nasscom report on it adoption in the auto component industry

TRANSCRIPT

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 1/54

IT Adoption in the

Indian Auto Component Industry

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 2/54

IT Adoption in the

Indian Auto Component Industry

National Association of Software and Service Companies

International Youth Centre, Teen Murti Marg, Chanakyapuri, New Delhi-110 021, India

Phone: 91 11 2301 0199 Fax: 91 11 2301 5452 Email: [email protected]

Website: www.nasscom.in

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 3/54

Copyright ©2007

National Association of Software and Service Companies

International Youth Centre, Teen Murti Marg, Chanakyapuri, New Delhi -110 021, India

Phone: 91 11 2301 0199 Fax: 91 11 2301 5452 E mail: [email protected]

First Print: December 2007

Published by

NASSCOM, New Delhi

Designed & Produced by

Creative Inc.

Phone: 91 11 4163 4469

Printed at

P. S. Press Services

Disclaimer

The information contained herein has been obtained from sources believed to be reliable. The

information contained in sections of the report reflects data that was derived from both public

and confidential information collected during the conduct of the study by NASSCOM. Readers

should note that NASSCOM has not independently verified all of the data and assumptions used

in these analyses. Each reader of this report should conduct their own independent evaluation

of the information provided herein. NASSCOM shall have no liability for errors, omissions or

inadequacies in the information contained herein or for interpretations thereof.

The material in this publication is copyrighted. No part of this can be reproduced either on paper

or electronic media without permission in writing from NASSCOM. Request for permission to

reproduce any part of the report may be sent to NASSCOM.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 4/54

Chapter 1: Introduction

The Indian Auto Component Industry .............................................................. 12

IT adoption in the Auto Component Industry ................................................... 14

Study objectives and methodology .................................................................. 15

Chapter 2: Business challenges and current state of IT adoption

Challenges faced by business heads .............................................................. 17

Challenges faced by IT heads ......................................................................... 20

Factors infl uencing IT adoption ....................................................................... 21

Measuring IT adoption effectiveness ............................................................... 22

Criticality of business processes ..................................................................... 23

IT adoption – implemented applications/systems ............................................ 27

IT budgets ........................................................................................................ 32

IT workforce and outsourcing .......................................................................... 33

Key features of IT adoption in auto component fi rms ...................................... 35

Chapter 3: Mapping supply chain strategies for

auto component fi rms

Linking capability levels to manufacturing practices ........................................ 37

Chapter 4: Evolving an IT strategy for different levels

Aligning IT strategy with manufacturing capabilities ........................................ 42

The MSC perspective ...................................................................................... 47

Chapter 5: Looking ahead

Call for action: Strategies for stakeholders ...................................................... 49

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

Table of Contents

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 5/54

Foreword

4

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 6/54

5

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 7/54

6

Foreword

The Indian Auto Component Industry has been amongst the drivers of the renaissance inIndia’s manufacturing sector, and given its strong performance over the last few years, it is

rightfully considered a ‘sunrise’ sector of the Indian economy. Years of sustained efforts by the

auto component fi rms and a pro-active government policy framework have transformed a

relatively small and unsophisticated domestic industry into one with world-class manufacturing

practices and a global footprint.

With success come greater challenges and expectations. To sustain and accelerate the current

growth trajectory and develop new competitive advantages, the Indian auto component fi rms will

need to continuously strive to increase their effi ciency, quality and value proposition. In this, IT

will increasingly play a crucial role by helping the auto component fi rms achieve step changes

in productivity benchmarks through the entire range of manufacturing processes and in enabling

the fi rms to seamlessly integrate with their global and domestic customers and suppliers.

Unfortunately, IT penetration in Indian manufacturing, especially among the SME segment,

continues to lag behind comparator industries in other countries. In order to increase

IT penetration, it is vitally important to understand the IT adoption challenges faced by the

manufacturing industry fi rms and especially the SME segment. Developing this understanding

is crucial to ensure that IT investments by the fi rms are deployed where they can result in

the greatest impact on a fi rm’s competitiveness and help the fi rm to derive positive outcomes

from the IT investments.

It is with this aim that this study has been undertaken. This report seeks to bring an understanding

of IT adoption thresholds, challenges and processes in the different segments of the Indian

auto component sector. This has been utilised to develop IT adoption strategies based upon

the manufacturing capabilities of the different segments of the Auto Component Industry.

This will enable the auto component fi rms to align their IT investments with the business

objectives, while enabling the IT fi rms to develop solutions specifi c to the needs of the different

segments of the industry.

NASSCOM is deeply committed to the development of the domestic IT market, since a strong

and vibrant domestic market is crucial to the continued growth of the Indian IT industry.

We hope this report will stimulate useful discussions and more importantly, actions onhow individual fi rms in the auto component and IT industries, as well as other ecosystem

partners such as the government, industry bodies, academia and others, can together work

to accelerate the adoption of IT by the Indian Auto Component Industry so as to further

stimulate its growth.

Kiran Karnik

President, NASSCOM

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 8/54

7

The Indian Automobile Component Industry has emerged as a sunrise sector of the Indianmanufacturing industry and a key stakeholder in the global automobile manufacturing industry.

While India’s share of the global auto components trade of US$ 185 billion (Rs 75,850 crores)

is only 0.4 percent currently, India is estimated to have the potential to become one of the top

fi ve auto component economies by 2025. By 2015, the global Auto Component Industry is

expected to source goods worth US$ 700 billion (Rs 2,870,000 crores) from low-cost countries

like India.

According to the Auto Component Manufacturers’ Association (ACMA), the Indian auto

component sector generated sales of about US$ 15 billion (Rs 61,500 crores) in fi scal year

2006-07, including US$ 2.8 billion (Rs 11,480 crores) worth of exports. The industry has

been experiencing a high growth rate of 20 per cent over the period 2000-05 and is expectedto grow at a CAGR of 17 per cent over the period 2006-14. Similarly, while growth rate of

exports has been 25 per cent during 2000-05, the exports are expected to grow by a CAGR of

34 per cent during 2006-14.

To sustain the current growth trajectory and face the increasing competition in the global and

domestic markets, the Indian auto component fi rms will have to create a new set of competitive

advantages based on value-capture rather than cost reduction. Achieving this will not be easy

and the Indian fi rms will have to focus on moving up the value curve and relentlessly increasing

fi rm level productivity through adoption of global manufacturing best practices. IT will be a key

enabler for the Indian auto component fi rms to achieve these aspirations.

An increase in IT adoption will provide the necessary productivity benefi ts only when the IT

investments are made in business processes which contribute to a fi rm’s competitiveness.

Thus, it is important to evaluate IT adoption at the level of business processes instead of at the

fi rm level. This understanding will fi rstly, help the automobile component fi rms to align their IT

investments with business objectives and secondly, help the IT fi rms to develop solutions which

are specifi c to the requirements of the Automobile Component Industry. The auto component

manufacturing sector in India has seen tremendous growth in recent years and therefore one

expects this sector to be ahead of others in IT adoption. An understanding of IT adoption

processes in this sector can also be useful in defi ning effective IT adoption strategies for this

as well as other sectors.

Current status of IT adoption in the Indian Auto Component Industry

Studies have shown that the adoption of information technologies can increase the performance

of fi rms. Despite these advantages, IT adoption among manufacturing fi rms in India is rather

low. The diversity in the Indian manufacturing sector is very high; apart from differences in fi rm

size, sector specifi c peculiarities can also play a role in the processes of IT adoption. While

policy initiatives to encourage adoption have been explored, it is equally important to understand

the process of IT adoption by fi rms along with the constraints faced by them.

