nb pb

TRANSCRIPT

“A Comparative Study of Nationalized & Private

Banks with Respect to Loan Process & Facilities for

SMEs”

History of Indian Banking Sector

Banking in India originated in the first decade of 18th century

The General Bank of India coming into existence in 1786.

The first fully Indian owned bank :- Allahabad Bank :-established in 1865.

In 1935, The Reserve Bank of India formally took on the responsibility of regulating the Indian banking sector.

After independence in 1947, the Reserve Bank was nationalized and given broader powers.

Current Scenario of Indian Banking Sector

Banking Industry in India is going through a transitional phase.

Private sector Banks have pioneered modern banking facilities

The PSBs are still grappling.

Flow Chart of Indian Banking Sector

Small & Medium Enterprises

20%

12%

19%10%

9%

8%

8%

6%8%

Retail

Manufacturing

ProfessionalServicesHospitality

Education

Travel

Real State

Logistics

Others

In small enterprise the investment in plant and machinery is more than Rs. 25 lakh but does not exceed Rs. 1 crores.

In medium the investment in plant and machinery is more than Rs.1 crore but does not exceed Rs.10 crores.

Source : Ministry of Micro, Small & Medium

EnterprisesYear 2014

Market Share of Nationalized Banks and Private Banks

SBI -19.10%

ICICI – 10.34%

PNB – 5.48%

BOI – 5.20%

HDFC – 2.91%

Axis - 2.73%

19.10%

10.34%

5.48%

5.20%

2.91%2.73%

SBI

ICICI Bank

PNB

Bank OfIndia

HDFCBank

Axis Bank

Fig 1.1 Market share

Source : NDTV ProfitYear 2010

Market Cap of Nationalized Banks and Private Banks

0.00 50,000.00100,000.00150,000.00200,000.00

SBI

Bank of Baroda

PNB

Canara Bank

Bank of India

182,145.17

37,497.07

34,626.56

18,431.90

17,669.64

Fig 1.2 Market Cap of Nationalized Banks(in Cr)

0.00 100,000.00 200,000.00

HDFC Bank

ICICI Bank

Axis Bank

Kotak Mahindra

IndusInd Bank

200,816.60

170,367.11

92,388.98

73,658.22

29,573.88

Fig 1.3 Market Cap of Private Banks(in Cr)

Source : Money ControlYear 2012

Major Players of Nationalized Banks and Private Banks

12,131.36

4,541.08

3,342.58 2,729.27

1,711.46

0.00

5,000.00

10,000.00

15,000.00

Fig 1.4 Major Players of Nationalized banks in terms of net profit(Rs. Cr)

9430.69

8478.38

6217.67

1617.78 1502.52

0

2000

4000

6000

8000

10000

Fig 1.5 Major Players of Private banks in terms of net profit(Rs. Cr)

Source : NDTV ProfitYear 2012

Current TrendsTele Banking

Real Time Gross Settlement (RTGS)

Electronic Funds Transfer (EFT)

Point of Sale Terminal

Automatic Teller Machine (ATM)

Electronic Clearing Service (ECS)

