new pathways to growth - water and sewer …wasda.com/wp-content/uploads/2015/03/mike-marks...new...

TRANSCRIPT

New Pathways To Growth

Monday, February 26, 2013 8:00am – 11:00am

The Sawgrass Marriott Golf ResortPonte Vedra Beach, FL

Presenter/Facilitator

J. Michael Marks, Managing Partner INDIAN RIVER CONSULTING GROUP

www.ircg.com

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Your Speaker Today- Mike Marks

Our firm has been in the business advisory services business for 25 years • The focus is on market access which aligns your

investments with real market growth opportunities

• Several in the audience have been clients

Mike Marks is the Managing Partner • Co-founder of the firm • Is the Senior Research Fellow with the NAW

Institute of Distribution Excellence - 5 books • Teaches B2B marketing at several universities

• Currently holds an SCCA Competition License

• Enjoys fine tequila & cigars

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Agenda

Market Access !!Pricing Practices

!!Channel Design

Market access measures how well your

investments are aligned with the true growth opportunities in your

market space. !

Most firms are too slow to reallocate or divest

resources from decaying opportunities which

either lowers their profit or dramatically limits

their ability to invest for growth

You become misaligned by changing slower than your market

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Market Access

Non-WTO Definition: Market Access is a measure of how well your sales and marketing investments are aligned with current market opportunities for

growth 1. In the beginning, manufacturers evaluate markets for opportunities and

scalable competitive advantage that will create shareholder value Manufacturers then develop, produce, source, and assemble products/services for

customers 2. They then make investments in sales reps, advertising, branding,

marketing, customer service, and multiple channel partners These investments are made as optimizing decisions to develop and serve

markets of customers 3. As markets are accessed and growth is generated these investments

typically scale up incrementally at each business planning cycle to maintain growth rates

Over time, markets evolve and the VP-Sales never wants a smaller sales force - so investments become misaligned to opportunities for growth

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Studebaker Lost Their Game In 1947

They failed to keep up with the changing market

Towards the end it was about cutting costs and hoping the economy would improve

• Died 03-16-66

The gap between what they were selling and what the customers were buying got too large

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

It is easy to see in someone else’s market

Business Models Are Changing:

Most firms act like Kodak until they fail, and the new world rises from the ashes. Best Buy and Barnes & Noble will be next.

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Three WASDA Specific Forces

Relationship buying and sourcing has been replaced by economic buying and sourcing

• Trusted relationships migrated to rabbits & advantaged players

The competitive pricing pressure in infrastructure rebuilding is much higher than new expansion construction because there is no investor-specific time pressure prior to bid award

Long term liability and risk is migrating up the channel

http://blogs.hbr.org/cs/2012/07/the_game_buyers_play_with_vend.html?

utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+harvardbusiness

+%28HBR.org%29

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

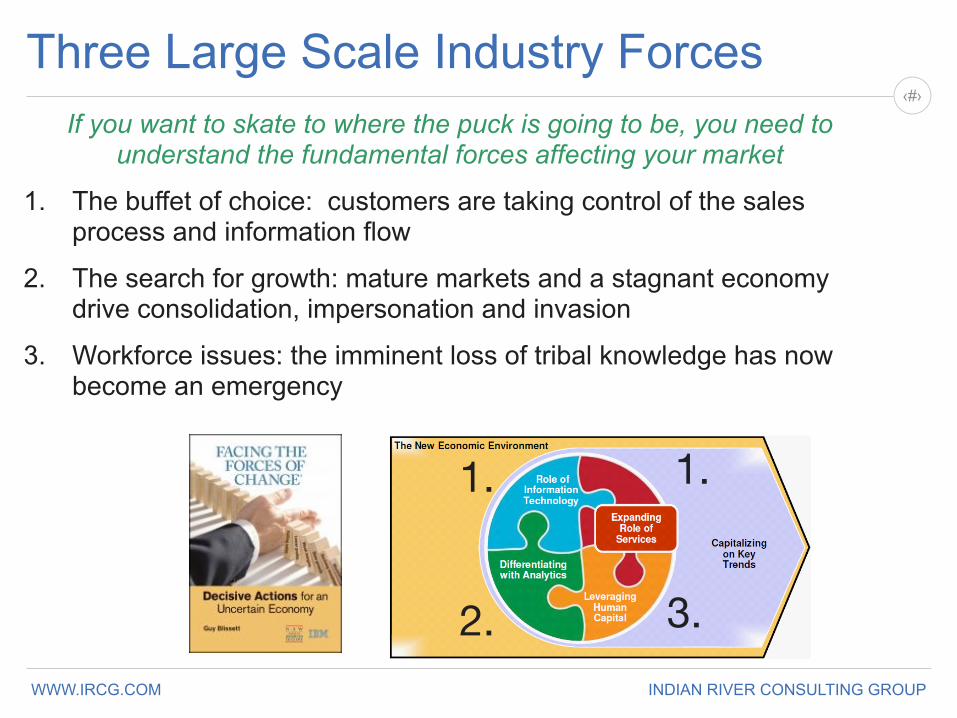

Three Large Scale Industry ForcesIf you want to skate to where the puck is going to be, you need to

understand the fundamental forces affecting your market

1. The buffet of choice: customers are taking control of the sales process and information flow

2. The search for growth: mature markets and a stagnant economy drive consolidation, impersonation and invasion

3. Workforce issues: the imminent loss of tribal knowledge has now become an emergency

3.

1.

2.

1.

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

Customers are no longer just passive consumers of a

product or service. They help to create it!

