national agricultural policy report israel –...

TRANSCRIPT

NATIONAL AGRICULTURAL POLICY REPORT ISRAEL – FINAL

Market and Trade Policies for Mediterranean Agriculture (MEDFROL): The case of fruit/vegetable and olive oil - SIXTH FRAMEWORK PROGRAMME PRIORITY 8.1 Policy-oriented research Integrating and Strengthening the European Research Area Call identifier: FP6-2002-SSP-1

Source: WorldAtlas .com

Research conducted under the European sixth framework program (Priority 8.1) “Integrating and Strengthening the European Research Area”. Views expressed in this paper are those of the authors and do not necessarily reflect those of the institutions of affiliation, the MEDFROL project or the EU. Any errors in the present report are the responsibility of the authors.

AGRICULTURAL RESEARCH INSTITUTE

Nicosia – CYPRUS OCTOBER 2005

Dr. Marinos Markou

Mr. George Stavri

CONTENTS

Page

LIST OF TABLES AND FIGURES 3 LIST OF ACRONYMS 4 1. GENERAL SETTING 5

1.1 – Macroeconomy 5 1.2 – Place of Agriculture in the National Economy 6 1.3 – National Economy and the World Economy 7

2. AGRICULTURAL AND FOOD POLICIES 9

2.1 – General Setting 9 2.2 – Price and Income Support 12 2.3 – Agricultural Trade Policy Measures 14 2.4 – Measures Affecting Input Use 19 2.5 – Infrastructure Policies 20 2.6 – Rural Development Policies 24 2.7 – Agro-Environmental Measures 25 2.8 – Measures Affecting Consumers 27 2.9 – Social Measures 28 2.10 – Budgetary Outlays Associated to Agricultural and Food Policies 30

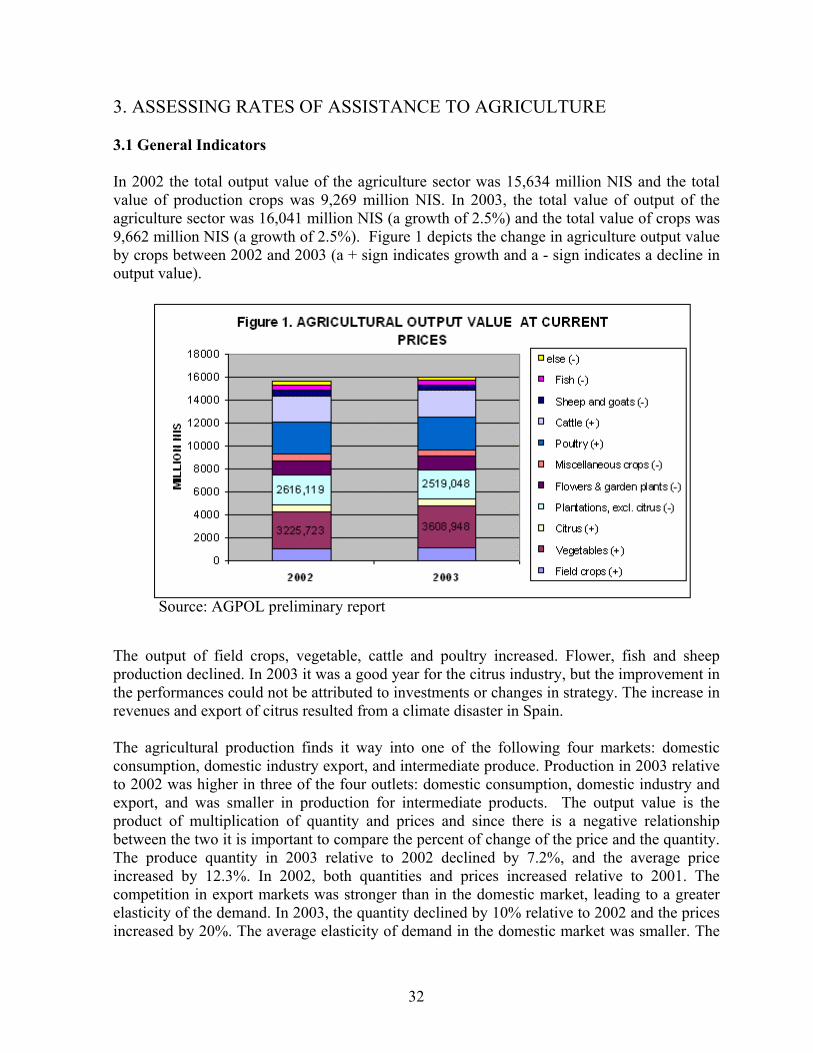

3. ASSESSING RATES OF ASSISTANCE TO AGRICULTURE 32

3.1 – General Indicators 32 3.2 – Rate of Assistance to Agricultural Products 33 3.3 – Rate of Assistance for Fruits & Vegetables 34

4. CONCLUDING REMARKS 36 5. POLICY OUTLOOK 38 REFERENCES 40

APPENDIX 41

2

LIST OF TABLES AND FIGURES Page Table 1. Israel’s Aggregate Indicators 6 Table 2. The Israeli Export of Agricultural Inputs 10 Table 3. Import Dependency Ratios (IDR) 15 Table 4. Foreign Trade Balance of Agriculture 16 Table 5. Foreign Trade 16 Table 6. Israeli Export of Agricultural Inputs 18 Table 7. Several indexes of Israel 29 Table 8. Compensation and other receipts 35 Figure 1. Agricultural output value 32 Appendix Table 1. General Indicators 42 Appendix Table 2. Output, input and domestic product in agriculture 43 Appendix Table 3. Price index of agricultural output 44 Appendix Table 4. Agricultural trade of Israel 45 Appendix Table 5. Imports of selected fresh agricultural products 46 Appendix Table 6. Agricultural account 47 Appendix Table 7. Export of selected products 48 Appendix Table 8. Production 49 Appendix Table 9. Yields of main products 50 Appendix Table 10. Water for agriculture 51 Appendix Table 11. Water production and consumption 52 Appendix Table 12. Input in Agriculture 53 Appendix Table 13. Agricultural output value, by purpose 54 Appendix Table 14. Estimated water usage for agriculture 55

3

LIST OF ACRONYMS AMS = Aggregate Measure of Support ARO = Agricultural Research Organization ATAP = Agreement on Trade in Agricultural Products CPI = Consumer Price Index EU = European Union FAO = Food and Agriculture Organization GDP = Gross Domestic Product HDI = Human Development Index IDR = Import Dependency Ration ILA = Israel Land Administration IT = Information Technology NIS = New Israeli Shekel (1 NIS = 0.22 US$ = 0.18 Euro) UN = United Nations UNDP = United Nations Development Program VAT = Value Added Tax WTO = World Trade Organization

