new transactional technology and exclusion? scottish executive financial inclusion conference...

TRANSCRIPT

New transactional technology and exclusion?

Scottish Executive financial inclusion conference October 2007

Key issues

• Potential for technology to help tackle financial exclusion

• Barriers- demand and supply-side- to using new technologies must both be addressed

• Segmentation- there is no one-size-fits-all solution

The financially excluded

• Low-income

• 2 million unbanked

• Half those with bank account managing money in cash

• Heterogeneous group – ages, abilities, life stages

Potential

"If you always do what you've always done, you'll always get

what you've always got."

-- Susan Jeffries

Potential

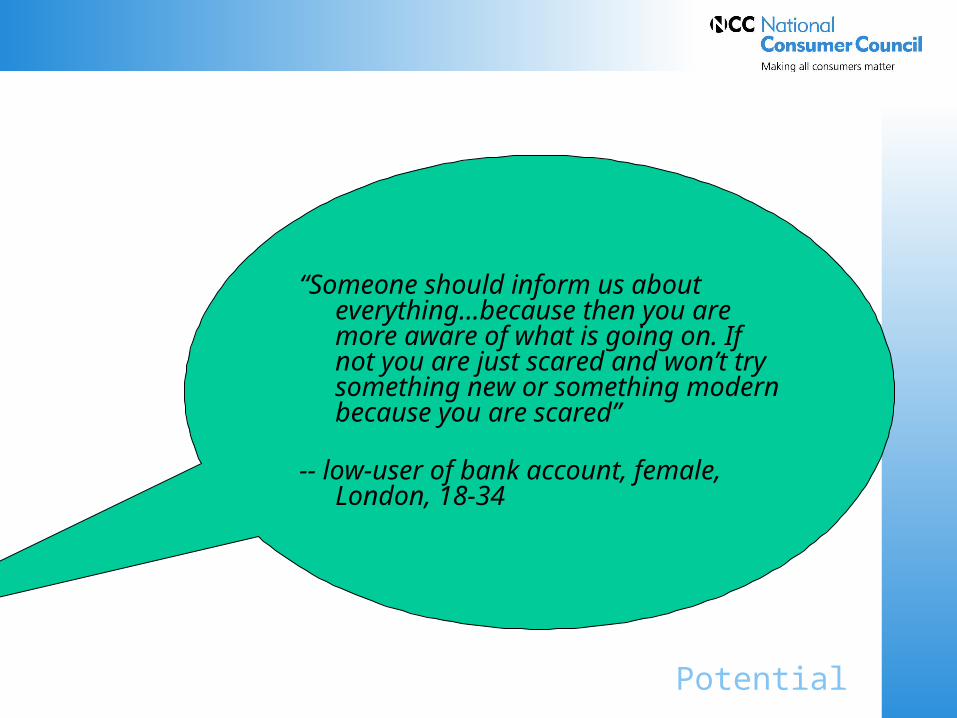

“Someone should inform us about everything…because then you are more aware of what is going on. If not you are just scared and won’t try something new or something modern because you are scared”

