nacm oregon may business credit journal

DESCRIPTION

ÂTRANSCRIPT

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 1

In This Issue

Mobile Devices Provide the Credit (and Sales) Team Another Alternative to Customers Signing on the Web’s Dotted Line ...... 1

International Corner ............... 2

Chair’s Message ..................... 3

President’s Message ............... 3

Questions from the Forum ...... 4

Antitrust: The Robison-Patman Act ....................................... 7

Tips & Tricks .......................... 11

Key to Success ....................... 12

Education ............................. 14

NOF Scholarships ................... 15

Training Tips for Collectors ..... 16

NACM National News .............. 17

Credit Learning Center ........... 18

Credit Basics: Setting Credit Limits .................................... 19

Contacts ................................ 20

Mobile Devices Provide the Credit (and Sales) Team Another

The Internet is revolutionizing how the credit department documents sales. Credit teams are loading their companies’ websites with form credit applications (including vendor-friendly terms and conditions), personal and corporate guarantees, security agreements, invoices, and proofs of delivery. The credit department has gone “electronic” to provide for faster payments and more timely credit application submissions, to reduce invoice discrepancies, and to lower the administrative costs tied to new account set up.

I. Mobile Devices, Customer Visits, and Documenting the Sale

For those credit teams that still have a sales team member call on customers with credit applications, or where credit team members make a customer visit at the evaluation stage of the trade relationship, smart phones and tablets are making it easier to close the deal with an electronic credit application.

a. Mobile Technology in the B2B Setting

Smart phones and tablets offer accessibility and portability. Developers have responded to the increasing use of mobile devices in the B2B setting with a surge in B2B-specific apps. In 2010, the business category of the Apple App Store grew 186% (the largest increase of any App Store sector that year). Many third-party digital signature providers now feature smart phone and tablet-based apps (iOS, Windows, and Android compatible). Smart phones and tablets also allow mobile access to email,

presentations, quote processing and approval platforms, and invoice submission. Mobile B2B solutions, however, are not limited to apps. Many developers are now incorporating HTML5 (“mobile site”) technology into their internet platform. HTML5 sites do not require purchase, can be accessed over Wi-Fi or 3G/4G, and function like native apps.

b. The Mobile Credit Team in Action

In the U.S., 92% of Fortune 500 companies are either utilizing tablets in day-to-day operations or testing it in preparation for deployment. According to one study, 50% of C-suite execs in the U.S. use at least one tablet device for their daily business activities. A 2010 study by the Yankee Group revealed considerable benefits for companies considering a switch to mobile technology. Based on a 2,400 employee sample, the study found:

1. 28% reported increased field selling time;

2. 27% reported reduced/eliminated redundant activities;

Alternative to Customers Signing on the Web’s Dotted Line (Credit Applications, Guarantees, Security Agreements, and Lien Releases)

continued on page 10

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 2

International Corner

Alice Knight is Vice President of Finance & Administration for Paper Products Marketing, Inc. Ms. Knight has more than 48 year's of experience in International Finance and is an active member of ICTF and NACM. She has served as Co-chair, Panel Member, and Presenter at Annual Global Conferences, and as President of ICTF Forest Products Group.

by Alice Knight, RGCP

Where would you find 140 international credit and trade finance professionals from the United States, Canada, Belgium, Brazil, China, Mexico, Switzerland, and the United Kingdom all together sharing knowledge and experience? The ICTF Global Credit Professionals Symposium at the Fairmont Hotel in Chicago, April 6-8 was the place.

The event started with a welcome reception Sunday evening. From the noise level in the room it was a great success and an excellent opportunity to meet the VIP’s (very important first-time attendees).

Monday morning featured the keynote speaker, Jeffrey Frieden, Stanfield Professor and distinguished author, from Harvard University. Dr. Frieden addressed Lost Decades, Global Debt Crises, Currency Wars, and the Future of Global Cooperation. He emphasized the critical interdependence of our global economy.

This was followed by the ICTF Speed networking session. Each participant was invited to share business cards with at least five people new to them and to share their greatest current challenges. Some people excelled and some ran out of business cards. NOTE – Business cards are a critical component of effective networking. Always be prepared!

Kevin Chandler, Senior Director Credit, Tesoro Companies, Inc., presented "Leveraging Technology to Enhance Credit Decisions and Review Processes, Create Good Quality Controls and Align Policies and Procedures with Company Business Strategy." Imagine the best possible scenario for developing, training, and building an integrated credit environment. It would probably

include total support from top management, friendly access to all areas of the company, dedicated and experienced IT support, innovative technology, and an atmosphere valuing the integration of technology and experienced people. Kevin shared what can be accomplished in such an environment. He noted that technology is a valuable tool and should be used to provide data so that people can work smarter and concentrate on higher value activities. Credit analysis is more than just financial information. Technology helps collect and integrate lots of data so that all the various pieces can be put together. Everyone should be challenged to grow, move out of comfort zones, teach and be taught, and gain respect for the credit profession. The Tesoro system is fed by the Financial Supply Chain Management module of SAP with many in-house modifications. The credit review process is organized around 12 independent areas that are fed internally and externally to roll up to a recommendation and the appropriate approvals. Several people around me, in the same industry as Tesoro, were amazed at the depth of information including a daily auto leveling of family credit limits. This was an outstanding example of what is possible with committed top management support and a credit professional with years of credit and technology experience.

Pamela Krank, President, The Credit Department, Inc., presented ”Beyond the Fundamentals: Anatomy of the Perfect Credit Department.” Pam explained that in their experience credit departments of less than ten people are often more efficient but less effective than larger departments while departments of more than ten people are often more effective and less efficient. Pam defined efficiency

as the best use of available resources and effectiveness as the best result. Larger departments often have greater resources both technological and people. Since top management often focuses on cost it is important that departments concentrate on both efficiency and effectiveness. One step would be to standardize process work flow with an integrated credit policy directing each process. Resources would be allocated based on the potential risk impact on the overall portfolio. Collection activity would focus on default risk and cash flow priorities. Pam recommended the use of credit committees composed of Credit, Finance, Sales, Marketing, and Executive Management to coordinate company expectations and polices. Pam also provided several different techniques for the valuation of the receivable asset including probability of default by category and historical data on bankruptcy/bad debt by category, and types and steps of collection activity.

Next month, I’ll share the balance of the presentations.

