navigating the regulatory maze

TRANSCRIPT

2

Jakarta20 July 2016

Navigating the Regulatory Maze

Presented at 1st Asian Financial Leaders ProgramPrasetiya Mulya Executive Learning Institute

Winang Budoyo([email protected])Chief EconomistPT Bank CIMB Niaga Tbk

Navigating Global Uncertainties

4

Increasing Global Market Uncertainty in 2016

Source: Various

Divergence of global

monetary policy:

Fed vs ECB & BoJ

Oil Price:

How low/high can it go?

Chinese Puzzle:

Downside on

Growth and

Fear of

Currency War

Global Capital

Volatility

Slower global

economic recovery

5

More Protectionism?

JapanThe ELDERLY vs The YOUTH

EuropeCompetition among member countries

UKThe New Epicentrum:

1. The RICH vs The POOR2. The ELDERLY vs The YOUTH

3. Among countries

USThe RICH vs The POOR

Higher Protectionism

Donald Trump

6

External Factors Remain the Main Risk PotentialDownward adjustments for IMF’s growth estimates in 2015 due to global headwinds

3.3 3.43.8

3.5 3.53.3

3.1 3.1

2013 2014 EO Oct 2014 WEO Jan 2015 WEO Apr 2015 WEO Jul 2015 WEO Oct 2015 WEO Jan 2016

IMF-WEO revised 2015 growth estimates downward

Source: IMF

(1) yoy growth comparing 3Q15 and 3Q14 real GDP

IMF’s Global Growth Estimates Project Downward Trends for 2015

GDP Growth Comparison among Major Global Economies

Advanced Economies Performance. US showssome improvements, but Japan and Europe arestill in low recovery stage Policy Uncertainties in Developed Countries.

The Fed normalization, BoJ and ECB stimuluspackages Global Commodity Market. Volatile with

tendency to weaken China Growth Slowdown. Hard or soft landing? Yuan Devaluation Policy. Exerting pressure to

other Asian Currencies

2015 Global Risks Sources

7

GDP Growth (yoy)

4.92

0

1

2

3

4

5

6

7

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

2012 GDP Growth:6.0% 2013 GDP Growth:

5.6% 2014 GDP Growth:5.0% 2015 GDP Growth:

4.8%

%

4.71 4.674.73

5.04

1Q15 2Q15 3Q15 4Q15

Recovery Point

2015 marks the turning point forIndonesia’s growth acceleration

Indonesia’s Economy on a Stable PathGovernment Spending and Investment as the main contributors to Growth and supported by robust HH Consumption, made the 3Q15 as the turning point

Source: Central Bureau of Statistics (CBS)

Expenditure Component (%)

2013 2014 2015 2016

Yearly Yearly Q1 Q2 Q3 Q4 Yearly Q1

HH Cons 5.4 5.1 5.0 5.0 5.0 4.9 5 4.9

Non Profit Cons 8.2 12.4 -8.3 -7.9 6.4 8.3 -0.6 6.4

Government Cons 6.9 1.9 2.2 2.3 6.6 7.3 5.4 2.9

Investment 5.3 4.1 4.4 3.6 4.6 6.9 5.1 5.6

Export 4.2 1.0 -0.9 -0.1 -0.7 -6.4 -2.0 -3.9

Import 1.9 2.2 -2.3 -6.8 -6.1 -8.1 -5.8 -4.2

GDP 5.6 5.0 4.7 4.7 4.7 5.0 4.8 4.9

GDP Growth by Sector2013 2014 2015 2016

Yearly Yearly Q1 Q2 Q3 Q4 Yearly Q1

Agriculture, Forestry, and Fishery 4.2 4.2 4.0 6.9 3.3 1.6 4.0 1.9

Mining Industry 1.7 0.6 -1.3 -5.2 -5.7 -7.9 -5.1 -0.7

Industrial Processing 4.5 4.6 4.0 4.1 4.5 4.4 4.2 4.6

Construction 6.1 7.0 6.0 5.4 6.8 8.2 6.6 7.9

Big Traders and Wholesale and Retail; Automotive Repair

4.7 4.8 4.1 1.7 1.4 2.8 2.5 4.0

Transportation and Warehousing 8.4 8.0 5.8 5.9 7.3 7.7 6.7 7.7

Information and Communication 10.4 10.0 10.1 9.7 10.7 9.7 10.1 8.3

Other Services (10 sectors) 6.5 5.5 5.7 5.9 5.9 7.0 6.1 6.6

GDP 5.6 5.0 4.7 4.7 4.7 5.0 4.8 4.9

Shifting from Commodity-based economy• In 4Q15, Indonesia booked 5.0% GDP growth yoy, making FY 2015 GDP growth at 4.8% yoy (the lowest level since 2010).• However, several regions expanded higher than national. These regions were benefited from strong USD episode and gave positive impacts to

Tourism industry in Bali and Nusa Tenggara and also to Fishery Product industry in Sulawesi.• While growth in resource-rich regions such as Sumatra and Kalimantan were still subdued• Indonesia continues to drive growth in resource-based industrialization to shift from commodity-based economy

Spatial GDP Growth Contribution

Source: CBS

SumateraGDP Growth2014: 4.7%2015: 3.5%

JavaGDP Growth2014: 5.6%2015: 5.5%

KalimantanGDP Growth2014: 3.2%2015: 1.3%%

SulawesiGDP Growth2014: 6.9%2015: 8.2%

Bali & Nusa TenggaraGDP Growth2014: 5.9%2015: 10.3%

Maluku & PapuaGDP Growth2014: 4.3%2015: 6.6%

2015 Regional GDP GrowthStrong USD benefited some regions and grew faster than national

9Source: BI & BPS

2015 GDP Growth per ProvinceMain engines of growth –i.e. Java & Sumatera- have revived, while the commodity-driven provinces still face setbacks. Regions with local content products , such as Sulawesi (sea products), were benefited from Rupiah depreciation

