namibia swaziland - iuj.ac.jp filethe economist intelligence unit the economist intelligence unit is...

TRANSCRIPT

COUNTRY REPORT

1st quarter 2000

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

Namibia

SwazilandThe full publishing schedule for Country Reports is nowavailable on our website at http://www.eiu.com/schedule.

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through subscription products ranging from newsletters toannual reference works; through specific research reports, whether for general release or for particularclients; through electronic publishing; and by organising conferences and roundtables. The firm is amember of The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1000Fax: (44.20) 7499 9767E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

Hong KongThe Economist Intelligence Unit25/F, Dah Sing Financial Centre108 Gloucester RoadWanchaiHong KongTel: (852) 2802 7288Fax: (852) 2802 7638E-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryEIU ElectronicNew York: Lou Celi or Lisa Hennessey Tel: (1.212) 554 0600 Fax: (1.212) 586 0248London: Jeremy Eagle Tel: (44.20) 7830 1183 Fax: (44.20) 7830 1023

This publication is available on the following electronic and other media:

Online databases

FT Profile (UK)Tel: (44.20) 7825 8000

DIALOG (US)Tel: (1.415) 254 7000

LEXIS-NEXIS (US)Tel: (1.800) 227 4908

M.A.I.D/Profound (UK)Tel: (44.20) 7930 6900

NewsEdge Corporation (US)Tel: (1.718) 229 3000

CD-ROM

The Dialog Corporation (US)SilverPlatter (US)

Microfilm

World Microfilms Publications(UK)Tel: (44.20) 7266 2202

Copyright© 1999 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

ISSN 1356-4218

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Contents

3 Summary

Namibia

5 Political structure

6 Economic structure

7 Outlook for 2000-01

11 The political scene

15 Economic policy

17 The domestic economy

17 Economic trends

18 Mining

20 Agriculture

20 Financial services

21 Infrastructure and other services

23 Foreign trade and payments

Swaziland

26 Political structure

27 Economic structure

28 Outlook for 2000-01

30 The political scene

32 Economic policy and the economy

36 Quarterly indicators and trade data

List of tables

7 Namibia: forecast summary

11 Namibia: presidential election results, 1999

12 Namibia: legislative election results, 1999

13 Namibia: notable retiring SWAPO officials

14 Namibia: Corruption Perception Index, selected countries, 1999

18 Namibia: consumer and food price inflation, 1999

19 Namibia: uranium oxide production, Jan-Sep

20 Namibia: total allowable catches, selected species

21 Namibia: stock exchange statistics, 1999

24 Namibia: exports of goods and services

25 Namibia: fish exports to Spain

33 Swaziland: foreign direct investment stocks by type

2

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

33 Swaziland: foreign direct investment stocks by sector, 1998

35 Swaziland: railway statistics

36 Namibia: quarterly indicators of economic activity

36 Swaziland: quarterly indicators of economic activity

37 Namibia and Swaziland: UK trade

List of figures

10 Namibia: gross domestic product

10 Namibia: real exchange rates

12 Namibia: SWAPO’s electoral strength

17 Namibia: real GDP growth

18 Namibia: inflation, 1999

3

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Summary

1st quarter 2000

Namibia

The re-election of President Sam Nujoma will turn attention to the successionbattle. The ruling SWAPO is likely to face a more formidable opposition inparliament, but may also find it difficult to meet its campaign promises totackle poverty and create jobs. Real GDP growth is forecast to improve from 3%in 1999 to 4.5% in 2000 and to 5% in 2001 on the back of higher output forthe fishing and offshore diamond sectors. The current-account surplus willwiden in 2000, owing to higher fish and diamond exports, before narrowingagain in 2001. Late note: Following the decision by Namibia to allowAngolan troops to operate on Namibian soil in their efforts to quash rebels ofthe União Nacional para a Independência Total de Angola (UNITA), severalheavy clashes have been reported, including, possibly, direct engagementbetween Namibian and UNITA forces.

Sam Nujoma has been overwhelmingly re-elected president with 77% of thevote. Ben Ulenga, of the newly formed Congress of Democrats, has won only11%, edging out Katuutire Kaura of the DTA for second place. SWAPO has alsoretained its two-thirds majority in parliament, taking 55 of the NationalAssembly’s 72 seats—two more than it held previously. The elections havepassed peacefully, but some questions about the voter roll have emerged. Theissue of corruption has been raised by the release of a new study.

The Ministry of Finance has announced that an additional budget will beintroduced in January, but its contents remain controversial. VAT legislationhas been introduced. The central bank has confirmed that Namibia will remainwithin the CMA. The EPZ programme has been criticised.

• Real GDP is estimated to have grown by about 3% in 1999. Inflation hasremained subdued, with the headline rate at 8% in September.

• Namco has continued to report strong growth. Uranium output has fallenagain. Tsumeb Corporation is to be sold off by tender.

• Hake and mackerel catch ceilings have been raised for 2000.

• The Namibia Stock Exchange has continued to record gains, with thedomestic market index up by 33% between January and November.

• A decision on the Epupa dam project has been delayed. Air Namibia hasacquired a new Boeing 747. A new rail link to Angola has begun.

New export data for 1998 have been released, showing a downward revision fordiamond revenue. Fish exports to Spain soared in 1993-97.

December 10th 1999

Outlook for 2000-01

The political scene

Economic policy

The domestic economy

Foreign trade andpayments

4

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Swaziland

A cabinet reshuffle is due after the Incwala recess ends in late January. Moredelays on constitutional reform can be expected. The issue of corruption islikely to be prominent because of an investigation into the minister of finance.The declining influence of the queen mother may indicate a change in themonarchy’s balance of power. Legislative action on several key policy issueswill be slow. The EU-South Africa trade accord will not have a serious impacton Swaziland for several years. Economic growth is expected to improve, butemployment prospects are poor.

The report of the Constitutional Review Commission has been delayed again,causing it to lose financial support from the EU. Cabinet members have beenfined by the king for failing to perform adequately. A bomb has exploded inMahlanya. The editor of a local newspaper has been dismissed for criticising theking’s new wife. The Swazi National Council has intervened in a business deal.

The Central Bank has completed its review of the economy, showing that realGDP growth fell to 2.3% in 1998/99 from 3.7% in 1997/98. Stocks of foreigndirect investment grew by 17% in 1998. The rate of inflation fell to 4.7% inOctober. The cabinet has approved a lower corporate tax rate for selectedsectors. A national tourism bill has been passed. Havelock asbestos mine hasannounced plans to downsize. Swaziland Railway has reported modest growth.

Editor: Todd MossAll queries: Tel: (44.20) 7830 1007 Fax: (44.20) 7830 1023

Next report: Our next Country Report will be published in April

Outlook for 2000-01

The political scene

Economic policy andthe economy

Namibia 5

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Namibia

Political structure

Republic of Namibia

Unitary republic

Based on the constitution of 1990 and Roman-Dutch law

Bicameral; National Assembly, with 72 members elected by universal suffrage andserving a six-year term; National Council, established in 1993, with limited powers ofreview, and 26 members nominated by 13 regional councils for a five-year term

December 1999 (legislative and presidential); next elections due in 2004

President, currently Sam Nujoma, elected by universal suffrage. A constitutionalamendment allowed Mr Nujoma to stand for a third presidential term in 1999

President and his appointed cabinet; last reshuffle December 1997; a new cabinet isexpected to be announced in March

South West African Peoples’ Organisation (SWAPO), the ruling party; Congress ofDemocrats (CoD); Democratic Turnhalle Alliance of Namibia (DTA); United DemocraticFront (UDF); Democratic Coalition of Namibia (DCN); South West African NationalUnion (SWANU)

Hage Geingob

Agriculture, water & rural development Helmut AngulaBasic education & culture John MutorwaDefence Erikki NghimtinaEnvironment & tourism Philemon MalimaFinance Nangolo MbumbaFisheries & marine resources Abrahim IyamboForeign affairs Theo-Ben GurirabHealth & social services Libertina AmathilaHome affairs Jerry EkandjoInformation & broadcasting Ben AmathilaJustice Ngarikutuke TjiriangeLabour Andimba Toivo ya ToivoLands & resettlement Pendukeni IthanaMines & energy Jesaya NyamuMinister without portfolio Hifikepunye PohambaPresidential political adviser Kanana HishoonoRegional/local government & housing Nicky IyamboSpecial adviser for economic affairs Gerhard “Gert” HanekomSpecial adviser for security affairs Peter TsheehamaTrade & industry Hidipo HamutenyaWorks, transport & communications Oscar “Hampie” Plichta

