor dies before the entire interest in the account is distributed, the entire remaining interest will be disposed of as follows: 1. If the beneficiary is the Depositor's spouse, the HSA shall become the spouse's HSA as of the date of death. 2. If the beneficiary is not the Depositor's spouse, the HSA shall cease to be an HSA account as of the date of death. If the beneficiary is the Depositor's estate, the fair market value of the account as

of the date of death is taxable on the Depositor's final return. For other beneficiaries, the fair market value of the account is taxable to that person in the tax year that includes such date.

ARTICLE VIII: The Depositor agrees to provide the Custodian with information necessary for the Custodian to prepare any report or return required by the IRS. The Custodian agrees to submit any report or return as prescribed by the IRS.

ARTICLE IX: Notwithstanding any other article that may be added or incorporated in this agreement, the provisions of Articles I through VIII and this sentence are controlling. Any additional article in this agreement that is inconsistent with Code Section 223 or IRS published guidance will be void.

ARTICLE X: This Agreement will be amended from time to time to comply with the provisions of the Code or IRS published guidance. Other amendments may be made with the consent of the Depositor and the Custodian.

ARTICLE XI 11.01 Definitions: In this part of the Agreement (Article XI), the words "you" and "your" refer to the Depositor. The Depositor is the person who establishes the custodial

account. The words "we," "our," and "us" refer to the Custodian, HSA Bank.

11.02 Notices and Changes of Address: Any required notice regarding this HSA will be considered effective when we mail it to the last address of the intended recipient which we have in our records. Any notice to be given to us will be considered effective when we actually receive it. You must notify us of any changes of address.

7.03 Representations and Responsibilities: You represent and warrant to us that any information you have given or will give us with respect to this Agreement is complete and accurate. Further, you agree that any directions you give us, or any action you take will be proper under this Agreement and that we are entitled to rely upon any such information or directions. We shall not be responsible for losses of any kind that may result from your directions to us or your actions or failures to act, and you agree to reimburse us for any losses we may incur as a result of such directions, actions or failures to act. We shall not be responsible for any penalties, taxes, judgments or expenses you incur in connection with your HSA. We have no duty to determine whether your contributions or distributions comply with the Code, regulations, rulings or this Agreement.

7.04 Service Fees: We have the right to charge an annual service fee or other designated fees (for example, a transfer, withdrawal or termination fee) for maintaining your HSA. In addition, we have the right to be reimbursed for all reasonable expenses we incur in connection with the administration of your HSA. We may charge you separately for any fees or expenses, or we may deduct the amount of the fees or expenses from the assets in your HSA, at our discretion. We reserve the right to charge any additional fee upon 30 days notice to you that the fee will be effective. Any brokerage commissions attributable to the assets in your HSA will be charged to your HSA. You cannot reimburse your HSA for those commissions.

7.05 Investment of Amounts in the HSA: You will select the type of investment for your HSA assets; provided, however, that your selection of investments shall be limited to those types of investments that we are authorized by our charter to offer and do in fact offer for investment in HSAs. Any investment you select for your HSA shall be subject to any and all restrictions or limitations, direct or indirect, which are imposed by or flow from the bylaws of our organization and all Federal and State laws and regulations which apply to us.

7.06 Beneficiaries: You may designate one or more persons or entities as beneficiary of your HSA. This designation can only be made on a form prescribed by us and will only be effective when filed with us during your lifetime. Unless specified otherwise in writing by you, each beneficiary designation you file with us will cancel all previous ones. The consent of a beneficiary shall not be required for you to revoke a beneficiary designation. If you do not designate a beneficiary, your estate will be the beneficiary.

7.07 Termination: Either party may terminate this Agreement at any time by giving written notice to the other. We can resign as custodian at any time effective 30 days after we mail written notice of our resignation to you. Upon receipt of that notice, you must make arrangements to transfer your HSA to another financial organization. If you do not complete a transfer to your HSA within 30 days from the date we mail the notice to you, we have the right to transfer your HSA assets to a successor HSA custodian or trustee that we choose in our sole discretion, or we may pay your HSA to you in a single sum. We shall not be liable for any actions or failures to act on the part of any successor custodian or trustee, nor for any tax consequences you may incur that result from the transfer or distribution of your assets pursuant to this Section.

If this Agreement is terminated, we may hold back from your HSA a reasonable amount that we believe is necessary to cover any one or more of the following:

• Any fees, expenses or taxes chargeable against your HSA; • Any penalties associated with the early withdrawal of any savings instrument or other investment in your HSA.

