ncr consumer mobility and e-commerce zinnov study

TRANSCRIPT

Previous Next

9:12 AMFriday, January 24, 2014

Click to start

Zinnov Consumer Mobility & E-commerce Survey

Previous Next

Contact Us

Consumer Mobility

Ecommerce

Previous Next

Ecommerce

Application Usage

Device Change Trend

Place of Purchase

App Authenticity

Concern

Spending on Devices

Ad Clicking Behavior

Devices Adoption

Payment Mechanisms

Consumer Mobility

Previous NextDevice Adoption

Mobility device adoption

Smartphone users also own a

Tablet 16%

Matriculates:

Graduates & above: 86%

47%

Educationpositively influences the

adoption of Laptops

Smartphone users also own a

Laptop/Desktop83%

76%Smartphone users use

Android

Previous NextDevice Change Trend (1/2)

Migration to Smartphone

An average respondent migrated to Smartphones

26 months ago

Addition of new users every year

31% new users

Urban:

Sub-Urban:

27 months

23 months4 months

late

Sub-Urban users

Previous NextDevice Change Trend (2/2)

39% users Retain Smartphones for at least 2 years

Retention of Smartphones

Urban :

Sub- Urban :

42%

31%

Urban users

more prone to retain smartphones

Age < 40 years :

Age > 60 years :

39%

56%

Retention increases

with Age

Retention of smartphones for at least 2 years

Previous Next

Online Device Purchase

~15%Devices :

~10%Devices :

Devices : ~4%

Windows phones fare best in sales through

e-retailing

18%Income >10 Lac :

6%Income < 3 Lac :

Affluentusers more likely to

purchase phones online

10% Smartphonesare sold online

Place of Purchase (1/2)

Previous NextPlace of Purchase (2/2)

Multi-brand Organized Retail, a hit in Urban India

45%Multi Brand

Organized Retail

25%Authorized Single-brand Showroom

Urban

Respondents

52%Local Mobile

Shop

25%Multi Brand

Organized Retail

Sub - Urban

Respondents

Offline Device Purchase

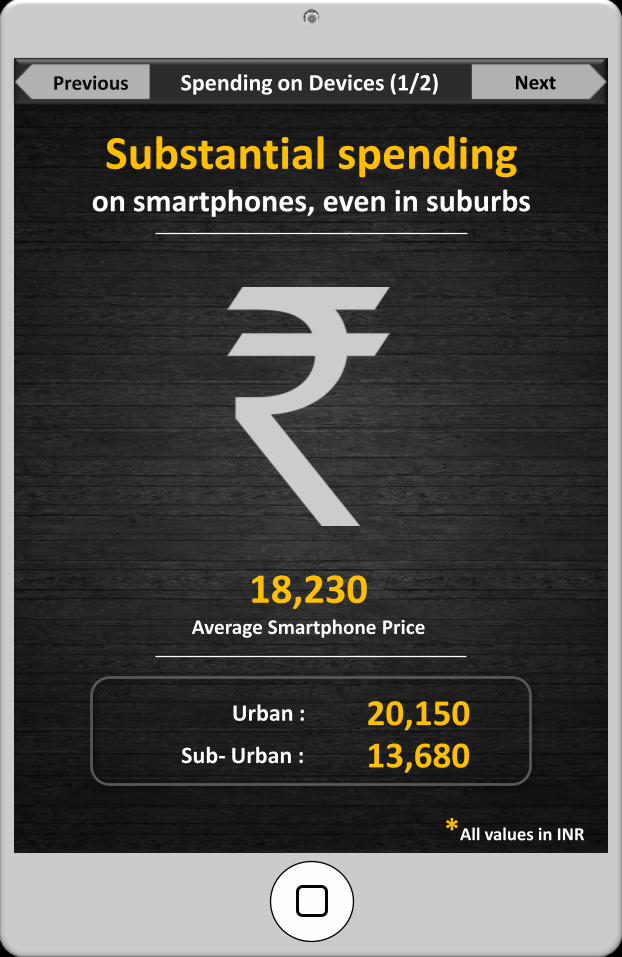

Previous NextSpending on Devices (1/2)