Executive Summary

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 9/54

8

The need of the auto component fi rms to integrate various functions and processes hasdriven them to invest in IT, and as a result, in fi rms that have implemented IT, there has been

a considerable increase in the productivity as well as revenues. However, very few fi rms have

aligned their IT investments with business objectives or adopted a clutch of applications to

maximise the potential of effi ciency gains and this obviously has an adverse effect on the

effi cacy of IT adoption.

The current study conducted by NASSCOM is based on an survey of 158 fi rms including

small, medium and large automobile component manufacturers across the key automobile

manufacturing clusters in Delhi, Mumbai, Chennai, Pune and Bangalore. Some key highlights

of the current IT adoption in the Indian Auto Component Industry, identifi ed through the survey

are as follows:• Different fi rms appear to be devising differing strategies for IT adoption and size of the

fi rm seems to be defi ning the trajectory that a fi rm will adopt for IT adoption. Firms are at

very different levels of IT implementation and the IT strategy of many fi rms is not based

on a judicious process improvement strategy.

• Supply Chain Management (SCM) has been ranked as the most critical challenge by

Business Unit (BU) heads. Some of the other challenges include fl uctuations in raw

material costs, meeting customer demands for product quality & timelines and procurement

of raw materials, reiterating the importance of the supply chain.

• The three most critical business processes identifi ed by the fi rms are:

Order receipt and demand managementProduction planning

Order processing

• Quick access to reliable business information is a key bottleneck as the auto component

fi rms possess disparate systems including manual paper based processes that lead to

disconnect amongst the supply chain constituents. This has two major impacts – fi rstly,

it impedes real-time decision making and secondly, it results in creation of ad-hoc sources

of information which further exacerbate the problem of availability of accurate data.

The survey reveals some variance in the criticality of business processes by fi rm size.

While for medium and large fi rms the three processes mentioned above remain the most

critical, for small fi rms, order processing is replaced by material handling.

• BU heads expect IT to play an important role in addressing their business challenges.

The key expectations of the BU heads from IT are meeting customer requirements

for timely delivery and product quality, tracking production costs and quick access to

business information.

• The IT heads have identifi ed the lack of alignment between business goals and IT

initiatives as a major challenge. The IT heads also fi nd it diffi cult to justify the current

levels of investments in any IT initiative, as the time for the complete deployment of the

initiative is quite long as compared to many other business function initiatives and the

impact of these IT initiatives and their effectiveness is also felt after a period of time.

1.2.

3.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 10/54

• The most common measure of IT effectiveness, amongst the auto componentmanufacturers is increased productivity. While the measure of increased productivity for

IT effectiveness is the most preferred one for both BU heads as well as IT heads of fi rms

of all sizes, it is not entirely clear how it is measured. Increased customer satisfaction, is

also a key measure for evaluating IT effectiveness by auto component manufacturers.

However, in many fi rms, none of the metrics that were mentioned are actually used to

measure the IT effectiveness.

• Broadly, large fi rms are ahead of small and medium fi rms in the adoption of all application

systems and Enterprise Resource Planning (ERP) is the most widely adopted IT application

among auto component fi rms. However, very few fi rms adopt a clutch of applications to

maximise the potential of effi ciency gains and this obviously has an adverse effect on

the effi cacy of IT adoption. In the adoption of networking and groupware systems also,

large fi rms are generally ahead of the small and medium fi rms.

• The fi rms are undertaking IT investments to integrate the fi rm’s production facilities with

the other constituents of the supply chain, so that real-time accurate information on the

inventory, production schedule and materials is available as and when required. In order

to have better access to business information, many auto component fi rms have deployed

intranets which are made available to all the relevant in-house business functions and

enable effective planning and scheduling.

• During the year 2005-06, a majority of the surveyed auto component manufacturers hadtheir annual IT budgets to the tune of Rs.20 lakhs. Hardware forms the major proportion

of the current IT investments. The annual IT budget is expected to increase for a

majority (~90%) of auto component manufacturers in the coming years.

• Hardware maintenance appears to be the most outsourced IT service by the auto

component fi rms. The outsourced activities related to hardware maintenance include

management and functioning of offi ce hardware such as PCs, laptops, etc. In a majority of

auto component manufacturing companies that participated in the survey, less than 10 full

time employees take care of the IT service and support function, across all locations. Most

fi rms on average have 1-5 servers, 50-199 workstations and 10-99 network nodes.

Aligning IT strategy with supply chain capabilities

Firms in the Auto Component Industry grow by producing more complex products that have

higher value add and the situation in India is no different especially with the changes in the

product technology. The Indian Auto Component Industry comprises fi rms ranging from tiny

and small producers to large fi rms who supply to both the OEM and replacement markets.

As a result, there is enormous diversity in the intent and strategies of the fi rms in the auto

component sector.

9

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 11/54

10

What fi rms require is a good understanding of how they can compete by building distinctivecompetitive capabilities. While there is no one answer to building their capabilities through

adoption of world-class practices and IT, there is, however, a trajectory through which fi rms

could look to building capabilities and develop distinctive competitive stances. This trajectory

can be defi ned terms of various stages or Levels with each Level being defi ned by certain

operational characteristics.

• Level I fi rms are essentially producers that perform job work. Level I fi rms receive material

from their customers and they produce to the blueprint provided by them. Most often, these

fi rms are tiny to small in size and turnover, and produce exclusively for their customer

from a single facility. Very often, the process technology employed in these fi rms is old

and the equipment is second-hand and obsolete.• Level II fi rms are also Tier 3 suppliers and posses the same characteristics as Level I

fi rms except that they have more experience in contract manufacturing and have a higher

turnover as compared to their Level I counterparts.

• Level III fi rms are also often small in size but on the verge of entering medium scale.

While Level I & Level II fi rms may be performing machining operations, the Level III

manufacturers produce a part or whole of a component for the industry. Many of these

fi rms may not be dedicated to a single customer and produce similar components for

different customers. As a result, they need to develop systems for maintaining various

designs as well as capabilities to manufacture for varying customer requirements.

• Level IV fi rms are medium size fi rms with multiple plants and customers and are beginningto make the fi rst entry into global supply chains. These manufacturers produce to

order(s) as well as in anticipation of orders. These fi rms possess design capabilities and

are capable of modifying blueprints, which becomes a core competence for becoming

vendors for new customers. Since they supply to many customers, their manufacturing

facilities are amenable to cellular manufacturing layout with single piece fl ow that helps

them to reduce production lead times in a medium volume and medium to high product

variety environment.

• Level V fi rms are upper-medium or large fi rms and supply to the automobile OEMs as well

as in the replacement market and a large majority of these fi rms export and are part of

a global supply chain. They produce to fi rm orders as well as to stock, i.e. in anticipationof orders from customers. They supply many customers from multiple manufacturing

facilities located within the country and sometimes from manufacturing facilities located

outside the country.

The above categorisation of manufacturing capabilit ies defi nes the complexity of tasks that

an auto component fi rm may be able to perform and consequently indicates the nature of IT

solutions required. Low manufacturing capability fi rms are transaction oriented while those

with high capabilities will deploy sophisticated technologies and high-end decision making

tools. Most auto component fi rms (other than the Level V fi rms) are SMEs and are often low

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 12/54

11

in capability. As one moves up the pyramid of capability, the number of fi rms in those higher categories of capabilities become small.

