national solar water heater programme roll out strategy to portfolio committee on small business...

TRANSCRIPT

National Solar Water Heater Programme Roll Out Strategy

To

Portfolio Committee on Small Business Development

05 November 2014

Presented by: Mokgadi Modise Chief Director: Clean Energy

1

2

Outline

1. Background and context

2. National Solar Water Heater Programme Objectives

3. Sequence of Events

4. National Solar Water Heater Programme Implementation Approach

5. Funding for the National Solar Water Heater Programme

6. Progress to date on the Status of SWH localisation

7. Opportunities for Energy Services Companies

8. Conclusion

Background & Context• Improving energy efficiency has long been advocated as a way to increase the

productivity and sustainability of society, primarily through the delivery of energy

savings. In 2009, the DoE in its budget vote speech pronounced on 1 million

SWH units installed over a five year period.

• In 2005, the South African National Energy Efficiency Strategy was developed

and published to explore potentials for improved energy utilisation through

reducing the country’s energy intensity, and decoupling economic growth from

energy demand.

• The SA’s Energy Efficiency Strategy states the aspirational targets for the

respective broad energy-use sectors as a percentage improvement in energy

intensity to be achieved relative to a baseline, projected from the baseline year

of 2000, and energy intensity reduction by 2015.

3

4

Objective Interventions Target Outcome1 Reducing electricity

demand by transferring the water heating load from the grid to a renewable energy source (solar)

Facilitation of switching from electric geysers to SWH in high consumption domestic segment

5 million high income households converted to SWHs

Reduced electricity demand in the residential segment defers power station investment

2 Mitigation of adverse climate change through an environmentally benign technology for water heating

Installation of SWH in the low- and high-income domestic segments

9.6 million low and high income households who use electricity for water heating

Increased uptake of clean energy for water heating purposes

3 Cushioning the poor from rising electricity tariffs

Universal access in the domestic low income segment

4.6 million low income households who use electricity and other no-conventional means for water heating

Reduction in the domestic electricity bill due to water heating being provided by SWH

4 Facilitating the creating of job opportunities through increased local manufacturing and industrialization

Setting up minimum thresholds for local content through the designation of the SWH Industry.

Not less than 70% local content on tanks and 70% local content on collectors

Manufacturing of SWH technology localized & imports phased out.

