newsletter march 2016 - baroda-icai.org · holi celebration date : faculty : time ... prohibition...

TRANSCRIPT

CA. Viral ShahChairman98243 62211

CA. Arpan DodiaVice-Chaimram98983 83530

CA. Dhiren ParikhSecretary93762 11099

CA. Kejal PandyaTreasurer98259 77220

CA. Pradeep AgrawalEx-officio98985 60967

CA. Yash BhattImm. Past Chairman99243 88339

CA. Utpal ShahCommittee Member &Study Circle Convener98250 28960

CA. Hitesh AgrawalCommittee Member99980 28737

CA. Krunal BrahmbhattCommittee Member78748 11551

CA. Vinod PahilwaniCommittee Member98980 78176

CA. Viral ShahCA. Krunal BrahmbhattCA. Priyanka ThakkarCA. Jigita Shah

EditorialTeam

Chairman Message

Volume - II March 2016

Dear Members

February 2016 saw the change of guards at ICAI Delhi where an

inspiring and mature leadership of CA. M. Devaraja Reddy and

visionary CA. Nilesh Vikamsey occupied the office of President and

Vice President respectively.

I also take the opportunity to congratulate new team of WIRC, CA.

Shruti Shah, CA. Hardik Shah, CA. Kamlesh Saboo and CA. Shipa

Shinagare on being elected as the Chairman, Vice Chairman,

Secretary and Treasurer respectively of Western India Regional

Council for the year 2016-17.

It gives me immense sense of pride to share about yet another victory

of TEAM BARODA 2015. Baroda Branch has been adjudged as

Commendable Branch at Western India Regional Council for the year

2015 and Baroda WICASA 2015 is conferred certificate of

appreciation by ICAI and Best Branch of Western India Regional

Council for the year 2015. Kudos to TEAM BARODA.

The month of February had a flurry of activities consisting of-

Workshop on ICDS, Half day seminar on Permanent Establishment

and Attribution of Business Profit, Interactive Meet with CIT-TDS,

Cricket Tournament League for CA members and 2 days Seminar on

Business Improvement – Restructuring and Turnaround.

Every year new generation of CAs arrive who become part of our

fraternity. To facilitate the transition from a student to a fully qualified

professional, Orientation program of fresh CAs was held at Baroda

branch during the month.

Further, during the year, we have taken up a herculean task to bring

out the Members’ Directory 2016 with members’ photographs. We

have adopted two methods to collect data from members

1. We have sent manual forms along with

Newsletter

2. Members can also fill up and upload the

Directory Form online from Baroda

Branch Website.

I am confident that sincere efforts of my team

and co-operation of all the members will help to

bring the Members’ Directory 2016 very soon.

Details of programs for the month of March are given in the

newsletter and I hope members will participate and be benefitted by

the same. We will begin the month with programs like Budget

Demystified, Women’s Day Celebrations to acknowledge the efforts

of women in each one of our lives, and Holi Celebration at the end of

the month to celebrate spring, a rejuvenation of nature and renewed

hope of happiness and peace.

I again reiterate and request all the members of Baroda Branch

including the new members to stay connected with the Baroda

Branch and in case of any issues directly report to the admin

department at Baroda Branch instead of writing to ICAI which causes

unnecessary chaos and unwanted communications. Also new

members are requested to submit their postal and email address to

the Branch to ensure you get the newsletter and other

correspondences.