4

1. GENERAL SETTING

1.1 Macroeconomy Economic recovery in Israel is currently under way after a prolonged recession. Growth is supported by more favorable global economic conditions, an improvement in the security situation and appropriate policies that have involved tightening the fiscal stance and easing monetary policy. The Gross Domestic Product (GDP) grew by 1.3% in the first three quarters of 2003, while the business product grew by 1.6%. Although this is definitely an improvement as compared with the negative growth recorded in 2001 and 2002, the composition of growth is not satisfactory. A considerable part of the growth originates from a sharp 3.9% decrease in imports, a development that derives from a relatively moderate increase in private consumption and a continued decrease in investments. Exports (excluding diamond exports and start-up companies) grew by a moderate 2.9%. Public consumption grew by only 0.2%. An analysis of the composition of public spending however indicates that a relatively large 1.2% increase was recorded in civilian consumption, coupled with a 0.8% rise in domestic defense consumption. These figures were offset by a 2.0% decrease in defense imports. Following the Israel Economic Recovery Plan that became effective July 2003, the Government’s civilian and defense spending is expected to decrease until the end of the year. Private consumption increased 0.8%. Although this increase is higher than the previous forecast for the period, it is nevertheless lower than the growth in GDP over the same period, indicating a decrease in private consumption per capita as well. In parallel, gross domestic investments also continued to fall. This decrease consists of 3% decrease in investments in fixed assets, along with a sharp drop in inventories. Inflation during this period was low, as the Consumer Price Index (CPI) rose by 1.6%, while product prices were up 1.2% for the first three quarters of 2003, as compared with the corresponding period last year. Prices nevertheless fell in 2003, as the CPI level in September was 1.5% lower than its level in December 2002. The process of lowering the nominal interest rate by the Bank of Israel started with a considerable delay after the lowering of inflationary expectations and the actual inflation. The short-term real interest rate therefore reached new records (approximately 7% during May-June 2003). This interest rate is not compatible with the recession in demand, the ongoing decline in wages, the lower investments and the decreasing long-term interest rates in the economy. It is expected to result in the inflation target being missed for the fifth consecutive time. In the labor market, the unemployment rate continued to rise, climbing from 10.3% of the civilian labor force in 2002, to 10.6% in the second quarter of 2003. In terms of the composition of employees, the number of foreign laborers continued to fall in 2003, along with a parallel rise in the number of employed Israelis. The number of foreign laborers in the second quarter of 2003 was lower by 54,000 in relation to their number in the fourth quarter of 2002. This represents an aggregate decrease of 77,000 (approximately 30%) from the record high in the fourth quarter of 2001. This decrease reflects the successful government policy of lowering the number of foreign laborers. There is no doubt that this success is one of the factors responsible for the increase in the number of jobs held by Israelis, despite the economic recession. The real wages per salaried employee continued to fall in 2003. The average such wages between January-July 2003 was 3% lower in the business sector and 5% lower in public services, than they were in 2002. The considerable decrease in real wages also reflects a decrease in nominal terms in both sectors. The exchange rate of the NIS (New Israeli

5

Shekel) is stable against the major currencies (i.e. US$ and the Euro) but the authorities in Israel face the difficult task of adhering to the strategy of reducing the government size and public debt. Over the medium term the authorities need to strictly observe the deficit target of 3% of GDP and limit expenditure growth in real terms to no more than 1% per year (Table 1 and Appendix Table 1).

Table 1. Israel’s Aggregate Indicators Population (million) 2003 6.7 Population Growth (%) 2003 1.8 Literacy Rate (%) 2002 96.3 GNI Per Capita (Atlas Method, US$) 2003 16,240.0 GDP (billion US$) 2003 110.2 GDP Growth Rate (annual, %) 2003 1.3 Source: World Bank

1.2 Place of Agriculture in the National Economy Israel’s agriculture continues to thrive and supplies most of the country’s food needs, though profitability in export sectors has declined sharply in recent years. Among the numerous problems the crop-growing sectors have contended with since the State was founded, water remains the principal and growing threat. Nevertheless, the ongoing introduction of new and recycled water sources, coupled with altered irrigation methods and more water-efficient crops, promises long-term security (Appendix Table 2 and 3). By the year 2020 Israel’s population is expected to grow by about a third to 8.5 million. This will result in huge increases in demand for agricultural products; but urban use of land and water will also increase enormously. Thus, the pressure on resources will be considerable. To leave all the increased demand for food supplies to be satisfied by imports would be an unnecessary burden to national security and finances, which are already precarious (Appendix Table 4 and 5). Today, agriculture in Israel contributes a mere 2.4% of the GDP and 4% of exports, compared to 30.3% of exports during the 1960s. In absolute terms though, agriculture has grown and has played an important part in Israeli economy for the last fifty years. Agriculture’s output in 2000 was at US$ 3.3 billion, of which 20% was exported (Appendix Table 6). Export revenues were volatile mostly due to exchange rate fluctuations rather than in absolute exports. Indicative of the net proceeds in foreign exchange to the country, inputs for the above exports were at US$ 2.2 billion. Another factor important in Israel’s agricultural development has been the sector’s performance in foreign trade. The rapid growth of agricultural exports was accompanied by a general increase in total exports. Between 1950 and 2003, a prominent development was the decline by 65% in citrus fruits exports in relation to total raw agricultural exports (Appendix Table 7). This decrease was more than balanced by the increase in processed agricultural products, whose exports increased by 4,000% in the same period (Federal Research Division, Country Studies, Israel).

6

Since independence in 1948, the total area under cultivation has increased from 165,000 ha to some 420,000 ha and the number of agricultural communities has grown from 400 to 900 (including 136 Arab villages). During the same period, agricultural production has grown sevenfold thus proving its advances in productivity as population in the country increased six fold (Appendix Table 8 and 9). In 2000, about 70,000 people had an agricultural full time job. Israel produces almost 70% of its food requirements. It imports sugar, coffee, cocoa and much of its grains, oilseeds, meat and fish. However, these imports are partially offset by exports of fresh agricultural produce and processed foods. About a fifth of the total income of Israeli farmers derives from the export of fresh produce, including such products as flowers, avocados, vegetables that are out of season elsewhere and certain exotic fruits grown specifically for exports. Furthermore, some 442,000 tons of fruit and vegetables (16% of the entire crop) were sold to factories for processing and export in 2000 (Fedler, 2002). 1.3 National Economy and the World Economy The Israeli economy has always been characterized by dynamism, versatility in facing threats from foreign competitors but in also dealing with its own inherent structural problems. Lack of natural resources (i.e. water, fertile land etc) as well as several security problems has forced the government to divert on a regular basis crucial resources to defense. By the latest count, Israel devotes close to an astounding 10 % of its GDP to its defense and military needs on an annual basis, in comparison to the US that spends 3.8% and India 2.5%. Admittedly some of it is covered by foreign grants but it would be important to note that each decrease of one percentage point in defense spending as a share of GDP frees more than 4 Billion NIS for other uses according to Israeli Ministry of Finance estimates. The local use of resources for the military has prevented the shift from outright purchases from overseas manufacturers and has helped Israel keep valuable foreign exchange within the country, employed tens of thousands in the industry, avoided the political risk of embargoes as well as secured military research that spills over to many civilian applications. In the communication field, advances in encoding allowed Israeli civilian manufacturers to produce advanced cellular phones and networks for export. In the agricultural engineering field progress in rapid entrenchment contributed to the creation of an advanced version of mechanized diggers (MERIA, 2001). Israel’s first Foreign Trade Agreement (FTA) was with the European Community in 1975 followed by the US in 1985. Since then it has signed agreements with several countries mainly in Eastern Europe, Turkey, Canada and Mexico. In 1996, Israel and the US signed a five-year Agreement on Trade in Agricultural Products (ATAP), which expired in 2001. The parties have recently accomplished a new agreement, which is supposed to be valid until 2008. Undoubtedly though the greatest impact on the import side of foreign trade for Israel in agriculture have been two seminal events: Israel’s accession to the WTO on April 21st, 1995 and Israel’s Association Agreement with the EU in July 2003. The latter had a large impact on a few select imported items like sugar and cheeses whose consumption takes place in large quantities to the direct detriment of local producers. Τhe main advantages of the agreement were the granting of export quotas for products in which no customs-exempt exports had been allowed and the creation of a mechanism for gradually increasing Israeli exports in products with quantitative quotas. These quotas can be increased by 3% per year, beyond current levels.

7

The combined thrust of accession to the WTO as well as the Association Agreement with the EU have had a major impact on the import of agricultural products into Israel as they both forced it to open summarily most markets and products to foreign imports. Israel, a traditionally and instinctively export-oriented producer has benefited by translating readily losses on the import front to major and sustainable gains in exports.

