nasdaq: mlhr delivering growth by design - … growth by design nasdaq: mlhr investor presentation...

TRANSCRIPT

Delivering Growth by Design

NASDAQ: MLHR

Investor PresentationFourth Quarter FY2017

2

This information contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act, as amended, that are based on management’s beliefs, assumptions, current expectations, estimates, and projections about the office furniture industry, the economy, and the company itself. Words like “anticipates,” “believes,” “confident,” “estimates,” “expects,” “forecasts,” likely,” “plans,” “projects,” “should,” variations of such words, and similar expressions identify such forward-looking statements.

These statements do not guarantee future performance and involve certain risks, uncertainties, and assumptions that are difficult to predict with regard to timing, extent, likelihood, and degree of occurrence. These risks include, without limitation, the success of our growth strategy, employment and general economic conditions, the pace of economic recovery in the U.S, and in our International markets, the increase in white-collar employment, the willingness of customers to undertake capital expenditures, the types of products purchased by customers, competitive-pricing pressures, the availability and pricing of raw materials, our reliance on a limited number of suppliers, our ability to expand globally given the risks associated with regulatory and legal compliance challenges and accompanying currency fluctuations, the ability to increase prices to absorb the additional costs of raw materials, the financial strength of our dealers and the financial strength of our customers, the mix of our products purchased by customers, our ability to locate new DWR studios, negotiate favorable lease terms for new and existing locations and the implementation of our studio portfolio transformation, our ability to attract and retain key executives and other qualified employees, our ability to continue to make product innovations, the success of newly

introduced products, our ability to serve all of our markets, possible acquisitions, divestitures or alliances, the pace and level of government procurement, the outcome of pending litigation or governmental audits or investigations, political risk in the markets we serve, and other risks identified in our filings with the Securities and Exchange Commission.

Therefore, actual results and outcomes may materially differ from what we express or forecast. Furthermore, Herman Miller, Inc., undertakes no obligation to update, amend or clarify forward-looking statements.

Forward looking statements

Headquarters: Zeeland, MI, USA Founded: 1905 Employees: ~8,000

FY17 Revenue: $2.28B FY17 Adj. EBITDA: $264M

Company Snapshot

Over 600 dealers in 109 countries and 31 Design Within Reach retail studios

North America 59%

Specialty 10%

Consumer 14%

ELA 17%

3

4

Our Compelling Story

Investment thesis

Powerful brands deliver design and innovation leadership

A higher ambition culture

Unique combination of value-drivers enabling above industry-average growth

Compelling financial outlook and opportunity for margin expansion

Strong track record of performance and healthy returns on capital

5

A higher ambition culture

66

Driven by a sense of purpose and values

A higher ambition culture

“A business is rightly judged by its products and services, but it must also face scrutiny as to its humanity.”- D.J. De Pree, Herman Miller Founder

Ten Consecutive Perfect Score in Human Rights Campaign Foundation’s Corporate Equality Index

Twelve of the Last Thirteen Years on the Dow Jones Sustainability World Index

Corporation of the Year in the Commercial sector for 9 of the last 11 years by the Michigan Minority Supplier Development Council

7

Powerful brands deliver design and innovation leadership

8

An inspiring brand that customers value

Powerful brands deliver design and innovation leadership 8

* Twitter followers as of June 2017 (Herman Miller, Allsteel, Haworth, Knoll, and Steelcase)

#1 in Brand that Inspires, Contract Magazine Survey

Social Media Followers – Over 4X all major competitors combined*

9Powerful brands deliver design and innovation leadership

Healthcare

Performance textiles

Ergonomic work tools

Asia distribution

Nemschoff

Maharam

Colebrook Bosson Saunders

POSH

A portfolio of leading global brands

TIMELESS CRAFT

The convergence of world-class designers, impeccable craftsmanship, and superior materials.

Brabo Sofa by Vincent Van Duysen

Crosshatch™ Chair by EOOS

H Frame Table by Ward Bennett

Full Twist™ Chair by Mark Goetz

Domino Storage™ by Isay Weinfeld

geigerfurniture.com

Herman Miller brands are #1 in six categories, Contract Magazine Survey (2016)

Craft wood furnishingsGeiger

Design Within ReachMarketplace for authentic modern furnishings

10

Commitment to innovation

Powerful brands deliver design and innovation leadership

– Innovation Priorities:

– 24% of our sales were from new products in fiscal 2017

– Introduced 50 new products and extensions in fiscal 2017

– Industry-leading investment in design, research and development at 3.2% of sales in fiscal 2017

10

Collaborative and other

work points

Active/healthy postures

Outdoor, lighting, and

materials

Technology enhanced user

experience

1111

An icon remastered - the new Aeron

Powerful brands deliver design and innovation leadership 11

– Reinforces Herman Miller’s worldwide leadership in high performance seating

– Incorporates the latest in ergonomics and material science innovation

– Extends a powerful franchise that has sold over 7 million chairs in 134 countries

1212

Bringing innovative solutions to our customers through the Living Office framework

Powerful brands deliver design and innovation leadership

– An insight-driven and research-based framework for making place a strategic asset