Thank you,

Chairman

CA. Viral Shah

Forth Coming Events

Direct Tax Updates

Judicial Decisions on Excise and Service Tax

Service Tax Updates

FAQS on IND AS 36

3D

Life Lessons

Direct Tax Budget Highlilghts

Due Date Planner

Memory Lane

Spiritual Corner

02

03

04

05

05

07

08

09

10

11

02

Co

nt

en

ts

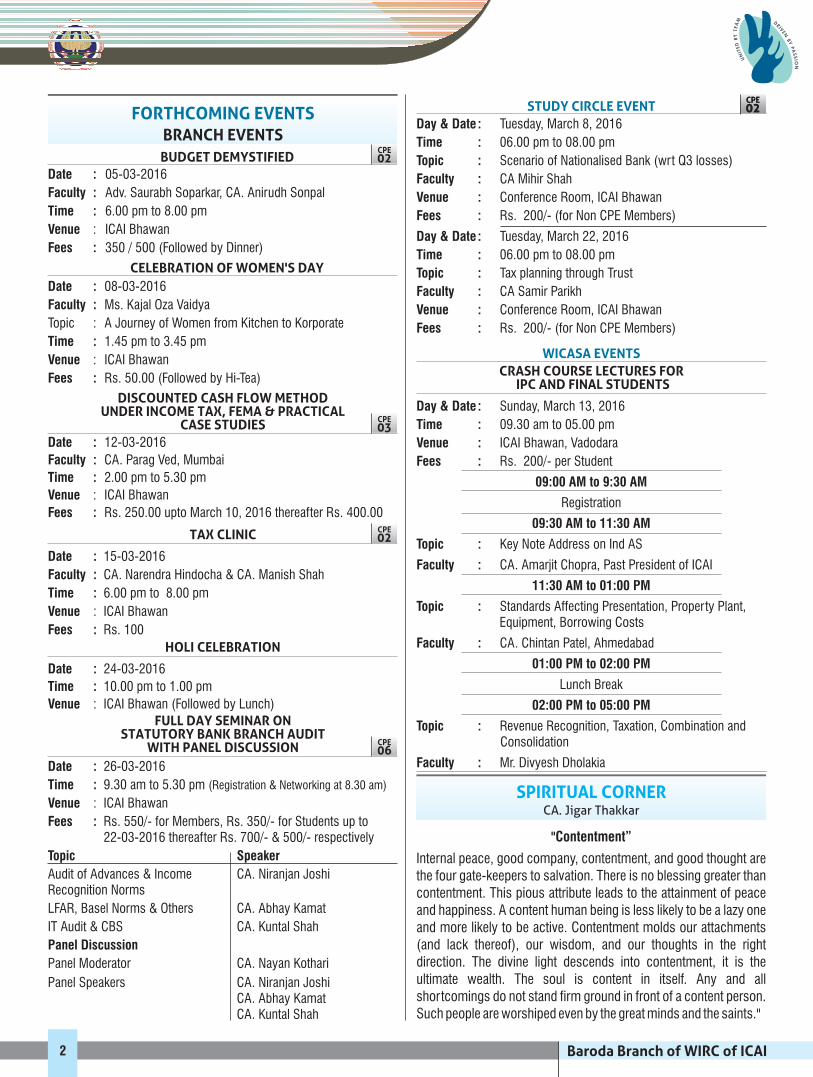

FORTHCOMING EVENTSBRANCH EVENTS

BUDGET DEMYSTIFIED

CELEBRATION OF WOMEN'S DAY

DISCOUNTED CASH FLOW METHODUNDER INCOME TAX, FEMA & PRACTICAL

CASE STUDIES

CRASH COURSE LECTURES FORIPC AND FINAL STUDENTS

TAX CLINIC

FULL DAY SEMINAR ONSTATUTORY BANK BRANCH AUDIT

WITH PANEL DISCUSSION

HOLI CELEBRATION

Date :

Faculty :

Time :

Venue

Fees :

05-03-2016

Adv. Saurabh Soparkar, CA. Anirudh Sonpal

6.00 pm to 8.00 pm

: ICAI Bhawan

350 / 500 (Followed by Dinner)

Date :

Faculty :

Time :

Venue

Fees :

08-03-2016

Ms. Kajal Oza Vaidya

Topic : A Journey of Women from Kitchen to Korporate

1.45 pm to 3.45 pm

: ICAI Bhawan

Rs. 50.00 (Followed by Hi-Tea)

Date :

Faculty :

Time :

Venue

Fees :

12-03-2016

CA. Parag Ved, Mumbai

2.00 pm to 5.30 pm

: ICAI Bhawan

Rs. 250.00 upto March 10, 2016 thereafter Rs. 400.00

Date :

Faculty :

Time :

Venue

Fees :

15-03-2016

CA. Narendra Hindocha & CA. Manish Shah

6.00 pm to 8.00 pm

: ICAI Bhawan

Rs. 100

Date :

Time :

Venue

Fees :

Topic Speaker

Panel Discussion

26-03-2016

9.30 am to 5.30 pm

: ICAI Bhawan

Rs. 550/- for Members, 350/- for Students up to22-03-2016 thereafter 700/- & 500/- respectively

Audit of Advances & IncomeRecognition Norms

LFAR, Basel Norms & Others CA. Abhay Kamat

IT Audit & CBS CA. Kuntal Shah

Panel Moderator CA. Nayan Kothari

Panel Speakers CA. Niranjan JoshiCA. Abhay KamatCA. Kuntal Shah

(Registration & Networking at 8.30 am)

Rs.Rs.

CA. Niranjan Joshi

Date :

Time :

Venue

24-03-2016

10.00 pm to 1.00 pm

: ICAI Bhawan (Followed by Lunch)

CPE02

CPE02CPE02

CPE03

CPE02

CPE06

STUDY CIRCLE EVENT

WICASA EVENTS

Day & Date :

Time :

Topic :

Faculty :

Venue :

Fees :

Day & Date :

Time :

Topic :

Faculty :

Venue :

Fees :

Tuesday, March 8, 2016

06.00 pm to 08.00 pm

Scenario of Nationalised Bank (wrt Q3 losses)

CA Mihir Shah

Conference Room, ICAI Bhawan

Rs. 200/- (for Non CPE Members)

Tax planning through Trust

CA Samir Parikh

Conference Room, ICAI Bhawan

Tuesday, March 22, 2016

06.00 pm to 08.00 pm

Rs. 200/- (for Non CPE Members)

Day & Date :

Time :

Venue :

Fees :

09:00 AM to 9:30 AM

09:30 AM to 11:30 AM

Topic :

Faculty :

11:30 AM to 01:00 PM

Sunday, March 13, 2016

09.30 am to 05.00 pm

ICAI Bhawan, Vadodara

Rs. 200/- per Student

Registration

Key Note Address on Ind AS

CA. Amarjit Chopra, Past President of ICAI

Topic :

Faculty :

01:00 PM to 02:00 PM

02:00 PM to 05:00 PM

Topic :

Faculty :

Standards Affecting Presentation, Property Plant,Equipment, Borrowing Costs

CA. Chintan Patel, Ahmedabad

Lunch Break

Revenue Recognition, Taxation, Combination andConsolidation

Mr. Divyesh Dholakia

2

"Contentment”

Internal peace, good company, contentment, and good thought arethe four gate-keepers to salvation. There is no blessing greater thancontentment. This pious attribute leads to the attainment of peaceand happiness. A content human being is less likely to be a lazy oneand more likely to be active. Contentment molds our attachments(and lack thereof), our wisdom, and our thoughts in the rightdirection. The divine light descends into contentment, it is theultimate wealth. The soul is content in itself. Any and allshortcomings do not stand firm ground in front of a content person.Such people are worshiped even by the great minds and the saints."

SPIRITUAL CORNERCA. Jigar Thakkar

DIRECT TAX UPDATESCA. Narendra Hindocha

1. Courtesies by Pharma Companies toDoctors

while doctors are not permitted toaccept courtesies, there is noprohibition on pharma companiesextending such courtesies.