Solutions are tailored based on

time and place

Information can be accessed from anywhere at anytime

#1 The Buffet of Choice

Some factoids from Grainger’s Geoff Robinson in emarketter.com, June 2012

Grainger’s mobile activity has increased 400% in the past 12 months

Over 50% of its users feel comfortable ordering over mobile devices

Google reported that 1 in 7 searches are now done on mobile devices (BYOD)

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

#2 The Search for GrowthLet’s go global (both ways) • Distributors are different

The Wal-Mart Disease • What do you do when you get to the bottom? • Cut prices for growth

Convergence is affecting everything now • “My market stinks and the margins in that other market look good, let’s go get it” • Product & industry silos are evaporating quickly, think Amazon • Pricing transparency, model analytics, and supplier control are the new order

Lots of capital + few options = goofy acquisition prices • Strategic acquirers are as desperate as the PE Firms • Likely to end as badly as the last round, but concerning nonetheless

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

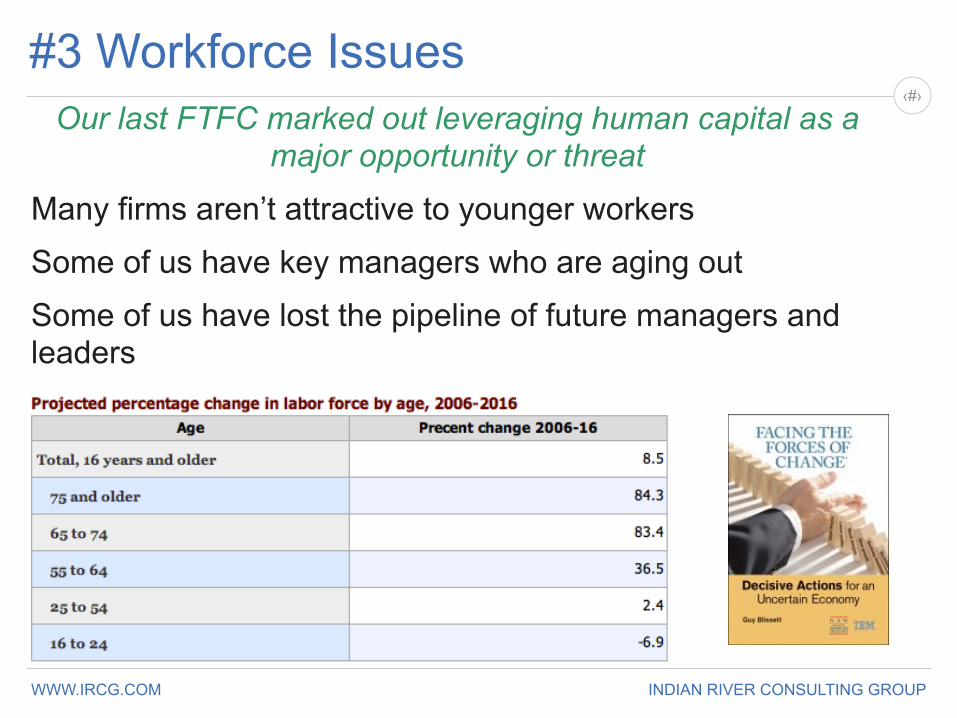

#3 Workforce IssuesOur last FTFC marked out leveraging human capital as a

major opportunity or threat

Many firms aren’t attractive to younger workers

Some of us have key managers who are aging out

Some of us have lost the pipeline of future managers and leaders

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Roy Vallee, Executive Chairman, Avnet

What should keep distributor managers awake at night?

1. Finding pathways for continued profitable growth that in today’s uncertain environment requires risk taking and innovation

2. Being able to attract and engage the new generation of workers

3. Being able to effectively allocate your resources (people and money) in a changing environment (sometimes reallocating is the biggest challenge)

!!!!Source: MDM October 25, 2012. Full interview available at www.mdm.com/ext/html/executivebriefing-7min-archive.html

Another Take Of Executive Insight

Consultant takeaway: these issues represent a profound and fundamental challenge to the risk averse, tactically-focused

“owner operator” distributors and their product-focused suppliers

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

The Responses Are Judo Moves

The following are a few of the top techniques that have proven to be the most powerful for IRCG clients who operate in markets similar to yours

1. Transition to intentional selling

2. Become strategy driven

3. Learn to be analytically led

Judo is about working with the forces of nature rather than trying to confront negative energy head on

Competing by providing excellent service with great people requires being seen by the customer as significantly better than their other alternatives. When everyone is good enough the race to the bottom on price begins

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

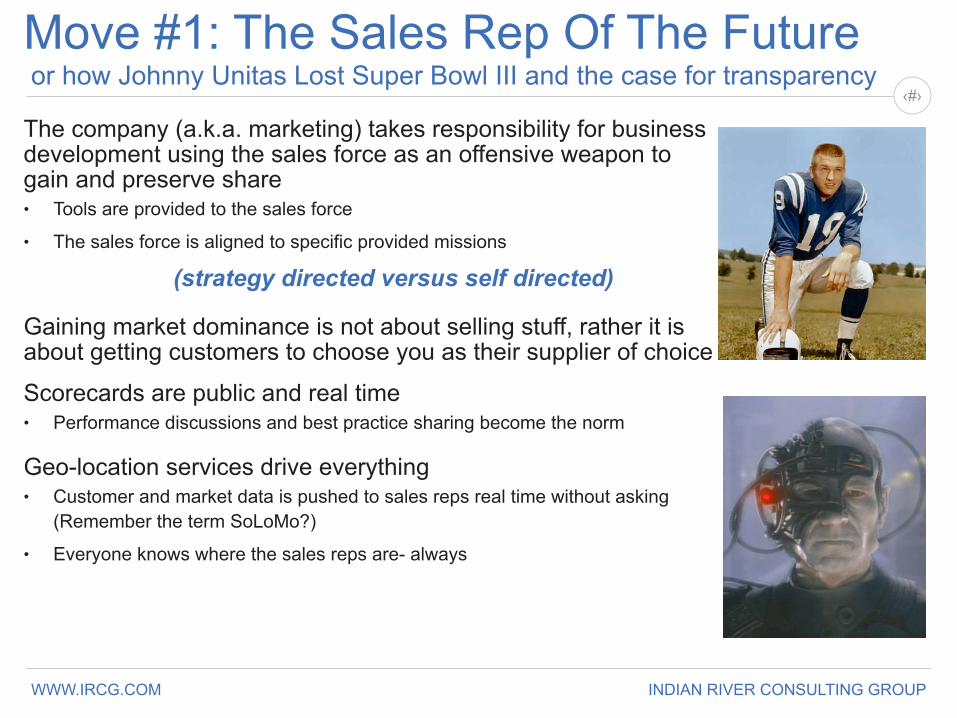

Move #1: The Sales Rep Of The Future or how Johnny Unitas Lost Super Bowl III and the case for transparency