– Delivers measurable results through improved: • Workplace Effectiveness • Work Activity Support • Workplace Experience

1313

Unique combination of value-drivers enabling above industry-average growth

14

LiveWork Heal Learn

14

The global leader dedicated to creating inspiring places

Unique combination of value-drivers enabling above industry-average growth

Capitalizing on an expanded total addressable market

Unique combination of value-drivers enabling above industry-average growth

North America (Contract)(1)

European (Contract)(2)

Target Emerging Markets (Contract)(3)

Consumer Lifestyle(4)

Healthcare/Education/Hospitality(3)

Small/Medium Business(3)

Textiles(5)

$8B

$10B

$8B$4B

$6B

$4B

$2B$1B

$9B

$2B

$4B

2011—$24B 2016—$35B

Source: (1) BIFMA; (2) CSIL; (3) Company Estimate; (4) Parthenon Group (2014); (5) ACT Financial Survey (2015)

15

Unparalleled multi-channel reach including direct to consumer

Unique combination of value-drivers enabling above industry-average growth

– Over 600 contract dealers in 109 countries

– 31 Design Within Reach retail studios

– Direct to consumer catalog

– Multiple global e-commerce storefronts

– Opportunities to grow share of channel/customer wallet

Catalog

31 Studios600 Dealers

y

E-Commerce

16

17

Clear path to revenue growth and margin expansion in Consumer business

Unique combination of value-drivers enabling above industry-average growth

– Double digit revenue growth opportunity from Design Within Reach by transforming legacy studios to larger formats and adding new locations • 3 to 6 new or expanded studios per year • Increase studio count to low forties and square footage to 500,000 by 2020

– Increase exclusive product mix from 60% to 70% of revenue

– Continued e-commerce growth

– High single digit operating margin target by 2020

17

1818

Positioned for global growth

Unique combination of value-drivers enabling above industry-average growth

– Growing and profitable business outside North America

– Favorable trends and demographics in Asia-Pacific

– Further growth opportunities: • Leverage Herman Miller and POSH brands in Asia-Pacific

• Expand dealer networks and e-commerce platforms • Regional R&D and manufacturing capabilities support new product growth • Leverage Healthcare, Education and Consumer franchises

2012 2017

+2%CAGR

(+5% organic)