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 3

Message from the President

I hope you will join us for the Meet & Greet reception May 8th, at the DoubleTree Lloyd Center, followed by International Business Day on the 9th. Please take a look at the calendar included in this issue and register for these and other events of interest today!

Do you know a company or credit manager who would benefit from NACM Oregon’s training or services and who may not be a member? Please consider providing a referral to us – let your Account Executive or Customer Service know – and we’ll provide this prospective member information about NACM Oregon and our programs, products, and services. Thank you!

Rod Wheeland, CCE, CAE Direct: 971.230.1158 [email protected]

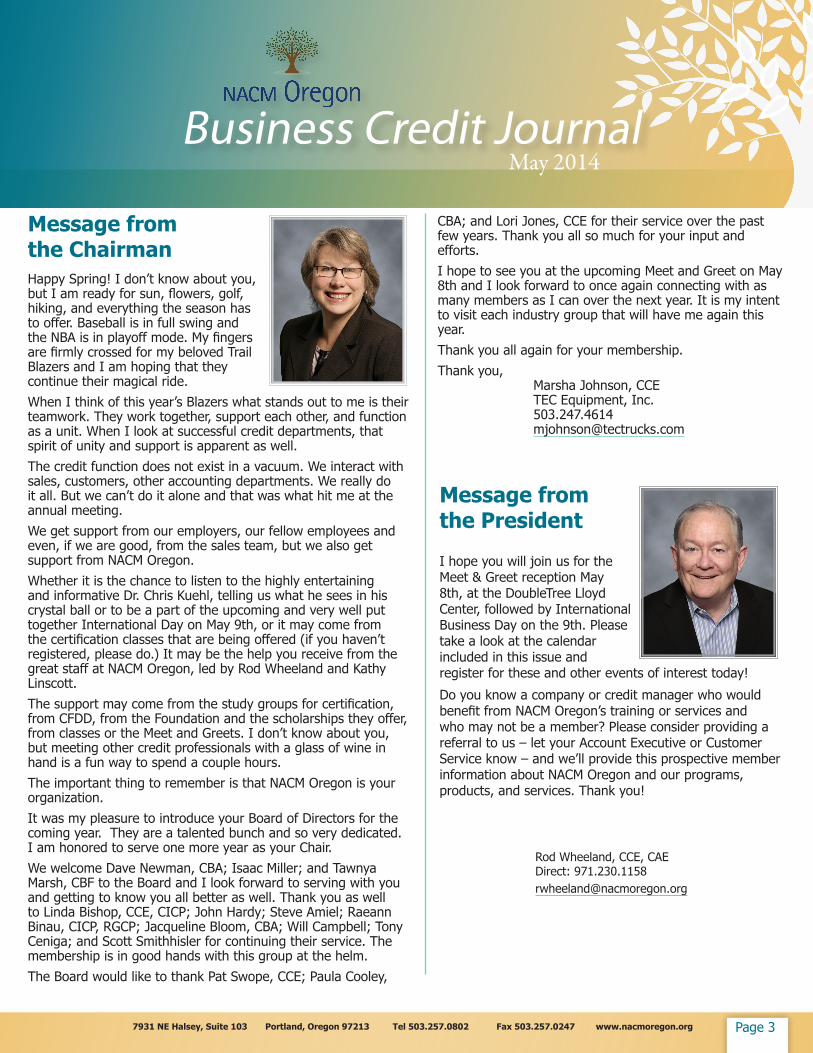

Message from the ChairmanHappy Spring! I don’t know about you, but I am ready for sun, flowers, golf, hiking, and everything the season has to offer. Baseball is in full swing and the NBA is in playoff mode. My fingers are firmly crossed for my beloved Trail Blazers and I am hoping that they continue their magical ride. When I think of this year’s Blazers what stands out to me is their teamwork. They work together, support each other, and function as a unit. When I look at successful credit departments, that spirit of unity and support is apparent as well. The credit function does not exist in a vacuum. We interact with sales, customers, other accounting departments. We really do it all. But we can’t do it alone and that was what hit me at the annual meeting. We get support from our employers, our fellow employees and even, if we are good, from the sales team, but we also get support from NACM Oregon. Whether it is the chance to listen to the highly entertaining and informative Dr. Chris Kuehl, telling us what he sees in his crystal ball or to be a part of the upcoming and very well put together International Day on May 9th, or it may come from the certification classes that are being offered (if you haven’t registered, please do.) It may be the help you receive from the great staff at NACM Oregon, led by Rod Wheeland and Kathy Linscott. The support may come from the study groups for certification, from CFDD, from the Foundation and the scholarships they offer, from classes or the Meet and Greets. I don’t know about you, but meeting other credit professionals with a glass of wine in hand is a fun way to spend a couple hours. The important thing to remember is that NACM Oregon is your organization. It was my pleasure to introduce your Board of Directors for the coming year. They are a talented bunch and so very dedicated. I am honored to serve one more year as your Chair. We welcome Dave Newman, CBA; Isaac Miller; and Tawnya Marsh, CBF to the Board and I look forward to serving with you and getting to know you all better as well. Thank you as well to Linda Bishop, CCE, CICP; John Hardy; Steve Amiel; Raeann Binau, CICP, RGCP; Jacqueline Bloom, CBA; Will Campbell; Tony Ceniga; and Scott Smithhisler for continuing their service. The membership is in good hands with this group at the helm. The Board would like to thank Pat Swope, CCE; Paula Cooley,

CBA; and Lori Jones, CCE for their service over the past few years. Thank you all so much for your input and efforts. I hope to see you at the upcoming Meet and Greet on May 8th and I look forward to once again connecting with as many members as I can over the next year. It is my intent to visit each industry group that will have me again this year. Thank you all again for your membership. Thank you, Marsha Johnson, CCE TEC Equipment, Inc. 503.247.4614 [email protected]

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 4

Questions from the Forum

Member: We are a Retail Store and have many contractors and subcontractors who have accounts with us. I was wondering if there are any laws stating if it is illegal to offer a discount to one customer but not to all of our customers who have accounts with us?

Expert: Unfortunately the response to your question is somewhat complicated. Such practices could result in liability under the federal Robinson-Patman Act (and its Oregon counterpart) that generally prohibit price discrimination between two or more purchasers. The first prong of the test requires an actual difference in the price of similar commodities. The price component means comparing net prices, after all discounts, rebates, etc. In your setting, the mere fact that you offer discounts to one account and not to another generally should not cause issues unless the same product is being sold to each account.