Board Circular was issued after theend of relevant year

small gifts bearingcompany logo to doctors does nottantamount to giving gifts

sponsoringdoctors

purpose isthat they gather contemporaryknowledge

2. Paperless proceedings underIncome-tax Act

Reading of this decision reminded meof Mulla Naseeruddin stories.

According to Explanation 1 to Section37, expenditure incurred for a purposewhich is prohibited by law is notallowable.

According to Board circular, thisrequires disallowance of courtesiesextended by Pharma companies toDoctors as the Doctors are notallowed to accept such courtesiesaccording to rules of Medical Council.

Mumbai Bench of ITAT in case ofSyncom Formulations (I) Ltd, ITANo.6429&6428/Mum/2012, held that

The disallowance was deleted for twoother reasons, one being that the

(although theExplanation 1 to section 37 wasexisting and applicable during therelevant year). The other reason wasthat giving of

to doctorsbut it is regarded as advertisingexpenses. As regards

for conferences andextending hospitality, the

about management ofcertain illness/disease and learnabout newer therapies.

We may be very close to a time whenall notices will be received, replies willbe sent, assessment proceedingstake place, applications are filed anddisposed off, and appeals are filed,all electronically by emails or onwebsite.

Notification No. 2016 dated 3rd dayof February, 2016 goes a step further

in that direction by prescribing theProcedure, Formats and Standards forensuring secured transmission ofelectronic communication.

Some takeaways:

- Sub-Section (1) of ofof the Income Tax Act 1961,

(the Act) provides that the

or order or any othercommunication under the Act

- As per Rule 127 which deals withfor Service of notice, summons,requisition, order and othercommunication communication

- Communication to be

to be his officialdesignation based email addressu n d e r t h e d o m a i [email protected] (hereinafterreferred to as "designationemail").

- For the purpose of electroniccommunication, the AO shallattach the scanned copy of thenotice under section 143(2) or142(1) bearing his/her signaturein PDF format to the email beingsent to the assessee.

- In case the total size of theattachments exceed 10 MB thenthe assesse shall split theattachment. In each suchattachment, assessee shalls p e c i f i c a l l y c l a r i f y t h ecorresponding Notice Numberand date in the footer to which theattachment relates and numberthe pages in continuation for allattachments to ensure properlinkage

For the purpose of keeping ana u d i t t r a i l o f

Section282

service of a notice or summon orrequisition

may be made by delivering ortransmitting a copy thereof inthe form of any electronicrecord

may be to email ID stated inreturn of that year or later year,or the site of MCA, or other IDintimated by the assessee toAssessing Officer.

from theemail address of AssessingOfficer

notices/questionnaire issued byAO to assessee and theassessee's response withsuppor t ing documents asattachments, a copy of the emails h a l l b e m a r k e d t o e [email protected] the subject line as under:

Subject in email from assessee toAO- should be in the format: "PAN(eg-XXXXX1234X) - AY (eg-AY201314)-Reply-N" (N is thes e r i a l n u m b e r o f t h enoticeeg.Reply-1, Reply-2 etc.).

- All as perthis procedure shall be stored inthe ITD database and thecommunication status shall be

- The AO shall pass the order andattach

This procedure is applicable to theassessment proceedings in respect ofselect non-corporate assessees as apart of the pilot project on paoerlessassessment proceedings and can beextended to other assessees or otherproceedings

We keep receiving notices undersection 245 for adjustment of wrongdemands against refunds due. Ourobjections are often not dealt withappropriately and the wrong demandsget adjusted against refunds.

CBDT Memorandum dated 29-1-2016 (F. No. 312/109/2015 – OT)tries to ensure that the

to notices under section245 for ITRs processed in F. Y. 15-16

The relevant paragraph:

In cases where the tax payer hascontested the demand, CPC wouldissue a reminder to the jurisdictionalAssessing Officers about thecontention of the taxpayer, askingthem to either confirm, or makeappropriate changes, to the demand,

emails sent or received

displayed the assesse's "MyAccount" on the E-filingportal

order u/s 143(3) bearinghis/her signature in PDF format

3. Adjustment of wrong demandsagainst refunds

adjustmentsare not made until disposal ofobjections

3

within thir ty days.

Theresponsibility of non-adjustment ofrefund against outstanding arrears, ifany, would lie with the AssessingOfficer.

In case noresponse is received from thejurisdictional Assessing Officer,within the stipulated period of thirtydays, CPC would issue the refundwithout any adjustment.

JUDICIAL DECISION ONEXCISE AND SERVICE TAX

CA. Anirudh Sonpal

I. CENVAT CREDIT

1.1 Assessee is an instrumentality ofUnion and is in business inter alia ofsupply of natural gas to industrial andother consumers - Hazira unit ofassessee was providing taxableoutput service of supply of goodsthrough pipeline to local consumersand others from other destinationsthrough Hazira, Vijaypur, Jagdishpur(HVJ), pipeline - They had takencenvat credit on basis of invoicesraised by its Vaghodia unit - If a personis discharging ST liability from hisregistered premises, benefit of cenvatcredit on ST paid by service providercannot be denied, only on ground thatinvoices are in name of branch officeswhich were not separately registered.[GAIL India Ltd vs CCE & ST – NewDelhi Cestat]

1.2 C o u r i e r S e r v i c e u s e d f o rsending/receiving documents relatedto business, or for movement ofinputs and finished goods is eligiblefor credit only upto place of removal;credit cannot be allowed formovement of finished goods, afterplace of removal.[Lear Automotive India(Pvt) Ltd vsCCE&ST- Ahmedabad Cestat]

1.3 Requirement of registration isprocedural; hence, credit cannot bedenied to input service distributoreven if it is unregistered, providedassessee has maintained all recordsfor verification by revenue.[CCE vs Dashion Ltd – Gujarat HC]