ELA Revenue$386M

$347M

19

Strong track record of performance and healthy returns on capital

20

$2.3B

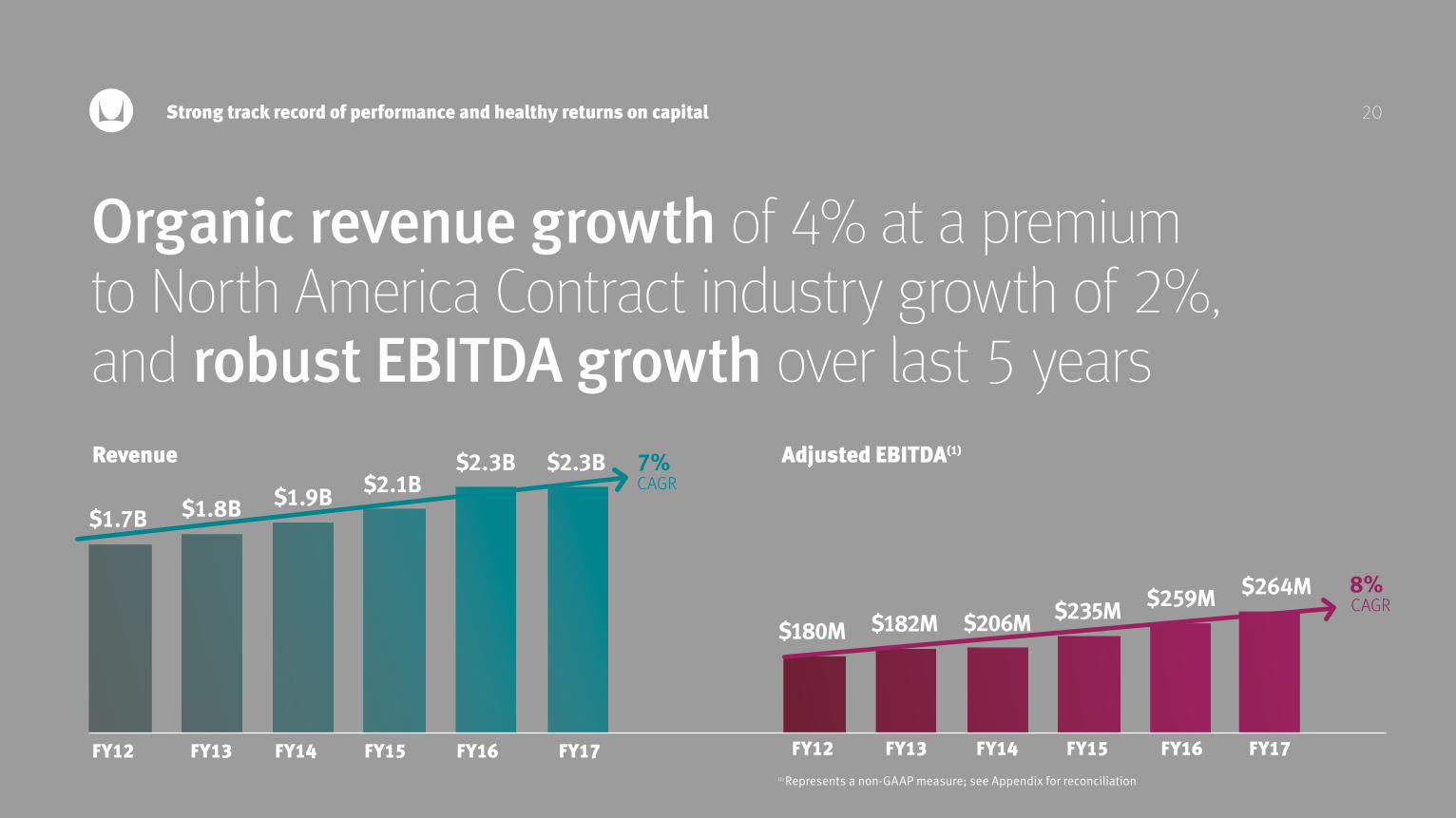

Organic revenue growth of 4% at a premium to North America Contract industry growth of 2%, and robust EBITDA growth over last 5 years

Strong track record of performance and healthy returns on capital

FY12 FY13 FY14 FY15 FY16 FY17

$2.1B$2.3B

$1.9B$1.8B$1.7B

FY12 FY13 FY14 FY15 FY16 FY17

$235M $259M$206M$182M$180M

Revenue Adjusted EBITDA(1)

(1) Represents a non-GAAP measure; see Appendix for reconciliation

8%

7%

CAGR

CAGR

20

$264M

2121

Focused acquisition strategy accelerates our performance

Strong track record of performance and healthy returns on capital

Entering New Areas:

Audience

Channel

Geography

Product

2222

Best-in-class lean enterprise delivers leverage

Strong track record of performance and healthy returns on capital

– Focused improvement through: • Customer first orientation • Waste reduction • Asset efficiency

– One of three U.S. companies showcased by Toyota Production System Support Center

– Further opportunity to spread more broadly and deeply through the organization and across the entire value chain

