navigating mexico's energy reform: the upstream...

TRANSCRIPT

Navigating Mexico’s Energy Reform: The Upstream Sector

Mexico’s 2013 energy reform was widespread, encompassing virtually all energy areas, ranging from hydrocarbons to renewables. The oil industry will keep its preeminence, but the reform will also have important effects upon natural gas and power.

M ex i co: K ey O i l I n d u stry I n d i cators - Upstream ( 1 9 9 4 = 1 0 0 ) M ex i co: K ey O i l I n d u stry I n d i cators - D ow n stream ( 1 9 9 4 = 1 0 0 )

1 6 0

C ru d e P rod . P rov en C ru d e R es.C ru d e E x p.

1 4 01 2 01 0 0

8 06 04 02 0

1 9 9 4 1 9 9 9 2 0 0 4 2 0 0 9 2 0 1 4

Sources: Pemex, SENER, EY

1 2 5 6 0 0

5 0 0

4 0 0

3 0 0

2 0 0

1 0 0

1 2 01 1 51 1 01 0 51 0 0

9 59 08 58 0

R ef . O u tpu t D eman dP rod . I mports ( R H S)

1 9 9 4 1 9 9 9 2 0 0 4 2 0 0 9 2 0 1 4

Sources: Pemex, SENER, EY

EY Mé xico 1

The most powerful incentive to reform was the urgent need to revert the continued worsening of the main operating metrics of Pemex, the now formerly state-owned monopoly and source of over a third of government revenue. Indeed, crude and liquids production shrank by a quarter over the past decade and p roven reserves h ave virtu al l y h al ved , w h il e cru d e exp orts have plummeted by almost 40%. Similarly refining capacity has remained stagnant and unable to match demand, leading to a surge in refined product imports, notably of gasoline. Investment opportunities are thus abundant. According to some preliminary estimates, investment needs will range between US$35 billion and US$100 billion over the next decade.

Upstream, the reform was designed around three broad themes: 1) five licensing rounds are to be held up to 2020: one to award Pemex’s acreage or “entitlements”, and four opened to private companies; 2) Pemex is expected to seek partners for selected promising areas; and 3) 22 “enhanced” service contracts between Pemex and private companies are to “migrate” to one of the new types specified in the new contractual framework.

M ex i co’ s Upstream A ttracti v en ess: V ast R esou rces, L ow C osts an d H i g h C hal l en g es

Mexico’s main upstream attraction is a potentially vast resource base and relatively low costs. Pemex estimates that “prospective” (i.e., yet to be discovered) oil & gas reserves could total as much as 115 billion barrels of oil equivalent (boe), roughly three times as much as current proven, probable and possible reserves (3P). Average development costs, meanwhile, are among the lowest in the world, at about $23/boe, of which $15/boe in capex and $8/boe in opex, with roughly 60% of production coming from areas at $10-21/boe. Thus, the case can be made that Mexico remains an attractive oil province even in an environment of subdued oil prices.

M ex i co: O i l & G as R eserv es

1 6 0

1 2 0

8 0

4 0

P roven

P rob ab l e

P ossi b

l e

Total

( 3P )

“ Pros

pecti v

e”

G rand To

tal

b n b oe

-

Sources: Pemex, SENER, EY

Navigating Mexico’s Energy Reform: The Upstream Sector2

M ex i co: E sti mated Total D ev . C O st b y Sel ected F i el d s, 2 0 1 4

US$/boe

6 05 04 03 02 01 0

Tampi co

- Mi sa

n tl a

M acu sp

ana -

Mu sp

ac

C hi con tepec

C antar

el l

B el l ota

- Ju j o

L i toral

d e Tab as

co

V eracru

z Bas

i n

C ou n try

C i n co P res

i d en tes

R od ador

M ex i co: P rod u cti on b y Sel ected A reas, 2 0 1 4

-

kboe/d

2 , 0 0 0

1 , 5 0 0

1 , 0 0 0

5 0 0 1 0 %

2 0 %

3 0 %

4 0 %

%of total

N E Mar

i n e

Sou thern

N orthern

SW Mar

i n e

The reform was the first step, but the challenges are significant. Limited exploration has failed to replenish the country’s oil reserves. Only once during the past decade have additions exceeded production (i.e., 100%); under current trends, oil output would last only 1 1 years.