National Solar Water Heater Programme Objectives

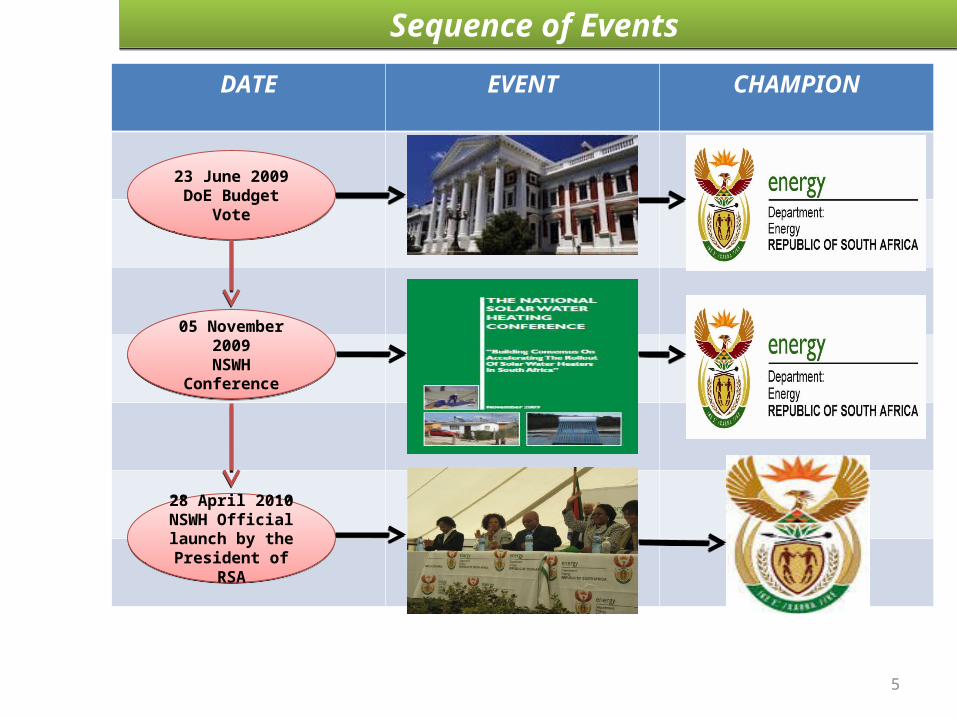

Sequence of Events Sequence of Events

5

DATE EVENT CHAMPION

23 June 2009DoE Budget Vote

23 June 2009DoE Budget Vote

05 November 2009NSWH Conference05 November 2009NSWH Conference

28 April 2010NSWH Official launch by the

President of RSA

28 April 2010NSWH Official launch by the

President of RSA

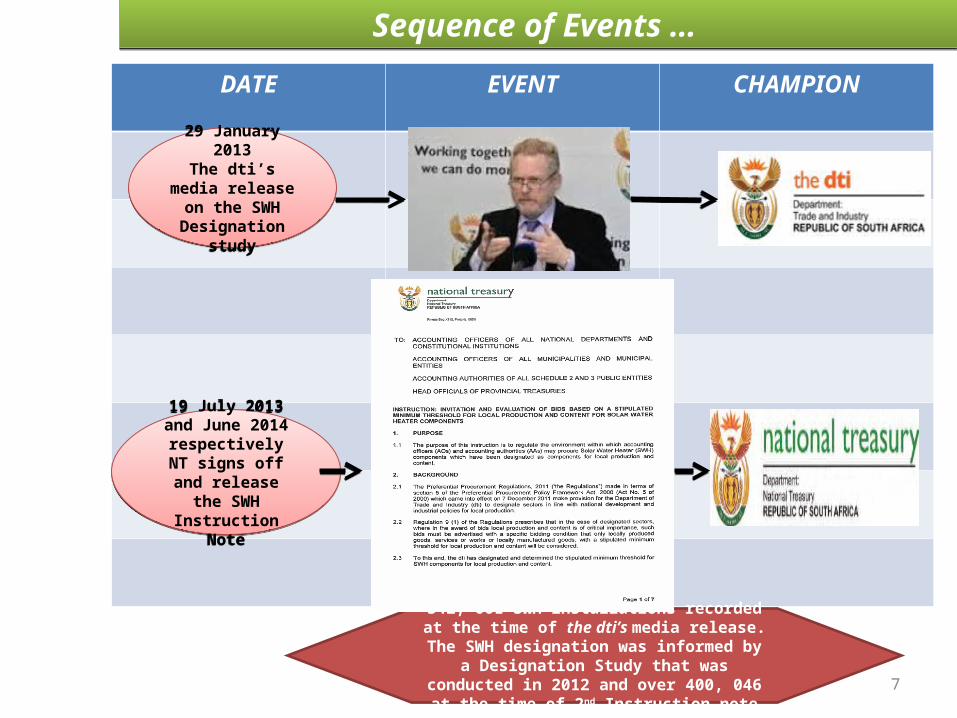

Sequence of Events … Sequence of Events …

6

DATE EVENT CHAMPION

17 November 2011Green Economy Accord signing

17 November 2011Green Economy Accord signing

22 February 2012Budget Speech :

NSWH Appropriation

22 February 2012Budget Speech :

NSWH Appropriation

31 December 2012SWH Rebate

programme ended

31 December 2012SWH Rebate

programme ended

R4.7bn

Sequence of Events … Sequence of Events …

7

DATE EVENT CHAMPION

29 January 2013The dti’s media release on the

SWH Designation study

29 January 2013The dti’s media release on the

SWH Designation study

342, 001 SWH installations recorded at the time of the dti’s media release. The SWH designation was

informed by a Designation Study that was conducted in 2012 and over 400, 046 at the time of

2nd Instruction note

19 July 2013 and June 2014

respectivelyNT signs off and release the SWH Instruction Note

19 July 2013 and June 2014

respectivelyNT signs off and release the SWH Instruction Note

Funding for the NSWH Programme

• On 14 February 2012, the Minister of Finance announced a 1 cent per kilowatt hour increase on the

Environmental Levy as a new mechanism that “will replace the current funding mechanism for

energy efficiency initiatives such as the solar water geyser programme”.

