national resources tax conference - greenwoods · this observation applies equally to the...

TRANSCRIPT

© Tim Kyle 2016

Disclaimer: The material and opinions in this paper are those of the author and not those of The Tax Institute. The Tax Institute did not review the contents of this paper and does not have any view as to its accuracy. The material and opinions in the paper should not be used or treated as professional advice and readers should rely on their own enquiries in making any decisions concerning their own interests. 510763622

National Resources Tax

Conference 26 – 28 October 2016

Session 3: The Legal Meaning of

“Market Value”

Written by:

Tim Kyle

Director

Greenwoods & Herbert Smith Freehills

Presented by:

Tim Kyle

Director

Greenwoods & Herbert Smith Freehills

WA Division

26-28 October 2016

Crown Perth

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 2

CONTENTS

1 Introduction .................................................................................................................................... 5

2 The roles that market value plays in the Tax Acts ..................................................................... 7

2.1.1 Determining tax attributes .................................................................................................. 7

2.1.2 Allocating consideration among multiple assets ................................................................ 8

2.1.3 Imposing a different character for Tax Act purposes ......................................................... 9

2.1.4 Determining access to particular provisions .................................................................... 10

3 The assumptions underpinning market value .......................................................................... 11

3.1.1 The market value of every “thing” can be determined ..................................................... 11

3.1.2 Market value is a single identifiable number ................................................................... 12

3.1.3 Market value can be divined in a rational way ................................................................. 13

3.2 Growing legislative awareness that market value is not a panacea ....................................... 13

4 The proper process for determining market value ................................................................... 15

4.1 The Tax Act market value definition ....................................................................................... 15

4.2 The specific Tax Act market value rules ................................................................................. 17

4.3 ATO administrative safe harbours .......................................................................................... 19

4.4 Where no specific Tax Act rule applies ................................................................................... 19

5 The general law meaning of market value ................................................................................. 20

5.1 Overview ................................................................................................................................. 20

5.2 Market value cases in different contexts ................................................................................. 20

5.3 Spencer’s case ....................................................................................................................... 21

5.4 Practical challenges in applying the Spencer test .................................................................. 23

5.4.1 Overview .......................................................................................................................... 23

5.4.2 How do Courts approach the Spencer market value test? .............................................. 23

5.4.3 MMAL Rentals ................................................................................................................. 24

5.5 Legislative context is critical ................................................................................................... 25

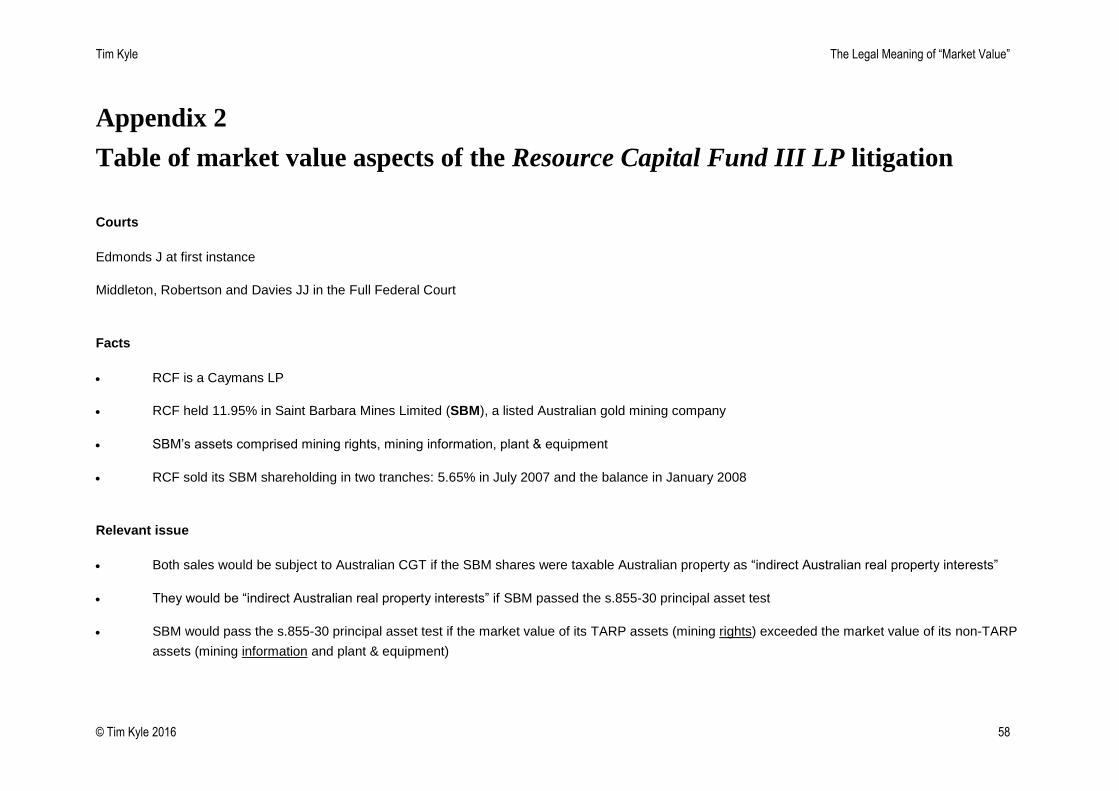

5.5.1 RCF.................................................................................................................................. 26

5.5.2 Case 2/99 ........................................................................................................................ 26

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 3

6 The nature of the Spencer hypothetical market ....................................................................... 28

6.1 What role do actual transactions play in the Spencer test? .................................................... 28

6.2 Aggregated disposals ............................................................................................................. 29

6.2.1 Spencer ........................................................................................................................... 29

6.2.2 Hustlers ............................................................................................................................ 29

6.2.3 Collis ................................................................................................................................ 30

6.2.4 RCF.................................................................................................................................. 30

6.2.5 Miley................................................................................................................................. 31

7 Special value to the purchaser ................................................................................................... 33

7.1 Overview ................................................................................................................................. 33

7.2 Market value under the IVS .................................................................................................... 33

7.3 The case law position on special value .................................................................................. 34

7.3.1 The Marks article ............................................................................................................. 35

7.3.2 Clay’s case ...................................................................................................................... 35

7.3.3 Vyricherla ......................................................................................................................... 37

7.3.4 Brisbane Water County Council ...................................................................................... 37

7.3.5 MMAL Rentals ................................................................................................................. 38

7.3.6 Boland v Yates ................................................................................................................. 38

7.3.7 Alacer Gold ...................................................................................................................... 39

7.4 ATO guidance ......................................................................................................................... 39

8 Immediately enforceable obligations to pay ............................................................................. 41

9 Specialised assets ....................................................................................................................... 43

9.1 Overview ................................................................................................................................. 43

9.2 Information .............................................................................................................................. 44

9.2.1 What is information? ........................................................................................................ 44

9.3 Is information an asset? .......................................................................................................... 44

9.3.1 Particular difficulties in valuing information ..................................................................... 45

9.3.2 Consequences of the valuation difficulties ...................................................................... 46

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 4

9.3.3 Approaches to valuing mining information ...................................................................... 46

9.3.4 Mining information in stamp duty cases .......................................................................... 49

9.3.5 Reconciling mining information and other information cases .......................................... 50

9.4 Goodwill .................................................................................................................................. 51

10 Potential market value reform options ...................................................................................... 54

Appendix 1 Table of cases ................................................................................................................. 56

Appendix 2 Table of market value aspects of the Resource Capital Fund III LP litigation.......... 58

Appendix 3 Table of market value aspects of the SPI PowerNet/AusNet litigation ..................... 63