The company (a.k.a. marketing) takes responsibility for business development using the sales force as an offensive weapon to gain and preserve share • Tools are provided to the sales force • The sales force is aligned to specific provided missions

(strategy directed versus self directed)

Gaining market dominance is not about selling stuff, rather it is about getting customers to choose you as their supplier of choice Scorecards are public and real time • Performance discussions and best practice sharing become the norm

Geo-location services drive everything • Customer and market data is pushed to sales reps real time without asking

(Remember the term SoLoMo?) • Everyone knows where the sales reps are- always

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

An example of strategic backward chaining

Move #2: Develop Your Own Strategy

Strategic Vision: !

Screaming fans and

groupies on the Sunset

strip

• Guitar lessons • Dance and drama

classes • Coffee house practice

Core Initiatives

Chain backwards to create strategy

1: Develop Talent

Execution Plans

2: Get the Look• Extreme diet • Hair extensions and

plastic surgery • Start drug habit

3: Work the Players• Develop biz contacts • Blackmail record

executive • Publicity campaign !

4: Roll Out the Band • Form band • Record single and

video • Promotional tour !

Current State: !

A serious, straight laced,

business executive

who is retiring

Don’t start with, “What should we do right now? Rather, start with, “Where do we want to finish?” Then just work backwards.

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Move #3: Learn To Be Analytically Led

Our legacy and our history

1. Our industry keeps tribal knowledge and relationship equity in the minds of our staff

What happens when key aging employees leave?

2. We have a folklore around impactful stories that when told are timeless

What innovation is lost because of the view, “We tried that once and it didn’t work?”

3. How do you really know what customers think of you?

How smart is it to rely solely on the sales force for insight?

A choice there for the taking

If you have data you can create a feedback loop and

dramatically improve performance

Allocate

resources

Execute

Debrief

Analyze & Plan

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Considerations For Your Future

Competitive advantage is not real unless you gain a significant cost advantage over your competitors or a significant price premium from your customers, either resulting in higher profits. Operational execution is an

activity, not a strategy.

1. How much of your product revenue is bought and not sold?

2. If you were designing a sales organization and market channel from scratch, would it look like what you have today?

3. How much of your investments in innovation and risk taking are allocated to tweaking your existing model versus creating a new one?

4. Why would customers buy from you, over your competitors, if all product was free?

5. What real fundamental disruption would occur in your market if you declared bankruptcy and exited the space?

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Group Activity

Break into groups as instructed and discuss the questions and subjects that follow, making sure that everyone weighs

in on the conversation

Compare your views on the forces and the responses that Mike discussed, specifically: 1. Where do you agree or disagree with those presented 2. What are your views on how the industry, as a whole, is

dealing with the the forces of change?

Out Of The Box Question For Extra Credit What are some of the initiatives that you are taking to get ahead of industry changes (feel free to lie if competitors are present)

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Agenda

Market Access

!!Pricing Practices !!Channel Design

Discounting on deal size with major input from your sales force is costing you 200

basis points or more

The foundation of any true pricing strategy is

customer segmentation. !

Manufacturers, we will explore functional pricing

and discounting in the channel design section

that follows. !

Much of this material is from the Purdue/UID

course on pricing.

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Anti Trust DisclaimerPlan on being deposed in the next 24 months about this meeting • It is important to be able to enthusiastically tell the whole truth • If you aren’t deposed- then you can be happy either way

We are NOT going to discuss any specific customers or any specific products or any specific prices or any specific geographical markets, however IN GENERAL* • We can speak freely about distributors and suppliers • We can speak freely about trading practice alternatives and channel economics

We are not going to make any agreements, either explicit or implied, with any other participant with respect to our future trading practice plans or intentions • Every firm is free to pursue their own best commercial interests unencumbered by

any other participant in this room

*This means no practice is ever linked to any specific firm and no firms are mentioned

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

Ove

rrides

0

7,500

15,000

22,500

30,000

Margin

SystemActual

Pricing: Key Mistake #1

YTD Override Frequency: What is market based versus easy?

20 and 25 easy to compute

30 and 35

40 easy to compute

Not only do rushed people use easy numbers but they apply them to everything that a customer purchases or to every product in a suppliers line

(This blanket response is very costly)

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Pricing: Key Mistake #2Problem: Rushed sales reps want to make a sale and move on- so the easiest path forward is to quote the Last Price Paid (LPP) • There is an assumption that the LPP was correct and worse, it is the path

of least resistance • They mistakenly assume that the customer remembers LPP even on

tertiary items (the 80% of items that are 20% of sales)

Solution: Create a monthly report that ranks all sales reps by percentage of line items sold at LPP • Even raising price a penny moves it out of the category • You have many situations where you are several price increases behind

the market

Let 5 wet monkeys show you the way http://www.youtube.com/watch?v=0_u8sF1sW4A

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›The LPP Permanent Margin Leak