The other prong required for liability is that the price difference results in competitive injury. In other words, the price discrimination must result a reasonable probability that competition will be lessened. This can be a difficult requirement to establish, and largely is dependent on the structure of the industry, whether there are dominant buyers or sellers, etc. The general rule is the larger the universe of potential buyers and sellers for the product, the more difficult it will be to find competitive injury.

To make this area of antitrust law more complicated, there are also a slew of potential exceptions to price discrimination that can avoid any liability. For example, if you are the seller and are being asked to meet a price being offered to one of your accounts by a competitor, then you can match that price (after good faith verification) and not run afoul of the price discrimination laws. If an account purchases a high volume of a certain product, and that enables you to achieve cost savings that you can then pass on to that account, then a lower price will not run afoul of Robinson-Patman.

But the bottom line here is that assuming these accounts do not compete with one another and purchase different goods, there should be no issues. If they are competing and use the same goods purchased from you to compete against each other, then more care should be taken.

As you can see, this can be a complex area of the antitrust laws. Don't hesitate to contact me to explore further.

George J. "Jack" Cooper, partner in the Portland law firm of Dunn, Carney, Allen, Higgins & Tongue, devotes his practice to management representation in antitrust and civil rights-related matters. His practice emphasizes assisting clients in implementing preventative measures in avoidance of claims and litigation. Mr. Cooper received his undergraduate degree from Willamette University and his law degree from Duke University School of Law.

Welcome to a new section of the BCJ-Questions from the Forum. We will list questions and answers we think others can learn from or frequently asked questions. Have a question for other members or experts. Log on to the NACM Oregon Portal. Click here to go to the website.

See article on Robinson-Patman Act page 7

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 5

New Deduction Codes for Electronic Payments

CRF has taken a leadership role in a national effort to convert B2B payments from paper checks to electronic remittance. One major stumbling block in allowing adoption of electronic payments is the lack of detail transmitted with the remittance. As a result, the Remittance Coalition was formed to address the issue of setting standards for transmitting remittance detail and streamlining this process. CRF has taken the lead in representing the interests of Credit and Accounts Receivable departments around the country in an effort to set standards for deduction codes used when processing remittance detail.

It was first suggested that the EDI-820 deduction codes standards be adopted. CRF objected to this as the EDI-820 deduction codes standards encompass nearly 620 deduction codes, many of which are repetitive. The small- to mid-size businesses that don’t have EDI systems to process electronic payment remittance detail would require a standardized process using far fewer codes. The thought was, for example, that 18 separate deduction codes to convey a shortage should be combined into one.

To accomplish this task, CRF formed a committee of experts whose goal was to significantly reduce the number of deduction codes. Through the successful efforts of this group, deductions have now been streamlined into a standard listing of 76 codes. This abbreviated listing is identified as Core Adjustment Reason Codes.

The Core Adjustment Reason Codes were submitted to the Accredited Standards Committee, X9, which is the nationally recognized standards board for financial standards related to commerce and banking in the United States. X9 immediately realized the value of the streamlined set of deduction codes and has adopted them for future use related to non-EDI B2B electronic payment transactions. These codes will be utilized in connection with B2B payments in the future.

CRF proudly presents the Core Adjustment Reason Codes to credit and A/R professionals in preparation for the evolvement of electronic payments in the very near future. To access the code listing click on this link: http://www.crfonline.org/publications/Core-Adjustment-Reason-Codes.pdf

We would also encourage you to download this PDF document and retain it for future reference.

CRF would like to take this opportunity to thank the following CRF members whose efforts made this initiative possible.

Jessica Butler, Attain Consulting Group Kathy Rotondo, IAB Solutions, LLC

Sandra Roth, Johnson & Johnson Sales & Logistics Brad Boe, Performance Food Group

The Credit Research Foundation is pleased to send you the 1st Quarter 2014 CRF News, available in Flipbook format.

Click Here to access the Flipbook.

In this edition:

• Successful training program for credit and accounts receivable employees

• Spring economic projections by nationally acclaimed economist, Mark Zandi

• Venue selection in Bankruptcy cases

• Chapter 9 Bankruptcy Creditors' Committees issues

• Virtual credit cards

• and more

The Flipbook version may be viewed on all Internet devices, including smart phones and tablets. For those readers who can't view Flash on their computers, a PDF version of the CRF News is available for download at this link: http://www.crfonline.org/publications/news.pdf

CRF Quarterly News

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 6

© New York Collection, Joe Dator. All Rights Reserved.

Hubert R. (Hugh) Ayers, Jr., was born May 1, 1925, in Macomb, Oklahoma, to Hubert and Ada (Rutledge) Ayers. He passed away on February 16, 2014.

Hugh grew up in the Texas Panhandle, graduating from Lefors High School in 1942.

He entered the U.S. Army in 1943. While stationed at Fort Sam Houston in San Antonio, he met his future wife, Tillie, and three months later married on February 14, 1946. In 1946, he was discharged as a Staff Sergeant.

Following his discharge, Hugh went to work for Carpenter Paper Company, a wholesale paper distributor. While working, he enrolled in evening classes at Trinity University, San Antonio, Texas. In 1955, he was transferred to Omaha, Nebraska, to establish a credit training program for the many branches of the company. He continued his classes at the University of Omaha. He graduated with a Bachelor Degree in 1960, having earned his degree entirely by attending evening classes.

Subsequent transfers took the family to Portland, Seattle, and Los Angeles. In 1969, he and his family returned to Portland where he and others formed the Carter Rice-Carpenter Co. He was Treasurer, later being promoted to Vice President.

Hugh earned his Certified Credit Executive (CCE) designation from the National Association of Credit Management in 1982 and received the Fellow Award from the National Institute of Credit. He was an active member of NACM Oregon and was elected to the NACM Oregon Board of Directors. He served as Chairman in 1980-81, and served three years as Western Regional Director for the National Association of Credit Management.

He retired in 1983, and he and his wife moved to the Oregon Coast.

He leaves behind his beloved wife, Tillie; daughters, Patricia and Paula; son, Russell; and grandson, Boone. A nephew, David Travis, resides in New Jersey with his family, and one great-granddaughter, Evelynn.