Substantial spending on smartphones, even in suburbs

18,230 Average Smartphone Price

*All values in INR

Urban :

Sub- Urban :

20,15013,680

Previous NextSpending on Devices (2/2)

Education and affluence positively influence spending

*All values in INR

Masters & above :

Matriculation & below :

19,970

11,740

> 10 Lac :

< 3 Lac :

23,190

14,160

Education

Income

Previous NextPayment Mechanism

*For Buying Devices

**89% sub-urban respondents prefer to pay by cheque/cash

Urban :

Sub- Urban** :

41%

5%

> 10 Lac :

< 3 Lac :

44%

20%

Location

Income

Plastic money usage* high in Urban and Affluent Respondents

Previous NextApplication Usage (1/4)

87%Respondents

download Apps

83%Do Not Purchase

Any Apps

Despite high usage, tendency to purchase apps low

INR 417*Average

Spendingon Apps

26 Apps*Average # of

Apps Downloaded

6 Apps*Average # of

Apps Purchased

*Figures are for those who purchase Apps

Previous NextApplication Usage (2/4)

More apps downloaded by Youngrespondents compared with elders

~2x Age 16-20 yrs: 29

13Age > 60 yrs:

Urban: 28

22Sub-Urban:More apps downloaded by Urban

users compared to Sub-Urban

27%

Male: 28

22Female:More apps downloaded by Male

users compared to females

27%

Trends in App Downloads

Previous NextApplication Usage (3/4)

Trends in Paid Apps

AffluencePositively Influences download and Spending on Apps

Android users Purchase and spend highest on apps

Income > INR 10 Lac

Income < INR 3 Lac

INR 636

INR 89

7

3

7

5

INR 417

INR 340

Amount spent on Apps

No. of Paid Apps downloaded

Amount spent on Apps

No. of Paid Apps downloaded

Previous NextApplication Usage (4/4)

App Use Cases

High Usage Among Urban and Sub-urban Respondents

AlikeMusic/Video

Internet Surfing

88%

93%86%

Social Networking

95%Gaming

83%

Previous NextApp Authenticity Concern

~46%* users not concerned About App Authenticity

Checks to Ensure Authenticity

68%**

Consumer Reviews

27%**

Developers Profile

24%**

Consultation with friends and peers

Indifference to Authenticity

Urban

40%*Sub-urban

60%*Higher in Suburbs:

Linked with Age:

60+ years

100%*21-25 years

42%*

<<

<<

*Among respondents who download Apps

* *Among respondents who download Apps and are concerned

Previous NextAd Clicking Behavior (1/2)

63% users Do not click on ads

Male: 8 ads*

4 ads*Female:

*Among those who click on Ads

More Ads clicked by males compared with females

2x

7 ads* clicked on an average over the last one year

Previous NextAd Clicking Behavior (2/2)

Incentivizing Ad Clicking

Interested

NotInterested

3/4th users uninterested in sharing demographic data in exchange

of incentives

Ads Most clicked

*Among those who click on Ads

46%*respondents

54%* respondents

E-commerceGamingHealth and

Wellness

10%*respondents

Previous Next

Consumer Mobility Ecommerce

Top E-com Websites

Initiation to E-com Sites

Deterrents to E-com Adoption

E-com on Mobility Devices

E-commerce as Info Medium

Purchasing Trends

Payment Mechanisms

Adoption of E-commerce

Previous NextAdoption of E-Commerce (1/2)

Massive e-commerce uptake

OVERALL RESPONDENTS : 34%

Female :

Male :

34%

34%

Similar adoption of e-commerce among Males and Females

Urban :

Sub-Urban :