1.4 Quantification - Revenue took viewthat admissible quantum of credit ofservice tax suffered on rent paid on theearmarked area to carry out thetaxable service of 'vehicles servicing'should be determined as per Rule 6(3)but not on the basis of the rent payablefor the relevant leased area- Ruleprescribes a formula to quantify thepermissible credit and is applicableonly when there is use of the commoninput without maintenance ofaccounts - In the case there is adocument in the form of Lease Deedwhich categorically brings out the twotypes of buildings used for respectivepurposes in terms of Schedule ofProperty, out of which the 'A.C.Roofing building' was leased toappellant for providing vehicleservicing service - Lease Deed wasthe basic document to avail the spaceto carry out servicing activity andcannot be ignored - When there wasan earmarked area with specifiedsq.ft., for the purpose of providing theservice which is apparent from LeaseDeed, in absence of any evidence orphysical inspection report showinganything contrary to the claim,creditof service tax paid on rent paid inrespect of that specified space isadmissible as input service credit.[Gem Motors vs CC, CE & ST –Chennai Cestat]

1.5 When assessee-manufacturer ofcement was required to plant trees toprevent pollution in its factory areaand paid service tax for suchmaintenance, it was entitled to inputservice credit.[CCE & ST, Tiruchirapalli vs GrasimIndustries Ltd – Chennai Cestat]

1.6 Appellant availed CENVAT Credit onthe duty paid inputs which arecommon to dutiable as well asexempted goods - Depar tmentdemanding an amount equivalent to10% of the value of exempted goods -Appellant reversed the exact amountattributable to the inputs which havegone in the manufacture of exemptedfinal products and producing C.A.

certificate in this regard. Held: Rule 6of the CCR is not enacted to extractillegal amount from the assessee - Ifthis is the objective then, at the most,amount which is to be recovered shallnot be in any case more than CenvatCredit attributed to the input or inputservices used in the exempted goods[Nitcon Valve Inds Ltd vs CCE –Mumbai Cestat]

1.7 Assessee is manufacturer of M.S.Ingots from sponge iron - Duringcourse of manufacture of M.S. Ingots,slag dust is generated as by-productswhich is fully exempt from duty undernotfn 4/06-CE and accordingly slagdust is cleared at nil rate of duty -Depar tment views that sinceassessee were using common inputsin relation to manufacture of dutiablegoods (M.S. Ingots) and exemptedgoods (Slag dust) without maintainingseparate accounts, an amount of 5%of sale value of slag dust would bepayable under Rule 6(3) of CCR, 2004- Complying with Rule 6 (2) isi m p o s s i b l e w h e r e w h i l emanufacturing a product, anotherproduct emerges as an unavoidableby-product or as waste - Sub-rule (3)of Rule 6 becomes applicable onlywhen manufacturer does not complyprovisions of sub-rule (2) andprovisions of sub-rule (3) would notbe applicable in cases where the sub-rule (2) is inapplicable - Assessee isnot liable to pay any amount in respectof clearance of slag/dust which hasbeen cleared by them withoutpayment of duty.[N S Ispat Pvt Ltd vs CCE – New DelhiCestat]

1.8 Where assessee, a manufacturer, hadthree units located at 'K', 'A' and 'R' and'R' unit was exempted from paymentof excise duty and during periodassessee paid service tax on variousservices received by it, which werebeing used in all three units, andfurther it considered services used at'R' unit as cenvatable and Cenvatcredit availed in respect of same wasdistributed to 'K' and 'A' units,

4

5

Adjudicating Authority was justified indisallowing cenvat credit of servicetax in respect of services used in 'R'unit on proportionate basis.[ Fosroc Chemicals India (P.) Ltd. vsCCE&ST, Bangalore LTU – BangaloreCestat]

2.1 Where assessee had exported goodsso manufactured by it after paymentof duty and filed rebate applications inincorrect format, which were returnedby Adjudicating Authority andthereupon assessee representedrebate applications in correct format,these applications would relate backto original date of filing of rebateapplications.[Apar Industries vs UoI – Gujarat HC]

2.2 Rule 5 of CCR, 2004 - There is noprovision in law that CENVAT creditcan be allowed only after registrationof the unit - credit is allowed in respectduty suffered on input/input servicesand the said payment has nothing todo with the registration of the recipientof the services, therefore, registrationcannot be made criteria to reject therefund claim.[Prudential Process ManagementServices India Pvt Ltd vs CST –Mumbai Cestat]

3.1 Crate rentals recovered by beverage-manufacturers is 'deemed sale' asthere is transfer of right to use witheffective control and possession ofcrates; hence, same is liable toVAT/CST and cannot be charged toservice tax[Hindustan Coca Cola Beverages (P.)Ltd. Vs CST – New Delhi Cestat]

3.2 Perquisite extended by employer byway of car provided for personal andofficial use to employees, againstpayment equal to cost incurred byemployer, does not amount to serviceunder section 65B(44)(b), as it is incourse of employment and therefore,excluded from scope of service[J.P. Morgan Services India (P.) Ltd -AAR

II. REFUND

III. SERVICE TAX - LEVIABILITY

SERVICE TAX UPDATESCA. Manilal Parsiya

The Central Government hereby appointsthe 1st day of April, 2016 as the date onwhich the provisions of sub-section (1) ofsection 109 of the said Act shall come intoeffect through

. Sec. 66D gets amendedand the word “support services” is replacedby “any service”. Meaning thereby allservices provided by the Government or alocal authority are now taxable unless andotherwise excluded by negative list or anyexemption notification.

inserts entry (48) in notification25/2016-ST dated 20.06.2012 providesexemption on services provided byGovernment or a local authority to abusiness entity with a turnover up to rupeesten lakh in the preceding financial year.