This is the long term cost of LPP. Notice the customers on the left (small order quantities) that are getting better than market pricing (below the regression line) so they will never leave and over time it will become a

crowded parking lot

This is worth 200 to 400 basis points for a typical WASDA distributor

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Pricing: Key Mistake #3You do not have a rules-based pricing process • If you need a process and don’t get it, you will pay the cost of getting it

with lower margins, forever • Rules and policies replace story telling

The industry is event driven by opportunity and circumstance • It is made up of a series of emotionally charged data free discussions • Distributors use a “sharp pencil” to capture initial business with a new

customer • Manufacturers use their “sharp pencil” to get incremental business that

improves plant utilization • Both plan, or hope, to make it up “down the road”

Neither have feedback loops to go back and measure results after the fact

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Analytics Without Process Will Fail

The art is the evolving customer segmentation, product grouping classifications, life cycle positions, bundling effects, and velocity

Each of these factors interacts with the others

If you’ve seen one good process, you’ve seen one

It is never done as it is a process and not an event

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

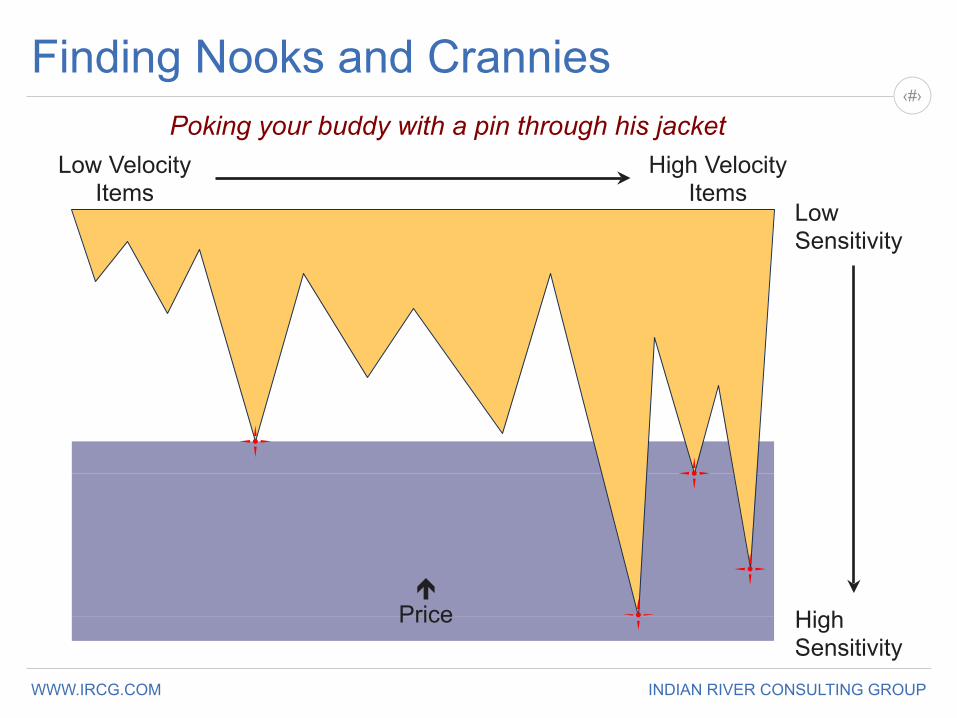

Finding Nooks and Crannies

Customer 12345

Low Velocity Items

High Velocity Items

Low Sensitivity

High Sensitivity

! Price

Poking your buddy with a pin through his jacket

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Analytics: ROI

This leverage works for any firm in any industry

In ages past revenue growth was the key because you could leverage volume for supplier concessions. Since nothing lasts forever, growth no

longer is the key leverage tool for distributors and even most manufacturers

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

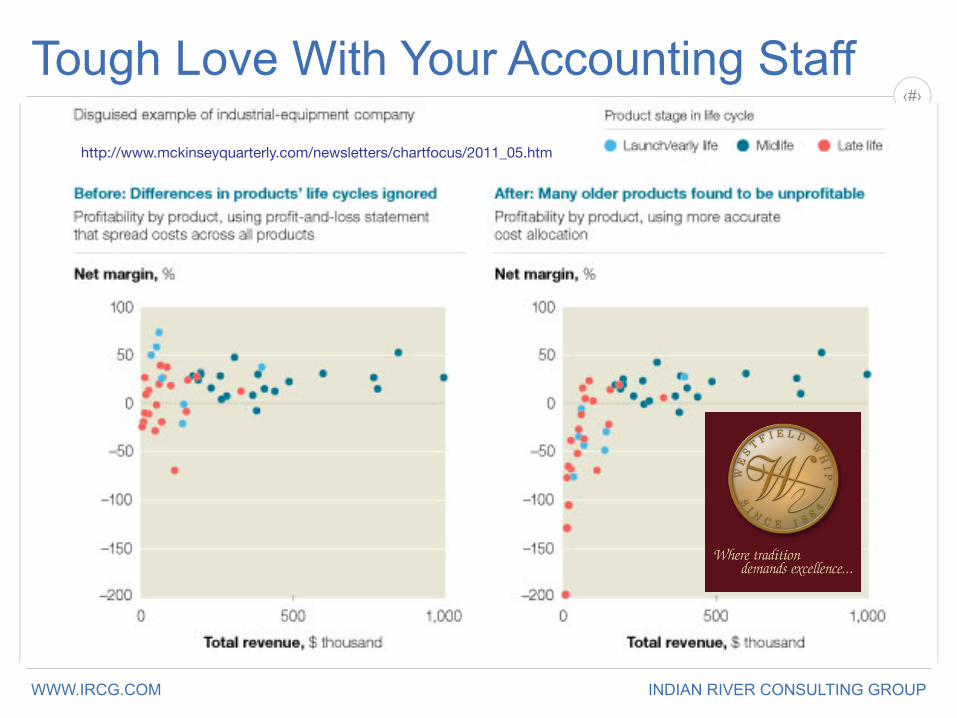

http://www.mckinseyquarterly.com/newsletters/chartfocus/2011_05.htm

Tough Love With Your Accounting Staff

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Changing The RulesThe basis for any pricing strategy is customer segmentation Elasticity is the measure of how much volume changes with a change in price • High elasticity means large volume swings with small changes in price • Low elasticity means small to no volume swings with small changes in

price

Margin goes up to the extent that • The customer is irrelevant to the core business • The product is tertiary to the specific customer • The product is slow moving (infrequent demand) Margin goes down with the inverse of the above • Or single transaction size increases

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Simple Size Example

Take Average Selling Price (ASP) for each SKU for each Customer Class* (with a

spreadsheet for each class) and change the ASPs by factors in the table. There is some

art to this.