8

2. AGRICULTURAL AND FOOD POLICIES 2.1 General Setting Despite the fact that Israel is in reality a market economy, it is also one that the Government tries to assist and support. Its various Ministries have always an input in activities crucial to the country’s interest. Agriculture and food policies are indeed one such sector. The Ministry of Agriculture supports and supervises the activities of the country’s agricultural sector, including research and development, maintenance of high standards for plant and animal health, agricultural planning, extension research and marketing. For many years, agriculture was tightly controlled, with allocations of production and water quotas for each crop. At present, only quotas for milk and selected milk products and some control of eggs, broilers and potatoes are in effect. Ongoing government programs to increase the country’s water potential involve rainfall enhancement through cloud seeding, desalination of brackish water and sewage recycling. In 2001, preparations began on a series of tenders for major seawater desalination plants, slated to have become operative by the end of 2004 onward. Supervision of the country’s water supply includes determining water quotas by the relevant Government authority, progressive pricing to penalize waste, fully controlling groundwater pumping, initiating conservation and supply enhancing projects. A ten year program, which is underway since the late 1990s, foresees, in addition to water rationing and desalination, the treatment and re-use of all urban wastewater (Appendix Table 10 and 11). Evidently, Israel has its own peculiarities due to its very nature, and therefore, agricultural and food policies are a blueprint of that. Most of the country’s agriculture is organized on cooperative principles, which evolved in the country during the first decades of the 20th century. Motivated by both ideology and circumstances, the early pioneers set up two unique forms of agricultural settlements: the kibbutz, a collective community in which the means of production are communally owned and income is equally distributed; and the moshav, a co-operative village where each family maintains its own household and works its own land, while purchasing and marketing are conducted cooperatively. In recent years both systems have undergone vast ideological and structural changes though they still account for the lion’s share of productive crop growing area. For example, in 1999 they accounted for three quarters of the total area producing crops. The Government specifically assists the creation and operation of such agricultural settlements with outright grants, concession of land and water resources, favorable tax treatment of the trading entities, as well as priority to various government programs in their field over others, i.e. city dwellers etc. Most of the above settlements are found in open desert areas where one would think establishing agricultural practices would be impossible. The desert area between Be’er Sheva and Eilat (the Arava & and the Negev) has played an important role in agricultural production. More than 40% of the country’s vegetables and filed crops are grown there, and 90% of the melons exported come from the Arava. Common advantages of the desert areas above are their long hours of sunshine and relatively high temperatures, the fact that land is relatively cheap and adequate water (saline or recycled effluent) is available. Even though the emphasis with crops in the desert Government-supported kibbutz and moshav agricultural farms was on field crops,

9

vegetables, fruit and dates until the early 1990s, new products are being tested like giant citrus groves, in an area covering 11,000 hectares. Furthermore, there are plans to expand into different goods and directions are government-orchestrated though the provision of incentives in the form of grants and subsidized inputs. These include flowers, grapes for wine, olives for oil, cattle for meat, ostriches and aquaculture projects. The government actively encourages close collaboration in between researchers, extension agents, farmers and agriculture-related industries. These develop and apply new methods in all agricultural branches. This is conducive to constant growth in agricultural production and results in what is currently known as high tech agriculture. This close cooperation between the research and development institutions prompted by favorable government policies, led to the development of a market-oriented agri-business that exports agricultural technology solutions worldwide. The following table encapsulates the results of such government policies in an impressive way on the financial benefits to the whole economy (Table 2 and Appendix Table 12).

Table 2. The Israeli Export of Agricultural Inputs in 2004 (000s US$) Water and Irrigation 89,364Plasticulture 37,693Veterinary Products & Feed Additives 42,923Livestock and poultry 12,814Consultancy and know-how 12,311Mechanization 56,029Seeds 61,270Fertilizers 648,714Chemicals 352,648Source: Ministry of Agriculture and Rural Development, Israel

Beyond the obvious indirect benefits, the Government in Israel provides generous financial assistance either through grants, subsidized loans or a combination of both. Through the rapid development of the agricultural sector, as a sector generating solutions to agribusiness, Israeli agro technology has received a boost and became an industry by itself exporting worldwide the fruits of this government support. Some of the results of this support are provided below. Greenhouse: The need to overcome natural restrictions of soil, water and climate has led Israel to develop greenhouse technologies that are particularly useful for high added value crops. Greenhouse systems, including specialized plastic films as well as heating, ventilation and structure systems, enable Israeli farmers to grow more than three million rose per hectare per season and in the fresh produce an average of 300 tons of tomatoes per hectare per season, four times the yields of open fields. Mechanization: Israel manufactures and exports a variety of specialized agricultural equipment including: a mobile celery packing house, machinery for digging silage and mixing the feed uniformly, poultry equipment like drinkers, automatic egg collectors, climate control systems and scales for weighing, an air-blast sprayer for use in citrus growing and vineyards

10

which provides an efficient cover of the tree, flower bulb transplanters, and machinery for packing houses. Fertilizers: Israel’s southern region and in particular the Dead Sea area, is rich in mines that provide potassium, phosphorus, and magnesium for the agricultural sector. Some of these resources are exported directly as raw materials while others undergo local processing and compounding to enhance their utility, effectiveness and their environmental safety. One of the remarkable developments is the application of fertilizers through drip irrigation buried in the ground in order to ensure that less mobile components, such as phosphorus, will reach the roots directly. Another innovation is the controlled release fertilizers. These are coated ion polymers to ensure slow, prolonged release and delivery via diffusion. Slow release fertilizers allow better exploitation of the fertilizer and less ground water pollution. Plant protection: Israeli companies manufacture and export pesticides and herbicides for the control of insects, fungi and weeds. As part of the growing awareness regarding environmental protection, biological materials that are non-pathogenic to both plants and humans have been developed for treating diseases in plants. These biological materials are effective in treating diseases caused by pests, fungus and viruses in a wide range of crops. In addition, a defoliant for cotton and herbicides for early and specific treatment of weeds have been developed. Environmental concerns have also stimulated the development of methods to disinfect the soil, using formalin as a substitute for methyl bromide, which use has been recently prohibited in the EU. Turnkey projects, consultancy and know how: Increasingly, Israeli agro technology companies join forces and supply turnkey projects for both crop and livestock development programs. Multiple skills, talents and experiences are enlisted to provide integrated solutions that embrace soil, water, additives, plant and livestock varieties, equipment and structures. The results are measured in improved yields produced at lower costs, a win-win situation in resource-stressed world. Poultry farming: Israel has developed innovations that are contributing to improved production and making the work of poultry farmers more efficient. A recent innovation in this field is the creation of a race of featherless broilers. Breeding: The breeds that are developed in Israel are highly disease-resistant, adaptable to extremes of climate and heat, characterized by a rapid growth rate, high egg production and low-fat meat. Control Systems: In order to maintain optimal condition in the henhouse in all climatic conditions, sophisticated control systems have been developed. These systems maintain desired levels of humidity, heat, lighting, feed, ventilation and cooling 24 hours a day. Aquaculture: The country’s semi-arid climate, characterized by a scarcity of water, required the development of an intensive form of aquaculture. Fish farming is carried out in the open sea in floating cages and in man-made reservoirs and ponds. Due to the lack of fresh water, fish farmers are using closed water systems for intensive farming. In some projects, water

11

from the reservoirs is used for irrigation. A wide range of ornamental fish and marine plants are bred, including coldwater fish, tropical fish and water lilies. The products are exported overseas especially to Europe.