Tom Alweendo

Official name

Form of state

Legal system

National legislature

National elections

Head of state

National government

Main political parties

Prime minister

Key ministers

Central bank governor

6 Namibia

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Economic structure

Latest available figures

Economic indicators 1995 1996 1997 1998 1999a

GDP at market pricesb (N$ m) 11,694 13,421 14,901 16,826 18,507

Real GDP growthb (%) 3.7 2.1 2.6 2.4 3.0

Consumer price inflationc (av; %) 10.0 8.0 8.8 6.2 8.5

Populationd (m) 1.54 1.58 1.61 1.64 1.67

Exports fob (US$ m) 1,418 1,404 1,343 1,278 1,400

Imports fob (US$ m) 1,548 1,531 1,615 1,451 1,500

Current-account balance (US$ m) 176 116 90 162 190

Total external debt (US$ m) 380 308 144 139a 159

Diamond production (‘000 carats) 1,385 1,402 1,416 1,440 1,550

Uranium oxide production (tonnes) 2,378 2,886 3,425 3,257 3,095

Fish catch (‘000 tonnes) 562 494 517 580a 620

International reserves (US$ m) 220.9 193.8 250.5 260.2 270.0

Exchange ratee (av; N$:US$) 3.63 4.30 4.61 5.53 6.08

December 10th 1999 N$6.13:US$1

Origins of gross domestic product 1998 % of total Components of gross domestic product 1998 % of total

Agriculture & fishing 12.2 Private consumption 58.5

Mining & quarrying 12.6 Government consumption 31.5

Manufacturing (incl fish processing) 16.3 Gross domestic fixed investment 18.1

Wholesale & retail trade 7.4 Change in stocks 1.8

Financial services & real estate 10.0 Exports of goods & services 52.7

Government 26.9 Imports of goods & services –62.6

GDP at factor cost incl others 100.0 GDP at market prices 100.0

Principal exports fobb 1998 US$ m Principal imports ciff 1997 US$ m

Diamonds 389 Food & beverages 337

Processed fish 365 Machinery & electrical goods 209

Other manufactures 232 Vehicles & transport equipment 205

Other minerals (incl uranium) 187 Chemicals & plastics 157

Live animals & animal products 102 Textiles, clothing & footwear 105

Metals & metal products 105

Main destinations of exports 1998 % of total Main origins of imports 1995 % of total

UK 43g South Africa 84h

South Africa 26 US 4

Spain 14 Germany 2

France 8 Russian Federation 1

a EIU estimates. b Revised official figures from latest edition of National Accounts. c Windhoek. d Extrapolated from 1991 census. e The Namibiadollar (N$), introduced in September 1993, is at par with the South African rand. f Imports cif, before deduction of duties payable, addition ofduties paid on imports from countries other than the Southern African Customs Union (SACU) and central bank adjustments. g Includes allNamibian diamonds contracted for marketing by De Beers’ Central Selling Organisation (CSO), which are shipped via Switzerland for sale inLondon. h Includes goods from third countries outside SACU purchased through South African suppliers.

Namibia 7

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Outlook for 2000-01

Namibia: forecast summary(US$ m unless otherwise indicated)

1998a 1999b 2000c 2001c

Real GDP growth (%) 2.4 3.0 4.5 5.0

Consumer price inflationd (av; %) 6.2 8.5 7.0 8.0

Exports fob 1,278 1,400 1,575 1,650 of which: diamondse 389 460 550 600 fishf 368 430 470 500 manufactured productsg 232 230 250 300 uranium & other minerals 187 180 210 240

Imports fob 1,451 1,500 1,600 1,700

Current-account balance 162 190 200 150

Average exchange rateh (N$:US$) 5.53 6.08 6.23 6.50

a Actual, revised. b EIU estimates. c EIU forecasts. d Windhoek. e Includes estimates by the Bank ofNamibia of smuggled stones, equivalent to some 5-10% of officially recorded sales. f Processed,semi-processed and unprocessed fish products. g Excluding prepared and preserved fish; mainlymeat and meat preparations, beverages and other processed foods. h The Namibia dollar isexpected to remain at par with the South African rand.

The outcome of the general elections held on November 30th andDecember 1st 1999 was the widely predicted victory both for the head of state,Sam Nujoma, in the presidential race and the ruling South West AfricanPeoples’ Organisation (SWAPO) in the National Assembly poll. There willtherefore be little change in prevailing policies in the short term, asMr Nujoma is healthy at 70 years old and can be expected to serve out his fullfive-year term. The cabinet will probably be reshuffled soon, and this mayinclude further promotions for younger members of the ruling party, althoughthe main senior ministers, including the minister of foreign affairs, Theo-BenGurirab, and the minister of finance, Nangolo Mbumba, are likely to retaintheir posts. Within a few years, however, the question of who is to beMr Nujoma’s designated successor will inevitably come to the fore, and thiscould prove divisive within SWAPO. Internal manoeuvring for positions withinthe party could lead in time to a loosening of Mr Nujoma’s tight grip,especially as some of his closest senior colleagues, such as the SWAPOsecretary-general, Hifikepunye Pohamba, are likely to retire relatively soon. Theprime minister, Hage Geingob, who has adopted an increasingly presidentialstyle in recent years, still seems to be the most likely successor, unless the partyfeels that it must have a leader from northern Namibia, in which case eitherthe minister of trade, Hidipo Hamutenya, or the minister of agriculture,Helmut Angula, appear to be the main contenders.

The breakaway Congress of Democrats (CoD) party, led by a former member ofSWAPO and guerrilla fighter, Ben Ulenga, has emerged as the main politicalalternative to the ruling party, just beating the Democratic Turnhalle Alliance ofNamibia (DTA) into third place in the presidential poll, although both partiesappear to have won seven parliamentary seats each (see The political scene).

Mr Nujoma’s third termwill refocus attention on

his successor—

—but SWAPO is likely toface a more effective

opposition—

8 Namibia

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Although the CoD failed to make significant inroads into SWAPO’s support inits political heartland of northern Namibia, Mr Ulenga has established the CoDas a viable party. Although there were obvious regional voting patterns, theelection results showed that the CoD’s appeal is more national, rather than thepredominantly ethnically based support as in the case of the DTA and theUnited Democratic Front (UDF). This is a relatively rare feat in African politicsand augurs well for the continued functioning of multiparty politics inNamibia. Although the opposition in parliament is now more divided, the CoDhas the advantage over the DTA of not being tainted by an association with theprevious South African colonial regime—although SWAPO’s portrayal ofMr Ulenga as a “sell-out” during the campaign appeared to hurt his campaign,especially among the crucial northern voters. Most SWAPO leaders, includingMr Nujoma, clearly feel deep bitterness towards Mr Ulenga for having desertedhis former political home, although his criticisms of its lack of internaldemocracy were privately endorsed by many members of the ruling party.

As SWAPO has retained its two-thirds majority in parliament, it will be able topush through whatever legislation it desires. Outwardly, the main impact thatMr Ulenga can hope to have is to improve the quality of public debates overgovernment policies. However, the fissures that he has exposed within theparty could also lead to internal changes within SWAPO and, in time,encourage the ruling party to become less monolithic and defensive in the faceof criticism.

During the campaign, Mr Nujoma pledged that, if re-elected, SWAPO wouldcreate 50,000 new jobs; intensify its programme to eradicate poverty byhelping Namibians establish more small- and medium-scale enterprises; pursueaffirmative action within the private as well as the public sector; and attractnew investment to diversify the economy. However, while the continuedexpansion of the fishing industry and offshore diamond mining sector areundoubtedly on course, these have created only a few thousand new jobs,many of which have been offset by job losses in other mining companies andin manufacturing. Mr Nujoma expects that most new jobs will be generated bythe ongoing expansion of capacity at Walvis Bay and Lüderitz harbour, theexploitation of the Kudu gasfield and construction of a large gas-fired powerplant at Oranjemund, and development of copper and zinc mines. Notably, thepresident has not referred to the export processing zone (EPZ) programme,where job creation remains well below the government’s target (see Economicpolicy), or the much delayed Epupa hydroelectric scheme (see Infrastructureand other services). However, exploitation of the Kudu field is unlikely to startbefore 2002-03 at the earliest, and much of the investment required to expandand diversify the productive economic sector will have to come from privateinvestment sources. This will require the government to take effective action tocurb growth in the public sector and reduce the fiscal deficit, both of which areproving problematic. Given that the civil sector jobs are one of the main perksfor party members and former guerrillas, it is politically very difficult for thegovernment to cut their number significantly. However, foreign investors willbe looking, at the very least, for more effective action to rein in public-sectorexpenditure. In this context, an additional budget for the fiscal year 1999/2000

—and may have difficultymeeting its election

promises

Namibia 9

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

(April-March), which was postponed until after the election, does not appear tobe helping the situation, as it contains extra spending commitments, mainlyrelated to Namibia’s continuing involvement in the Democratic Republic ofCongo (see Economic policy). The main budget for 2000/01, due to be tabledin March or April, will therefore have to be tough if the goal of reducing thedeficit to 3% of GDP is to be achieved.