The IT strategy of auto component manufacturers at different Levels could be evolved from

these requirements appropriately. It would be effective to recognise that fi rms at different Levels

have varying needs and therefore it would be useful to design Level specifi c IT strategy.

The key to successful IT interventions lies in recognising that the Indian Auto Component Industry

comprises fi rms that are at different stages of industrial development. As a consequence, the

fi rms possess a heterogeneous mix of IT capabilities, ranging from low-tech with no or little

IT knowledge to very sophisticated, providing IT related services to its own fi rms and others.

The challenge is to design appropriate interventions for these different categories of fi rmswhich are both cost-effective and result oriented. This objective gets further complicated by

the fact that most fi rms in the auto component sector are tiny to small (and sometimes medium

enterprises) whose ability and sometimes desire to invest in building capabilities through IT

interventions is limited. In addition, strong IT systems are required to meet compliance and

regulatory requirements either from governments or customers.

Given that most auto component fi rms are tiny to small fi rms with low IT capabilities, and use

PCs and simple software products, the challenge for large IT fi rms is to devise a service model

that will generate revenues to cover its higher overheads while the challenge for small/mid

sized IT fi rms is to convince auto component fi rms that they can deliver solutions which create

strong capabilities in the auto component fi rms. Perhaps a hub and spoke model can becreated where large IT fi rms could be involved in setting up network platforms for collaboration

between large and small auto component fi rms while the ‘last mile connectivity’ required for

actual execution of IT implementation and after-sales service is done by small IT fi rms using

the large fi rm’s platforms, tools and design capabilities.

Looking ahead

The IT and Auto Component Industry must visualise themselves differently if they are to move

to another stage of industrial development and consequently competitiveness. The goal must

be to create a sector where IT is seen as integral to the competitiveness of the industry andnot as a service often provided by external sources.

Based on the current status of IT adoption in the Indian Auto Component Industry, fi rms may

not have followed the manufacturing capability – IT adoption trajectory and therefore may have

over or under invested in IT. For example, fi rms that did not require ERP may have invested

in ERP and so on. The IT and auto component fi rms will have to collaboratively think about

future IT investments in order to create an environment where IT becomes an integral part

of the manufacturing operation and becomes capable of delivering competitive advantage at

various levels.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 13/54

Chapter 1: Introduction

1 1 lakh = 0.1 million2 1 crore = 10 million3 Rs 41 = 1US$

12

1. The Indian Auto Component Industry

The automobile industry, one of the most dynamic constituents of India’s manufacturing

sector produces approximately 75 lakh1 vehicles per year with two-wheelers constituting more

than three-fourths of the total number of units. The turnover of the automobile industry is around

Rs 150,000 crores2 and has grown rapidly in recent years (2006-2007). With a total investment

of more than Rs 50,000 crores, the industry provides employment to about 1.3 crore people.

The industry contributes close to 20 per cent of indirect tax revenue and exports more than

Rs 10,000 crores. The automobile industry is a crucial sector for the overall Indian economy

due to its signifi cant linkages with the rest of the economy. Among the forward linkages, the

ones with insurance and oil industry are important. Linkages with components, rubber, steel,

plastics and electronics constitute signifi cant backward linkages. The industry has a largeinternational outsourcing potential, and investments to enhance the sector’s competitiveness

can go a long way in making this possible.

Riding this success, and capitalising on the spiralling demand of domestic automobile OEMs,

the Indian Automobile Components Industry has transformed into one of India’s fastest growing

manufacturing sectors, and is rapidly attaining global competitiveness. The sector comprises

fi rms that range from tiny (with a turnover of less than few lakh rupees) to large (with a turnover

above Rs 500 crores).

India’s competitive advantage in this sector does not come from costs alone, but from its capability

to manufacture the entire range of auto components, such as engine parts, drive, transmissionparts, suspension and braking parts, electrical parts, and body and chassis parts. India’s Top 500

Companies, published by Dun & Bradstreet in 2006, listed 22 auto component manufacturers

as top companies in India with a total turnover of US$ 3 billion (Rs 12,300 crores)3.

According to the Auto Component Manufacturers’ Association (ACMA), the Indian auto

component sector generated sales of about US$ 15 billion (Rs. 61,500 crores) in fi scal year

2006-07, including US$ 2.8 billion (Rs 11,480 crores) worth of exports. The industry has been

experiencing a high growth rate of over twenty per cent during the period 2000-05 and is

expected to grow at a CAGR of 17 per cent over the period 2006-14. Similarly, while growth

rate of exports has been 25 per cent during 2000-05, the exports are expected to grow by a

CAGR of 34 per cent during 2006-14.

While India’s share of the global auto components trade of US$ 185 billion (Rs 758,500 crores)

is only 0.4 per cent currently, India is estimated to have the potential to become one of the

top fi ve auto component economies by 2025. By 2015, the global Auto Component Industry is

potentially expected to source nearly US$ 700 billion (Rs 2,870,000 crores) worth of products

from low-cost countries like India.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 14/54

13

ACMA forecasts that industry sales will grow to US$ 40 billion (Rs 164,000 crores) by 2016with US$ 20 billion (Rs 82,000 crores) coming from exports. Around 70 per cent of the exports

are sourced by global majors such as General Motors, Ford Motor and DaimlerChrysler who

source critical components, with engine parts making up nearly a third of all exports. A break-

up of the constituency of the exports by the auto component sector is as follows:

• Engine parts (31 per cent)

• Drive transmission and steering parts (19 per cent)

• Body and chassis (12 per cent)

• Suspension and braking parts (12 per cent)

• Equipment (10 per cent)• Electrical parts (9 per cent)

• Others (7 per cent)

According to ACMA, more than a third (36 per cent) of Indian auto component exports head

for Europe, with North America featuring a close second at 26 per cent. The composition of

exports in terms of the proportion of Original Equipment Manufacturer (OEM) and aftermarket

has undergone a sweeping change since the past decade. The ratio of OEM to aftermarket

has changed from 35:65 in the 1990s to 75:25 in 2006.

The quality consciousness of the industry matches global standards now. This is corroborated

by the fact that nine Indian companies in the automotive sector have received the coveted

Deming Prize, which is the largest number outside Japan.

Recognising the potential of the Auto Component Industry, the Government of India has not

only provided an enabling policy framework but also invested substantially to provide state-of-

the-art infrastructure for the industry. Some of the key initiatives include the following:

• Automatic approval for foreign equity investment up to 100 per cent for the manufacture

of auto components.

• Manufacturing and imports in this sector is free from licensing and approvals.

• No local content regulation in the Auto Component Industry.

• A reduction in customs duty – maximum level of 7.5 per cent – on key metallic raw

materials and inputs for the Auto Component Industry.

• Reduction of peak rates of duty from 15 to 12.5 per cent.

• Finalisation of the Automotive Mission Plan (AMP) 2006-16 for making India a preferred

destination for design and manufacture of automobile and automotive components.

• Reduced excise duty on small cars to 16 per cent, a step which is intended to propel India

as a global manufacturing hub for small cars and directly enable the auto component

supplier industry to attain volumes.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 15/54

14

• Setting up of the National Automotive Testing and R&D Infrastructure Project (NATRIP)at a total cost of US$ 388.5 million for enabling the industry to usher in global standards

of vehicular safety, emission and performance standards.

• Setting up an automobile testing and homologation centre, International Centre for

Automotive Technology (iCAT), at an investment of US$ 15.23 million which would act

as an accredited agency to approve homologation standards for automobiles.