2.2 Price and Income Support Israel maintains a relatively large array of trade and trade-related measures intended to support the domestic agricultural sector. The sector has traditionally been regarded in Israel as mainly fulfilling an important national role, though the past focus on attaining self-sufficiency in all products and the promotion of exports is no longer as pronounced. Domestic support to agriculture, as measured by the current total Aggregate Measure of Support (AMS) reached US$ 424 million in 1997 (approximately one fifth of the value of agricultural output. Provisional data for 1998 suggests an AMS of US$ 422 million, about one fifth of agricultural output. The support increased between 1995 and 1997, but declined in 1998, and it has remained below the ceiling set by Israel’s total AMS commitments. Under these commitments, domestic support for the agricultural sector was to be reduced over a ten-year period beginning in 1995 by around 12 % from US$ 646 Million in 1995 to about US$ 569 Million in 2004. For 1997, almost one half of product-specific AMS (plus support ‘de minimis’ levels) was for milk production, followed by poultry meat (28.3% of the total) and eggs (17.1%). Support reached around two thirds of output value for milk and eggs and 53% for poultry meat. Support to all other products such as vegetables, citrus, fruit, flowers and meat of bovine animals was reported as ‘de minimis’. These supports are subject to limits: ‘de minimis’, minimal supports that is allowed 5% of agricultural production for developed countries and 10% for developing countries. The 30 WTO members that had larger subsidies than the ‘de minimis’ levels at the beginning of the post-Uruguay Round reform period are committed to reduce these subsidies. In WTO terminology, subsidies in general are identified by ‘boxes’, which are given the colors of traffic lights: green (permitted), amber (slow down/reduced), and red (forbidden) (WTO). Market price support constitutes the main instrument of income support, accounting for 90% of total product-specific AMS in 1997. In particular, support to milk, egg and poultry meat production involves production quotas and target prices. In addition to price support, the Ministry of Agriculture operates deficiency payments and investment programs for horticulture, egg, poultry and bovine meat production. The total direct payments under this item amounted to US$ 51 million in 1997, down from US$ 63 million in 1996 and US$ 97 million in 1995. ‘Green Box’ expenditures, consisting of measures exempt from the reduction commitment, amounted to US$ 338 million in 1997 compared with US$ 414 million in 1996 and US$ 292 in 1995. The largest expenditure consists of specific assistance programs for the Kibbutzim and Moshavim under the Rural Development Agreement, expenses of the Agriculture

12

Research Center, new settlement infrastructure, and general sanitary and phytosanitary and other services provided to farmers. In 1994, other domestic support measures included support price schemes for non-irrigated crops such as wheat and sunflowers and for which prices were fixed according to different regions and an insurance fund for national disasters. As in 1994, fresh fruit and vegetables are exempt from value-added tax. Production and marketing boards still operate in certain agricultural sectors. There are six statutory boards covering citrus fruit, flowers, vegetables, groundnuts, poultry and other fresh fruit. Their objectives are to finance marketing, research and development programs and provide insurance in case of natural disasters. The fruit and vegetable boards also deal with exports (WTO). Grains: In a world where no more than six countries grow approximately 90% of the world’s grains and forty countries import more than 90% of the world’s traded grains, Israel is stuck in its own reality of importing more than 90% of its grains. Domestic support for grains in Israel never really happened due to the small scale of the activity, and the government devoted its efforts in stockpiling by providing financial incentives to the growers.

Beef: In 2000, Israel’s consumption of beef was 106,000 tons of which 62% were imported. In terms of volume, beef consumption was 29% to the volume of poultry products consumption. This pattern is partly habit and partly price-dictated. Pasture is a limiting factor in production, though efforts have been made to expand grazing areas by improving existing pastures and introducing different grasses and new grazing techniques. Between 1990 and 2000, the herd increase was 21% while output increased from 50,000 tons to 80,000 tons. Most of this was a result of the lifting of government barriers on the import of live calves; about 80,000 were imported in 2000 compared with 26,000 in 1998.

Dairy farming and products: Dairy and beef herd account for 17% of the country’s total agricultural production. Israel has for several years held the world record for milk production (10,200 kg with 3.3% butterfat milk per cow). This reflects a number of complementary steps, each aimed at achieving maximum efficiency. The sector supplies all of the country’s dairy requirements. A surplus of butterfat is used to produce a wide variety of dairy products. Until the late 1990s production was regulated by a strict policy of planning and quotas imposed by the Government as a measure of support to the sector. Currently, the government has been reducing the (regulated) prices on an annual basis, while encouraging small dairies to merge in order to cut production costs and make the revamped sector more competitive. The downside of these measures of course has been the drastic reduction of profitability and the eventual closure or merging of some 300 small dairies. The results of advancements in the sector have all been promoted by the government through an elaborate scheme of incentives. A major side benefit of this government support is the growth of exports in livestock and related products. Exports include heifers, computerized milking and feeding systems, cooling systems to recycle organic waste into cattle feed and recycling systems for cattle manure. Fruits: The country’s varied climate has enabled Israeli growers to grow a wide range of fruit and collect them in longer periods of the season compared to foreign growers. Declining prices abroad as a result of currency fluctuations and a corresponding trend to reduce orchards,

13

have been reflected in a continuous decline in export sales (i.e. US$ 278 million in 1996 to US$ 192 million in 2000). The most marked decline has been in citrus, whose sales abroad plummeted by half during that period. A shortage of laborers mainly due to political instability has led to the abandonment of approximately 16% of the citrus plantation areas. Nevertheless, the revolution in the fruit sector in the country has been the dramatic increase of yields; new plantations and varieties offering better yields along with the introduction of the latest agro technology. Within a period of seven years, the average yield of avocados was increase from 70 Kg per 1000 m2 to 1,250 Kg per 1000 m2. Also, in the citrus sector despite the fall in the plantation area, income has fallen by only 6% and that was mainly due to currency fluctuations. Domestic support measures have overall managed to cushion growers from the full impact of inevitable changes and allow them time and flexibility in shifting into different activities still in the same sector. Vegetables: Growing vegetables in Israel has become a multilateral task, which includes different hybrid varieties, fertilizers and irrigation methods, selecting green house covers, employing innovative tools and post-harvesting techniques. Special market niches are also a particular attribute to local growers like organic farming produce and the application of hydroponics. Organic production has been rising constantly and herbs (a lucrative item) have become the darling of growers fetching high margins of profit to them. Vegetables account for about 17% of Israel’s total crop output value. In 2000, the country’s farmers produced some 1.2 million tons of which 150,000 tons were exported. Greenhouse use has increased and now it covers about 3,000 hectares. Greenhouse use has obvious benefits (i.e. raising tomatoes in the open field yields about 80 tons per hectare whereas greenhouse production raises that to as much as 300 tons per hectare). Furthermore, growing vegetables in the desert through vast support measures by the government allows Israeli growers to offer off-season vegetables through the application of saline water irrigation (Appendix Table 13). 2.3 – Agricultural Trade Policy Measures Throughout the world governments have always tried to aid producers by providing support through various measures always at the expense of state finances and local consumers. Israel, despite its weakness of circumstances and location, has been engaged in such practices too for years to a varying degree of course. These policy measures had the following aims: to maintain domestic prices of farm goods at levels higher and occasionally lower than those at the country’s border (i.e. market price support) and to provide payments to farmers based on criteria such as the quantity of a commodity produced, the amount of inputs used, the number of animals kept, the area farmed or the revenue or income received by farmers (i.e. budgetary payments). A crucial point to note here is that contrary to popular opinion, support not only comprises budgetary payments that appear in government accounts but also the price gap for farm good between domestic and world markets as measured at a country’s border. In fact, the latter constitutes the lion’s share of support for some agricultural commodities in many countries. Israel’s main barriers to trade in industrial goods appear to be non-tariff barriers rather than tariffs. As a result of the wide array of free-trade agreements concluded by Israel with foreign

14

countries, the large majority of manufacturing imports enter Israel under preferential (mostly duty free) rates. For manufacturing imports from other sources, the overall tariff protection is moderate (simple average, including ad valorem equivalents of 6.6% for non-food products and 8.2% for electronic products except for food, beverages, clothing and footwear industries which face relatively high tariffs). In this context it is interesting to note that seems to be a negative relationship between the degree of tariff protection and the industries’ performance. The high performing high-tech industries tend to have lower than average tariff protection, whereas the slow growing traditional industries tend to be protected by higher than average tariffs. Israel has a number of other measures affecting trade and production of manufactured products including strict enforcement of technical regulations in the form of mandatory standards covering most imports of the ISIC industries food, beverages and tobacco and textiles, clothing and leather products and government procurement references for all industries. Government support to the agricultural sector amounted in 2000 to US$ 169.7 million. This figure represented 5% of agricultural production value. The long-term trend in Government policy is towards a sharp decline in the overall subsidies to the sector. The two most important items, which represent public support to the sector are the Development Budget, which assists farmers in investing in production assets (US$ 32 million) and the Use of Water (US$ 65.7 million).