*In a marketing world these would be targeted segments based on both potential to grow and cost to grow- not size categories

Customer Class Importance

Primary Product Tertiary Product Overall Slow Moving

Small No Change +20% Add 8%Medium No change +15% Add 6%Large -1% +10% Add 4%Huge -2% +5% Add 2%

Growth Target Temporary -2% Temporary 0% Temporary 0%

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›The Price To PlayField sales people will let retaining or capturing business trump margin optimization (value expectancy theory) so they can’t be in charge • You must answer the question, “Who is our pricing Czar?”

You must develop a rules based pricing policy You must have a measurement system to measure elasticity, e.g. Quote Kill Rate (QKR) • It must be SKU and customer specific • It will require segmenting customers in advance

It must have an adaptive feedback loop • Margin gains are created with changes from the feedback loop

At some point you must say no to some customers and some of your own sales people

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

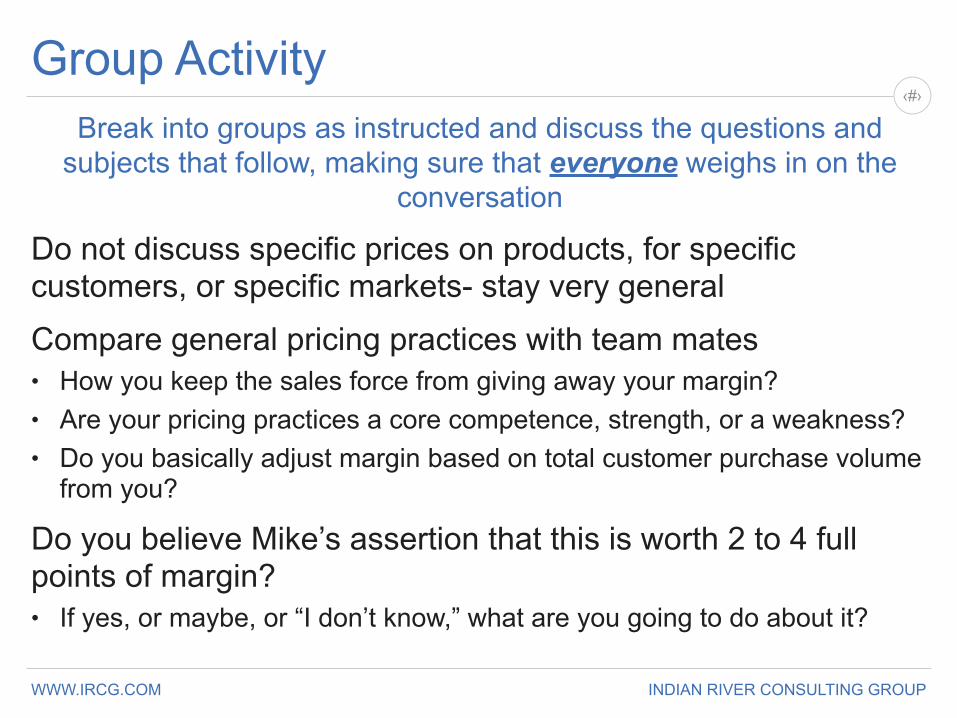

‹#›Group Activity

Break into groups as instructed and discuss the questions and subjects that follow, making sure that everyone weighs in on the

conversation

Do not discuss specific prices on products, for specific customers, or specific markets- stay very general

Compare general pricing practices with team mates • How you keep the sales force from giving away your margin? • Are your pricing practices a core competence, strength, or a weakness? • Do you basically adjust margin based on total customer purchase volume

from you?

Do you believe Mike’s assertion that this is worth 2 to 4 full points of margin? • If yes, or maybe, or “I don’t know,” what are you going to do about it?