10Source: BI & BPS

1Q 2016 GDP Growth per ProvinceSlower growth across the country

11

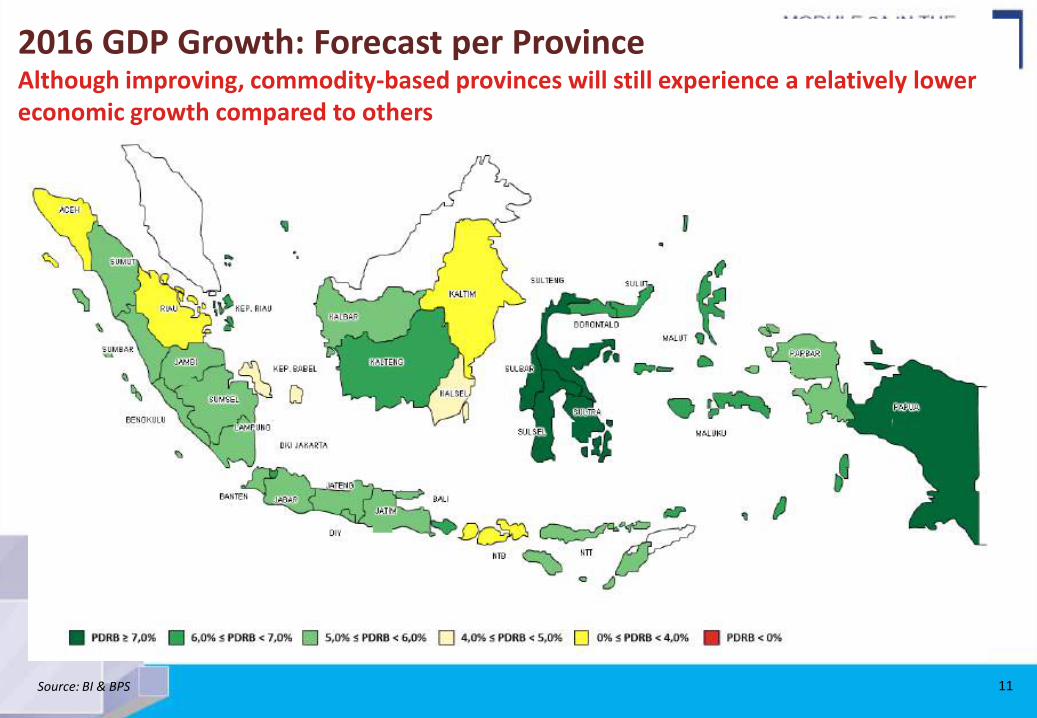

2016 GDP Growth: Forecast per ProvinceAlthough improving, commodity-based provinces will still experience a relatively lower economic growth compared to others

Source: BI & BPS

12

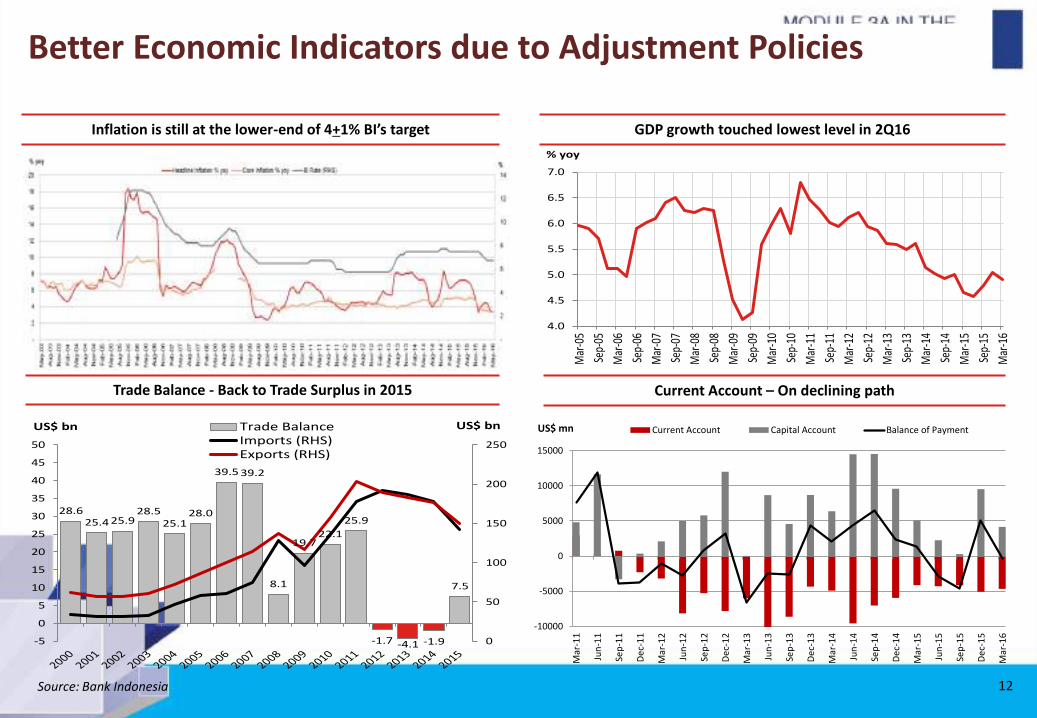

Better Economic Indicators due to Adjustment Policies

Inflation is still at the lower-end of 4+1% BI’s target GDP growth touched lowest level in 2Q16

Trade Balance - Back to Trade Surplus in 2015 Current Account – On declining path

Source: Bank Indonesia

28.625.4 25.9

28.525.1

28.0

39.5 39.2

8.1

19.722.1

25.9

-1.7 -4.1 -1.9

7.5

0

50

100

150

200

250

-5

0

5

10

15

20

25

30

35

40

45

50

Trade BalanceImports (RHS)Exports (RHS)

US$ bn US$ bn

4.0

4.5

5.0

5.5

6.0

6.5

7.0

Mar

-05

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

Mar

-16

% yoy

-10000

-5000

0

5000

10000

15000

Mar

-11

Jun

-11

Sep

-11

De

c-1

1

Mar

-12

Jun

-12

Sep

-12

De

c-1

2

Mar

-13

Jun

-13

Sep

-13

De

c-1

3

Mar

-14

Jun

-14

Sep

-14

De

c-1

4

Mar

-15

Jun

-15

Sep

-15

De

c-1

5

Mar

-16

Current Account Capital Account Balance of PaymentUS$ mn

13

Financial System Stability was Maintained, but Both LoanGrowth and Deposit Growth are still Low