Agricultural products discussed below have enjoyed over the years very favorable treatment by the Israeli Government through heavy use of an arsenal of subsidies, cheap water, protected markets of relevant products which are further enhanced through high levels of tariff protection and import quotas. Measures Affecting Imports: The import of agricultural fresh produce is much smaller than the export of fruits and vegetables. The positive balance of trade results from regulation and custom barriers aimed at protecting the local agricultural sector. Import licenses are a pre requirement for imports of fruits and vegetables and are issued only in two cases: in a natural disaster that causes production to be insufficient and without imports the price would sharply climb and if a bilateral agreement forced the import. As a measure of how dependent Israel is on imports of agricultural products the Import Dependency Ration (IDR), a customary yardstick, is used; the higher the IDR, the higher the dependency of Israel on agricultural imports. The Central Bureau of Statistics in Israel offers the following relevant data on Israel (Table 3).

Table 3. Import Dependency Ratios (IDR) Product Group IDR (%) Bread and Cereals 99.5 Sugar & Sweets 94.8 Beans and nuts 61.7 Oil & Fat 40.3 Fruits, Vegetables and Potatoes 26.1 Dairy 1.1 Source: Central Bureau of Statistics

15

Overall the foreign trade of fresh and processed agricultural produces in 1999 showed a deficit of US $890 millions. However, the deficit in the trade of fresh produce was only US$ 176 millions. This gap between export and import is the result of large imports of cereals and timber in the range of unprocessed produce and of also importing processed products such as sugar, meat and fish which are only partly produced in Israel or not at all. The foreign trade balance of Agriculture in Israel is shown in Table 4. A monitoring of the agriculture trade balance from 1979 until 2001 shows the steady inclining course of imports (Table 5). As an added statistic note that agricultural imports were at US$ 2.1 billion in 2003 of which $568 million were from the US and US$ 780 million from the EU.

Table 4. Foreign Trade Balance of Agriculture (US$ Millions at 1999 Prices) Export fob value % Import cif value % Grand Total 1,228 2,118Fresh Agricultural Produce (Total) 782 100.0 958 100.0Field Crops* 89 11.4 509 53.1Vegetables 159 20.3 36 3.8Flowers** 221 28.3 6 0.6Fruit 81 10.4 88 9.2Citrus 134 17.1 0 0.0Livestock Products 22 2.8 131 13.7Seeds 76 9.7 19 2.0Timber -- --- 169 17.6Processed Produce (Total) 446 100.0 1160 100.0Meat and Fish Products 34 7.6 184 15.9Fruit and Vegetables Products 175 39.2 144 12.4Sugar and Sugar Products 26 5.8 158 13.6Cereals 29 6.5 92 7.9Others*** 182 40.8 582 50.2Source: Planning Authority, Ministry of Agriculture and Rural Development * Imported field crops include grains, raw cotton and tobacco ** Flowers include propagation material, *** Others including tropical products, such as coffee, cocoa and tea, alcoholic beverages, etc

Table 5. Foreign Trade (Imports in US$ Millions) Period Agricultural Total 1979-1981 936 7,843 1989-1991 1,204 15,144 1998 1,832 27,469 1999 1,842 31,090 2000 1,810 35,750 2001 1,864 33,319 Source: Ministry of Agriculture

16

Measures Affecting Exports: The export of agricultural products in Israel is a practice and industry unlike similar others in other countries worldwide. Reasons for this abound but it is important to define the most important ones that are the sign of the high degree of development and professionalism in the sector in terms of high value added achieved in agriculture and the links that have been created by and for it throughout the economy. An overall general analysis of the export industry of agricultural products in Israel shows that the volumes are growing, the volume of exports of processed agricultural processed products is declining, and imports over exports stand at a ratio of seven in value and at fifty in quantities. Comparisons in terms of value added shows that what Israel exports is far superior to what it imports (estimates show this to be at an average of US$ 1,697 per ton of exports to US$ 246 of imports). A big part of this is owed to the fact that Israel is unique in that it exports large quantities of agricultural inputs in addition to doing so with agricultural outputs (i.e. goods). In 1990, imports vs exports stood at a ratio of 3.3 and in 2002 it had reached 6.5 due to the Treaties and Agreements Israel had entered into covering its trade with the outside world. Such developments of paramount importance were the WTO Membership extended to Israel in 1995 as well as the Association Agreement with the EU that opened the doors wide open to imports of agricultural products – and others – from various other countries. Even when dealing with imports, the Government’s priority is with the increase in the value of exports. An excellent case in point is the 2003 signing of the ‘New Agricultural Trade Agreement’ with the EU. The Agreement increased customs-exempt export quotas for wine, flowers, grapes and salads among clauses on imports as well. The previous (Regular) Trade Agreement between Israel and the EU included customs-exempt exports (and imports) but excluded agricultural trade. The new Trade Agreement increased quotas for agricultural and agricultural-based industrial products, including customs-exempt Israeli export quotas for products mentioned above. For example, the quota for Israeli wines exports was increased by 200,000 liters per year. Customs-exempt quotas were increased for Israeli imports for specific imports to the dismay of local producers. The official Government reply to them is of interest and demonstrates the grave importance they attach to the export of agricultural goods and foreign trade overall to Israel as a whole. The main advantages of the Agreement were the granting of export quotas for products in which no customs-exempt exports had been allowed and the creation of a mechanism for gradually increasing Israeli exports in products with quantitative quotas. An important part of Israeli exports of agriculture-related goods is also that of the trade in agricultural inputs in which Israel has managed to create and sustain an advantage worldwide. It is the direct product of a conscious support policy by the Government over many years and careful planning due to the collaboration of various stakeholders, i.e. researchers, extension workers, farmers and agriculture-related industries. Israel’s agricultural sector is characterized by an intensive system of production stemming from the need to overcome the scarcity in natural resources, particularly water and arable land. The constant growth in agricultural production (both inputs and outputs) is due to the close cooperation of the above-mentioned stakeholders. These four factors develop and apply new

17

methods in all agricultural branches. The result is modern agriculture in a country where more than half of its area is desert. The close collaboration between the research and development and the industry led to the development of a market-oriented agribusiness that exports agro-technology solutions worldwide (Table 6).

Table 6. Israeli Export of Agricultural Inputs in 2001 (000s USD$) Input Type Export Sales Water and Irrigation 89,364 Plasticulture 37,693 Veterinary Products and Feed Additives 42,923 Livestock and Poultry 12,814 Consultancy and Know-how 12,311 Mechanization 56,029 Seeds 61, 270 Fertilizers 648,714 Chemicals 352,648 Source: Ministry of Agriculture

Furthermore, various agricultural inputs industries that have developed on this logic that include greenhouses, dairy farming, poultry farming, aquaculture, water and irrigation, seeds, mechanization, fertilizers and pesticides as well as turnkey projects, consultancy and know how. Greenhouse technologies like specialized plastic films and heating, ventilation and structure systems, that are particularly useful for high added value crops and enable Israeli farmers to grow more than three million roses per hectare per season, are export oriented. The irrigation industry in Israel was a pioneer in developing innovative technologies and accessories like drip irrigation, automatic valves and controllers, media and automatic filtration, low discharge sprayers and mini-sprinklers, compensated drippers and sprinklers. The computer-controlled drip irrigation saves huge quantities of water and enables them the supply of fertilizers with irrigation (i.e. fertigation). The innovative irrigation industry has a worldwide reputation and more than 80% of its production is exported. However, the most remarkable development is the application of fertilizers through drip irrigation buried in the ground in order to ensure that less mobile components such as phosphorous, will reach the roots directly. Other innovations include the controlled release fertilizers, coated in polymers to ensure slow, prolonged release and delivery via diffusion and allow better exploitation of the fertilizer and less groundwater pollution.