SWOT Analysis of SBISWOT Analysis

Strength

1. The biggest bank in the country

2. Has a separate act for itself. Thus, a special privilege.

3. Biggest branch network in the country

4. First public sector to move to CBS

Weakness

1. Huge amount of staff

2. Expected to experience high level of attrition due to

retirement of its top management

3. Still carries the image of the old Govt. sector bank

Opportunity

1. Pool in talent to replace the going top management to serve

the next generation

2. Make better use of its CRM

3. Expansion into rural areas

Threats

1. Consolidation among private banks

2. New bank licenses by RBI

3. Foreign banks that have sophisticated products

SWOT Analysis of ICICI Bank

Strength

1. Front runner in the Indian Private Banking Sector

2. Strong presence via its branches

3. High use of technology to make life simpler for the

customers

4.Large no. of facilities for the customers in terms of products

and services

5. Over 75,000 employees at ICICI

6. Decades of Experience in the Banking sector along with

marketing has added to the brand name

7. Presence in over 19 countries

Weakness

1. Too much competition in the banking sector affecting

employee and customer management

2. Many branches in urban areas has led to high cost

Opportunity

1. Opening more branches in the rural areas

2. Use of technology to penetrate rural markets

3. Venturing into countries like Africa where the economy is

coming up

Threats

1. Ever changing RBI policies

2. International and other Competitors

3.Inability to adapt to changing conditions due to large size

Analysis of Questionnaire for SMEs

Years In Business

0

4

6

10

0 2 4 6 8 10 12

< 1 yr

1-5 yrs

5-10 yrs

> 10 yrs

Fig 1.1 No. of years in business

No. of SME’s

Year

s

Annual Turnover

2

6

7

5

0

1

2

3

4

5

6

7

8

20-30 Lakhs 31-50 Lakhs 51-100 Lakhs > 1 crore

Fig 1.2 Annual Turnover

No

. of

SME’

s

Turnover

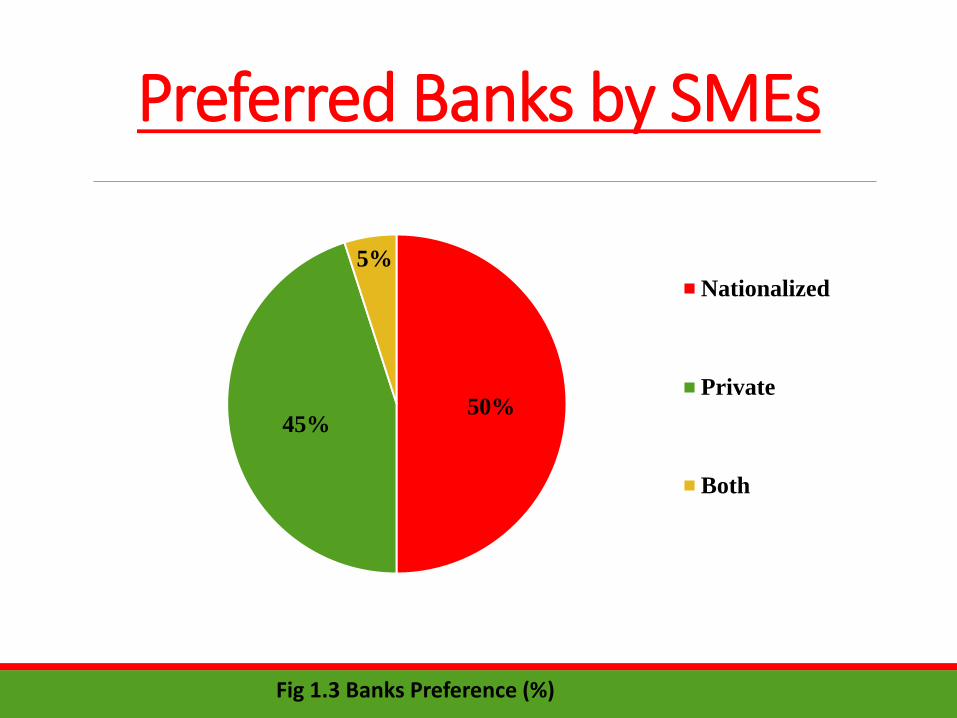

Preferred Banks by SMEs

50%45%

5%

Nationalized

Private

Both

Fig 1.3 Banks Preference (%)