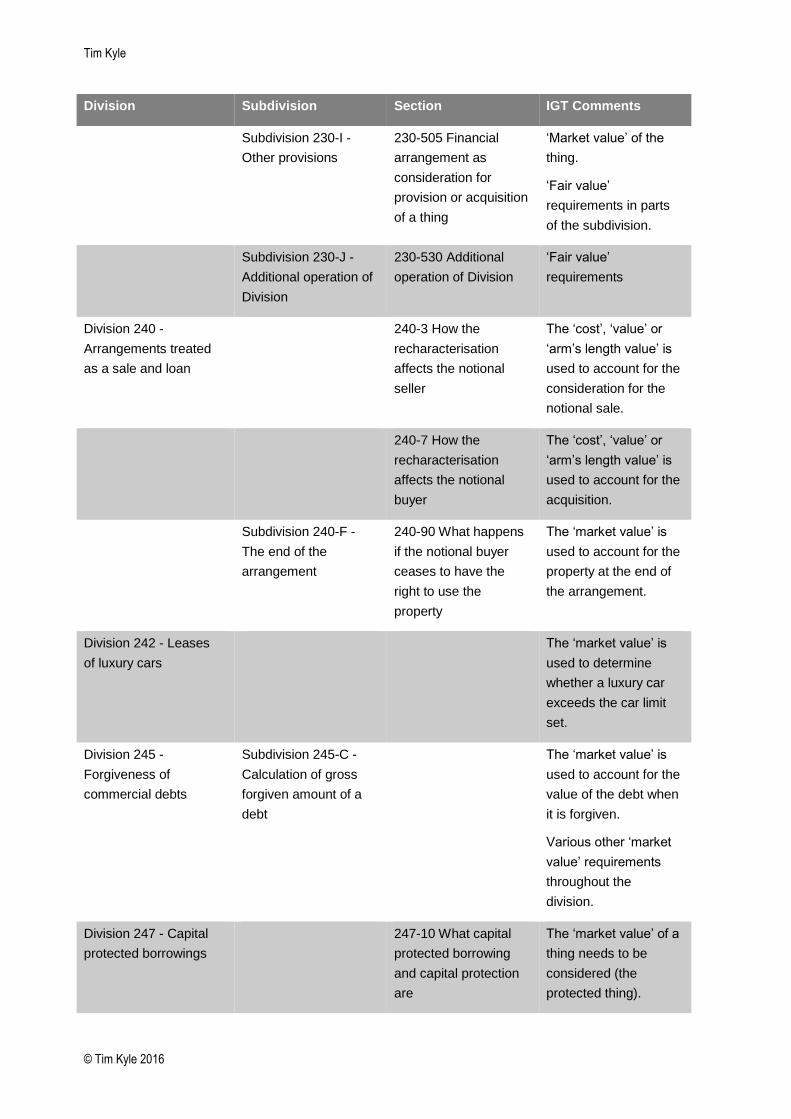

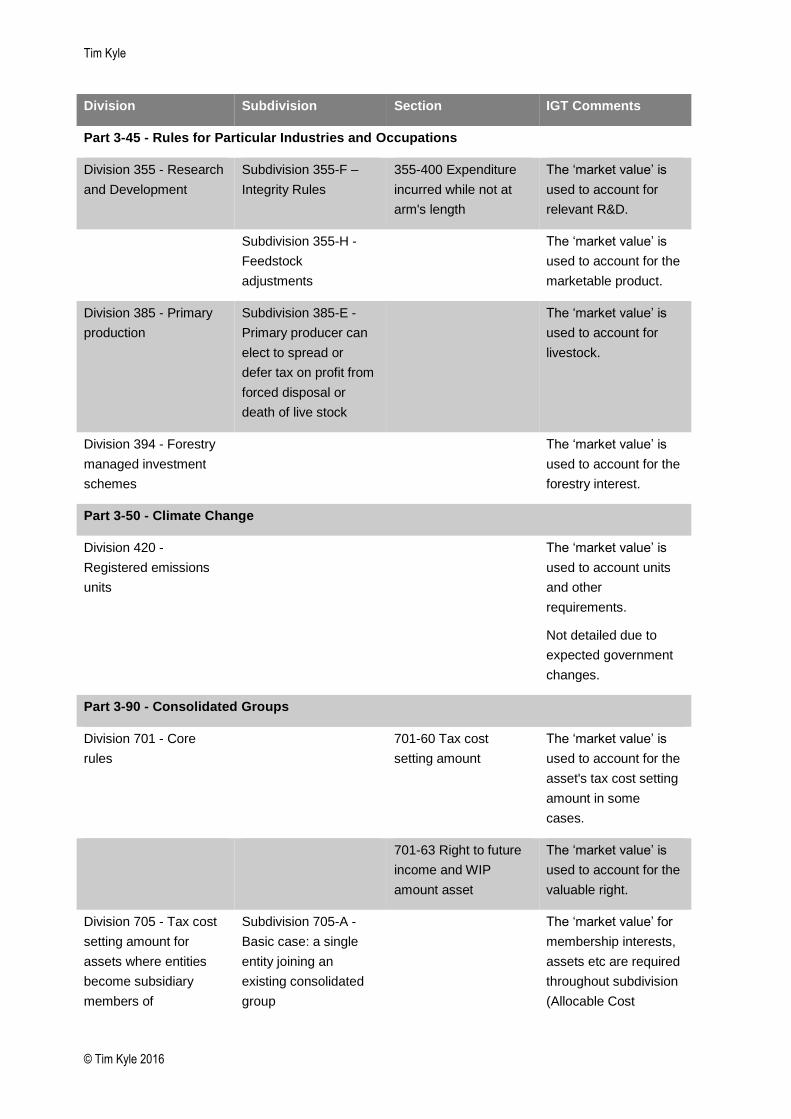

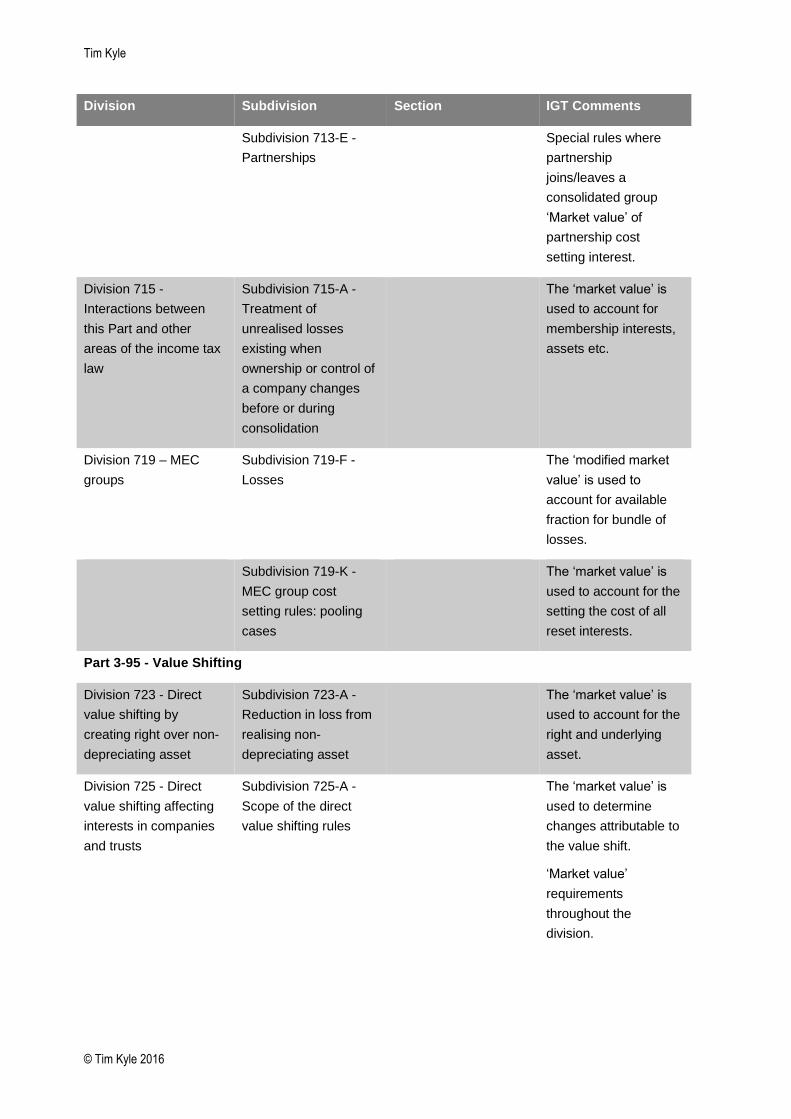

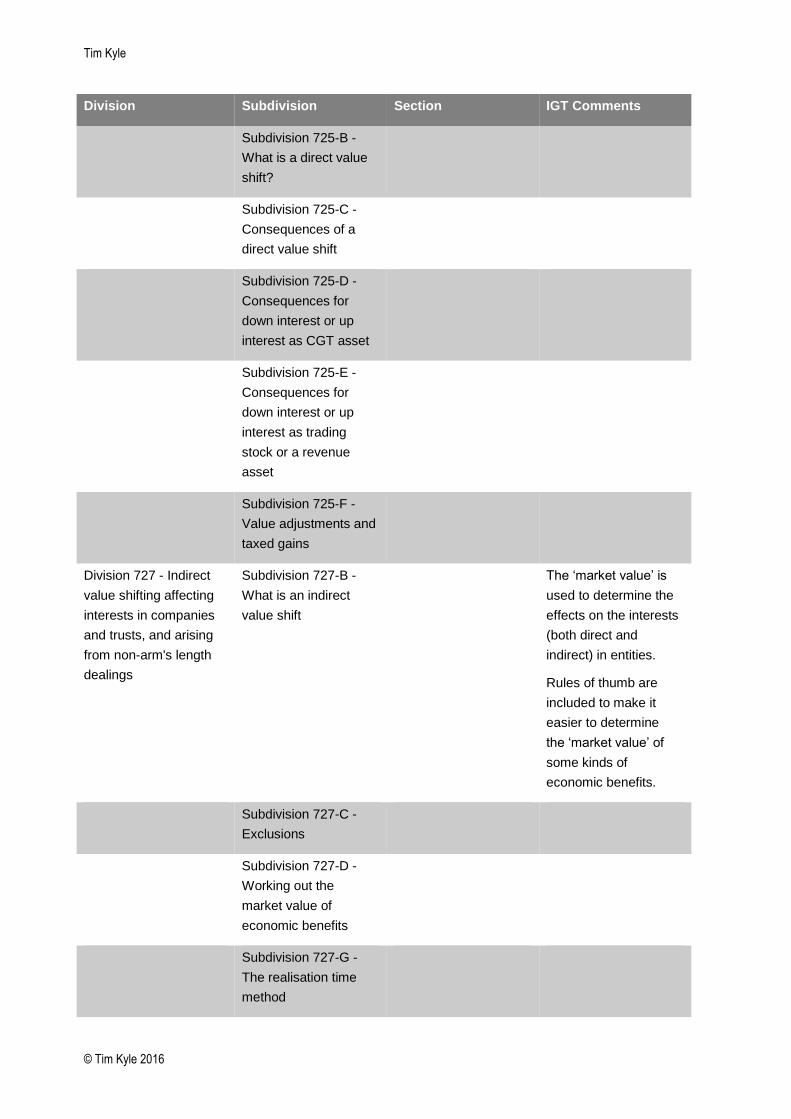

Appendix 4 IGOT Review Tables of valuation-related Tax Act provisions ................................... 73

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 5

1 Introduction

This paper focuses on the meaning of the term “market value” for the purposes of the Income Tax

Assessment Act 1936 and the Income Tax Assessment Act 1997 (Tax Acts).

Overwhelmingly, the term takes its general law meaning in the Tax Acts.

The views expressed in this paper are the author’s personal views.

An important concept with shaky foundations

Market value has incrementally become one of the most important terms the Tax Acts: the term

appears over 500 times and performs very significant roles.

Yet, the cases reveal that determining market value for Tax Act purposes is a fraught process:

the proper approach is shaped by the vagaries of legislative context;

as Courts frequently acknowledge, valuation is an art and not a science;1

the art-like nature of valuation is borne out by violent disagreements between valuers as to

methodologies and outcomes;

case law-established valuation methods clearly diverge from the valuation guidelines in a number

of respects;

judges are often reluctant to provide meaningful guidance; and

there is significant litigation risk in market value cases.

And so this important Tax Act concept has decidedly shaky foundations.

Topics covered

Topic Section

the roles that market value performs in the Tax Acts 2

the (often mistaken) legislative assumptions underpinning the legislative use of market value:

3

the proper approach to determining market value 4

the general law meaning of market value 5

the nature of the Spencer hypothetical market 6

1 AP Energy, Tomanovic v One Australia

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 6

special value to the purchaser 7

immediately enforceable obligations to pay 8

specialised assets 9

potential market value reform options 10

Appendices

Appendix Topic

1 citations of cases referred to in this paper

2 table of market value aspects of the RCF litigation

3 table of market value aspects of the SPI PowerNet/AusNet litigation

4 IGOT Market Value Review tables of valuation-related Tax Act provisions

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 7

2 The roles that market value plays in the Tax Acts

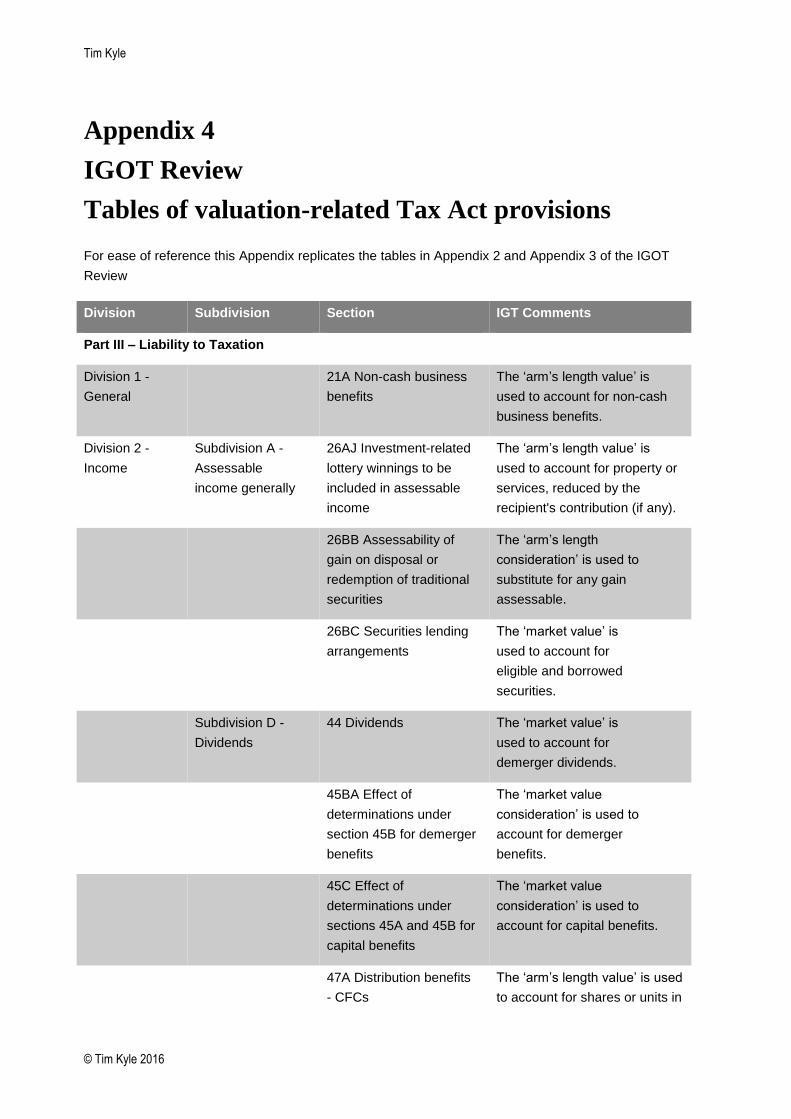

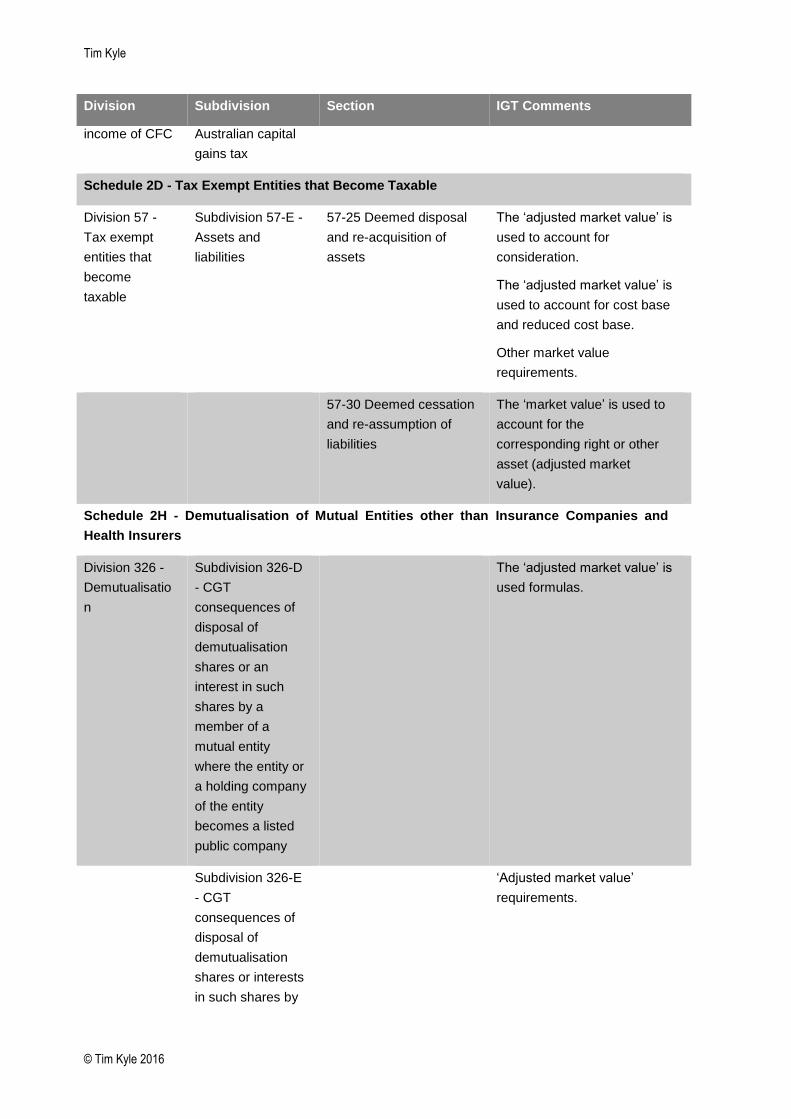

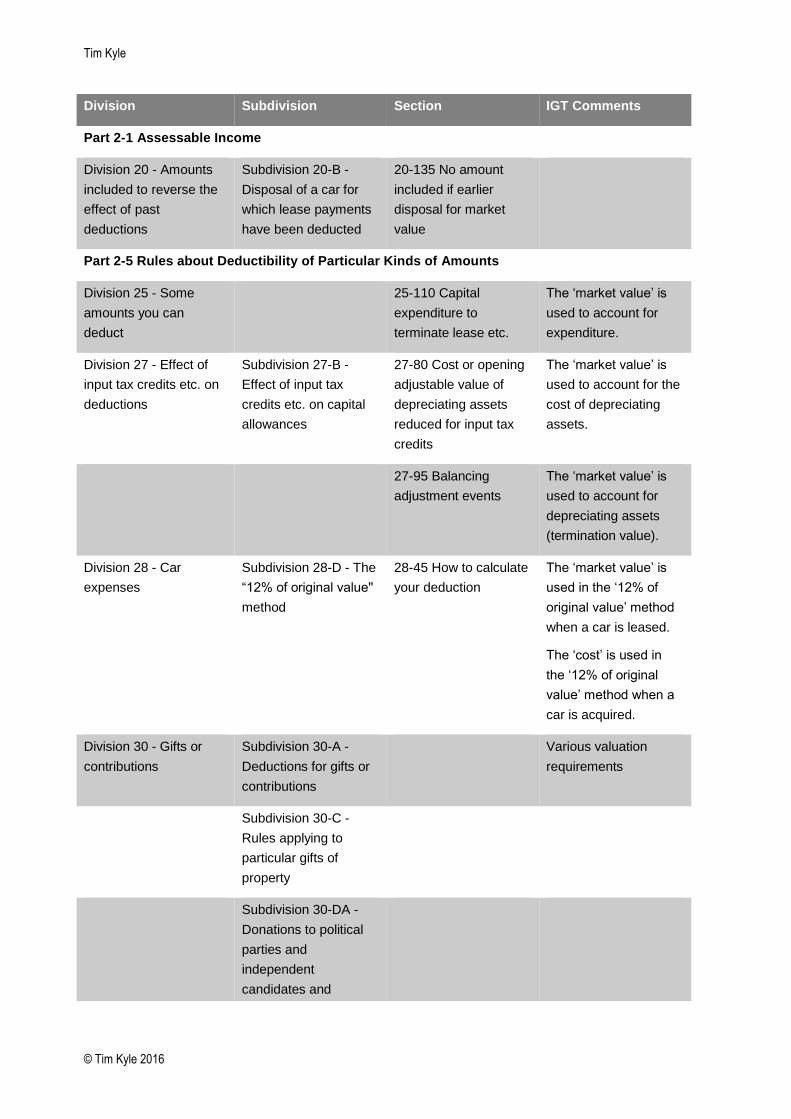

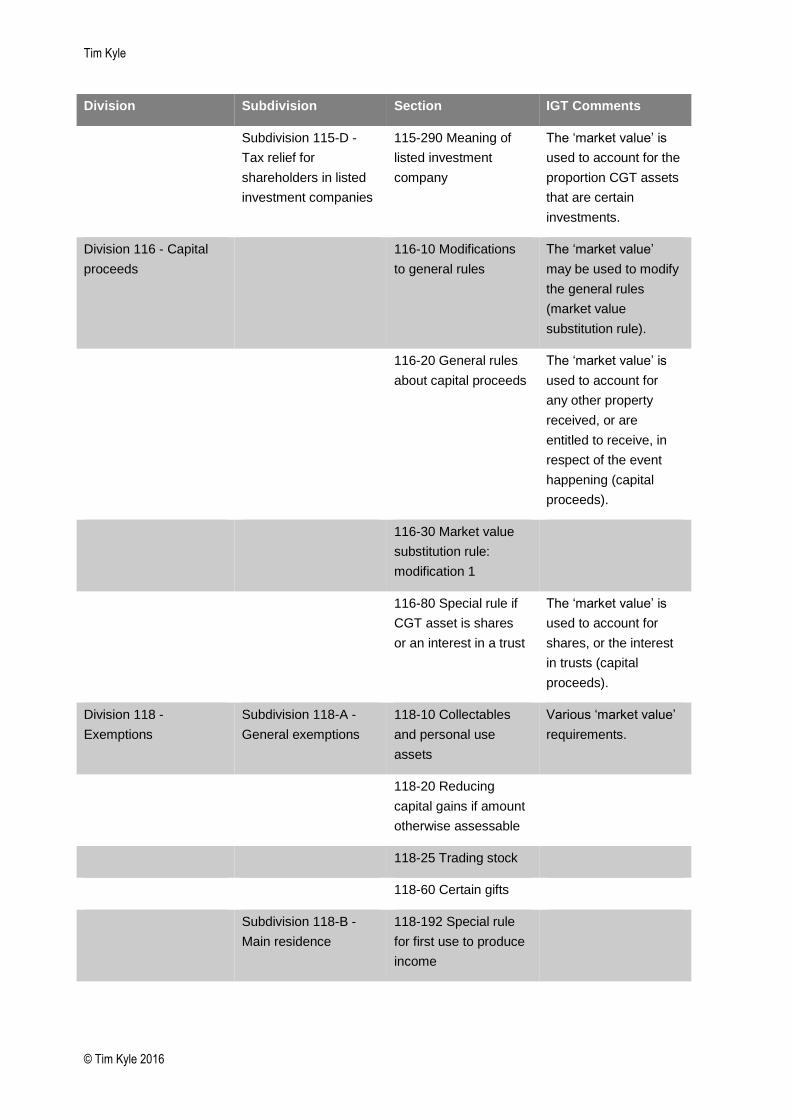

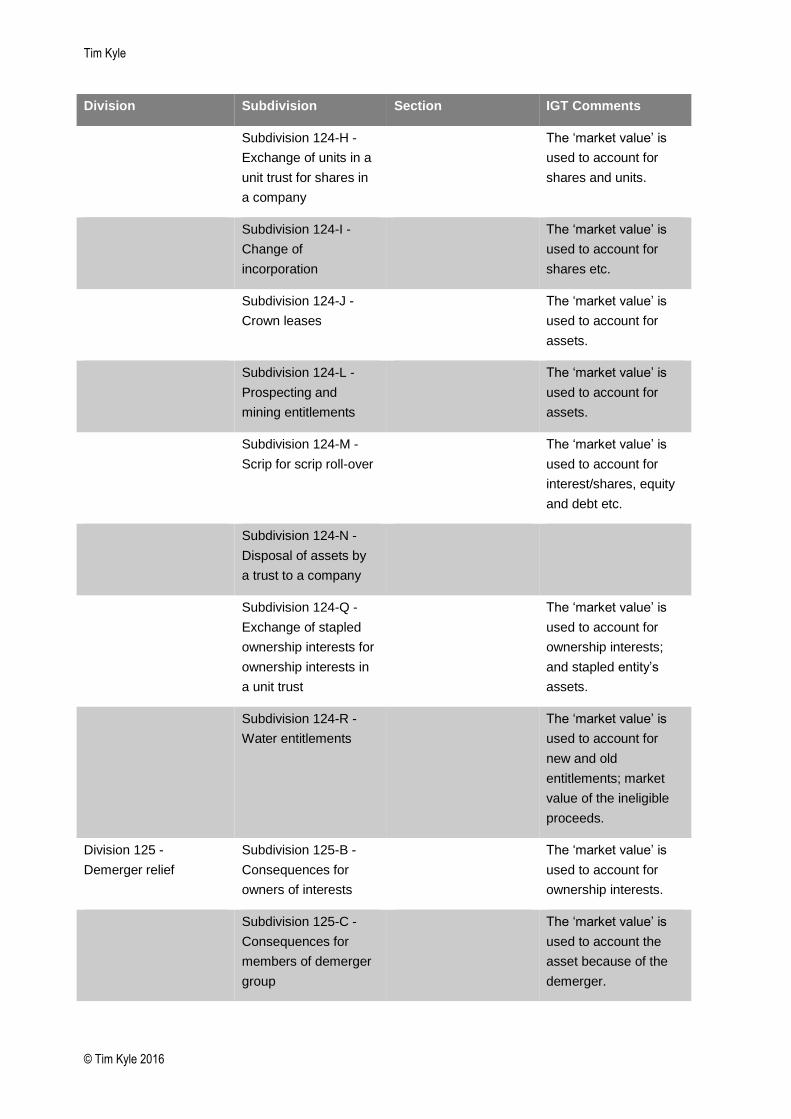

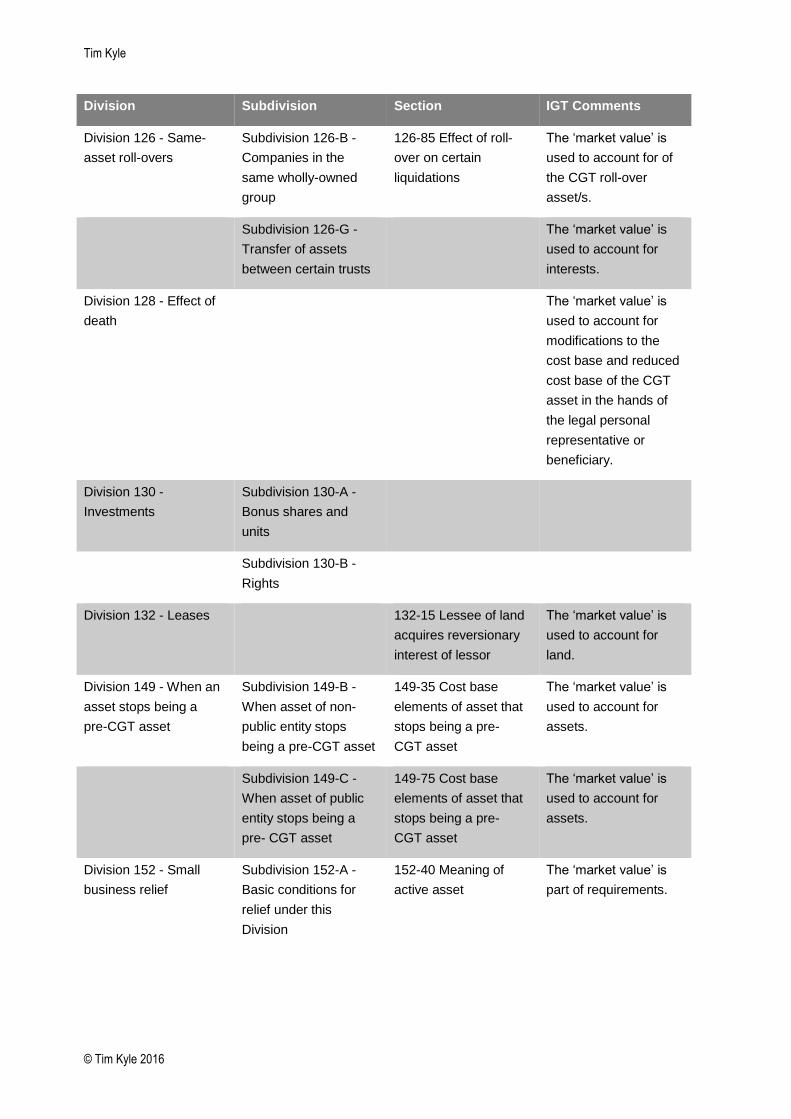

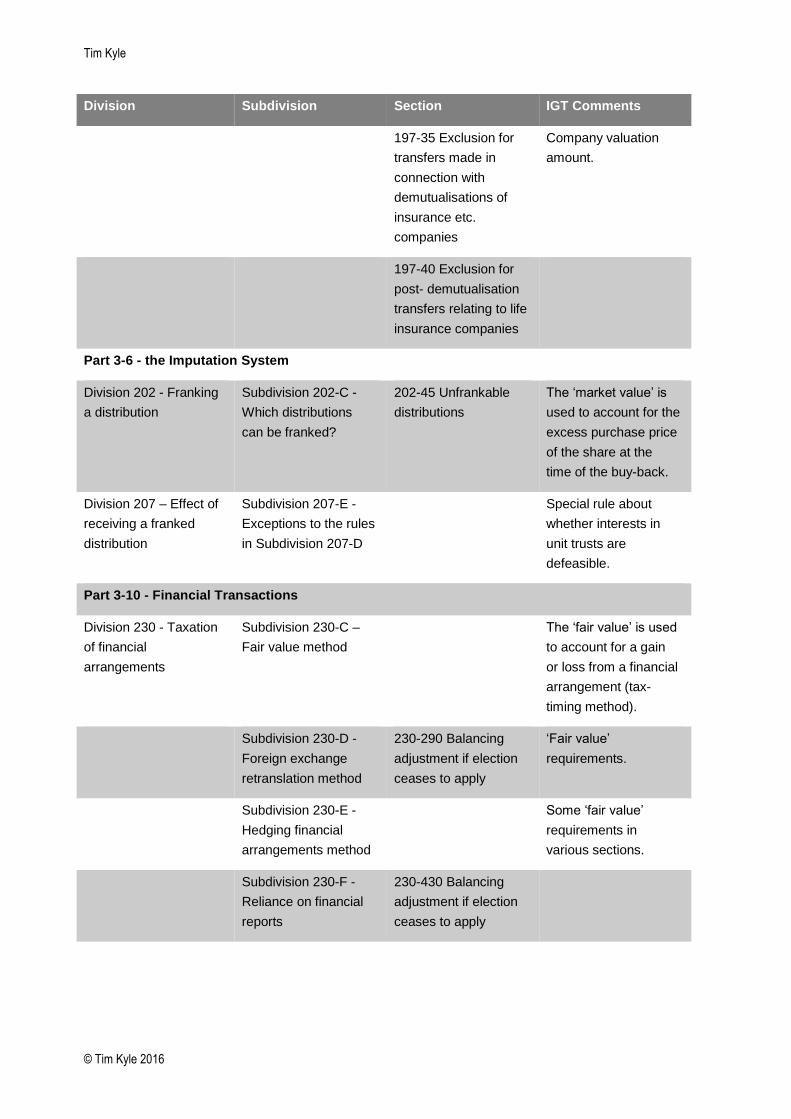

The Inspector-General of Taxation helpfully set out in table form the Tax Act provisions that rely on

the term “market value” in schedules 2 and 3 of his September 2014 Review into the Australian

Taxation Office’s administration of valuation matters (IGOT Review).2

Those tables are set out in Appendix 4.

Four integrity-related themes can extracted from those provisions:

determining tax attributes;

allocating consideration among multiple assets;

imposing a different character for Tax Act purposes; and

determining access to particular provisions.

These themes are discussed below, together with examples of the relevant provisions.

2.1.1 Determining tax attributes

The actual consideration for almost every transaction (whether or not a cross border element is

present) is potentially susceptible to market value substitution for Tax Act purposes.

Sometimes market value substitution is self-executing. Other times market value substitution requires

non-arm’s length dealing.

self-executing market value substitution

Topic Market value substitution trigger Section

trading stock seller sells (and buyer buys) trading stock

outside the ordinary course of business

70-90, 70-95

financial arrangements financial arrangement as consideration for

provision or acquisition of a thing

230-505

direct value shifting value is shifted from one set of company or

trust equity or loan interests to another set of

interests

Division 725

indirect value shifting provisions economic benefits pass between entities for

other than market value consideration –

Division 727

2 http://igt.gov.au/files/2015/01/administration-of-valuation-matters.pdf

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 8

impacting the market value of equity and

loan interests

off-market share buy-backs an off-market share buy-back price is less

than the market value of the shares would

have been if the buy-back did not occur and

was never proposed to occur

159GZZZQ(2)

non-arm’s length dealing triggered market value substitution

Topic tax attribute impacted Section

CGT asset cost base and capital proceeds 112-20, 116-30

depreciating asset tax cost and terminating value 40-180, 40-300

trading stock the buyer’s outgoing/seller’s disposal

proceeds for the trading stock

70-20

2.1.2 Allocating consideration among multiple assets

Often it is necessary for Tax Act purposes to allocate transaction consideration or other amounts among multiple assets or outgoings/expenditure.

Topic Matter Section

tax consolidation tax cost setting amount of reset cost base

assets

705-35

CGT cost and proceeds the amount that is “reasonably attributable”

to the acquisition/CGT event3

112-30, 116-40

deprecating assets the amount that is "reasonably attributable”

to depreciating assets4

40-195

general and “black hole”

deductions

“to the extent that” apportionment 8-1, 40-880

3 Despite the agnostic nature of TD 9, conventionally the “reasonably attributable” amount is based on relative market values

4 Conventionally, the “reasonably attributable” amount is based on relative market values

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 9

2.1.3 Imposing a different character for Tax Act purposes

Market value can also effectively impose a different tax character for Tax Act purposes.

Topic effective recharacterisation Section

direct value shifting value shifting transactions are recharacterised as taxable disposals if market value is shifted between assets of a different class or to a different taxpayer

Division 725

CGT “principal asset test” for non-residents

certain shares/trust interests owned by non-residents are characterised as taxable Australian property (TAP) where the market value of Australian taxable Australian real property (TARP) assets exceed the market

value of non-TARP assets

855-30

participation exemption CGT gains/losses made by a company in respect of shares in a foreign company are disregarded to the extent of the active foreign business asset percentage – which can be determined using the market value method

768-510(2)

thin capitalisation interest is rendered non-deductible to the extent that the average value of an entity’s debt exceeds a statutory safe harbour (subject to alternative tests)

Division 820

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 10

2.1.4 Determining access to particular provisions

Topic Matter Section

scrip for scrip rollover relief market value of original interest and capital proceeds must be substantially the same for certain non-arm’s length dealings

124-780(4)/(5)