In Memory

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 7

An underlying objective of the United States antitrust laws is to enhance competition in the economic marketplace, with a primary goal of promoting the highest possible quality of goods and services at the lowest possible price.

In the face of these objectives, Congress in 1936 enacted antitrust legislation purportedly designed to assist small businesses by preventing so-called “price discrimination.” Known as the Robinson-Patman Act, this amendment to Section 2 of the Clayton Act remains an enigma within the overall antitrust framework and, to a large extent, is inconsistent with the fundamental principles and objectives of the antitrust laws. Of all the antitrust laws, Robinson-Patman is arguably the least understood.

While the Sherman Act expects that businesses will engage in robust price competition, Robinson-Patman potentially impedes the type of negotiations that would ordinarily lead to market-driven price differences, and further places limits on the ability to undersell a competitor in the normal course of business.

As a threshold matter, Robinson-Patman requires at least two actual and contemporaneous sales of commodities in interstate commerce from a single seller to at least two different purchasers. Note that the Act applies only to tangible products. It does not apply to services or intangible items, such as leases, licenses, advertising, insurance, medical services, etc. However, keep in mind that many state versions of Robinson-Patman, including Oregon, cover intangible goods and services.

To fall within the coverage of the Act, the sales also must be of commodities “of like grade and quality.” Products that are physically and chemically identical have been found to be of like grade and quality, even though they may be labeled differently and may appeal to different consumer segments. On the other hand, competing goods which are physically dissimilar will often not be found to be of like grade and quality. These determinations are highly individualized in nature.

In order to violate the Act, the seller must discriminate in price between the products being sold. The term “price” is generally the amount actually paid for the goods by the buyer; in other words, the invoice price, less any discounts, offsets or allowances. It should be noted that the U.S. Supreme Court has specifically held that payment or credit terms are inseparable parts of price.

Assuming that all of the requirements listed above have been satisfied, the inquiry then shifts to determine whether the pricing practices will result in competitive injury. The Act does not prohibit all price discrimination, but only those practices which have an adverse effect on competition. Just because there are price differences does not automatically mean there is unlawful price “discrimination.” Under the Act, price differences become suspect whenever the effect of those differences may be substantially to lessen competition in any line of

commerce, to create a monopoly, or injury, to destroy, or prevent competition with any person who either grants or knowingly receives the benefit of such price discrimination.

It is also important to note that, generally, the test is not whether the pricing practices have injured a

particular competitor. Rather, it is whether the overall level of competition in a particular market or industry has been impacted. Thus, in a highly fragmented market characterized by many buyers and many sellers, with no true dominate players, it might arguably be difficult (at least under current economic analysis) to establish a violation of Robinson-Patman.

It should also be noted that competitive injury under the Act can take place at various levels within the overall chain of distribution. For example, competitors of a seller engaged in price discrimination may be injured by those pricing practices. Such competitors may be consistently underpriced, and thus lose business because of the price discrimination. There may also be pricing practices that cause competitive injury between the customers of the seller. Generally, a favored customer of a seller is able to pass on a price break to its customers, thus undercutting its competitors. Competitors of such a favored customer are thus likely to lose business as a result of discriminatory pricing.

Reprinted from previous Business Credit Journal

Antitrust: The Robinson-Patman Act

continued on page 8

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 8

Significantly, under Robinson-Patman both the seller engaging in price discrimination and the favored buyer receiving lower prices are potentially liable for monetary damages. This can make life troublesome for a buyer which has successfully negotiated a low price, only to discover later that those ultimate prices are suspect.

There are several broad defenses to the application of Robinson-Patman. For example, the so-called “quantity discount” defense provides that pricing practices based upon differences in the cost of manufacture, sale, or delivery resulting from quantity purchasing, may not violate the Act. This defense has been narrowly construed by the courts. In order to fall within this safe harbor, price differentials should be justified by concrete and specific evidence of cost savings resulting from high quantity orders. There should be mathematical specificity and cost accounting certainty which can justify a lower price. Such precise price justifications of economies of scale can be difficult to achieve.

It is also permissible for a seller to have different pricing structures based upon the distributive services performed by downstream buyers. For example, because most wholesalers undertake certain functions in the distribution chain that are otherwise generally performed by a manufacturer, certain functional discounts are appropriate. Thus, it is generally permissible to charge different (lower) prices to wholesalers than to retailers to account for these distribution services.

The Act also permits a seller to “lower” its price to meet an equally low price being offered by a competitor. In

order to qualify for this “meeting competition” defense, a seller must be able to establish that it has lowered its price in good faith in order to remain competitive. It is generally recommended that a seller take reasonable steps to confirm and verify that the other lower price has been quoted, and to document such verification. Keep in mind that the defense generally permits “meeting” competition, not “beating” a competitor’s lower price.

Sellers must be careful, however, in this verification process. For example, it is permissible for a seller to ask its buyer for evidence of a lower price quote from a competitor. However, a seller should never make such inquiry of the competitor who presumably has offered the lower price. This could be construed as a preamble to price fixing, thus a potential violation of the Sherman Act.

The Act also includes a defense for price differences resulting from so-called “changing conditions.” The primary purpose of this defense is to permit a seller to dispose of goods where economic losses are imminent because of deterioration or perishability, obsolescence, distress sales, etc. Thus, price differences in products as a result of technological obsolescence fall within this defense, as do perishable fresh foods and seasonable goods.

In addition to price discrimination, Robinson-Patman also makes it unlawful for a seller or buyer to give or receive compensation for placing or obtaining an order for the purchase or sale of goods. The Act further prohibits payments by sellers to buyers for the performance of advertising

services, unless such payments are made available to all buyers on proportionately equal terms.

This article has attempted to present a general overview of a complex statutory scheme. Compliance with the Robinson-Patman Act can be difficult. As noted above, there are several potentially broad exceptions and defenses to the Act; however, these are narrowly construed, and may not always be available. Consulting with antitrust counsel on all these issues is strongly recommended.

