navigating choppy waters opportunities and … choppy waters – opportunities and challenges in the...

TRANSCRIPT

www.nsr.com © 2016 – NSR

Claude Rousseau

Research Director

Northern Sky Research

Navigating Choppy Waters – Opportunities and Challenges in the Shipping Industry

Intelsat Briefing, Digital Ship @Posidonia

8th June 2016

Athens, Greece

www.nsr.com © 2016 – NSR

About NSR

Maritime Satcom Market

• Addressable Markets

• Market Overview

• Broadband Maritime Markets

• Similarities with Aircraft Connectivity

• Merchant Maritime – Satcom Value Proposition

Challenges & Opportunities

• Applications

• Revenues Opportunities

• Non-Broadband != ‘Unconnected’

• Bigger & Better

• Addressable Markets and Forecasts

• Market Outlook and Strategic considerations

Agenda

June 2016 NSR Presentation 2

www.nsr.com © 2016 – NSR

About NSR

www.nsr.com © 2016 – NSR

About NSR

Intelsat Briefing @ Digital Ship Posidonia

NSR is a Global Leader in Satellite Market Research and Consulting

Founded in 2000, NSR specializes in analysis of growth

opportunities across the satellite industry

NSR’s expert consultants are located globally and possess over 140 years of combined

industry experience.

Multi-Client Reports on Various Satellite Topics

Extensive Client Research, Consulting and Advisory Services

“Holistic” approach to research enables NSR to anticipate trends with a higher

degree of confidence and precision than the competition and stay ahead of the curve.

www.nsr.com

June 2016 NSR Presentation 4

www.nsr.com © 2016 – NSR

Fixed Applications &

Capacity Analysis

June 2016

The NSR Team

Intelsat Briefing @ Digital Ship Posidonia

Chris Baugh

President

Carlos Placido

Senior Analyst

Claude Rousseau

Research Director

Jose Del Rosario

Research Director

Kristen Kloster

Marketing Manager

Ken Marini

Director

Alan Crisp

Analyst

Blaine Curcio

Senior Analyst

Lluc Palerm-Serra

Analyst

Brad Grady

Senior Analyst

Dallas Kasboski

Analyst

Prateep Basu

Analyst

Mobility Applications &

Commercial Space

Carolyn Belle

Senior Analyst

NSR Presentation 5

www.nsr.com © 2016 – NSR

NSR Market Research Reports

Intelsat Briefing @ Digital Ship Posidonia

NSR’s reports present an independent view of the markets

It is a tool for strategic business planning.

Our equal emphasis on both market based issues and technology trends allow

our clients to create comprehensive plans for the future.

Topics:

• Global Satellite Capacity & Supply Demand

• Government and Military Satellite Communications

• Maritime Satellite Services

• Aeronautical Satcom Markets

• Linear TV

• Wireless Backhaul via Satellite

• Global Satellite Manufacturing and Launch Markets

• Oil and Gas via Satellite

• Satellite Operator Financial Analysis

• VSAT and Broadband Satellite Markets

• M2M and IoT via Satellite Markets

• Nano and Microsatellite Markets

• Global Satellite-Based Earth Observation

• Flat Panel Satellite Antennas

June 2016 NSR Presentation 6

www.nsr.com © 2016 – NSR

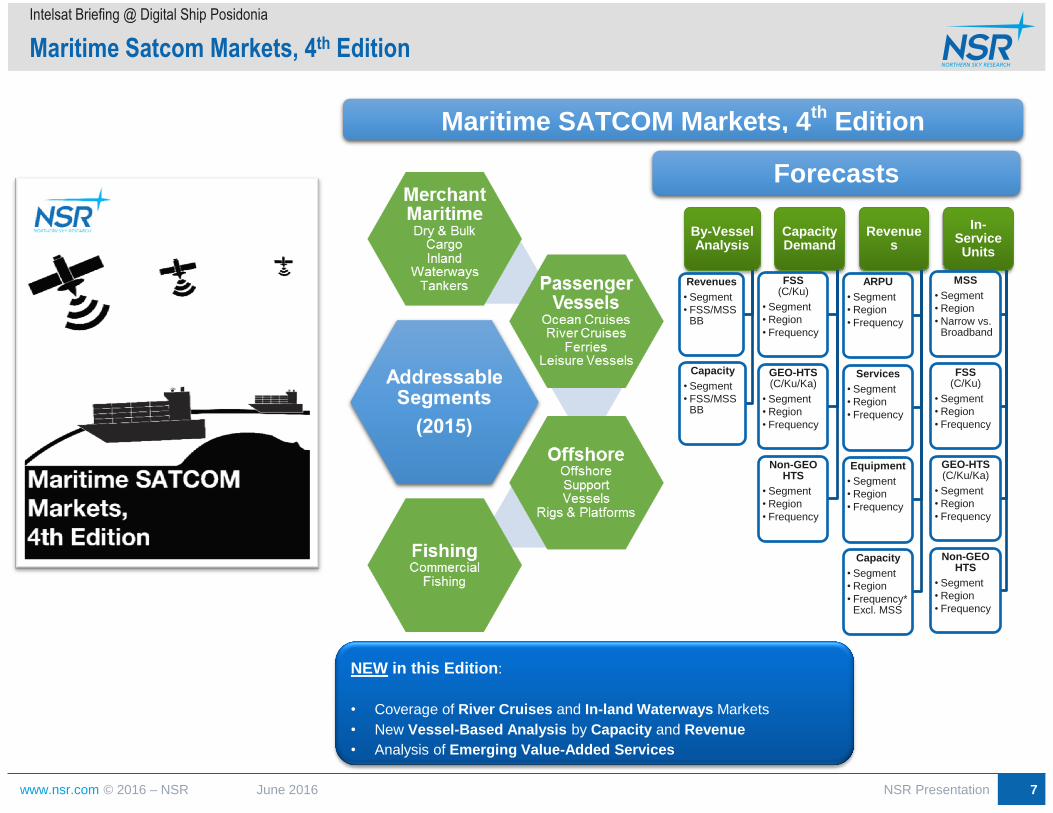

Maritime Satcom Markets, 4th Edition

Intelsat Briefing @ Digital Ship Posidonia

June 2016

Off

sh

ore

NSR Presentation 7

NEW in this Edition:

• Coverage of River Cruises and In-land Waterways Markets

• New Vessel-Based Analysis by Capacity and Revenue

• Analysis of Emerging Value-Added Services

Maritime SATCOM Markets, 4th

Edition

Forecasts

In-Service Units

MSS

• Segment

• Region

• Narrow vs. Broadband

FSS (C/Ku)

• Segment

• Region

• Frequency

GEO-HTS (C/Ku/Ka)

• Segment

• Region

• Frequency

Non-GEO HTS

• Segment

• Region

• Frequency

Revenues

ARPU

• Segment

• Region

• Frequency

Services

• Segment

• Region

• Frequency

Equipment

• Segment

• Region

• Frequency

Capacity

• Segment

• Region

• Frequency* Excl. MSS

Capacity Demand

FSS (C/Ku)

• Segment

• Region

• Frequency

GEO-HTS (C/Ku/Ka)

• Segment

• Region

• Frequency

Non-GEO HTS

• Segment

• Region

• Frequency

By-Vessel Analysis

Revenues

• Segment

• FSS/MSS BB

Capacity

• Segment

• FSS/MSS BB

www.nsr.com © 2016 – NSR

Maritime Satcom Markets

www.nsr.com © 2016 – NSR

Addressable Market

Intelsat Briefing @ Digital Ship Posidonia

June 2016

Maritime Addressable MarketsNSR's Maritime SATCOM Markets, 4th Edition

430,000

390,000

343,000

2015

2020

2025

Maritime

Addressable Market

Merchant Maritime

Passenger Vessels

Offshore

Fishing

Merchant Maritime

Passenger Vessels

Offshore

Fishing

Off

sh

ore

Evolving Addressable:

Fishing provides a weak opportunity for satcom services, and outlook is unlikely to significantly change.

Merchant maritime faces vessel oversupply challenges which has ripple effects through how vessel owners approach operations.

Passenger is dominated by ‘leisure’ (specifically smaller leisure vessels) that, like fishing, are weaker adopters of SATCOM services.

Offshore is largely ‘reset’, which means fewer sites to connect but not offset by the remaining sites requiring more capacity.

NSR Presentation 9

www.nsr.com © 2016 – NSR

More VSAT-enabled Vessels

– A steady rise in the amount of VSAT-connected vessels over the forecast period fuels the ubiquity of ‘always-on’ connectivity in

the maritime sector.

