national political economy analysis and fiscal space ... · case study – tanzania mainland fiscal...

TRANSCRIPT

Fiscal Space Profiles of Countries in

Eastern and Southern Africa

Case Study – Tanzania Mainland

Fiscal Space Analysis

June 2017

3

Table of Contents

List of abbreviations 5

Executive Summary 7

1 Introduction and methodology 9

2 Defining the Fiscal space 13

2.1 Macroeconomic and fiscal characteristics 13

2.2 Tanzania’s priority expenditure and fiscal space in recent years 16

2.2.1 Current and future challenges and implications for the fiscal space in the priority

sectors 18

3 Tanzania’s options for enhancing the fiscal space 23

3.1.1 Base scenario and fiscal space “mapping” 23

3.1.2 Option to increase fiscal space: increasing tax and non tax-revenue (Scenario 1-3) 25

3.1.3 Other scenarios (4 and 5) 28

3.1.4 Effects of scaling up priority expenditure in line with current policies and

programmes 29

3.1.5 Other options to increase fiscal space 32

4 Conclusions 35

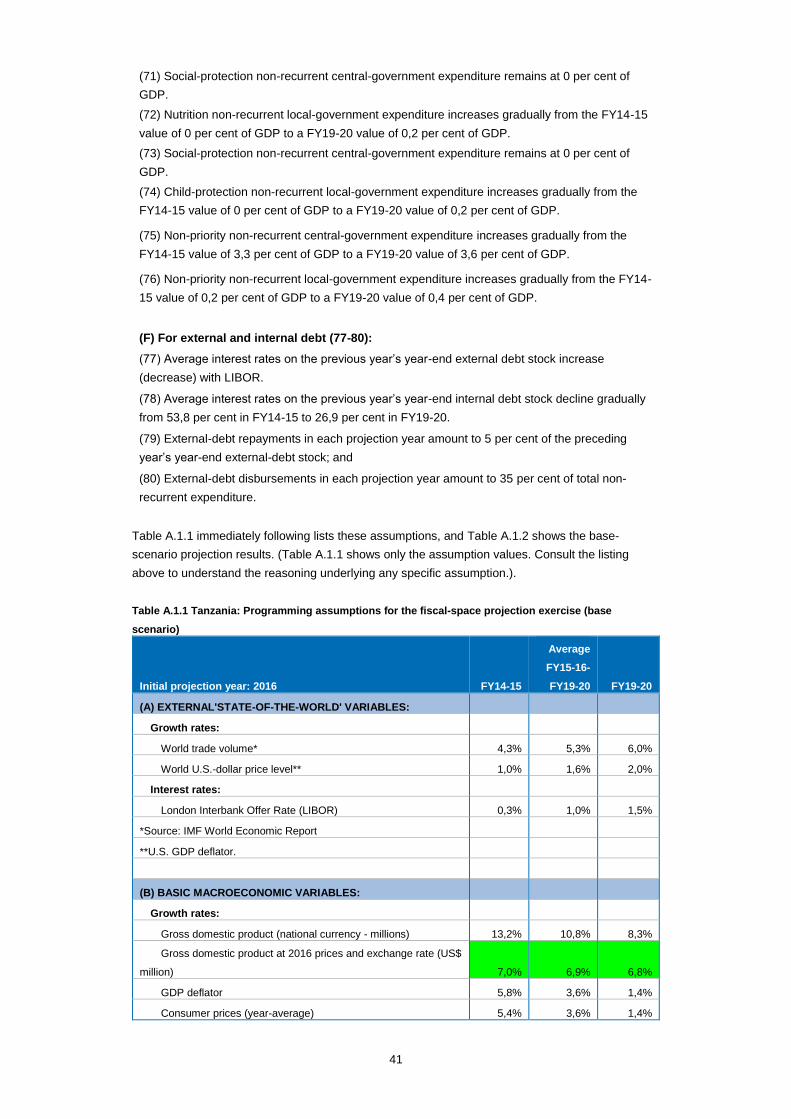

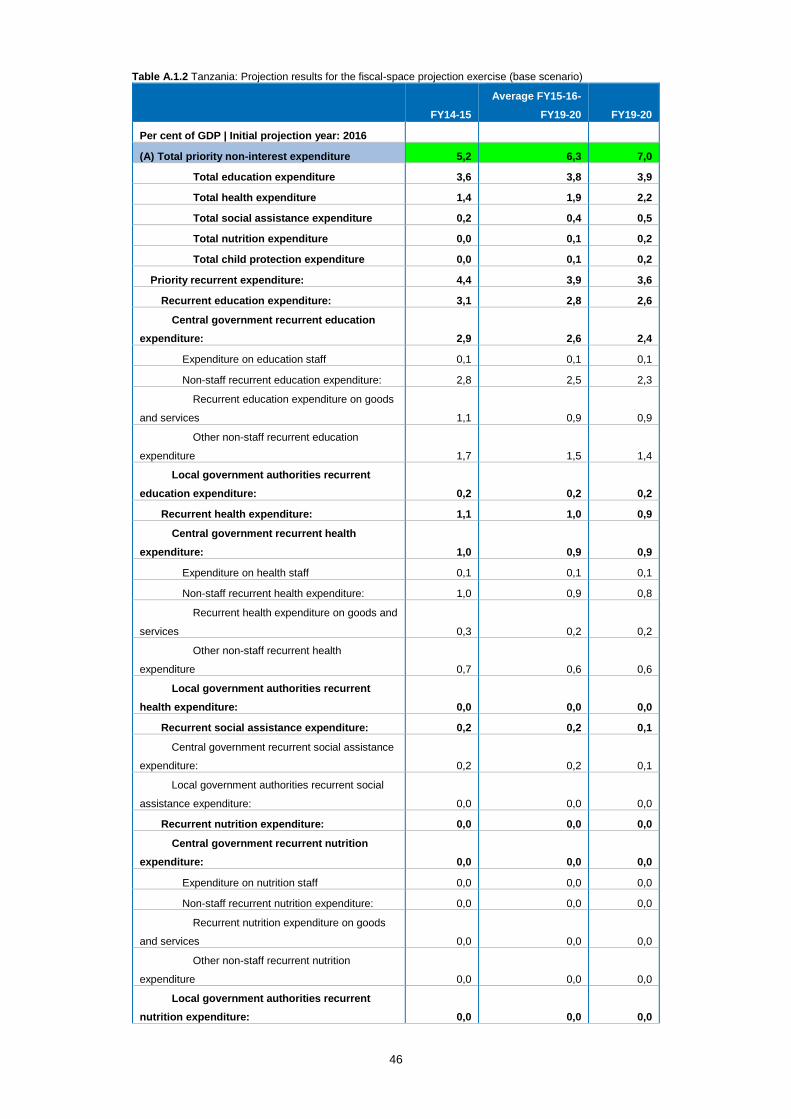

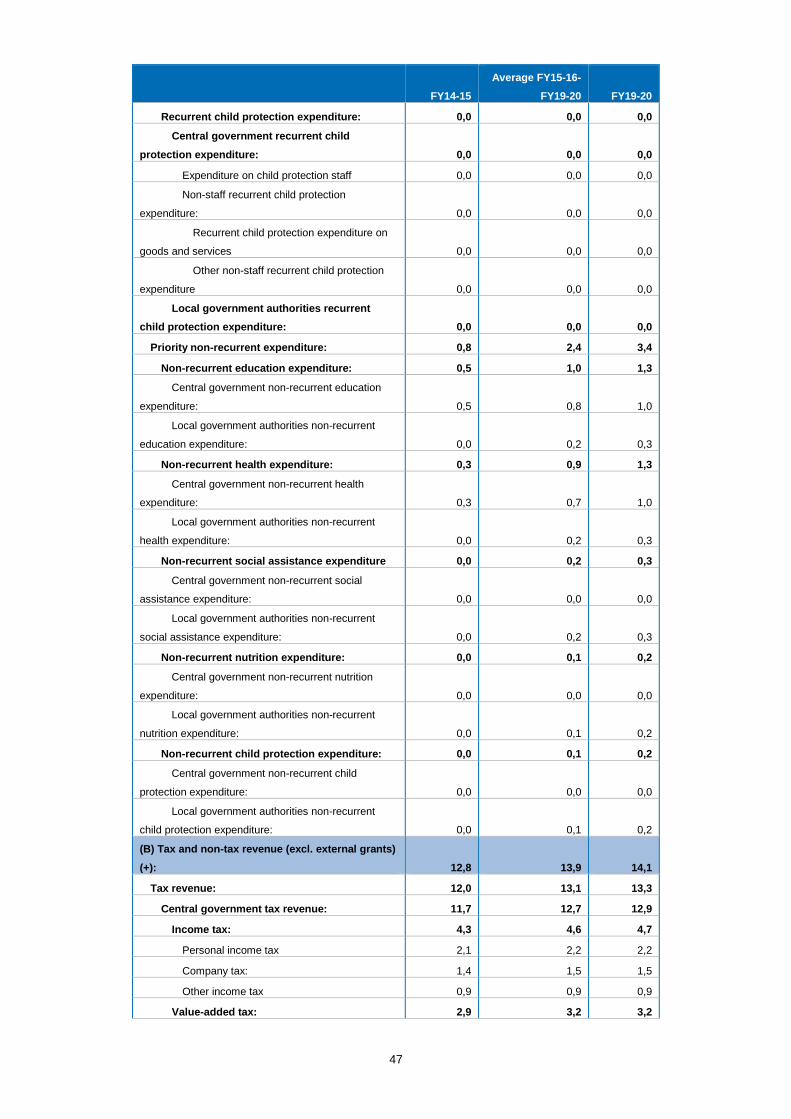

Appendix 1: Fiscal space projections 37

5

List of abbreviations

AFDB African Development Bank

CCHP Comprehensive Council Health Plan

CCM Chama Cha Mapinduzi

CSO Civil Society Organisations

EAC East African Community

FY Fiscal Year

FYDP Five Year Development Plan

GDP Gross Domestic Product

IDA International Development Association

IMTC Inter-Ministerial Technical Committee

IMF International Monetary Fund

LGA Local Government Authority

LIC Lower Income Country

MDA Ministries, departments and agencies

MoFP Ministry of Finance and Planning

MP Member of Parliament

MTEF Medium-term expenditure framework

MVC Most vulnerable children

NCPA National Costed Plan of Action

NGO Non-government organisation

NMNAP National Multi-sectoral Nutrition Action Plan

NPAC-VACW National Plan of Action to End Violence Against Children and Women

ODA Official Development Assistance

PANITA Partnership for Nutrition in Tanzania

PO-RALG President's Office Regional and Local Government

PSSN Productive Social Safety Net

SUN Scaling up Nutrition

SWO Social Welfare Officers

TASAF Tanzania Social Action Fund

TFNC Tanzania Food and Nutrition Centre

TPSF Tanzania Private Sector Foundation

TZS Tanzanian Shilling

UKAWA Umoja wa Katiba ya Wananchi [Coalition for the People’s Constitution]

US United States

VAT Value Added Tax

6

Preface

This report is part of a series of country studies carried out by Ecorys and associates for UNICEF in

Eastern and Southern Africa. The project aims to strengthen UNICEF’s advocacy efforts through a

better understanding of the role of political economy factors in processes and decisions around the

creation and use of fiscal space for investments in children.

This report was written by Paul Beckerman, Dafina Dimitrova, Jan-Willem Knippels, Gabriele Pinto

and Ivo Gijsberts.

The writers of this report wish to thank the staff from UNICEF Tanzania for their support and

guidance. They also express gratitude to the various government officials and other stakeholders

who provided inputs.

The findings, interpretations and conclusions expressed in this report are those of the authors and

do not necessarily reflect the policies or views of UNICEF or of the United Nations. The text has not

been edited to official publication standards, and UNICEF accepts no responsibility for errors. The

designations in this publication do not imply an opinion on legal status of any country or territory, or

of its authorities, or the delimitation of frontiers.

7

Executive Summary

The main challenges to expanding Tanzania’s fiscal space for priority sectors for children

include an ambitious infrastructure program, budget deficit targets, an outflow of donor

funding and rapid population growth. Tanzania recently initiated a Five Year Development Plan

(FYDP II). This includes major investments to improve facilities and infrastructure and will require a

significant increase in development spending. The government also aims to keep the fiscal balance

at -3% of GDP. Given that the fiscal balance in fiscal year (FY) 2016/17 amounted to -4.5% of GDP

and that donor funding is likely to diminish, resources will need to come from other parts of the

budget, potentially from priority sectors. At the same time, the number of children and young people

is projected to rise significantly over the coming years, and simply maintaining current levels of

spending will create additional budgetary pressures.

Among priority sectors – defined for the purpose of this study as education, health,

nutrition, social assistance and child protection – government spending has grown in recent

years, but there is still a need to improve budget execution rates and plug funding gaps.

Between FY2011/12 and FY2014/15, the Government of Tanzania spent an average of 16% of its

total budget on education, and around 8% on health. Over this period, actual expenditures on both

sectors also grew significantly in real terms. In addition, the reduction in donor support to education

and health has been met with an increase in domestic funding. Despite the increase in budgets of

the major social sectors, execution rates have not performed well, especially at sub-national levels.