• The anticipated revenue to be collected through the levy increase over a three year period is about

R4.7bn.

• The above mentioned on-budget allocation (R4.7bn) was made through the Appropriation Act, 2012

(Act No 7 of 2012), via the DoE’s Vote, as an exclusive and specific allocation to Eskom. To facilitate

implementation of the now DoE-funded NSWHP, the DoE and Eskom entered into a Memorandum

of Agreement (MoA) that was signed on 06 November 2012, and a revised MoA covering Medium

Term Expenditure Framework (2013/14, 2014/15 and 2015/16 financial years) was signed in

January 2014.

• The agreed new SWH Contracting Model, will now for the first time allow Eskom to enter into longer

term supply contracts with local SWH manufacturers that comply with the SWH industry designation

requirement of a minimum of 70% local content on tanks and 70% local content on collectors.

• It is envisaged that such contracts will provide the local industry with the much-needed investment

certainty for justifying setting up of local SWH manufacturing facilities.

8

SWH Installation Progress as of 30 SEPTEMBER 2014

9

Data Source, Eskom. DoE does not have reakdown of the installation data

IMPLEMENTATION CHALLENGES

• After the Instruction Note was issued by National Treasury, the roll out could not

proceed outside these requirements;

• Local Content Verification had to be undertaken in terms of SATS 1286;

• Delays in rolling out on the basis of the MoA

• Risks that funding would not be utilised

• Details to be presented after Cabinet consideration

10

ANALYSIS AND REVIEW OF THE PREVIOUS SWH DELIVERY MODEL

• The following were problems identified with the previous low-pressure SWH delivery model:

– There is little impact on electricity demand and local manufacturing as aspiring local manufacturers

cannot secure contracts that are huge enough to justify the investment;

– There is no technology standardization as a result too many different and mainly imported products

are available;

– The most prevalent SWH technology installed is evacuated tube type, whilst flat plates are not being

utilised although they have potential for localisation;

– Measuring the local content of SWH products is difficult with no technology standardisation; and

– The life cycle management of installed SWH systems is either inadequate or non-existent, particularly

with respect to the provision of post-installation services.

– The distribution of the current installations is skewed towards certain provinces due to the following

reasons:

• The majority of the current SWH footprint have been funded through an electricity tariff and delivered

through a first come first serve capital subsidy scheme (the rebate programme) implemented by Eskom,

thus not allowing for an equitable pre-selection of installation areas;

• To quickly access the rebate, service providers approached municipalities and secured approvals for

signing up interested households within the municipal jurisdictions and once again this resulted in SWH

installations largely happening in metropolitan areas as most service providers were not keen to operate

in areas in which they have no presence i.e. mostly in rural municipalities;

11

ANALYSIS AND REVIEW OF THE PREVIOUS SWH DELIVERY

MODEL[2]

• Logistical constraints most common in the poorest provinces of the country prompted service providers

to rather prioritise operating in major towns than in far flung areas; and

• This preference led to installations that are skewed in favour of provinces such as Gauteng, Kwa-Zulu

Natal, Eastern Cape and Western Cape whilst others such as Limpopo, North West, Mpumalanga and

Northern Cape remained least served.

• Against the foregoing discussion, the DoE is now adopting a redress approach in tackling

this problematic provincial spread of installations. For example, with the 2013/14 and

2014/15 financial years’ allocation funding has also been allocated in a manner that

prioritises South Africa’s 23 Least Developed Districts whilst having due regard for the water

quality and water reticulation status of these districts.

• New contracting model has thus been developed having due regard of the above.