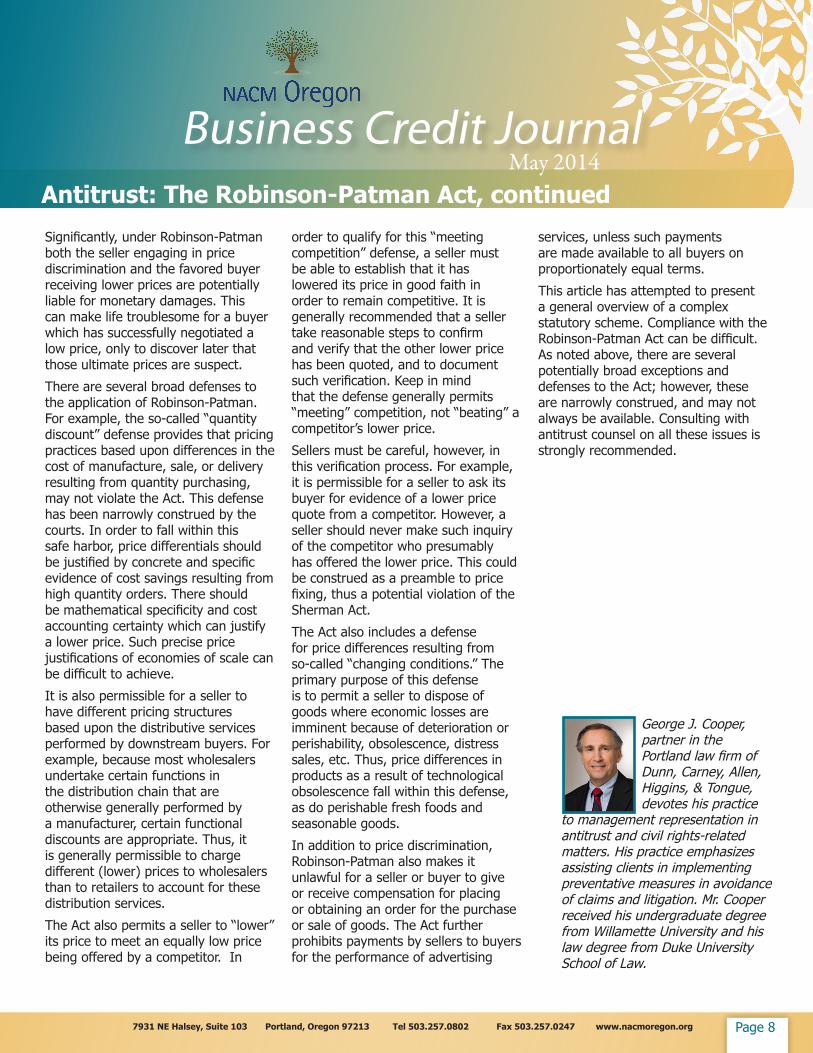

George J. Cooper, partner in the Portland law firm of Dunn, Carney, Allen, Higgins, & Tongue, devotes his practice

to management representation in antitrust and civil rights-related matters. His practice emphasizes assisting clients in implementing preventative measures in avoidance of claims and litigation. Mr. Cooper received his undergraduate degree from Willamette University and his law degree from Duke University School of Law.

Antitrust: The Robinson-Patman Act, continued

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 9

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 10

3. 26% reported increased win rates;

4. 25% reported redeuced cost of sales calls;

5. 25% reported increased forecast accuracy;

6. 24% reported decreased administrative time;

7. 23% reported decreased sales cycle time.

The tablet market continues to grow. Research firm IDC predicts that shipments of tablet computers will reach 84.1 million in this year’s fourth quarter and, by 2015, will overtake PC sales. Until recently, tablets have been a predominantly consumer-based product. Tablet producers, such as Microsoft, however, are now specifically gearing their tablet products for the B2B setting.

II. Digital Signatures: Understanding the Laws, the Risks, and the Benefits

a. The ESIGN Act

The Electronic Signatures in Global and National Commerce Act (ESIGN), a federal law applicable in all states, recognizes that digital signatures have the same force as their ink-and-paper counterparts. Under the ESIGN Act, an electronic signature is defined as the technology used to verify a party’s identity and certify contracts that are agreed to over the Internet. For vendors, some of the most important provisions of The ESIGN Act include: (1) parties to the contract decide on the form of digital signature technology used to validate the contract; (2) vendors may use e-signatures on checks; (3) vendors must require parties to the contract to make at least two clicks of a computer to complete a transaction and (4) records of e-contracts may be stored electronically.

b. Digital Signatures and the Documentation Process

Since the ESIGN Act passed, companies are turning to third-party digital signature solutions to facilitate the exchange of contracts, documents, and other materials. Through digital signature services, these companies have eliminated the delays associated with the processing and approving of pen-and-paper

supply contracts. With digital signature software, such as DocuSign, the initiating party can send their to-be-signed documents onto the secure, cloud-based server, where tags are inserted to

indicate where signatures are needed. The document can then be sent via email to the requisite parties and DocuSign walks the signer through the process. Once all the fields are signed, the customer selects the confirmation option and a notification is sent to all attached parties on the document/contract.

Article 2 of the Uniform Commercial Code provides that with the sale of goods over $500, there must be a signed writing. A signature is to certify the writing for the sale of goods. Traditionally, the credit team memorializes such a sale agreement with a signed credit application. Before digital signatures, this required the customer to download the application from the vendor’s webpage, fill it out by hand, and then email or fax the completed credit application with the pen-and-ink signature back to the vendor. The traditional process is undeniably time-consuming. With electronic signatures, however, credit applications completed electronically and sealed with an e-signature bind the customers to the terms and conditions of the credit application. The credit team may also receive completed guarantees, security agreements, and lien releases in the same manner and form a binding contract.

Mobile Devices Provide the Credit (and Sales) Team AnotherAlternative to Customers Signing on the Web’s Dotted Line (Credit Applications, Guarantees, Security Agreements, and Lien Releases) (continued from cover)

continued on page 11

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 11

Excel Tips & TricksMake your workflow faster and easier with these little tips and shortcuts when using Excel.

• Need to undo or reverse an action: Ctrl + Z

• Repeat any action (as long as it has not been undone): Ctrl + Y

• Bold: Ctrl + B

• Italic: Ctrl + I

• Underline: Ctrl + U

• Strikethrough (example): Ctrl + 5

• New Line Same Cell: Alt + Enter

• Find and Replace: Ctrl + F (Wildcards: ?,*,~)

» SHIFT+F5 also displays this tab, while SHIFT+F4 repeats the last Find action.

» CTRL+SHIFT+F opens the Format Cells dialog box with the Font tab selected.

Mobile Devices Provide the Credit (and Sales) Team AnotherAlternative to Customers Signing on the Web’s Dotted Line (Credit Applications, Guarantees, Security Agreements, and Lien Releases) (continued from page 10)

c. Can Documents Sealed by Electronic Signature Be Trusted?