Analysis of Banks Based on Preference

SBI

37%

BOI

18%

BOB

18%

UNION

Bank

9%

IDBI

9%

Others

9%

HDFC

60.00%

ICICI

20.00%

AXIS

10.00%

Kotak

10.00%

ING Vysta

0.00%Others

0.00%

Fig 1.5 National Banks Fig 1.6 Private Banks

Convenience of Interest Rates of Banks

Yes,

72.73%

No,

18.18%

Can't Say,

9.09%

Yes 60.00%

No 30.00%

Can't Say

10.00%

Fig 1.8 Private Banks

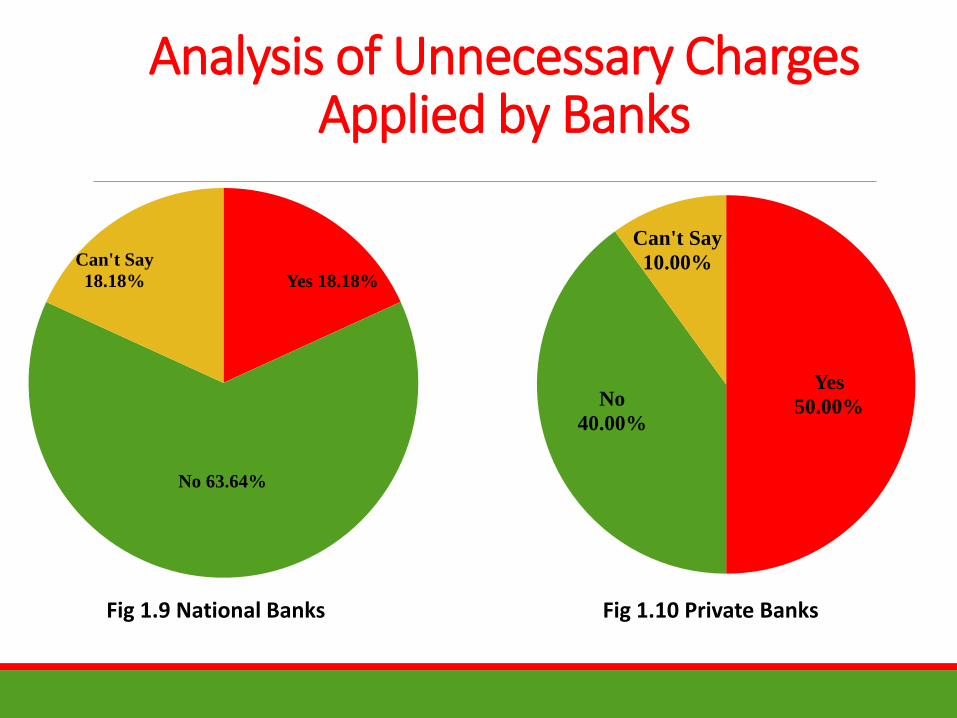

Analysis of Unnecessary Charges Applied by Banks

Yes 18.18%

No 63.64%

Can't Say

18.18%

Yes

50.00%No

40.00%

Can't Say

10.00%

Fig 1.9 National Banks Fig 1.10 Private Banks

Ratings Based on Services

2

3

4

2 2

3

4

2

3

4

2 2

3 3

2 2

3 3

2

33

4

3

2

3

4

3

2

4

3

1

2 2

3

1

2 2

3

2 2

1

2

3 3

1

2

3 3

2

33 3

2 2

3 3

2 2

3

2

0

2

4

SB

I

BO

I

BO

B

UN

ION

IDB

I

ICIC

I

HD

FC

AX

IS

KO

TA

K

OT

HE

RS

Loan Services Staff Knowledge Staff Behaviour

Speed of issuing knowledge Easy Access Abilty to address problems

Fig 1.11 Average Ratings

Banks SBI BOI BOB UNION CANARA DNSBLack of

assistance1 2 1 1

Security Concern

2 1 1 1