amends notification 22/2015-ST dated 06.11.2015 so as to grant powerto Central Government to exempt fromSwachh Bharat Cess by way of specialorder U/s. 93(1) as well as U/s. 93(2) of theFinance Act, 1994.

introduces Annual InformationReturns (AIR) under Central Excise andService Tax laws to be furnished by ReserveBank of India for details of foreignremittance receipts of services declaredunder purpose codes for such entitieswhose value of remittances aggregates tomore than fifty lakh rupees in a financial yearto which the return pertains. And by a StateElectricity Board or an electricity distributionor transmission licensee under theElectricity Act 2003, or any other entityentrusted with such functions by the CentralGovernment or State Government, in caseof electr ici ty consumed by suchmanufacturers, using an induction furnaceor rolling mill to manufacture goods fallingunder Section XV of the First Schedule to theCentral Excise Tariff Act, 1985 (5 of 1986)whose aggregate value of clearancesexceeds one hundred and fifty lakh rupeesin the financial year to which the returnpertains, as identified and intimated to himby the Principal Chief Commissioner or the

Notification No. 06/2016-STdated 18.02.2016

Notification No. 07/2016-ST dated18.02.2016

Notification No. 05/2016-ST dated17.02.2016

Notification No. 04/2016-ST dated15.02.2016

Chief Commissioner of Central Excise andService Tax in-charge of the Central Exciseor Service Tax Zone, by the 30th June of thesubsequent financial year.

seeks to amend notification No.39/2012- ST, dated the 20th June, 2012 soas to provide for rebate of Swachh BharatCess paid on all services, used in providingservices exported in terms of rule 6A of theService Tax Rules.

seeks to amend notification No.12/2013- ST, dated the 1st July, 2013 so asto allow refund of Swachh Bharat Cess paidon specified services used in an SEZ.

seeks to amend notification No.41/2012- ST, dated 29.06. 2012 so as toallow refund of service tax on services usedbeyond the factory or any other place orpremises of production or manufacture ofthe said goods for the export of the saidgoods and to increase the refund amountcommensurate to the increased service taxrate.

Notification No. 03/2016-ST dated03.02.2016

Notification No. 02/2016-ST dated03.02.2016

Notification No. 01/2016-ST dated03.02.2016

FAQS ON IND AS 36:IMPAIRMENT OF ASSETS: PART III

CA. Prashant Upadhyay

1) What are the provisions in thestandard relating to reversal ofImpairment Loss?

Impairment loss recognized for anasset in prior accounting periodsshould be reversed if there has been achange in the estimates of cashinflows, cash outflows or discountrates used to determine the asset’srecoverable amount since the lastimpairment loss was recognizedleading to increase in carrying out ofasset and consequent reversal.

Increase in carrying amount cannotexceed the car r y ing amountdetermined had no impairment lossbeen determined net of amortisationor depreciat ion. Reversa l ofimpairment loss should be recognizedas income unless in terms of Ind AS16 – Property, Plant and Equipment inwhich case any reversal is on revaluedasset which should be treated as

6

revaluation increase under thatStandard.

Reversal of impairment loss of CGUshould be allocated to increasecarrying amount of assets of unit first,to assets other than Goodwill on pro-rate basis based on carrying amountof each asset in the unit; and then togoodwill allocated to CGU. Thecarrying amount of asset should notbe increased above the lower of a) Itsrecoverable amount and b) carryingamount had no impairment loss wouldhave been recognized in the asset.

An impairment loss recognized forgoodwill shall not be reversed insubsequent period. Ind AS 38,Intangible Assets, prohibits therecognition of internally generatedgoodwill. Any increase in therecoverable amount of goodwill in theperiods following the recognition of animpairment loss for that goodwill islikely to be an increase in internallygenerated goodwill, rather than areversal of the impairment lossrecognized for the acquired goodwill.

In terms with 126, entity shoulddisclose for each class of assets:

a) The amount of impairment lossesrecognized in P&L during theperiod and line items of statementof Profit & Loss in which thoseimpairment losses are included

b) The amount of reversals ofimpairment losses recognizedduring the period and line items inwhich those impairment lossesare reversed in statement of Profit& Loss

c) The amount of reversals ofimpairment losses on revaluedassets recognized in othercomprehensive income duringthe period.

Para 129 stipulates that, an entity thatrepor ts segment information inaccordance with Ind AS 108, shalldisclose the following for eachreportable segment:

2) What are the disclosures under thestandard?

a) The amount of impairment lossesrecognized in profit and loss andin other comprehensive income

b) The amount of reversals ofimpairment losses recognizedduring the period.

In terms in with 130 entity shalldisclose following for an individualasset (including goodwill) or a CGU,relating to impairment loss recognizedor reversed during the period:

a) The events & circumstancesleading recognition of impairment orreversal

b) Amount of impairment loss orreversal

c) For an individual asset:

i) Nature of asset & ii) if theentity repor ts segmentinformation in accordancewith Ind AS 108, thereportable segment to whichthe asset belongs.

d) For a CGU

i) A descr ipt ion of CGU(whether it is product line, aplant, a business operation, ageographical area, or arepor table segment asdefined in Ind AS 108) ;

ii) The amount of impairmentloss recognized or reversedby class of assets and if theentity repor ts segmentinformation in accordancewi th Ind AS 108, byreportable segment; and

iii) If the aggregation of assetsfor identifying the CGU haschanged since the previouse s t i m a t e o f C G U ’ srecoverable, a description ofcurrent and former way ofaggregating assets and thereasons for changing the wayCGU is identified.

e) The recoverable amount of asset( C G U ) a n d w h e t h e r t h erecoverable amount of asset(CGU) is its fair value less costs

of disposal or its value in use.