-- low-user of bank account, female, London, 18-34

Potential

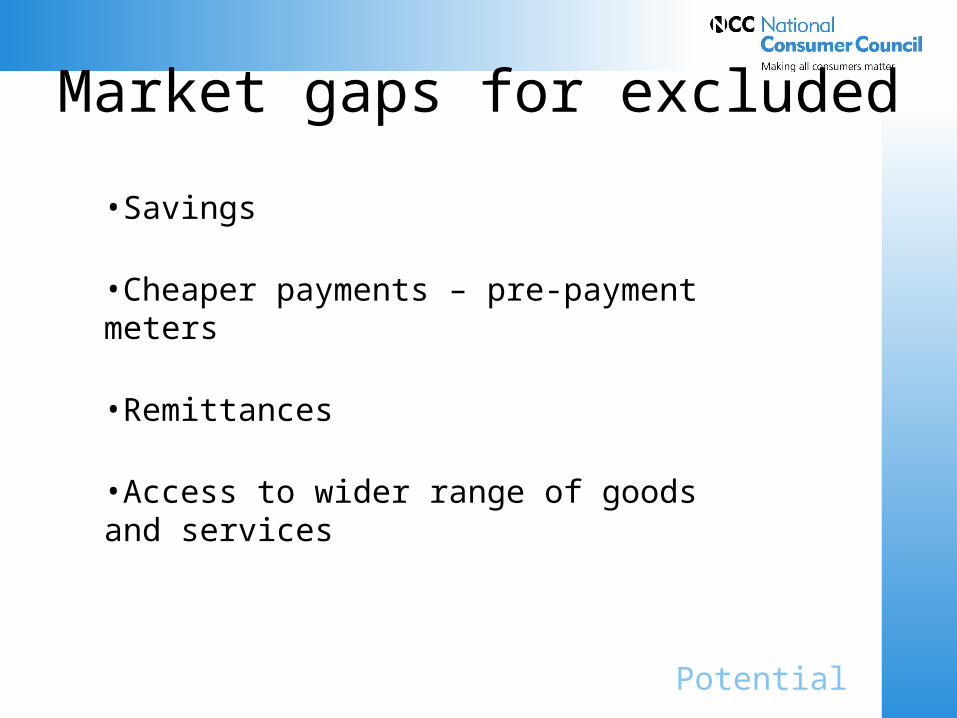

Market gaps for excluded

•Savings

•Cheaper payments – pre-payment meters

•Remittances

•Access to wider range of goods and services

Potential

Market developments• Increased ATM capability – mobile top-ups

• Internet and phone banking

• Mobile banking and text updates

• Pre-paid debit cards

• Contactless cards – wave and pay, One plus etc

• Mobile payments – refunds, text debit

• TV payments

• TV pay

Potential

Consumer needs

Money management requirements:

– Staying in control – avoiding debt

– Keeping track – sticking to budget

– Visibility – certainty

– Flexibility – what I want, when I need it

Potential + Barriers

Challenge for new technologies

Being part of the solution to exclusion by:

– Being a better option than the competition

– Successfully tackling demand and supply side barriers by building on what works

– Recognising limits / targeting successfully – no one size fits all solution

Barriers

The competition

• Cash – accessible, affordable, available and appropriate. Offering familiarity, simplicity, known risks and costs.

• Habit – I know where I am, and what I’m doing

• Inertia- if it’s not broken, don’t try to fix it

Barriers

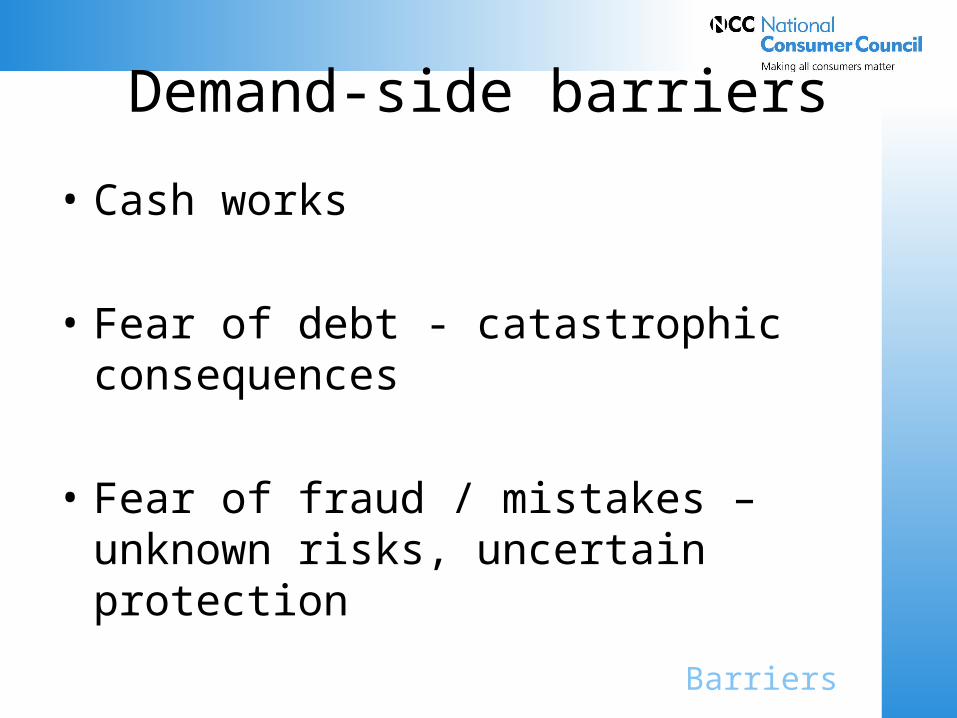

Demand-side barriers

• Cash works

• Fear of debt - catastrophic consequences

• Fear of fraud / mistakes – unknown risks, uncertain protection

Barriers

Demand-side barriers

• Need for simplicity and clarity on roles and responsibilities “who do I go to when things go wrong?”