Other priority areas, including nutrition, social assistance and child protection, are characterized by

low budget credibility, with major variances between budget allocations and releases.

In a baseline status-quo scenario where economic growth is in line with recent trends,

increasing spending on priority sectors based on projected needs will lead to a fiscal deficit.

Between FY2016/17 and FY2020/21, overall priority expenditure is projected to average 6.3% of

GDP, which amounts to approximately US$145 per child (at FY2015/16 prices and exchange rate).

Under this scenario, the fiscal deficit would average 3.9% of GDP.

Improving the VAT tax administration system is a first option to raise funds to pay for more

education and social protection staff. Assuming a 20% improvement in domestic and import

VAT collection, coupled with an increase in education and social protection staff, the internal debt

would be 3.0% of GDP, which is below the baseline scenario. Total government debt in FY2020/21

would total 30.8% of GDP, which is also below the baseline forecast of 31.7% of GDP.

Maintaining the current level of economic growth is another option to increase spending on

sectors that are important to children. A minor slowdown in economic growth below the

projected rate of 6.9% of GDP will not affect priority expenditure. However, if average GDP growth

slows to 4.0% or less over the projection period, the fiscal gap would be significantly larger and

likely result in an increase of total government debt by 3% of GDP compared to the baseline

scenario. This underlines the importance of sustaining current levels of GDP growth to allow for

increases in priority expenditure on children.

A third option to scale up priority expenditure is to increase administrative efficiencies.

Achieving higher budget execution rates would allow for greater actual expenditure, as available

funds would be used. The total effect on fiscal space, however, is likely to be minimal, although the

impact of current budgets would be improved. Likewise, increasing expenditure, such as by hiring

8

more staff in the education sector, will only result in a small negative effect on the fiscal space gap

since these policies are already captured in FYDP II.

Less feasible options to create fiscal space include expanding external and internal debt

levels as well as receiving greater foreign aid. Non-concessional external debt is not

recommended to fund social sector expenditure as yields from these investments are only reaped

over the long term, which extend far beyond the terms of these types of debt arrangements; the

same rationale applies to internal debt for these purposes. Moreover, in line with global trends,

external grants are likely to decline over the projection period and are not expected to be a potential

source for expanding priority spending.

Despite the challenges presented by self-imposed budget deficit targets, other spending

priorities, lower donor funding and population growth, there are many options that would

allow Tanzania to continue its commitment to boosting spending on sectors that matter for

children. The most beneficial and strategic approach is for the government to foster robust

economic growth over the near term, which will naturally increase the available revenue pool that

can be accessed for priority sectors. Other possibilities include strengthening the VAT

administration system as well as addressing existing inefficiencies in social sectors, especially

related to budget execution. Whether combined or pursued individually, these options can go a long

way to expand fiscal space and improve the lives of children across the country.

9

1 Introduction and methodology

This chapter analyses the Tanzanian government’s recent and future financial capacity to carry out

expenditure on which children depend for their human development and general welfare. This

financial capacity is understood to be the “fiscal space” underlying such expenditure. The fiscal-

space analysis has been carried out using a fiscal-projection exercise in Excel (TzFS.xlsm).

Priority expenditure categories for children

This chapter refers to expenditure categories regarded as beneficial to children as “priority”

expenditure. For Tanzania, such priority expenditure categories for children comprise the following

five “institutional” expenditure categories:

1. Education;

2. Health;

3. Social Assistance;

4. Nutrition; and

5. Child protection.

The composition of the government’s priority expenditures for children is, inevitably, somewhat

arbitrary. Government expenditure classified as “as priority” includes aspects that are unrelated, or

only loosely related, to children’s welfare, such as higher education expenditure. At the same time,

some expenditure categories classified as non-priority are highly relevant to children, notably, for

example, in the water and sanitation sector. This is especially important to bear in mind when

considering possible scenarios to enhance priority expenditure by reducing non-priority

expenditure. Future analyses of this kind may work with different definitions of priority expenditures

for children. Even so, however, the methodological approach used in this study could work in the

same way. That is, the methodological approach in itself is the fundamental recommendation.