High interest rate

1

Limited service 1 2

Quality of service

1

Waiting 4 2 1

Impersonality of the service

No disadvantage

Issues in Nationalized Bank

Issues in Private Bank

Banks IDBI ICICI HDFC AXIS KOTAK

Lack of assistance 1

Security Concern 1 1 1

High interest rate 2 1 1

Limited service 1 1

Quality of service

Waiting 1

Impersonality of the service 1 1

No disadvantage 1 1

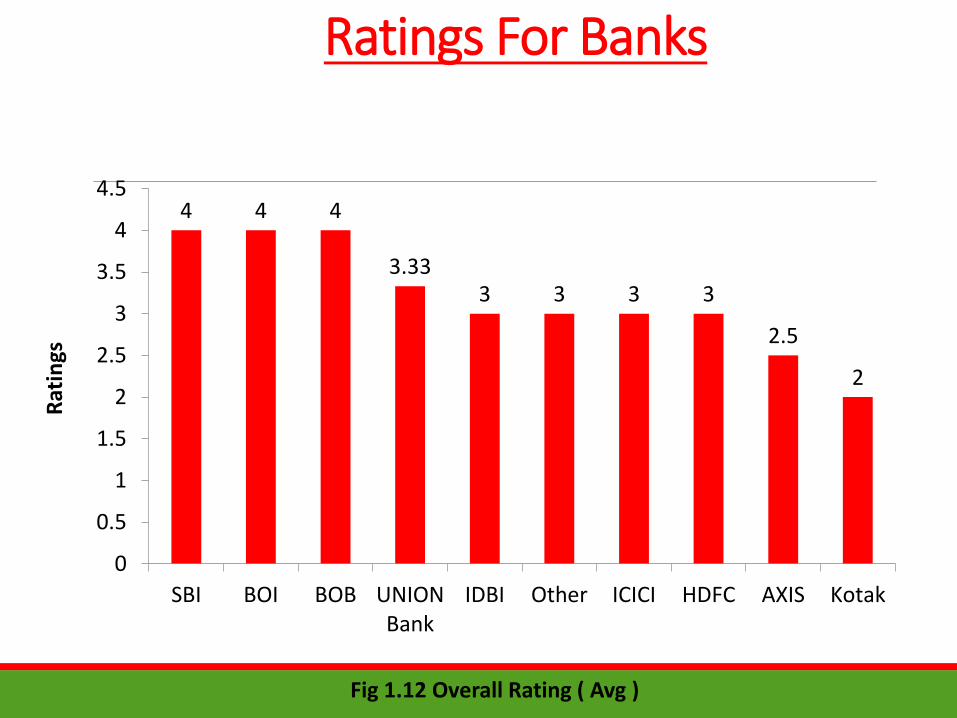

Ratings For Banks

4 4 4

3.333 3 3 3

2.5

2

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

SBI BOI BOB UNIONBank

IDBI Other ICICI HDFC AXIS Kotak

Rat

ings

Fig 1.12 Overall Rating ( Avg )

Analysis of Response Sheet for Banks

Why do you provide loans to SMEs?

Great growth chances and low risk involved

To promote entrepreneurship

To bailout SMEs

Government of India guidelines

Documents Required

63.64%

81.82%

36.36%

18.18%

Financial Stability

Last 3 years BalanceSheet

Project Cost

Future Balance Sheet

Fig. 1.13 Documents Required

What is the Interest Rate ?

14% 14%12% 12% 12% 12% 12% 12%

11% 10%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Fig 1.14 Interest Rates