2. IT adoption in the Indian Auto Component Industry

Studies have shown that the adoption of IT based technologies can increase the performance

of fi rms. Despite these advantages, IT adoption among manufacturing fi rms in India is rather low. While policy initiatives to encourage adoption have been explored, it is equally important

to understand the process of IT adoption by fi rms along with the constraints faced by them.

The diversity in the Indian manufacturing sector is very high; apart from differences in fi rm size,

sector specifi c peculiarities can also play a role in the process of IT adoption. Given this huge

diversity, it is important that the right sub-segments are identifi ed for IT diffusion initiatives so

that they have appropriate demonstration and spill-over effects.

The auto component manufacturing sector in India has seen tremendous growth in recent years

and therefore one expects this sector to be ahead of others in IT adoption. An understanding

of IT adoption processes in this sector can be useful in defi ning adoption strategies for this aswell as other sectors. Given the linkages of the Auto Component Industry with other sectors

mentioned earlier in this chapter, faster growth of this sector can have signifi cant ripple effects

in the rest of the economy.

A large majority of the fi rms (over 85 per cent) in the Auto Component Industry are SMEs.

These fi rms serve both the OEM as well as replacement demands and work with a variety of

technologies in areas of machining, electronics, plastics & rubber moulding, welding, casting &

forging, etc. These SMEs also vary considerably in terms of their capabilities depending upon,

often, on the markets that they serve, i.e., exports or domestic and within domestic – national

or regional. Increasing IT penetration in the SME segment of the auto component sector is a

critical enabler for enhancing their competitiveness.

Detailed fi rm level interviews conducted during the study have highlighted that the key business

challenges faced by the auto component manufacturers relate to raw material availability

and their price fl uctuations, gaps in real-time availability of business information and lack of

smoothness in business processes. Once the fi rms develop smooth information channels,

it enables them to track costs as well as delays in the various functional processes of the

enterprise. The study also reveals that supply chain is one of the most critical components of

the auto component business and that it has to be integrated for the timely and orderly fl ow

of material as well as fi nished products.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 16/54

15

The need of organisations to integrate various functions and processes has driven themto implement ERP, SCM and other similar packages, and as a result, in fi rms that have

implemented IT, there has been a considerable increase in the productivity as well as revenues.

However, very few fi rms adopt a clutch of applications to maximise the potential of effi ciency

gains and this obviously has an adverse effect on the effi cacy of IT adoption. The current study

has also shown that while a large majority of the fi rms in the Auto Component Industry have

invested in IT, these fi rms are not convinced about the effectiveness of these IT investments.

While BU heads expect IT to be a key enabler for them to address their business challenge,

the IT heads believe that the IT investments are often not aligned with the business objectives

and given the long gestation period of IT investments, it becomes diffi cult for them to justify

the IT investments.

3. Study objectives and methodology

Given the qualitative insights discussed in the above section, the key objectives of the study

are to:

• Understand IT deployment and its usage patterns in the various segments of the auto

component fi rms

• Identify stages of IT adoption and relationship between IT adoption and decision domains

(or business processes) for performance improvements

• Evolve an IT adoption strategy for different tiers of the fi rms

This report seeks to address the following issues in order to achieve the above objectives:

• Understand the extent of IT adoption in the auto component sector

Identifi cation of sub-sectoral patterns of adoption within the industry

Postulation of the strategies currently followed by fi rms in adoption of IT

Identifi cation of characteristics of fi rms that adopt IT

Reasons for deployment

Areas of deployment

• Identifi cation of the drivers of IT adoption in the auto component sector

Factors that support adoption of IT

Reasons for non-deployment of IT

• Analysis of adoption within fi rms – region-wise

• Identifi cation of stages of IT implementation based on extent of adoption and its

effective utilisation

• Exploring relationship between adoption, business processes (or decision domains) and

performance of fi rms

• Develop a strategy for the future

1.

2.

3.

4.

5.

1.

2.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 17/54

16

Imperatives for growthImpediments and ways to overcome them

Linking IT fi rms’ strategies to manufacturing requirements

Future and challenges

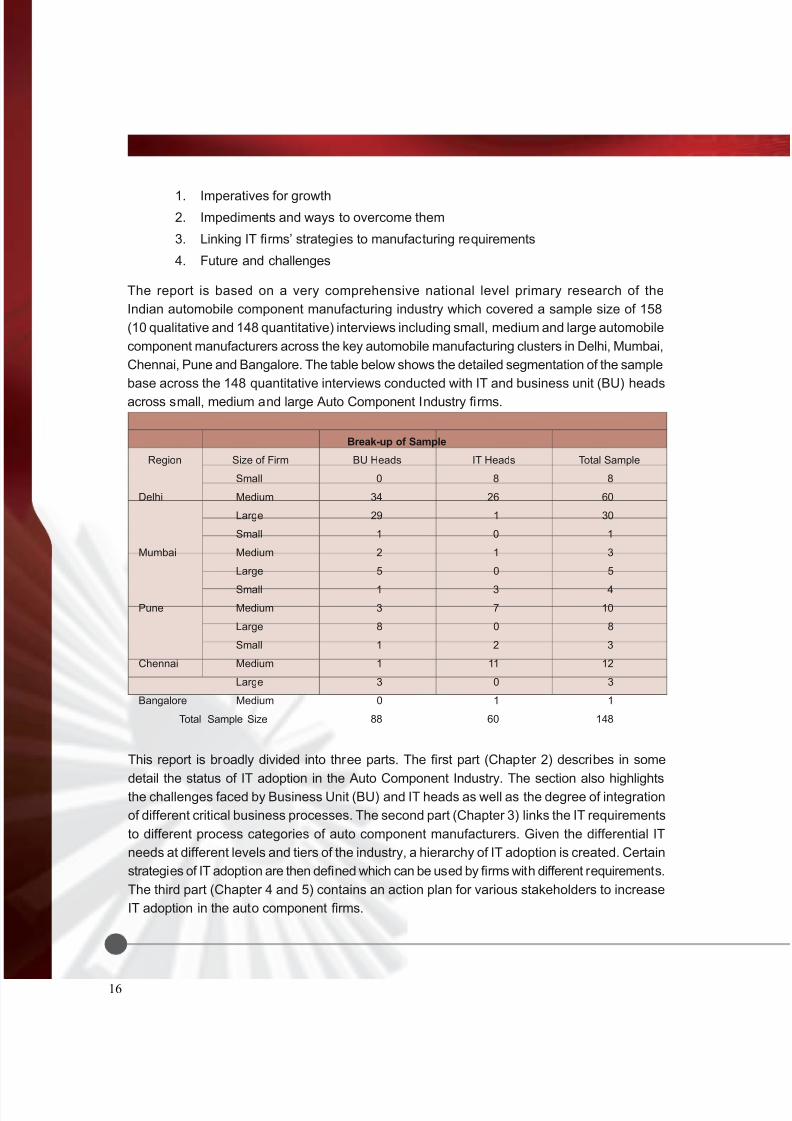

The report is based on a very comprehensive national level primary research of the

Indian automobile component manufacturing industry which covered a sample size of 158

(10 qualitative and 148 quantitative) interviews including small, medium and large automobile

component manufacturers across the key automobile manufacturing clusters in Delhi, Mumbai,

Chennai, Pune and Bangalore. The table below shows the detailed segmentation of the sample

base across the 148 quantitative interviews conducted with IT and business unit (BU) heads

across small, medium and large Auto Component Industry fi rms.