CAR (Capital Adequacy Ratio) NPL (Non Performing Loan)

Loan Growth (yoy) Deposit Growth (yoy)

Source: OJK 2016

14

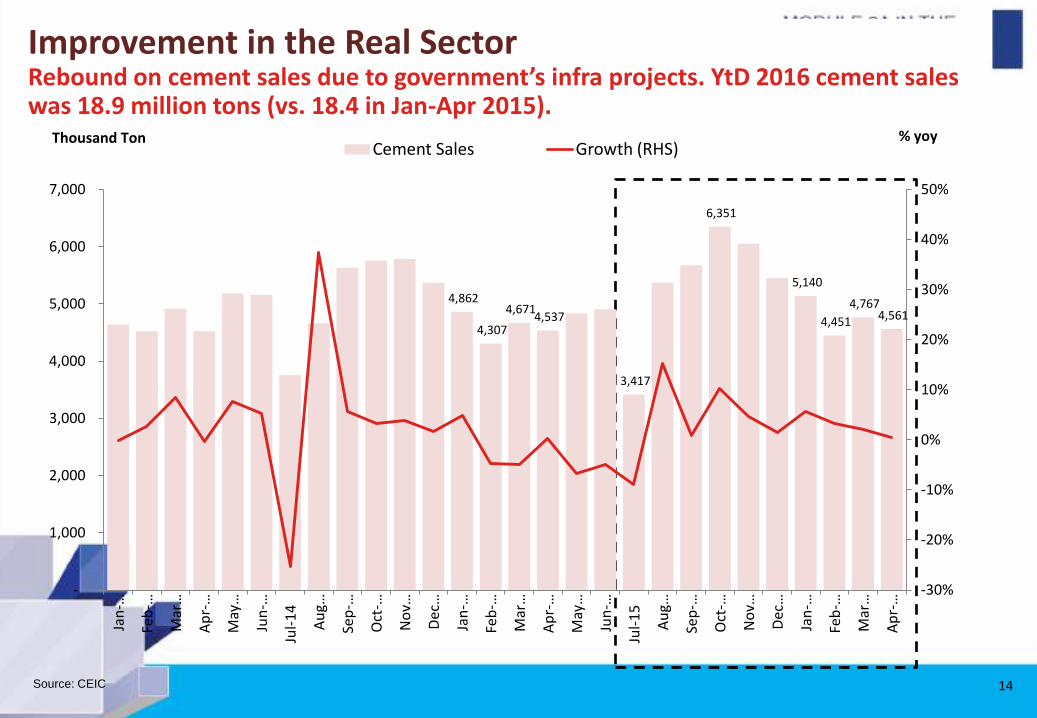

Improvement in the Real SectorRebound on cement sales due to government’s infra projects. YtD 2016 cement sales was 18.9 million tons (vs. 18.4 in Jan-Apr 2015).

Source: CEIC

4,862

4,307

4,671 4,537

3,417

6,351

5,140

4,451

4,767 4,561

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Jan

-…

Feb

-…

Mar

…

Ap

r-…

May

…

Jun

-…

Jul-

14

Au

g…

Sep

-…

Oct

-…

No

v…

Dec

…

Jan

-…

Feb

-…

Mar

…

Ap

r-…

May

…

Jun

-…

Jul-

15

Au

g…

Sep

-…

Oct

-…

No

v…

Dec

…

Jan

-…

Feb

-…

Mar

…

Ap

r-…

Cement Sales Growth (RHS)Thousand Ton % yoy

15

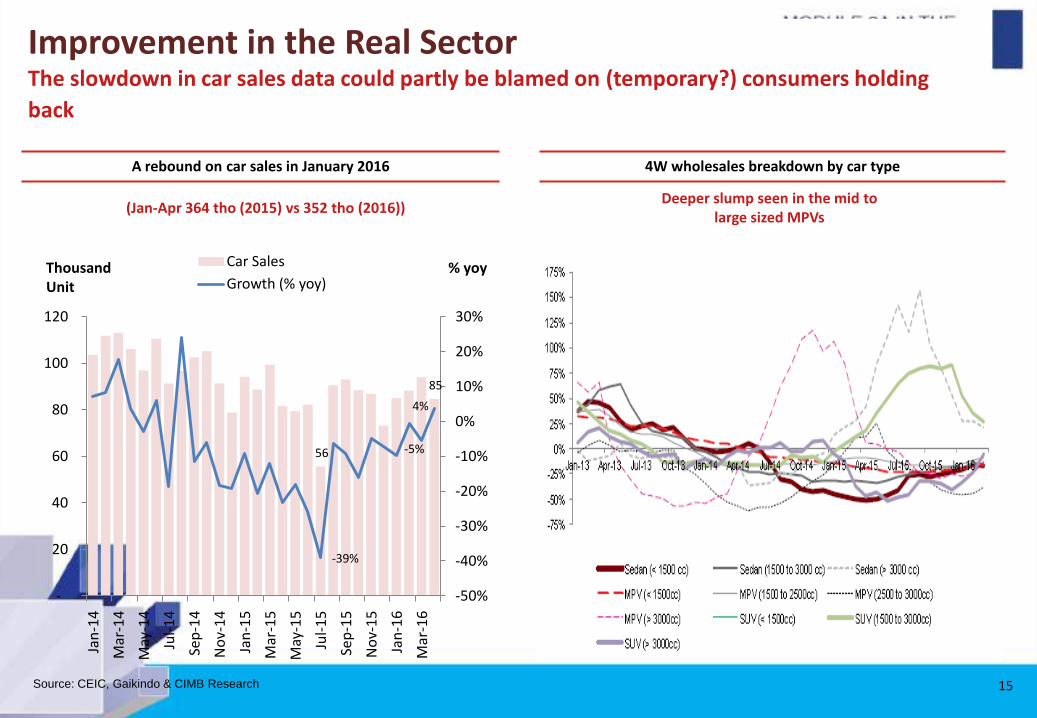

Improvement in the Real SectorThe slowdown in car sales data could partly be blamed on (temporary?) consumers holding

back

Source: CEIC, Gaikindo & CIMB Research

56

85

-39%

-5%

4%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

-

20

40

60

80

100

120

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

Car Sales

Growth (% yoy)Thousand Unit

% yoy

A rebound on car sales in January 2016 4W wholesales breakdown by car type

Deeper slump seen in the mid tolarge sized MPVs

(Jan-Apr 364 tho (2015) vs 352 tho (2016))

16

Improving Consumer Confidence Index since Sep 2015

Source: CEIC

Consumer Confidence Index (CCI) has been on increasing trend since Sep 15, showing that there is animprovement of people to their life prospect.