While this technology streamlines the documentation process, it raises concerns over the validity and enforceability of the customer’s signature. How can a vendor ensure the identity of the signer? Can a customer dispute the enforceability of the terms and conditions of a document signed by electronic signature? Will an electronic signature stand up in court? Using several different levels of authentication, third-party signature services allow for verification of signer identity and document validity. These signature services also provide an audit trail tracking the entire signing process. The audit trail includes: a record of all parties involved, the locations where documents were sent (i.e. IP addresses), the locations where documents were

opened, the amount of time the documents were open, the precise time and location of signatures. Further, these signature services feature anti-tampering software to ensure the authenticity and originality of the document through all stages of the signing process.

Scott Blakeley is a principal with Blakeley & Blakeley LLP,where he practices creditors’ rights and bankruptcy. Hisemail is [email protected].

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 12

Joanne Swyers began her career in credit management as many do - far away from credit management. Swyers had just started as the inside sales manager at Vancouver Extrusion, an Alcoa subsidiary in Vancouver, WA, when the company president asked her to establish a sales-oriented credit department.

Six months into her new job, Joanne’s adventure in credit had begun.

As the new credit manager of the new credit department Swyers was connected with an experienced credit manager in California who became a mentor. As Swyers remembers it, the last piece of advice he passed on was “Join NACM and go to every educational class you can and every networking opportunity you can and you will be prepared for everything that comes your way.”

Seeking out new opportunities and professional challenges has been a consistent theme in Joanne’s career. When it came time to move on from Vancouver Extrusion, Swyers found a position at Miller Paint as their Corporate Credit Manager.

She left her credit department in the capable hands of Elese Clausen, a Personnel-turned-Credit Manager. Swyers and Clausen stayed in contact and became friends over the years.

At Miller Swyers was once again looking for her next professional challenge. Thinking, as many do, that education usually comes in the form of a degree, she was considering graduate programs.

It was in talking things over with Clausen that the option of Credit Executive certification arose. The idea sounded good to Swyers, who received the CCE certification during her tenure at Miller Paint.

“It’s a good program,” Swyers says. “It was as hard as getting a Bachelor’s degree and has substance behind it.”

As beneficial as her new certification was at Miller, much of the credit management tools went unused due to the unsubstantial, unsecured credit lines typically found with paint contractors.

There was one exception.

To help increase the Miller Paint dealers’ inventory - and therefore their capacity to sell - Swyers helped established Purchase Money Security Agreements. These contracts had

never been tried before at Miller and Swyers turned it into a powerful internal tool.

The next adventure in credit management began when a recruiter connected Swyers with Shelter Products, a national building supply distributor. “It was a growth step I wanted to take,” she says.

At Shelter Swyers looked forward to working at a national company and managing lien-secured debt. Her certified credit expertise and NACM contacts would come in handy. Promoted from Credit Manager to Director of Credit, she was surprised when Shelter suddenly hired a salesperson making deals in Mexico and the Caribbean.

“[We] went into international credit overnight,” Swyers says.

Swyers reached out to her NACM contacts and had account receivable insurance set up within weeks. All while a sales rep was actively making deals. Of the lessons learned during that hectic time, Joanne puts it best: “Never underestimate the value of networking.”

As much of a professional growth opportunity Shelter Products was, Swyers eventually felt ready for the next challenge, and joined two former colleagues at Bridgewell Resources in Tigard, OR.

Key to Success

Joanne Swyers, CCE, Bridgewell Resources

continued on page 13

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 13

Though she worked in Bridgewell’s credit department, Swyers was hired to support Contractor Direct, a brand new division. Swyers was, once again, breaking new ground at an established company. “It has been very exciting,” she says.

Contractor Direct began operations in March 2011 with zero in sales. Swyers joined the team months later. They closed the first year with $16 million in sales and quintupled sales their second year. This year they are projected to book more than $100 million in sales.

Every sale requires an extension of credit. “It’s intense,” says Swyers. “Every job goes through my desk.”

It’s been the job she was preparing for.

To manage the credit needed to meet the sales volume in Contractor Direct, Swyers must keep track of lien laws in twenty-nine states. From there it gets more complicated. To extend the level of credit needed for each order, Swyers must investigate the job, credit banker, owner, general contractor, and subcontractor. She must make ensure, as best she can, that all parties are “free of liens and with the experience to do the job.”

To effectively manage her division’s credit, Swyers points out that it’s the support she gets from Bridgewell’s credit department and the continuing education that started with her Credit Executive certification. “I originally learned about lien laws through NACM’s continuing eduction,” Swyers says. “Their ongoing education has been a base for juggling the needs of all my jobs.”

The success of her division has Joanne, once again, looking for the next professional challenge. “I think it’s my continual need for growth,” Swyers says, in describing the motivation for moving on. She’s looking forward to the challenges her new position as Senior Credit & Collections Manager at Solar World in Hillsboro, OR will bring.

Looking back on picking the CCE over a Masters degree, Swyers has no regrets. “If I went back to school to get my Masters, it would just be because I am driven and I love to keep learning,” she says. “That, too, is why the CCE is such a good investment. The ongoing education keeps you up to date and continually learning.”

Jake Faris is a business technology consultant and sometimes-freelance writer who lives in the Portland area with his wife, Charity, and their two children, Harper and Xavier.

Key to Success, continued

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 14

We hope to see you at one or more of the following meetings.

CFDD Portland Chapter Meeting

Program: "Installation of Officers and Board of Directors and International Business" Date: Thursday, May 8, 2014Time: 6:30 p.m. (following Meet & Greet)Location: Doubletree Hotel Portland1000 NE Multnomah St., Portland, Oregon

Our monthly meeting will be at the DoubleTree in conjunction with NACM’s International Meet & Greet. After the Meet & Greet we will move to a private room for our meeting and installation. Our speaker for the evening will be Paul Beretz. All attendees at the Meet & Greet will be invited to join us for the presentation and installation. There will be no charge for this meeting.

International Meet & Greet May 8, 2014 5 - 6:15 p.m. The Multnomah Grille Doubletree Hotel Portland 1000 NE Multnomah St.Portland, Oregon

Please join us for hors d'oeuvres wine & beer. The Meet & Greet is free to the members. Free parking is available.