small business concessions $6m maximum net asset value test

152-15/20

Division 230 $100m/$300m minimum asset thresholds

230-455

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 11

3 The assumptions underpinning market value

Mark Brabazon SC made this observation in relation to the s.177CB “reasonable alternative”

counterfactual which was enacted in 2013:

“Reasonableness is the darling of Parliament. It gives an appearance of objectivity and has the

cachet of moderation. Its meaning is also remarkably difficult to pin down.”5

This observation applies equally to the long-standing legislative practice of outsourcing many critical

functions to the market value concept.

This legislative practice appears to be based on a series of implicit assumptions about market value.

Those assumptions are set out in the following sections.

However, when those assumptions are tested, it is clear that they have serious flaws – and so neither

objectivity nor moderation is in fact achieved by the legislative outsourcing to market value.

It must be a bit breezy for the Emperor in his (not so) new clothes.

3.1.1 The market value of every “thing” can be determined

There is an assumption that it is possible to arrive at a market value for every “thing” that the Tax Acts

might be concerned with.

However, the need to isolate the market value of individual specialised assets in particular puts a

great deal of pressure on this assumption.

For example, in the SPI PowerNet/AusNet litigation, the Full Federal Court preferred the ATO

valuation expert’s view that the copyrighted information in 105,000 drawings – which was critical to

operating electricity transmission assets - had no market value independent of those assets.

Additional pressure on this assumption comes from the fact that the legislature has at various times

acknowledged that it may be impossible to value assets. In that regard:

If market value cannot be determined, then there is typically no legislative “plan B”.

However, there are at least two instances in the CGT provisions where the legislature

contemplated the fallacy of this critical assumption and provided a back-up plan.

If a taxpayer exchanges asset A for asset B, then the general rule is that the capital proceeds for

the CGT event is the market value of asset B: s.116-20(1).

However, the legislature contemplated that asset B “cannot be valued” – in which case the capital

proceeds are instead the market value of asset A: s.116-30(2)(a).

The mirror provision in relation to cost base is s.112-20(1)(b).

5 (2014) 43 AT Rev 150.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 12

So, the legislative solution when valuation proves impossible is yet more valuation.

Joseph Heller would have appreciated the additional material.

3.1.2 Market value is a single identifiable number

The Tax Acts very clearly assume that the market value of a particular thing is a single identifiable

dollar amount.

However, determining the inputs into any given valuation methodology involves an exercise of

professional judgment. That is, subjectivity is inherently part of the valuation process.

A valuer will have a particular level of confidence about a range of inputs and so will typically report

that the value falls within the range of outcomes generated by those inputs.

That is, typically a valuer will not choose one particular set of inputs to the exclusion of all others and

produce a single value number.

But a market value range doesn’t “work” for most Tax Act purposes.

So, how is the square peg made to fit into the round hole?

It may be that the valuer has the same level of confidence about all outcomes within the valuation

range – in which case the mid-point of the range is generally chosen.

But it may be that the valuer is more confident about particular values within the range than other

values – in which case the task of arriving at a single number is more nuanced.6

The over-simplification inherent in the Tax Act single number value assumption raises two compliance

risks: proportional compliance risk and threshold compliance risk.

Proportional compliance risk

Certain tax outcomes will vary proportionately depending on where in the relevant range the single

number falls.

Determining the precise dollar amount of a capital gain is an example of a proportional outcome.

Disputes involving proportional outcomes occur particularly where the respective valuation experts

produce very different valuation ranges. For example the SPI PowerNet/AusNet litigation, the

difference in the value to be used to determine depreciation cost was hundreds of millions of dollars.

Threshold compliance risk

Other tax outcomes may depend entirely on precisely where in the relevant range market value falls.

6 The charts at Figure 1 of the IGOT Review set out a number of scenarios where there is an uneven distribution of possible

values.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 13

For example, whether the company in which a non-resident is shareholder passes the principal asset

test (and so is an indirect Australian real property interest) or whether a taxpayer can access the

small business concession.

As the IGOT Review notes, even a relatively small change in market value can result in a large and

disproportionate change to a taxpayer’s tax liability.7 The worked small business concession example

shows that a mere $5,000 change in market value can result in a $232,500 additional tax liability.

Legislative provisions in this category inappropriately tend to create “all or nothing” situations because

of the failure of the drafters to understand the true nature of the valuation process.