West Michigan sales per mfg. square foot

+28%

Manufacturing Quality

Engineering lead time for custom requests

+17% +39%

Improvement from FY11 to FY16

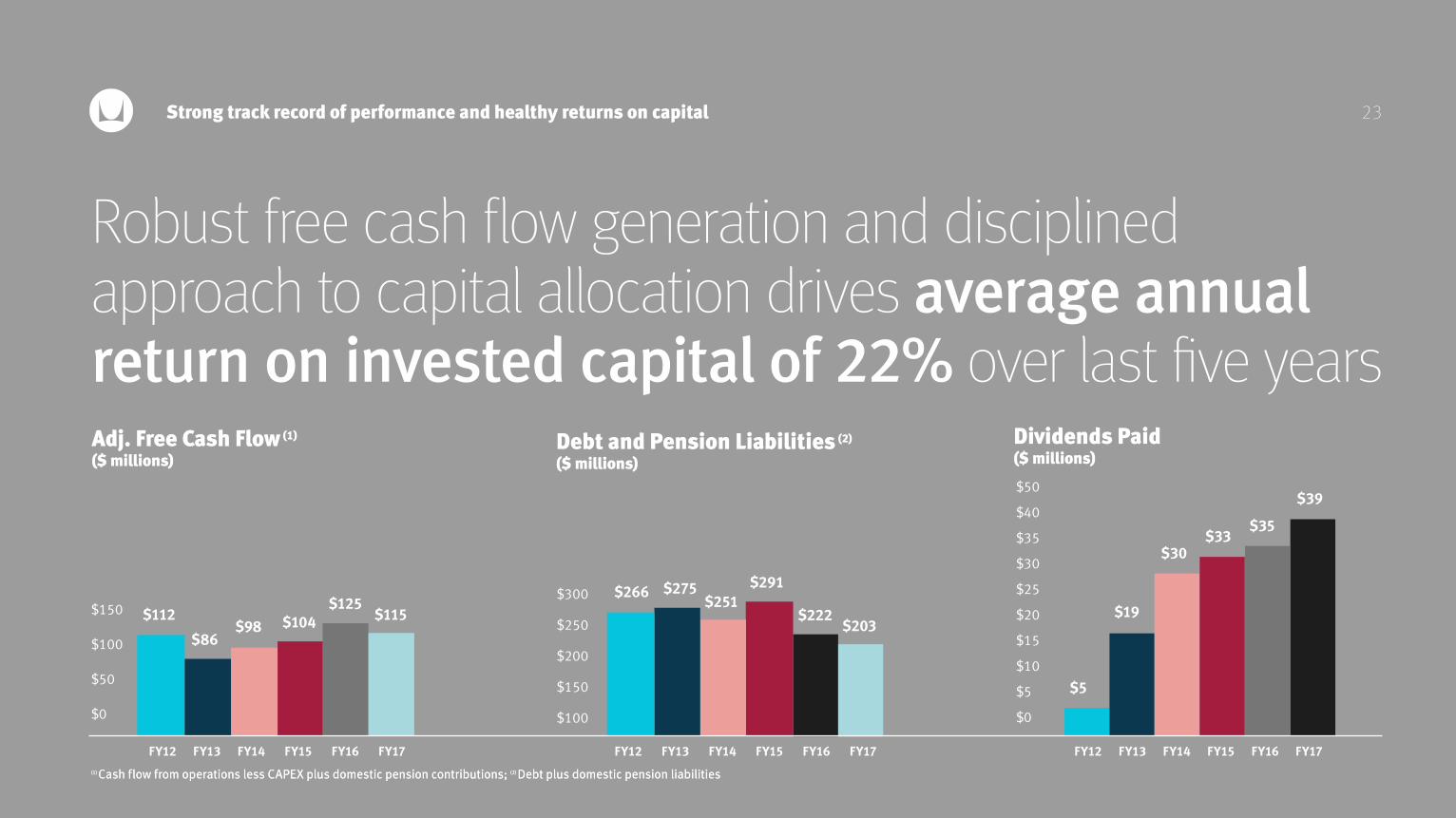

Robust free cash flow generation and disciplined approach to capital allocation drives average annual return on invested capital of 22% over last five years

Strong track record of performance and healthy returns on capital

(1) Cash flow from operations less CAPEX plus domestic pension contributions; (2) Debt plus domestic pension liabilities

23

(1) Cash flow from operations less CAPEX plus domestic pension contributions; (2) Debt plus domestic pension liabilities

FY12 FY13 FY14 FY15 FY16 FY17

$39

Adj. Free Cash Flow (1)

($ millions)

FY12 FY13 FY14 FY15 FY16 FY17

$150

$100

$50

$0

Debt and Pension Liabilities (2)

($ millions)

$300

$250

$200

$150

$100

$125$115

FY12 FY13 FY14 FY15 FY16 FY17

Dividends Paid($ millions)

$35

$50

$40

$35

$30

$25

$20

$15

$10

$5

$0

$98$112

$86$104

$266 $275$251

$291

$222$203

$5

$19

$30$33

2424

Compelling financial outlook and opportunity for margin expansion

25

Housing GDP Forecast

Existing Home Sales (thousands of units)

Housing Starts(thousands of units)

2015 2016 2017 2018

5,250 5,450 5,640 5,806

History Forecast

16.7

2013

17.4

2014

18.2

2015

18.3

2016

19.3

2017

20.2

2018

Forecast

2015 2016 2017 2018

1,1121,174 1,265 1,375

History Forecast

Supportive industry trends

Compelling financial outlook and opportunity for margin expansion 25

Source: BIFMA (May 2017)

Source: World Bank (June 2017)Source: National Association of Realtors (June 2017)

AIA Consensus Construction Forecast

Office (% YOY Growth)

2018

2017

4.6%

10.6%

Jan 2017

201720182019

UK Europe & Cent. Asia

Middle East & N. Africa

IndiaChina Mexico

2.5%2.7%2.8%

2.1%

3.1%2.9%

6.5%7.2%

7.5%7.7%

1.8%2.2%

2.5%

6.3% 6.3%

1.2%1.3%1.3%

North America Sales (in US$ billions) U.S. Architects Billing IndexSource: American Institute of Architects

58

56

54

52

50

48

46

44Ja

n-13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sept

- 15

Nov

- 15

Jan-

16

Ma-

16

May

-16

Jul-1

6

Sept

-16

Nov

-16

Dec

-16

Jan-

16

Feb-

16

Mar

-16

Apr-

16

May

-16

Opportunity for continued above-average revenue performance over the next three to five years

Compelling financial outlook and opportunity for margin expansion

Core Contract Industry 1-3%New Products and Initiatives 1-1.5% Consumer Growth 1-1.5%

Estimated Annual Organic Revenue Growth 3-6%Targeted Acquisitions 1-2%

Estimated Annual Revenue Growth Including Acquisitions 4-8%

Revenue

26

Operating income growth of 2x to 2.5x the rate of organic revenue growth

Compelling financial outlook and opportunity for margin expansion

– Structurally higher operating margins driven by: • Expanding business and channel mix • Consumer growth and higher exclusive product mix • Volume leverage • Lean enterprise focus • Cost savings initiative targeting $25M to $35M in annual savings by FY20

27

28

Our Compelling Story

Investment thesis

Compelling financial outlook and opportunity for margin expansion

Powerful brands deliver design and innovation leadership

A higher ambition culture

Unique combination of value-drivers enabling above industry-average growth

Strong track record of performance and healthy returns on capital

Recent Quarterly Financial Trends

30Recent Quarterly Financial Trends

Quarterly Net Sales + Orders ($ millions) Gross Margin and Adjusted Operating Margin (% net sales)

Quarterly Operating Expenses ($ millions)

Net SalesOrders

Gross Margin %Adjusted Operating Income %

Q1 FY17Q2 FY17Q3 FY17Q4 FY17

Q1 FY17Q1 FY17

Q2 FY17Q2 FY17

Q3 FY17Q3 FY17

Q4 FY17Q4 FY17

$167

38.4% 37.7%

9.4%

37.2%

8.8%

38.3%

7.0%10.2%

$158 $162

$599$578 $577

$525

$174

$596$576 $568$543

$600

$500

$400

$300

$200

50.0%

40.0%

30.0%

20.0%

10.0%

0.0%

$190

$170

$150

$130

$110

$90

$70

$50

Q4 net sales and orders decreased 0.9% and 6.3%, respectively, from the prior year; on an organic basis, excluding the impact of dealer divestitures, the impact of Q4 orders from a Q3 increase and foreign exchange, sales increased 2.7%, while orders were essentially flat compared to the prior year.