It is also important to bear in mind that the fiscal space discussion concerns only expenditure

carried out by government within its budget, as reflected in the consolidated budget of national

government entities. Government expenditure on education and health plainly constitutes the bulk

of the resources dedicated to education and public health in Tanzania. Much of this expenditure is

in categories that only the government carries out, or could carry out. Nevertheless, non-

governmental expenditure in these sectors is also significant. Especially in the health and social

protection sector, some important programmes are funded by private and NGO entities, some of

which receive donor support. These would not be included in the government budget. The present

focus, however, is the expenditure flows in the priority sectors that flow through Tanzania’s fiscal

accounts.1

A final note refers to one of the key measures used in the FSA in order to examine and compare

both historical spending and the variation in priority expenditure under different scenarios, namely

priority spending per child. This measure takes the total spending in the priority expenditure

categories, and divides this by the total number of children aged 15 or less in Tanzania2. The

1 While it would be possible to carry out the kind of analysis this chapter describes using an enhanced set of accounts going

beyond the official budget accounts, it may prove challenging to identify and incorporate all relevant expenditure programs

and funding sources. 2 The report uses the World Development Indicators (original) United Nation’s population statistics to obtain time-series data

on age cohorts. Accordingly, data for the age cohort 0-14 is used, in the absence of statistics for the age cohort 0-17.

10

figures on per-child priority spending obtained in this way are to be treated with caution since only a

proportion of total expenditure at the institutional level benefits children directly.

Priority expenditure ‘identity’ and analysis

To analyse the fiscal space for priority expenditure, the methodology first sets from the “identity”

that governs the relationship of priority spending with its

underlying fiscal space.

This identity states that total expenditure (comprising current,

non-interest, interest, and capital expenditure) less the sum of

total revenue and external grants is equal to the overall

deficit, which is in turn equal to the net flow of external and

internal financing. If total expenditure is broken down into the

three categories of (1) priority and (2) non-priority non-interest

expenditure and (3) interest expenditure, this identity can be

rearranged for any year as shown in the box.

The “below-the-line” accounts taken together constitute the

fiscal space for the priority-expenditure flow. For a

retrospective analysis – that is, for analysis of fiscal performance in historical years – this structure

can be applied directly to show how the below-the-line flows (the retrospective fiscal space)

combined to finance the priority expenditure flows. Section 1.3 describes the historical quantitative

analysis for Tanzania, for the years FY2011/12- 2014/15.

For the projection analysis, the accounting identity is applied in a different way. For each projection

year, the priority-expenditure flow is projected on the basis of programming assumptions,

encompassing the various determinants of recurrent and non-recurrent expenditure in the

education, health, nutrition, child protection and social assistance categories. Similarly, the below-

the-line accounts, except for the net internal financing flows, are projected on the basis of

programming assumptions. The total net internal financing flow for each year is then calculated

residually, to ensure that the accounting identity is satisfied.

For any projection year, this net internal financing flow is the fiscal-space “gap”, that is, the

difference between the projected priority-expenditure flow and the fiscal space. If this gap is “too

large,” then the programming assumptions, taken together, would be considered unfeasible. The

criteria for “too large” include the limits on the government’s capacity to borrow in domestic financial

markets and the implied increase in the government’s debt-GDP ratio. Policy-makers would

presumably want to avoid having the net internal borrowing flow exceed 2-3 per cent of GDP in

coming years, to avoid having the internal-debt burden rise as a percentage of GDP.

The projection exercise is formulated by applying various assumptions, together constituting a

“scenario,” to the historical data base. The relatively simplified, illustrative projection exercise

applies scenarios to historical data (as discussed in Appendix 1). Each scenario comprises

programming assumptions for the years FY2016-2020, covering:

world economic conditions;

basic Tanzanian macroeconomic variables;

merchandise exports and imports;

tax and non-tax revenue;

external grants to the government;

government expenditure in the priority and non-priority categories; and

external and internal debt.

Fiscal identity

Priority expenditure

=

Tax and non-tax revenue

+ External grants

- Non-priority expenditure

- External debt service

- Internal interest

expenditure

+ External debt

disbursements

+ Net internal financing flows

11

For each scenario, some of the assumptions lines are set as simple numbers (growth rates,

percentages of GDP, etc.). Many of the assumptions, however, are constructed from other

assumptions. For example, the growth rates of real GDP and of the price level are numbers that the

analyst chooses for any given scenario. It is straightforward to combine these assumptions into an

assumed growth rate for nominal GDP.

Limitations of the data

This analysis is based on budgetary data covering actual figures (budget outturn) for the fiscal

years (FY) 2011/12- 2014/15. The main data source has been the Tanzania Ministry of Finance,

which publishes quarterly budget-spending reports. Additional data sources include the Bank of

Tanzania, UNICEF, as well as the World Bank/ IFC. Despite a substantial data-collection effort, the

quantitative analysis presented in the sections below is subjected to two important caveats. First,

budget execution data were unavailable for FY2015/16. Thus, the projection exercise does not take

account of actual spending figures past June 2015. Second, data on spending in the priority-

expenditure categories is limited. Functional level breakdown of data, and associated expenditure

classified under the economic classification, were not readily available in more detail. Time and

resource restructions for this study did not allow for an in-depth reclassification of expenditure.

Thus, as noted before, for the modelling exercise, which looks into aspects such as increases in

staff levels, priority expenditure categories were taken to be those of the main government

institution responsible for the respective area. Since disaggregated data were not available for more

detailed expenditure categories, we could not produce more refined definitions and calculations for

scenarios involving relevant sub-categories.

Organization of the FSA

The remainder of this report is organized as follows. Chapter 2 summarizes Tanzania’s present

macroeconomic and fiscal circumstances. It also analyses the recent evolution of the priority

expenditure flows in the categories of priority expenditure and outlines some specific challenges in

the various areas relevant for expenditure on children. Chapter 3 discusses various options

available to policy makers to enhance the fiscal space with an illustrative projection exercise for the

priority expenditure flows and the fiscal space that would fund them for the years FY2016/17-

FY2020/21. The exercise consists of a base scenario, comprising a broad range of macroeconomic

and fiscal-policy assumptions, and various alternative scenarios. Chapter 4 summarises the main

findings from the analysis. Further projection details are included in Annex 1.

13

2 Defining the Fiscal space

2.1 Macroeconomic and fiscal characteristics

Table 2.1 shows some of the basic macroeconomic indicators for Tanzania for the fiscal years

FY2011/12-FY2015/16.

Table 2.1 Tanzania: Selected macroeconomic indicators, FY2011-2016

FY11-12 FY12-13 FY13-14 FY14-15 FY15-16

Gross domestic product* $34.612.5 $36.768.3 $39.382.2 $42.124.0 $45.086.2

Growth rate 6.5% 6.2% 7.1% 7.0% 7.0%

Per-capita:

Gross domestic product** $722.8 $743.9 $771.9 $800.1 $830.0

Growth rate 3.1% 2.9% 3.8% 3.7% 3.7%

Non-government consumption** $487.8 $495.2 $503.7 $480.4 $499.7

Growth rate 2.5% 1.5% 1.7% -4.6% 4.0%

Per cent of GDP:

Gross fixed capital formation 31.6% 30.5% 31.6% 33.6% 35.6%

Central-government fiscal surplus -3.2% -4.6% -3.1% -3.6% 0.0%

Merchandise-trade surplus -13.4% -13.9% -14.4% -11.5% -9.2%

Growth rate:

Consumer prices (December) 17.4% 7.6% 6.4% 6.2% 5.5%

Exchange rate (December) 1.5% 1.6% 2.6% 24.8% 6.2%

Growth rate:

Population 3.2% 3.2% 3.2% 3.2% 3.2%

Population under fifteen 3.3% 3.3% 3.2% 3.3% 3.1%

* US$ million at 2015 prices and exchange rate.

** US$ at 2015 prices and exchange rate.

Data sources: International Financial Statistics, World Development Indicators, Tanzania Ministry of Finance.

Recent economic developments

The economic performance of the Tanzanian economy has followed a relatively strong and stable

pattern over the period under consideration. As reported in Table 1-1, real GDP has grown at an

annual average rate of 6.7 per cent over the period FY2011/12 – FY 2015/16. The growth of per-

capita real GDP has risen since FY201/12. International observers have noted that a combination

of stable performance in agriculture, as well as sustained improvements in sectors such as mining,

communications and financial services, is likely to underpin relatively high real growth rates over

the medium term.3 Reform efforts in areas such as taxation and governance may also contribute to

growth performance, even in the medium term.

GDP growth has been accompanied by strong growth in private consumption and investment, while

there was a slowdown in government consumption. The economic activities that have played a

major role in the growth rate include construction, services and basic manufacturing, as well as,

3 Tanzania has been categorized as a ‘stable grower’ whose economic growth has been based on economic reforms and

competitiveness improvements. (McKinsey&Company, 2016).

14

more recently, communications and transport. The agriculture sector remains crucial for Tanzania,

since it engages most of the labour force, however it has grown more slowly.