1.2.

3.

4.

Break-up of Sample

Region Size of Firm BU Heads IT Heads Total Sample

Delhi

Small 0 8 8

Medium 34 26 60

Large 29 1 30

Mumbai

Small 1 0 1

Medium 2 1 3

Large 5 0 5

Pune

Small 1 3 4

Medium 3 7 10

Large 8 0 8

Chennai

Small 1 2 3

Medium 1 11 12

Large 3 0 3

Bangalore Medium 0 1 1

Total Sample Size 88 60 148

This report is broadly divided into three parts. The fi rst part (Chapter 2) describes in some

detail the status of IT adoption in the Auto Component Industry. The section also highlights

the challenges faced by Business Unit (BU) and IT heads as well as the degree of integration

of different critical business processes. The second part (Chapter 3) links the IT requirements

to different process categories of auto component manufacturers. Given the differential IT

needs at different levels and tiers of the industry, a hierarchy of IT adoption is created. Certain

strategies of IT adoption are then defi ned which can be used by fi rms with different requirements.

The third part (Chapter 4 and 5) contains an action plan for various stakeholders to increase

IT adoption in the auto component fi rms.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 18/54

As mentioned in the previous chapter, a primary research of 148 auto component fi rms indifferent parts of the country was undertaken to collect information on their business challenges

and IT adoption. Of these, 46 fi rms were small (with a turnover between Rs 20-99 crores),

86 were of medium size (turnover in the range of Rs 100-299 crores) and 16 large (with

turnover between Rs 300-500 crores). In 88 fi rms, business heads were interviewed while in

the remaining 60, information was collected from IT heads. The discussion, in this section is

primarily based on the analysis of this dataset.

1. Challenges faced by business heads

Any investment decision in a fi rm is infl uenced by the challenges that the management faces

and IT related investments are no exception. Apart from maintaining price competitiveness and

meeting customer demand for product quality, availability and volatility in costs of raw material

seem to be the major challenges that business heads in Indian auto component fi rms face

(Figure 1). The cost of raw materials must be strictly controlled as it has a direct impact on the

overall cost of production and therefore competitiveness. Similarly, the procurement and the

timely availability of raw material also pose a concern for the surveyed fi rms as it affects their

ability to meet their customer’s demands within due dates. In addition, fi rms face problems

while responding quickly to the customer demands of consistent product quality within the

agreed delivery time.

Another important business challenge faced by the business heads is quick access to

business information. Apparently, the auto component manufacturers are faced with disparate

systems including manual paper based processes that lead to disconnect amongst the value

chain partners. This disjoint makes it diffi cult to develop and quickly share accurate business

information such as projection of demand and tracking the production schedule and the costs

associated with it.

Interestingly, the availability and the implementation of IT is not seen by the BU heads as a

critical business challenge. Similarly, resistance to the use of these technologies amongst theemployees of the company is also not a critical challenge.

Overall, some of the key components of Supply Chain Management (SCM) have been ranked

as the most critical challenge by business unit (BU) heads. These include fl uctuations in raw

material costs, meeting customer demands for product quality & timelines and procurement

of raw materials, reiterating the importance of the supply chain.

A key question is whether these challenges differ with fi rm characteristics? Table 1 below

provides some interesting insights. A few of these may be noted:

Chapter 2: Business challenges and

current state of IT adoption

17

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 19/54

Figure 1: Challenges faced by Business Unit heads

18

Table 1: Average ranks of challenges faced by fi rms with different characteristics

Challenge Firm Size ForeignCollaboration Export

Small Medium Large Yes No Yes No

Meeting customer demand in product quality 6.44 7.03 6.33 6.14 6.89 6.25 7.92

Meeting customer demand in timeliness 6.20 7.53 4.00 6.32 6.86 6.06 8.50

Diffi culty in estimating demand 7.53 8.43 11.00 9.45 7.59 7.83 8.67

Quick/easy access to critical information 8.24 8.53 5.33 8.50 8.20 8.27 8.29

Maintaining price competitiveness 6.62 6.65 6.67 6.05 6.83 6.61 6.71

Fluctuations in raw material costs 5.27 6.18 7.67 5.68 5.79 6.03 5.04

Ease of procurement of raw material 8.71 8.80 9.00 8.95 8.70 8.86 8.50

Timely availability of raw material for production 8.22 8.73 7.33 7.95 8.58 8.63 7.88

Track/trace production timeliness across manufacturing cycle 7.91 8.75 6.67 8.23 8.26 8.05 8.79

Track/trace production costs across manufactur ing cycle 8.84 7.73 4.67 7.55 8.41 8.59 7.13

High attrition rates among employees 9.49 10.33 11.00 10.23 9.82 10.38 8.71

Training and development of employees 9.84 8.88 9.67 10.09 9.17 9.83 8.25

Availability of good IT technology for business 10.49 8.15 9.33 7.77 9.92 9.09 10.17

Implementing IT technology in business 10.62 9.80 12.67 10.23 10.35 10.13 10.83

Resistance to new IT technology among employees 11.00 9.93 10.00 10.95 10.32 10.45 10.54

Infrastructure bottlenecks 10.56 10.60 14.67 11.91 10.32 10.95 10.08

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 20/54

• The main challenges faced by small and medium sized fi rms are similar-fl uctuationsin raw material costs, delivery of quality products in time and price competitiveness.

For large fi rms, while timeliness of delivery is the most important challenge, other

challenges include tracking of manufacturing costs and easy access to critical information.

The large fi rms seem to have reached a stage of IT adoption where signifi cant decisions

are taken on the basis of available real-time data, making quick access to information

and tracking of costs critical. The other important feature refl ected in Table 1 is that there

is more heterogeneity of challenges among SMEs than among large fi rms; the average

ranks of the most important (top 5) challenges show a much higher consistency of

responses among large fi rms than among SMEs. On average, non-availability of good

IT technology for business is felt more by medium fi rms, followed by large ones and theleast by small ones.

• Auto component fi rms with or without foreign collaboration face similar major (top 4-5)

challenges. But there are other interesting differences. Availability of good IT solutions

for business is more of a challenge for fi rms with foreign collaboration than for the ones

without it. Presumably, the former are looking for such technologies more actively. In a

similar vein, tracking production costs is more of a concern for collaborating fi rms, while

estimation of demand is more challenging for fi rms without foreign collaboration.

• Dealing with fl uctuations in raw material costs is the most important challenge for both

exporting and non-exporting fi rms but it is somewhat more critical for the latter. Timeliness

of delivery and product quality on average are more critical for exporting fi rms while

tracking production costs is more of an issue for non-exporting fi rms.

Given these business challenges, what do BU heads expect from IT?

Figure 2: Expectations of Business Unit heads from IT

19

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 21/54

Figure 2 suggests that BU heads expect IT to play an important role in addressing most of their business challenges. The key expectations of the BU heads from IT are meeting customer

requirements for timely delivery and product quality, tracking production costs and quick

access to business information. Interestingly, several of these expectations are inter-linked.

For example, maintaining price competitiveness is an important expectation which can partly

be achieved by reducing production costs (or improving operational effi ciency), which in turn

requires tracking these costs and quick access to real-time business information.

2. Challenges faced by IT heads

The expectations of the BU heads in a fi rm will not be adequately met if the IT function of the

fi rm is not able to implement IT initiatives appropriately. But IT heads face their own challenges

in IT implementation. The survey responses (Figure 3) reveal that the most critical challenge

faced by the IT heads is the lack of alignment between business goals and IT initiatives.