Gross margin in Q4 declined 40 bps from the prior year primarily due to higher commodity costs and discounting levels, offset by price realization.

EPS in Q4 totaled $0.55 per share; $0.64 per share on an adjusted basis.

31Recent Quarterly Financial Trends

Quarterly Cash Flow from Operations ($ millions) Rolling 4 Qtr Coverage Ration (EBITDA(1) to Interest)

Rolling 4 Qtr Leverage Ration (Debt to EBITDA)(1)

Q1 FY17Q2 FY17Q3 FY17Q4 FY17

Q1 FY17Q2 FY17Q3 FY17Q4 FY17

Q1 FY17Q2 FY17Q3 FY17Q4 FY17

0.9

Bank Covenant < 3.5

0.80.9

0.8

$80 18.0

$30

18.3

$60

17.9

$28

17.9$90$80$70$60$50$40$30$20$10$0

20.018.016.014.012.010.08.06.04.02.00.0

4.0

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

Q4 ending cash and equivalents totaled $96 million.

LT Debt maturity schedule:

–PPN ($150M) due 2018 –PPN ($50M) due 2021 –Revolver ($0M) due 2021

Availability of $392 million on the revolving line of credit at the end of Q4.

CAPEX totaled $17 million in Q4 and $87 million for the full fiscal year.

Q4 dividends paid totaled $10 million and share repurchases of $7 million. (1) Represents a Non-GAAP Measure, see Appendix for reconciliation

Bank Covenant > 4.0

32Recent Quarterly Financial Trends

Guidance as provided in July 5, 2017 earnings press release:

Q1 Fiscal 2018

Net Sales $570 to $590 million

Gross Margin % 37.5% to 38.5%

Operating Expenses $166 to $170 million

Effective Tax Rate 30.5% to 32.5%

Earnings Per Share, Diluted $0.55 to $0.59

Appendix

Segment Overviews

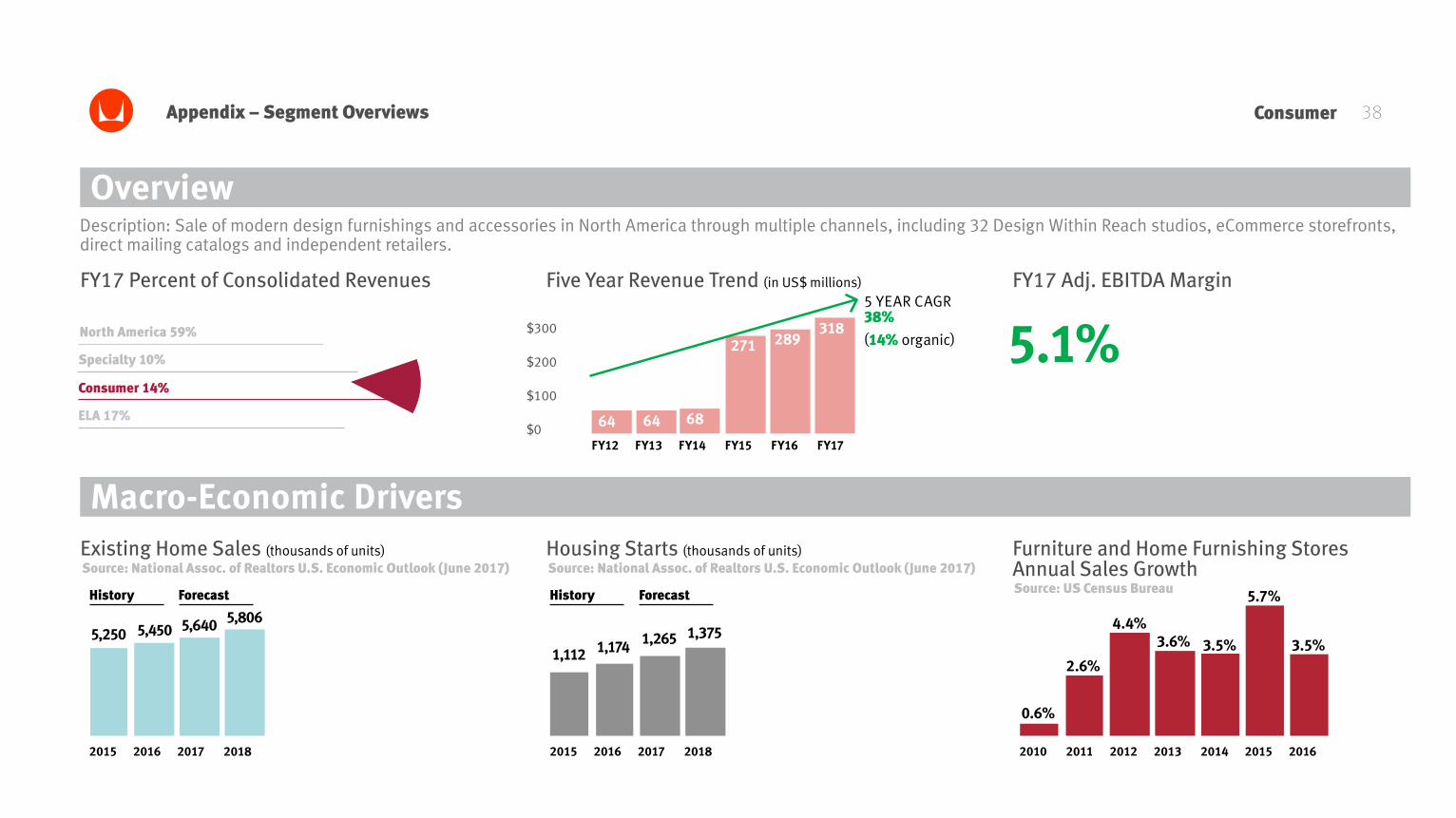

35Appendix – Segment Overviews

Overview

FY17 Percent of Consolidated Revenues

Macro-Economic Drivers

Five Year Revenue Trend (in US$ millions) FY17 Adj. EBITDA Margin

13.4%

Description: Design, manufacture and sale of furniture products for office, education and healthcare environments in the United States and Canada

Source: BIFMA, May 2017North America Sales (in US$ billions) Healthcare Construction Spending (in US$ billions)

FY12 FY13 FY14 FY15 FY16 FY17

5 YEAR CAGR 2%(3% organic)

Other Leading Economic Indicators include: Corporate profitability, service sector employment, Architectural Billings Index (ABI), Office vacancy rates, CEO and small business confidence, Non-residential Construction

North America Furniture Solutions

Source: U.S. Census Bureau and AIA Fcst, Jan 2017

201

3

201

4

201

5

201

6

2017

2018

2002

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

2017

2018

History Forecast History Forecast

Education Construction Spending (in US$ billions)Source: U.S. Census Bureau and AIA Fcst, Jan 2017

2002

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

2017

2018

History Forecast

70.5 71.2 72.377.1 86.0

98.4104.1 103.1

88.2 88.794.3 100.6

83.579.784.684.779.1

27.5 29.434.1 36.7

39.545.0

47.7 47.0

39.943.4

45.6

41.440.738.4

41.839.7 40.7

1,219 1,222 1,216 1,242$1500

$1300

$1100

$900

$700

$500

North America 59%

Specialty 10%

Consumer 14%

ELA 17%

16.717.4

18.2 18.3 19.320.2

1,332 1,342

36Appendix – Segment Overviews

FY17 Percent of Consolidated Revenues FY16 Adj. EBITDA Margin

Source: CSIL (December 2016)Regional Office Furniture Consumption (in US$ billions) GDP Forecast

201720182019

Region Annual 5 Year CAGR Consumption

Europe $8.7 2.1%China $11.1 7.6%India $2.1 4.3%Brazil $1.3 -10.0%Mexico $0.3 -8.0%

Source: World Bank (June 2017)

10.5%

Overview

Macro-Economic Drivers

Description: Design, manufacture and sale of furniture products primarily for office settings in EMEA (39% of sales in FY17), Latin America (21% of sales in FY17) and Asia-Pacific (41% of sales in FY17)

ELA Furniture Solutions

North America 59%

Specialty 10%

Consumer 14%

ELA 17%

Five Year Revenue Trend (in US$ millions)

413

5 YEAR CAGR 2%(5% organic)

FY12 FY13 FY14 FY15 FY16 FY17

347 377 392 386410

$500

$400

$300

$200

$100

$0

UK Europe & Cent. Asia

Middle East & N. Africa

IndiaChina Mexico

2.5%2.7%2.8%

2.1%

3.1%2.9%

6.5%7.2%

7.5%7.7%

1.8%2.2%

2.5%

6.3% 6.3%

1.2%1.3%1.3%

37

North America 59%

Specialty 10%

Consumer 14%

ELA 17%

FY17 Percent of Consolidated Revenues Five Year Revenue Trend (in US$ millions) FY17 Adj. EBITDA Margin5 YEAR CAGR 20%(6% organic) 11.1%

SpecialtyAppendix – Segment Overviews

FY12 FY13 FY14 FY15 FY16 FY17

Overview

Macro-Economic Drivers

Description: Design, manufacture and sale of high-craft furniture products and textiles focused on architect and design specifiers. The Specialty portfolio includes Geiger wood products, Maharam textiles and Herman Miller Collection products.