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Agenda

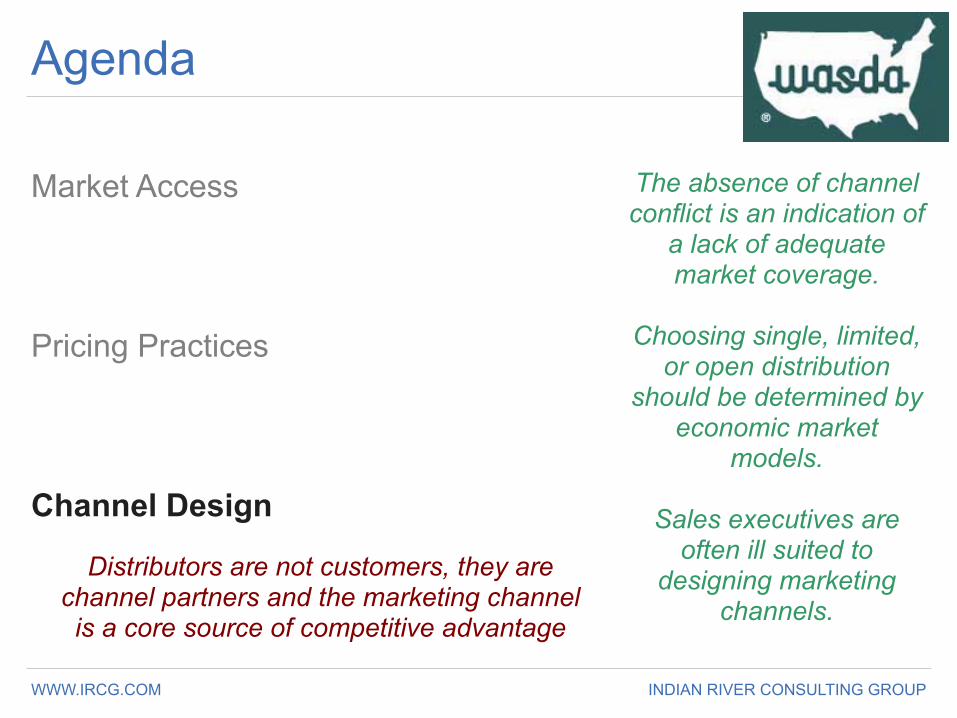

Market Access

!!Pricing Practices

!!Channel Design

Distributors are not customers, they are channel partners and the marketing channel is a core source of competitive advantage

The absence of channel conflict is an indication of

a lack of adequate market coverage.

!Choosing single, limited,

or open distribution should be determined by

economic market models.

!Sales executives are

often ill suited to designing marketing

channels.

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›What Is A Marketing Channel?A channel is an interdependent group of firms who are involved in how a product is used or consumed Compensation is provided to channel members to reflect the value of services that they provide • Some are over and under compensated as

channels evolve

Many firms confuse products and channels • The wiener is the product; the bun and

condiments are the channel; and all the customer wants is a good lunch

• Even more firms mistakenly assume that the brand is only about the product

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Marketing Channel FunctionsMarketing channels connect end customers with suppliers by providing demand creation, logistics, financing and support services • They can provide lower cost coverage with their gross margin basket,

they can pull through sales by winning ties when the customer is indifferent, and they can lower transaction costs independent of order size

This includes distributors, buying groups, agents, reps, brokers and third party specifiers • They survive if they perform activities more cost effectively than those

they buy from (suppliers) and sell to (customers)

Channel players can be eliminated but channel functions cannot • Selling costs are visible, other costs may be buried in COGS or

commercial expense

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

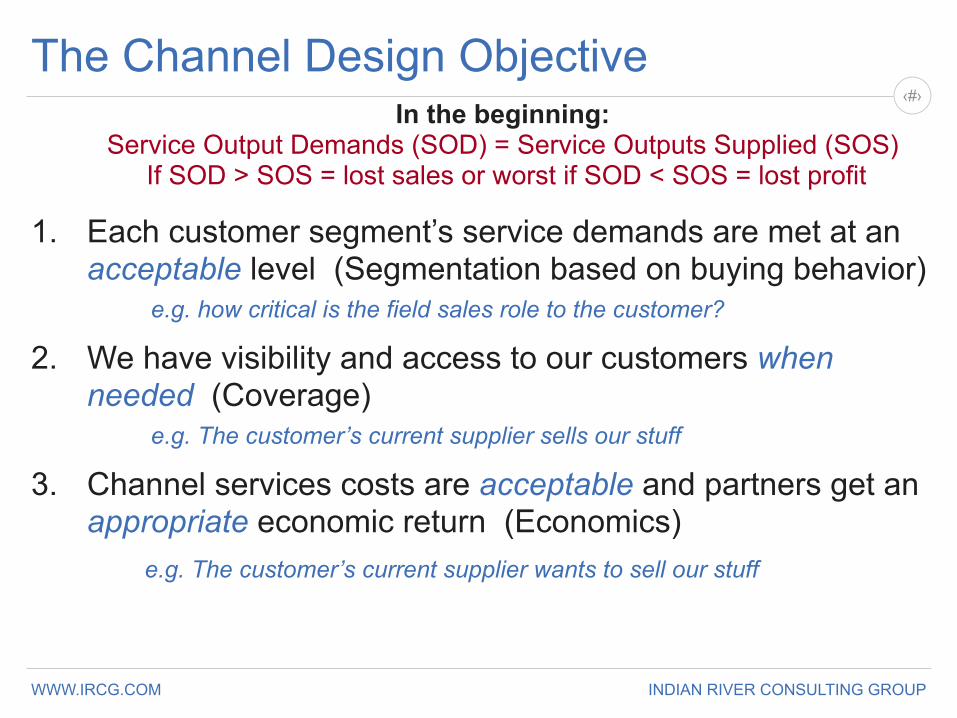

The Channel Design Objective

1. Each customer segment’s service demands are met at an acceptable level (Segmentation based on buying behavior)

e.g. how critical is the field sales role to the customer?

2. We have visibility and access to our customers when needed (Coverage)

e.g. The customer’s current supplier sells our stuff

3. Channel services costs are acceptable and partners get an appropriate economic return (Economics)

e.g. The customer’s current supplier wants to sell our stuff

In the beginning: Service Output Demands (SOD) = Service Outputs Supplied (SOS)

If SOD > SOS = lost sales or worst if SOD < SOS = lost profit

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

Manufacturer

The Channel Story Gather information from multiple sources and look for key drivers and

incorrect assumptions to create actionable choices.