3.1.3 Market value can be divined in a rational way

There is an assumption that market value is a rationally divined question of fact.

This would be the a valid assumption if there were only modest differences in the market value

outcomes produced by different valuers.

Put differently, this assumption would hold if 10 different valuers were asked to value a particular item

and, although unanimity was not achieved, there was a strong level of commonality in methodologies,

inputs and outcomes.

However, as we have seen in many recent cases, valuation experts can (and frequently do) produce

wildly different valuation outcomes.

That is, this assumption overstates the science and understates the art involved in valuation.

And so an intolerable amount of pressure has been brought to bear on this assumption.

3.2 Growing legislative awareness that market value is not a panacea

There is a growing recognition at policy setter level that market value is not a panacea – and

alternative legislative solutions are being implemented.

For example, the earn-out provisions deliberately adopted an income based “active asset” test for

shares rather than an asset based test. The explanatory memorandum to the relevant bill expressly

acknowledges that this choice was made as the parties put in place an earn-out precisely because

they cannot agree on the market value of that subject asset.

Presumably this thinking was also behind the income based “significant global entity” test that now

applies for MAAL as well as Part IVA penalties.

This growing legislative awareness is welcome.

But there is a long way to go if it is to have any material impact on the Tax Acts.

7 IGOT review at page 27.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 14

Moreover, the use of the new approach just serves to highlight the defects of the old approach in the

earn-out context. This is because many fact patterns will not be covered by the (restrictively drafted)

earn-out provisions. Rather, those fact patterns are still stuck with the ATO’s view in TR 2007/D10

that tax outcomes are determined based on the market value of the earn-out right. The obvious

difficulty with this ATO view is that the market value of the earn-out right is derived from the market

value of the subject asset – and as noted above, the parties put in place an earn-out precisely

because they cannot agree on the market value of that subject asset.

So the ATO view just kicks the valuation can down the road.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 15

4 The proper process for determining market value

Whenever a Tax Act provision requires market value to be determined, a clearly defined process

should be followed.

Departure from that process – for example, immediately outsourcing the task to a valuer – greatly

increases the risk of producing a defective outcome.

The proper process should be:

determine whether any Tax Act modifications to the definition of “market value” apply: see section

4.1;

determine whether a specific Tax Act market value rule applies: see section 4.2;

consider any ATO administrative safe harbours that apply to the provision: see section 4.3; and

apply the general law market value test, having particular regard to the impact of the provision’s

statutory context: see section 5.

4.1 The Tax Act market value definition

The term “market value” appears in the Tax Act in its defined sense.

However, the Tax Act definition of “market value” is spectacularly unhelpful:

“market value has a meaning affected by Subdivision 960-S”. [emphasis added]

Clearly it is not intended to be an exhaustive definition.

This is reinforced by the fact that Subdivision 960-S is very short and only deals with the two very

specific issues discussed below.

The s.960-400 guide to Subdivision 960-S provides as follows:

The expression "market value" is often used in this Act with its ordinary meaning.

However, in some cases that expression has a meaning affected by this Subdivision.

The Commissioner may approve methods to use for working out the market value of assets or

non-cash benefits.

GST exclusive amounts

The first issue that Subdivision 960-S deals with is the impact of GST on the market value of assets

(only).

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 16

Broadly, s.960-405 excises from the market value of an asset the input tax credit that the taxpayer

would be entitled to under a hypothetical acquisition.

It is an important section because it is easily overlooked and can have a material impact on the

market value of assets.

The section provides as follows:

960-405(1) The market value of an asset at a particular time is reduced by the amount of the

*input tax credit (if any) to which you would be entitled assuming that:

(a) you had *acquired the asset at that time; and

(b) the acquisition had been solely for a *creditable purpose.

960-405(2) Subsection (1) does not apply:

(a) to an asset the *supply of which cannot be a *taxable supply; or

(b) in working out the *market value of economic benefits, or of *equity or loan interests, for

the purposes of Part 3-95 (about value shifting).

Note: Some assets, such as shares, cannot be the subject of a taxable supply.

The intention is clearly for the tax market value of an asset to reflect what would be the real economic

outlay to the taxpayer (ie, net of any available input tax credit) on a hypothetical acquisition of the

asset at that time.

So, if the taxpayer (hypothetically) acquired a particular asset for $110 consideration at a particular

time and the taxpayer would have (hypothetically) been entitled to a $10 input tax credit in respect of

the acquisition, then the asset’s market value for income tax purposes is $100, and not $110.

Interestingly, the use of the term “you” appears to direct attention to the input tax credit entitlement of

a particular taxpayer. And so, if taxpayer A is registered for GST purposes, then the market value of

the particular asset would be $100. But if taxpayer B is not registered for GST purposes, then the

market value of that asset for taxpayer B would be $110.

This means that a particular asset can have a different tax market value for the two different

taxpayers.

Yet most people would intuitively think that a particular asset has one single market value. This is

also the implicit assumption referred to in section 3.1.2 above.

Disregard non-convertibility of non-cash benefits to money

Section 960-410 provides as follows:

960-410 In working out the market value of a *non-cash benefit, disregard anything that would

prevent or restrict conversion of the benefit to money.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 17

The precise operation of this section can be critical in determining whether or not a share, right or

option (interest) has been acquired at a discount – and so whether the employee share scheme

provisions apply to it.

The ATO takes an expansive view of 960-410 in a number of private rulings that the section requires

vesting conditions and performance hurdles to be ignored in determining market value of the interest:

see for example the edited private ruling with authorisation number 1011690719326.

With respect, this view may read too much into the words of the section.

Vesting conditions and performance hurdles can have a significant impact on the market value of the

interest because, if they are not satisfied, the employee will not become entitled to the interest.

However, entitlement to the interest is a matter unrelated to the taxpayer’s ability to convert the

interest to money.

Rather, context indicates that the section is directed towards the kind of fact patterns considered in

Cooke & Sherden (free holiday), Tennant v Smith (qualified occupation of an employer provided

house) and Payne (airline loyalty points from employer provided travel that could only be transferred

to relatives) and to which s.21 is directed.

Having said that, s.960-410 clearly does have work to do in the ESS context. For example, it would

require that disposal restrictions be disregarded in determining the interest’s market value.

4.2 The specific Tax Act market value rules

There are various specific Tax Act rules for determining market value.

A number of them are discussed below.

The thin capitalisation regime

Various provisions in the thin capitalisation rules require the value of assets, liabilities or equity capital

to be determined.

An entity must comply with modified accounting standards in determining these values: s.820-680(1).

That is, as a compliance saving measure, determining these values is statutorily outsourced to

modified accounting standards.

Aligning tax values with values used in accounts also imposes a degree of rigour on taxpayers in

circumstances where the accounts are audited and published.

However, this legislative technique is not a complete success. The thin capitalisation provisions apply

a modified version of the accounting standards. For example, internally generated intangibles such

as brands, mastheads, publishing titles and customer lists can be recognised for thin capitalisation

purposes whereas they cannot be recognised for accounting purposes – and intangible assets that

are “recognisable” for accounting purposes can be revalued for thin capitalisation purposes in

circumstances where they cannot be revalued for accounting purposes.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 18

The ATO is concerned about arbitrage opportunities arising from the lack of complete book/tax

alignment: see TA 2016/1

Division 230

Various parts of the “TOFA” provisions also outsource tax outcomes to accounting standards.

For example, movements in the accounting fair value of assets and liabilities may be

assessable/deductible under the fair value and financial reports elective methods.

Also, the s.230-455 asset value threshold is determined by applying accounting standards.

Again, one of the principal drivers for this legislative technique was its role as a compliance saving

measure and it certainly achieves that goal.

However, this legislative technique really only replaces one inherently uncertain concept (market

value) with another inherently uncertain concept (fair value).

Safe harbour amounts in the ESS provisions

As a compliance saving measure, regulations provide a safe harbour for valuing employee share

scheme interests that are unlisted rights to shares: s.83A-315 and Division 83A of the 1997 Tax Act

Regulations.

Safe harbour methodologies

An interesting development that has gone relatively unnoticed was the 2015 introduction of the

Commissioner’s power under s.960-412 to develop regulations setting out methodologies for valuing

particular assets/non-cash benefits.

A specified methodology would be a safe harbour for taxpayers as the ATO would be bound to accept

the use of that methodology in valuing the particular asset/non-cash benefit.

One approved methodology is for the purpose of determining market value eligibility for the ESS start

up provisions: in very restrictive circumstances accounting net assets can be used:

http://law.ato.gov.au/atolaw/view.htm?DocID=ITD/ESS20151/00001

There is no specific indication on the face of the legislation that the methodologies would be confined

to the ESS space. However, the explanatory memorandum to the bill that introduced s.960-410

provides as follows:

1.99 While the new approved safe harbour valuation methodology applies more broadly than

ESS, it is anticipated that the Commissioner will initially only exercise this new power with

regard to ESS arrangements for small unlisted corporate tax entities only.

Where particular methodologies are specified, this would undoubtedly be of some utility for taxpayers.

However, it should be noted that many market value cases the dispute is not over the methodology to

be applied – but rather the result of applying that methodology.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 19

4.3 ATO administrative safe harbours

The ATO has produced the following elective administrative safe harbours as a compliance saving

measure:

s.70-110 value of goods taken from trading stock: TD 2014/2 and PS LA 2004/3 (GA)

fuel tax credit apportionment percentages: PCG 2016/11 and PS LA 2013/4 (GA)

valuation shortcuts for ACA pushdown: Part H of the ATO’s market value guidelines:

https://www.ato.gov.au/General/Capital-gains-tax/In-detail/Calculating-a-capital-gain-or-

loss/Market-valuation-for-tax-purposes/

This represents a disappointingly small number of administrative safe harbours in the context of the

extensive Tax Act use of market value.

Moreover, the valuation shortcuts for ACA pushdown (while welcome) are deliberately very limited in

their scope and are subject to a number of constraints.

4.4 Where no specific Tax Act rule applies

Few Tax Act provisions are impacted by specific Tax Act market value rules or ATO administrative

safe harbours.

Rather, for the overwhelming majority of Tax Act provisions, consistent with the note to Subdivision

960-S and well-established principles of statutory construction, market value takes its “ordinary” (ie,

general law) meaning.

The general law meaning of market value is discussed in section 5 below.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 20

5 The general law meaning of market value

5.1 Overview

This section:

considers the very different contexts in which market value cases have arisen;

reviews the Spencer hypothetical market;

discusses some of the practical challenges in applying the Spencer test; and

highlights the importance of considering legislative context in applying the Spencer test.

5.2 Market value cases in different contexts

Market value cases have arisen in a range of different contexts.

However, despite the different contexts, over time the Spencer test has become accepted as the

universal legal test for determining market value under the general law.

Government compulsory acquisition compensation cases

There is a considerable body of case law on compulsory acquisition cases.

These cases arise where a Government authority compulsorily acquires an owner’s asset and the

authority is charged with paying the market value of the asset.

Spencer is a Government compulsory acquisition case.

Contractual disputes

A body of case law has developed dealing with contractual arrangements requiring market value

consideration.

Often a shareholders agreement will have mechanisms in place designed to ensure that an exiting

shareholder receives market value consideration for their shares.

Examples of disputes involving these contractual arrangements include MMAL Rentals and

Tomanovic v One Australia.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 21

Revenue law cases

Market value has become a key concept in a wide range of revenue cases, including income tax,

GST, stamp duty, council rates and death duties.

The body of case law on market value in a revenue law context is expanding rapidly.

5.3 Spencer’s case

Much has been written about Spencer. This section is not a detailed analysis of the case - rather, it is

intended to highlight key aspects of the decision.

Context

Spencer is a Government compulsory acquisition compensation case.

Facts

The facts can be summarised as follows:

Mr Spencer owned a large tract of land in Fremantle near the harbour and railway line;

on 1 January 1905 the Commonwealth resumed the land in order to build a fort;

the Commonwealth was required by statute to pay Spencer compensation effectively by reference

to the “value” of the land as at 1 January 1905; and

at first instance, Higgins J held that the “true value” of the land was £2,250 - on the basis that that

is what could have realised by subdividing and selling the land to be developed for workers

cottages of the type already in the area.