The government’s economic goals will be assisted in the short term by therenewed buoyancy of the economy, primarily reflecting the positive impact ofthe reduction in interest rates, and the continued expansion in fishing andoffshore diamond mining. The real GDP growth rate for 1998 has been reviseddownwards slightly to 2.4%, but the EIU is estimating that real GDP growthwill have improved to 3% in 1999, underpinned by the larger than anticipatedexpansion of offshore diamond recoveries by Namibian Minerals Corporation(Namco) and a booming fishing sector. We are also maintaining our forecast of4.5% growth in 2000, mainly because the prospects for demand for diamondson the global market have continued to improve. De Beers’ recent declarationthat it will no longer purchase any Angolan diamonds on the open market willincrease its requirements for high-quality gemstones, which make up the bulkof Namibia’s output. Therefore, a rise in both onshore and offshore output tosome 1.6m-1.7m carats can be expected in 2000. Fish catch ceilings, at least forhake and mackerel, have been increased for the 2000 fishing season, givenaccumulated evidence that the biomass has largely recovered in the past fewyears, owing to restricted catch quotas (see Agriculture). Fishing value added isofficially forecast to rise by 10% in 1999, and growth of at least a similarmagnitude is probable in 2000. An increasing proportion of the hake fishingfleet is made up wetfish vessels, which land their catches for onshoreprocessing, rather than freezer trawlers. An increase in physical landings willtranslate into higher fish-processing output, which will provide a sizeable boostto overall manufacturing output.

Assuming that these trends continue in 2001, boosted by further falls ininterest rates, real GDP growth is expected to rise to 5%. In addition, there isthe prospect that production of base and precious metals by TsumebCorporation Limited’s mines will resume, provided that a buyer for theliquidated company has been found by early 2000, along with the start of high-grade zinc production from the Skorpion mine and refinery being developed byAnglo American Corporation. Although exploitation of the Kudu gasfield isunlikely now before 2002-03, it remains possible that some initial constructionof related infrastructure will get under way in 2001. This would provide a majorboost to construction and other services, which—along with continuedexpansion in financial services and tourism—should be on a sufficient scale forthe economy to achieve its highest real growth rate since 1994.

Mainly as a result of higher diamond and fish export earnings, Namibia’sforeign trade deficit is forecast to narrow significantly in 2000, to just US$25m,from US$100m in 1999, before widening modestly in 2001, to US$50m. Arecovery in the global diamond industry is forecast, especially as Japan beginsto emerge from recession. Global demand will rise, with larger quota purchases

Real GDP growth is set torise in 2000-01 on the back

of diamonds and fish

The current-accountsurplus will widen in 2000

10 Namibia

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

from Namibian producers by De Beers, including sales of some stockpiles leftover from 1998. We expect Namibia’s diamond exports to reach US$550m in2000 and US$600m in 2001. Higher exports will be partly offset in 2000—andmore than offset the following year—by an upturn in imports, driven bygreater consumer demand and increased procurements of capital plant,equipment and construction inputs. On the invisibles side, higher import-related services will widen the services deficit over the forecast period. Tourismreceipts should, however, also continue to show strong growth, despite theshort-term negative impact of the Caprivi crisis. Although in the long termcurrent-transfers receipts from the Southern African Customs Union (SACU)are set to fall eventually, as South Africa phases out external tariffs under itsfree-trade agreement with the EU, this will not significantly affect Namibia’sbalance-of-payments position during the forecast period. Overall, we expectthe current-account surplus to improve from US$190m in 1999 to US$200m in2000, before narrowing to US$150m in 2001.

The security situation in the north of Namibia deteriorated rapidly in lateDecember 1999 and into early January 2000. Following the decision byNamibia to allow Angolan troops to operate on Namibian soil in their efforts toquash rebels of the União Nacional para a Independência Total de Angola(UNITA), several heavy clashes have been reported, including, possibly, directengagement between Namibian and UNITA forces. Reports indicate that therehave been modest casualties on all sides, while three French tourists have alsobeen killed in Caprivi, presumably by UNITA. Regardless of the costs, Namibiahas pledged to continue assisting Angola, a close ally, which helped SWAPOduring its campaign against South African rule in the 1980s. Although theborder remains highly porous, and these developments have been damaging toNamibia’s image as a stable and safe destination for tourists and business,serious disruptions outside the border areas are not expected.

Late note

Namibia 11

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

The political scene

Sam Nujoma has won a convincing re-election in the presidential poll held onNovember 30th and December 1st. His margin of victory—preliminary resultsput his share of the vote at 76%—appears to be even greater than in theprevious election. In 1994 Mr Nujoma won 72% of the vote against a soleopponent, Mishake Muyongo, then leader of the Democratic TurnhalleAlliance (DTA), who became a Caprivi secessionist organiser in 1998. This timeMr Nujoma faced three opponents: Ben Ulenga, leader of the newly formedCongress of Democrats (CoD); Katuutire Kaura, leader of the DTA (nowtechnically called the Democratic Turnhalle Alliance of Namibia); and JustusGaroeb, the veteran leader of the mainly Damara-based United DemocraticFront (UDF). A fifth potential candidate, Moses Katjuoungua, leader of thesmall Democratic Coalition of Namibia (DCN), was unable to stand because hefailed to meet the registration deadline, although his party contested thesimultaneous National Assembly elections.

Namibia: presidential election results, 1999a

Candidate Party % of vote

Sam Nujoma SWAPO 77

Ben Ulenga CoD 11

Katuutire Kaura DTA 10

Justus Garoeb UDF 3

Total – 100b

Turnout (%) – 62

a Preliminary results, subject to minor revisions. b Does not sum, owing to rounding.

Source: Electoral Commission.

Mr Ulenga took second place, just ahead of Mr Kaura, while, as expected,Mr Garoeb came in a poor fourth with only 3% of the vote. The ruling SouthWest African Peoples’ Organisation (SWAPO) won so overwhelmingly in the fournorth-central regions of Oshana, Oshikoto, Omusati and Ohangwena—takingbetween 95% and 98% of the vote in both the presidential and parliamentarypolls in those regions—that the outcome in the rest of the country was almostirrelevant. The ruling party’s depiction of Mr Ulenga as a “sell-out” appears tohave worked, as northern Namibians suffered the brunt of South Africa’scounter-insurgency operations prior to independence and remain deeply loyal toSWAPO for having ensured a decade of peace. About three weeks before theelections, the education minister, Nahas Angula, produced documentationpurportedly showing that Mr Ulenga had given details of SWAPO’s guerrillaoperations when captured and interrogated by South African troops in the mid-1970s. Mr Ulenga admitted that he had been captured, but denied that he hadmade the specific confession attributed to him. However, the charge clearlydamaged the CoD leader’s standing in the north. The defection in October of theinformation and broadcasting minister, Ignatius Shixwameni, from SWAPO tothe CoD, also appears to have failed to win over SWAPO supporters.

Mr Nujoma has beenoverwhelmingly re-elected

as president—

—as Mr Ulenga comes in adistant second—

12 Namibia

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Mr Ulenga performed best in the central Khomas region, particularly theaffluent Windhoek West constituency (where he beat Mr Nujoma into secondplace), parts of the western Erongo region, including Swakopmund and thesouthern Hardap region, while gaining a majority of votes from the small Bastercommunity of Rehoboth, south of Windhoek, at the DTA’s expense. Mr Kauraperformed best in areas where the Herero are preponderant, mainly the north-western Kunene region, and the eastern Otjozondupa and Omaheke regions,while Mr Garoeb picked up the ethnic Damara vote in Kunene and Erongo.

