near term prospects for the u.s. sugar industry edward evans, sikavas na lampang and john vansickle...

TRANSCRIPT

Near Term Prospects for the U.S. Sugar Industry

Edward Evans, Sikavas Na Lampang and John VanSickle

International Agricultural Trade and Policy Center (IATPC)University of Florida

May 2002

Near Term Prospects for the U.S. Sugar Industry

Edward Evans, Sikavas Na Lampang and John VanSickle

International Agricultural Trade and Policy Center (IATPC)University of Florida

May 2002

Outline

• Trends in U.S. sugar market• Long & short-term issues• Model• Policy scenarios• Results• Conclusions

• Trends in U.S. sugar market• Long & short-term issues• Model• Policy scenarios• Results• Conclusions

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002Consumption Production Imports Ending Stocks

Trends in U.S. Sugar Consumption, Production, Imports and Stocks, FY 1991-

2001(‘000 metric tons)

0

5

10

15

20

25

30

35

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

US Refined US Raw World Refined World Raw

Trends in U.S. and World Raw and Refined Sugar Prices, FY 1991-2001

(U.S. cents a pound)

• New rounds of WTO negotiations on agriculture– Alliance for Sugar Trade Reform and

Liberalization

• Proposed formation of FTAA in 2005– Brazil

• Single sugar market between U.S. and Mexico in 2008

• New rounds of WTO negotiations on agriculture– Alliance for Sugar Trade Reform and

Liberalization

• Proposed formation of FTAA in 2005– Brazil

• Single sugar market between U.S. and Mexico in 2008

Long-Term Issues

• Proposed formation of free trade area with APEC in 2010– Australia

• Impending trade with Cuba– Cuban Humanitarian Trade Act of

1999– Cuban Food and Medicine

Security Act of 1999– U.S.-Cuba Trade Act of 2000

• Proposed formation of free trade area with APEC in 2010– Australia

• Impending trade with Cuba– Cuban Humanitarian Trade Act of

1999– Cuban Food and Medicine

Security Act of 1999– U.S.-Cuba Trade Act of 2000

Long-Term Issues

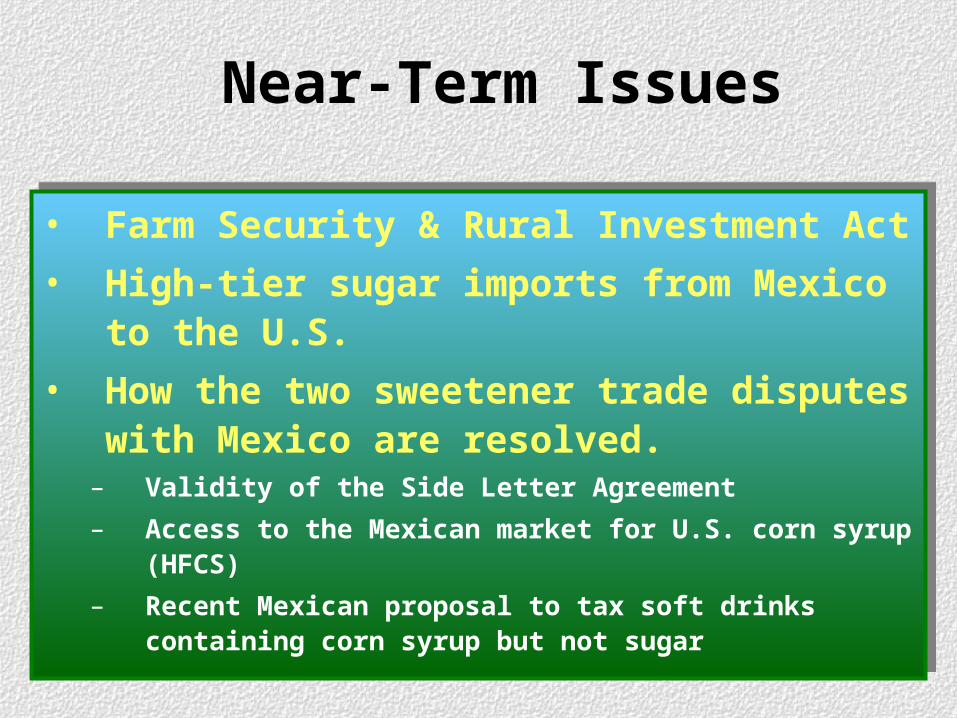

• Farm Security & Rural Investment Act

• High-tier sugar imports from Mexico to the U.S.