Meet & Greet - Eugene May 22, 2014Location:Hop Valley Brewery990 W 1st AveEugene, OR 97402

In-House Class Schedule

International Business Day May 9, 2014 8 a.m. - 4 p.m.Doubletree Hotel Portland 1000 NE Multnomah, Portland, OregonSpeakers: Courtney Seelinger, Dr. Christopher Kuehl, Paul Beretz, Romelio Hernandez & more

Cost: Members - $225 each; $175 per additional registrant from the same company;Nonmembers - $325 each

Oregon & Washington Lien Law ClassJune 5, 20147:30 a.m. - 4 p.m.NACM Oregon Classroom 7931 NE Halsey, Suite 201, Portland, Oregon 97213

Cost: Members - $145 each; Nonmembers - $225 each

International Business Series June 12- October 16, 2014 (Thursdays) 8 - 10 a.m. NACM Oregon Classroom 7931 NE Halsey, Suite 201, Portland, Oregon 97213 Instructors: Jean Boudreau; Ken Carraro; Raeann Binau CICP, RGCP; Scott Smithhisler

Cost: Members - $45 each; Nonmembers - $75 each

Basic Accounting September 10 - November 21, 2014 (Wednesdays) 1 - 4:30 p.m. NACM Oregon Classroom 7931 NE Halsey, Suite 201, Portland, Oregon Instructor: TBA

Cost: Members - $345 each; Nonmembers - $545 each

Mark your calendars for these exciting events!

Registration

Visit www.nacmoregon.org/events to register online. If you have any questions regarding these classes, please call Shawna Kelly at 971.230.1202 or email [email protected].

Meet & Greet - Salem June 17, 2014Location: TBA

Membership Breakfast October 14, 2014 7:30 - 9 a.m. Location: TBA Speaker: John Mitchell

Watch your mail for more details!

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 15

• Western Regional Conference

October 15-17, 2014, Las Vegas, Nevada

One (1), $500 scholarship

Deadline: August 31, 2014

• CFDD National Conference

September 18-19, 2014, DoubleTree Bloomington - Minneapolis South, Minneapolis (Bloomington), Minnesota

Two (2), $500 scholarships

Deadline: August 31, 2014

• Professional Certification Fees

$2,000 for certifications fees. Application must include an acknowledgement letter from NACM National.

$2,000 for certification classes fees. Applicant must include letter of completion and grade from the respective instructor and cost of the class. No funds available for texts.

• NACM Oregon International Seminars

$2,000 to support NACM Oregon International seminars. Request can be for the International Day Seminar, May 9, 2014; International Credit individual sessions.

To Apply or for question contact:

Lourdes (Lou) A. Rice NOF Scholarship Chair

Pacific Metal Co. 10700 SW Manhasset Dr. Tualatin, Oregon 97062

p: 503.454.1051

f: 503.454.1065

NACM-Oregon Foundation Scholarships

The NACM-Oregon Foundation (NOF) is an independent, public benefit, nonprofit organization that provides scholarship opportunities to credit professionals to assist them in the pursuit of education and training, to achieve professional designation, and to attend national and regional programs and conferences.

In the spirit of sharing the wealth of scholarships, the NOF is providing financial assistance to eligible applicants. These scholarships are only available to NACM Oregon members. Nonmembers are not eligible for these or any other scholarships offered by the NOF.

NOF has established the following eligibility requirements and cooperates with other organizations (NACM National, CFDD National, and the CFDD Portland and Salem/Albany Chapters) to avoid double awards.

The NOF is offering the following scholarships in 2014:

• One scholarship per person per year from any one category.

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 16

Training Tips for Collectors

The majority of outstanding collectors are trained to be effective communicators, negotiators, and problem-solvers. The trouble with on-the-job training for collectors is that it is usually unplanned and unsupervised. As a result, new collectors learn by trial and error. Errors can be serious, and they can easily be avoided by developing a training program for all new collectors. The goal of any training program is to make the new employee as productive as possible as quickly as possible. A formal training program has a much higher success rate than an informal program, or worse, on-the-job training and in particular any type of training that essentially involves the sink or swim method of new employee training and performance evaluation.

Unfortunately, some collectors do not learn, or do not learn enough, or do not learn quickly enough from their experience. It has been said about many collectors that rather than having ten years of experience, their performance suggests that they have one year of experience repeated ten times. Collectors need to learn from their mistakes, and from others. Credit managers need to develop a formal training process, and encourage informal discussions among collectors. These discussions can be a valuable source of new collection ideas, and should be actively encouraged rather than discouraged. I suggest that the outline of any training process is this three-step process:

1. Watch while I do the work and explain it to you,

2. Watch while they perform the task,

3. When they are fully competent, the task is theirs.

© 2012. Michael C. Dennis. All Rights Reserved. Michael has been training credit and collection teams for more than 10 years.

Click here to sign up!

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 17

NACM National News

2014 Credit Congress & exposition

Join us at the Rosen Shingle Creek Resort

June 8-11, 2014, Orlando, Florida,

for the year’s largest gathering of business credit

professionals in the country. For more information go to

http://creditcongress.nacm.org/.

June 16-20, 2014

GSCFM International delves into complex global issues facing credit and financial management executives throughout the world.

Participants have the unique chance to network with students in the GSCFM program running concurrently with the GSCFMI.

Click here to learn more about

June 16-26, 2014

& June 22-July 2, 2015

GSCFM is an intensive program providing a foundation in disciplines, such as financial analysis, valuation, business economics, business law, corporate strategy, ethics and treasury management.

Click here to learn more about GSCFM.

Survey DatesCredit Manager’s IndexThe CMI is created from a monthly survey of U.S. credit and collections professionals. The survey asks participants to rate whether factors in their monthly business cycle—such as sales, new credit applications, accounts placed for collections, dollar amount beyond terms—are higher than, lower than, or same as the previous month. The results reflect the entire cycle of commercial business transactions, providing an accurate, predictive benchmarking tool.

CMI reports are released to the media the last business day of each month.

All credit and collections professionals are invited to take the survey each month. NACM membership is not required.

To sign up to receive monthly email reminders to take the survey click here.