Constraints to growth include access to finance, issues in governance development, and problems

with infrastructure and public investment implementation4. Those are addressed in the second Five

Year Development Plan 2016/17 - 2020/21 (FYDP II) of Tanzania, launched in 2016. Under the

theme “Nurturing Industrialization for Economic Transformation and Human Development”, the

FYDP II continues the focus on growth and transformation from the first FYDP, and emphasises the

importance of addressing infrastructure gaps and job creation. Despite its emphasis on

industrialisation and economic restructuring, the FYDP II also incorporates an enhanced framework

for investment in human development and poverty reduction from the previous National Strategy for

Growth and Poverty Reduction (MKUKUTA II).5

Monetary policy has generally been steady and cautious. The slowdown in the depreciation path of

the local currency (Tanzanian Shilling, TZS) in 2016 is believed to result from a weaker United

States dollar (US$) and an improvement in domestic market expectations. However, some reversal

in the evolution of the local currency could occur if the current appreciation trend of the US$

continues. Borrowing costs remain high, with lending rates driven largely by liquidity requirements

of large firms and government institutions, although to some degree by the monetary authorities’

intervention.6

Tanzania’s external debt was significantly reduced in 2006/2007 by the Multilateral Debt Relief

Initiative, although since then it has grown as Tanzania has received new concessional credit. Over

the past decade, total public sector debt (including an estimation of arrears) has gradually

increased, reaching 37.5 percent of GDP in 2015/16. Currently, it is estimated that external public

debt amounts to around three-quarters of total public sector debt. Tanzania’s largest creditors are

the International Development Association (IDA) and the African Development Bank (AfDB),

accounting for more than two-thirds of its public external debt. A July 2016 IMF Debt Sustainability

Analysis argues that Tanzania continues to have a low risk of external debt distress, although the

relevant stress tests have pointed to some vulnerabilities related to exchange rate depreciation and

the lack of fiscal consolidation. In particular, the IMF’s recommendations to ensure debt

sustainability are: (i) to maintain a gradual increase in non-concessional borrowing; (ii) to

strengthen Tanzania’s debt management capacity; and (iii) to implement further public financial

reforms.7

Tanzania’s economy has also been affected by the overall reduction in financial-resource flows

from international donors to low income countries. The overall value of donor financing (external

grants and concessional loans) relative to total government expenditure has declined dramatically

over the past decade, dropping from 44 per cent in FY2004/05 to 19 per cent in FY2013/14. It is

estimated that it has decreased further to 14 percent in 2014/15. One reason for this development

is the overall decline in Official Development Assistance (ODA) due to political pressures in

development partners ‘own countries. Another is the halt in the provision of budget support in 2014,

due to allegations of mismanagement, as well as the delays in release of funds in 2016 due to

difficulties in meeting disbursement conditions. A new agreement on sector budget support from the

EU is currently being prepared, however such issues may continue to play a role. Among bilateral

donors, the largest contribution comes from the United States, with an average contribution of US$

4 World Bank Ease of Doing Business 2016, and IMF Art. IV Report 2017. 5 President’s Office Planning Commission, Supporting the preparation of Tanzania’s second five year development plan

(FYDP II) 2016/17-2021/22, May 2016. 6 Deloitte, Tanzania Economic Outlook 2016: The story behind the numbers. June 2016. 7 IMF, Tanzania Debt Sustainability Analysis. June 2016.

15

623 million in the fiscal year 2013/14 allocated mainly to education, infrastructure, health and

population issues.8

Current and future challenges and implications for the fiscal space

While Tanzania has made impressive progress in recent years in improving its fiscal position, it

continues to face a policy challenge, especially in light of the ambitious infrastructure spending it is

aiming at.9 On the one hand, Tanzanian revenue collection has recently been enhanced, and

should continue to improve, as a consequence of administrative reforms implemented as of

November 2015. A sharper focus on tax administration has led to significant gains, with tax

collection for January 2016 doubling as compared to the same period in 2015. For the fiscal year

2016/17 the Tanzania Revenue Authority has set a revenue collection target at 13.8 per cent of

GDP. Also, the government has made significant reductions in public expenditures, notably the

reduction of civil service overheads.

On the other hand, the government has accumulated large arrears with pensions funds and the

private sector (amounting to US$ 700 million and US$ 400 million respectively). 10,11 This increase

came about in part because revenue collection fell below government targets for FY 2013/14 and

2014/15. Moreover, the government has accumulated arrears with the national power companies.

The full amounts due to utility providers such as TANESCO and DAWASCO have not yet been

completely clarified.12 In order to be able to expand its expenditure on infrastructure, Tanzanian

policy-makers have concluded that they need to pursue a fiscal policy that targets a fiscal deficit of

3 percent of GDP.13 That level should permit them to limit net internal financing. In such a scenario,

Tanzanian policy makers would rely on external financing to help fund the government’s

infrastructure investment.

Another significant pressure on the fiscal space stems from the already mentioned outflow in donor

funding. External aid, including concessional loans, still provides more than 10 per cent of the

government budget and a disproportionate share of the financing for development and investment,

but given that the trend of declining ODA is highly likely to continue, the Government of Tanzania is

facing increasing pressures to substitute the respective funding. This is particularly relevant in light

of the various infrastructure-related goals of the FYDP II, including concrete objectives on improving

facilities and infrastructure in priority areas for children, where substantial parts of development

spending are currently donor-funded.

For the future, Tanzania’s main challenge in macro-fiscal terms stem from the interplay between

relative poverty and rapid population growth. As a result of those, the Tanzanian government

effectively faces a three-way set of policy imperatives. First, it must promote real growth, which is

ultimately Tanzania’s best hope of reducing poverty over the longer term. Second, it must invest in

human capital, dedicating the “right” amount of resources to addressing children’s welfare, in the

areas of education, health, social protection, nutrition, water and sanitation, and child protection.

With the share of children and young people projected to rise significantly over the coming period,

this will put significant pressure to maintain current levels of related spending. Thus, third, the

8 UN Economic Commission for Africa, Tanzania Country Profile 2015. March 2016. 9 World Bank, Why Should Tanzanians Pay Taxes? The Unavoidable Need to Finance Economic Development. July 2015. 10 In order to clear these arrears issuing bonds and injecting funds seem to be the most suitable options. See, also, World

Bank (2015) for further details. 11 The consultation during the PEA exercise with the country authorities has revealed that clearing the arrears became a

priority and some efforts in this area have already been done. 12 The consultation with TFNC revealed that they were not able to face some of their commitments with the utility providers

due to a shortage of finance that was expected to come from MoFP. 13 IMF, Tanzania Debt Sustainability Analysis. June 2015.

16

Tanzania Government must pursue the first two objectives while sustaining the government’s fiscal

balance.

The fact that so far Tanzania has been managing its fiscal accounts conservatively, and has

maintained a relatively high growth rate, can be interpreted positively in terms of future prospects. If

these circumstances continue, it should be possible for the authorities to maintain a sustained and

growing expenditure flow in the priority areas. Sustained growth should enable Tanzania to

maintain the fiscal space required to keep its priority expenditures for children growing in real terms

and to maintain pace with its rapidly growing population. This would be possible in particular

through maintaining a steady growth of tax revenue, which would be expected to be the mainstay of

the growth of priority expenditures for children. In this context, whatever serves to enhance revenue

performance would also help enhance the fiscal space: improved tax administration, diminishing

informality, and solid company profitability would all contribute to the fiscal space. For the medium

term, an additional source of fiscal space for Tanzania is its continuing access to concessional IDA

funds. Because IDA loans (and of course IDA grants) are highly concessional carrying no or low

interest rates, it makes sense to use them in social sectors such as education, health and social

protection.

Keeping in mind Tanzania’s plan to implement an ambitious infrastructure programme, which will

put pressure on the fiscal balance and is projected to lead to a fiscal deficit of 4.5 per cent for

FY2016/17, policy-makers aim to reduce the size of the informal sector. This would increase the

tax-revenue flow and open the way for formal financial operations to large segments of the

economically active population. However, the large proportion of the population who live in

extremely poor conditions may make it challenging to decrease informality.

Efficiency gains in current spending, in particular for investment, as well as clear prioritisation of

foreseen policies and projects, are another pathway to providing room to finance the increases in

infrastructure spending. Even in this case, Tanzania will likely continue to rely on funds provided by

the international community for some years to come. Thus, a conservative approach in which

priority expenditure is maintained seems to be a sensible ‘avenue’ to follow.

2.2 Tanzania’s priority expenditure and fiscal space in recent years

Over the years FY2011/12- 2014/15 Tanzania’s priority expenditure for children and the fiscal-

space flows evolved as shown in Table 2.2. It depicts the composition and the identity of Tanzania’s

priority expenditure, that is, expenditure relevant for children’s development and welfare, in terms of

percentages of GDP; as well as priority expenditures for children (based on the priority spending

categories defined at the beginning of the report) expressed as spending per child.