Inte

rest

Rat

e

What Guaranty do you take?Collateral Securities,

27.27%

Mortgage of company, 27.27%

Personal gurantee of

owner, 45.45%

No Gurantee, 18.18%

Collateral Securities

Mortgage of company

Personal gurantee ofowner

No Gurantee

Fig 1.15 Guarantee Preferences

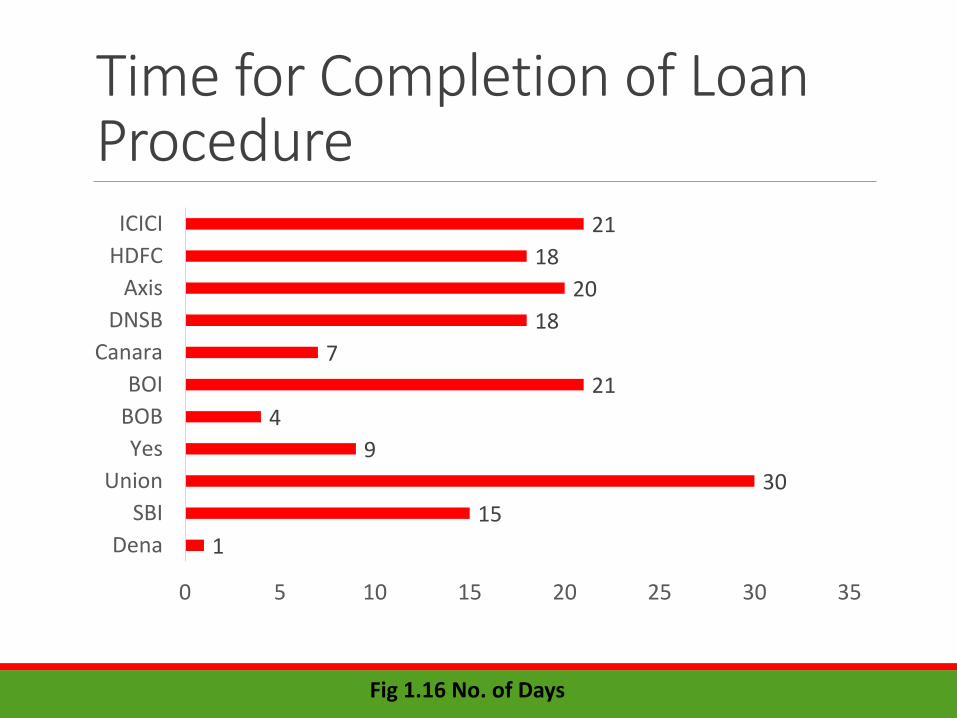

Time for Completion of Loan Procedure

1

15

30

9

4

21

7

18

20

18

21

0 5 10 15 20 25 30 35

Dena

SBI

Union

Yes

BOB

BOI

Canara

DNSB

Axis

HDFC

ICICI

Fig 1.16 No. of Days

Loan Recovery Process

Monthly Installments

Post Dated Cheques on ECS

What about Loan Defaulters?

Send legal notice

Hire 3rd party recovery agents

Taking possession of company assets

Any Special Facilities for SMEs?

Cash credit facility

Overdraft

Term Loan

Salary Accounts

Special interest Rates

Current Trends in Lending w.r.t SME

SMEs continued to face the dual challenges of an uneven recovery and bank deleveraging.

Despite monetary easing, credit availability was a constraint for SMEs.

Credit conditions remained tighter for SMEs in relation to large firms.

Alternative sources of finance for SMEs and entrepreneurs were limited and volatile.

Most governments extended SME finance support measures and adopted new instruments.

Analysis of Core indicators in financing SMEs

The allocation of credit by size of firm.

Varied interest rates.

Payment delays.

Bankruptcies.

BIBLIOGRAPHYInternet websites:

Statistical Tables Related to Banks in India, Reserve Bank of India, Retrieved from http://www.rbi.org.in

Micro, Small and Medium Enterprises, Reserve Bank of India, 30 December 2013, Retrieved from http://www.rbi.org.in

Shareholding Pattern, 30 June 2013, Retrieved from MoneyControl.com.

Market share, Retrieved from http://www.profit.ndtv.com

Top Companies in India by Market Capitalization – BSE, 6th August 2014, Retrieved from http://www.moneycontrol.com/stocks/marketinfo/marketcap/bse/banks-public-sector.html

Indian Banking Sector, January 2013, Retrieved from http://www.ibef.org

Top Companies in India by Net Sales, August 2013, Retrieved from http://www.moneycontrol.com/stocks/marketinfo/netsales/bse/banks-public-sector.html

Top Companies in India by Net Sales, August 2013, Retrieved from http://www.moneycontrol.com/stocks/marketinfo/netsales/bse/banks-private-sector.html

http://www.moneycontrol.com/financials/icicibank/profit-loss/ICI02#ICI02

RECENT TRENDS IN INDIAN BANKING INDUSTRY, Sanjay Kumar Dhanwani, Retrieved from http://www.abhinavjournal.com

https://www.sbi.co.in

History, ICICI bank, Retrieved from http://www.icicibank.com/aboutus/history.page

SME Segment, Loan Schemes, Retrieved from http://www.sbi.co.in/portal/web/interest-rates/sme-segment

Loans for SME Segment, Retrieved from http://www.icicibank.com/business-banking/business-loans/working-capital/loans-for-sme-segment.page?

Presenters:

Sumeet Bomblat 03

Shivkumar Chauhan 04

Shounak Dasgupta 06

Nitesh Walke 60

Tanay Mishra 29

Advait More 28

Rushabh