12

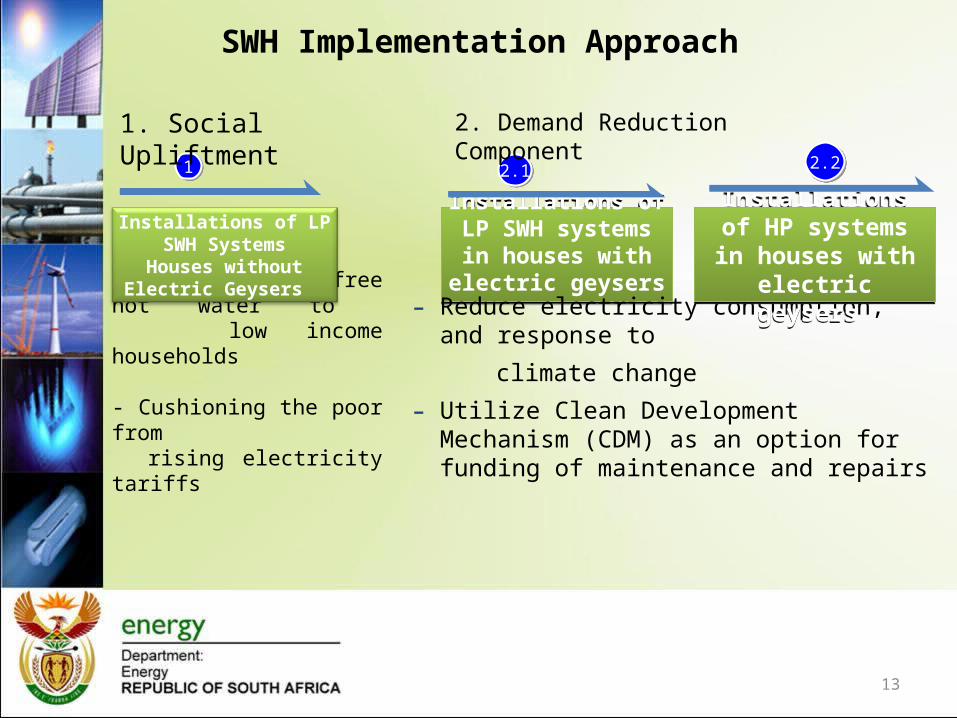

- Provision of free hot water to low income households

- Cushioning the poor from rising electricity tariffs

13

Installations of LP SWH Systems

Houses without Electric Geysers

11

Installations of LP SWH systems in houses with

electric geysers

Installations of LP SWH systems in houses with

electric geysers

2.12.1

- Reduce electricity consumption, and response to

climate change- Utilize Clean Development Mechanism (CDM) as

an option for funding of maintenance and repairs

Installations of HP systems in houses with

electric geysers

Installations of HP systems in houses with

electric geysers

2.22.2

SWH Implementation Approach

2. Demand Reduction Component 1. Social Upliftment

14

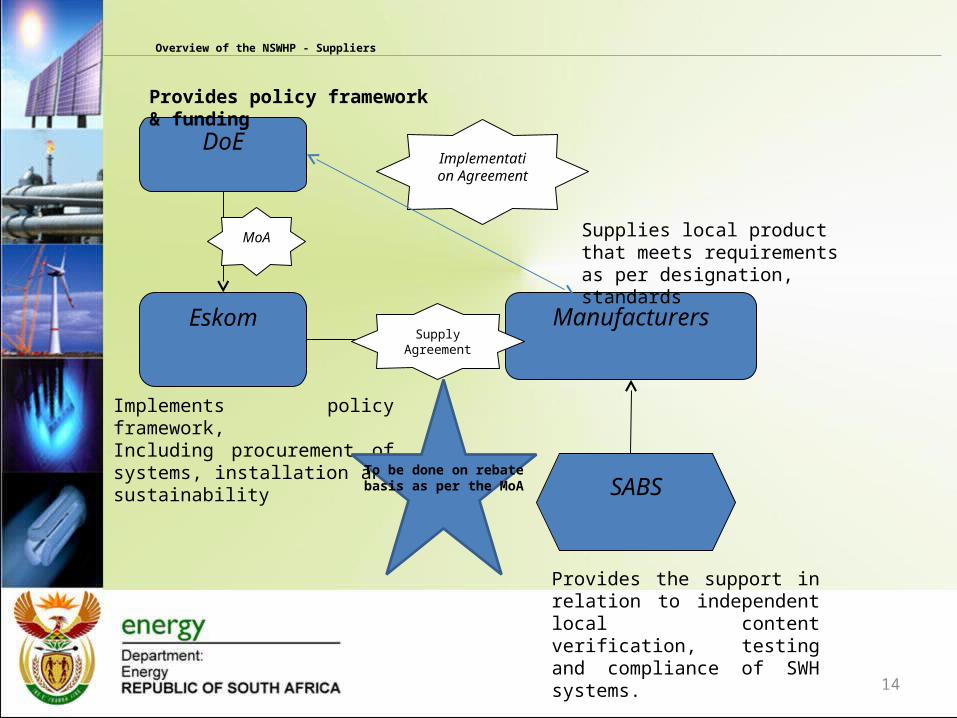

Overview of the NSWHP - Suppliers

Eskom Manufacturers

SABS

DoE

Provides policy framework & funding

Implements policy framework, Including procurement of systems, installation and sustainability

Supplies local product that meets requirements as per designation, standards