Export subsidies: Israel provides export subsidies to a number of agricultural products like cut flowers, vegetables, citrus and other fruit, goose liver and cotton. In 1997/1998, export subsidies of around US$ 1 million were granted only to cut flowers. However, this does not mean that the export subsidy system was eliminated for the other products. Israel’s current policy is aimed at reducing the provision of such export subsidies to a minimum. Israel has also made export subsidy commitments regarding the six-product groups under the WTO Agreement on Agriculture. Over the 1995-2004 period, agricultural export subsidies were to

18

be reduced by 24% in value from a total of around US$ 56 million in the base period to US$ 43 million in 2004. Generally, this has progressed well and it has already taken place with minor adjustments and postponements. 2.4 – Measures Affecting Input Use Input Subsidies (Water): In Israel, water is perhaps the most important factor of production in agriculture and inevitably has to be supported by the Government through various schemes. Thus, supervision of the country’s water supply includes: determining water quotas, progressive pricing, fully controlling groundwater pumping, initiating conservation, and supply-enhancing projects. All of the above measures have in fact the impact of input subsidies on this important input in agriculture by placing a premium on the ability to access water. Furthermore, in addition to water rationing and desalination, the treatment and reuse of all urban wastewater is another array of support measures by the Israeli authorities that can assist growers in a cost-reducing manner (i.e. subsidy like) by providing the initiative and infrastructure needed (Appendix Table 14). Tax (fiscal) policy: In Israel all government activities are highly programmed well into the future, which remains always a source of hope and anxiety for the country. Fiscal and tax policies could not be any different since multiple demands on the state’s economy and budgets are always present driven by issues of foreign policies and security concerns. At the same time, the economy has to be kept on track with its sub sectors (i.e. tourism, agriculture, etc) contributing their dues allowing them to progress and prosper. Beyond favorable tax treatment to farmers who opt to reside and work either at the various Kibbutz and Moshav settlements around the country, most other tax measures and discounts come in the form of subsidies and grants. The last three State Budgets have tried to combine solutions to the simultaneous problems of increasing deficits with ways to assist economic activity through reductions in government expenditures and taxes. The simultaneous allocation of resources for the recent disengagement from the Gaza Strip has made the task even harder. Thus, priorities had to be established and by looking at the reduction of resources allotted to various Ministries in Israel is adequate proof that currently the sector of agriculture is not a priority for Israel. In the 2004 and 2005 State Budgets 6% and 5% reduction on all ministries was imposed. Evidently structural changes in the Israeli economy have now become part of the annual state budgets and the tools for taxes and incentives to work. Tax rates in Israel are high in relation to the standard in western developed nations. An elevated tax rate on labor incomes serves to lower the incentive to seek gainful employment and is detrimental to the economy’s growth potential. The tax reforms whose implementation began in 2003 are intended to lower the tax burden on labor while enlarging the tax base on revenues from capital and revenues originating from abroad. Income taxes were reduced further in 2004 in order to increase the profitability of work. The budget of 2005 continues the existing policy of lowering taxes and will include the continued lowering income taxes, lower stamp duty and corporate taxes. This clearly benefits agriculture both at an individual as well as at a corporate level.

19

2.5 Infrastructure Policies Research and Development: Israeli seeds and seedlings are sought after on world markets. Disease resistant seed varieties that are durable in storage and are suitable to a variety of climatic conditions are under constant development at Israel’s research institute and at private companies. Some 40% of the tomato greenhouses in Europe utilize seeds of a tomato hybrid with long shelf life developed and produced in Israel. Other successful developments are: seedless watermelon, resistant squash, high-yielding cucumbers, saucer-shaped yellow zucchini, a variety of hybrid cotton with longer and stronger fibers and high yield crop requiring less water, naturally colored cotton and more. Agricultural research in Israel is a nationally accepted mission and thus, significant long term effort and funds are diverted to it for many years. With such little arable land, scarce water resources, an increasing population and a permanent political problem that goes to the core of the Israeli state’s very existence, solutions to the ensuing problems will be provided through innovative approaches. These approaches and modes of thinking can only be implemented through constant and relentless research. For example, advancing agriculture through research and innovations is a very important tool for Israel against the incident of desertification. The currently trendy labeling of high tech agriculture currently sweeping the dry areas of our planet attributes a lot of its beginnings to a long array of Israeli innovations. Currently, in Israel, there are many research institutions focused on agricultural research aside from the ones active within Universities. These are the Agricultural Research Organization, Central Experimental Station, Desert Agriculture Research Station, Gilat Research Center, Golan Research Institute, Institute for Technology and Storage of Agricultural Products, Institute of Agricultural Engineering, Institute of Animal Science, Institute of Field and Garden Crops, Institute of Horticulture, Institute of Plant Protection, Institute of Soil, Water and Environmental Sciences, Newe Ya’ar Research Center, and Soil Erosion Research Station. It should be noted that approximately 75% of all research in agriculture is currently conducted at the Agricultural Research Organization (ARO). As such it is the primary driving force behind Israel’s internationally acclaimed agricultural achievements. The ARO incorporates seven institutes on its main campus and four off-campus experimental stations. Numerous ARO developments, particularly in irrigation, arid zone agriculture and unique varieties of fruits, vegetables and ornamentals have been commercialized in Israel and abroad. Extension and Education: Dealing with subjects ranging from plant genetics and blight control to arid zone cultivation, Israel’s agricultural research and development has developed science-based technologies, which have dramatically enhanced the quantity and quality of the country’s produce. The key to this success lies in the two-way flow of information between researchers and farmers. Through a network of extension services (and active farmers’ involvement in all research and development stages) problems in the field are brought directly to the researcher for solutions and scientific results are quickly transmitted to the field for trial adaptation and implementation.

20

The drive to achieve maximum yields and crop quality has led to new plant varieties, breeding of improved animal species, and a wide range of innovations in irrigation and fertigation, machinery, automation, chemicals, cultivation and harvesting. The telecommunications revolution of the late 1990s also made its mark on farming methods in some sectors with more and more farmers employing mobile phones, the Internet and computer-guided supervision as basic working and marketing tools. These are also found in other countries, but the unique permanent relationship between researchers, farmers, agriculture-related services/industries and extension workers is only found in Israel. Through this association there is a permanent Extension and Education branch at work in Israeli agriculture whose benefits are magnified in the economy due to its effectiveness. Since the late 1950s, Israel has been sharing its agricultural expertise with scores of countries. MASHAV, the Center for International Cooperation of the Ministry of Foreign Affairs is active in Asia, Africa, the Mediterranean Basin, Eastern Europe and Latin America as well as several Middle Eastern countries.

Quality and Sanitary Control: Israel is very active in all facets of sanitary control that result in an increase in the quality of life. Recycle services of solid waste are one such area in which Israel has been making strides through innovative approaches in creating and evaluating options for the efficient solid waste management. Municipalities have been coping with increasing amounts of solid waste and the need to formulate efficient and sustainable solutions to deal with problem. Recycling is often proposed as one of the options. High household participation in the recycling effort would result in the most economically efficient solution. However, households in Israel are not always willing to fully cooperate, especially if cooperation involves a large amount of investment of time, space and out-of-pocket expenditure. Studies conducted to examine policy measures which would render recycling the preferred solution on economic efficiency grounds were apocalyptic as they were able to monetize the costs and benefits of the practice thus specifying the optimum subsidy for the households to buy double-compartment containers for ‘wet’ and ‘dry’ waste separation (Ayalon and Avnimelech, 2002). In the field of quality and sanitary control noticeable advances include: environmental growth, air pollution, environmental and resource valuation, waste management, climate change, biodiversity, and water management. Freshwater sources in Israel have been almost fully exploited. Reliance is now being placed on re-use of sewage effluent and (in the future) desalination of both seawater and sewage effluents. The Shafdan Plant in Tel Aviv has led the way in re-use of sewage effluents on a large scale. Wastewater from a regional population of 1.3 million is treated and then discharged into adjacent aquifers. This water is then transferred to the Negev in the ‘Third Negev Pipeline’ for use in irrigation of agriculture in the western Negev. On a smaller scale, plants in the Negev itself provide effluent for local agricultural products. Desalination of Mediterranean Sea water is currently becoming a reality with the construction of a Reverse Osmosis Plant.