At times, it also becomes diffi cult for the IT head to justify the current levels of investments

in any IT initiative, as the time for the complete deployment of the initiative is quite long

compared to many other business function initiatives. Besides, the impact of these IT initiatives

and their effectiveness is also felt after a period of time. Linked to this is the diffi culty faced

by the IT heads of proving the value of IT. While some IT spending lends itself to somewhat

Figure 3: Challenges faced by IT heads

20

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 22/54

straightforward cost-benefi t analysis, most IT investments do not. Typically, new IT investmentssuch as implementation of supply chain management applications are made in conjunction with

non-IT investments, such as new process design and training. The combined inputs of the

two create measurable value, but allocation of value created by the two types of investment is

virtually impossible. Studies have shown that in order to maximise the impact of IT investment,

it needs to be combined effectively with other elements of the business architecture including

organisational change, ability of managers to use the knowledge made available through IT

and the functional knowledge of business among IT related employees.

3. Factors infl uencing IT adoption

In a situation where the impact of IT investments cannot be easily seen, what factors infl uence

IT adoption by the auto component manufacturers and how is the effectiveness of such

investments measured? Evidently, the need of having better control over the inventory is the

most important reason to implement IT systems in a fi rm (Figure 4). This is followed by the

need to improve business process fl ows and increase operational effi ciency in the processes

because streamlined business process fl ows improve delivery time and reduce bottlenecks.

These processes may be internal (manufacturing or operational) or external (processes related

to suppliers and customers). This business process integration can be achieved by a variety

of technology solutions, some of which can be partial while others can be comprehensive and

integrated. The impact would actually depend on the nature of solutions used. This issue isdiscussed later in the report.

Figure 4: Factors infl uencing IT adoption

21

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 23/54

4. Measuring IT adoption effectiveness

The most common measure of IT effectiveness, amongst the auto component manufacturers

is increased productivity (Figures 5a and 5b). While the measure of increased productivity for

IT effectiveness is the most preferred choice for both BU heads as well as IT heads of fi rms

of all sizes, it is not entirely clear as to how it is measured. It may be recalled that one of the

key expectations of business heads from IT is to meet the customer requirements of product

quality and timelines. This results in increased customer satisfaction, which is also a key

measure for evaluating IT effectiveness by auto component manufacturers.

Interestingly, in many fi rms, none of the measures that were mentioned are actually used to

fi nd out the IT effectiveness. The primary reason probably is that there are many IT related

investments for which a cost-benefi t analysis is not possible. Similarly, calculating the

value of ongoing IT operations spending on hardware, system and software is even more

diffi cult, because the discrete investments made in IT become a part of the broader business

environment after a period of time.

Figure 5a: Measuring IT effectiveness by size of fi rm

22

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 24/54

5. Criticality of business processesAnother way to approach issues of IT adoption in a fi rm is to identify processes that are

critical to the fi rm and then ascertain how IT can enhance the effi ciency of these processes.

Figure 6 illustrates some of the most critical business processes identifi ed by the auto

component manufacturers. The top three critical processes are:

Order receipt and demand management

Production planning and scheduling

Order processing

The survey reveals some variance in the criticality of business processes by fi rm size. While

for medium and large fi rms, the three processes mentioned above remain the most critical,

for small fi rms, order processing is replaced by material handling (Figure 7). Interestingly, the

three least critical processes for small and medium fi rms are the same – invoice generation/

payment collection, traceability compliance requirements and bank reconciliation. For large

fi rms, however, bank reconciliation is the only process that is least critical alongwith customer

service management and HR & payroll systems. Most of these fi rms have already gone through

their IT implementation for these processes and hence don’t fi nd it very critical at this juncture.

The survey provides some interesting insights on how smoothly do these critical processes

work in the auto component fi rms.

1.

2.

3.

Figure 5b: Measuring IT effectiveness by BU and IT heads

23

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 25/54

Figure 6: Critical business processes across fi rms

Figure 7: Criticality of processes by size of fi rm

24

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 26/54

Table 2: Smoothness of critical business processes

ProcessPercentage of fi rms reporting level of smoothness

High Medium Average Low Poor

A. Order receipt and Demand management

Capturing orders in least time 26 53 14 5 2

Ensure and manage supply terms with customers 34 36 25 3 1

Analyse impact of demand variation and take

decision in the interest of supply chain 17 45 26 10 1

B. Order processing and production planning

Recording, sorting and prioritisation of orders 49 25 19 6 1

Processing orders with respect to checks and constraints 28 41 22 7 2

C. Material scheduling

Plan for material requirements at various levels effi ciently

fl oor using Kanban24 42 26 8 0

Material scheduling including WIP etc. in the shop 22 39 26 8 5

Vendor relationship and purchase terms 22 42 26 8 5

Manage sub-contracting 31 38 25 6 0

D. Accounting

Track profi t margins to take pre-emptive corrective action 22 38 17 16 7

Real-time visibility into actual vs. real budget to take

corrective action11 35 30 14 9

Annual 3-months rolling plan to manage

budgeting against actual13 45 25 11 5

Sample: Business Heads - 88

Order receipt and Demand management

This process combines receiving the orders, providing a timeline for the delivery of the fi nished

products and the projection of the demand, a majority of auto component manufacturers have

extremely smooth processes for receiving orders (Table 2). This is achieved without manual

intervention, by the use of IT as in most of the companies, this process is fully or partially IT

enabled (Table 3). The auto component manufacturers are also able to effectively manage the

supply terms with the customers as the system accepts orders through the extranet, reducing the

time taken to receive the orders considerably. However, the ability of the companies to project

and analyse the impact of demand variation and to manage the supply chain accordingly is not

smooth enough (Table 2). Similarly, the validation of orders in auto component manufacturers

is also not IT enabled in a signifi cant proportion of the fi rms.

25

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 27/54

Table 3: IT enablement of critical business processes

Process Percentage of Firms

FullyEnabled

PartiallyEnabled

Not ITEnabled

A. Order receipt and Demand management

System to accept orders from OEMs(without manual intervention) through extranet

20 69 11

Automatic validation of orders 29 43 29

B. Order processing

Ability to confi rm orders online 24 62 14

Seamless integration with production planning,scheduling and order receipt

28 55 17

Capability of information exchange withOEMs in case of order processing variation

17 69 14

C. Production planning and scheduling

Production plan visibility to self and OEM at various horizons 24 64 12

Day-wise, shop/job-wise scheduling for shorter horizons 27 61 12

Monitoring system for execution w.r.t. plan,manage changes and measure variances from plan

24 58 18

D. Material scheduling

Well defi ned error-free bill of material (BOM) structures 43 48 10

Vendor wise specifi c material requirements 33 57 10

Established electronic links with suppliers 29 43 29

Capability to share requirements with OEMsfor collective buying/electronic auctions

29 43 29

E. Accounting

Budgeting and variance monitoring system 29 67 4

Ability to carry out accounting based on theoperational system from other related systems

42 42 17

Ability to generate fi nancial systems online (B/S, P&L) 29 63 8

Sample: IT Heads – 60

26

Order processing

The auto component manufacturers prioritise orders and schedule production based upon the

fi rm’s shop fl oor capacity and customer delivery dates. A majority of auto component fi rms

have smooth processes related to order processing, wherein orders are effi ciently recorded,

sorted and prioritised (Table 2). These processes consume less time because of IT enablement

as the orders are received and confi rmed online in most organisations (Table 3). Once the

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 28/54

orders are received, they are checked against the constraints related to production, as theorder processing system is integrated with the production planning and scheduling facility

through IT in most fi rms (Table 3). The ability to evaluate and check the orders and to provide

a feedback to the OEMs, especially in case of any changes in the plan, is IT enabled (at least

partially) in a large majority of fi rms.