Based on preliminary results for the parliamentary election (which are subjectto minor revisions), SWAPO won majorities in more than 90 of the 114electoral wards, including all the main towns. From this data it appears thatthe ruling party has gained two new seats in parliament, giving it a total of 55seats. While SWAPO was expected easily to win a majority, the opposition hadbeen hoping to remove its two-thirds majority—which has permitted theruling party to make constitutional changes unilaterally, including allowingMr Nujoma to stand for a third term; this result has only enhanced its domina-tion of the National Assembly. In the end, the CoD gained only 10% of thevote, giving it just seven seats. The DTA, with about 9%, also won seven seats,significantly fewer than the 15 seats that it held in the previous parliament.The UDF more or less held on to its 1994 level of support and retained its twoseats. The tiny Monitor Action Group (MAG) won 0.7% of the vote, butmanaged to secure a single seat. Parliamentary seats are distributed on the basisof proportional representation using a party list system (see below), hence theapproximate correlation between percentage of vote and percentage of seats.

Namibia: legislative election results, 1999a

Party % of the vote seats won % of seats

SWAPO 76 55 76

CoD 10 7 10

DTA 9 7 10

UDF 3 2 3

MAG 1 1 1

Others 1 0 0

Total 100 72 100

a Preliminary results, subject to minor revisions.

Source: Electoral Commission.

The DTA had initially appeared relatively well disposed towards the CoD, in the hopethat it might succeed in gaining votes at SWAPO’s expense in the north. However,now that it seems that the CoD and DTA simply split the anti-SWAPO vote, it mayprove more difficult for the two parties to co-operate. In the Caprivi region, the CoDwon three of the six constituencies previously held by the DTA (SWAPO won theother three), indicating that it was benefiting from continuing anti-governmentsentiment there more than the DTA. Nevertheless, the presence in parliament ofMr Ulenga, along with the former trade and industry permanent secretary, TsudaoGurirab, and Mr Shixwameni—who held the three most senior slots on the CoDparty list—should provide the opposition with reasonably strong leadership.

SWAPO also retains itstwo-thirds majority

in parliament

—and regional votingpatterns become apparent

Namibia 13

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

The election passed largely peacefully, with no evidence of widespread fraud orirregularities. There did not appear to be any significant organised intimidationof voters in the north, although the CoD reportedly cancelled a string of ralliesjust before polling, following alleged threats to the party’s campaign organisers.However, some doubts over the accuracy of the list of registered voters havebeen raised. This is mainly owing to the fact that the electoral roll totalled878,000 voters, up by more than one-third from the total in 1994. The head ofthe EU observer mission, Eeva Kuuskoski, told a press briefing on December 4ththat the existing roll was inaccurate and that, in particular, verification oftendered votes (votes cast by people from outside their registered constituency)was rendered impossible. More than 20% of all ballots cast were tendered votes,and these proved to be crucial in several constituencies where opposition partieswere winning before the tendered votes came in, including Windhoek Eastwhere the CoD had been ahead, and Katutura Central, where the DTA had beentied with SWAPO. However, Ms Kuuskoski said that her team had not detectedany evidence of fraud, despite opposition party protests that the indelible inkused on people’s thumbs to prevent them voting twice could be washed off.

A post-election cabinet reshuffle—which is likely to take place after March2000, as the constitution stipulates that the government has to remain in placefor three months after an election—will bring a number of new faces into thegovernment, as several senior officials announced their retirement, whileothers were not even included on SWAPO’s candidate list.

Namibia: notable retiring SWAPO officials

Official Post

Vekuii Rukoro Attorney-general

Hartmut Ruppel Former attorney-general

Oscar “Hampie” Plichta Minister of works, transport & communications

Richard Kapelwa-Kabajani Minister of youth & sport

Klaus Dierks Deputy minister of mines & energy

Nangolo Ithete Deputy minister of environment & tourism

Partly because of the manoeuvring instigated by the retirements, the selectionof candidates for the SWAPO party list proved unexpectedly controversial.Mr Nujoma’s initial choices for the top 30 places—all virtually guaranteedelection—left out most of the existing cabinet. His assumption of the rightunilaterally to determine these 30 candidates, which unsurprisingly includedthose most loyal to the president, almost derailed the party’s convention inlate October, with several senior ministers threatening not to make themselvesavailable at all. A private convocation of the party’s senior leadership had tostrike a compromise under which most of the cabinet were included in the first20 names, with some of Mr Nujoma’s initial choices relegated to lowerpositions, although within the “comfort zone” of the 50 or so members ofparliament (MPs) that SWAPO was likely to return. The fact that partyrepresentatives at the congress openly objected to Mr Nujoma’s choices mayindicate that a gradual shift towards a more accountable leadership is underway. Certainly, the episode did little to alter Mr Nujoma’s autocratic reputation.

SWAPO’s final candidatelist is controversial—

Questions are raised aboutthe electoral roll

14 Namibia

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

In a renewed demonstration of his skill in co-opting potential opponents, inOctober Mr Nujoma appointed the Namibia National Farmers Union (NNFU)president, Gabes Shihepo, to the post of deputy information minister, whichwas left vacant by the resignation of Mr Shixwameni. Mr Shihepo had beeninstrumental in organising a protest march by some 800 communal farmers toState House in September, which the government had tried to stop for fear thatit would harm SWAPO’s election campaign. So far there has been no responseby Mr Nujoma to the NNFU’s petition calling for land reforms, an end to unfairland management practices and measures to ensure land tenure security(4th quarter 1999, page 13). The NNFU—which is not affiliated to SWAPO—had also accused government members and relatives of being among thosebenefiting most from the illegal fencing of communal land in the north. Onpast experience, hopes by NNFU leaders that Mr Shihepo will be able to use hisnew government position to advance their case seem likely to be disappointed.

A Namibian chapter of the Berlin-based non-governmental organisationTransparency International (TI) is reportedly soon to be established. However,TI’s latest report, which gave Namibia a mixed rating, was criticised by the primeminister, Hage Geingob, for not reflecting “reality on the ground”. TI’s 1999Corruption Perception Index has ranked Namibia 29th out of 99 countriesassessed, with a score of 5.3 out of 10 points. Although Mr Geingob defended thegovernment’s anti-corruption credentials, the cabinet has rescinded a decisiontaken in early 1999 to establish an anti-corruption unit in the prosecutor-general’s office. Political will to establish an effective anti-corruption programmestill seems lacking. No legislation has yet been enacted that would requireministers and public officials publicly to declare their private assets, althoughMr Geingob stated that consultations on establishing a properly resourcedindependent anti-corruption unit would lead to new laws being enacted in 2000.

Namibia: Corruption Perception Index, selected countries, 1999

Country Rank Score

Denmark 1 10.0

Botswana 24 6.1

Belgium 29 5.3

Namibia 29 5.3

Hungary 31 5.2

South Africa 34 5.0

Zimbabwe 45 4.1

Mozambique 56 3.5

Zambia 56 3.5

Ghana 63 3.3

Uganda 87 2.2

Kenya 90 2.0

Nigeria 98 1.6

Cameroon 99 1.5

Source: Transparency International.

—but a potential opponentis brought into the

government

Anti-corruption laws areback on the agenda

Namibia 15

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Economic policy

Tabling of an additional budget for the 1999/2000 fiscal year (April-March) hasbeen postponed until January, ostensibly because there was insufficient timefor parliament to deal with it before it was dissolved prior to the nationalelections. The deputy finance minister, Rick Kukuri, confirmed in October thatan additional budget providing for an extra N$360m (US$58m) in publicexpenditure had been drafted, but denied claims made by the daily newspaperThe Namibian that the real reason for the delay had been to avoid negativereactions to a sharp increase in defence expenditure, associated with Namibia’smilitary operations in the Democratic Republic of Congo (DRC). According tothe newspaper, an additional N$173m has been earmarked for defence, ofwhich N$50m is for the daily allowances of Namibia Defence Force (NDF)soldiers serving in the DRC. Including the N$24m already allocated from thegovernment’s contingency fund this fiscal year, a total of N$74m, or someN$1.4m a week, is being spent on allowances alone. Defence received N$599min the main budget for 1999/2000 tabled in April 1999, the third highestallocation after education and health (3rd quarter 1999, pages 11-12).

In contrast to the extra spending on defence, the draft additional budgetapparently contains no extra funds for health, despite the fact that statepharmacies and hospitals are running out of basic medicines such as penicillin.The cabinet reportedly rejected a request for N$82m from the Ministry ofHealth and Social Services for medicines, and for a further N$37m to increasepensions. The N$82m allocation in the main 1999/2000 budget forpharmaceuticals has apparently been diverted to pay for social pensions andextra wage costs. The additional budget also includes extra funds for thepresident’s office, as State House has reportedly overspent its travel budget byalmost twice the N$6m allocated in the main budget.

