new jersey tax liens · new jersey tax liens robert w. keyser, esquire adam greenberg, esquire...

TRANSCRIPT

New Jersey Tax Liens

Robert W. Keyser, Esquire Adam Greenberg, Esquire

Taylor and Keyser Honig & Greenberg

76 E. Euclid Avenue, Suite 202 1949 Haddonfield-Berlin Road

Haddonfield, NJ 08033 Cherry Hill, NJ 08003

609-803-2180 856-770-0990

[email protected] [email protected]

© 2015 National Tax Lien Association www.theNTLA.com

1

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

I. New Jersey assesses taxes on the local (municipal) level. We have 566 municipalities, each of which has its own tax sale. Most auctions are in person, call out. Now about 10-20 or so are on line.

© 2015 National Tax Lien Association www.theNTLA.com

2

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

II. The bidding:

A. If in person – bid the interest rate, starting at 18%. The interest rate is bid downward. After 0%, then premiums are bid. Premiums are held by the municipality for five years. If you are redeemed in that period (which may be extended by a bankruptcy filing), you get the premium back, without interest. If you are not redeemed in that time frame, or you take title to the property by foreclosure, the premium is released (“escheats”) to the municipality.

B. On line, the bidding procedure is the same, but may be proxy or non-proxy bids – read the rules.

© 2015 National Tax Lien Association www.theNTLA.com

3

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

III. Basic Inquiry – What should you do?

A. What type of property - residential, commercial, industrial, vacant, tax exempt?

B. What are your lender’s limitations, or parameters?

C. What are the risks you are trying to avoid: unbuildable lots, crack houses, meth labs, environmentally challenged, wetlands, burnouts, demolished properties.

D. Types or methods of inquiry: on line searches, drive by, DEP known site website. How much money do you spend on research for a lien you may not obtain?

E. REMEMBER - Purchasers of tax sale certificates in New Jersey buy at their own risk. In the present case the Appellate Division said: "In these transactions caveat emptor should be the rule."

F. In New Jersey, you can pay subsequent taxes in each quarter that the owner does not, and add the amount paid as principal to your lien, earning 18% above $1500 (lien amount plus subsequent taxes), regardless of the interest rate on the certificate. If you don’t, you allow a lien senior in priority to your lien to be sold. But, inspect again before paying subsequent taxes (no use throwing away good money after bad.)

© 2015 National Tax Lien Association www.theNTLA.com

4

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

IV. ABANDONED PROPERTIES – the statute.

a. Any person holding a tax sale certificate on a property that meets the definition of abandoned property as set forth in P.L. 2003, c. 210 (C. 55:19-78 et al.), either at the time of the tax sale or thereafter, may at any time file an action with the Superior Court in the county wherein said municipality is situate, demanding that the right of redemption on such property be barred, pursuant to the "tax sale law," R.S.54:5-1 et seq. N.J.S. 54:5-77.

b. Any person holding a tax sale certificate on a property that meets the definition of abandoned property as set forth in P.L.2003, c.210 (C.55:19-78 et al.), either at the time of the tax sale or thereafter, may enter upon that property at any time after written notice to the owner by certified mail return receipt requested in order to make repairs, or abate, remove or correct any condition harmful to the public health, safety and welfare, or any condition that is materially reducing the value of the property.

c. Any sums incurred or advanced pursuant to subsection c. of this section may be added to the unpaid balance due the holder of the tax sale certificate at the statutory interest rate for subsequent liens.