Table 2.2 Tanzania: Priority expenditure for children and its fiscal space FY 2011/12-2014/15

Fiscal year FY11/12 FY12/13 FY13/14 FY14/15

Per cent of GDP

Total priority expenditures for children 4.9% 5.2% 5.2% 5.2%

Total education expenditure14 3.57% 3.67% 3.45% 3.61%

Total health expenditure 1.15% 1.37% 1.49% 1.38%

14 Education expenditure shown here is equated to the budget of the Ministry of Education, and thus differs somewhat from

the total education expenditure at sector level.

17

Fiscal year FY11/12 FY12/13 FY13/14 FY14/15

Total social assistance expenditure15 0.14% 0.16% 0.19% 0.22%

Total nutrition expenditure 0.02% 0.02% 0.03% 0.03%

Total child protection expenditure16 0.01% 0.01% 0.01% 0.01%

Overall fiscal space 4.9% 5.2% 5.2% 5.2%

Tax and non-tax revenue (excl. external grants) (+) 12.5% 12.8% 13.4% 12.8%

External grants (+) 3.1% 2.6% 2.1% 1.1%

Total non-priority non-interest expenditure (-) -11.8% -11.2% -9.0% -9.1%

External-debt disbursements (+) 2.8% 2.9% 2.4% 2.6%

External debt service (-) -0.3% -0.5% -0.5% -0.7%

Net internal financial flows (incl. internal interest) (+) -1.4% -1.4% -3.2% -1.6%

Growth rates (US$ per child)

Total priority non-interest expenditure: 10.24% 2.29% 5.14%

Contribution to the growth of total priority expenditure:

Tax and non-tax revenue (excl. external grants) (+) 21.59% -2.27% 24.7%

External grants (+) -7.89% -18.47% 0.9%

Total non-priority non-interest expenditure (-) 34.79% -7.10% -9.0%

External-debt disbursements (+) -8.35% 6.96% -25.2%

External debt service (-) -1.06% -4.25% -11.7%

Net internal financial flows (incl. internal interest) (+) -36.80% 30.27% 30.9%

Data source: Tanzania Ministry of Finance, International Financial Statistics.

Over the observed years, the structure of priority expenditures for children has remained relatively

steady as a percentage of GDP, ranging between 4.9 and 5.2 per cent, while increases in the

various expenditure categories have been marginal (Table 2). The fiscal-space analysis shows

broadly how the flows of priority expenditures for children have been funded. In the structure set out

in Section 2.1 above, tax and non-tax revenue, external grants, external-debt disbursements, and

the net internal debt flow including internal interest contribute positively to the fiscal space that

funds priority expenditures for children, while non-priority expenditure and external debt service

contribute negatively to the fiscal space for priority expenditures for children.17 From the historical

analysis, the following can be noted:

Tax and non-tax revenue has been stable at around 12.5 per cent of GDP for all years apart

from FY2013/14, when it demonstrates a one-off increase up to 13.5 per cent of GDP, before

diminishing again to its FY2013/14 level. The authorities intend to improve revenue

15 Due to data availability, social assistance spending has been equated to spending on the Productive Social Safety Net

(PSSN) program under the Tanzania Social Action Fund (TASAF). PSSN spending amounts to 90 per cent of social

protection spending. Other programmes under TASAF include a complementary public works program, as well as

interventions to support livelihoods enhancement and targeted infrastructure. Spending on social assistance as used in

this report and the underlying modelling framework does not include spending on other social assistance programs,

including those specifically targeting children such as the Most Vulnerable Children (MVC) program and school feeding

programs under the Ministry of Social Welfare. No historical data on spending on those programmes could be obtained.

Social assistance as included in the model also excludes contributory spending on social insurance measures. 16 Child protection expenditure, for the purposes of this analysis, is estimated to equal 0.3 per cent of the budgets of the

ministries of Constitutional and Legal Affairs, Education, Health and Social Welfare, and Home Affairs (Police and Prison).

This estimate is based on data that shows spending on nutrition to be of a similar magnitude. The estimate also takes into

account findings from a 2011 Public Expenditure Identification Survey that estimated child protection spending at the

district level to be 0.2 per cent of total allocation at the district level. 17 Note that internal interest payments contribute negatively to the fiscal space. It may help to note that while, for example,

infrastructure expenditure is non-priority expenditure and so contributes negatively to the fiscal space, an external

disbursement that funds it would contribute positively to the fiscal space, and at least partially offset the effect of the

infrastructure expenditure.

18

performance principally through improved tax administration, increased formalization, and

maintenance of high real growth;

External grants declined markedly as a percentage of GDP, from 3.1 per cent of GDP in

FY2011/12 to 1.1 per cent in FY2-14/15, which is consistent with the decline in the ODA that is

provided through the government budget. This is the consequence of political pressures in

donor countries, but also of the difficulty in meeting disbursement conditions;

Non-priority non-interest expenditure also declined some as a percentage of GDP, from

11.8 per cent of GDP in FY2011/12 to 9.1 per cent in FY2014/15. This is partly the

consequence of strong policy efforts by the fiscal authorities to carry out significant reductions in

overhead expenditure. This decline had the effect of opening fiscal space for priority

expenditure;

External-debt disbursements remained relatively steady averaging 2.7 per cent of GDP.

External-debt service was also relatively stable, remaining below 1 per cent although drifting

upward over the period;

Finally, net internal-debt flows taking account of interest due were almost constant (apart from a

sharp jump to 3.2 per cent in FY2013/14) although the overall flow is negative because of the

interest bill. This is evidence of the conservative management of the fiscal accounts.

The historical performance of the fiscal space components demonstrates that despite pressures

stemming from decreases in external grans, the Government of Tanzania has been able not only to

maintain, but even to increase spending on the priority expenditure categories. The second part of

Table 2.2 shows that when expressed in $US at 2015 prices, total priority expenditure growth

averaged 5.9 per cent over the period, with the highest year on year increase of 10.4 per cent being

recorded between per cent between FY2011/12 and FY 2012/13. This growth is also evident when

considering that total real expenditure over the number of children aged 15 or less has increased

from $US 78.24 in FY2011/12 to $US 92.75 in FY2014/2015 (Table 2.3). A combination of savings

in non-priority expenditure, and a stable (though not necessarily improving) tax and non-tax

revenue performance has supported this development. A contribution analysis shows that the 0.6

per cent of GDP increase in tax and non-tax revenue receipts in FY2013/14 funded a quarter of the

increase in total priority spending observed over the following year. This demonstrates that the

Government of Tanzania has maintained a strong commitment to funding policies and programmes

affecting child well-being.

Table 2.3 Per child spending in priority expenditure categories18 US$

US$ per child at prices and exchange rate of 2015 FY11/12 FY12/13 FY13/14 FY14/15

Total priority expenditures for children $78.24 $86.25 $88.22 $92.75

Total education expenditure $57.07 $60.44 $58.94 $63.81

Total health expenditure $18.48 $22.59 $25.44 $24.34

Total social assistance expenditure $2.21 $2.64 $3.23 $3.97

Total nutrition expenditure $0.29 $0.41 $0.44 $0.47

Total child protection expenditure $0.18 $0.16 $0.17 $0.17

2.2.1 Current and future challenges and implications for the fiscal space in the priority sectors

Table 2.4 shows again the composition of priority expenditures for children, not expressed in

percentage of GDP but as percentage of total priority expenditures for children. The expenditure

18 As highlighted in the methodological introduction to this report, the herewith constructed measure of per child priority

expenditure should be interpreted with care, as it is based on total institutional spending in priority areas, which may

include expenditures that are not at all, or only loosely related to children.

19

categories here are defined institutionally.19 The budget data are for the general government,

comprising the central and the subnational government levels.

Table 2.4 Priority expenditure for children, relative shares of total, FY 2012/13 – FY 2014/15

Fiscal year: FY12/13 FY13/14 FY14/15

Per cent of total priority expenditure:

Total priority non-interest expenditure: 100.00% 100.00% 100.00%

Total education expenditure 70.08% 66.81% 68.79%

Total health expenditure 26.19% 28.84% 26.24%

Total social assistance expenditure 3.06% 3.66% 4.28%

Total nutrition expenditure 0.47% 0.50% 0.50%

Total child protection expenditure 0.19% 0.19% 0.18%

As evident, education constitutes the bulk of spending on priority categories (ca. 66-70 per cent),

followed by health (ca. 26-29 per cent). Furthermore, the relative shares of the various categories in

the total priority expenditure for children appear to be remarkably stable over the period. The only

exception is expenditure on social assistance, which is equated to spending on PSSN in this

analysis, and which increases somewhat.

Education and health spending together amounts to over 90 per cent of total priority spending. As a

share of the total budget, over the period FY2011/12 – FY2014/15, the Government of Tanzania

has spent on average around 16 per cent on education, and around 7.7 per cent on health.

Importantly, allocations to both sectors have grown significantly in nominal terms over the examined

period, both in terms of budgeted and actual amounts.