Annual Fabric Sales (in US$ millions)Source: ACT Financial Survey

AIA Consensus Construction Forecast (% YOY Growth)Source: The American Institute of Architects, Jan 2017

2017 2018

Non-Residential 5.6% 4.9%Commercial Total 8.3% 4.4%Office 10.6% 4.6%Health 4.9% 4.9%Education 6.3% 6.7%Hotel 7.2% 1.8% 2009 2010 2011 2012 2013 2014 2015

738 814 895929 990

760

1,069

94 112

206 220

$250

$200

$150

$100

$0

232 232

U.S. Architects Billing IndexSource: The American Institute of Architects

58

56

54

52

50

48

46

44

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sept

- 15

Nov

- 15

Jan-

16

Ma-

16

May

-16

Jul-1

6

Sept

-16

Nov

-16

Dec

-16

Jan-

16

Feb-

16

Mar

-16

Apr-

16

May

-16

38

FY17 Percent of Consolidated Revenues Five Year Revenue Trend (in US$ millions) FY17 Adj. EBITDA Margin

64 64 68

271

5 YEAR CAGR 38%(14% organic) 5.1%

ConsumerAppendix – Segment Overviews

FY12 FY13 FY14 FY15 FY16 FY17

Overview

Macro-Economic Drivers

Description: Sale of modern design furnishings and accessories in North America through multiple channels, including 32 Design Within Reach studios, eCommerce storefronts, direct mailing catalogs and independent retailers.

Source: National Assoc. of Realtors U.S. Economic Outlook (June 2017)Existing Home Sales (thousands of units) Housing Starts (thousands of units) Furniture and Home Furnishing Stores

Annual Sales Growth

2010 2011 2012 2013 2014 2015 2016

0.6%

2.6%

4.4%3.6% 3.5%

5.7%

3.5%

Source: US Census Bureau

2015 2016 2017 2018

5,250 5,450 5,640 5,806

Source: National Assoc. of Realtors U.S. Economic Outlook (June 2017)

History Forecast

2015 2016 2017 2018

1,174 1,265 1,375

History Forecast

1,112

North America 59%

Specialty 10%

Consumer 14%

ELA 17%

$300

$200

$100

$0

289318

39

This presentation contains Organic Sales Growth, Adjusted EBITDA, Adjusted EBITDA ratios, Adjusted Operating Earnings, and Adjusted Earnings Per Share, all of which constitute non-GAAP financial measures. Each of these financial measures is calculated by excluding items the Company believes are not indicative of its ongoing operating performance. The Company presents these non-GAAP financial measures because it considers them to be important supplemental indicators of financial performance and believes them to be useful in analyzing ongoing results from operations.

These non-GAAP financial measures are not measures of financial performance under GAAP and should not be considered alternatives to GAAP. Non-GAAP financial measures have limitations as analytical tools and should not be considered in isolation or as a substitute for analysis of the Company’s results as reported under GAAP. In addition, you should be aware that in the future the Company may incur expenses similar to the adjustments presented.

Appendix –Reconciliation of Non-GAAP Measures

40Appendix –Reconciliation of Non-GAAP MeasuresOrganic Sales Growth (Decline) by Reportable Segment ($ Millions); (unaudited)

Sales, as reported

Proforma Adjustments Dealer DivestituresCumulative foreign exchangeAcquisition - base year

Sales, pro forma

Compound Annual Growth Rate, as reported Compound Annual Growth Rate, pro forma

$ 1,218.5

(70.3)-

-

$ 1,148.2

$ 1,724.1

(95.3) - (7.0)

$ 1,621.8

$ 347.3

(25.0)-

(7.0)

$ 315.3

$ 94.1

---

$ 94.1

$ 64.2

---

$ 64.2

$ 1,342.2

(16.6) 25.6

-

$ 1,351.2

2.0% 3.3%

$ 2,278.2

(16.6)

88.2(353.2)

$ 1,996.6

5.7% 4.2%

$ 385.5

- 60.3

(51.4)

$ 394.4

2.1% 4.6%

$ 232.4

-

1.0 (107.5)

$ 125.9

19.8% 6.0%

$ 318.1

- 1.3

(194.3)

$ 125.1

37.7% 14.3%

North America ELA Specialty Consumer Total

2012 2012 2012 2012 20122017 2017 2017 2017 2017

41Appendix –Herman Miller Inc. Reconciliation of Non-GAAP MeasuresAdjusted EBITDA by Reportable Segment ($ Millions) (unaudited)

Segment Operating EarningsAdd: Allocated Depreciation & AmortizationAdd: Acquisition-related AdjustmentsAdd: Legacy Pension ExpensesAdd: Restructuring/Impairment ExpensesLess: POSH Contingent Consideration ReductionAdjusted EBITDARevenue by SegmentAdjusted EBITDA Margin

Segment Operating EarningsAdd: Allocated Depreciation & AmortizationAdd: Acquisition-related AdjustmentsAdd: Legacy Pension ExpensesAdd: Restructuring/Impairment ExpensesLess: Other, netLess: POSH Contingent Consideration ReductionAdjusted EBITDARevenue by SegmentAdjusted EBITDA Margin

Segment Operating EarningsAdd: Allocated Depreciation & AmortizationAdd: Acquisition-related AdjustmentsAdd: Restructuring/Impairment ExpensesLess: Nonrecurring gainsOther, netAdjusted EBITDARevenue by SegmentAdjusted EBITDA Margin