Use of Reclaimed Sewage Effluents: Currently Israel uses approximately 250 to 300 m3 million/yr of reclaimed sewage effluents, principally to augment supplies for agricultural irrigation. The use of reclaimed water for agricultural purposes, aquifer recharge, and even

21

urban purposes is expected to increase markedly in the near future. The use of membrane filtration to ensure safe water for a range of uses is also expected to be actively pursued.

Water Use Efficiency and Water Conservation: Water conservation and water use efficiency are extremely important to water resource management in Israel. These objectives are being achieved through realistic water pricing, community education and awareness, advances in irrigation technology and revolutionary agricultural practices.

Mitigation of Salinity Impacts on Infrastructure: Urban salinity and its deleterious impacts are not a major issue in Israel, principally because most aquifers are very deep and there is an absence of dry land salinity. Overall, it is anticipated that future supplies of fresh water will largely rely on desalination of Mediterranean Sea water (McGregor, 2002). Structural Policies (land, land reform, etc): Israel’s very small agricultural land available for productive purposes is divided in other sub-categories in terms of uses. Thus, land is used either as pasture, irrigated orchard, non-irrigated orchard, irrigated field crops, and non-irrigated field crops. The regions where this land is found are in the Upper Galilee-Golan, Western Galilee, Northern Valleys, Central Region, Central Plain and Mountain, and in the Negev Region. Approximately, 93% of the land in Israel is public domain; that is, either property of the state, the Jewish National Fund or the Development Authority. The Israel Land Administration (ILA) is the government agency responsible for managing this land, which comprises of 5,750,000 acres. Ownership of real estate in Israel usually means leasing rights from the ILA for 49 to 98 years. The legal framework of the above environment is comprised of four cornerstones that make up the legal basis of the Israel lands policy: basic law establishing the Israel Lands Administration (1960), Israel Lands Law (1960), Covenant between the state of Israel and the World Zionist, and Organization (Jewish National Fund) 1960. The Israeli Lands Council functions are: guarantee that the national lands are used in accordance with Israeli laws, actively protect and supervise state lands, make state land available for public use, plan, develop and manage state land reserves, initiate planning and development (include relocation of existing occupants), regulate and manage registration of state lands, authorization of contracts and agreements with other parties, provide services to the general public, designation of land areas for public and state requirements, assuring land reserves for future needs, preservation of agricultural lands, land usage in accordance with the law, safe guarding the state lands (Israel Land Administration). Agricultural Infrastructure: Water: Israel has three main water sources: the Sea of Galilee, the Coastal Aquifer and the Western and Northern Aquifer of the so-called Mountain Aquifer. Together these sources have a safe annual yield of roughly 1,350 million m3 (Kliot, 1994). The Galilee and the Coastal Aquifer are both entirely within the pre-1967 borders of Israel and both were extensively developed and used by Jewish residents even during the period of the British Mandate (this is well before 1948).

22

The Western Aquifer has a safe annual yield of roughly 360 million m3, and it is fed by rain falling on the western slopes of the West Bank’s Judean and Samarian Mountains. The water percolates through porous surface rock into the aquifer below the surface and then naturally flows downwards towards the Israeli coastline. Prevented from actually reaching the coast by natural hydrologic barriers the water instead emerges in natural springs, which are almost entirely in Israel. As early as the 1950s, Israel used 95% of the Western Aquifer’s Water. Most of the Western Aquifer’s water is stored under Israel and the water is easily accessible only where the storage area approaches the surface. The Northern Aquifer has a safe annual yield of 140 million m3, and it is fed by rain falling on the north-central slopes of the Samarian Mountains. Most of the aquifer’s catchments are in the West Bank. On the other hand most of the water from wells and springs emerges in pre-1967 Israel, a fact that keeps the debate of Israel using Palestinian water alive. The natural scarcity of water for agriculture in Israel has been a major factor for the strong Israeli drive towards agricultural irrigation technology as well as agricultural practices that are fundamentally, water-efficient. Irrigation: The country has eight major and several small-to-medium-sized companies producing irrigation and filtration equipment, all internationally active. The last few years due to the continuous incident of low rainfall, agricultural use of potable water has been reduced substantially – from 900 million m3 in 1995 to an estimated 740 million m3 in 2001. As a result of ongoing government pricing and rationing measures to curb fresh water use and the commissioning of more sewage treatment plants, use of treated sewage rose from 250 million m3 in 1990 to 270 million m3 at present and is expected to rise to 500 million m3 by the end of 2005 as new sewage treatment plants and pipelines are commissioned. Over the past twenty-five years, agricultural output has increased sevenfold with hardly any increase in the amount of water used (Statistical Abstract of Israel). This reflects technological advances, water-use efficiency (up by more than 30 %) and crops with higher yields and market value. To reduce the water used for agriculture, advanced water and saving techniques were applied, notably the drip system, which directs the water flow straight to the root zone of plants. In addition, computerized irrigation systems were introduced and climate-controlled greenhouse agriculture was significantly expanded (Appendix Table 10 and 14).

Israeli engineers and agriculturalists created the revolutionary drip system, which has reduced water consumption by 50-70% compared with gravity irrigation and by 10-20% compared to sprinkler irrigation. Recently growers have been introducing the first generation of ultra-low application rate (minute irrigation) drip emitters for soil-less media in greenhouses, emitters with 100-200 cc/h flow rates. Even more advanced than the drip system, they create optimal air-water relationships in the plants’ root zones and, being more efficient, save yet more water. Micro-spaying and micro-sprinkling irrigation accessories have also been developed, mainly for use in orchards where each tree is irrigated by its individual sprayer. To overcome regional imbalances in water availability most of the country’s freshwater sources have been joined into the National Water Carrier, an integrated network of pumping stations, reservoirs, canals and pipelines, which transfers water from the north where most of

23

the sources are, to the agricultural areas of the semi-arid south. As a result, the amount of irrigated farmland has increased from 30,000 ha in 1948 to some 192,000 today. The future direction and success of Israeli farming, too, will depend on water availability: in particular, the ability to even further minimalises water use and in general to use more saline and/or recycled wastewater and less potable water (Fedler, 2002). Use of Recycled Sewage Water: A frequently cited proposal is that recycled sewage water can be used to solve the water shortage in Israel by replacing the fresh water used for agriculture (Appendix Table 11). There are however, serious limitations to this measure that severely impair the scope of its feasibility as an overall solution. There are undesirable side effects indeed both economic and environmental. These include the following: Recycled Water after the usual secondary purification treatment (i.e. of biological but not chemical pollutants) prevalent today, has a high content of salt and contains other dissolved substances and apparently even traces of heavy metals and carcinogenic materials thus posing the risk of severe damage to drinking water supplies; Recycled water can also cause the ruin of agricultural land because of its high salinity resulting in significant damage to the soil; The use of recycled waste also impairs agricultural yields up to 25% relative to those attained with fresh water irrigation; The cost of conveyance and storage may result in a heavy economic burden on the country and carrying wastewater from the urban centers where the facilities of recycled sewage water are located to the rural areas for agricultural use is an expensive feat on the Israeli taxpayer. 2.6 – Rural Development Policies In the early 1990’s it had become abundantly clear in the Israeli Government that by 2020 more than 50% of the area of Israel will inevitably become one of the most crowded areas in the world. In 1992, the Government proceeded to establish the Ministry of Environment. The general trend in rural areas was and still is the declining effective labor power working in agriculture, and increasing non-agricultural entrepreneurship (from a low percentage to approximately 10% today and projected increases for the future).