The increase in the CCI indicates an increase in consumer purchasing power ahead CCI has risen to a level similar to the average of the last 8 years

107.5

112.6

110

70

80

90

100

110

120

130

Consumer Confidence Index

Fuel Price Hike 1

Fuel Price Hike 2

Food Price HikeFlood

Fuel Price Hike 3

Fuel Price Decline

Fuel Price Decline

Food Price Hike

Food Price Hike Fuel Price Hike 4

Fuel Price Hike 5

Fiscal Policies

18

Fiscal Policy: Budget Re-AllocationAllocation of Energy Subsidy Spending to Education, Infrastructure and Regional Development for Sustainable Economic Growth

2016 Budget Allocation Plan Compared to 2015 Revised Budget

Energy-12%

Education+4%

Infrastructure+8%

Transfer to Regional+17.5%

2016 Key Budget Policy:Central Government Expenditure: Continue budget efficiency framework

Subsidy Policies• Fuel Subsidy Policy: Continue “Fixed Subsidy” scheme to

Diesel and “Price Subsidy” for Kerosene and 3 kg LPG• Electricity Subsidy Policy: Switch to direct subsidy scheme

given to small households (450 VA and part of 900 VA)• Food Subsidy: Rice for targeted household (15.5 million

households)• Subsidy for Fertilizer: Production price close to economic

price targeted volume of 9.55 million ton, with retail price to be adjusted to close price gap

• Interest Subsidy for SME credit: For selected sectors such as agriculture, fishery, manufacturing and trade and including for migrant worker

Regional Transfer Policy• Formulate Transfer Fund nomenclature• Enhance Special Transfer Fund (DTK)• Optimize the implementation of reward and punishment to

regional Government

Village Fund Policy• Significantly Increase allocation compared to 2015• To support growth equality and empowerment in village area

Source: Ministry of Finance

19

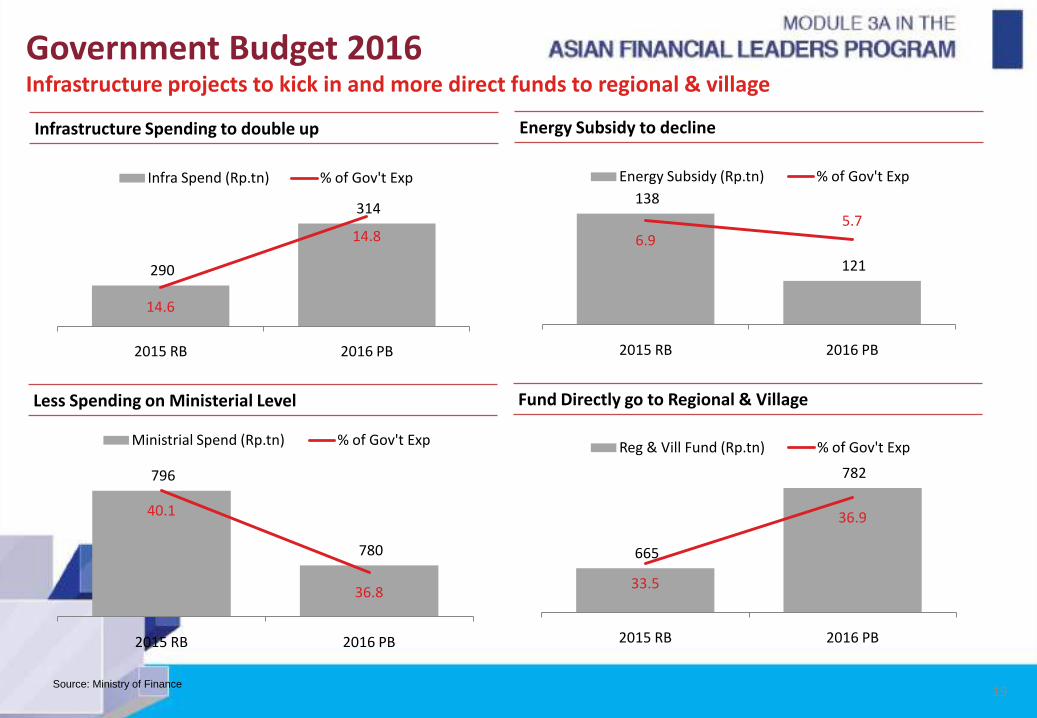

Government Budget 2016Infrastructure projects to kick in and more direct funds to regional & village

Infrastructure Spending to double up

290

314

14.6

14.8

2015 RB 2016 PB

Infra Spend (Rp.tn) % of Gov't Exp

138

121

6.95.7

2015 RB 2016 PB

Energy Subsidy (Rp.tn) % of Gov't Exp

796

780

40.1

36.8

2015 RB 2016 PB

Ministrial Spend (Rp.tn) % of Gov't Exp

665

782

33.5

36.9

2015 RB 2016 PB

Reg & Vill Fund (Rp.tn) % of Gov't Exp

Energy Subsidy to decline

Less Spending on Ministerial Level Fund Directly go to Regional & Village

Source: Ministry of Finance

20

The Government is focusing on basic infrastructureBetter connectivity for remote areas to reduce costs

Source: Ministry of Finance

21

o Financing Breakdown (2015 – 2019)

Indonesia Infrastructure Projects and Financing SchemesPPP, SOEs and Private Sector as Alternatives to Direct Budgetary Spending

o Establishment of PPP Unit

Total Financing Needs:

~US$345.1 bn

Govt & Local Budget (41.3%)

Financing Gap

SOE(22.2%)

PPP(36.5%)

~US$142.4 Bn

~US$76.7 Bn

~US$126.0 Bn

Broad Objective

• Champion project preparation and acceleration of the PPP agenda in Indonesia

Core Mandates

• Improve quality of project selection under KKPPI – OBC criteria• Support project preparation through PDF support and use a high quality Transaction

Advisor• Act on behalf the Minister of Finance in providing government support approvals for

projects

AdditionalMandates

• Coordinate all public finance instruments• Provide input for PPP Policy Development and Regulations• Implement capacity building program to GCA• One stop shop for PPP promotion & Information

Sea Port New Sea Ports 24

Sea port developments 59

Roads New Roads 2650 km

Highway 1000 km

Road maintenance 46770 km

Bus Corridors 2

Railways Railway lines 24

Intra City Rail Lines 59

Airport New Airports 24

Airplanes for new routes 59

Budget

• Central & Regional Budget (SpecialAllocation Fund & Rural Transfer)

• Mainly to support basic infrastructure projects:

- Food Security: Irrigation, dams etc.