$ 96.928.7

----

$ 125.6$ 1,218.5

10.3%

$ (27.0)26.8

-147.0

---

$ 146.8$ 1,216.3

12.1%

$ 152.027.9

----

$ 179.9$ 1,331.8

13.5%

$ 32.15.7

----

$ 37.8$ 347.3

10.9%

$ 23.17.6

----

(2.6)$ 28.1

$ 392.27.2%

$ 35.38.5

--

(6.1)-

$ 37.7$ 412.6

9.1%

$ 1.12.2

----

$ 3.3$ 94.1

3.5%

$ (5.3)6.81.4

12.2---

$ 15.1$ 205.8

7.3%

$ 16.47.4

----

$ 23.8$ 231.8

10.3%

$ 14.10.7

----

$ 14.8$ 64.223.1%

$ 9.91.2

-5.2

---

$ 16.3$ 67.724.1%

$ 8.18.6

----

$ 16.7$ 288.7

5.8%

$ (6.6)---

5.4-

$ (1.2)-

0.0%

$ (26.4)---

26.5--

$ 0.1-

0.0%

$ (0.3)0.6

---

0.5$ 0.8

-0.0%

$ 137.637.3

--

5.4-

$ 180.3$ 1,724.1

10.5%

$ (25.7)42.4

1.4164.4

26.5-

(2.6)$ 206.4

$ 1,882.011.0%

$ 211.553.0

--

(6.1)0.5

$ 258.9$ 2,264.9

11.4%

$ 76.628.0

-26.5

--

$ 131.1$ 1,221.9

10.7%

$ 125.226.5

-----

$ 151.7$ 1,241.9

12.2%

$ 137.732.0

-10.3(0.7)

-$179.3

$ 1,342.213.4%

$ 24.76.6

----

$ 31.3$ 377.3

8.3%

$ 25.98.2

-----

$ 34.1$ 409.9

8.3%

$ 30.88.8

-1.0

--

$ 40.6$ 385.5

10.5%

$ 1.82.4

-1.7

--

$ 5.9$ 111.7

5.3%

$ 13.57.4

-----

$ 20.9$ 219.9

9.5%

$ 17.77.5

-0.6

--

$ 25.8$ 232.4

11.1%

$ 13.60.6

----

$ 14.2$ 64.022.2%

$ 14.77.37.8

----

$ 29.8$ 270.5

11.0%

$ 5.310.2

-0.6

--

$ 16.1$ 318.1

5.1%

$ (1.8)---

1.2-

(0.6)-

0.0%

$ (15.9)0.42.2

-12.7(0.7)

-$ (1.3)

-0.0%

$ (0.7)0.4

---

2.0$ 1.7

-0.0%

$ 114.937.6

-28.2

1.2-

$ 181.9$ 1,774.9

10.2%

$ 163.449.810.0

-12.7(0.7)

-$ 235.2

$ 2,142.211.0%

$ 190.858.9

-12.5(0.7)

2.0$ 263.5

$ 2,278.211.6%

NA NA

NA

NA

ELA ELA

ELA

ELA

Specialty Specialty

Specialty

Specialty

2012 Actual 2013 ActualConsumer Consumer

Consumer

Consumer

Corporate Corporate

Corporate

Corporate

Consol.

NA ELA Specialty2014 Actual 2015 Actual

Consumer Corporate Consol.

NA ELA Specialty2016 Actual 2017 Actual

Consumer Corporate Consol.

Consol.

Consol.

Consol.

42Appendix Adjusted Operating Earnings and Adjusted Earnings Per Share ($ millions, except for per share amounts) (unaudited)

Operating Earnings (GAAP)Operating Earnings (%)Add: Restructuring and Impairment Expenses Adj. Operating Earnings (non-GAAP)Adj. Operating Earnings (%)

Earnings per Share - DilutedAdd: Restructuring ExpensesAdjusted Earnings per Share - Diluted

Net Sales

Q4 FY17 Q4 FY17

$ 577.2

$ 49.8 8.6%

8.8$ 58.6

10.2%

$ 0.55$ 0.09 $ 0.64

Adjusted Operating Earnings Adjusted Earnings per Share

43Appendix Adjusted EBITDA and Adjusted EBITDA Ratios (Bank) ($ millions) (unaudited)

Earnings Before Income Taxes (EBT)Add: Depreciation Amortization InterestOther Adjustments(1)

Adjusted EBITDA - Bank

Total Debt, End of Trailing Period (includes outstanding LC’s)

Rolling 4-Quarter Debt-to-Adj. EBITDA

Rolling 4-Quarter Adj. EBITDA-to-Interest

Q1 FY17 Q2 FY17 Q3 FY17 Q4 FY17

184.6 177.6

$ 271.5 $ 272.9

$ 243.3 $ 211.6

0.9 0.8

17.9 18.0

192.4

$ 273.3

$ 228.5

0.8

17.9

199.1

$ 278.8

$ 242.8

0.9

18.3

50.1 52.96.0 6.0

15.2 15.215.6 21.2

47.76.0

15.311.9

47.16.0

15.211.4

Adjusted EBITDA (Bank) RatiosTrailing 4-Quarter Period Ended

(1) “Other Adjustments” include, as applicable in the period, charges associated with business restructuring actions, non-cash stock-based compensation, as described in lending agreements.