Before its dissolution, parliament managed to find time for the introduction ofvalue-added tax (VAT). The minister of finance, Nangolo Mbumba, tabledlegislation during October, and VAT is now expected to come into effect duringthe 2000/01 fiscal year, replacing existing indirect taxes such as the additionalsales duty (ASD) and general sales tax (GST). VAT will be levied at a rate of 15%on basic consumption goods, excepting certain essential commodities whichform a large part of the budgets of low-income Namibians, and at a rate of 30%on luxury items. Mr Mbumba stated that implementation of VAT is expected totake place about six months after final approval of the bill as—given thetroubles encountered in introducing VAT in other countries, such as Ghana—time was needed to train staff and familiarise the public with its provisions.

An additional budget willbe introduced—

Legislation to introduceVAT has been tabled

—but its contents remaincontroversial

16 Namibia

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Namibia: proposed VAT rates

All goods and services will be taxed at a rate of 15% except:

VAT exempt: fuel, millet and maize meal, exported goods, financial services, medicalservices, education, public transport, supply of water and electricity, residential sewage,refuse removal.

Luxury 30% rate: cars priced above N$200,000 (US$32,100), double cab vehicles,revolvers, rifles, casino equipment, cosmetics, antiques, wine, spirits, televisions, videorecorders, hi-fi equipment and radios.

The governor of the Bank of Namibia (BoN, the central bank), Tom Alweendo,has confirmed that for the foreseeable future Namibia will remain a member ofthe Common Monetary Area (CMA) and that the Namibian dollar willcontinue to be pegged directly to the South African rand. Exchange rateswithin the CMA—which comprises Namibia, South Africa, Lesotho andSwaziland—are fixed at par, with no payment restrictions between theparticipating countries. The declaration by Mr Alweendo in his annualstatement given in November will provide welcome reassurance to the localbusiness sector and overseas investors of continued monetary stability,especially as the development subcommittee of the Presidential EconomicAdvisory Council recently proposed a review of Namibia’s CMA membershipand the possible delinking of the Namibian dollar from the rand. However,Mr Alweendo said that the decision to join the CMA after Namibia’sindependence in 1990 was perceived as the most appropriate arrangement inthe prevailing circumstances of Namibia’s close economic relationship withSouth Africa, and that, in the opinion of the central bank, the benefitscontinued to outweigh the costs. He emphasised that a fixed exchange rateremains the best option while the government was attempting to reduce thebudget deficit. Namibia’s foreign-exchange reserves remain modest—US$218min mid-1999, or less than six weeks’ import cover—giving the central banklittle scope to intervene. Under the present arrangements the country’s foreignreserves are in effect underpinned by the South African Reserve Bank (SARB,the South African central bank). Instead, Mr Alweendo suggested that Namibiawould benefit from an evolution of the CMA towards full monetary union,including other countries in the region, and involving a closer co-ordination ofmonetary policies. The recent establishment by the SARB of a monetary policycommittee, including government and business representatives, should assistthis process, as decisions affecting South Africa’s CMA partners are now likelybe taken on a broader basis than they were previously.

The effectiveness of the government’s export processing zone (EPZ) programmehas been challenged in a controversial study by the Labour Resource andResearch Institute (LRRI), an independent body with close links to the NationalUnion of Namibian Workers (NUNW). The report states that the programmehas created far fewer jobs than claimed, with just nine companies listed as

The central bank favourscontinued CMA

membership

The EPZ programme iscriticised for failing

to deliver

Namibia 17

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

being operational as of April 1999, employing only 370 people, mainly in low-paid positions. The report also puts total investment at only N$130m(US$21m)—half of the figure given by the EPZ promotional agency, theOffshore Development Company (ODC). Moreover, of this total, more than50% came from investment in a single enterprise, Ostrich Production Namibia,outside Keetmanshoop. The LRRI maintains that the EPZ regime has fallen farshort of its stated objectives of creating 25,000 jobs and expanding industrialdevelopment. The study also found that most EPZ companies were importingalmost all their materials and, in consequence, had created few new indirectjobs with existing local companies, apart from in transportation. However, theODC responded by claiming that it was far too soon to judge the success orfailure of the EPZ scheme, and accused the LRRI of missing data on neweroperations. The ODC continues to project the creation of more than 4,000 jobsin the next few years, with investments totalling N$7bn.

The domestic economy

Economic trends

Provisional data from the Bank of Namibia (BoN, the central bank) indicate animproved economic performance during the second and third quarters of1999, with year-on-year real GDP growth of 3.4% and 2.8% respectively,compared with fractional growth of 0.2% in the first quarter (4th quarter 1999,page 14). According to projections by the BoN’s research department seniormanager, Chris Hoveka, the central bank expects the overall growth rate for1999 to average 3.2%. (The EIU is estimating a growth rate of just 3%, whichstill implies a surge in output in the fourth quarter.) Fishing, mining, tourismand government services have been the main growth generators during 1999,offset by weaker performances by the agriculture, wholesale and retail trade,transport and communications, water and electricity sectors. However, creditgrowth to the private sector remained relatively sluggish in 1999, with year-on-year lending to businesses down, despite the reduction in interest rates (seebelow). According to Mr Hoveka, this could be attributed to a lag effect, withthe prospect that credit will respond to lower interest rates in time, or to thepossibility that businesses were primarily refinancing old debt rather thantaking up new loans.

Year-on-year consumer price inflation, measured by the Windhoek all-itemsindex, eased further to 8% in September, the lowest level for ten months.However, the average rate, year on year, for January-September 1999 of 8.6% is3 percentage points higher than for the corresponding period of the previousyear. Food price inflation, with the largest weighting in the index, declined inSeptember on a year-on-year basis, but upward price pressures continued else-where, particularly in transport and communications. Another fuel priceincrease in October—the third within five months—makes it likely that overallinflation will have risen again in that month. Pump prices for leaded fuel wentup by N$0.28/litre (5 US cents/l) and diesel by N$0.20/l, bringing the

Inflation remainssubdued—

The economy is estimatedto have grown by just

over 3% in 1999

18 Namibia

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

cumulative rise since the start of 1999 to 33% for all petrol grades and 27% fordiesel, including the effects of increased fuel taxes levied from April. The recentrise in global crude oil prices and a widening in the margins for refinedproducts have made it increasingly unviable for the government to continuesubsidising pump prices at prevailing rates—this policy has cost the NationalEnergy Fund (NEF) some N$8m a month since July. The price equalisationfund is almost depleted and the Ministry of Mines and Energy claims thatfuture pump prices will have to move more directly in line with the trend inrefined import costs. However, although public transport fares withinWindhoek increased by 50% in October, the Namibia Bus and Taxi Association(Nabta) promised to freeze fares for six months, irrespective of further fuel pricerises, to ensure that low-income Namibians could continue to afford to useits services.

Namibia: consumer and food price inflation, 1999(1992=100)

Aug Sep Jan-Sep

All-items index 175.4 176.4 – % change, year on year 8.1 8.0 8.6

Food index 162.0 163.2 – % change, year on year 6.3 5.9 6.0

Source: Central Bureau of Statistics.

Local interest rates were further reduced during October, reflecting a 21-basis-point reduction in the SARB’s repo rate. The Namibian bank rate was cut by aslightly higher margin of 25 basis points to 11.75%, while commercial banksreduced their prime lending rates by 1 percentage point to 16.5%. Thismatched the reduction in interest rates by South African banks, althoughNamibian prime rates are still 1 percentage point higher. Further interest-ratecuts are not expected before the end of 1999. However, inflation in SouthAfrica has continued to decline—falling to just 1.7% in October. This trend,along with expectations of continued low inflation in the early part of 2000,will enable further interest-rate cuts.

Mining

The UK-based Namibian Minerals Corporation (Namco) now ranks as theworld’s second largest marine diamond mining company, after De Beers Marine(Debmarine). Namco has reported production of 208,000 carats from LüderitzBay in the first nine months of 1999 and has successfully taken over the CapeTown-based Ocean Diamond Mining (ODM; 4th quarter 1999, page 17). Namcohad secured a 92% stake in ODM when its offer closed at the end of Octoberand it is expected to buy out the remaining shareholders soon. This has added a20,000-sq-km offshore acreage to Namco’s existing 3,000-sq-km concessions,along with three mining vessels and the prospect of combined synergies from alarger resource base, improved fleet utilisation and reduced overheads. Of moreimmediate significance to Namco’s expansion prospects, in November it wasgranted a second 15-year mining licence, covering the 359-sq-km Saddle Hill

—and interest rates havefallen further

Namco continues togrow strongly

Namibia 19

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

prospect in the company’s 526-sq-km Hottentot Bay concession. This containsan estimated resource of 650,000 carats, but only 2% of the concession area hasso far been prospected and a substantial upward revision is likely followingfurther exploration scheduled for 2000—for which Namco has commissioned aUS$1.5m seabed drilling tool from Germany’s Wirth.