- Maritime: Seaports, shipyards etc.

- Connectivity: Village roads, public transportation etc.

Public Private Partnership

• Certain infrastructure projects to be funded and operated through a partnership between the Indonesian government and private sector companieso Projects Ready for Auction under PPP scheme:o Toll roads projects such as Balikpapan-Samarinda and

Manado-Belitungo Railway projects such as an Express Line into Soekarno-

Hatta International Airporto Water supply such as West Semarang water supply project

• Government to support the PPP via initiatives:o Land Fundo Project Development Facility (PDF)o Indonesia Infrastructure Guarantee Fund (IIGF)o Viability Gap Fund (VGF)o Infrastructure Fundo Availability Payment (AP)

State Owned Enterprise & Private Sector

• Government to inject capital into SOEs –Intention is that through a multiplier effect, more infrastructure projects can be developed

• Key focus areas:o Infrastructure and

maritime developmento Transportation and

connectitvityo Food security

• Medium term infrastructure developments in focus:o Water Supplyo Airportso Seaportso Electricity and power

plantso Housingo Mining

Source: Ministry of Finance

22

Alternative Source of Infrastructure FinancingSOEs and PPP become alternative source of funding to supplement Government Budget

2015 – 2019 Infrastructure Plan

• New Roads – 2650 km• Highway – 1000 km• Road Maintenance – 46,770 km• Bus Corridors - 2

• New Sea ports – 24• Sea Port Development – 59• Pioneer Cargo Ships

• New Airports – 24• Airport Infrastructure Development

Airplanes - 20

• Rail Lines – 2,159 km• Intra City Rail Lines – 1099 km

Infrastructure Financing Needs 2015 - 2019 Scenario 1 (full Scenario)

Scenario 2 (PartialScenario)

Baseline (Baseline)

Roads 1,274 851 637

Rail System 278 222 140

Urban Transportation 155 115 75

Sea Transportation 563 424 282

Ferry and Other Waster Transportation 91 80 60

Air Transportation 182 165 100

Electricity 1,080 762 714

Other Energy dan Gas 535 420 268

Water Resources 1,091 845 645

Water and Sanitation 666 450 330

Public Housing 384 247 180

Information and Communication Technology

242 200 130

Total 6,541 4,781 3,561

SOEs and PPP Become Alternative Source of Funding as Government Budget Could only Support ~20% of our Infrastructure Needs

Bu

dge

t

Pu

blic

Pri

vate

P

artn

ers

hip

an

d p

riva

te

sect

or

• Central & Regional Budget (Special Allocation Fund & Rural Transfer)• Mainly to support basic infrastructure projects:o Food Security: Irrigation, dams etc.o Maritime: Seaports, shipyards etc.o Connectivity: Village roads, public transportation etc

• Government support for PPP:o Land Fund: Modification and simplification of land acquisition processo Project Development Facility:through PT Sarana Multi Infrastructureo Indonesia Infrastructure Guarantee Fund (IIGF)o Viability Gap Fund (VGF)o Infrastructure Fund & Availability Payment (AP)

• Projects Ready for Auction under PPP Scheme:o Toll roads projects such as Balikpapan-Samarinda, Manado-Bitungo Railway projects such as Halim-Soetta Airport Express Railwayo Water supply such as West Semarang water supply project

Stat

e O

wn

ed

En

terp

rise

s

• Government to inject capital to SOEs – with leveraging process a multiplier effect, more infrastructure projects can be developed

• Key Focus areas:o For commercial and/or complex projects

• Medium term infrastructure developments focus: electricity and power plants, toll road

Source: Ministry of Finance

Economic Policy Package I – XIIFocusing on investment climate-incentive

Source: Bank Indonesia and Ministry of Finance

Source: Bank Indonesia and Ministry of Finance

Economic Policy Package XIIFocusing on improving the ease of doing business and targeting Indonesia to be ranked 40 on Ease of Doing Business in 2017

Through 10 points of policy, streamlining was pursued in procedures to start business, completion time for establishing business, and number of required permits

Stimuli to Maintain Purchasing Power and Promote Investments

Stimuli to maintain Purchasing Power Stimuli to promote Investments

Source: Ministry of Finance

Key Reforms in Negative Foreign Investment List

Cold Storage Sports Center;Film Processing Lab; Crumb Rubber

Restaurant; Bars Pharmaceutical Raw Material Manufacturing

Toll Road Operator;Telecommunication Testing Company

Revision of “Partnership” category to refer to partnership with Micro, Small and Medium

Enterprise (MSMEs)

Professional Training; Golf Course Management; Air Transport Support

Services; Travel Bureau

Consultancy for Construction1 Telecommunication Provider with Integrated Service

Distribution; Warehousing

Private Museum; Catering; Apparel Manufacturing; Exhibitions &

Conventions

Strengthen implementation of Negative Investment Law through

active roles from Ministries, Agencies and Regional

Government

Grandfather Law: If a particular sector is tightened in

future, existing foreign investor does not need to comply with

tighter stake

1. For total project value of Rp10 billion and aboveAllowed foreign stake (%)

Increase in Allowed Foreign Stake (Before and After Relaxation)