Issue

Was the compensation payable:

£10,000 as Spencer claimed - on the basis that the land could potentially be used as a factory “or

some other enterprise requiring considerable space”; or

£3,000 plus interest, being the amount that the Commonwealth “brought into court”?

Held

In summary, the High Court held that:

the land was undoubtedly suitable for use as a factory;

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 22

however, the value of the land could not take into account its potential use as a factory because

there was no evidence that any demand for a factory at the site existed at the relevant time;

the evidence only supported use for subdivision and sale to be developed for workers cottages;

and

Spencer had not discharged the onus of proving that he was entitled to more than the £3,000 that

the Commonwealth “brought into court”.

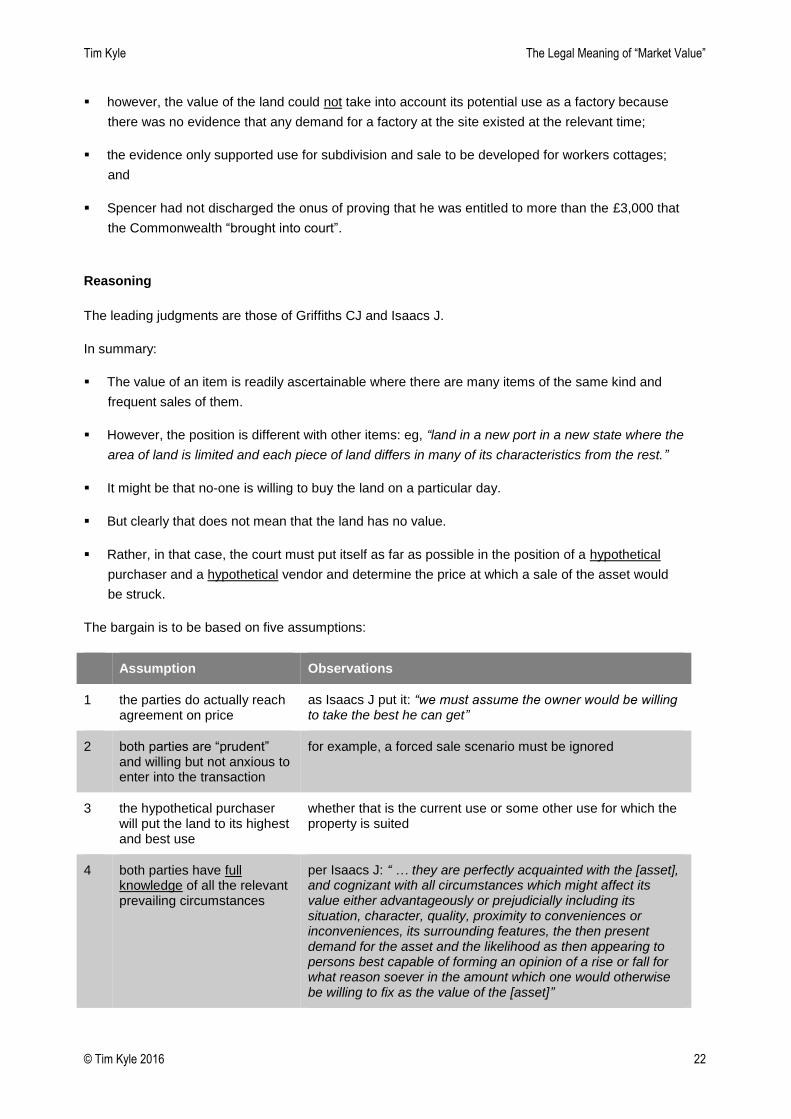

Reasoning

The leading judgments are those of Griffiths CJ and Isaacs J.

In summary:

The value of an item is readily ascertainable where there are many items of the same kind and

frequent sales of them.

However, the position is different with other items: eg, “land in a new port in a new state where the

area of land is limited and each piece of land differs in many of its characteristics from the rest.”

It might be that no-one is willing to buy the land on a particular day.

But clearly that does not mean that the land has no value.

Rather, in that case, the court must put itself as far as possible in the position of a hypothetical

purchaser and a hypothetical vendor and determine the price at which a sale of the asset would

be struck.

The bargain is to be based on five assumptions:

Assumption Observations

1 the parties do actually reach agreement on price

as Isaacs J put it: “we must assume the owner would be willing to take the best he can get”

2 both parties are “prudent” and willing but not anxious to enter into the transaction

for example, a forced sale scenario must be ignored

3 the hypothetical purchaser will put the land to its highest and best use

whether that is the current use or some other use for which the property is suited

4 both parties have full knowledge of all the relevant prevailing circumstances

per Isaacs J: “ … they are perfectly acquainted with the [asset], and cognizant with all circumstances which might affect its value either advantageously or prejudicially including its situation, character, quality, proximity to conveniences or inconveniences, its surrounding features, the then present demand for the asset and the likelihood as then appearing to persons best capable of forming an opinion of a rise or fall for what reason soever in the amount which one would otherwise be willing to fix as the value of the [asset]”

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 23

5 the value is to be unaffected by hindsight

any events occurring after the test time must be ignored

5.4 Practical challenges in applying the Spencer test

5.4.1 Overview

Certain legal tests are remarkably simple on their face, yet are incredibly difficult to apply in practice.

Dixon J’s revenue/capital distinction test in Sun Newspapers is the best known.

And the Spencer market value test is also in this category.

As Griffiths CJ himself put it, with masterful understatement:

“[i]t is, no doubt, very difficult to answer such a question, and any answer must be to some

extent conjectural”.

Over a century after Spencer was decided, the judicial approach to applying the test can still only be

described as in relatively early stages of development: there are numerous unresolved issues and a

dearth of meaningful guidance.

5.4.2 How do Courts approach the Spencer market value test?

Market value cases produce particular challenges for judges.

Typically judges are not professional valuers.

Yet both sides will typically lead very detailed evidence from experts as to their opinion of the market

value.

Almost inevitably, the experts for the respective parties will produce very different market value

amounts – and each expert ostensibly has a plausible position.

There are generally four potential outcomes from market value cases:

The most common outcome is that the court will accept one expert’s approach. The acceptance

may be qualified, but that approach is considered superior to the approach taken by the other

experts (ie, the Court simply “picks a horse”).

Where the Court is not satisfied with the approach taken by the experts, the Court will typically

either:

find that the requisite onus of proof has not been discharged – which typically results in the

taxpayer losing in income tax cases; or

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 24

remit the matter to the lower Court/tribunal to re-determine market value: eg, the SPI

PowerNet/AusNet Full Federal Court decision.

Sometimes (although now very rarely) judges arrive at market value independently:8

they may make adjustments to the approach advocated by valuer experts in order to arrive at

a result they find more sensible: eg, Edmonds J in RCF at first instance; or

they may rely on other (non-valuer) evidence in order to achieve a sensible result (eg, MMAL

Rentals, Collis and Case 2/99).

But whichever approach a Court takes, they know that the dissatisfied party may well appeal – and

they also know that appeal courts have demonstrated little compunction in overturning market value

decisions of lower courts.

Indeed, in many cases, appeal courts have been highly critical of the lower court decision. See for

example the Full Federal Court decisions in RCF and SPI PowerNet/AusNet.

5.4.3 MMAL Rentals

Facts

MMAL Rentals Pty Limited (M) owned 80% of T, a company carrying on the Thrifty car rental

business;

Bruning (B) was managing director of the business and held 20% of T;

T was in losses and was significantly indebted to M, the controlling shareholder, so that the

prospects of receiving dividends on B’s 20% T shareholding was remote;

M exercised an option in the management agreement to buy the 20% for its “fair market value”;

M had recently offered $535,000 for B’s shareholding – an offer that B had rejected;

M’s valuer asserted an approximately $60,000 valuation using a net asset methodology (which

the first instance judge described as being “as useful as valuing the Sydney Harbour Bridge on

the basis of its scrap metal value”); and

B’s valuer asserted a $6m value based on what the Court found were unrealistic assumptions.

Held

The value was $535,000.

8 This used to be how most cases were decided. But it has become much less common in recent years with the growth of

expert valuation evidence.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 25

Reasoning

The first instance judge’s determination was upheld.

M’s recent offer was a “signpost” with probative value.

The first instance judge was right to take into account the “special value” to M arising from acquiring

100% control by retiring B’s minority interest. And so no discount applied on the basis that the shares

were only a minority interest.

5.5 Legislative context is critical

Unfortunately, there is no universally applicable market value principle/methodology for income tax

purposes (or indeed for any purposes).

Rather, the market value of a particular thing can vary depending on the statutory context of the

relevant inquiry.

The challenges that this presents were neatly captured by the IGOT Review:

2.42 Furthermore, laws imposing valuation do not necessarily lend themselves to a common

or unified valuation approach, even if one standard of value is commonly used. This

difference in approach arises from the difference in statutory schemes. For example, the Full

Federal Court recently cited with approval the following comments made by the New South

Wales Court of Appeal in Leichhardt Municipal Council v Roads and Traffic Authority of New

South Wales:

Matters of valuation turn in large measure on the precise statutory scheme. These

schemes differ from one area of discourse to another. It is always important to

commence with the precise words of the statute. There appears to be a tendency to

take a judgment about one statutory regime and classify its conclusion as a “valuation

principle” which is applied to any process of valuation, no matter how different the

statutory regime may be.

The need to determine the value of assets arises in many different legal contexts. It is

the context which determines the relevant principles of valuation to be applied. An

assumption that there is in existence some abstract body of “valuation principles”

applicable in all contexts, irrespective of the statutory scheme or contractual

provision, is liable to lead to error. Judgments in one context may prove instructive by

way of an analogy when dealing with another context. Nevertheless, statutory

differences must be borne in mind. The ultimate task must always come back to the

application of the principles in the particular context…

The impact of legislative context on market value is demonstrated in the cases discussed in the

following sections.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 26

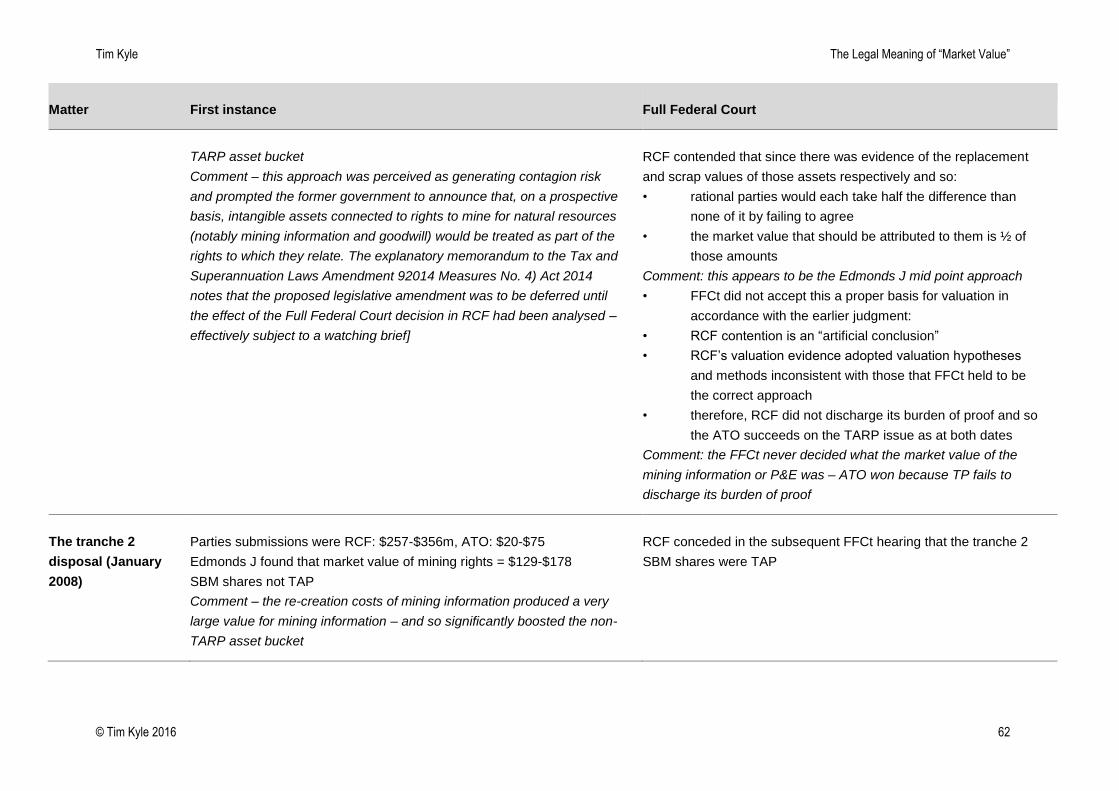

5.5.1 RCF

In RCF, whether the taxpayer’s St Barbara Mines Limited (SBM) shares were taxable Australian

property (TAP) ultimately turned on whether the s.855-30 principal asset test required that SBM’s

assets be valued assuming that they were sold either:

under a series of stand-alone sales; or

in a single simultaneous sale.