• Tools: No bank account / credit / debit card/ 3G phone / digital exclusion

• Additional costs of new technologies

• Skills, confidence and information gaps

Barriers

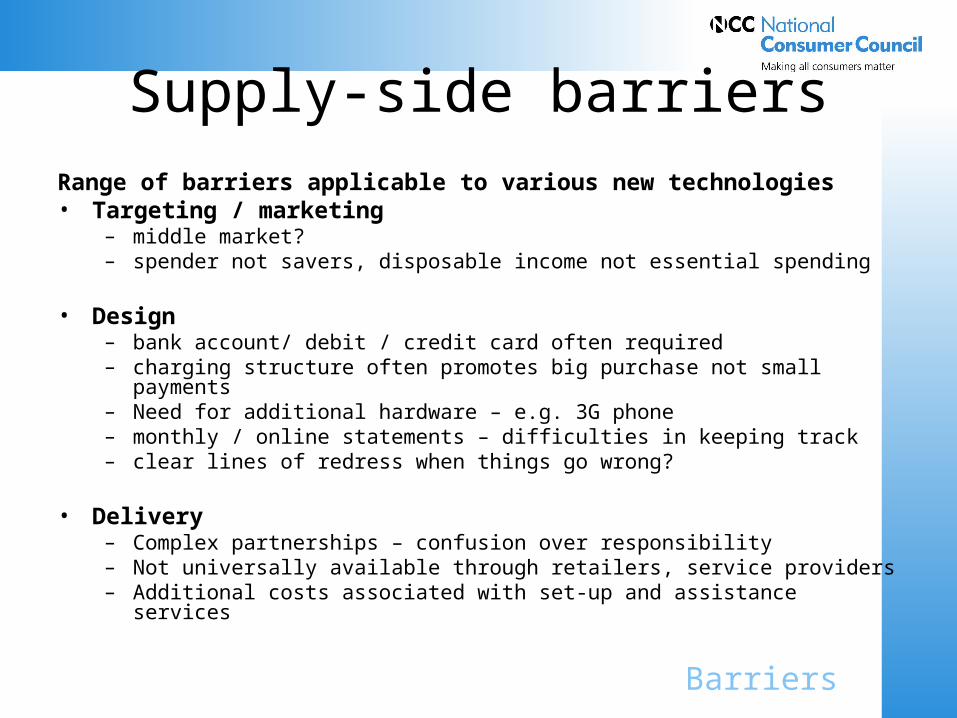

Supply-side barriersRange of barriers applicable to various new technologies• Targeting / marketing

– middle market? – spender not savers, disposable income not essential spending

• Design– bank account/ debit / credit card often required– charging structure often promotes big purchase not small payments– Need for additional hardware – e.g. 3G phone– monthly / online statements – difficulties in keeping track– clear lines of redress when things go wrong?

• Delivery – Complex partnerships – confusion over responsibility– Not universally available through retailers, service providers– Additional costs associated with set-up and assistance services

Barriers

Targeting successfully to change behavior

adapted from social marketing theory

Ready and willing

Unable Resistant

Awareness Education Education Education

Attitude Education Tackle barriers and educate

Enforce, Educ

Trial Behavior Education Tackle barriers + incentives

Enforcement

Repeat Behavior

Education Tackle barriers and educate

Enforcement

Segmenting

To conclude

•Potential on both supply and demand sides for technology to make a difference

•Barriers- demand and supply-side- work to do on both sides to harness potential and get inclusive design and delivery •Segmentation- there is no one-size-fits-all solution- targeting certain groups of excluded people may be more effective than a blanket approach

Future scenarios

1. No change- cashless society is a myth

2. Higher degree of financial inclusion for some groups, but not others

3. Further financial exclusion as middle market needs are met by technology and cash becomes more expensive

Some questions for discussion• Which new technologies are currently being used to promote financial inclusion and by who?

What can be done to roll these out?

• What is the role of local organisations, including the third sector and the public sector in using and promoting new technology?

• How do we measure and monitor exclusion from new technologies over time given the diversity of the market?

• Is there adequate consumer protection in place to limit consumer detriment with regards to: the pre-pay market; security risks; and fraud e.g. ID theft. Who should be examining these issues?

• Which scenario(s) is / are most likely, and what are the implications for financial inclusion? is there an alternative not set out here?

• What is the role of the National payments plan in promoting financial inclusion? Which other bodies / policy changes could make a difference?

Thank you for your time and contributions to the discussion

Nicola O’Reilly

Senior Policy Advocate

National Consumer Council