f) If the recoverable amounts is fairvalue less costs of disposal, theentity shall disclose the followinginformation:

i) The level of the fair valuehierarchy (see Ind AS 113)within which the fair valuemeasurement of the asset(CGU) is categorised in itsentirety (without taking intoaccount whether the ‘costsof disposal’ are observable);

ii) For fair value measurementscategorised within Level 2and Level 3 of the fair valuehierarchy, a despription of thevaluation techniques used tomeasure fair value less costsof disposal. If there has beena change in valuat iontechnique, the entity shalldisclose that change and thereasons for making it; and

iii) For fair value measurementscategorised within Level 2and Level 3 of the fair valueh i e r a r c h y, e a c h k e yassumpt ion on wh ichmanagement has based itsdetermination of fair valueless costs of disposal. Keyassumptions are those towhich the asset’s (CGU)recoverable amount is mostsensitive.

The entity shall also disclosethe discount rate(s) used incurrent measurement andprevious measurement if fairvalue less costs of disposalis measured using presentvalue technique.

g) If recoverable amount is value inuse, the discount rate(s) used inthe current estimate and previousestimate(if any) of value in use.

In terms with para 131 an entity shalldisclose following information foraggregate impairment losses and theaggregate reversals of impairmentlosses recognized during the periodfor which no information is disclosed

7

in accordance with para 130:

a) The main classes of assetsaffected by impairment lossesand the main classes of assetsa f fec ted by reversa ls o fimpairment losses.

b) T h e m a i n e v e n t s a n dcircumstances that led to therecognition of these impairmentl osses and reve rsa l s o fimpairment losses.

According to para 133, if, inaccordance with Para 84, any portionof the goodwill acquired in a businesscombination during the period has notbeen allocated to a CGU or group ofCGUs at the end of reporting period,the amount of unallocated goodwillshall be disclosed together withreasons why that amount remainsunallocated.

3-DCA. Abhay Desai

CENVAT CREDIT OF SALES COMMISSION –FINALLY SETTLED !!

1) INTRODUCTION

Lao Tzu said “The key to growth is the

introduction of higher dimensions of

consciousness into our awareness”.

Thinking about an issue only from one-

dimension may result in faulty action. This is

also true for indirect taxes. One has to think

from all points of view to get the best answer.

This column attempts to discuss various

issues pertaining to indirect taxes from all

the three dimensions i.e. Central Excise,

Service Tax & VAT.

1.1 Last week, Government has come outwith a notification (NOTIFICATIONNO.2/2016-C.E. (N.T.), DATED 3-2-2016) through which an explanationhas been inserted in the definition ofinput service under Rule 2(l) of CENVATCredit Rules, 2004 (CCR, 2004) whichprovides that sales promotion includesservices by way of sale of dutiablegoods on commission basis. This willprovide a good respite to large numberof manufacturer’s who have beenfacing litigation on this issue speciallyin Gujarat due to the decision of Hon.Gujarat High Court in the case of CCE v.Cadila Healthcare Ltd. [2013] 32

taxmann.com 105 (Guj.). Thiscommunication is aimed to understandthe background which leads to theissuance of above stated notificationand the implications of the same.

2.1 Definition of input service under Rule2( l ) o f CCR, 2004 inc ludesadvertisement or sales promotion asone of the input services. Hon. GujaratHigh Court in the case of CadilaHealthcare (supra) took a view that ift h e a g e n t s w o r k i n g f o r t h emanufacturer are only selling theirgoods but are not engaged in anypromotional activities, they are notcovered under “sales promotion” andhence service tax paid on thecommission to such agents is notadmissible for CENVAT credit. It washeld that such commission agentswhich enables sale but does not carryout any activities for promoting thesales is not covered in the definition ofinput service as it covers only salespromotion and not sales commission.While passing the said judgment, Hon.Gujarat High Court did not concur withthe view of Hon. Punjab & HaryanaH i g h C o u r t i n t h e c a s e o fCommissioner of Central Excise,Ludhiana v. Ambika Overseas [2012]22 taxmann.com 83 (Punj. & Har.)wherein they allowed the CENVATcredit on commission paid to theagents in procuring the orders eventhough they were not engaged in anypromotional activities. Relevantparagraph of Cadila’s decision isreproduced below for quick reference:

"(viii) From the definition of salespromotion, it is apparent that in case ofsales promotion a large population ofconsumers is targeted. Such activitiesrelate to promotion of sales in generalto the consumers at large and are morein the nature of the activities referred toin the p reced ing pa rag raph .Commission agent has been definedunder the explanation to businessauxiliary service and insofar as thesame is relevant for the presentpurpose means any person who actson behalf of another person and causessale or purchase of goods, or provisionor receipt of services, for a

2) HISTORY

consideration. Thus, the commissionagent merely acts as an agent of theprincipal for sale of goods and suchsales are directly made by thecommission agent to the consumer. Inthe present case, it is the case of theassessee that service tax had been paidon commiss ion pa i d to t hecommission agent for sale of finalproduct. However, there is nothing toindicate that such commission agentswere actually involved in any salespromotion activities as envisagedunder the said expression. The terminput service as defined in the rulesmeans any service used by a providerof taxable service for providing anoutput service or used by themanufacturer whether directly orindirectly, in or in relation to themanufacture of final products andclearance of final products from theplace of removal and includes servicesused in relation to various activities ofthe description provided thereinincluding adver tisement or salespromotion. Thus, the portion of thedefinition of input service insofar as thesame is relevant for the presentpurpose refers to any service used bythe manufacturer directly or indirectlyin relation to the manufacture of finalproducts and clearance of finalproducts from the place of removal.Obviously, commission paid to thevarious agents would not be covered inthis expression since it cannot bestated to be a service used directly orindirectly in or in relation to themanufacture of final products orclearance of final products from theplace of removal. The includes portionof the definition refers to advertisementor sales promotion. It was in thisbackground that this cour t hasexamined whether the services offoreign agent availed by the assesseecan be stated to services used as salespromotion. In the absence of anymaterial on record, as noted above toindicate that such commission agentswere involved in the activity of salespromotion as explained in the earlierportion of the judgement, in the opinionof this court, the claim of the assesseewas rightly rejected by the Tribunal.