© 2015 National Tax Lien Association www.theNTLA.com

5

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

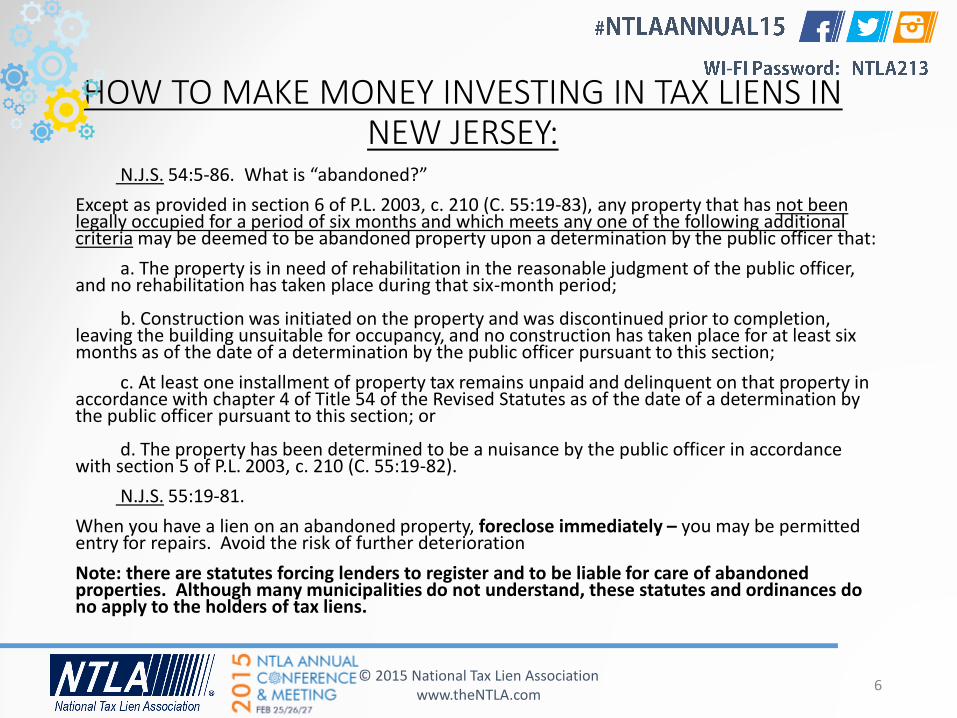

N.J.S. 54:5-86. What is “abandoned?”

Except as provided in section 6 of P.L. 2003, c. 210 (C. 55:19-83), any property that has not been legally occupied for a period of six months and which meets any one of the following additional criteria may be deemed to be abandoned property upon a determination by the public officer that:

a. The property is in need of rehabilitation in the reasonable judgment of the public officer, and no rehabilitation has taken place during that six-month period;

b. Construction was initiated on the property and was discontinued prior to completion, leaving the building unsuitable for occupancy, and no construction has taken place for at least six months as of the date of a determination by the public officer pursuant to this section;

c. At least one installment of property tax remains unpaid and delinquent on that property in accordance with chapter 4 of Title 54 of the Revised Statutes as of the date of a determination by the public officer pursuant to this section; or

d. The property has been determined to be a nuisance by the public officer in accordance with section 5 of P.L. 2003, c. 210 (C. 55:19-82).

N.J.S. 55:19-81.

When you have a lien on an abandoned property, foreclose immediately – you may be permitted entry for repairs. Avoid the risk of further deterioration

Note: there are statutes forcing lenders to register and to be liable for care of abandoned properties. Although many municipalities do not understand, these statutes and ordinances do no apply to the holders of tax liens.

© 2015 National Tax Lien Association www.theNTLA.com

6

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

V FORECLOSURE

A. When do you start? Not before two years from the date of issuance, but there may be strategic reasons why you may wait beyond that date? Many lien holders want you to start on the first permissible day. Your lender may have parameters as to when you must start foreclosure.

B. The Foreclosure Process in a nutshell:

1. Pre-foreclosure notice to owners, mortgagees, holders of older tax liens.

2. Thirty-three days later, file your complaint. In NJ, all foreclosures are filed centrally in the Foreclosure Section of the Superior Court. They are listed as being in the County where the property is located. Name everyone who has an interest in the property –owners, mortgagees, other junior tax liens, judgments, condo liens. Everyone who has an interest of record that is junior in priority to your tax lien. That means everyone except senior (newer) tax liens, and NJ Spill Act liens (bad)

3. Serve your filed complaint on everyone you can find and start due diligence on everyone you can’t find. Personal service can be difficult, but is always best. (See “Now you own it”). There are a number of alternate ways to serve, but you must demonstrate to the Court why you had to use an alternate form of service. DUE PROCESS IS THE KEY.

© 2015 National Tax Lien Association www.theNTLA.com

7

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

V FORECLOSURE (CONTINUED)