– Passenger Vessels (driven by huge demand in the ocean-going cruise segment) and Offshore drive strong capacity

demand. With already strong adoption of VSAT technologies, these ‘early adopter’ markets could be a sign of where

merchant and even fishing markets are heading.

Broadband vs. Non-Broadband Maritime Markets

Intelsat Briefing @ Digital Ship Posidonia

June 2016

Merchant Maritime

Passenger Vessels

Offshore

Fishing

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

$D

olla

rs P

er

Mo

nth

Average Revenue Per Month for Maritime Broadband by Vessel

Source: NSR

NSR Presentation 10

www.nsr.com © 2016 – NSR

Similarities with Aircraft Connectivity

Intelsat Briefing @ Digital Ship Posidonia

June 2016 NSR Presentation 11

Source: maritimetraffic.com Source: ESA

Aeronautical Traffic Patterns Maritime Traffic Patterns

Aero+Maritime routes

will continue to push

high-utilization rates for

HTS spot-beam

capacity.. But each

vertical has their own

individual ‘hot-spots’.

For Maritime,

Africa+IOR is a unique

area for SPs to acquire

capacity.

For Aero, Northern

Atlantic Route will see

‘heavy’ traffic

Maritime-

Heavy Area

Aero-Heavy

Area

www.nsr.com © 2016 – NSR

Similarities with Aircraft Connectivity

Intelsat Briefing @ Digital Ship Posidonia

June 2016

Airline Connectivity Model Transitioning to Whole Aircraft Connectivity

NOW

Difference in needs for cockpit and cabin

– Cockpit : L-band systems certified for safety

(FANS) and operational services (Swift64,

Iridium)

– Cabin: ATG, Ku-, L-, and Ka-band HTS

Traditional model, with low storage and data

transfer rate capabilities with growing bandwidth

demand

Tomorrow

Migration of cabin connectivity to HTS as

available capacity supply comes online (GX,

ViaSat-1, -2 & -3, KA-sat, EPIC series, etc..)

Cockpit communications to continue on L-band

for safety.

Next generation broadband services could lead to

migration away from ACARS and towards IP-

based communications with M2M interactions.

Electronic Flight

Bag

Internet Access

Entertainment

Engine Monitoring

Maintenance

Cockpit Communications Cabin & Crew Communications

Migration of cabin connectivity to HTS - Cockpit Communications on L-band

Next-Generation Broadband Systems - Wi-Fi as a Necessary Service –

More Data Off the Aircraft While In-Flight

Voice Calls, texting,

NSR Presentation 12

www.nsr.com © 2016 – NSR

State of the Market

Intelsat Briefing @ Digital Ship Posidonia

June 2016 NSR Presentation 13

By 2025

• Service Providers need access to all types of capacity.

• Vessels doubling their bandwidth demand.

Near-Term

• More throughput for More Apps.

• Sometimes, my Service Provider should provide the app.

Today

• Connectivity is becoming a “Must-have”.

• Lower Pricing is Making that Achievable. Today.

Today through Tomorrow

• Broadband Adoption on the rise – in both VSAT and MSS.

• Spending on a vessel basis for connectivity is largely flat.

• A shift towards more “apps” or “outsourced” activities on-board the vessel.

Merchant Shipping

A Look at Merchant Maritime

www.nsr.com © 2016 – NSR

Merchant Maritime – Satcom Value Proposition

June 2016

ERP

Business Optimization

Vessel Monitoring Crew Calling

Streaming Media Crew Internet

VOD

Live TV E-Learning

Revenue and Capacity Revenue Opportunities Capacity Opportunities

Intelsat Briefing @ Digital Ship Posidonia

2015 2025

Merchant In-service Units MSS-BB

Non-GEO HTS

GEO-HTS, Ka-Band

GEO-HTS, Ku-band

GEO-HTS, C-band

FSS Ku-band

FSS C-band0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Broadband vs. Non-Broadband Maritime Vessels