Optimized Channels

Economics CoverageRecommendations & Action Planning

Channel Partners Customers

Segmentation

IRCG Channel Analysis ModelWe’ve all got cherished beliefs

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›

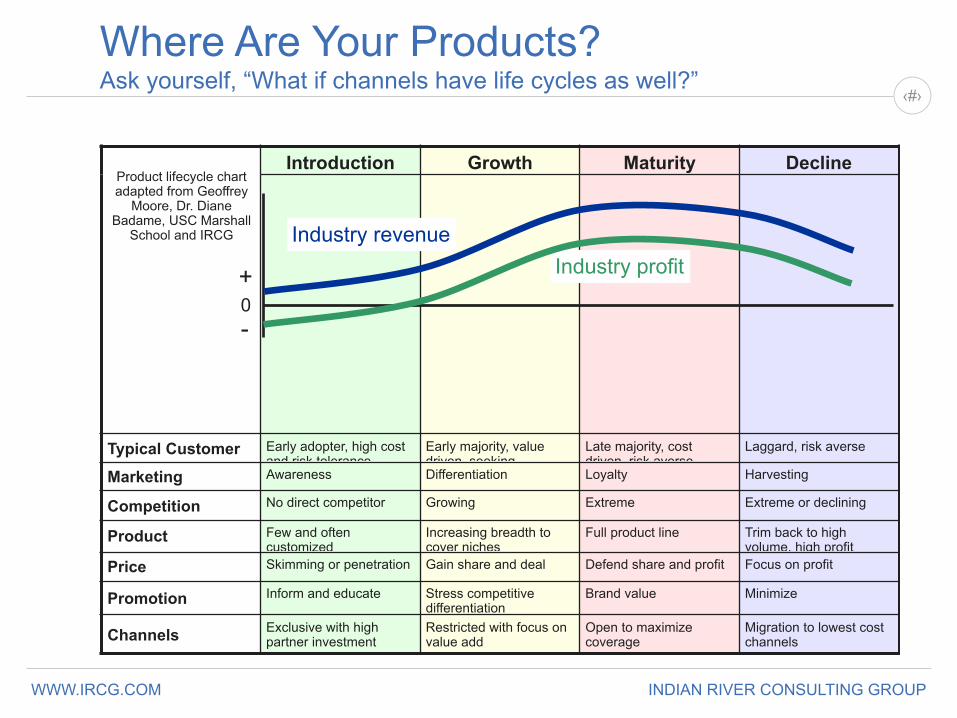

Where Are Your Products?Ask yourself, “What if channels have life cycles as well?”

Introduction Growth Maturity Decline

Typical Customer Early adopter, high cost and risk tolerance,

Early majority, value driven, seeking

Late majority, cost driven, risk averse

Laggard, risk averse

Marketing Strategies

Awareness Differentiation Loyalty Harvesting

Competition No direct competitor Growing Extreme Extreme or declining

Product Few and often customized

Increasing breadth to cover niches

Full product line Trim back to high volume, high profit

Price Skimming or penetration Gain share and deal Defend share and profit Focus on profit

Promotion Inform and educate Stress competitive differentiation

Brand value Minimize

Channels Exclusive with high partner investment

Restricted with focus on value add

Open to maximize coverage

Migration to lowest cost channels

0+

Industry revenueIndustry profit

-

Product lifecycle chart adapted from Geoffrey

Moore, Dr. Diane Badame, USC Marshall

School and IRCG

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

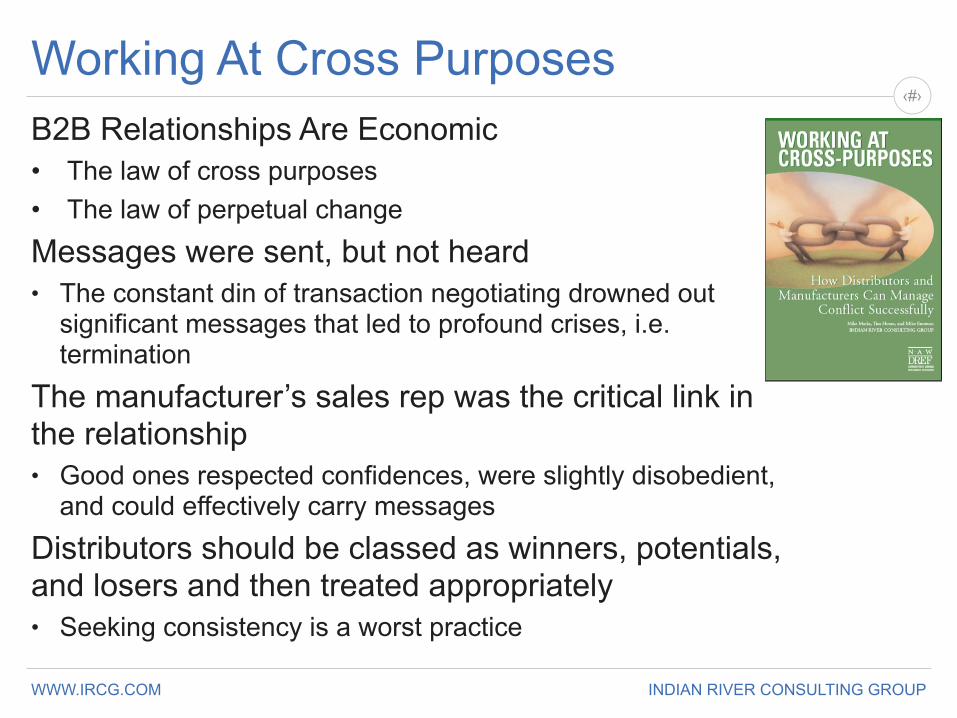

‹#›Working At Cross PurposesB2B Relationships Are Economic • The law of cross purposes • The law of perpetual change Messages were sent, but not heard • The constant din of transaction negotiating drowned out

significant messages that led to profound crises, i.e. termination

The manufacturer’s sales rep was the critical link in the relationship • Good ones respected confidences, were slightly disobedient,

and could effectively carry messages

Distributors should be classed as winners, potentials, and losers and then treated appropriately • Seeking consistency is a worst practice