• How the two sweetener trade disputes with Mexico are resolved.– Validity of the Side Letter Agreement

– Access to the Mexican market for U.S. corn syrup (HFCS)

– Recent Mexican proposal to tax soft drinks containing corn syrup but not sugar

• Farm Security & Rural Investment Act

• High-tier sugar imports from Mexico to the U.S.

• How the two sweetener trade disputes with Mexico are resolved.– Validity of the Side Letter Agreement

– Access to the Mexican market for U.S. corn syrup (HFCS)

– Recent Mexican proposal to tax soft drinks containing corn syrup but not sugar

Near-Term Issues

1. Farm Security & Rural Investment Act:– Honors International Sugar Commitments

• Effectively increases minimum TRQ from 1.13 to 1.38 million metric tons (MMT)

– Reduces the Burden on Producers• Terminates marketing assessments

• Eliminates the forfeiture penalty

• Eliminates the 1-percentage point payment above the CCC’s cost of borrowing

– Reestablishes No-Net-Cost Feature of Program• Reinstates marketing allotments for domestically

grown sugar

• Pre-Plant Payment-in-Kind Program

1. Farm Security & Rural Investment Act:– Honors International Sugar Commitments

• Effectively increases minimum TRQ from 1.13 to 1.38 million metric tons (MMT)

– Reduces the Burden on Producers• Terminates marketing assessments

• Eliminates the forfeiture penalty

• Eliminates the 1-percentage point payment above the CCC’s cost of borrowing

– Reestablishes No-Net-Cost Feature of Program• Reinstates marketing allotments for domestically

grown sugar

• Pre-Plant Payment-in-Kind Program

Near-Term Issues

Raw Cane Sugar Old Farm Bill

(Cents/lb)

New Farm Bill

(Cents/lb)

Loan rate 18.08 18.08

Less forfeiture penalty 1.00 0.00

Effective loan rate 17.08 18.08

Plus Cost of Loan Redemption and Marketing - Interest expense - Transportation costs - Location discounts

0.911.410.20

0.901.410.20

Effective (Target) Price 19.60 20.59

Calculation of U.S. Average Effective Loan Rate and Target Price for Raw Sugar

2.High-tier sugar imports from Mexico to the U.S.

2.High-tier sugar imports from Mexico to the U.S.

Near-Term Issues

Selected Second-Tier of the U.S., 1995-2008

0

5

10

15

20

25

US

cent

s pe

r po

und

0

5

10

15

20

25

US

cent

s pe

r po

und

Mexico’s Raw Sugar

Most Countries’ Raw Sugar

Years

Year Target Price

High Tariff

Mkting Costs

Implicit Barrier

Max World Raw Sugar Mtk. Price

2001 21.00

2002 21.00

2003 21.00

2004 21.00

2005 21.00

2006 21.00

2007 21.00

Mexico’s High Tier Tariff Scenarios*, 2001-07

(U.S. cents/lb)

*Assumption: Loan Rate of 18 cents a pound, for raw sugar

Year Target Price

High Tariff

Mkting Costs

Implicit Barrier

Max World Raw Sugar Mtk. Price

2001 21.00 10.58

2002 21.00 9.07

2003 21.00 7.56

2004 21.00 6.04

2005 21.00 4.53

2006 21.00 3.02

2007 21.00 1.51

Year Target Price

High Tariff

Mkting Costs

Implicit Barrier

Max World Raw Sugar Mtk. Price

2001 21.00 10.58 1.00

2002 21.00 9.07 1.00

2003 21.00 7.56 1.00

2004 21.00 6.04 1.00

2005 21.00 4.53 1.00

2006 21.00 3.02 1.00

2007 21.00 1.51 1.00

Year Target

Price(1)