2015 Additions through 2025 Non-Broadband Vessels Source: NSR

NSR Presentation 14

www.nsr.com © 2016 – NSR

Challenges & Opportunities

www.nsr.com © 2016 – NSR

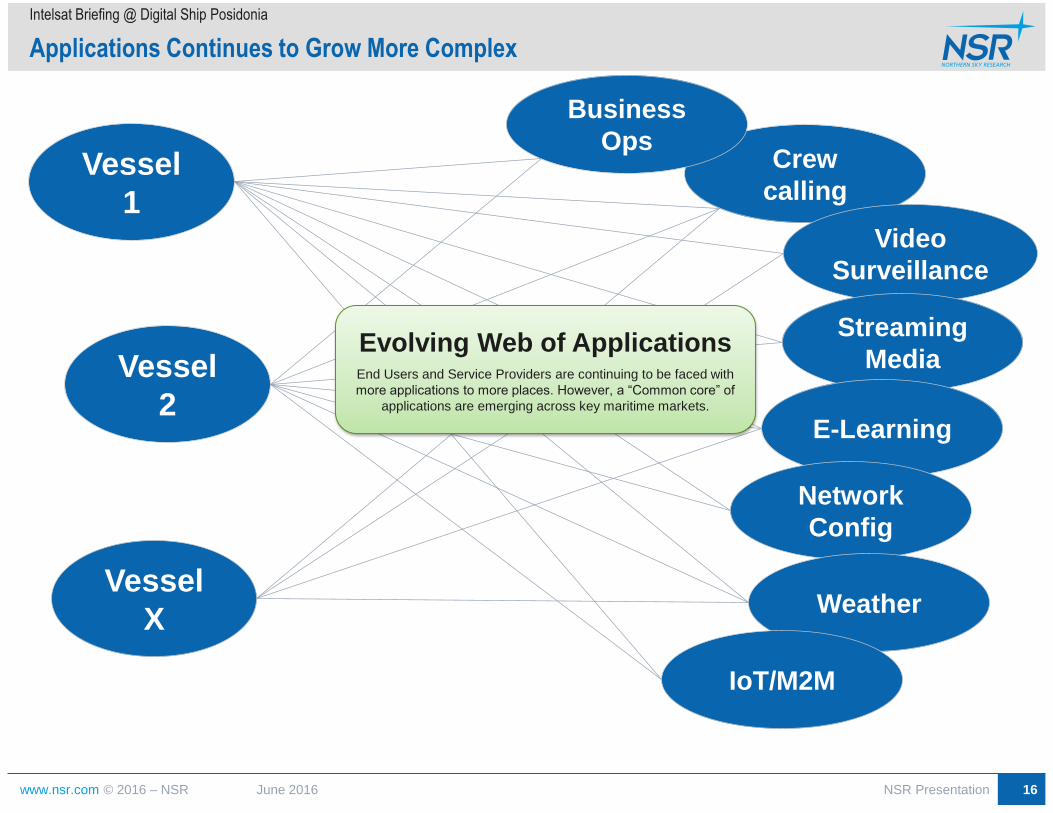

Applications Continues to Grow More Complex

Intelsat Briefing @ Digital Ship Posidonia

June 2016

Vessel

1

Vessel

2

Crew

calling

Video

Surveillance

Streaming

Media

Business

Ops

E-Learning

Network

Config

Weather

IoT/M2M

Vessel

X

Evolving Web of Applications End Users and Service Providers are continuing to be faced with

more applications to more places. However, a “Common core” of

applications are emerging across key maritime markets.

NSR Presentation 16

www.nsr.com © 2016 – NSR

SP’s Server

Ship

Business

Crew

End-user Server

Revenues Opportunities?

Intelsat Briefing @ Digital Ship Posidonia

June 2016

How Should these

Areas be

Monetized?

“Monetizing the bytes”

Service Providers are increasingly adding

their own server infrastructure ‘behind the

modem’ to get closer to an application-

centric revenue stream.

Closer End-user

Interaction Than

Ever Before

NSR Presentation 17

www.nsr.com © 2016 – NSR

0 20,000 40,000 60,000 80,000

Merchant Maritime

Passenger Vessels

Offshore

Fishing

No. of Broadband Satellite Vessels

Broadband Maritime Vessels

2015 Additions through 2025

Source: NSR

More Broadband Vessels to Enter

Market Through 2025

– Merchant Maritime Markets continue to

lead the sector in overall broadband

connected vessels;

– Merchant is an increasing opportunity

with the pipeline of ‘connectivity’ still

largely starting in MSS and

transitioning towards VSAT

connectivity.