Provides the support in relation to independent local content verification, testing and compliance of SWH systems.

MoA

Supply Agreement

Implementation Agreement

To be done on rebate basis as per the MoA

15

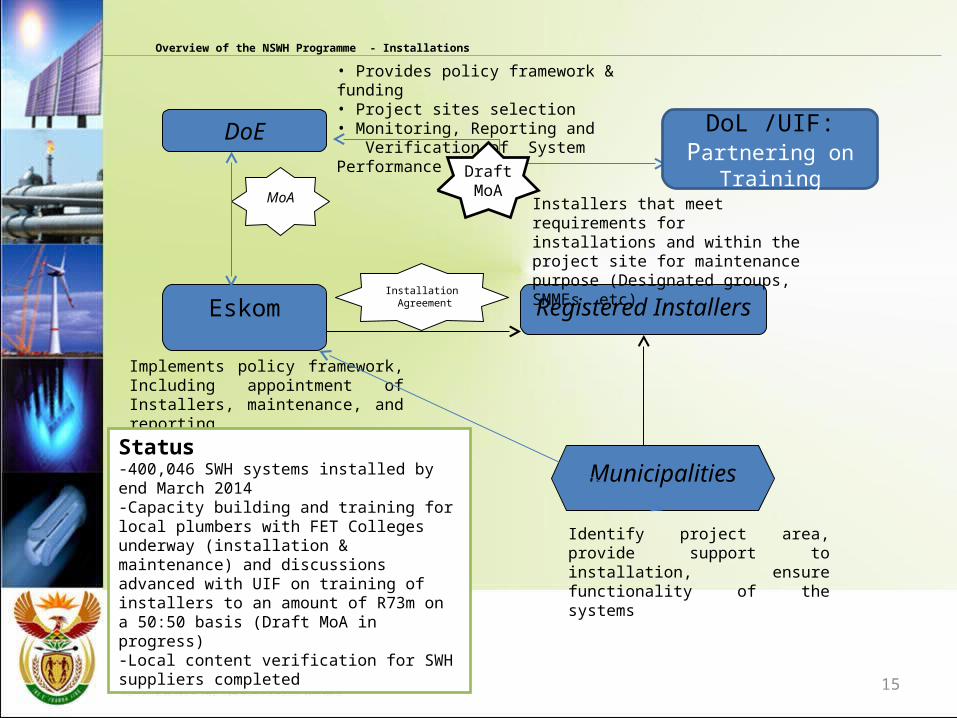

Overview of the NSWH Programme - Installations

Eskom Registered Installers

Municipalities

DoE

• Provides policy framework & funding • Project sites selection • Monitoring, Reporting and Verification of System Performance

Implements policy framework, Including appointment of Installers, maintenance, and reporting

Installers that meet requirements for installations and within the project site for maintenance purpose (Designated groups, SMMEs, etc)

Identify project area, provide support to installation, ensure functionality of the systems

MoA

Installation Agreement

Status-400,046 SWH systems installed by end March 2014 -Capacity building and training for local plumbers with FET Colleges underway (installation & maintenance) and discussions advanced with UIF on training of installers to an amount of R73m on a 50:50 basis (Draft MoA in progress)-Local content verification for SWH suppliers completed