Namco is now generating a stronger cashflow, although, apart from the 10%diamond royalty payable to the government, it will not incur a tax liabilityuntil the 2000/01 fiscal year (April-March), as it has been able to offsetexploration and capital costs against profits. Revenue of US$34m from the saleof 229,000 carats in the first nine months of 1999, up from US$5m in the sameperiod of 1998, has left Namco with net earnings of US$16m.

Uranium oxide production at the Rossing mine declined by 7%, year on year,in the third quarter of 1999 to 813 tonnes. This was the second successivequarterly fall and production for the first nine months of the year is 5% lowerthan in the same period of 1998. Delivery requirements have been reduced bythe current weak state of the global uranium market, as an increasing pro-portion of the fuel requirements for nuclear power plants is being met fromreprocessed supplies, including recycled weapons-grade material. Primarysupply from uranium mines accounted for only 54% of the market in 1998.The London-based Uranium Institute forecasts that demand should recover by2001, owing to higher reactor load factors and depletion of primary uraniuminventories, although uncertainties remain over the extent and timing of therelease on to the market of blended-down enriched uranium sold by Russia tothe US. To maintain competitiveness, the mine management has commencedthe second phase of its Rossing Beyond 2000 (RB2000) programme aimed atcutting costs by 20% over the next two years. One-sixth of the present work-force of 1,200 are due to be retrenched by the end of 2000, leading most of themine’s employees to stage a protest at the mine in October.

Namibia: uranium oxide production, Jan-Sep

1998 1999 % change

Production (tonnes) 2,572 2,453 –4.6

Source: Rio Tinto.

The mining assets of Tsumeb Corporation Limited (TCL), the country’s largestbase and precious metals producer, are now being disposed on a tender basis,with bids due in by December 15th (4th quarter 1999, page 18). This followsthe failure of Australia’s Metals and Mining Corporation of Namibia (MMN) toconvince the Ministry of Mines and Energy that a US$20m loan facility whichit had arranged with N M Rothschild was an adequate capital guarantee.Although MMN signed a sales agreement at the end of October, after initialassurances from TCL’s liquidators that it had complied with the terms of anexclusive option to buy, the creditors subsequently rejected the deal. TCL’sassets—three mines producing copper, lead, silver, gold and pyrites, plus thecopper-lead smelter at Tsumeb—are scheduled to be sold individually to thehighest bidder. However, an offer to acquire TCL as a going concern stillremains possible. Ongopolo Mining and Processing, a partnership between

Uranium output hascontinued to fall

Tsumeb Corporation isbeing sold off by tender

20 Namibia

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

trade unionists and former TCL managers, has deposited N$1m (US$162,000)into the liquidators’ account as a first step towards acquiring the assets, but hasyet to secure full financing. These delays in finding a buyer make it unlikelythat mining operations will resume before mid-2000.

Agriculture

The bumper catch of white fish in 1999—the best in four years—could beexceeded in 2000 with the government’s decision to increase the totalallowable catch (tac) for hake by 15,000 tonnes to 210,000 tonnes, and formackerel by 35,000 tonnes to 410,000 tonnes (4th quarter 1999, page 19). Thefishable hake biomass is currently estimated at just over 400,000 tonnes, withthe next survey planned for February 2000, while the mackerel tac is regardedas conservative in view of the strong state of the biomass, currently estimatedat 1.9m tonnes. In contrast, the pilchard biomass has declined from280,000 tonnes in April 1999 to about 100,000 tonnes, according to the latestsurvey completed in November 1999. Although a final pilchard tac of55,000 tonnes was set for 1999, only 45,000 tonnes were allocated in quotas tofishing companies, with some 43,000 tonnes actually caught. The pelagicindustry is faced by a huge overhang of canned pilchard stocks, as a result ofincreased catches in South Africa, the main market, and depending on theresults of the next biomass survey in February or March, the pilchard tac for2000 may well be reduced. However, this should be more than offset bycontinued growth in white fish landings.

Namibia: total allowable catches, selected species(tonnes)

1998 1999 2000

Hake 165,000 195,000 210,000

Horse mackerel 375,000 375,000 410,000

Source: Ministries of Fisheries and Marine Resources.

Financial services

Rising prices for the majority of shares listed on the Namibian Stock Exchange(NSX) boosted total market capitalisation to a new record of N$286bn(US$46bn) in November, while the overall index climbed to 252 by the end ofthe month, eclipsing the previous peak of 242 in July 1999 (4th quarter 1999,page 21). The volume of shares traded in locally listed companies also reacheda record 12m in October, mainly as a result of the purchase of shares in OceanDiamond Mining (ODM) by Namibian Minerals Corporation (Namco) underits takeover offer (see Mining). The planned listing of Canadian-ownedDiamond Fields International (DFI), which holds exploration rights offshorefrom Lüderitz, was postponed from November to sometime in early 2000. DFIplans to raise the equivalent of US$4m through a private and public placementof 2.5m shares, but following a fall in the value of its shares on the Torontoexchange, the company decided to delay its Namibian listing.

The NSX has continued torecord strong gains

Hake and mackerel catchceilings are raised

Namibia 21

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Namibia: stock exchange statistics, 1999a

(end-period)

% change,Sep Oct Nov Jan-Nov

Market capitalisation (N$ bn)Overall 260.0 271.0 285.9 79.4Local 3.7 3.6 3.8 52.0

Market indicesOverall 230 239 252 43.2Local 143 137 141 33.0

a The NSX has a total of 43 listed companies, 15 of which are local Namibian-based companies,while the rest are mainly cross-listings from the Johannesburg Stock Exchange.

Source: Namibian Stock Exchange.

Infrastructure and other services

Prospects for an early start on construction of the controversial Epupa hydro-electric scheme on the Kunene river have dimmed. A meeting betweenNamibian and Angolan government representatives to finalise the location ofthe planned dam and 450-mw generating station has been delayed again andwill not now take place until sometime in 2000. The continuing civil war inAngola and unavailability of government officials are given as the officialreasons for the delay, but the two countries also disagree over the site. WhereasNamibia favours Epupa Falls, with its scope for a larger reservoir, Angolafavours the alternative Baynes Mountains site, some 40 km downstream fromEpupa, where there is room for only a small reservoir, but which would be lessenvironmentally and socially damaging. The Baynes site would also directlybenefit Angola as it would require the renovation of its Gove dam, whichwould be needed to regulate the flow of water to the generating plant. The1998 feasibility report by the Namang consortium estimated the cost of Epupaat US$539m, with Baynes slightly more expensive at US$551m. As the existingRuacana hydrostation on the Kunene is operating below capacity, Namibia’sdependence on imported South African power is likely to intensify, with aprojected substantial increase in electricity demand over the next five years,arising from several major projects currently in the pipeline. These include theSkorpion zinc mine and refinery, which will require 70 mw, and the Haibcopper mine, with an estimated requirement of 180 mw. However, both ofthese projects are located in the south of the country, and their power demandcould potentially be met just as economically by the proposed combined-cyclepower station at Oranjemund, under the phase one development of the Kuduoffshore gasfield (3rd quarter 1999, page 18).

The national carrier, Air Namibia, took delivery of a new Boeing 747-400Combi aircraft in October, which the company hopes will help it to turnaround its dire financial position. However, the purchase was arranged directlywith the US aircraft manufacturer without a competitive tendering processand, despite a government guarantee, could prove to be a financial burden if itdoes not lead to a sustained upturn in revenue. The new aircraft is being used

Air Namibia hopes for aboost from a new

Boeing 747

A decision on the Epupadam project has been

postponed

22 Namibia

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

on Air Namibia’s twice-weekly Windhoek-Frankfurt-London service, and hasmore cargo and passenger capacity than the leased Boeing 767-300 aircraftpreviously used on that route. Civil servants travelling to destinations servicedby the airline have been instructed to fly with Air Namibia if seats are available.The US$114m cost of the aircraft has been part-financed by a long-term loanguarantee from the US Export-Import Bank (Eximbank), but the bulk is subjectto a Namibian government guarantee, structured as a 12-year lease. AirNamibia’s managing director, Jafaar Ahmad, has launched a five-year businessplan to reverse the airline’s losses, which are currently running at more thanN$50m (US$8m) a year, with partial privatisation envisaged.