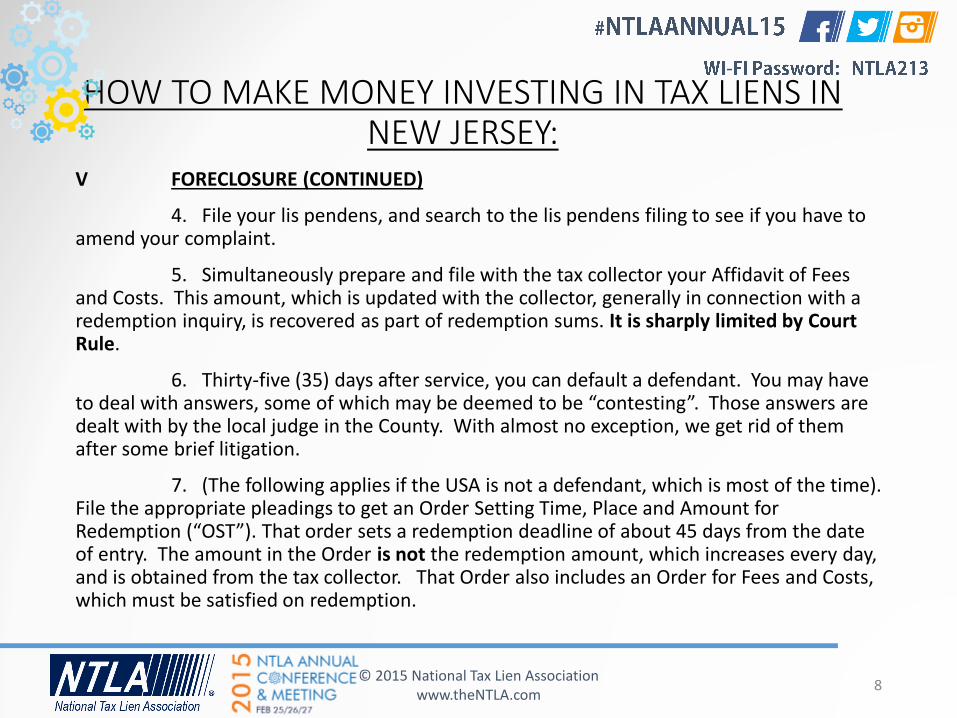

4. File your lis pendens, and search to the lis pendens filing to see if you have to amend your complaint.

5. Simultaneously prepare and file with the tax collector your Affidavit of Fees and Costs. This amount, which is updated with the collector, generally in connection with a redemption inquiry, is recovered as part of redemption sums. It is sharply limited by Court Rule.

6. Thirty-five (35) days after service, you can default a defendant. You may have to deal with answers, some of which may be deemed to be “contesting”. Those answers are dealt with by the local judge in the County. With almost no exception, we get rid of them after some brief litigation.

7. (The following applies if the USA is not a defendant, which is most of the time). File the appropriate pleadings to get an Order Setting Time, Place and Amount for Redemption (“OST”). That order sets a redemption deadline of about 45 days from the date of entry. The amount in the Order is not the redemption amount, which increases every day, and is obtained from the tax collector. That Order also includes an Order for Fees and Costs, which must be satisfied on redemption.

© 2015 National Tax Lien Association www.theNTLA.com

8

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

V FORECLOSURE (CONTINUED)

8. The OST is served on all defendants, but not all defendants may redeem the lien. Only owners, mortgage holders, holders of junior (older) tax sale certificates, and “parties in lawful possession” (generally bona fide tenants, but they rarely redeem). Judgment holders and other lien interests may not redeem.

9. Once the time for redemption has expired, you obtain from the tax collector an Affidavit of Non-Redemption, where the collector certifies that the lien has not redeemed. You will also have the collector certify that all taxes have been paid to the date of the filing of the Complaint.

10. The Affidavit of Non-Redemption and a Final Judgment is submitted to the Court, either by application or Motion. When entered, the property is owned by the Plaintiff. You serve the Judgment on all defendants, and record it in the real estate records. It is your deed to the property.

© 2015 National Tax Lien Association www.theNTLA.com

9

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

V FORECLOSURE (CONTINUED)

11. If the USA (generally the IRS) has a lien, an alternate procedure must be followed. There is no OST issued. Rather, instead of the OST, we apply for Final Judgment, submitting it to the Court with a Writ of Execution. That Final Judgment and Writ provides for a Sheriff’s Sale of the property, as if you were foreclosing on a mortgage. You do have priority over IRS liens.

12. One other note: Many lien holders take title to certificates in the name of a custodian or trustee. Most of these relationships (all of the ones with which I am familiar) require that final judgment not be entered in the name of the custodian. You may have an REO holding entity to take title to properties. Therefore, before the judgment package is submitted, a motion and order changing the name of the Plaintiff will have to be filed and served. The Assignment out of the custodian, which must be recorded, is submitted to the court with that motion.

© 2015 National Tax Lien Association www.theNTLA.com

10

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

VI. NOW YOU OWN THE PROPERTY (what happens next?)

A. You may have to deal with a hostile court system if the former owner decides that the years during which he didn’t pay property taxes were enough time, and files an action. An action to undo what you have done may be filed. Reprinted below is one Court’s somewhat biased view of the process:

The facts of this case reveal the harshness of the tax sale certificate foreclosure proceedings in this State, where people with substantial equity in a property, for whatever reason, fail to pay property taxes and thereafter default in the tax sale certificate foreclosure proceedings. They may lose all of the equity in their homes even where the unpaid taxes and accumulated interest and fees are relatively minor.