8

Under the circumstances, theadjudicating authority was justified inholding that the commission agent isdirectly concerned with the sales ratherthan sales promotion and as such theservices provided by such commissionagent would not fall within the purviewof the main or inclusive part of thedefinition of input service as laid downin rule 2(l) of the Rules.

(ix) As regards the contention that inany event the service rendered by acommission agent is a service receivedin relation to the assessees activityrelating to business, it may be notedthat the includes part of the definition ofinput service includes activities relatingto the business, such as accounting,auditing, financing, recruitment andquality control, coaching and training,computer networking, credit rating,share registry, and security. The wordsactivities relating to business arefollowed by the words such as.Therefore, the words such as must begiven some meaning. In RoyalHatcheries (P) Ltd. v. State of A.P.,1994 Supp (1) SCC 429, the SupremeCourt held that the words such asindicate that what are mentionedthereafter are only illustrative and notexhaustive. Thus, the activities thatfollow the words such as are illustrativeof the activities relating to businesswhich are included in the definition ofinput service and are not exhaustive.Therefore, activities relating tobusiness could also be other than theactivities mentioned in the sub-rule.However, that does not mean that everyactivity related to the business of theassessee would fall within the inclusivepart of the definition. For an activityrelated to the business, it has to be anactivity which is analogous to theactivities mentioned after the wordssuch as. What follows the words suchas is accounting, auditing, financing,recruitment and quality control,coaching and training, computernetworking, credit rating, shareregistry, and security. Thus, what isrequired to be examined is as towhether the service rendered bycommission agents can be said to bean activity which is analogous to any of

the said activities. The activity ofcommission agent, therefore, shouldbear some similarity to the illustrativeactivities. In the opinion of this court,none of the illustrative activities, viz.,accounting, auditing, financing,recruitment and quality control,coaching and training, computernetworking, credit rating, shareregistry, and security is in any mannersimilar to the services rendered bycommission agents nor are the same inany manner related to such services.Under the circumstances, though thebusiness activities mentioned in thedefinition are not exhaustive, theservice rendered by the commissionagents not being analogous to theactivities mentioned in the definition,would not fall within the ambit of theexpression activities relating tobusiness. Consequently, CENVATcredit would not be admissible inrespect of the commission paid toforeign agents.

(x) For the reasons stated hereinabove,this court is unable to concur with thecontrary view taken by the Punjab andHaryana High Court in Commissionerof Central Excise, Ludhiana v. AmbikaOverseas (supra). Insofar as this issueis concerned, the question is answeredin favour of the revenue and against theassessee."

2.2 Due to the above view of Hon. GujaratHigh Cour t, several subsequentdecisions latest being the decision inthe case of Gujarat State Fertilizers &Chemicals Ltd. (Fiber Unit) v.Commissioner of Central Excise[2016] 65 taxmann.com 283 (Gujarat)has taken a similar view and deniedCENVAT credit on input services ofcommission agents who only enablethe sale of goods but do not carry outany promotional activities.

3.1 Through notification no. 2/2016-C.E.(N.T.), DATED 3-2-2016) referred in theintroduction, an explanation has beeninserted in the definition of inputservice wherein even the services byway of sale of dutiable goods oncommission basis (even if not carryingout any promotional activity) is

3) LATEST AMENDMENT

regarded as sales promotion and henceeligible for CENVAT credit. Hence theabove notification puts an end to thediffering opinions expressed by Hon.High Courts and provides respite to themanufacturers.

4.1) Hon. Supreme Court in the case ofSedco Forex International Drill Inc. vs.Commissioner (2002) (141 ELTA180)(SC) relying on the decision ofCommissioner of Income Tax vs.Goslino Mario (2000) (241 ITR314)(SC) has held that a cardinalprinciple of the tax is that the law to beapplied is that which is in force in therelevant assessment year unlessotherwise provided expressly or bynecessary implication. (See alsoReliance Jute and Industries Lit. vs.CIT). An Explanation to a statutoryProvision may fulfill the purpose ofclearing up an ambiguity in the mainProvision or an Explanation can add toand widen the scope of the mainSection. If it is in its nature clarificatorythen the Explanation must be read intothe main provision with effect from thetime that the main Provision came intoforce. But if it changes the law it is notpresumed to be retrospective,irrespective of the fact that the phrasesused are “it is declared” or “for theremoval of doubts”. Thus the test laiddown by the apex court is that theexplanation will have a retrospectiveeffect if it clears up an ambiguity. It canbe seen from above that Hon. GujaratHigh Court has taken a view which iscontrary to the view taken by Hon.Punjab & Haryana High Court. Thisresulted into ambiguity in theinterpretation of the definition of inputservice. To clarify the same, the abovereferred explanation has been insertedand hence in my view should have aretrospective effect.

4) WHETHER RETROSPECTIVE?

LIFE LESSONSCA. Bimal R. Bhatt

The Invisible Hand Inside Your Family

All parents aspire to raise the kind of childrenthat they know will make the rightchoices—even when they themselves are notthere to supervise. One of the most effectiveways to do that is to build the right family

9

Direct Tax-Budget HighlightsCA. Ronak Shah

culture. It becomes the informal but powerfulset of guidelines about how your familybehaves.