Air Namibia has also acquired a Fokker F28 aircraft to operate a dailyWindhoek-Cape Town service and other regional flights. The plane had beenoriginally ordered by Kalahari Express Airlines (KEA), a venture promoted bythe Saudi entrepreneur Hani Ahmed Zaki Yamani, which never got off theground. KEA was taken over by the TransNamib parastatal, which planned torun it as a joint venture between Air Namibia and South African Airlink, asubsidiary of South African Airways. However, following the government’sdecision to transfer control of KEA directly to Air Namibia at the end of 1998,Airlink has pulled out of the scheme, leaving the national carrier to bear all thecosts, including the planned purchase of a second F28.

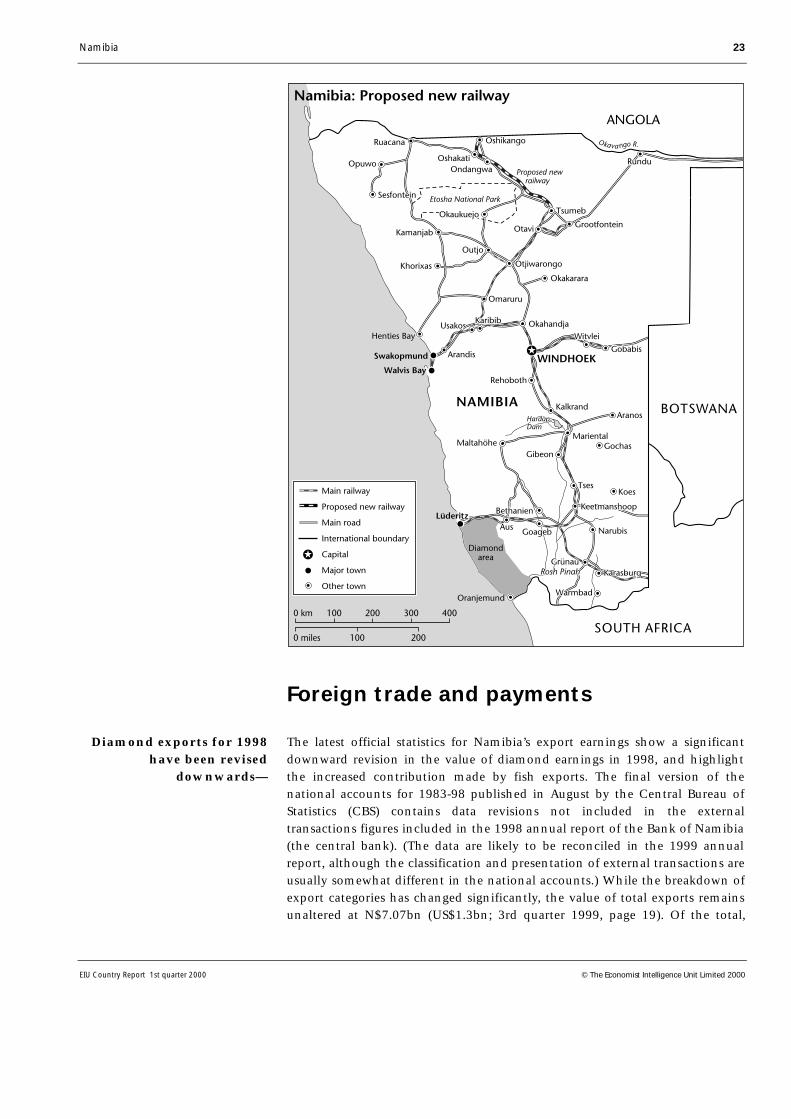

Construction of the long-mooted northern extension to the railway system isdue to get under way by the end of 1999, with completion earmarked for 2005.The project, which has the enthusiastic backing of the president, Sam Nujoma,involves laying some 400 km of new track from the existing northern railheadat Tsumeb to Oshikango on the Angolan border, via the main northern townsof Ondangwa and Oshakati. The extension would provide a boost to export-processing zone (EPZ) activities in Oshikango, which is already beingtransformed into a border trading hub.

The government expects to meet 25% of the estimated N$400m (US$65m) costand is soliciting funds from overseas donors for the remainder; so far theKuwait Fund for Arab Economic Development has pledged US$20m. Afeasibility study on the extension by the US Trade and Development Agencywas completed in 1998 and recommended using second-hand rails and labour-intensive construction methods. Ultimately, it is planned to link the northernextension to the Angolan railway system running inland from Namibe,although this line is only partly operative at present, under the Lubango-Oshikango-Walvis Bay development corridor, an approved regional transportproject of the Southern African Development Community (SADC).

A northern rail link isbeing built

Namibia 23

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Foreign trade and payments

The latest official statistics for Namibia’s export earnings show a significantdownward revision in the value of diamond earnings in 1998, and highlightthe increased contribution made by fish exports. The final version of thenational accounts for 1983-98 published in August by the Central Bureau ofStatistics (CBS) contains data revisions not included in the externaltransactions figures included in the 1998 annual report of the Bank of Namibia(the central bank). (The data are likely to be reconciled in the 1999 annualreport, although the classification and presentation of external transactions areusually somewhat different in the national accounts.) While the breakdown ofexport categories has changed significantly, the value of total exports remainsunaltered at N$7.07bn (US$1.3bn; 3rd quarter 1999, page 19). Of the total,

Diamond exports for 1998have been revised

downwards—

24 Namibia

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

diamond exports stood at N$2.15bn in 1998—N$286m, or 12%, less than theinitial official figure. Compared with 1997, diamond exports fell by N$345m or14%, despite increased production in 1998, reflecting the impact of the 84%quota on normal producer deliveries applied by De Beers’ Central SellingOrganisation (CSO) throughout 1998. The quota arrangement was lifted at thebeginning of 1999, and therefore the further increase in diamond productionin 1999 should be more fully translated into higher export earnings.

The CBS data also show that earnings from all types of fish exports reached arecord N$2bn (US$365m) in 1998, 40% higher than the preceding year andequivalent to 29% of total export earnings. This was just under the 30% con-tribution of diamond exports, narrowing the differential to just 1 percentagepoint, from 16 percentage points in 1997. Live animals and animal productexports also rose sharply, by 41%, to N$562m, reflecting a sizeable upturn inexports of live cattle, sheep and goats, although earnings remained below therecord level of 1996.

Namibia: exports of goods and services(N$ m; fob)

1997 1998 % change

Live animals & animal products 400 562 41 of which: cattle 126 259 106 sheep & goats 144 179 24 ostriches 34 22 –35 fisha 14 14 0

Minerals 3,605 3,186 –12 Diamondsb 2,495 2,150 –14 Copper 194 52 –73 Gold 123 102 –17 Zinc 116 118 2 Uranium & all othersc 677 763 13

Manufactured products 2,171 3,303 52 of which: meat & meat preparations 315 644 104 prepared & preserved fish 1,447 2,020 40 white fishd 1,081 1,461 35 canned fishe 191 320 68 rock lobster & crabf 141 190 35 fishmeal, fish oil & dried fish 33 49 48

Total exports of goods incl others 6,190 7,067 14

Purchases by non-residents 1,597 1,659 4

Other services 154 149 –3

Total exports of services 1,752 1,808 4

a Tuna, guano and oysters. b Including value of smuggled stones, estimated by the Bank ofNamibia. c Including silver, lead, fluorspar, salt, dimension stone and semi-precious stones. d Mainlysemi-processed hake. e Mainly pilchard. f Including seal products and seaweed.

Source: Central Bureau of Statistics, National Accounts, 1983-1998.

—but fish exports showstrong growth

Namibia 25

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

While growth in the output value and export earnings for most fish speciescaught in Namibian waters resumed in 1998, the value of hake exports toSpain has maintained a steady upward course over the past five years. OfficialSpanish trade statistics show that the value of Namibian fish exports wasPta19.25bn (US$156m) in 1997 (the latest year for which data are available),almost double the 1993 value. The increase was concentrated in exports offresh and chilled fish and hake fillets, with virtually no rise in exports of frozenfish, reflecting the increasing proportion of the Namibian hake catch landed aswet fish for onshore processing.

Namibia: fish exports to Spain(Pta m unless indicated otherwise)

1993 1997 % change

Totala 11,152 19,252 73 Unprocessed (fresh & chilled) 1,567 3,486 123 Unprocessed (frozen) 5,811 5,862 1 Fillets (fresh, chilled & frozen) 3,774 9,904 162

Total (US$ m) 78 156 100

a Virtually all hake.

Source: Agencia Tributaria Departamento de Advanas e Impuestos Especiales, Estadistica del Comercio Exterior de Espana, Volumen I,Commercio por Paises y Productos.