Of course, the legislature's concern in fostering payment of property taxes and in barring the right of redemption to permit transfer of clear title to property involved in tax sale certificate foreclosures is legitimate. The system is equitable where property is abandoned or where the liens against it exceed its value. Nevertheless, in circumstances where the owners hold substantial equity in the property, the system can be Dickensonian. Until the Legislature devises a better system, courts of equity must do their best to balance the equities, taking into account the necessity of allowing the transfer of clear title and the need to compel the payment of property taxes against the necessity of ameliorating, in appropriate circumstances, the onerous impact of the procedure in circumstances where the party has remained in possession of the property and has substantial equity in it.

© 2015 National Tax Lien Association www.theNTLA.com

11

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

VI. NOW YOU OWN THE PROPERTY (what happens next?) (CONTINUED)

IE’s L.L.C. v. Simmons, 392 N.J.Super. 520, 536-537 (Ch.Div. 2006)

As you can see, this Judge felt the obligation to mitigate what he viewed were harsh effects of laws passed by legislatures and signed by Governors.

B. Taking possession. You have a number of alternatives, depending upon the nature of the occupant.

1. A former owner or someone who claims the right to be on the property through a former owner (family member) can be evicted by use of a Writ of Possession. This is issue by the Court, and results from the fact that your Final Judgment includes a judgment for possession.

2. Bona Fide Tenants. These may be thorny issues, including whether or not you have a bona fide tenant. New Jersey affords real residential (not commercial) tenants with substantial protection, starting with the fact that the Final Judgment does not cut off the right of the tenant under a lease (written or oral). We call this the Anti-Eviction Act. You will have to deal with a party who has the right to stay, subject to certain terms, including the payment of rent. If you need to get that tenant out, you will need to go to Landlord Tenant Court, or file for Ejectment proceedings in very difficult situations.

© 2015 National Tax Lien Association www.theNTLA.com

12

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

VII. SALE OF REAL ESTATE

A. There are issues that arise in the sale of REO acquired by tax foreclosure. Apart from the decisions to sell “as is” (typical, in my experience) or agree to make some improvements, you have municipalities with varied requirements for “Certificates of Occupancy”, the possibility of underground storage tanks and other environmental issues, and State laws impacting upon wells and septic systems in the more rural sections of the State. All rights and responsibilities of the parties should be clearly delineated in a Contract of Sale.

B. The availability of title insurance can be problematic. No title company will insure a tax foreclosed property in less than ninety days from the entry of Final Judgment, and in increasing number require a one-year time frame before title insurance against a former owner’s possible claim to vacate the judgment can be purchased. The reason for this is the unpredictability of judges, and the title company’s unwillingness to risk a claim based upon a motion to vacate the judgment. (See, as illustrative, Section IV, and that Judge’s opinion.) Personal service in the foreclosure is the best way to convince a title company to insure your sale after 90 days, but even that doesn’t always work.

C. Shameless plug – it is enormously helpful to you to use the services of an attorney and a title company who understands the tax foreclosure process when selling your REO.

© 2015 National Tax Lien Association www.theNTLA.com

13

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

TAX FORECLOSURE – HEY, I’D PREFER IF YOU GIVE THAT BACK

New Bankruptcy Cases Present New Issues

In re Berley, 492 B.R. 433 (Bankr.D.N.J. 2013)

In Re Varquez, 502 B.R. 186 (Bankr.D.N.J. 2014)

In Berley, the debtor lost the property by way of foreclosure prior to the filing of bankruptcy and the debtor filed an adversary proceeding seeking to undo the transfer both as a preference and as a fraudulent conveyance.

© 2015 National Tax Lien Association www.theNTLA.com

14

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

New Bankruptcy Cases Present New Issues (CONTINUED)

The applicable code section, 11 U.S.C. 547(b), states:

(b) Except as provided in subsections (c) and (i) of this section, the trustee may avoid any transfer of an interest of the debtor in property –

(1) to or for the benefit of a creditor;

(2) for or on account of an antecedent debt owed by the debtor before such transfer was made;

(3) made while the debtor was insolvent;

(4) made -

(A) on or within 90 days before the date of the filing of the petition; or

(B) between ninety days and one year before the date of the filing of the petition, if such creditor at the time of such transfer was an insider; and

(5) that enables such creditor to receive more than such creditor would receive if -

(A) the case were a case under chapter 7 of this title;

(B) the transfer had not been made; and

(C) such creditor received payment of such debt to the extent provided by the provisions of this title.