At first instance

Edmonds J held that the context of s.855-30 required that each asset be valued on the basis that it

was sold on a stand-alone basis, separately from the other assets and using different valuation

methods depending on the asset.

His Honour saw particular significance in the use of the plural “market values” in the phrase “sum of

the market values of the entity’s assets”.

This approach produced a very large value for mining information. Because both parties determined

the market value of the mining rights on a residual basis, the consequence of this approach was that

the taxpayer’s SBM shares did not pass the principal asset test and so were not TAP.

Full Federal Court

The Full Federal Court held instead that the assets were to be valued on the basis that they were

offered for sale as a bundle in one single transaction to a single hypothetical purchaser.

This issue was critical to the s.855-30 outcome – yet the reasoning in both judgments on this point

could be criticised as being poorly developed and far from compelling.

5.5.2 Case 2/99

It may be that an asset is capable of being sold in a number of different markets.

For example, trading stock is typically purchased in the wholesale market and sold in the retail market

at very different prices.

Where trading stock is sold outside the ordinary course of the seller’s business, the actual sale price

is disregarded and the trading stock’s market value is substituted - for both buyer and seller - under

s.70-90 and s.70-95 respectively.

The interesting issue considered in Case 2/99 was which market was the appropriate market for

determining the market value of trading stock.

Facts

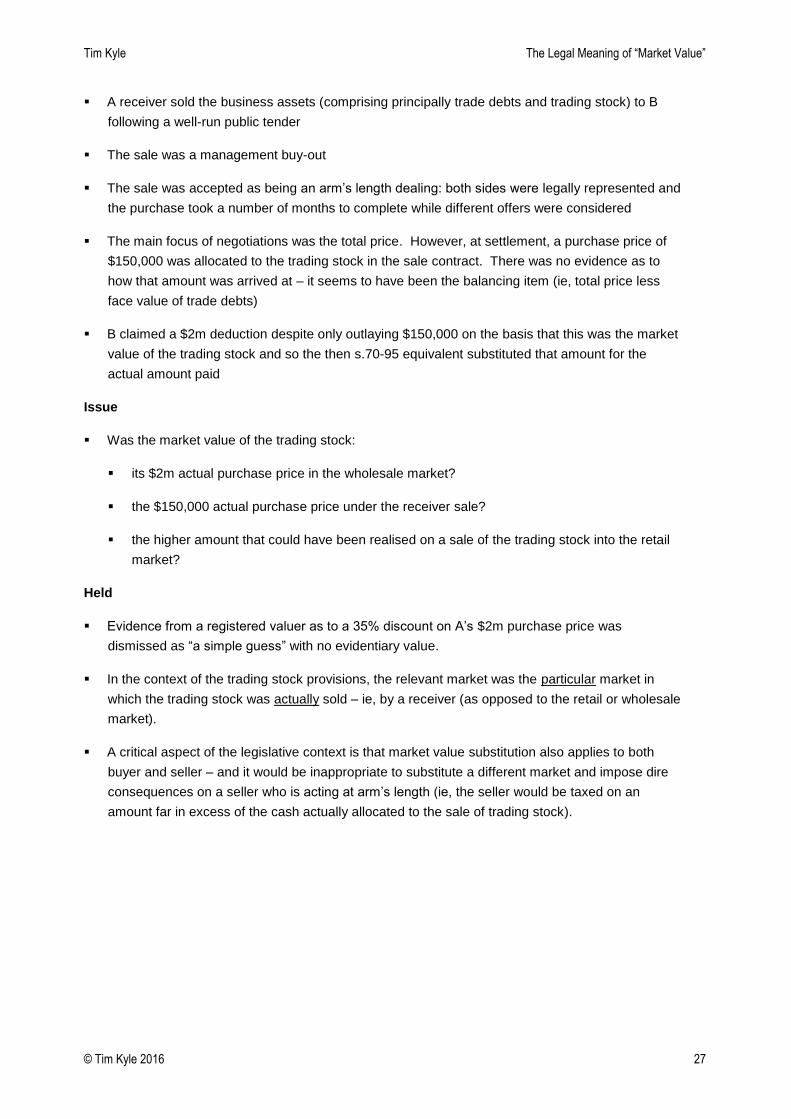

A owned a vacuum cleaner spare parts business which got into financial trouble

A had bought the trading stock in the wholesale market for $2m

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 27

A receiver sold the business assets (comprising principally trade debts and trading stock) to B

following a well-run public tender

The sale was a management buy-out

The sale was accepted as being an arm’s length dealing: both sides were legally represented and

the purchase took a number of months to complete while different offers were considered

The main focus of negotiations was the total price. However, at settlement, a purchase price of

$150,000 was allocated to the trading stock in the sale contract. There was no evidence as to

how that amount was arrived at – it seems to have been the balancing item (ie, total price less

face value of trade debts)

B claimed a $2m deduction despite only outlaying $150,000 on the basis that this was the market

value of the trading stock and so the then s.70-95 equivalent substituted that amount for the

actual amount paid

Issue

Was the market value of the trading stock:

its $2m actual purchase price in the wholesale market?

the $150,000 actual purchase price under the receiver sale?

the higher amount that could have been realised on a sale of the trading stock into the retail

market?

Held

Evidence from a registered valuer as to a 35% discount on A’s $2m purchase price was

dismissed as “a simple guess” with no evidentiary value.

In the context of the trading stock provisions, the relevant market was the particular market in

which the trading stock was actually sold – ie, by a receiver (as opposed to the retail or wholesale

market).

A critical aspect of the legislative context is that market value substitution also applies to both

buyer and seller – and it would be inappropriate to substitute a different market and impose dire

consequences on a seller who is acting at arm’s length (ie, the seller would be taxed on an

amount far in excess of the cash actually allocated to the sale of trading stock).

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 28

6 The nature of the Spencer hypothetical market

Where there is no readily identifiable actual market (ie, involving multiple transactions and essentially

homogenous items), Spencer creates a hypothetical market operating under specific assumptions.

The Spencer hypothetical market participants are a hypothetical vendor and a hypothetical potential

purchaser.

At first blush, this hypothetical market may appear to take no account of actual transactions between

actual vendors and purchasers.

However, it is clear from case law that the hypothetical market is not a pure hypothetical abstraction.

Particular issues in this hybrid approach include:

the extent to which actual transactions can determine market value: see section 6.1; and

the extent to which evidence of actual purchaser demand can determine market value: see

section 6.2.

6.1 What role do actual transactions play in the Spencer test?

Where neither party is anxious and the other Spencer assumptions are satisfied, then Courts

generally proceed on the basis that the price arrived at under an arm’s length dealing represents

market value consideration.9

That is, evidence of actual transactions informs (and may even determine) the relevant market value.

The ATO accepts this as a general proposition in rulings10

and has argued it many times in market

value cases.

On that basis, the Spencer market should be seen as a hybrid market rather than a purely

hypothetical market.

Indeed arguments that the parties to an actual transaction “are too close to the transaction” and so an

independent valuation should be preferred to the actual transaction price were quickly dispatched in

Excellar.

9 For example, McLelland CJ. in Solomon Pacific Resources NV v Acacia Resources Ltd (No 2) (1996) 14 ACLC 637 at 684” 'In

the case of an honest arms-length transaction, it could generally be presumed that no discrepancy (such as between the value

of the Solpac shares to be acquired and the fair value of the Acacia shares to be issued) would exist, and it could not be

supposed that one party would be willing to acquire property for a consideration significantly greater than the perceived value to

the acquirer of the property acquired.’

See also Case 2/99 at [25]: ‘In relation to a particular market, the best evidence of the market price prevailing is what the

parties dealing with each other at arm’s length at the conclusion of a hard headed business negotiation have agreed upon.’

Sharp J in Alacer Gold at [250]: ‘Where there are no abnormalities affecting a market, the price at which property changes

hands in the ordinary course of business and the market is usually its true value; Nischu at 443, Perpetual at 579 and

Commissioner of Succession Duties (SA) v Executor Trustee and Agency Co (SA) Ltd (1947) 74 CLR 358 at 361.’ 10

See GSTR 2001/6 at paragraph 19

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 29

However, the Spencer hypothetical market is governed by particular assumptions.

Where the circumstances of an actual transaction are inconsistent with one or more of those

assumptions, then the actual transaction will not produce market value consideration.

For example, the parties may deal with each other at arm’s length, but one party is “anxious” – in

which case the actual consideration will not be market value consideration.

6.2 Aggregated disposals

The hypothetical market test has a highest and best use requirement.

The highest and best use – and so the market value – of an asset may well be different depending on

whether the asset is properly considered:

on a stand-alone basis; or

in combination with other related assets.

This is because a combination approach may open up other potential uses that do not apply on a

stand-alone approach.

But which approach is correct?

Case law establishes that the answer is that a combination approach is the correct approach -

provided that there is evidence that there was demand for that higher/best use at the relevant time.

6.2.1 Spencer

It is tolerably clear from Spencer that only the absence of evidence showing demand for the land to

be used as a factory “or some other enterprise requiring considerable space” prevented the

taxpayer’s £10,000 compensation claim from being successful.

6.2.2 Hustlers

In Hustlers, it was necessary to value three adjoining parcels of land on the Bathurst main street.

The Court rejected valuations prepared on a stand-alone basis.

The greatest value for the parcels would have been derived from the parcels being used for a retail

shop (eg, a Coles supermarket). However, the Court found no evidence of any demand for this use.

Rather, the value was instead derived from their use as a commercial business (eg, CBA or MLC

branch) – as there was evidence of demand for this use.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 30

6.2.3 Collis

Facts

C owned 4 parcels of adjoining land of equal size fronting the same road

C had purchased the 4th parcel recently for $200,000

All 4 parcels were sold together at auction under an (overall) arm’s length dealing for one single

amount of $1.43m

C would be taxed on the amount by which the market value of the 4th parcel exceeded $200,000

Issue

Was the market value of the 4th parcel at the time of sale to be determined:

on a stand-alone basis - if so, the highest and best use was as a residential home.

on a combination basis - If so, the highest and best use of the 4 parcels was as an office

development.

Held

The combination basis was the appropriate valuation basis because there was evidence of a demand

for land of such an area for office development

As a result, the market value of the 4th parcel was $357,000 – being ¼ of the total purchase price.

6.2.4 RCF

Where a single seller sells multiple assets, the advantages accruing from that asset combination may

mean that the total sale price is higher than if the assets were sold under separate arrangements to

different purchasers.

For example, there is a clear difference between the expected sale proceeds of a business on a going

concern basis and on a break-up of the business.

RCF wrestled with this issue in the context of the s.855-30 principal asset test, with the Full Federal

Court holding that the legislative context required an assumed simultaneous sale of the SBM assets.

It should be noted that Edmonds J arrived at a similar position at first instance with highest and best

use assumption that he applied effectively aggregating the disposal of the mining rights and mining

information.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 31

6.2.5 Miley

Facts

Miley was one of three equal shareholders in a company

the three shareholders sold their shares in the company to a single purchaser for $17.7m under

an arm’s length transaction – so that each shareholder received $5.9m sale proceeds;

Miley would be eligible for the small business concession provided the market value of his shares,

determined just before the CGT event, was not more than $5.81m (ie, an amount less than

Miley’s $5.9m sale proceeds).