100%49% 49%

95%

51%

51% 85%100% 100% 100%

100%67% 67%

67% 67% 67%55%

51%33%

65%

Relaxation of Negative Foreign Investment List will Promote Healthy Competition

Source: Ministry of Finance

Government’s Investment strategy 2015-2019

Power Generation35 GW new

projects

7 GW projects in

the pipeline

Labor-intensive industry TextileFood &

BeveragesFurniture Toys

Import-substitution industry

Chemical & Pharmaceutical

Iron & Steel

Export-oriented industry

ElectronicsCPO &

derivative products

Wood products, pulp & paper

Automotive

MachineryRubber

products

Fish & derivative products

Shrimp

Downstream industry of natural resources

Cacao Sugar Smelter

Maritime Shipping Ship building Sea port Cold storage ICT for maritime

TourismStrategic tourism

areasMICE

Source: Ministry of Finance

28

Business Sector Investment Priorities: 1. Power Generation

To sustain economic growth of 6.9 per year (RPJMN 2015-2019), with 8.8% growth in electricity demand and electrification ratio 97.2%

Additional electricity infrastructure 2015 - 2019Development of electricity infrastructure 2015 -2019: 42 GW (7 GW Construction, 35 GW Pre-Construction)

By PLN (State Electricity Company):Generator: 17.4 GWTransmission: 50 thousand KMSSubstation: 743 location

By Prviate:Generator: 24.9 GWTransmission: 360 kms

Needs of Capital Expenditure:Rp 545 Tn

Needs of Capital Expenditure:Rp 545 Tn

Gas23%

Coal65%

Water5%

Geothermal5% Fuel

2%

2019

Gas

Coal

Water

Geothermal

Fuel

Gas25%

Coal54%

Water6%

Geothermal5% Fuel

10%

2014

Gas

Coal

Water

Geothermal

Fuel

Source: PLN, 2014

29

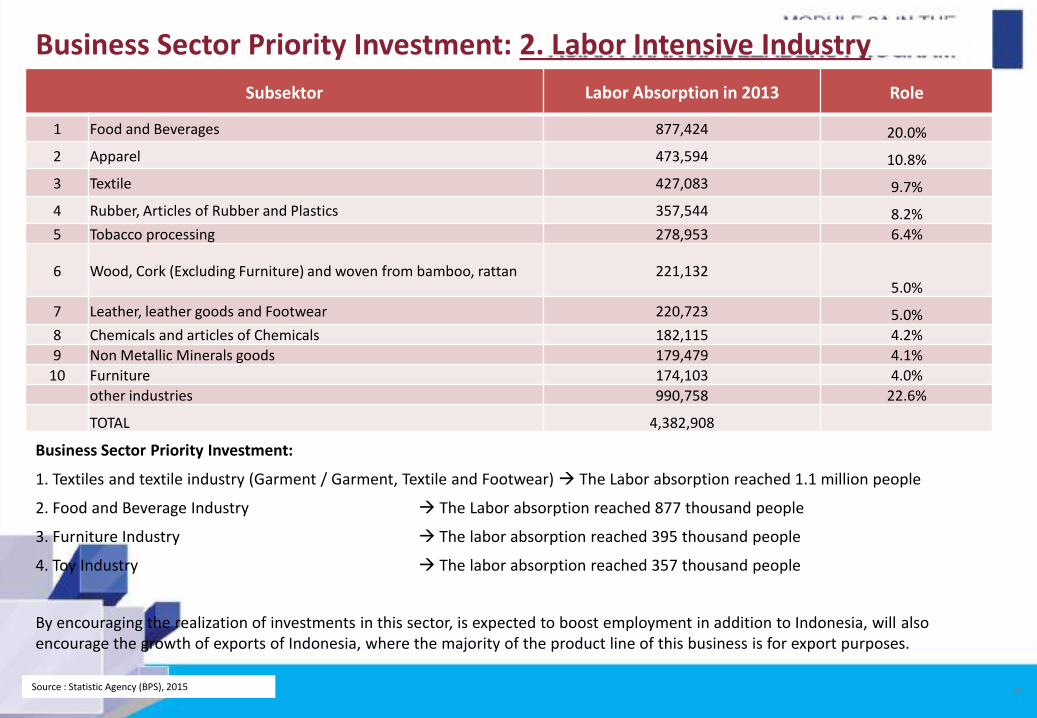

Business Sector Priority Investment: 2. Labor Intensive Industry

Business Sector Priority Investment:

1. Textiles and textile industry (Garment / Garment, Textile and Footwear) The Labor absorption reached 1.1 million people

2. Food and Beverage Industry The Labor absorption reached 877 thousand people

3. Furniture Industry The labor absorption reached 395 thousand people

4. Toy Industry The labor absorption reached 357 thousand people

By encouraging the realization of investments in this sector, is expected to boost employment in addition to Indonesia, will also encourage the growth of exports of Indonesia, where the majority of the product line of this business is for export purposes.

Subsektor Labor Absorption in 2013 Role

1 Food and Beverages 877,424 20.0%

2 Apparel 473,594 10.8%

3 Textile 427,083 9.7%

4 Rubber, Articles of Rubber and Plastics 357,544 8.2%

5 Tobacco processing 278,953 6.4%

6 Wood, Cork (Excluding Furniture) and woven from bamboo, rattan 221,132 5.0%

7 Leather, leather goods and Footwear 220,723 5.0%

8 Chemicals and articles of Chemicals 182,115 4.2%

9 Non Metallic Minerals goods 179,479 4.1%

10 Furniture 174,103 4.0%

other industries 990,758 22.6%

TOTAL 4,382,908

Source : Statistic Agency (BPS), 2015

30

Business Sector Investment Priorities: 3. Import Substitution Industry

NO Business Filed 2010 2011 2012 2013

1Basic Chemical Industry, Chemical Products, and Pharmaceutical

(22,7) (34,5) (39,5) (39,0)

2Basic Metal Industry, Metal Products, Machinery & Electronics

(21,6) (27,6) (37,1) (35,8)

3Industrial Transport Equipment & Other Transportation

(10,3) (11,8) (14,5) (8,5)

4Industrial Transport Equipment & Other Transportation

(1,1) (1,2) (1,5) (1,7)