“Non-Broadband != ‘Unconnected’…

but Probably Under-connected?

– Unconnected and under-connected

markets will be amongst the ‘core growth

opportunities’,

– Technology advances (‘flat panels’ and

‘cheap capacity’) will help

“Non-Broadband != ‘Unconnected’… but Probably Under-connected?

Intelsat Briefing @ Digital Ship Posidonia

June 2016

0% 20% 40% 60% 80% 100%

Merchant Maritime

Passenger Vessels

Offshore

Fishing

No. of Broadband Satellite Vessels

Broadband vs. Non-Broadband Maritime Vessels by 2025

2015 Additions through 2025 Non-Broadband Vessels

Source: NSR

NSR Presentation 18

www.nsr.com © 2016 – NSR

Trend: Bigger, yet Better?

Intelsat Briefing @ Digital Ship Posidonia

June 2016

• Consumers spending more as reflection of dropping fuel prices.

• Combined with the nearly completed Panama Canal Expansion, more shipping fleets are using fewer

ships, opting to increase the freight/ship.

• This trend is likely to continue as a means of keeping CAPEX low, especially as crude oil prices stay low.

Source www.APL.com

Source http://micanaldepanama.com/expansion/

NSR Presentation 19

www.nsr.com © 2016 – NSR

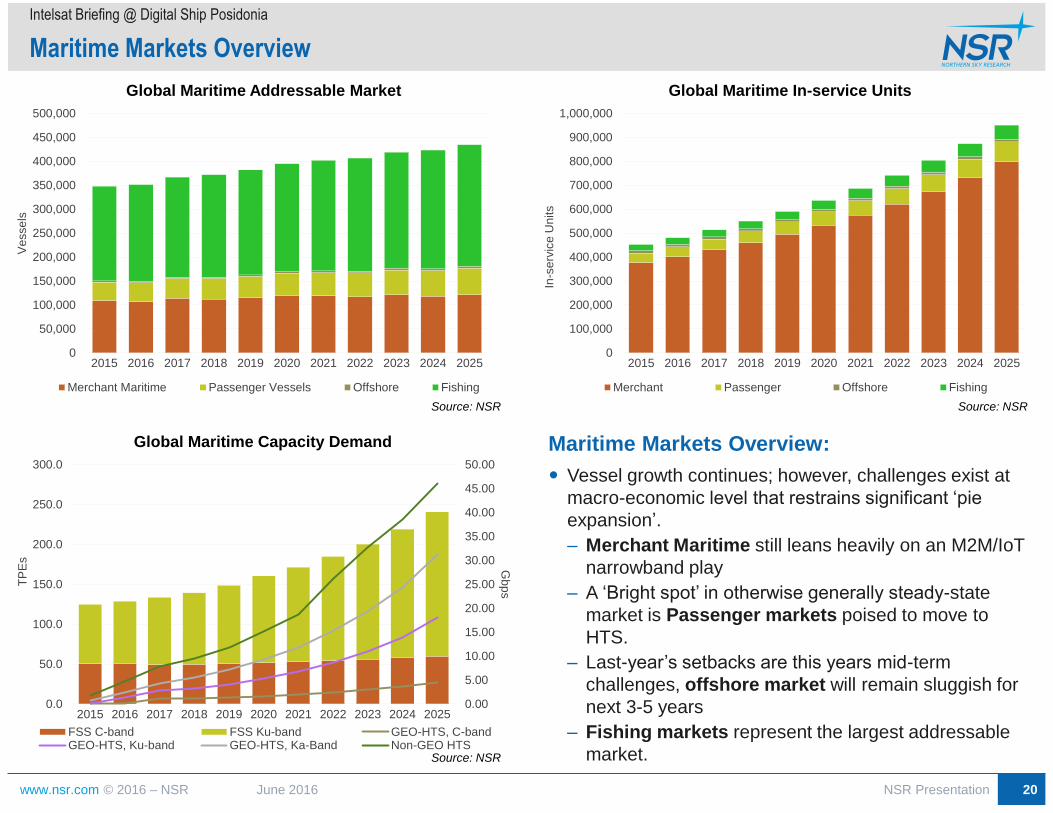

Maritime Markets Overview:

Vessel growth continues; however, challenges exist at

macro-economic level that restrains significant ‘pie

expansion’.