Education

Current priorities in the area of education are defined in the recent FYDP II, which sets out to

address in particular issues related to improving teacher-pupil ratios, since there is a strong need to

further increase staff numbers at primary and secondary level. In budgetary terms, this objective

implies the need for a significant increase in recurrent spending, which amounted to around 86 per

cent of total education spending in FY2014/15. At the same time, further objectives in education

pertain to improving the quality of educational facilities and related infrastructure, which will in turn

put pressure on development spending in the education area. In terms of funding sources,

education spending has been affected by the decline in foreign assistance, especially for the

development part of the budget, however the Government of Tanzania has responded by

increasing domestic resource allocation in this area (Figure 2.1). Finally, budget execution rates in

education still leave room for improvement, especially for the development part of the budget, and

there is a trend of growing disparities at sub-national level. Addressing stated objectives in

education for both the recurrent and development part will thus put significant pressure on the fiscal

space, which could be further exacerbated by the limitations in absorption capacity and the outflow

of donor funding.

19 Thus, for example, any expenditure by the armed forces on education of children of staff is classified as defence

expenditure rather than education expenditure.

20

Figure 2.1 Funding sources of education sector expenditure, FY2011/12 – FY2014/15

Source: UNICEF based on MoFP IFMS data.

Health

The FYDP II states a number of objectives in the area of health. Many of those aim at addressing

issues related to quality of health systems, equipment and training. The FYDP II also reiterates the

emphasis on preventive health care, which is a key priority from a child-friendly perspective. In fact,

spending on preventive services has already outpaced spending on curative services in 2014/15

(Figure 2.2). In nominal terms, allocations and spending on health have continuously increased

over the period FY2011/12 – FY2014/15, and this has also led to a real increase in the per child

expenditure in the health sector20 from $ US18.48 to $US 24.34 between FY2011/12 and

FY2014/15. As in the education sector, the outflow of donor funding poses an important challenge

for achieving the stated objectives in health and bears implications for the fiscal space, as it implies

the need to free up additional resources. In areas where the reductions in donor support have been

particularly high, such as drugs and medical supplies, there have been significant increases in the

own government contributions, e.g. a threefold increase in the funding of medicines for preventive

services, but previous levels are yet to be matched. Taken as whole, budget execution in health is

strong (Figure 2. 3), averaging 88 per cent over the period FY2011/12-FY2014/15. Nevertheless,

the trend is a declining one, and there are substantial geographical variations.

Figure 2.2 Health education spending FY2014/15, % of total government spending

Figure 2.3 Allocated vs. actual spending in health, FY2011/12-FY2014/15

Source: UNCIEF based on MoH data.

Social assistance21

Despite the impressive and continuous economic growth experienced by Tanzania for over a

decade, poverty levels in the country are still very high. According to a 2012 national survey, 28.2

20 Estimated as total spending in the health sector over the number of children aged 15 or less. 21 For the purposes of this analysis, due to data availability, social protection is equalled to TASAF expenditure on the PSSN

programme. Therefore the term “social assistance” is used as the PSSN is a social assistance cash transfer programme to

the most vulnerable.

0

5

10

15

20

25

30

FY 2011/12 FY 2012/13 FY 2013/14 FY 2014/15

Bil

lio

ns

Sh

illi

ng

s (

at

2013

-2014 p

rices)

Recurrent(PE)

Recurrent(OC)

Developmentforeign

Developmentlocal

21

per cent of the population were found to live under the national poverty line22. The World Bank

estimated that in absolute terms, the number of Tanzanians who live below the national poverty line

has not changed since 2001, and is still about 12 million. If a different poverty line of US$ 1.25

(2005 PPP) a day is considered, then 43.5 per cent of the population would be considered income

poor23. The combination of staggering poverty prevalence and strong population growth bears

enormous challenges for the future in terms of ensuring the well-being of a significant part of the

Tanzanian population.

Social Protection is mentioned in the FYDP II as part of the larger agenda to reduce poverty by

addressing social and economic risks, deprivation and vulnerability; protecting human rights and

improving capabilities and labour market results. The flagship project in the field of social protection

is the Tanzania Social Action Fund (TASAF) which was initiated in 2000. Under the current third

(TASAF III), a key intervention is the PSSN (Productive Social Safety Net), which is a nation-wide

conditional cash transfer programme. While a means-tested cash benefit is provided under PSSN,

TSAAF III emphasis lies on enabling productivity and participation in income-generating activities.

Therefore, it is complemented by a public works, livelihoods enhancement and infrastructure

interventions.

Tanzania has recently scaled up the PSSN to target more extreme poor across the country and in

addition, there have been moves to finalise a national social protection framework. However, while

overall TASAF III expenditure has been mainly donor-funded (World Bank, DIFD, SIDA), the recent

scale up has put more pressure on the Government to add own resources. Allocated amounts have

indeed increase substantially, however this has not necessarily resulted in higher actual spending.

In FY2015/16, US$7 million was allocated in the government budget for the entire TASAF III

project, with PSSN comprising roughly 90 per cent of this. However, only US$300,000 were

released. For the fiscal year 2016/2017 the Government allocated additional US$7 million but in

2013, at the beginning of the scale up, the government had committed to provide US$ 100 million

per year. The existing financial support by the government is not enough to sustain the program

beyond early 2018.

Nutrition and child protection

Nutrition and child protection are key focus areas of UNICEF’s engagement in Tanzania. UNICEF

works here in strong partnership with the government in policy development and implementation

and has supported the development of new National Action Plans have been developed in both

sectors. For nutrition this is the National Multi-sectoral Nutrition Action Plan (NMNAP) 2016-2021

while for Child protection this is the National Plan of Action to End Violence against Women and

Children (NPA-VAWC) 2017- 2021.

The NMNAP seeks to scale up of evidence-based multisectoral nutrition specific and nutrition

sensitive interventions to all segments of the population and providing a conducive enabling

environment. The overall financial requirement for the NMNAP is about TZS 590 billion (US$ 268

million) of which TZS 254 billion (US$ 115 million) is to be provided by the government of Tanzania.

In addition, the Government of Tanzania is committed to continue24:

Strengthening capacities of regional and district nutrition officers in planning, budgeting and

coordination of nutrition activities;

22 Ulriksen, M. (2016) The development of social protection policies in Tanzania, 2000-2015, CSSR Working Paper No. 337. 23 World Bank (2015), United Republic of Tanzania: Tanzania Mainland Poverty Assessment. Washington DC: World Bank. 24 Mpango, P. Human Capital Summit: Investing in the Early Years for Growth and Productivity. Speech by Tanzania Minister

of Finance and Planning, Honourable Minister Philip Mpango.

22

Strengthening multi-sectoral coordination and accountability to national nutrition commitments

through annual review of Common, Results, Resources and Accountability Framework for

nutrition and roll out of multi-sectoral nutrition scorecard at decentralized level.

Nutrition is a cross-institutional sector, and thus spending on nutrition-related activities comprises

expenditure under, among others, education, health, agriculture, water and sanitation and other

areas. Importantly, allocations to fund nutrition-specific activities have been rising, and actual

spending has more than doubled in the period FY201-/11-FY2014/15. Nevertheless, nutrition-

related spending comprises only 0.03 per cent of GDP and 0.13 per cent of total public spending

(Figure 2.4). In addition, a significant proportion of the resources in nutrition are donor-funded,

which raises questions about the sustainability of spending. Another issue is the gap between

allocated and actual expenditure for the realisation of the NMNAP, with the latter reaching less than

a quarter of the originally budgeted amounts for the FY 2011/12 and FY2012/13 according to MoF

data. Finally, from a budgetary perspective, a significant challenge is related to devolved spending.

Differences between allocated and released funds appear to be significant for sub-national level as

well. What is more, there are issues with prioritisation of nutrition spending at that level.

Figure 2.4 Nutrition and child protection spending (actual), FY 2011/12-FY2014/15, % of GDP

Source: UNCIEF based on MoF data.

As for child protection, the NPA-VAWC has been developed by consolidating eight different action

plans addressing violence against women and children to create a single comprehensive, National

Plan of Action. Linking to the FYDP II the NPA-VAWC recognizes that investing in violence

prevention initiatives has a positive impact on inclusive growth and creating human capital.

However, as evident from Figure 2.4, spending on child protection related activities is very small

(0.01 per cent of GDP). UNICEF estimates the funding gap for the realization of the objectives and

activities of the NPA-VAWC to be more than 60 per cent25.

25 UNICEF (2016), Child protection factsheet.

0

0.005

0.01

0.015

0.02

0.025

0.03

FY11-12 FY12-13 FY13-14 FY14-15

% o

f G

DP Total nutrition

expenditure

Total childprotectionexpenditure

23

3 Tanzania’s options for enhancing the fiscal space

The first part of this chapter discusses a multiannual projection in Excel of Tanzania’s fiscal space

under a set of “base-scenario” assumptions. (Appendix 1 describes the base-scenario assumptions

in detail.) The second and third part describes alternative scenarios and the consequences of the

options they embody on the fiscal space, as determined quantitatively by the projection exercise.