DoL /UIF: Partnering on

TrainingDraft MoA

New Growth Path: Accord 4: Green Economy Accord Commitment on SWH

• The Green Economy Accord signed by Government and its Social Partners outlines the

following on Commitment One: Rollout of Solar Water Heaters

• Accordingly, parties committed the following:

(1) Increase the roll out of one million units

(2) Improve localisation of the components

(3) Secure support from the insurance industry for replaced units

(4) Secure guarantees in installed units

(5) Promote the marketing of solar water heating systems

(6) Promote uniform technical and performance standards for SWH

16

Progress to Date on the Status of SWH Localisation…

DoE recognised as a “Champion for Local Content”

Progress to Date on the Status of SWH Localisation

• In the beginning, the NSWH programme was dominated by imported units which ultimately,

and to some extent, did not create flexibility for the programme to achieve all the much

needed and committed competing national objectives.

• Consequently, the low-pressure SWH rebate programme was discontinued as from

December 2012 and is being replaced by the New Contracting Model. The proposed SWH

New Contracting Model is aimed at promoting local manufacturing and development of

Small Medium Micro Enterprises (SMMEs) largely as installers within the SWH value chain.

• The localisation objective was intensified and affirmed by the designation of solar water

heating as an industry. The designation seeks to define and determine the level of local

content on solar geysers and as such the tanks and collectors as of August 2013 were

indeed designated as per the SWH Instruction Note released by National Treasury.

• In order to allow local manufacturers ample time to ramp up production capacity necessary

to meet local demand, about R700m from the combined allocations for the 2013/14 and

2014/15 financial years has been shifted to the outer year 2015/16 financial year.

18

Indicative NSWHP Allocations

19

2012/13 2013/14 2014/15 2015/16MPUMALANGA R 72 000 000.00 R 202 077 000.00 R 116 150 789.00 R 49 685 622.00NORTH WEST R 72 000 000.00 R 157 167 000.00 R 112 378 175.00 R 48 071 818.00LIMPOPO R 56 000 000.00 R 202 077 000.00 R 159 478 692.00 R 68 219 925.00KWAZULU NATAL R 56 000 000.00 R 100 359 000.00 R 310 154 618.00 R 132 674 305.00FREE STATE R 48 000 000.00 R 157 167 000.00 R 101 288 976.00 R 43 328 210.00NORTHERN CAPE R 40 000 000.00 R 134 712 000.00 R 36 697 247.00 R 15 697 918.00WESTERN CAPE R 40 000 000.00 R 112 266 000.00 R 175 255 079.00 R 74 968 562.00EASTERN CAPE R 35 760 000.00 R 112 266 000.00 R 203 721 168.00 R 87 145 452.00GAUTENG R 32 000 000.00 R 89 811 000.00 R 421 275 255.00 R 180 208 188.00

TOTAL R 451 760 000.00 R 1 267 902 000.00 R 1 636 399 999.00 R 700 000 000.00

PROVINCESALLOCATIONS

INDICATIVE PROVINCIAL SWH ALLOCATIONS (For Load Reduction)INDICATIVE PROVINCIAL SWH ALLOCATIONS (For Load Reduction)