– Merchant Maritime still leans heavily on an M2M/IoT

narrowband play

– A ‘Bright spot’ in otherwise generally steady-state

market is Passenger markets poised to move to

HTS.

– Last-year’s setbacks are this years mid-term

challenges, offshore market will remain sluggish for

next 3-5 years

– Fishing markets represent the largest addressable

market.

Maritime Markets Overview

Intelsat Briefing @ Digital Ship Posidonia

June 2016

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

In-s

erv

ice

Units

Global Maritime In-service Units

Merchant Passenger Offshore Fishing

Source: NSR

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

0.0

50.0

100.0

150.0

200.0

250.0

300.0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Gb

ps

TP

Es

Global Maritime Capacity Demand

FSS C-band FSS Ku-band GEO-HTS, C-bandGEO-HTS, Ku-band GEO-HTS, Ka-Band Non-GEO HTS

Source: NSR

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Ve

sse

ls

Global Maritime Addressable Market

Merchant Maritime Passenger Vessels Offshore Fishing

Source: NSR

NSR Presentation 20

www.nsr.com © 2016 – NSR

Global Maritime In-service Units

Intelsat Briefing @ Digital Ship Posidonia

June 2016

FSS & HTS

– Pricing decreases across both FSS

and HTS largely smooth out adoption

between one or the other..

MSS Narrow- and

Broadband

– With terminal form

factors on the VSAT side

continuing to mirror the

MSS area of market,

MSS will be the driving

force for ‘pie growth’

– Driven by GMDSS or

VMS –depending on

certification process.

82%

84%

86%

88%

90%

92%

94%

96%

98%

100%

2015 2020 2025

Global Maritime Verticals In-service Units MSS

MSS-NB MSS-BB

0

250,000

500,000

750,000

1,000,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

In-s

erv

ice

Units

Global Maritime In-service Units, by Verticals

Merchant Passenger Offshore Fishing

Source: NSR

Verticals

– Merchant maritime still holds 1st

place in terms of satcom in-service

units.

– Legacy market with 100,000s of units

in use today.