Production planning and scheduling

As indicated earlier, production planning is one of the most critical processes for the auto

component manufacturers. Earning and retaining the business of a larger number of customers

underscores the need for suppliers to effectively manage the production schedules to reduce

delays in delivery to the customers. Additionally, suppliers must be able to manage a regular

fl ow of changes to production schedules and quantities by having a robust production

planning system. Through IT adoption, a majority of auto component manufacturers make

the production plan visible at various horizons internally as well as to the customer. Similarly,

day-wise shop / job-wise scheduling for shorter horizons are also IT enabled by most of the

auto component manufacturers (Table 3).

Overall, while IT enablement of critical processes has resulted in smoothening of these

processes, the fact remains that a large proportion of fi rms have not yet achieved full

IT enablement. In fact, for several processes like automatic validation of orders, electroniclinkages with suppliers, etc. more than 25 per cent fi rms do not have any IT support. There is

tremendous scope, for the auto component manufacturing fi rms to increase IT adoption.

6. IT adoption – implemented applications/systems

Enterprise Resource Planning (ERP) is the most widely adopted IT application among auto

component fi rms. Some effort is also being undertaken to integrate the fi rm’s production

facilities with the other constituents of the supply chain, so that real-time accurate information

on the inventory, production schedule and materials is available as and when required. In order

to have better access to business information, many auto component fi rms have deployed

intranets which are made available to all the relevant in-house business functions and enable

effective planning and scheduling. A signifi cant proportion of fi rms that were surveyed have also

implemented wireless LANs to achieve this, whereas large organisations have also deployed

Virtual Private Networks (Figures 8-10). Broadly, large fi rms are ahead of small and medium

fi rms in the adoption of all application systems except Customer Relationship Management

(CRM) and Sales Force Automation (SFA) where adoption rates are similar. In the adoption

of networking and groupware systems also, large fi rms are generally ahead of the small and

medium fi rms.

27

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 29/54

Figure 8: Adoption of IT applications/systems

Figure 9: Adoption of IT applications/systems by fi rm size

28

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 30/54

One interesting insight that emerges from a more detailed analysis of the IT adoption data

is that very few fi rms adopt a clutch of applications to maximise the potential of effi ciency

gains. As shown in Table 4, only about 34 per cent fi rms having ERP also adopt SCM and the

proportion of ERP based fi rms adopting CRM is even lower (30 per cent). Similarly, Table 5

shows that only about 28 per cent ERP adopters integrate plants to the head offi ce. In fact,

only about 3 per cent fi rms combine CRM, SCM and IT enabled integration of plant systems

with ERP. This obviously has an adverse effect on the effi cacy of IT adoption. It also shows

that the surveyed sample comprises fi rms that are at very different levels of implementation

of IT and that the IT strategy of many fi rms is not based on a judicious process improvement

strategy. For instance, implementing a SCM module without integrating the manufacturing

facilities to the fi rm’s headquarter or with suppliers would not yield commensurate returns

on investment in an SCM application package, except in the exceptional situation of single

plant/supplier fi rms.

Figure 10: Adoption of IT infrastructure by size

29

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 31/54

Table 4: Percentage of fi rms adopting different applications and networking systems

ERP SCM CRM SFA EL IT BWIDTH LANS VPNS SAN/NAS

INTRANET GPWARE

ERP (47) 100.0 34.0 29.8 8.5 31.9 27.7 31.9 40.4 12.8 87.2 44.7 23.4

SCM (24) 66.7 100.0 41.7 25.0 29.2 29.2 45.8 45.8 16.7 75.0 41.7 29.2

CRM (19) 73.7 126.3 100.0 26.3 52.6 36.8 47.4 52.6 15.8 68.4 68.4 31.6

SFA (10) 40.0 60.0 50.0 100.0 40.0 30.0 40.0 50.0 10.0 70.0 70.0 20.0

EL (22) 68.2 31.8 45.5 18.2 100.0 45.5 50.0 54.6 13.6 81.8 59.1 36.4

IT (22) 59.1 31.8 31.8 13.6 45.5 100.0 40.9 40.9 18.2 81.8 40.9 22.7

BWIDTH (26) 57.7 42.3 34.6 15.4 42.3 34.6 100.0 46.2 15.4 73.1 53.9 34.6

LANS (30) 63.3 36.7 33.3 16.7 40.0 30.0 40.0 100.0 16.7 83.3 60.0 36.7

VPNS (8) 75.0 50.0 37.5 12.5 37.5 50.0 50.0 62.5 100.0 50.0 62.5 50.0

SAN/NAS (76) 53.9 23.7 17.1 9.2 23.7 23.7 25.00 32.9 5.3 100.0 31.6 14.5

INTRANET (55) 38.2 18.2 23.6 12.7 23.6 16.4 25.5 32.7 9.1 43.6 100.0 21.8

GPWARE (15) 73.3 46.7 40.0 13.3 53.3 33.3 60.0 73.3 26.7 73.3 80.0 100.0

ERP – Enterprise Resource Planning; SCM – Supply Chain Management; CRM – Customer Relationship Management;SFA – Sales Force Automation; EL – Electronic Linkages with customers & suppliers; IT – Integrating plants/factoriesIT systems to the corporate office IT systems on the internet; BWIDTH – Bandwidth up-gradation for data networking;LANS – Implementing wireless LANs; VPN – Deploying Virtual Private Networks; SAN/NAS – Enhancing/adding network storagecapabilities; INTRANET – Intranet deployment and expansion; GPWARE – Deploying and expanding groupware/workfl ow applications(lotus notes, project management)

30

Table 5: Combinations of selected applications adopted by sample fi rms – mutually exclusive cases

Combinations of select applications adopted Frequency %

ERP, SCM, CRM and IT (Integration of plants to HO) 3 3.4

ERP, SCM, CRM but not IT (Integration of plants to HO) 5 5.7

ERP, SCM and IT but no CRM 1 1.1

ERP, CRM and IT but no SCM 1 1.1

SCM, CRM and IT but no ERP 1 1.1

ERP and SCM but not CRM and IT 7 8.0

ERP and IT but not SCM and CRM 8 9.1

CRM and IT but not ERP and SCM 2 2.3

ERP and CRM but not SCM and IT 5 5.7SCM and IT but not ERP and CRM 2 2.3

SCM and CRM but not ERP and IT 1 1.1

Only ERP 17 19.3

Only SCM 4 4.5

Only CRM 1 1.1

Only IT 4 4.5

None of ERP, SCM, CRM, and IT 26 29.5

Total 88 100.0

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 32/54

Figure 11: Future investment plans for enterprise application systems

Will the future IT adoption plans help auto component fi rms reap synergies across variousIT applications? Including the investment plans of the next one to two years, a large majority

of fi rms would like to implement ERP and SCM packages and would like to integrate plants

with the head offi ce through IT enabled systems (Figure 11). Evidently, adoption of these three

applications is a priority for the companies which have not yet implemented them. CRM and

SCM implementation may only pick up in the next fi ve years. This is particularly true for CRM.