Moreover, total liquids production (crude, NGLs and condensates) has plummeted uninterruptedly for the past decade. The historical mainstay of Mexican production – the Cantarell giant field – has virtually become commercially depleted, with the second main producing asset – KMZ – expected to begin declining imminently.

M ex i co: O i l R eserv es

B il l ion b oe

6 0

5 0

4 0

3 0

2 0

1 0

1 9 9 4 1 9 9 9 2 0 0 4 2 0 0 9 2 0 1 4

P ossi b l e P rob ab l e P rob en

1 5 0

5 0

( 5 0 )

( 1 0 0 )

( 1 5 0 )

( 2 0 0 )

-

1 0 0

1 9 9 9 2 0 0 4 2 0 0 9 2 0 1 4

A d opti on of i n t’ l .

measu remen t

M ex i co: N et P rov en O i l R eserv e A d d i ti on s

-

Sources: Pemex, WoodMac, EY Sources: Pemex, WoodMac, EY

Sources: Pemex, SENER, EY Sources: Pemex, SENER, EY

EY Mé xico 3

W hat D i d P emex G et i n R ou n d Z ero?

Pemex was formally granted by the state specific producing and prospective assets (83% and 20%, respectively, of the country’s base) under the so-called Round Zero, in August 2014. The state-owned company got 100% of the proven and probable reserves it had requested, but only two-thirds of its “prospective” resources (which are admittedly highly uncertain). Pemex requested in effect most currently producing assets, which sustain its declining production base, relinquished the most problematic, such as the high-cost onshore Chicontepec field, and kept promising areas such as deepwater.

M ex i co: O i l P rod u cti on

1 9 9 4 1 9 9 9 2 0 0 4 2 0 0 9 2 0 1 4

mb/d3 . 9

3 . 7

3 . 5

3 . 3

3 . 1

2 . 9

2 . 7

M ex i co: C ru d e P rod u cti on B y F i el d

mb / d3 . 5

3 . 0

2 . 5

0 . 5

-

1 . 5

2 . 0

1 . 0

1 9 9 4 1 9 9 9 2 0 0 4 2 0 0 9 2 0 1 4C an tarel l K M Z O ther

M ex i co: O i l an d G as R eserv es

P emex

2 P “ P rospecti v e” Total

1 6 0

1 4 0

1 2 0

1 0 0

8 0

6 0

4 0

2 0

-

b n b oe

C ou n try

P emex : O i l & G as R eserv es G ran ted i n R ou n d Z ero

b n b oe

5 0

4 0

3 0

2 0

1 0

-2 P “ P rospecti v e” Total

O n shore, Shal l ow W ater & E x tra H eav y C ru d eUn con v en ti on al

D eep W ater

Sources: Pemex, SENER, EY

Sources: Pemex, SENER, EY Sources: Pemex, SENER, EY

Sources: Pemex, SENER, EY

Navigating Mexico’s Energy Reform: The Upstream Sector4

Armed with its new endowments, the company announced it would seek ten partnerships before end-2015, but these have been delayed. Under a tight budget because of government restrictions – oil revenues account for one-third of fiscal revenues – Pemex needs private expertise, capital and technology to develop its assets. If it fails to meet its work commitment, the company could conceivably be forced to relinquish some of these assets, which would be then auctioned in future rounds.