NSR Presentation 21

www.nsr.com © 2016 – NSR

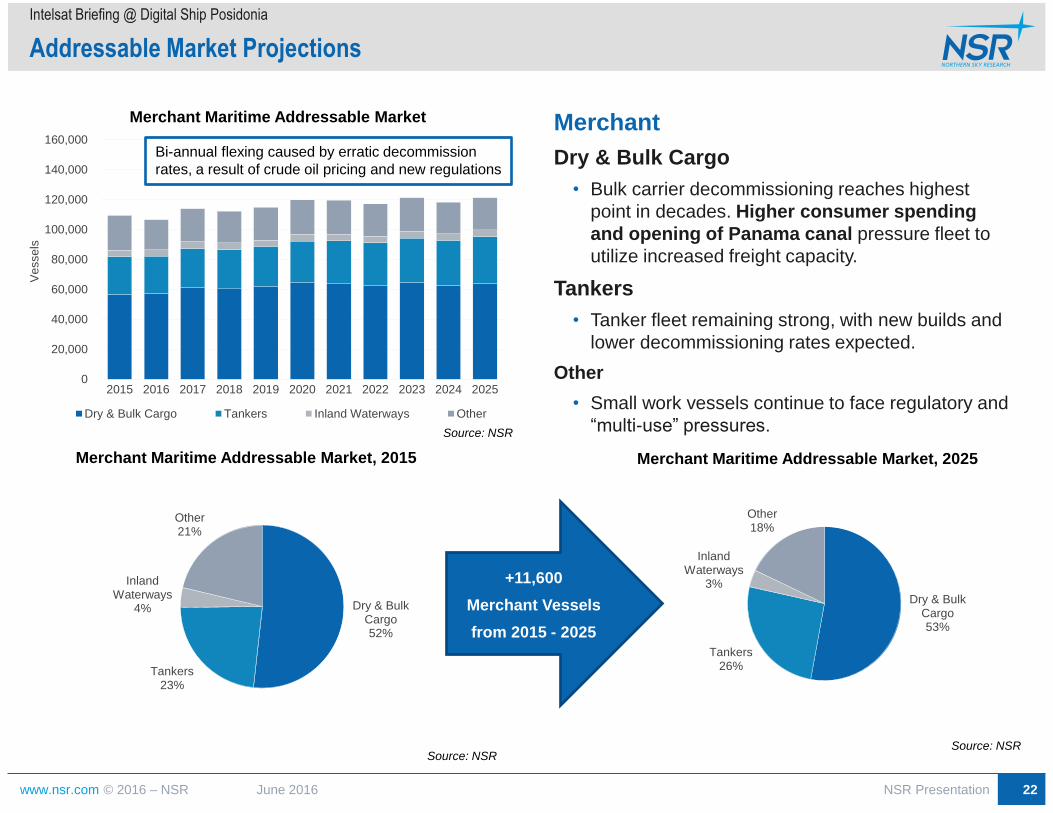

Addressable Market Projections

Intelsat Briefing @ Digital Ship Posidonia

June 2016

Merchant

Dry & Bulk Cargo

• Bulk carrier decommissioning reaches highest

point in decades. Higher consumer spending

and opening of Panama canal pressure fleet to

utilize increased freight capacity.

Tankers

• Tanker fleet remaining strong, with new builds and

lower decommissioning rates expected.

Other

• Small work vessels continue to face regulatory and

“multi-use” pressures.

+11,600

Merchant Vessels

from 2015 - 2025

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Ve

sse

ls

Merchant Maritime Addressable Market

Dry & Bulk Cargo Tankers Inland Waterways Other

Source: NSR

Bi-annual flexing caused by erratic decommission

rates, a result of crude oil pricing and new regulations

Dry & Bulk Cargo 52%

Tankers 23%

Inland Waterways

4%

Other 21%

Merchant Maritime Addressable Market, 2015

Source: NSR

Dry & Bulk Cargo 53%

Tankers 26%

Inland Waterways

3%

Other 18%

Merchant Maritime Addressable Market, 2025

Source: NSR

NSR Presentation 22

www.nsr.com © 2016 – NSR

In-Service Units & Retail Revenue

– Dominated by L-band units for equipment

andrevenues but ARPU higher for VSAT

solutions

Capacity Demand

– Increased capacity consumption…“Mostly, I’ll

pay what I paid last year but with significantly

more capacity consumption”

Capacity Revenues

– The “Pricing response” significantly picks up

towards end of forecast as FSS capacity

revenue growth is flat while capacity demand

continues.

Units In-Service, Revenues & Capacity

Intelsat Briefing @ Digital Ship Posidonia

June 2016

$-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

$M

Merchant Retail Revenues, by Capacity Type

FSS C-band FSS Ku-band GEO-HTS, C-band GEO-HTS, Ku-bandGEO-HTS, Ka-Band Non-GEO HTS MSS-NB MSS-BB

Source: NSR

0

5

10

15

0

40

80

120

160

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Gb

ps

TP

Es

Merchant Capacity Demand

FSS C-band FSS Ku-bandGEO-HTS, C-band GEO-HTS, Ku-bandGEO-HTS, Ka-Band Non-GEO HTS Source: NSR

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

In-s

erv

ice

Units

Merchant In-service Units, by Capacity Type

FSS C-band FSS Ku-band GEO-HTS, C-bandGEO-HTS, Ku-band GEO-HTS, Ka-Band Non-GEO HTSMSS-NB MSS-BB Source: NSR

NSR Presentation 23

www.nsr.com © 2016 – NSR

Market Outlook and Strategic Considerations

Intelsat Briefing @ Digital Ship Posidonia

June 2016

Drivers

More Capacity + Cheaper Operational

Improvements

Focus on “Data-driven”

analysis

Restraints

Vessel Over-

supply

Slow(ish) to adapt to

change Lower Global

Economic Activity

Factor Near-term Mid-term Long-term

More Capacity + Cheaper Strong Strong Strong

Focus on “Data-driven” analysis Medium Strong to Medium Medium

Operational Improvements Strong Strong Strong

Vessel Over-supply Weak Weak to Medium Medium to Strong

Slow(ish) to adapt to change Weak Weak Weak

Lower Global Economic Activity Weak Weak to Medium Medium

NSR Presentation 24

www.nsr.com © 2016 – NSR

www.nsr.com @NSR_Satcom

Northern Sky Research, LLC (NSR)

One Mifflin Place

Suite 400

Cambridge, MA 02138

United States

Phone: 617-674-7743

Thank You! Questions