The main activities that substitute agricultural sustainable activities include tourism, commerce and services. Areas and subjects addressing rural and agricultural development are covered by projects, which may include: research, development, semi-commercial and commercial. Furthermore, another spectrum of activities in which work is carried out at the decision-making level includes: national level projects, regional and district level projects and community and private level projects. A number of Ministries, including the Ministry of Agriculture, Health, Environment and Labor, among others, are involved in projects aimed at promoting rural development and sustainable agriculture. One of the most significant changes in raising awareness, regarding this subject includes the introduction of periodical statistics, which attempt to cover and understand the major trends relating to changes in the rural structure. This applies mainly to the shift from traditional farming to developed entrepreneurship going beyond agriculture. This however, creates other environmental problems.

24

The rural population represents 8.6% of the total population of Israel. However, employment in agriculture occupies only 14.5% of the total manpower living in rural areas. The remaining employed people are engaged in various economic activities, such as industry, construction and transport (26.7%), tourism and commerce (13.4%) and services. Difficulties in the agricultural sector forced the need to look for alternative sources of employment in the non-agricultural sector. In general, the number of persons employed in agriculture amounts to approximately 30% of total population in the rural area. Farmers’ awareness is reflected in their work and their participation in symposia and volunteering committees. Although, through the two formats of agricultural activity mentioned above, farmers are indeed in a position to identify major problems, the lack of financial resources limit their capacity for further achievements. Two of the most relevant achievements in this area are Integrated Pest Management and Bio-Organic crops. Both of them are well advanced both on a scientific and practical commercial level. As part of the rural development policies, Israel embodied the Convention on Biological Diversity (signed in 1992 and ratified in 1995) as well as the Convention on International Trade in Endangered Species of Wild Fauna and Flora (ratified in 1980) into a National Strategy plan for the conservation of its biological diversity thus inevitably linking them with rural development policies. One of the major activities indirectly related to agriculture was the creation and expansion of tourism facilities in rural communities. During the last decade these efforts resulted in a very rapid increase in the number of rooms offered to tourists. The tourism industry in the rural area is composed of bed and breakfast accommodation in the villages themselves as well as youth hostels, hotels and resorts located in rural regions. In 1999, the total number of rooms available for tourists has reached 13,047 and the number of employed people in the industry is estimated to be 5,000. In the past, it has been stated that agricultural land should be abandoned as part of state policy and used for construction purposes, a sector that offers higher valued added to the economy (The Israel Center for Social and Economic Progress, 2001). 2.7 Agro-Environmental Measures Israel is a well-developed country with complete access to potable water and sanitation. Water is by far the most limiting natural resource and supplies located near national boundaries have been a source of conflict. Despite this, Israel has maintained agricultural growth, partly by water conservation measures such as drip irrigation. Marine pollution has decreased through legislation and enforcement. The air quality in urban centers is expected to improve as unleaded fuel and catalytic converters become more prevalent. Forests are found mostly in the higher elevations. About 6% of the country is forested and about 37% of that is natural forest. Roughly 25 km2 are replanted with trees each year. Limited but important fringing coral reefs occur along the short Red Sea coast. Much of the arable land is intensively farmed and water run-off from irrigated plots is frequently

25

contaminated with farm chemicals. Nearly all of the region’s wetlands had disappeared by the mid-20th century leaving only one small parcel of any significance by 1980. The ravages of modern warfare have made it difficult to establish and maintain protected land and to preserve habitats. Nevertheless, about 14.9% of the land is protected as national parks, nature reserves or forest reserves. The country is a participant of the United Nations Education, Science and Culture Organization (UNESCO) Man and the Environment program and contains one designated biosphere reserve. Nature conservation and biodiversity protection in Israel is not a recent development. Israel’s location at the crossroads of climatic and botanic regions gives the country a rich variety of plant and animal life. Within the small land area of Israel, two opposing climatic regimes are found – Mediterranean in the north and desert in the south. The central part of the country is essentially a transition area between these two bio-geographical regions. Following the second meeting of the parties to the Convention on Biological Diversity, Israel set out a series of steps to be taken for the purpose of preparing a national strategy plan for the conservation of biological diversity. Some are as follows: the establishment of an interministerial committee comprised of representatives of the Ministries of Environment, Agriculture, Interior, Science, Trade and Industry, Transport, Defense and Education, the integration of conservation of biological diversity into environmental planning and the preparation of guidelines for the protection of biological diversity, which will constitute part of the Ministry of the Environment guidelines and priority to research proposals on the conservation of biological diversity to be partly financed by the Ministry of the Environment. Israel has ratified a number of international environmental agreements, including those on biodiversity, endangered species, hazardous wastes, and nuclear test ban, ozone layer and ship pollution. It has also signed the World Heritage Convention and the Ramsar Convention on Wetlands. Israel is a participant in several regional agreements focused on the protection of the Mediterranean coast. The Ministry of Environmental Affairs, in collaboration with the Ministry of Agriculture and others are addressing agro-environmental issues. They relate to three levels of decision-making and time frame; long term strategy at the national level, medium term tactic at the regional/district levels, and short term operative at the regional, community and private levels. The spectrum of intervention means include: information, master planning, available forecasting and environmental legislation and regulation against various types of pollution. As part of agro-environmental measures, there are plans to implement regional pilot projects such as recycling organic matters and plastic. Progress is also reflected in locally organized institutes, which identify ideas and needs and put them into practice. Farmers, local entrepreneurs and the scientific and technological community participate in projects, which promote rural and agricultural development. There has been an impressive change in farmers and local entrepreneurs who are aware of the environmental problems that they create. The commitment of farmers and their representatives has been achieved and in some cases, it has been possible to come to positive decisions, which include investments and

26

programs (mainly in the North of Israel, a very sensitive area for the quality of water for the entire nation). In order to promote environment issues the government conducted negotiations with the various stakeholders that resulted in the definition of criteria for direct financing of preferred environmental projects related to agricultural activities. 2.8 Measures Affecting Consumers Until 2004 the agricultural production and marketing was been regulated by 10 production and marketing boards: 3 boards administrated the marketing of livestock, poultry, milk, and honey and 7 administrated the marketing of fruits, vegetables, citrus, flower and ornaments, wine and grapes, peanuts and olives. The boards were established based on the perception that many growers who produce undifferentiated products and few buyers result in unfair balance of power. To be specific, most fruits and vegetables are sensitive to climate change, non storable, and their quality cannot be fully monitored. Production flexibility is very limited (i.e. growers plant long time before demand and supply are realized) and buyers of agricultural products are stronger than sellers (i.e. institutional buyers have stronger bargaining power than sellers and marketing to foreign countries is characterized by economics of scale). The marketing and production boards aim is to balance out this uneven state of affairs between growers and distributors. The production and marketing boards had the authority to control long run and short run quantities. Long run quantities were controlled by law. It used to be illegal to plant perennial (trees) crops without getting a permit issued by the production boards. A similar principle was implemented in the production of meat, fish, poultry and eggs. Short-term stability was achieved by controlling quantities produced via a monopolist mechanism. Crop surpluses were destroyed to prevent price falling below certain levels (an act that was termed surplus clearance). For many years the Israeli government backed up this policy to guarantee minimum price for most of the fruits and vegetables, but recently this policy has changed and no such guarantee is given. Production and marketing boards and other grower associations finance their operation by charging farmers about 4.5% of their revenue. This mandatory fee is designated for research and development of new products, to publish professional agricultural magazines, and public relation activities. Marketing: The majority of produce is distributed through packinghouses, which are either owned by cooperative of growers, or are private entities. Packinghouses classify and pack the produce and then sell it to local wholesalers or directly to the supermarket chains. If the produce is exported then the packinghouse is only another stage in the distribution channel. The classified and packed produce is then exported by one of the export companies. There are about 22 packinghouses that specialize in citrus; several other packinghouses are specialized in avocado, potatoes, persimmons and mangos.

27