123456789

1 01 11 21 31 4

R od ad orO g arri oC á rd en as- M oraSamari aB ol on ti k úSi n á nE k A y atasi lTek elUtsi lK u n ahP i k l i sTri ó nE x pl oratu s

3 1 2 . 8 2 4 7 . 9 2 6 3 . 6 1 . 7 Onshore mature fields ( V eracru z an d Tab asco) ; l i g ht oi l

Offshore mature fields ( Tab asco an d C ampeche shal l ow w aters) ; l i g ht oi l

Offshore fields (Campeche); ex tra- heav y oi l

Offshore fields (Veracruz d eepw ater) ; n atu ral g as

Offshore fields (Tamaulipas d eepw ater) ; oi l

4

3

1

4 9 7 . 3 6 . 3

6 . 2

3 5 0 . 1

7 4 6 . 6 8 6 2 . 5

5 0 1 . 6 6 . 8 1

1

2 1 1 . 9

1 1 9 . 4

8 8 . 8

5 5 . 3

2 2 . 6 1 2 . 9

--

3 0 4 . 6 2 3 4 . 4

8 . 1 3 . 2

F i el d A rea ( sq . k ms)

2 P R eserv es ( M M B O E )

3 P R eserv es ( M M B O E )

E x pected I n v estmen t ( USD B i l l i on )

C on tracts A rea

Total 1 4 6 1 1 . 8 1 , 5 5 6 . 5 2 , 6 6 4 . 0 3 2 . 3 1 0

S ou rces: S ener, EY

EY Mé xico 5

In addition, Pemex must convert or “migrate” 22 contracts into the new framework put in place by the reform. These “enhanced” service contracts – the result of the last partial reform of the industry in the late 2000s – must migrate to either licenses (similar to concessions, excepting that below ground hydrocarbon resources belong to the state), profit- or production-sharing agreements, services contracts or a combination of the above. The migration, though, has been delayed, as half of the existing service contracts sh ou l d h ave b een converted l ast year.

123456789

1 01 1

1 21 31 41 51 61 71 81 92 02 12 2

E b an oO l mosN ej oSan A n d ré sTi erra B l an caA ren q u eM ag al l an esSan tu ari oP á n u coA l tami raM i si ó n

C arri z oM on cl ov aH u mapaA mati tl á nF ron teri z oM i ahu apá nP i ri n eoP i tepecM i q u etl aC u erv i toSol ed ad

1 , 5 8 43 5 8

1 , 1 6 5 2 0 9 3 5 8

2 , 0 3 5 1 6 9 1 3 0

1 , 8 3 9 1 , 6 2 5 1 , 9 7 2

1 3 3 , 3 5 8 1 2 8 2 3 0 2 3 1 1 2 8 3 , 8 4 0 2 3 0 1 1 2 2 3 1 1 2 5

4 0 1 3 3 2

2 0 2 3 6 6 6 3 6 4 1 2 9 6

6 8

6 3

2 6 0 3 6 8 3 1 8 8 1 1

4 4 0 1 9 5 5 8 1 7 9

5 6 4 5 4 4

5 3 1 6 0 8 2 9 3 4 13 7 1 3 8 1

5 1 4

5 0 3 9 2 9 3 5

2 7 9 1 6

1 , 0 4 9 2 2 4 6 8

2 8 1

- - -

1 0 0 3 7

9 9 4 - -

1 3 2 1 3 -

- -

1 5 7 2 5 2

- 1 0 1

- 2 5 2 8 6 -

1 2 8

C I E P C O P F C I E P C I E P C I E P C I E P C I E P C I E P C I E P C I E P C O P F

C I E P C O P F C O P F C I E P C O P F C I E P C O P F C I E P C I E P C O P F C I E P

D i av azL ew i s

M on cl ov a P i ri n eos G asM on cl ov a P i ri n eos G asM on cl ov a P i ri n eos G as

P etrof acP etrof acP etrof acP etrof ac

C hei ron H ol d i n g s L i mi tedTecpetrol & Techi n t

D ow el l Schl u mb erg erG P A E n erg y & other

H al l i b u rtonN on eN on eN on eN on eN on e

O perad ora d e C ampos D W FP etrob ras, D i av az & Tei k ok u

P etrol i te

To b e ori g i n al l y mi g rated b ef ore en d - 2 0 1 4

To b e ori g i n al l y mi g rated b ef ore en d - 2 0 1 5

F i el d A rea ( sq . k ms)