DoE URGES MUNICS TO ACTIVELY PARTICIPATES IN THE RFIs

21

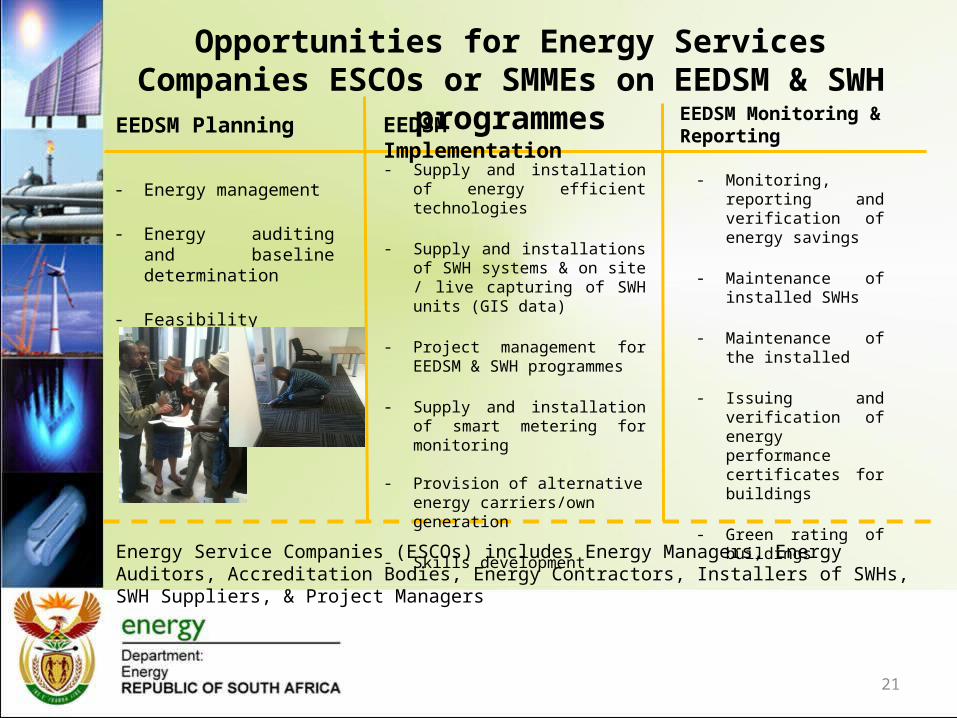

Opportunities for Energy Services Companies ESCOs or SMMEs on EEDSM & SWH programmes

EEDSM Planning EEDSM Implementation

Energy Service Companies (ESCOs) includes Energy Managers, Energy Auditors, Accreditation Bodies, Energy Contractors, Installers of SWHs, SWH Suppliers, & Project Managers

- Supply and installation of energy efficient technologies

- Supply and installations of SWH systems & on site / live capturing of SWH units (GIS data)

- Project management for EEDSM & SWH programmes

- Supply and installation of smart metering for monitoring

- Provision of alternative energy

carriers/own generation

- Skills development

- Energy management

- Energy auditing and baseline determination

- Feasibility studies for SWH programme

- Monitoring, reporting and verification of energy savings

- Maintenance of installed SWHs

- Maintenance of the installed

- Issuing and verification of energy performance certificates for buildings

- Green rating of buildings

EEDSM Monitoring & Reporting

NSWHP Monitoring and Evaluation

• To facilitate this process the provincial spread concern, the department issued a request for

information to establish primarily the water quality of the different municipalities. However,

many municipalities in the least performing provinces have not been responsive in providing

the crucial pre-feasibility data to guide municipal allocations.

• The following are some of the major monitoring and evaluation activities of the NSWHP:

– The DoE is responsible for conducting the initial screening and pre-feasibility

assessments (water quality, water reticulation, etc.) in various municipalities in order to

ensure that the selected project sites have no fatal flaws and other risks that could

have been avoided.

– The DoE and Eskom will ensure that systems installed will be tracked and

geographically mapped, to facilitate monitoring and management of programme;

– Eskom will conduct detailed feasibility studies plus measurement and verification of

energy savings and other socio-economic aspects;

22

NSWH programme Monitoring and Evaluation [2]

• The Department of Higher Education and Training, the relevant Sector Education

and Training Authorities (SETAs), Eskom and Municipalities will ensure that

installation companies across all provinces are accredited and also registered

with the DoE; and

• The DoE and SABS will conduct technical audits of the SWH systems to

evaluate their performance and monitor non-functional systems.

23

Conclusion

• It is recommended that the Portfolio Committee on Small Business Development:

• Notes that the upfront capital costs of the SWH systems have, and continue to be, one

of the major barriers to wide spread dissemination of SWH systems;

• Notes that the jobs within the Solar Water Heater industry are created at various levels

of the value chain with most jobs during installation and maintenance

• Notes progress on installation to date; and

• Notes implementation problems experienced and the review of model underway.

24

Mokgadi ModiseChief Director: Clean Energy

Tel: +27 (0) 12 406 7712Cell: +27 (0) 82 449 7550

Email: [email protected] Website: www.energy.gov.za

25