If our organization is merged with another organization (or comes under the control of any Federal or State agency) or if our entire organization (or any portion which includes your HSA) is bought by another organization, that organization (or agency) shall automatically become the trustee or custodian of your HSA, but only if it is the type of organization authorized to serve as an HSA trustee or custodian.

If we fail to comply with certain Treasury regulations, or we are not keeping the records, making the returns, or sending the statements as are required by forms or regulations, the IRS may, after notifying you, require you to substitute another custodian or trustee.

7.08 Amendments: We have the right to amend this Agreement at any time. Any amendment we make to comply with the Code and related regulations does not require your consent. You will be deemed to have consented to any other amendments unless, within 30 days from the date we mailed the amendment, you notify us in writing that you do not consent.

7.09 Withdrawals: All requests for withdrawal shall be in writing on a form provided by or acceptable to us. The method of distribution must be specified in writing. The tax identification number of the recipient must be provided to us before we are obligated to make a distribution. Any withdrawals shall be subject to all applicable tax and other laws and regulations including possible early withdrawal penalties and withholding requirements. We reserve the right to reasonably restrict the frequency and/or minimum amount of distributions.

7.10 Transfer from Other Plans: We can receive amounts transferred to this HSA from the custodian or trustee of another HSA or MSA. However, we also reserve the right not to accept any transfer.

7.11 Liquidation of assets: We have the right to liquidate assets in your HSA if necessary to make distributions or to pay fees, expenses or taxes properly chargeable against your HSA. If you fail to direct us to which assets to liquidate, we will decide in our complete and sole discretion and you agree not to hold us liable for any adverse consequences that result from our decision.

7.12 Restrictions On The Fund: Neither you nor any beneficiary may sell, transfer or pledge any interest in your HSA in any manner whatsoever, except as provided by law or this Agreement. The assets in your HSA shall not be responsible for the debts, contracts or torts of any person entitled to distributions under this Agreement.

7.13 What Law Applies: This Agreement is subject to all applicable Federal and State laws and regulations. If it is necessary to apply any State law to interpret and administer this Agreement, the law of our domicile shall govern. If any part of this Agreement is held to be illegal or invalid, the remaining parts shall not be affected. Neither your nor our failure to enforce at any time or for any period of time any of the provisions of the Agreement shall be construed as a waiver either of such provisions of your or our right thereafter to enforce each and every such provision.

7.14 Identifying Number: The Depositor's social security number will serve as the identification number of this HSA. For married persons, each spouse who is eligible to open an HSA and wants to contribute to an HSA must establish his or her own account. An employer identification number is required only for an HSA for which a return is filed to report unrelated business taxable income. An employer identification number is required for a common fund created for HSAs.

We shall not be liable to you for any losses, damages, costs, penalties or expenses you incur as a result of your employer's failure to make any employer contributions to your HSA. We are not responsible for monitoring or notifying you of your employer's contributions to your HSA. You are responsible for contacting your employer regarding its contributions and monitoring those contributions. We will provide monthly statements to you.

We shall not be liable to you for any statements, representations, actions or inactions of any insurance agent or agency that sold you an insurance plan in connection with your HSA. The insurance agent or agency is not our partner, agent, affiliate, representative or co-venture.

DISCLOSURE STATEMENT

The following is a general explanation of the laws and IRS guidance governing HSAs. Refer to the Code or a competent tax advisor for more detailed information.

INCOME TAX CONSEQUENCES OF ESTABLISHING AN HSA A. HSA DEDUCTIBLITY – If you or your employer establishes a high deductible health plan, you may be eligible to establish an HSA. If eligible, you, your employer, a family

member, or any other person can make contributions to your HSA. Amounts contributed to an eligible Depositor's HSA are excluded from federal tax unless they exceed the maximum contribution limits described above. Tax treatments concerning state law may vary by state.

B. TAX-DEFERRED EARNINGS – The investment earnings of your HSA are not subject to federal income tax while they remain in your HSA.

C. TAXATION OF DISTRIBUTIONS – As discussed above, the taxation of HSA distributions depends on whether the distribution is for a qualifying medical expense. Qualifying medical expenses are amounts you pay for medical care (as defined in Code Section 213(d)) for yourself, your spouse and your dependents (as defined in Code Section 152), but only to the extent that such amounts are not compensated for by insurance or otherwise.