Held

The AAT held that:

the $5.9m sale proceeds reflected a 1/3 share of the control premium arising from the sale of

100% of the company;

however, considered in isolation, Miley’s shareholding represented only a 1/3 interest in the

company – and so did not confer control of the company;

accordingly, a 20% control premium was to be deducted from the $5.9m sale proceeds to arrive at

a general law market value of $4.9m for Miley’s shareholding.

Miley is currently on appeal.

Observations

There may well be many circumstances in which the market value of a minority shareholding should

not reflect a control premium. One minority shareholder selling to another minority shareholder

without the purchaser obtaining control of the company would be an example.

But it would be inappropriate in other circumstances. By way of example:

as we saw in MMAL Rentals, the Court held that the market value of a minority shareholding to be

acquired by a majority shareholder reflects the special value to the majority shareholder of retiring

the minority interest; and

when a listed company takeover bid is announced, the target’s trading price typically increases to

reflect the control premium expected to paid by the bidder – and that increased trading price

applies to minority shareholdings.

Moreover, in Miley, it can be presumed that, just before the CGT event, there would have been

evidence of the purchaser’s intention to take over the company and pay a control premium – as well

as evidence of the three minority shareholders collaborating to effect a sale on that basis.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 32

And so, with respect, in Miley the hypothetical nature of the Spencer market may have been taken too

literally.

Rather, having regard to the cases referred to above, evidence of actual demand for the shares

should inform the market value analysis. When that is done, there is a clear basis for concluding that

the market value of Miley’s shareholding just before the CGT event was $5.9m.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 33

7 Special value to the purchaser

7.1 Overview

Valuers apply the international valuation standards (IVS).

The IVS formulation of market value is remarkably similar to the Spencer hypothetical market test:

The estimated amount [see section 7.2 below] for which an asset or liability should exchange

on the valuation date between a willing buyer and willing seller in an arm’s length transaction,

after proper marketing and where the parties had each acted knowledgeably, prudently and

without compulsion.

Because the two tests are so similar, the Spencer test and the IVS market value formulation to

produce similar amounts in most cases.

However, the two disciplines diverge in relation to a number of issues.

One of the points of divergence is in relation to special value to the purchaser.

Special value arises where an asset has particular value to one particular buyer that is above and

beyond the value to all other buyers. The classic example is a parcel of land that the neighbour wants

to acquire (eg, in order to expand their business operations).

The two tests produce divergent outcomes because the IVS rigidly respect the purely hypothetical

nature of the assumed market, whereas - as was seen in section 6 above - the Spencer test is applied

on a hybrid basis by taking into account evidence of real world matters.

7.2 Market value under the IVS

The IVS are very clear that market value excludes special value for valuation purposes.

Paragraph 30 of the 2013 IVS Frameworks and Requirements provides that:

The definition of market value shall be applied in accordance with the following conceptual

framework:

(a) the “estimated amount” refers to a price expressed in terms of money payable for the

asset in an arm’s length transaction. … This estimate specifically excludes an

estimated price inflated or deflated by special terms or circumstances such as

atypical financing, sale and leaseback arrangements, special considerations or

concessions granted by anyone associated with the sale, or any element of special

value. [emphasis added]

Special value is defined as follows:

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 34

An amount that reflects particular attributes of an asset that are only of value to a special

purchaser.

Special purchaser is defined as follows:

A particular buyer for whom a particular asset has special value because of advantages

arising from its ownership that would not be available to other buyers in a market.

Paragraphs 45 and 46 provide as follows:

Special value can arise where an asset has attributes that make it more attractive to a

particular buyer than any other buyers in a market. These attributes can include the physical,

geographic, economic or legal characteristics of an asset. Market value requires the disregard

of any element of special value because at any given date it is only assumed that there is a

willing buyer, not a particular willing buyer.

When special value is identified, it should be reported and clearly distinguished from market

value.

7.3 The case law position on special value

The argument for excluding special value from market value is that the neighbour is properly

characterised as an anxious buyer and so is discounted in applying the Spencer test.

The argument for including special value in market value is that doing so merely reflects the intended

operation of one or more of the following express Spencer assumptions that apply to the hypothetical

market:

all purchasers have full knowledge of the prevailing circumstances, including “the then present

demand for the asset”; and

the vendor is willing but not anxious so knows of particular appeal to the purchaser; and

the hypothetical purchaser will put the asset to its highest and best use.

There is significant case law support for the proposition that market value reflects special value to a

particular purchaser. An overview of that case law is provided below.

On this issue, valuers are much more disciplined than judges in preserving the intellectual purity of the

hypothetical market.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 35

7.3.1 The Marks article

The most comprehensive technical article addressing special value in a legal and tax context is

“Valuation Principles in the Income Tax Assessment Act” by Professor Bernard Marks of Bond

University.11

After a detailed survey of case law across a range of jurisdictions, Marks concludes that, to exclude

special value from market value “especially for the purposes of the application of the ITAA is incorrect

– indeed, it is contrary to well developed judicial doctrine in Australia, the United Kingdom and

Canada”.

In particular, Marks concludes that:

… the proposition that the special value which a person can obtain from an asset because of

its special adaptability or usefulness or because of the synergistic advantages is excluded

from market value cannot, on any proper analysis of the relevant law, be sustained. The last

time an appellate court directly and definitively supported that proposition was in 1898 [which

was subsequently] decisively overruled in Robinson Bros (Brewers) Limited v Durham County

Assessment Committee by the Court of Appeal in 193712

and the House of Lords the

following year.13

It is submitted that, on proper consideration, an Australian court would both quickly and

decisively recognise … that the exclusion of special value from market value in the

hypothetical market test was an ‘economic paradox’ and a ‘contradiction in terms’.

Marks’s article is over 20 years old. However, cases decided subsequently only fortify his conclusion.

The following sections contain a selection of the cases considered by Marks as well as cases decided

subsequently.

7.3.2 Clay’s case

Clay’s case is a UK land tax case.14

Facts

C owned land which was subject to land tax based on its “gross value”

gross value was defined in a similar way to the Spencer test

if used as a private residence, the land had a value of £750

however, the land was located adjacent to a nurses home

11 Bond Law Review Vol 8, Issue 2, 1996. Available at http://epublications.bond.edu.au/blr/vol8/iss2/2

12 [1937] 2 KB 445.

13 [1938] AC 321.

14 Inland Revenue Commissioners v Clay [1914] 3 KB 466

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 36

there was evidence that the nurses home was willing to pay £1000 (unlike Spencer where there

was no evidence of demand for the land to be used as a factory)

Held

the gross value of the land was £1000, not £750

Reasoning

there is no basis for excluding from the market value of an asset the price that a special purchaser

is prepared to pay for it

Relevant quotes

I can see no ground for excluding from consideration the fact that the property is so situate that to

one or more persons it presents greater attractions than to anybody else. The house or the land

may immediately adjoin one or more landowners likely to offer more than the property would be

worth to anybody else. This is a fact which cannot be disregarded …15

An “open market” sale of property “in its then condition” presupposes a knowledge of its situation

with all surrounding circumstances. To say that a small farm in the middle of a wealthy

landowner’s estate is to be valued without reference to the fact that he will probably be willing to

pay a large price, but solely with reference to its ordinary agricultural value, seems to me absurd.

If the landowner does not at the moment buy, land brokers or speculators will give more than its

purely agricultural value with a view to reselling it at a profit to the landowner.16

The Solicitor-General contended that as the section said “if sold at the time in the open market”,

the price which only one particular buyer was prepared to pay must be excluded from all

consideration; it might possibly be a fancy price which had no relation to market price; that a

reference to open market shewed that the statute referred to a current market price of land, a

price which one or more valuers might determine to be the market value of the land.

In my opinion this contention is unsound. A value, ascertained by reference to the amount

obtainable in an open market, shews an intention to include every possible purchaser … it is

common knowledge … that when the fact becomes known that one probable buyer desires to

obtain any property, that raises the general price or value of the thing in the market. Not only is

the probable buyer a competitor in the market, but other persons, such as property brokers,

compete in the market for what they know another person wants, with a view to a resale to him at

an enhanced price, so as to realize a profit. A vendor desiring to realize any land would ordinarily

give full publicity to all facts within his knowledge likely to enhance the price.17

[There is an] important question of principle in dispute … The Crown contends that in estimating

the gross value of land … I must exclude the price which one particular buyer will give because of

his particular need; that this is not the price in “the open market”; and that the willing seller must

be willing to sell at a market price, not a fancy price. The Solicitor-General relied on the course of

15 Lord Cozens-Hardy MR at p472

16 ibid

17 Swinfen Eady LJ at p474-475:

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 37

authorities summarized in Lucas … that in assessing compensation … for compulsory purchase

you cannot consider the special need of the compulsory purchaser; the existence of the scheme

cannot enhance the value of the lands to be purchased under it. This is true, but it is also true

that if there are other possible purchasers besides the compulsory purchaser, even in such a

case the competition of special needs may be taken into account in fixing the compensation to the

vendor … [the vendor] is not required to exclude the principal bidder from his market, because

that principal bidder wants the house [more] than any one else and will therefore give more for it

… the obvious business way to look at the transaction [is that] I cannot exclude from the “open

market” the principal buyer, though for a genuine business reason he will pay a price higher than

others.18

7.3.3 Vyricherla

Vyricherla is a Privy Council resumption compensation case.

The facts are complex and not ultimately relevant.

What is relevant is the following Lord Romer quote at 314 which was cited with approved in several

High Court decisions:19

Take as an example the case of an owner of a vacant land that adjoins his factory. The land

possessed the potentiality of being profitably used for an extension of the factory. But the

owner is the only person who can turn that potentiality to account.

In valuing the land, however, as between him and a willing purchaser, the value to him of the

potentiality would necessarily have to be included.

7.3.4 Brisbane Water County Council

In Brisbane Water County Council, Waddell J held that:

… the ordinary meaning of the term “market value” is the best price which may reasonably be

obtained for the property to be valued if sold in the general market. The cases cited indicate

that where the “value” of an item of property is to be ascertained, this means its value in the

general market with three qualifications. Firstly, if there is no general market, as in the case of

shares in a private company, such a market is to be assumed. Secondly, all possible

purchasers are to be taken into account, even a purchaser prepared for his own reasons to

pay a fancy price. [emphasis added]

18 Scrutton J at p348-349

19 Geita Sebea v Territory of Papua (1941) 67 CLR 544; McClintock v Cth (1947) 75 CLR 1; Nelungaloo Pty Ltd v Cth (1948) 75

CLR 495; Cth v Arklay (1952) 87 CLR 159; Turner v Minister for Public Instruction (1956) 95 CLR 245; Collins v Lingstone Shire

Council (1972) 127 CLR 477; Brisbane City Council v Valuer-General (Qld) (1978) 140 CLR 41.

Tim Kyle The Legal Meaning of “Market Value”

© Tim Kyle 2016 38

7.3.5 MMAL Rentals

The facts in MMAL Rentals are set out in section 5.4.3 above.

A strong NSW Court of Appeal bench (Spigelman CJ, with whom Mason P and Hodgson JA agreed)

held that the value of the Thrifty shares had to take into account the special potentiality to MMAL (the

80% shareholder) of preventing another minority shareholder from acquiring those shares (eg for

greenmail purposes).

This was because special potentiality (ie, special value) to a particular purchaser should not be

excluded from the exchange value test of market value even where that purchaser is the only

purchaser. That is, to exclude a special purchaser would be to contravene the Spencer approach,

and the Spencer approach properly included such a special purchaser.

Spigelman CJ said:

[A special purchaser] represents the operation of a market and does so even if called

greenmail. This is not an exception to the exchange bargain test established by Spencer’s

case. It is an application of the test involving the determination of how a willing vendor of a

minority interest would behave … It is well-established that if property has some special

potentiality which only one person would buy, it is to be valued on the basis of a notional sale

to that person. The property is not valueless or diminished in value because there would be

no other buyers. [emphasis added]

The Court of Appeal disposed of the proceedings by applying Spencer, and so the application of the

Clay principle as part of the Spencer exchange value test is critical to the ratio of this case.

7.3.6 Boland v Yates