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

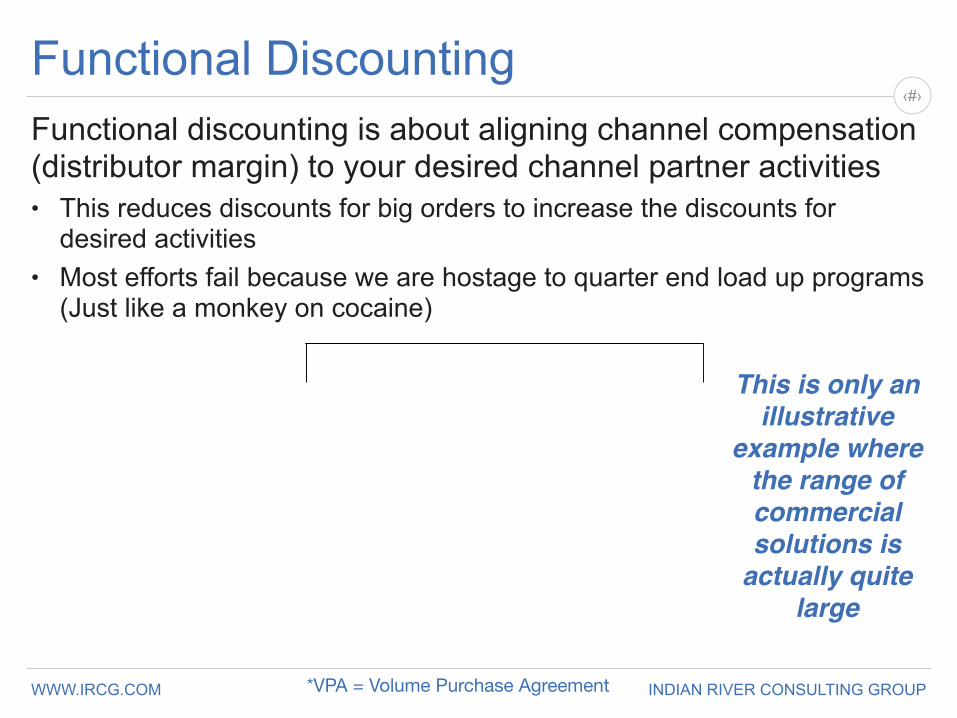

‹#›Functional DiscountingFunctional discounting is about aligning channel compensation (distributor margin) to your desired channel partner activities • This reduces discounts for big orders to increase the discounts for

desired activities • Most efforts fail because we are hostage to quarter end load up programs

(Just like a monkey on cocaine)

Distributor Annual Volume

>300K 101-300K <100K

Base discount 32% 29% 26%

Market data 3% 3% 3%

EDI Ordering 4% 4% 4%

Meeting plan 2% 2% 2%

Total discount 41% 38% 35%

VPA* for Over Plan 5% 5% 5%

*VPA = Volume Purchase Agreement

This is only an illustrative

example where the range of commercial solutions is

actually quite large

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›I Will Compensate My Partner More If…They do more of these things • Order in standard quantities or in truckload quantities • Provide responsive point of sale reporting • Price their activity within my guidelines • Increase the number of market leading contractors that specify my product • Sell the full product offering not just the fast movers • Stock appropriate product breadth • Increase their sales (not purchases) of my product • Increase my revenue share of the product category

They do less of these things • Carry competing brands in my core product areas • Take unauthorized discounts • Competitively capture business that I already have with another distributor • Ordering product with rush expediting

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Mass CustomizationBy focusing on end users rather than products, distributors can cross subsidize within their product basket (think of loss leaders at Home Depot) • Lose money on individual items to secure an overall profitable order • Lose money on individual orders to secure an overall profitable customer • Accept lower margins on high velocity items or strong brands

Customization and variation increase customer switching costs which creates higher distributor margins

!!Manufacturers are often incapable of providing transactional support services for end users

% of Sales Gross Margin % of Gross Profit % of Sales EffortPrimary Products 60% 18 – 20% 47% 68%

Secondary Products 30% 25 – 35% 37% 30%

Tertiary Products 10% 40% 16% 2%

Distributors really care about their total bundle margin more than the margin on your product

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Product Position* Implications

Distributor objectives Manufacturer strategies

Primary Products

• Drive volume • Premier brands and door openers • High turns support lower margins

• Leverage market power • Volume based pricing with growth rebates • Brand building

Secondary Products

• Fill product gaps and expand wallet share • Recognized brands • Medium turns and margins

• Be “easy to do business with” • Functional pricing with loyalty rebates • Direct demand creation

Tertiary Products

• Drive profit • Safe brands • High margins support lower turns

• Be “easy to do business with” • Simple pricing • Wide and multiple channel availability

All the rest

#6 - #20

#1 - #5

~60%

Product Lines Portion of Revenue

~30%~10%

Primary

Secondary

Tertiary

* Within the distributor’s ranking of ALL their suppliers

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Group ActivityBreak into groups as instructed and discuss the questions and subjects that follow, making sure that everyone weighs in on

the conversation

On a scale of 1 to 10 how good are you at delivering tough love around channel conflict to your channel partners?

Who are the manufacturers that are best at using channel design as a part of their competitive advantage?

Out Of The Box Question For Extra Credit

Are there any industry examples where distributors have employed multiple selling channel design with low cost solutions and Internet selling?

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

‹#›Questions to PonderFor manufacturers • How effectively do you reallocate capital and staff to

changing market opportunities? • Is your pricing strategy driven mostly by take away

power? • Is the primary role of distribution for you mostly

market making or market serving?

For distributors • How effectively do you reallocate capital and staff to

changing market opportunities? • How much of your pricing practices are driven by

data-free stories or field sales input? • Are you strategy driven or simply selling service with

excellent people?

https://www.mckinseyquarterly.com/Strategy/

Growth/How_to_put_your_money_where_your_strategy_is_2946