While each option takes account of Tanzania’s specific circumstances, it is important to remember

that the projection results are based on specified, quantitative programming assumptions. In no

case should the results be regarded as forecasts. Also important to keep in mind is the fact that the

“priority expenditure per child” measure is calculated on the basis of projected total expenditure at

institutional level (including such spending that is not directly child-related), divided by population

projections for the number of children aged 15 or less. The final part of the section discusses some

options that are less feasible in Tanzania’s present circumstances, but have figured in other many

governments’ fiscal-reform approaches.

3.1.1 Base scenario and fiscal space “mapping”

In its presentation of the base scenario, Appendix 1 describes its programming assumptions and

characterizes the projection results. The real-GDP annual growth rate is assumed to average 7 per

cent over the projection period in keeping with recent IMF projections. Most of the remaining

programming assumptions are intended as “neutral”, non-controversial, base-line assumptions that

would produce no significant changes in the fiscal structure as the real economy grows. The results

of the base scenario provide a basis for comparison with alternative scenarios incorporating

different assumptions.

Under the base scenario, priority expenditures in categories relevant for children would average 6.3

per cent of GDP over the years FY2016/17-2020/21. Over these same years, in real terms, total

priority expenditures for children would average US$144.87 per child at FY2015/16 prices and

exchange rate. Under the base-scenario assumptions regarding tax and non-tax revenue, external

grants, non-priority expenditure, and external- and internal-debt stocks and flows, the projected

flows of priority expenditures for children would produce a fiscal-space financing “gap” that would

have to be covered with internal financing. For the specific quantitative assumptions, the required

internal-financing flow would average 3.2 per cent of GDP over the projection years. The implied

fiscal deficit would average 3.9 per cent of GDP, on the order of the deficit outturns for FY13/14 and

FY14/15.

Figure 3.1 shows a fiscal-mapping chart for FY2011/12-2019/20, with projections according to the

base scenario. The projections are set out as percentages of GDP26. In the “stacked-bar”

presentation, funding sources are above and expenditure flows below the horizontal axis: in effect,

the sum of everything above the horizontal axis effectively funds everything below. For each year,

the sum of all flows above the horizontal axis is precisely equal to the sum of all flows below the

horizontal axis. Stated differently, the tax and non-tax revenue, the external grants, and external-

debt disbursements, shown above the horizontal axis, together fund the priority expenditure, the

non-interest non-priority expenditure, the external-debt service, and the (negative) internal financing

26 In the Excel file, it is straightforward to select alternative units of account, such as U.S. dollars, U.S. dollars at base-year

prices and exchange rate, or U.S. dollars at base-year prices and exchange rate per child.

24

flow including internal interest. The net internal financing flows include the interest on the internal

debt.

Figure 3.1 Fiscal space and its components over the historical and projection period in the base

scenario (FY2011/12-FY2019/20)

Source: TzFS.xls model calculations based on Government of Tanzania, UNICEF and IFS data.

The projection exercise can be used to evaluate different policy approaches involving priority

expenditure and its fiscal space. In general, if a scenario is proposed that involves an increase in

the priority-expenditure flow relative to what is in the base scenario, the “fiscal gap” would

presumably increase. The exercise would show an increase in the net internal financing flow to the

government compared with the base scenario. On the other hand, if a scenario is proposed

involving an enhancement through one or more elements of the fiscal space, the exercise would

show a reduction in the net internal financing flow to the government compared with the base

scenario. Naturally, combined scenarios are possible, in which both the priority-expenditure and the

fiscal-space flows are increased. The idea would be to determine the net consequence of the two

changes. The exercise shows the multiannual internal financing flows for the whole projection

period, and accumulates these flows so that the exercise shows the government’s total debt at the

end of the projection period.

Since these results are quantitative, they can be discussed in terms of their feasibility: Would the

net internal financing flow be likely to exceed the capacity of internal financial markets?, and would

the government’s total debt stock rise too high too quickly as a percentage of GDP?

In principle, policy-makers could be asked to consider enhancements to the fiscal space for priority

expenditure by considering the following options: (1) increasing tax and non-tax revenue; (2)

increasing external grants for budget support and projects; (3) reducing non-priority expenditures;

(4) reducing external debt service through agreements with creditors; (5) increasing external debt

disbursements; and (6) increasing net internal borrowing flows. In general, evaluation of the

alternative-scenario results suggests that the best policy approaches to securing sustained

increases in the fiscal space and so in the priority-expenditure flows appear to lie with improved tax

administration. As explained below, the other approaches are likely, in the base of tax increases

and reducing non-priority expenditure, to face political obstacles and may be counterproductive in

the medium term, since they might reduce the GDP growth that powers the revenue flows. Debt

funding for priority expenditure is inherently undesirable, because the cost of the debt is likely to

25

exceed the return on priority expenditure, at least until the long term. Finally, agreed reductions in

external-debt service are unlikely to be feasible – the international debt-reduction programs of the

1990s and 2000s are unlikely to be repeated in coming years.

Of course, other pathways to achieving improvements in the fiscal space are possible as well, most

notably in terms of improving allocative and cost-efficiency in the priority expenditure categories. In

all priority categories, achievement of development targets and objectives falls short of the original

aims. Some examples include the continued prevalence of stunting among Tanzanian children

younger than 5, high neonatal mortality, or access to pre-primary education. It is plausible to

assume that significant resources could be freed up through improving decision-making and

management through the continuous use and analysis of performance information, monitoring and

evaluation in conjunction with budgetary allocation information.

3.1.2 Option to increase fiscal space: increasing tax and non tax-revenue (Scenario 1-3)

Broadly speaking, Tanzania appears to possess potential to enhance its revenue flow by increasing

the efficiency of tax collection, broadening the tax base, and changing the cultural perception

towards taxation. Non-tax revenue might also be increased by increased efficiency in the

performance of State-Owned Enterprises. A possible future source for tax- as well as non-tax

revenue could be the extraction and selling of natural gas. It is unlikely, however, that overall tax-

rate increases will prove possible in the present political context, and might, in any case,

discourage economic activity. In 2016 the government of Tanzania in its pursuit of increasing

income has decided to go ahead with the introduction of an 18% VAT to all tourism activities that

were earlier exempt, including park entry fees. Critics warn that Tanzania will become prohibitively

expensive compared with rival destinations and point to Kenya which learned a hard lesson in 2015

when it imposed VAT on tourist services.

Despite expectations of growing tax revenue if the current high GDP growth is maintained and the

credibility in the system improves, Tanzania will also need to make a determined effort to narrow

the gap between potential and actual revenue collection under existing rules. IMF calculations

suggest that the revenue gap is now around 4 percentage points of GDP.27 The actual tax revenue

collection for 2014/15 amounted to 88 percent of the government’s target (TZS 9,892 billion versus

TZS 11,297 billion). However, there is some agreement that revenue collection targets set by GoT

are rather ambitious, and thus mask the impressive growth of actual revenue collection. In 2014/15,

revenue grew 6.4 per cent in nominal terms with respect to 2013/14. As reported by Lee et al.

(2015), the 88-per-cent collection rate was the lowest registered in the last 10 years - performance

had previously reached at least 90 per cent of the target.

To improve collection performance and reduce evasion, the Government of Tanzania has begun to

promote the use of Electronic Fiscal Device machines by the Tanzania Revenue Authority to

traders, regardless of whether they charge VAT on their transactions. Their use should improve

collection efficiency through automatic issuance of receipts, storage of sales transactions on

computer networks, as well as the generation of unique signatures.

Several initiatives to improve tax performance are now under consideration. During the mission,

policy-makers mentioned the possibility of reducing the current general VAT rate from 18 per cent

to 16 per cent. In itself, this reduction would reduce the revenue flow, but might encourage

compliance.

27 IMF, Tanzania selected issues paper, July 2016.

26

Although several changes in the existing body of legislation have been implemented since 2014,

such as a new VAT Act, policy-makers believe further efforts to enhance the relevant tax bases are

required. Options include a reduction in the list of exemptions, adopting recommended “best

practices” in the design of the taxation system, and simplification of administrative procedures.

An additional challenge for Tanzania’s revenue authorities is the huge size of the informal sector. It

is estimated that only 2.3 million workers, 12 per cent of the total labour force, work in the formal

sector. Increased formalization would increase the tax base (as well as open opportunities to

citizens to use financial services to save and to secure credit on reasonable terms).

Overall, further tax policy and administration reforms will be required to close the revenue gap

efficiently without compromising economic growth, while public financial management, governance,

and more broadly, government effectiveness also needs to be improved. An improved cultural

perception of taxation would also help. There have been proposals for a “social pact” between the

government and business organizations, among other purposes, to help promote tax compliance.