5 Non Metallic Minerals Industry 0,3 0,2 (0,4) (0,4)6 Other industries 2,5 2,3 2,4 2,4

7Paper Industry, Manufactures of Paper, & Printing

3,0 2,5 2,5 2,5

8 Leather, leather goods & Shoes 1,9 2,3 2,5 2,89 Wood industry 2,6 3,0 3,0 3,210 Textile Industry 6,1 6,5 5,8 5,7

11 Rubber Industry, Manufactures of Rubber & Plastics

8,2 12,7 8,3 7,3

12 Food Industry 14,5 17,6 17,5 16,2

INDUSTRIAL SECTOR (16,6) (28,0) (51,0) (45,3)

The development of trade balance 12 industry groups the highest trade balance deficit(Export Import)

(Source: Ministry of Trade)

Business Sector Priority of Investment:1. Basic Chemical Industries (Petrochemical, Pharmaceutical, and Oil Refinery)

2. Iron and Steel Industry

Source: Ministry of Trade, 2015

31

Business Sector Investment Priorities: 4. Export-Oriented IndustryTop 10 Traditional Commodity Indonesia

NO Commodity 5 Main Destination Countries

1. TPT United States, Japan, Germany, Turkey, South Korea,

2. Electronic Singapore, United States, Japan, Hongkong, China

3. Rubber and Rubber Products United States, Japan, China, South Korea, Singapore,

4. Palm Oil Hong Kong, India, Vietnam, China

5. Forest Products Indian, China, Malaysia, Bangladesh, the Netherlands,

6. Foot Wear Japan, China, United States, South Korea, Australia,

7. Automotive United States, Belgium, Germany, England, Holland,

8. Shrimp Thailand, Japan, Saudi Arabia, Philippines, Malaysia

9. Cocoa United States, Japan, China, Britain, Belgium,

10. Coffee Malaysia, USA, Singapore, North Korea, Spain

Business Sector Priority Investment:1. Rubber2. Palm Oil3. Forest Products4. Shrimp5. Cocoa6. CoffeeSource: Ministry of Trade, 2015

32

Business Sector Priority Investment: 5. Agroindustry

Business Sector Priority for Agroindustry (processed products):

1. Crude Palm Oil (CPO): oleofood industry, oleochemical, energy (Biodiesel) and pharmaceutical

2. Cocoa: cocoa liquor, cocoa cake, cocoa butter, cocoa powder, food and baverages

3. Furniture: wood working, wood furniture, pulp paper industry

4. Sugar: White sugar, refined crystal sugar

Sources: Ministry of Industry, 2014 (Processed)

Examples:

33

Business Sector Priority Investment : 6. Maritime Industry

THREE MAIN BOOSTER MARITIME INDUSTRY

1. Developing Investment in BUSINESS SECTORS AND SERVICE PROVIDER: Shipping Industry Fishing Industry

2. Developing Investment in LOGISTIC INFRASTRUCTURE SECTORS: Development of the port / sea toll Developing Investment in INFORMATION TECHNOLOGY AND COMMUNICATION Appling ICT

Source: RPJMN, 2015

34

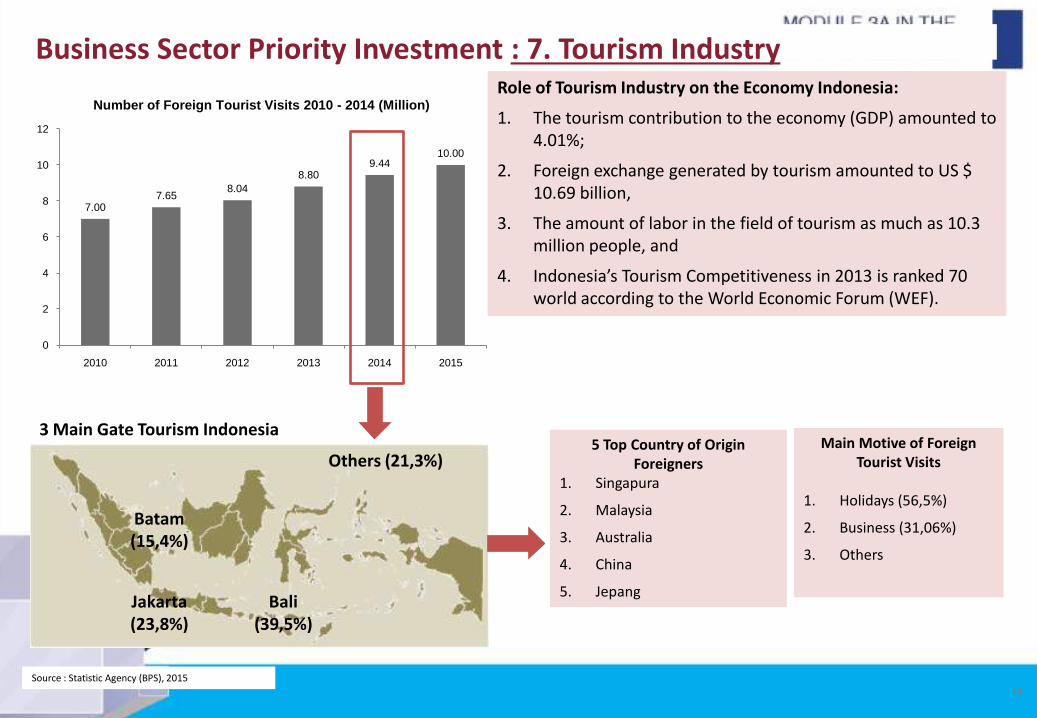

Business Sector Priority Investment : 7. Tourism Industry

3 Main Gate Tourism Indonesia

Jakarta(23,8%)

Bali(39,5%)

Batam(15,4%)

Others (21,3%)5 Top Country of Origin

Foreigners1. Singapura

2. Malaysia

3. Australia

4. China

5. Jepang

Main Motive of Foreign Tourist Visits

1. Holidays (56,5%)

2. Business (31,06%)

3. Others

Role of Tourism Industry on the Economy Indonesia:

1. The tourism contribution to the economy (GDP) amounted to 4.01%;

2. Foreign exchange generated by tourism amounted to US $ 10.69 billion,

3. The amount of labor in the field of tourism as much as 10.3 million people, and

4. Indonesia’s Tourism Competitiveness in 2013 is ranked 70 world according to the World Economic Forum (WEF).

Source : Statistic Agency (BPS), 2015

7.007.65

8.048.80

9.4410.00

0

2

4

6

8

10

12

2010 2011 2012 2013 2014 2015

Number of Foreign Tourist Visits 2010 - 2014 (Million)