Because of this growth, the Spanish hake market has become the second mostimportant source of Namibia’s foreign-exchange earnings (after diamonds).This partly explains the concern among trade ministry officials over thepotential impact of the recently finalised trade agreement between the EU andSouth Africa. The competitiveness of Namibia’s fish exports to EU countries willnot be immediately affected, as Namibian fish products enjoy duty-free entryunder the provisions of Lomé II. However, Lomé will expire at the end of 2000,and the EU appears unwilling to negotiate a similar comprehensive successor,on the grounds that providing preferential access to other countries would becontrary to its commitment to provide open market access to developingcountries under World Trade Organisation (WTO) agreements.

Fish exports to Spainhave soared

26 Swaziland

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Swaziland

Political structure

Kingdom of Swaziland

Absolute monarchy

Parallel systems of Roman-Dutch law and customary law

A bicameral parliament. The House of Assembly is elected through the tinkhundlaelectoral system, which has three stages: nomination, primary election and secondaryelection. A secret ballot is now conducted for the last two stages. The Assembly has 55elected members and 10 royal appointees. The Senate consists of 30 members, 20 ofthem royal appointees and 10 selected by the Assembly. The king may legislate by decree

Last parliamentary election October 1998; next elections are likely to be held in 2003

Monarch, succession governed by custom

The monarch and his cabinet, last reshuffled in November 1998

None; party political organisation is banned, although some groups operate illegally

Monarch King Mswati IIIPrime minister Sibusiso DlaminiDeputy prime minister Arthur Khoza

Agriculture & co-operatives Roy FanourakisEconomic planning & development Majozi SitholeEducation Abednego NtshangaseEnterprise & employment Lutfo DlaminiFinance John CarmichaelForeign affairs & trade Albert ShabanguHealth & social welfare Phetsile DlaminiHome affairs Prince SobandlaHousing & urban development Stella LukheleJustice Chief Maweni SimelaneNatural resources & energy Prince GuduzaPublic service & information Magwagwa MdluliPublic works & transport vacantTourism & communications George Vilakati

Martin Dlamini

Official name

Form of state

Legal system

National legislature

National elections

Head of state

National government

Main political parties

The government

Key ministers

Central Bank governor

Swaziland 27

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Economic structure

Latest available figures

Economic indicators 1995 1996 1997 1998 1999a

GDP at market pricesb (E m) 5,243 6,045 6,714a 7,418a 8,107

Real GDP growthb (%) 3.0 3.6 3.7 2.3c 3.1c

Consumer price inflationd (av; %) 12.2 6.4 7.1 8.2 6.0

Population (m) 0.91 0.94 0.95a 0.96a 0.97

Exports fobe (US$ m) 868 850 864 790 825

Imports fob (US$ m) 1,009 1,050 1,041 941 1,050

Current-account balance (US$ m) 21 –46 –48 –7 –50

Reserves excl gold (US$ m) 298 254 295 359 380

Total external debt (US$ m) 232 193 178 175a 180

External debt-service ratio (%) 2.5 2.7 2.6 2.8a 2.7

Sugar productionf (‘000 tonnes) 421 471 476 475 485

Exchange rate (av; E:US$) 3.63 4.30 4.61 5.53 6.08

December 10th 1999 E6.13:US$1

Origins of gross domestic product 1997bc % of total Components of gross domestic product 1997bc % of total

Agriculture 9.8 Private consumption 53.4

Industry 47.7 Government consumption 27.1

of which: manufacturing 38.0 Gross fixed investment 33.0

Services 42.5 Change in stocks & statistical discrepancy 0.9

GDP at factor cost 100.0 Exports of goods & services 81.8

Imports of goods & services –96.3

GDP at market prices 100.0

Principal exports fob 1998c US$ m Principal imports fob 1996c US$ m

Soft drink concentrate 383 Manufactured goods 275

Sugar 106 Machinery & transport equipment 312

Wood pulp 75 Chemicals 173

Refrigerators 50 Food & live animals 172

Citrus & canned fruit 30 Fuel & lubricants 96

Main destinations of exports 1997c % of total Main origins of imports 1997c % of total

South Africa 74.0 South Africa 82.9

EU 12.3 EU 5.5

Mozambique 5.2 Japan 1.9

US 2.4 Singapore 1.5

a EIU estimates. b Years beginning April 1st. c Official estimate. d Low-income index for Mbabane and Manzini. e Including re-exports. f Cropyears (May-April) beginning in the calendar year indicated.

28 Swaziland

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Outlook for 2000-01

King Mswati III went into semi-seclusion (the small Incwala) onNovember 10th and into proper seclusion (the Incwala recess) onDecember 2nd. While permanent secretaries were reshuffled beforehand, thecabinet reshuffle which had been anticipated before Incwala has failed tomaterialise. However, the cabinet vacancy arising from the death of theminister of public works and transport, Peter Dlamini—a capable youngtechnocrat, who will be a serious loss to the government—in a motor accidenton November 3rd provides a pretext for the prime minister, Sibusiso Dlamini,and the king to rearrange portfolios. The only question now is when this mayoccur. Despite the king being in seclusion, where he normally attends only tourgent matters, ministerial changes could be announced soon, as some of thetraditional norms have been relaxed. The reshuffle will probably be announcedwhen the king dismisses the traditional regiments at the end of Incwala in lateJanuary, as this occasion has often been used in the past to make importantpolicy announcements.

The bomb that exploded at Mahlanya on November 12th has again illustratedthat the lack of political modernisation is creating a climate of growingfrustration (see The political scene). While the Constitutional ReviewCommission (CRC) is considered irrelevant by the so-called progressivemovements, its mere existence continues to be a source of irritation fortraditionalists. The CRC has managed to extract another extension out of theking (see The political scene), but the details of this are unclear, as nothing hasyet been gazetted. Although the chairman of the CRC, Prince Mangaliso, hasrecently stated that the commission would not complete its work before 2001,and that the final constitution may not be in place for the elections in 2003, adraft report is likely to be presented to the king by mid-2000. This will thenenable him either to extend the CRC’s term or to take the opportunity ofdissolving the commission altogether, as it has become a source ofembarrassment and has increasingly lost its credibility. This could open thedoor for the appointment of a new group to compile a report, perhaps withmore transparency.

The Anti-Corruption Commission has launched an investigation into theminister of finance, John Carmichael, for alleged irregularities in the allocationof plots while he was minister of housing and urban development. Thefindings could instigate more investigations or, if the process is perceived as awhitewash, could also escalate popular frustration at the lack of governmentaction to curb corruption. The issue appears to be gaining political support,creating such unlikely bedfellows as the minister of justice, Maweni Simelane—who told the Senate on October 12th that government corruption had reacheduncontrollable levels—the People’s United Democratic Movement (Pudemo)and the Swaziland National Association of Civil Servants.

A cabinet reshuffle is dueafter the Incwala recess

There are further delays onconstitutional reform

Corruption will becarefully watched

Swaziland 29

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

The queen mother (the Indlovukati), who returned in November after medicaltreatment in Taiwan, is rumoured to be seriously ill. If this is true, it couldpresage a substantial change in the balance of power in the dual monarchy inthe medium term. The present queen mother is the mother of King Mswati III,and is often regarded as being more powerful than the king. In the complexSwazi tradition, however, her successor is more likely to be one of his wives,rather than another surviving wife of the king’s father, the late KingSobhuza II. If one of the king’s wives becomes Indlovukati, she is certain to haveless experience and influence than an elder. More importantly, the advisers tothe queen mother—who are widely considered to be thwarting attempts atmodernisation—could lose some of their power. Traditionally, the queenmother’s court has protected the interests of the traditionalist hierarchy, butthe king appears to be more aware of the need for change, realising that thereis simmering discontent and that reform of the monarchy may be the best wayof preserving it. There are fears that, unless the authorities enter into dialoguewith the progressive forces and some political changes are made, Swazilandmay face political unrest or even a violent revolt.

Despite the urging of officials at the Ministry of Economic Planning andDevelopment, policy changes have been slow to be enacted. Technocratswithin the government and business leaders are reportedly chafing at the paceof economic reform to boost competitiveness. Most importantly, keylegislation has been stalled for years. The Industrial Relations Act passed by theSenate in September is now awaiting royal assent, while the Income TaxAmendment Bill may be enacted before the budget speech in March(4th quarter 1999, page 29). Nevertheless, both the Company Act and theInsurance and Pensions Bill have yet to be tabled in parliament. In light ofSwaziland’s poor competitiveness ranking (4th quarter 1999, page 31), thisdoes not bode well for swift or bold policy changes.