High Tariff

(2)

Mkting

Costs(3)

Implicit

Barrier

(4)

Incentive to Ship to

US(1)- (4)

2001 21.00 10.58 1.00 11.58

2002 21.00 9.07 1.00 10.07

2003 21.00 7.56 1.00 8.56

2004 21.00 6.04 1.00 7.04

2005 21.00 4.53 1.00 5.53

2006 21.00 3.02 1.00 4.02

2007 21.00 1.51 1.00 2.51

Year Target

Price(1)

High Tariff

(2)

Mkting

Costs(3)

Implicit

Barrier

(4)

Incentive to Ship to

US(1)- (4)

2001 21.00 10.58 1.00 11.58 9.42

2002 21.00 9.07 1.00 10.07 10.93

2003 21.00 7.56 1.00 8.56 12.44

2004 21.00 6.04 1.00 7.04 13.96

2005 21.00 4.53 1.00 5.53 15.47

2006 21.00 3.02 1.00 4.02 16.98

2007 21.00 1.51 1.00 2.51 18.49

0

2

4

6

8

10

12

14

16

18

20

2001 2002 2003 2004 2005 2006 2007

Incentive for Mexico to Ship Over-the-Quota Sugar to the U.S. Market, 2001-07

(U.S. cents/lb)

Model

• Modified version of World Sugar Policy Simulation Model

– Dr. Won Koo, North Dakota State University

– Dynamic partial equilibrium net trade model

– Comprises 18 sugar producing and consuming countries and regions

– Makes specific assumptions about growth rate of various macroeconomic policy variables

• Modified version of World Sugar Policy Simulation Model

– Dr. Won Koo, North Dakota State University

– Dynamic partial equilibrium net trade model

– Comprises 18 sugar producing and consuming countries and regions

– Makes specific assumptions about growth rate of various macroeconomic policy variables

Scenarios

Scenarios ConditionsBaseline

S0

Increased minimum TRQ from 1.13 to 1.38 MMT

Mexico allowed to export all of sugar surplus to U.S. market beginning in FY 2002

No PIK program or direct sugar purchases by government

No restrictions on U.S. sugar production

S1 Same as in baseline (S0) except U.S. domestic sugar production restricted to 1999 level of 7.5 MMT

S2 Same as in baseline (S0) except U.S. domestic sugar price is maintained at 21 cents/lb for raw sugar (loan rate 18 cents/lb)

U.S. Raw Sugar Price Projections, 2002-06(U.S. cents/lb)

10

12

14

16

18

20

22

24

26

1999 2002 2003 2004 2005 2006

S0 S1 S2

6,800

7,000

7,200

7,400

7,600

7,800

8,000

8,200

8,400

8,600

1999 2002 2003 2004 2005 2006

S0 S1 S2

U.S. Sugar Production Projections, 2001-06

(‘000 metric tons)

1,440

1,460

1,480

1,500

1,520

1,540

1,560

1,580

1999 2002 2003 2004 2005 2006

S0 S1 S2

U.S. Sugar Beet Acres Harvested Projections, 2001-06

(‘000 acres)

840

860

880

900

920

940

960

980

1,000

1,020

1999 2002 2003 2004 2005 2006

S0 S1 S2

U.S. Sugarcane Acres Harvested Projections, 2001-06

(‘000 acres)

• The near term prospects and

indeed the long term prospects for

the U.S. sugar industry appear

bleak

• It will be virtually impossible to

operate the sugar program at no or

minimum cost to the federal

government

• The near term prospects and

indeed the long term prospects for

the U.S. sugar industry appear

bleak

• It will be virtually impossible to

operate the sugar program at no or

minimum cost to the federal

government

Concluding Remarks