2 P R eserv es ( M M B O E )

3 P R eserv es ( M M B O E )

C on tract Ty pe C ompan y C ommen ts

P rospecti v e R eserv es ( M M B O E )

Sources: Pemex, Sener, EY

Total 2 0 , 0 7 0 2 , 2 0 8 4 , 5 2 2 2 , 2 5 2

Navigating Mexico’s Energy Reform: The Upstream Sector6

W hat I s on O f f er i n R ou n d O n e?

The Mexican reform is unique in that it offers all types of assets to prospective upstream players. Round One (R1), to be held during 2015 and early 2016 and which is due to encompass 65 blocks (down from 169 originally), is a reflection of such diversity. It started in mid-July with an auction of shallow-water exploration blocks (Call 1 or R1C1), followed by another of shallow-water development assets in September (R1C2) and one for onshore mature fields in December (R1C3). Round One will include two further bidding processes: one for deepwater blocks (R1C4), tentatively by 3Q16, and one for unconventional areas (R1C5), yet to be announced.

By mid-July, just before starting, Round One had nominally attracted a significant number of potential bidders, with over 60 companies formally pre-qualified. For R1C1 (shallow-water exploration blocks), 33 companies were on the list, with 17 pre-qualified on their own and 16 as part of seven consortia. H ow ever, th e b id d ing tu rned ou t to b e w el l b el ow exp ectations. Only nine companies ended up participating (on their own and in consortia), there were only six bids but 14 blocks on offer, and only two were awarded – to the same consortium, comprising Mexico’s Sierra Oil & Gas, US Telos Energy and UK Premier Oil.

Despite its results, the first process was in many ways historic: for the first time in over 75 years blocks were awarded to private companies, including a Mexican one, thus symbolizing the emergence of a new industry. The whole procedure was transparent, and the bids for the winning blocks were highly lucrative for the state, with the government take likely to average well above 80%.

Nonetheless, given that only 14% of the blocks on offer were awarded, rather than an expected 30-40%, the government

signaled its willingness to introduce several changes to improve the success rate of subsequent processes. Indeed, the fields on offer in R1C1 were generally considered to be relative small, and some were mostly geared to less appealing gas, yet most had the same minimum government take—which highlighted that such a minimum should henceforth be probably better calibrated to suit the geological conditions of each block on offer in forthcoming processes. Moreover, the minimum was probably too high: four bids were rejected because they were below it, yet three were very close. As much as the Finance Ministry, which sets contractual terms, may attempt to maximize the value of Mexico’s resources, the country is competing against others in a context of depressed oil prices and should not exp ect to extract excessive rents. A noth er d isincentive was the very high corporate guarantee (US$6 billion), which deterred several potential bidders, and a lack of flexibility with regards to consortia. Finally, several companies probably opted to pre-qualify to test the procedures, intent on bidding in other p rocesses.

EY Mé xico 7

The second auction, with five shallow-water development blocks on offer, of which four with proven reserves, was carried out in late September. Contrary to the first call, R1C2 proved to be highly successful, partly reflecting the changes described above, as well as lower development risks. Of the 19 companies pre-qualified (nine on an individual basis and ten as part of four consortia), nine chose to participate (five on their own plus the four consortia). Collectively, there were 15 bids, and three blocks were awarded – equivalent to a 60% success rate – under very favorable fiscal conditions for the government. The winners include one major (ENI International) and two consortia (Mexico’s E&P Hidrocarburos y Servicios with Argentina’s Pan American Energy, and US Fieldwood Energy in tandem with Mexico’s Petrobal).R1C3, offering 25 mature fields, was intended to attract independent companies, notably Mexican. The government, indeed, viewed this bidding process as the first stepping stone for the emergence of domestic E&P industry. Being onshore, the blocks are relatively easier to operate, and many have seismic data and some degree of infrastructure in place, so existing fields could be turned around relatively quickly with appropriate enhanced recovery techniques. Moreover, the financial and operating requirements were much laxer than the first two processes. For the government, which had previously declared that a 20% award rate would be acceptable, the December results exceeded all expectations: all the blocks on offer were awarded, often with high bids (raising concerns, though, that some winners may have overpaid). Of the 22 winners (either stand alone or in consortia), 16 are Mexican companies, most of them Pemex contractors aiming to graduate into full-flown E&P p l ayers.