41%

18%

~2x more urban respondents

shopping online

Online shopping at least once a month

Previous NextAdoption of E-Commerce (2/2)

Reluctance to E-com

32%Income < INR 3 Lac:

22%Income >INR 10 Lac:

25% Respondents do not intend to shop online

46%Sub-Urban :

15%Urban :

Less resistance among

Affluent Respondents

10%

More reluctance among

Sub-Urban Respondents

3x

28%Males :

16%Urban :More males reluctant to shop online

~2x

Previous NextE-com as Info Medium

~50% consumers Use E-com websites to

research on Products before buying them Offline

Urban Respondents :

Sub-Urban Respondents :

64%

20%

E-com websites widely used as

Medium of Information

Tendency higher among urban respondents

Previous NextPurchasing Trends (1/2)

Substantial Percentage of Monthly Budgets spent on

E-commerce

Affluent Respondents spend higher share of

wallet online

Income < 3 Lac :

Income > 10 Lac :

14%

19%

Education positively influences the spending

on E-commerce

Matriculates & less :

Graduates & above :

12%

19%

Average share of e-commerce in expenditures: 19%

Previous NextPurchasing trends (2/2)

Products most shopped for Online

Books

51%

46%Electronic GoodsApparels

47%

Travel Tickets/Packages

47%Shoes

38%

*All figures are for those who shopped online over the last one year

Previous NextPayment Mechanisms

Credit/Debit Card paymentUsers most comfortable using this payment

model

48% respondents use Credit/Debit Cards for e-commerce

transactions

Urban respondents

more comfortable using Credit/Debit

cards

Sub-Urban :

Urban :

36%

50%

Female users more inclined to using

Credit/Debit cards

Females :

Males :

55%

44%

*All figures are for those who shopped online over the last one year

Previous NextTop E-com Sites

Unless specifically asked 73% customers don’t consider

IRCTC ticketing as e-commerce

Brand recall limited to few E-com websites

71%

17.3%

17.5% 29.6%

30%

E-com Websites with Highest Recall

Previous NextInitiation to E-com Sites

Peer Recommendations critical to site selection

13% Influenced by TV ads

40% on Peer Suggestion

35% Through Product Web Search

Initiation on an E-commerce site:

Previous NextDeterrents to E-commerce

31% respondentsBelieve that a local intermediary will help uptake of

E-commerce

Key deterrents to E-com

Concerns regarding product quality

Fear of wrong product delivery

Immediate Product delivery

Preference to visit shops

36%

29.7% 28.7%

30%

Previous NextE-com On Mobile Devices

Education and Affluencepositively influence use of Mobility Devices for

E-commerce

Mobility Devices for E-Com

35% respondents use mobility devices for e-commerce

Smartphones Tablets

Matriculates :

Graduates & above :

8%

37%

Income < 3 Lac :

Income > 10 Lac:

30%

40%

* All values for Smartphone and Tablet users who responded

23%

41%

33%

43%

Previous Next

69 "Prathiba Complex", 4th 'A' Cross, Koramangala Ind. Layout5th Block, KoramangalaBangalore – 560095Phone: +91-80-41127925/6

First Floor, Plot # 131, Sector - 44,Gurgaon – 122002Phone: +91-124- 4420100

21, Waterway AveSuite 300 The WoodlandsTX-77380 USAPhone:+1-281-362-2773

3080 Olcott Street Suite A125, Santa Clara, CA 95054 Phone: +408-716-8432

Level 42, Suntec Tower Three8 Temasek BoulevardSingapore 038988Phone:+65 6829 2123

Meilifang Tower 4, Entrance 4, 10/F #1003,11 Beiyuan Shuangying Road,Chaoyang District, BeijingChina 100012

Thank You

[email protected] www.zinnov.com

@zinnov

This report is solely for the use of Zinnov Client and Zinnov Personnel. No Part of it may be quoted, circulated or reproduced for distribution outside the client organization without prior written approval from Zinnov