Figure 12 summarises the main highlights of IT related investment plans for both applications

and networking systems for fi rms of different sizes. Upgrading groupware, CRM and upgrading

bandwidth are on top of the priority list. These investments may eventually result in some

synergies being reaped.

31

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 33/54

Figure 12: A perspective for future plans by size of company for IT adoption

32

7. IT budgets

During the year 2005-06, a majority of auto component manufacturers that were surveyed had

their annual IT budgets to the tune of Rs 20 lakhs. Hardware maintenance forms the major

proportion of the current IT investments for the auto component manufacturers (Figure 13). This

component includes the expansion of intranet to integrate the various in-house functions for

increasing effi ciency, as well as the upgradation of bandwidth for data networking to increase

the sharing of real-time business information between the auto component manufacturers, their

suppliers as well as customers. Signifi cant investments were made by the auto component

manufacturers, related to the purchase of new hardware.

The investments made by the auto component manufacturers in terms of software include

purchase of new software/applications as well as the software maintenance cost. As noted

earlier, software application packages such as ERP and SCM have been implemented by

a signifi cant proportion of auto component manufacturers (perhaps the larger ones in the

surveyed sample). The solution cost for these software packages includes the license cost,

maintenance and up gradation cost as well as the cost of training and consulting.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 34/54

Figure 13: Annual IT budget

33

The annual IT budget is expected to increase for a majority (90 per cent) of auto component

manufacturers in the coming year. The signifi cant contributors to this increase are expected

to be:

Branded hardware

Vertical specifi c applications

Upgradation of the networking facilities such as wireless LANs, bandwidth for data

networking as well as implementation of Virtual Private Networks (VPN)

Implementation and upgradation of enterprise application software packages such

as SCM and CRM

8. IT workforce and outsourcing

In a majority of auto component manufacturing companies that participated in the survey, less

than 10 full time employees take care of the IT service and support function, across all locations.

(In Figure 14, the numbers indicate total number of full time employees across all locations).

The distribution of fi rms by number of servers, workstation and nodes is provided in Figure 15.

Most fi rms on average have 1-5 servers, 50-199 workstations and 10-99 network nodes.

1.

2.

3.

4.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 35/54

34

Figure 14: Full-time employees across locations handling IT service and support

Figure 15: IT infrastructure in auto component fi rms

Outsourcing offers a wide range of potential advantages. Many auto component fi rms have

implemented or are considering outsourcing various functions within IT. Outsourcing can provide

companies cost savings for transactional work, particularly if sourced to lower-cost vendors.

It can improve effectiveness as outsourcing companies have talent, methods and content that

can be leveraged. As illustrated by Figure 16, hardware maintenance appears to be the most

outsourced IT service by the auto component fi rms.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 36/54

35

Figure 16: Outsourcing of IT services by auto component fi rms

The outsourced activities related to hardware maintenance include management and functioning

of offi ce hardware such as PCs, laptops, etc. Another important IT service outsourced by the

auto component manufacturers is software maintenance. This includes the implementation and

up gradation costs of the software packages such as the enterprise application systems like

ERP, SCM and CRM. These services are being outsourced to external vendors, who study the

internal processes, implement software modules as per the requirement, train the employees

and also upgrade the software whenever needed.

9. Key features of IT adoption in auto component fi rms

Raw material price fl uctuations and maintaining price competitiveness fi gure as major

challenges for BU heads in auto component fi rms. IT heads do not seem to perceive their

function as an integral part of organisation goals and fi nd it diffi cult to prove the value of IT

in their companies. Despite this perception, BU heads do expect IT to be a strong enabler

to meet changing customer requirements, track production costs and gain access to critical

business information for better decision making.

While the larger companies are more positively disposed towards IT solutions (constant

upgradation, branded IT solutions, etc), the small ones are trying to get their basic

IT infrastructure in place.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 37/54

36

The responses of the survey suggest that key driver to increase IT adoption is streamlining of processes. The top fi ve key business processes are as follows:

Order receipt and demand management

Production planning

Order processing

Material scheduling

Accounting

While the basic procedures with respect to order receipts and processing seem to be running

smoothly, a need is felt by the BU heads for real-time visibility of certain key information. ERP

systems have either been implemented or are on the short-term IT investment horizon of mostfi rms. The need for real-time data capture, applications that cater to shop fl oor operations and

those having a greater focus the key business processes defi ned above have driven the advent

of PLCs, shop fl oor automation applications and Manufacturing Execution Systems (MES).

As fi rms expand their IT application portfolio and move to an automated real-time information

system, these are likely to gain in popularity.

Most fi rms seem to have planned their IT deployment only in the short run. There are very

few companies with a concrete long-term plan for IT deployment. Outsourcing is a familiar

option as a majority of auto component manufacturers have outsourced IT functions such as

hardware maintenance and software maintenance.

The fi ndings of this survey reveal that different fi rms appear to be devising differing strategies

for IT adoption and size of the fi rm seems to be defi ning the trajectory that a fi rm will adopt

for IT adoption. The next section of the report characterises these different types of fi rms in

the auto component manufacturing sector and maps the supply chain decisions (including the

manufacturing and distribution processes) they seem to be facing. Once the fi rms understand

these key manufacturing processes, they could design their strategy appropriately to add value

through IT investments.

1.

2.

3.

4.

5.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry

http://slidepdf.com/reader/full/nasscom-report-on-it-adoption-in-the-auto-component-industry 38/54

37

Chapter 3: Mapping supply chain strategies

for auto component fi rms

The auto component manufacturers in India come in a variety of sizes – mostly micro, small andmid-size and a few large ones. While the micro and small fi rms may be struggling to get their

products in the replacement markets, the large fi rms are looking towards developing products

for the automobile OEMs. Therefore their capabilities and complexities vary considerably.

This section describes the linkage between various capability stages at which these differently

sized fi rms are and the nature of managerial practices they require to succeed. The next section

of the report outlines the IT strategy required to support implementation of these manufacturing

practices in the different types of auto component fi rms.

1. Linking capability levels to manufacturing practices

Firms in the Auto Component Industry, globally, grow by producing more complex products

that have higher value add. The situation in India is no different, especially with the changes in

the product technology. However, the auto component supply chain comprises tiny and small

producers that supply both to the suppliers of OEMs as well as in the replacement market.

As a result, there is enormous diversity in the intent and strategies of the fi rms in the auto

component sector. While operational excellence is acknowledged as the key requirement

for winning orders, the state of fi rms on this dimension varies tremendously. Often, bigger

fi rms compete on their supplier ’s ability to generate low-cost operation through low wages to

low skilled operators, less robust equipment, evasion of cost of utilities, etc. and not through

effective manufacturing. This, however, turns out to be a temporal advantage that takes the

focus away from operations to clever accounting practices.

What fi rms require is a good understanding of how they can compete by building distinct

competitive capabilities. There is no one answer to building their capabilities through adoption

of world-class practices and IT. However there is a trajectory through which fi rms in this sector

could look to building capabilities and develop distinct competitive stances. This trajectory

can be defi ned in terms of various stages or Levels with each Level being defi ned by certain

operational characteristics. The competitiveness of a fi rm, at an operational Level, is a function

of the following:

Operational characteristics of the Level to which the fi rms belong

Nature of managerial practices that the fi rms have implemented

Extent of adoption of IT to support the improvements in decision making

Table 6 describes how fi rms at different Levels of the supply chain can build up their

manufacturing effectiveness.

1.

2.

3.

8/7/2019 NASSCOM Report on IT Adoption in the Auto Component Industry