For international majors, endowed with technical, financial and managerial resources to develop complex projects, the deepwater areas in the Gulf of México are probably the most attractive assets. R1C4, to be carried out tentatively in September or October 2016, will offer 10 blocks, of which four in the northern region of the Gulf of Mexico (the Perdido Fold Belt and neighboring areas) and six in the southern part (the Pre-Salt Basin). Even though the slide in oil prices has raised concerns over deepwater profitability, the potential resource base – the Gulf of Mexico is one of the world’s most prolific basins – will remain very attractive given the very long-term nature of such projects, particularly in the Perdido Fold Belt, which is close enough to the US maritime border to be conceivably connected to existing subsea infrastructure. Some of these projects may be carried out in partnership with Pemex.Finally, R1C5, offering unconventional resources (shale oil & gas in northern Mexico and tracks of the vast Chicontepec field in Veracruz, and also yet to be announced), has been downsized relative to original plans in terms of the number of blocks of offer. Although potential resources are significant – some studies suggest that México ranks sixth worldwide – the conditions that made possible the shale “revolution” in the US are not easily replicable, particularly in an environment of persistent low prices. Only the Chicontepec field, which is not a shale deposit but which could be developed with fracking techniques, could perhaps attract some interest. Mining companies already operating in México may be the prime candidates to undertake shale projects, at least in the first few years after the reform

Round One: Pre-Qualification Number of Companies by Type*

8 0

1 9

7 5

9 0

6 0

4 5

3 0

1 5 4 2 3 3

2 6

1 4

8 0

3 3

-M aj ors N O C s I n d ep. Total

F i rst b i d d i n g process secon d b i d d i n g processThi rd b i d d i n g process

Sources: CNH, EY *As of September 30, 2015

R ou n d O n e: R esu l ts

O f f ered B l ock

s

P arti c

i patin g

B i d s

A w ards

2 0 0

2 5 0

1 5 0

1 0 0

5 05 61 4 2 5 2 54 0

991 5

2 2 4

32-

Sources: CNH, EY

C al l 1 C al l 2 C al l 2

Navigating Mexico’s Energy Reform: The Upstream Sector8

The F i v e- Y ear L i cen si n g P l an

In July 2015, the Energy Ministry released details for three new bidding rounds (and changes to the first one). The five-year licensing plan was subsequently revised following consultations with the industry, and its definitive version was released in early October. Including R1, 338 blocks are to be auctioned over the next five years (down from 914 in the first draft), with total reserves (3P + “prospective”) of 107 billion barrels of oil equivalent (broadly unchanged), spread over 236,000 square kilometers (rather than 179,000). Thus, there will be fewer blocks, but they will be much larger and hold higher reserves on

average. Another key difference with the first draft is that the emphasis has switched to developing existing resources rather than finding new ones, with 78% of the blocks on offer in the four rounds to be located in development areas (compared to 39% before), which suggests a new-found urgency to revert the cu rrent p rod u ction d ecl ine. A s su ch , Rou nd O ne concentrates most of 3P reserves (61 out of 67 billion boe for the four rounds). By contrast, Rounds 2-4 hold the bulk of “prospective” resources (29 out of 40 bboe).