35

Development Way of Tourism Industry Investment in Indonesia

Preparation of investment property, infrastructure, vehicle attractions, tourism services and facilities in 16 National Tourism Strategic Area:

Development of investment in the sector "Meetings, incentives, conferences, and exhibitions (MICE)" in the Main Large Cities Indonesia, that is in Medan, Padang, Batam, Jakarta, Yogyakarta, Surabaya, Bali, Makassar, Manado

Development of "connectivity" with the international world of Indonesian tourism

36

Recapitulation Business Sectors for Investment Priorities 2015-2019

Business Sector Priorities Category Business Fields

Electricity Power 1. 35 GW Electricity Power Project

Labor-Intensive Industries2. Textile and Its Product Industry (Garment, Textile and Footwear) 3. Food and Beverage Industry4. Furniture Industry5. Toys Industry

Impor Substitution Industry 6. Basic Chemical Industry (Petrochemical, Pharmaceutical, and Oil Refineries)7. Iron and Steel Industry

Export Oriented Industry 8. Rubber Commodity9. Crude Palm Oil10. Forest Product11. Shrimp12. Cocoa Commodity13. Coffee Commodity

Agro Industry 14. Processed Crude Palm Oil15. Processed Cocoa16. Furniture17. Processed Sugar

Maritime Industry 18. Shipping Industry19. Fishing Industry20. Port/Sea toll21. ICT Maritime Sector

Tourism 22. 16 National Tourism Strategic Area23. Meetings, incentives, conferences, and exhibitions (MICE)

Source: Ministry of Finance

The Future of Indonesia

Long Term Strategies to Achieve Sustainable Growth Key focus to strengthen Indonesia’s economic development fundamentals

Maintain Purchasing

Power

• Maintain price stability • Provide social security for workers • Improve basic needs services to the poor : Health services, Education,

Conditional cash transfer • Provide better employment climate, particularly related to min. wage

policy

• Promote Public Private Partnership (PPP) as infrastructure development financing scheme

• Develop fiscal and non-fiscal incentive and investment facilities to attract direct investment

• Improve the role of SOE and private in Infrastructure development• Develop the alternative infrastructure financing such as infrastructure

bank, trust fund, and infrastructure bond

• Develop downstream industries particularly on primary sectors (agricultural and mining sector)

• Increase the supply of high value added and competitive goods • Increase export quality, determine competitive price and develop

international standard services • Participate in the global value chain and the global production network

to enhance export performance • Improve quantity and quality of exports in manufacturing and services

sector • Develop a more efficient trade facility, particularly related to permit

process • More effective import management

Accelerate Infrastructure Development

State Owned Enterprise

& Private Sector

Strategies & Policy Formulations to Boost Investments

1. Maintain economic stability to promote strong business and investment climate

2. Simplify licensing and investment procedures

3. Harmonize investment regulations between central government and local governments

4. Consistently improve the involvement of state owned enterprise (SOE) in infrastructure development

5. Increase the role of banking institutions in lending rate development, especially for working capital and investment credits

6. Expand the role of non-bank financial institutions in the development of infrastructure financing alternative

Source: Ministry of Finance

Conducive environment underpinning growth fundamentalsThe fundamental long term growth drivers for Indonesia remain strong – equipped with abundant naturalresources, a young and technically trained workforce and a large consumer base with a fast growing spendingpower

The largest economy in South-East Asia

According to McKinsey, Indonesia is projected to be the 7th largest economy in the world by 2030 5.9% average real GDP growth over

the period 2008-2013 Exports are 23.7% of GDP for the

year of 2013, one of the lowest in Asia, creating low volatility in GDP Foreign direct investment grew at

an average rate of 21.1% from 2010-2013

Male Female

A large, culturally diverse, young and vibrant workforce

4th most populous country in the world 66.6% of the population is of

working age(1)and 68.5% were 39 years and younger as of 2012 Working population projected to

grow at 0.7% compared to 0.5% CAGR for total population from 2012-2017 A high literacy rate of more than

90%

Large consumer base with fast growing spending power

~7mn people are expected to join the middle class each year Consumer expenditure has grown

at a 12.3% CAGR from 2007-2012 and is expected to continue at a 9.1% rate from 2012-2017 Disposable incomes are projected

to grow at 12.1% from 2012-2017 According to McKinsey, 135-

170mn people will join the consuming class by 2030

Increase in infrastructure investment to improve overall efficiency

Announced an expansion of fiscal spending on infrastructure by 19.2% CAGR from2012 to2014 Infrastructure investments are spread

over Indonesia’s 6 economic corridors Encompass various sectors such as

seaports, roads, railways, airports, energy and many others Government continues to align

regional and national regulations to attract further private sector investors

Thank You

Important Notice

This presentation has been prepared by CIMB Group exclusively for the benefit and internal use of the recipient in order toindicate, on a preliminary basis, the feasibility of possible transactions. Terms contained in this presentation are intended fordiscussion purposes only and are subject to a definitive agreement. All information contained in this presentation belongs toCIMB Group and may not be copied, distributed or otherwise disseminated in whole or in part without the written consent ofCIMB Group.

This presentation has been prepared on the basis of information that is believed to be correct at the time the presentation wasprepared, but that may not have been independently verified. CIMB Group makes no express or implied warranty as to theaccuracy or completeness of any such information.

CIMB Group is not acting as an advisor or agent to any person to whom this presentation is directed. Such persons must maketheir own independent assessment of the contents of this presentation, should not treat such content as advice relating tolegal, accounting, taxation or investment matters and should consult their own advisers.

CIMB Group or its affiliates may act as a principal or agent in any transaction contemplated by this presentation, or any othertransaction connected with any such transaction, and may as a result earn brokerage, commission or other income. Nothing inthis presentation is intended to be, or should be construed as an offer to buy or sell, or invitation to subscribe for, anysecurities.

Neither CIMB Group nor any of its their directors, employees or representatives are to have any liability (including liability toany person by reason of negligence or negligent misstatement) from any statement, opinion, information or matter (express orimplied) arising out of, contained in or derived from or any omission from the presentation, except liability under statute thatcannot be excluded.