.

© 2015 National Tax Lien Association www.theNTLA.com

15

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

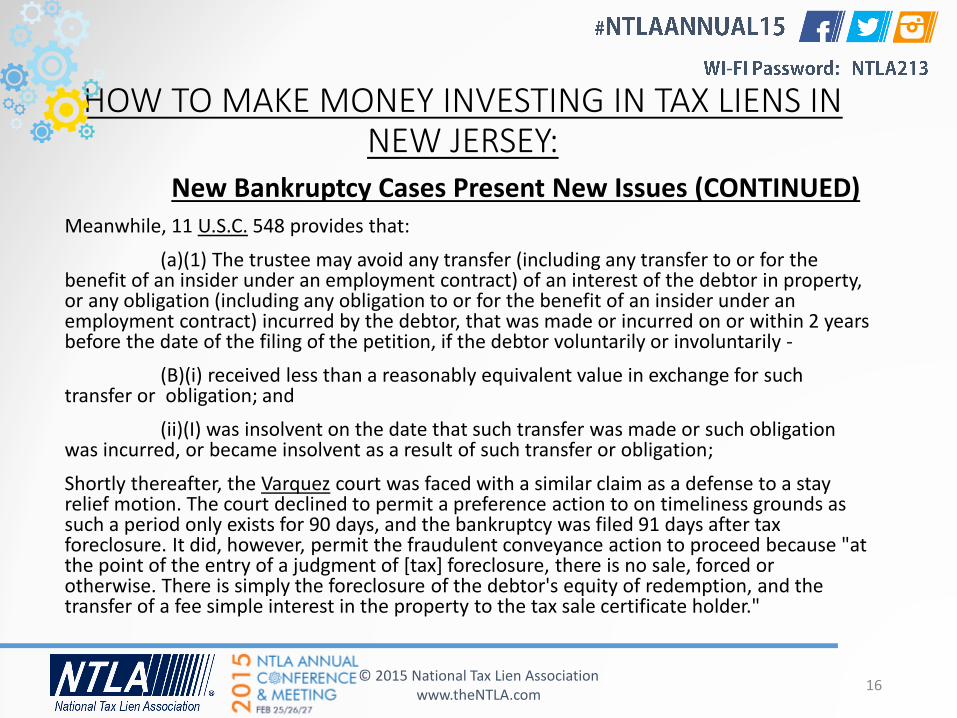

New Bankruptcy Cases Present New Issues (CONTINUED)Meanwhile, 11 U.S.C. 548 provides that:

(a)(1) The trustee may avoid any transfer (including any transfer to or for the benefit of an insider under an employment contract) of an interest of the debtor in property, or any obligation (including any obligation to or for the benefit of an insider under an employment contract) incurred by the debtor, that was made or incurred on or within 2 years before the date of the filing of the petition, if the debtor voluntarily or involuntarily -

(B)(i) received less than a reasonably equivalent value in exchange for such transfer or obligation; and

(ii)(I) was insolvent on the date that such transfer was made or such obligation was incurred, or became insolvent as a result of such transfer or obligation;

Shortly thereafter, the Varquez court was faced with a similar claim as a defense to a stay relief motion. The court declined to permit a preference action to on timeliness grounds as such a period only exists for 90 days, and the bankruptcy was filed 91 days after tax foreclosure. It did, however, permit the fraudulent conveyance action to proceed because "at the point of the entry of a judgment of [tax] foreclosure, there is no sale, forced or otherwise. There is simply the foreclosure of the debtor's equity of redemption, and the transfer of a fee simple interest in the property to the tax sale certificate holder."

© 2015 National Tax Lien Association www.theNTLA.com

16

HOW TO MAKE MONEY INVESTING IN TAX LIENS IN NEW JERSEY:

WHAT IS THE REMEDY TO APPLY?

• 11 U.S.C. 550 states, in pertinent part, that "the trustee may recover, for the benefit of the estate, the property transferred, or, if the court so orders, the value of such property." The question thus remains, does the debtor get the real property back, or do they simply get a money judgment against the creditor for "the value of such property."

• No court in New Jersey has yet decided this issue but at least one court has indicated that it will not take a course of action that places into question real estate titles in the state, thus evidencing a preference for awarding the value of such property to the estate.

• Note that any award in this regard would also be subject to a lien in favor of the transferee as described in section 550(e) for improvements, taxes, property preservation, and similar charges.

© 2015 National Tax Lien Association www.theNTLA.com

17

© 2015 National Tax Lien Association www.theNTLA.com

18

© 2015 National Tax Lien Association www.theNTLA.com

19