Mexico: Five-Year Licensing PlanAs of July 2015

6 1

3 2 1

1 2

1 1 1 0 7

R ou n d 1 R ou n d 2 R ou n d 3 R ou n d 43 P P rospecti v e

R eserv esb b oe

6 0

8 0

4 0

2 0

-

Sources: CNH, Woodmac, EY

Mexico: Five-Year Licensing PlanAs of July 2015

3 3 8

6 59 1 9 2

9 0

4 0 0

3 0 0

2 5 0

3 5 0

2 0 0

1 5 0

1 0 0

5 0

A l l R ou n d 1 R ou n d 2 R ou n d 3 R ou n d 4-

Sources: CNH, Woodmac, EY

Mexico: Five-Year Licensing PlanAs of July 2015

2 4 0

5 1 6 32 8 2 3 3 3

6 9 5 71 4

9 8

A l l R ou n d 1 R ou n d 2 R ou n d 3 R ou n d 4

B l ock s

4 0 0

3 0 0

2 0 0

1 0 0

-

D ev el opmen t E x pl orati on

Sources: CNH, Woodmac, EY

Mexico: Five-Year Licensing PlanAs of July 2015

5 4

R ou n d 1 R ou n d 2 R ou n d 3 R ou n d 4

7 36 0 6 3

D ev el opmen t E x pl orati on

1 , 0 0 0sq . k ms

8 0

6 0

4 0

2 0

-

Sources: CNH, EY

23 1 1

3 1

EY Mé xico 9

A Ten tati v e O i l & G as O u tpu t F orecast

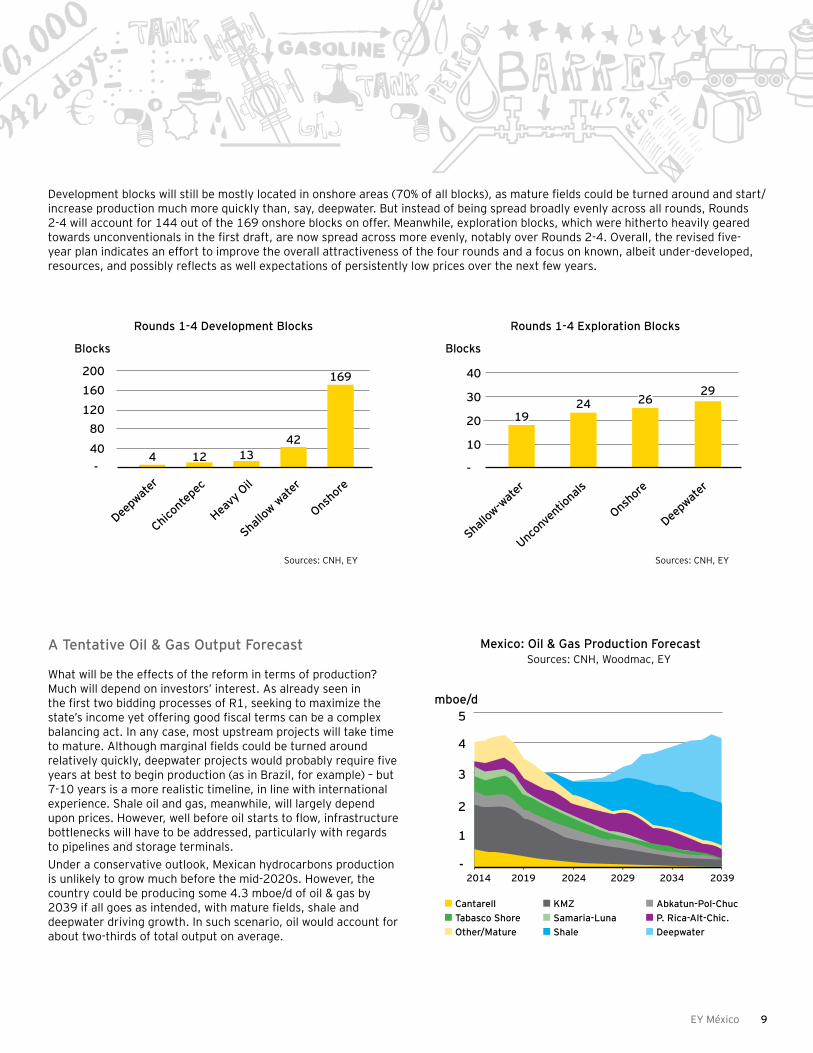

What will be the effects of the reform in terms of production? Much will depend on investors’ interest. As already seen in the first two bidding processes of R1, seeking to maximize the state’s income yet offering good fiscal terms can be a complex balancing act. In any case, most upstream projects will take time to mature. Although marginal fields could be turned around relatively quickly, deepwater projects would probably require five years at best to begin production (as in Brazil, for example) – but 7-10 years is a more realistic timeline, in line with international experience. Shale oil and gas, meanwhile, will largely depend upon prices. However, well before oil starts to flow, infrastructure bottlenecks will have to be addressed, particularly with regards to pipelines and storage terminals.Under a conservative outlook, Mexican hydrocarbons production is unlikely to grow much before the mid-2020s. However, the country could be producing some 4.3 mboe/d of oil & gas by 2039 if all goes as intended, with mature fields, shale and deepwater driving growth. In such scenario, oil would account for about two-thirds of total output on average.