There may also be some scope for increasing non-tax revenue by improving the performance of

state-owned enterprises. In 2011 there were 283 state-owned enterprises, many of which have

been underperforming on both service delivery and profitability. Although enterprises are likely to

reinvest resources secured through higher profitability,28 it would also open the way to higher

taxation and at least some dividend income for the government.

An eventual potential source of fiscal-space enhancement is revenue from natural gas. The recent

discovery of additional natural gas reserves has raised expectations. However, private investors as

well as policy-makers have been cautious regarding the stream of revenue that could eventually be

obtained since sustained low oil prices affect investment decisions to exploit natural-gas deposits

(LNG contracts are indexed to oil prices). It is believed that extraction in Tanzania would be cost-

effective as long as world gas prices do not fall below US$ 10-12/mm BTU,29 but, even so, there

would have to be solid prospects of sustained high prices to persuade firms to undertake the

investment.

The first of the “alternative” scenarios, Scenario 1 suggests that a realistic improvement in the

VAT tax administration could bring about some reduction in the fiscal-space gap. The assumptions

of Scenario 1 are the same as those of the base scenario, except that in Scenario 1 the collection

efficiency of domestic and import VAT would gradually increase from 12.7 to 15.2 per cent and 28.2

to 33.8 respectively (a 20-per-cent improvement in both instances). The projection exercise

suggests that this would lead to a 0.4 percentage-points increase in the average tax revenue to

GDP over the projection period, reduce the net internal debt flow to GDP by 0.5 percentage-points,

and reduce the end-FY2020 government debt stock to 29.7 per cent of GDP from 31.72 per cent of

the base scenario. While, as mentioned, this suggests some reduction of the fiscal space gap, the

question is whether this would be sufficient to offset fiscal pressures through increased spending on

priority categories.

Box A Enhanced VAT administration

Results Scenario 0 Scenario 1 Variation

Average tax revenue/GDP, FY2016-2020 13,10 13,48 0,38

Average priority expenditure/GDP, FY2016-2020 6,27 6,27 0,00

28 OECD, CEOs roundtable dinner comments by Zitto Kabwe. October 2011. 29 World Bank, Why Should Tanzanians Pay Taxes? The Unavoidable Need to Finance Economic Development. July 2015

Roe, A. Tanzania: From mining to oil and gas. United Nations University. June 2016.

27

Results Scenario 0 Scenario 1 Variation

Average priority expenditure per child (USD at 2016 prices and

exchange rate), FY2016-2020 $ 144,87 $ 144,87 $ -

Net internal debt flow/GDP, FY2016-2020 3,21 2,67 -0,54

Total government debt/GDP, 2020 31,72 29,25 -2,47

Scenario 2 considers an increase of priority expenditure compared with the base scenario: the

elasticities of staff in the education and child-protection sectors with respect to the child population,

and the elasticities of all other priority sectors with respect to the overall population would rise to 1.3

for the entire projection period.( This means, for example, that each per cent increase in the child

population would lead to a 1.3-per cent increase, rather than a 1 per cent increase, in the education

staff.) This change would require an increase in the fiscal-space gap. With this change, total real

per-child priority expenditure would average US$150.53 over the projection period, an increase of

$5.66 compared to the base scenario. The net internal debt flow would have to rise to 3.55 per cent

of GDP, compared with 3.2 per cent of GDP in the base scenario. Total government debt would

conclude 2020 at 33.3 per cent of GDP, compared with 31.7 per cent of GDP in the base scenario.

BOX B Increased priority expenditure

Results Scenario 0 Scenario 2 Variation

Average tax revenue/GDP, FY2016-2020 13,1 13,1 0,00

Average priority expenditure/GDP, FY2016-2020 6,27 6,51 0,24

Average priority expenditure per child (USD at 2016 prices and

exchange rate), FY2016-2020 $ 144,87 $ 150,53 $5,66

Net internal debt flow/GDP, FY2016-2020 3,21 3,55 0,34

Total government debt/GDP, 2020 31,72 33,26 1,53

Scenario 3 combines the first two scenarios to set up an increase in priority expenditure funded by

improved tax collection efficiency. With the specific figures assumed, total real per-child priority

expenditure would (again) average US$150.53 over the projection period, thus 5.6 US$ more than

in the base scenario. The net internal debt flow would be 3.0 per cent of GDP, less than the 3.2 per

cent of GDP in the base scenario. Total government debt would conclude 2020 at 30.78 per cent of

GDP, compared with 31.73 per cent of GDP in the base scenario.

BOX C Enhanced VAT administration and increase priority expenditure

Results Scenario 0 Scenario 3 Variation

Average tax revenue/GDP, FY2016-2020 13,10 13,48 0,38

Average priority expenditure/GDP, FY2016-2020 6,27 6,51 0,24

Average priority expenditure per child (USD at 2016 prices and

exchange rate), FY2016-2020 $ 144,87 $ 150,53 $5,66

Net internal debt flow/GDP, FY2016-2020 3,21 3,00 -0,21

Total government debt/GDP, 2020 31,72 30,78 -0,94

As a conclusion, the scenarios examined in this section clearly reveal that a realistic improvement

in VAT administration could successfully be used to fund additional expenditure on children. Given

the objectives in the FYDP II aiming at improving staff levels in education, the existing shortages in

health personnel, as well as further needs to scale up personnel e.g. in relation to social welfare

officers and specialized police units that are sensitized on children’s issues, increases in priority

recurrent and in particular personnel costs expenditure are likely. At the same time, there are signs

that the Government of Tanzania is taking decisive steps towards improving VAT administration.

What is more, only recently an increase in VAT levied on tourism services has been announced.

28

This will probably result in additional revenue windfall. As evident from Scenario 3, under the

concrete assumptions outlined above, the revenue increase from revenue administration

improvements alone would be sufficient not only to fund the increase in priority expenditure, but

also to further reduce the fiscal space gap as compared to the base scenario. If additional revenue

collection can be realised, this is a strong signal that envisaged child-friendly policies are

affordable.

3.1.3 Other scenarios (4 and 5)

Scenario 4 considers the consequences of lower real-GDP growth for the projection. Lower real-

GDP growth would reduce real tax-revenue flows, because the revenue flows positively related to

GDP. In Scenario 4 (Box D), real-GDP growth is assumed to average 6.5 per cent of GDP over the

projection period, as compared to 6.9 average GDP growth in the base scenario. This scenario is

based on recent IMF assessment that points to the potential risks of weaker economic activity due

to the slow growth of private sector credit, further accumulation of arrears, as well as possible

adverse effects from an eventual slowdown in Europe and China30.

Under the assumption of slower economic growth, total real per-child priority expenditure would

(again) average US$144 over the projection period, which is the corresponding figure in the base

scenario. Economic slowdown to the extent assumed in the scenario would not have any further

impact on the average priority expenditure per child, and would increase the fiscal space gap only

marginally. However, in the same scenario, but under the assumption of average GDP growth of

only 4 per cent over the projection period, the fiscal space gap would be significantly larger.

Namely, lower GDP growth would result in 0.3 per cent of GDP increase in the net internal debt

flow, and in almost 3 per cent of GDP increase in total government debt. At the same time, priority

expenditure on children would fall with almost 2 US$ over the projection period. This underlines the

importance of strong GDP growth in view of maintaining and possibly increasing priority

expenditure on children.

BOX D Lower real GDP growth (6.5 percent over the period)

Results Scenario 0 Scenario

4

Variation

Average tax revenue/GDP, FY2016-2020 13,10 13,09 -0,01

Average priority expenditure/GDP, FY2016-2020 6,27 6,30 0,03

Average priority expenditure per child (USD at 2016 prices and

exchange rate), FY2016-2020 $ 144,87 $ 144,30 -$ 0.57

Net internal debt flow/GDP, FY2016-2020 3,21 3,29 0,08

Total government debt/GDP, 2020 31,72 32,51 0,78

Although in simple arithmetic terms reductions in non-priority expenditure would be a source of

enhanced fiscal space for priority expenditures for children, matters are not so straightforward. In

the recent years, inadequate financial resources have forced Tanzanian policy-makers to reduce

public expenditure and postpone investment plans. This inevitably affected Tanzania’s real growth.

Since revenue depends directly and indirectly on GDP, lower real growth reduced the revenue flow

from what it would otherwise have been, and so reduced the fiscal space.

Indeed, for 2015/2016, the government has prioritized strategic infrastructure projects such as: (I)

development of an integrated land management information system; (ii) strengthening and

30 IMF Country Report No. 17/13, January 2017.

29

improving working tools and services for the central railway; (iv) construction of phase III of the

National Optic Fibre; and (v) extension of Julius Nyerere International Airport.31 These projects can

be expected to maintain or enhance real-GDP growth for the medium term. This is one reason why

policy-makers would probably prefer not to finance priority expenditure by reducing non-priority

expenditure.

Scenario 5 considers the consequence of a specific kind of reduction in non-priority expenditure. In

the base scenario, the real growth rate of current non-priority expenditure on goods and services is