2014 CMi tiMeline survey opens survey Closes

May Mon, May 19 Fri, May 23

June Mon, June 16 Fri, June 20

July Mon, July 21 Fri, July 25

August Mon, August 18 Fri, August 22

September Mon, September 22 Fri, September 26 (noon)

October Mon, October 20 Fri, October 26

November Mon, November 17 Fri, November 21 (noon)

December Mon, December 15 Fri, December 19

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 18

Credit Learning Center

Don’t forget to take advantage of your two, complimentary webinars which are included in your Full, Premium, or Corporate Membership Package.

To view the Event Calendar go to http://www.nacm.org/event-calendar.html.

NACM Event CalendarDescription coming soon on the following classes

Teleconference: Emerging Trends for Small/Mid-Market Credit Departments: Credit May 5, 12 - 1 p.m. PDT

Webinar: Liens and Bonds—Taking Advantage of Your Rights to Avoid Write-offs and Sell More May 7, 12 - 1 p.m. PDT

Webinar: The Target Data Breach: Lessons LearnedMay 14, 12 - 1 p.m. PDT

Teleconference: Preference Defense Toolkit May 21, 12 - 1:30 p.m. PDT

Webinar: Bankruptcy for Beginners (Day 1)July 14, 12 - 1:00 p.m PDT

Webinar: Bankruptcy for Beginners (Day 2) July 16, 12 - 1:00 p.m PDT

Webinar: UCCs—The Financial and Psychological Advantages of Being a Secured CreditorJuly 23, 12 -1 p.m. PDT

Webinar: Buried by Paper: A Creditor’s Guide to Making Sense of the Mountains of Papers Received in the Mail in a Chapter 11 CaseAugust 4, 12 - 1 p.m. PDT

NACM Event Calendar, continuedWebinar: Are You Perfected? Perfecting Your UCC Lien Rights to Ensure You Are PaidAugust 6, 12 - 1 p.m. PDT

Webinar: You Asked for It; You Got It…NOW, What Do You Do with That Financial Statement? Part IAugust 11, 12 - 1 p.m. PDT

Webinar: You Asked for It; You Got It…NOW, What Do You Do with That Financial Statement?Part IIAugust 13, 12 - 1 p.m. PDT

Teleconference: Commercial Credit Scoring Models: Pros, Cons and Legal ConsiderationsAugust 18, 12 - 1 p.m. PDT

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 19

It seems that no two companies are alike when it comes to actually setting a customer's credit limit, but doing so is often more art than science. Here are some factors and strategies companies consider when they tell their buyers just how much in the way of goods or services they can borrow.

-Payment Record: This works when the customer in question actually has a payment history with your company. Pay on time or early and the credit limit goes up. Pay late, or not at all, and a credit review process is triggered. This is a sales department's favorite method for setting credit limits because it incentivizes buyers that pay better to buy more.

-Competition: If your competitors are offering x amount of dollars then it behooves your company to offer something similar, lest a lower limit box your company out of potential sales. This is a difficult factor to evaluate if your company is much smaller or larger than your competitors, or if it plays a different role than other suppliers.

-Security: The presence of lien rights in certain transactions makes it a lot easier to set higher credit limits.

-Payment Performance: Often effective when the company has a conservative risk appetite but is looking to take on new customers, this basically starts new buyers with little in the way of payment history off with a lower credit limit, but rewards them as they pay. Sales is less of a fan of this philosophy, because it slows sales growth.

-Period of Time: A method wherein the amount a customer can purchase over a designated period of time, be it a week or a month or otherwise, cannot exceed the established credit limit. This can speed up the order approval process since anything that fits within the given credit threshold can be approved.

-Agency Rating: Companies can create a matrix wherein a certain agency rating on a credit report garners a specific credit limit.

-By Formula: When setting a credit limit companies can take into account a number of different calculations that suit their specific needs and then establish a way to combine them, divide them, and then average them to set a credit limit. This depends on data availability though, as some of the more important figures on a new customer might not be available. Companies that use a formula also tend to rely on it as a preliminary tool that's then extrapolated using other methods into an actual appropriate credit limit.

-Expectation of Use: This method takes the expected dollar volume of credit sales over a period of time and then divides it by the number of expected orders over the course of the same period, and the result is used as a basis for a preliminary credit limit estimate.

-Collection: Like a secured investment with slightly less security, the more confident a company is that any receivable is able to be collected, the easier it is to set higher limits since whatever sales are made are expected to be collected.

Source: NACM-National

Credit Basics: Setting Credit Limits

Business Credit JournalMay 2014

7931 NE Halsey, Suite 103 Portland, Oregon 97213 Tel 503.257.0802 Fax 503.257.0247 www.nacmoregon.org

Page 20

Board of Directors NACM Oregon

ChairmanMarsha Johnson, CCE TEC Equipment, Inc. [email protected]

Secretary - Treasurer Linda Bishop, CCE, ICCE Tektronix, Inc. [email protected]

CounselorJohn Hardy Emerson Hardwood Co. [email protected]

PresidentRod Wheeland, CCE, CAENACM [email protected]

Directors Steve Amiel Tektronix, [email protected]

Raeann Binau, ICCE, RGCP Columbia Machine, Inc. [email protected]

Jacqueline Bloom, CBA Wright Business [email protected]

Will Campbell Standard Supply [email protected]

Tony Ceniga Industrial Finishes & [email protected]

Tawnya Marsh, CBAColumbia River Knife & [email protected]

Isaac MillerFood Services of [email protected]

Dave Newman, [email protected]

Scott Smithhisler US Bank Global Trade Service [email protected]

NACM National Director Rick Weisman, CCE Graybar Electric Co., Inc. [email protected]

Customer Service/ Credit Reporting971.230.1220 [email protected]

Data ContributionShannon Abnal, CGA 971.230.1166 [email protected]

Member Services Kathy Linscott, CGA 971.230.1164 [email protected]

Member Services Account Executives Clara Nemeth, CGA, [email protected] Kendall Sun 971.230.1178 [email protected]

National Account Executive Caroline Anderson, CGA 971.230.1168 [email protected]

EducationShawna Kelly [email protected]

Industry GroupsRichard Browning, CGA 971.230.1188 [email protected]

Kristen McBride, CGA 971.230.1176 [email protected]

Collection ServicesDennis [email protected]

Marc [email protected]

BillingMarmie Carpenter971.230.1146 [email protected]

Meeting Room RentalShawna [email protected]

Newsletter EditorAmanda Garrick971.230.1172 [email protected]

Building Suites Lisa Rogstad971.230.1160 [email protected]

Contacts