Development blocks will still be mostly located in onshore areas (70% of all blocks), as mature fields could be turned around and start/increase production much more quickly than, say, deepwater. But instead of being spread broadly evenly across all rounds, Rounds 2-4 will account for 144 out of the 169 onshore blocks on offer. Meanwhile, exploration blocks, which were hitherto heavily geared towards unconventionals in the first draft, are now spread across more evenly, notably over Rounds 2-4. Overall, the revised five-year plan indicates an effort to improve the overall attractiveness of the four rounds and a focus on known, albeit under-developed, resources, and possibly reflects as well expectations of persistently low prices over the next few years.

M ex i co: O i l & G as P rod u cti on F orecast Sources: CNH, Woodmac, EY

mb oe/ d5

4

3

2

1

-2 0 1 4 2 0 1 9 2 0 2 4 2 0 2 9 2 0 3 4 2 0 3 9

C an tarel l K M Z A b k atu n - P ol - C hu cSamari a- L u n a P . R i ca- A l t- C hi c.Shal e D eepw ater

Tab asco ShoreO ther/ M atu re

R ou n d s 1 - 4 E x pl orati on B l ock s

1 92 4 2 6

2 94 0

3 0

1 0

2 0

-

B l ock s

Shal low

- wate

r

Un con v

enti o

n al s

O n shore

D eepw

ater

Sources: CNH, EY

R ou n d s 1 - 4 D ev el opmen t B l ock s

Sources: CNH, EY

1 24 1 34 2

1 6 92 0 0

B l ock s

1 6 0

1 2 08 0

4 0-

C hi con tepec

H eav y

Oi l

Shal low

wate

r

O n shore

D eepw

ater

E Y | A ssu rance | T ax | T ransactions | A d visory

About EY

EY is a gl ob al l ead er in assu rance, tax, transaction and ad visory services. T h e insigh ts and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey . com.

© 2015 EYGM Limited.A l l Righ ts Reserved .

EYG no.ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

A l f red o Á l v arezEnergy Sector Leader+ 5 2 5 5 1 1 0 1 8 4 2 [email protected]

G i l b erto L oz an oAdvisory Partner+ 5 2 5 5 5 2 8 3 1 4 5 [email protected]

R od ri g o O choaTax Partner+ 5 2 5 5 5 2 8 3 1 4 9 [email protected]

R af ael A g u i rreTAS Partner+ 5 2 5 5 5 2 8 3 8 6 5 [email protected]

G erard o F l oresAssurance Partner+ 5 2 5 5 1 1 0 1 8 4 0 [email protected]

F ran ci sco F orasti eriLegal Partner+ 5 2 5 5 1 1 0 1 7 2 9 [email protected]

C on tacts