D. ROLLOVERS – Your HSA may be rolled over to another HSA of yours, or your HSA account with us may receive rollover contributions, provided that applicable rollover rules including the requirements of Code Section 223(f)(5) are followed. Rollovers from a qualified MSA to an HSA account are permitted if made in accordance with applicable MSA rollover laws and regulations. Rollover is a term used to describe a tax-free movement of cash or other property between any of your HSAs. These transactions are often complex. If you have any questions regarding a rollover, please see a competent tax advisor. Certain rollover rules are generally summarized as follows: Rollovers may be made directly from one trustee/custodian to another, or you may have the HSA funds distributed to you to rollover to another HSA. If the funds are distributed to you, 1) to avoid being taxed on the amount, you must rollover the entire distribution not later than 60 days after the distribution is received, and 2) you may roll over the same dollars or assets only once every 12 months. At the time you make a proper rollover contribution to an HSA with us, you must designate to us in writing your election to treat that contribution as a rollover. Once made, the rollover election is irrevocable.

E. CARRYBACK CONTRIBUTIONS – A contribution is deemed to have been made on the last day of the preceding taxable year if made by the deadline for filing your income tax return (not including extensions), and you designate the contribution as a contribution for the preceding taxable year. For example, if you are a calendar year taxpayer and you make your HSA contribution on or before April 15, your contribution is considered to have been made for the previous tax year if you designated it as such.

F. TAX AND SAVINGS CONSEQUENCES – We make no guarantees of any tax or savings consequences.

LIMITATIONS AND RESTRICTIONS A. DEDUCTION OF ROLLOVERS AND TRANSFERS – A deduction is not allowed for rollover or transfer contributions.

B. SPECIAL TAX TREATMENT – Capital gains treatment and the favorable five or ten-year forward averaging tax under Code Section 402 do not apply to HSA distributions.

C. PROHIBITED TRANSACTIONS – If you or your beneficiary engage in a prohibited transaction with your HSA, as described in Code Section 4975, your HSA will lose its tax-exempt status and you must include the value of your account in your gross income for the taxable year.

D. PLEDGING – If you pledge any portion of your HSA as collateral for a loan, that portion will be treated as a distribution and included in your gross income for that year. Member FDIC HSA Bank™ and MSA Bank™ are tradenames and trademarks owned and used by State Bank of Howards Grove. HSACA093004

Nationwide Service ; Small Town IntegrityTM

InvestmentOptions

Now you can put your HSA funds towork for an investment advantage thatyou direct. Simply open a brokerageaccount through HSA BankTM andbegin trading your HSA funds online!

By visiting www.hsabankusa.com, wecan link you to our brokerage tradingsite. You can access your brokerageaccount 24 hours a day to place trades,get stock quotes, track your portfolio,research securities, and more.

You can also talk to a registered brokerto discuss your account, or you canplace trades and check your portfolio24 hours a day by accessing an automated touch-tone telephone system.

Three Easy Steps1) After opening your HSA accountwith HSA Bank, simply call or e-mail us for a brokerage accountapplication and ACH authorizationform.

2) Once the applications have beencompleted and processed by HSABank’s brokerage partner, your brokerage account will be open.

3) Our brokerage partner will provide you with an account numberand instructions to initiate trades onyour account.

Low Minimum Bank BalanceA minimum bank balance of $100 isrequired. You can invest the entireremaining balance as you choose. (HSAbrokerage trading fees apply.) All tradesclear electronically through your HSAbank account. What could be simpler?

Variety of Vesting OptionsIn addition to a wide range of stocksand bonds, you can invest in over 8,000mutual funds from over 260 fund families, including a supermarket ofover 600 popular no-load, NTF (nontransaction fee) funds.

HSA Bank also accepts HSA brokerageaccount transfers. Please contact us ifyou would like an HSA TransferApplication.

Open your new HSA brokerage accounttoday and take advantage of moreinvestment options than ever before.It’s convenient, it’s easy, and it’s only atHSA Bank.

HSA BankTM

211 N. Wisconsin DriveHowards Grove, WI 53083-1118

Phone: (800) 357-6246 • Fax: (920) 565-5283E-mail: [email protected] • Internet: www.hsabankusa.com

HSA BankTM and MSA BankTM are tradenames and trademarks owned and used by State Bank of Howards Grove.

NOT FDIC INSUREDNot bank guaranteed. May lose value

January 2004

ALSO KNOWN AS MSA BANKTM