As people work together to solve challengesrepeatedly, norms begin to form. The same istrue in your family: when you first run upagainst a problem or need to get somethingdone together, you will need to find a solution.

It’s not just about controlling bad behavior;it’s about celebrating the good. What doesyour family value” Is it creativity? Hard work?Entrepreneurship? Generosity? Humility?What do the kids know they have to do that willget their parents to say, “Well done”?

This is what is so powerful about culture. It’slike an auto-pilot. What is critical tounderstand is that for it to be an effective fore,you have to properly program theautopilot—you have to build the culture thatyou want in your family. If you do notconspicuously build it and reinforce it fromthe earliest stages of your family life, a culturewill still form—but it will from in ways youmay not like. Allowing your children to getaway with lazy or disrespectful behavior a fewtimes will begin the process of making it yourfamily’s culture. So will telling them that youare proud of them when they work hard tosolve a problem. Although it’s difficult for aparent to always be consistent and rememberto give your children positive feedback whenthey do something right, it’s in these everydayinteractions that culture is being set. And oncethat happens, it’s almost impossible tochange.

The challenges your children face serve animportant purpose: they will help them honeand develop the capabilities necessary tosucceed throughout their lives. Coping with adifficult teacher, failing at a sport, learning tonavigate the complex social structure ofcliques in school—all these things become“courses” in the school of experience. Weknow that people who fail in their jobs often doso not because they are inherently incapableof succeeding but because their experienceshave not prepared them for the challenges ofthat job—in other words, they have taken thewrong “courses”.

The natural tendency of many parents is tofocus entirely on building your child’sresume: good grades, sports successes andso on. It would be a mistake, however, toneglect the courses your children need to

The Schools of Experience

equip them for the future. Once you have thatfigured out, work backward: find the rightexperiences to help them build the skills theywill need to succeed. It’s one of the greatestgifts you can give them.

A strategy—whether in companies or inlife—is created through hundreds ofeveryday decisions about how you spendyour time, energy and money. With everymoment of your time, every decision abouthow you spend your energy and your money,you are making a statement about what reallymatters to you. You can talk all you want abouthaving a clear purpose and strategy for yourlife, but ultimately this means nothing if youare not investing the resources you have in away that is consistent with your strategy. Inthe end, a strategy is nothing but goodintentions unless it’s effectively implemented.

How do you make sure that you areimplementing the strategy you truly want toimplement? Watch where your resourcesflow—the resource allocation process. If it isnot supporting the strategy you have decidedupon, you run the risk of a serious problem.You might think you are a charitable person,but how often do you really give your time ormoney to a cause or an organisation that youcare about? If your family matters most toyou, when you think about all the choices youhave made with your time in a week, doesyour family seem to come out on top?Because if the decisions you make aboutwhere you invest your blood, sweat and tearsare not consistent with the person you aspireto be, you will never become that person.

( “How Will You Measure Your Life?”by Clayton M. Christensen)

Your Strategy is Not What You Say ItIs

Source:

INCOME-TAX�

�

�

�

Income-tax rates for individuals remainunchanged.Surcharge has been increased from 12%to 15% on income-tax for incomeexceeding INR 10 million for individual,HUF, AOP, BOI or artificial judicial person.No requirement to furnish PAN by non-resident individuals and foreigncompanies in respect of certainincomes, subject to prescribedconditions.Deduction under section 80GG of theIncome-tax Act on account of rent paid byan individual increased from INR 2,000

per month to INR 5,000 per month.Exemption on funds withdrawn fromRPF/SAF in respect of contributionsmade on or after 1 April, 2016 restrictedto 40% of such contributions.Exempt ion l imi t o f employer ’scontribution to RPF on behalf ofemployee is equal to 12% of employee’ssalary or INR 150,000, whichever is less.Exempt ion l imi t o f employer ’scontribution to an approved SAFincreased from INR 100,000 to INR150,000.Transfer of balance from RPF/SAF to NPSexempt from tax.Up to 40% of the amount withdrawn fromNPS upon closure of account or optingout of the scheme is exempt from tax.Rates of corporate tax remainunchanged for both domestic andforeign companies except the following:Corporate tax rate of 25% for domesticcompanies, if set-up and registered after1 March, 2016 and does not claim anytax incentives.Corporate tax rate of 29% for domesticcompanies if total turnover or grossreceipts in the financial year 2014-15does not exceed INR 50 million.Rate of surcharge & cess remainsunchanged for domestic and foreigncompanies.Dividend income from domesticcompanies received by residentIndividuals, HUFs and Firms in excess ofINR 1 million taxable at the rate of 10%.Exemption from DDT proposed fordividends received by Business Trustprovided it holds 100% of SPV’s sharecapital excluding the share capitalrequired to be mandatorily held byGovernment or Government bodies or asper its directions.MAT provisions will not be applicable toforeign companies having no PE in Indiaor having no registration requirementunder any other law in India. Thisamendment is proposed to be madee f fe c t i ve r e t ro s p e c t i ve l y f ro massessment year 2001-02.With effect from 1 April, 2016, units inIFSC eligible to following tax benefits:

Deduction under section 80LA tocontinue without a sunset clause.Companies not liable to DDT.MAT rate reduced to 9%.

Royalty income earned by an Indianresident from a patent developed andregistered in India shall be taxable on agross basis at the rate of 10%.Withholding tax at 25% applicable onpayment in respect of investment in asecuritization trust (if the payee is

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

�

st

st

st

10

Important Due Dates for March, 2016 CA. Abhijit J. Kotecha

DATES COMPLIANCE PERIOD

01-Mar-16 VAT/CST E-return - Monthly (Regular) Jan.'16

06-Mar-16 E-Payment of Service Tax Feb.'16

Excise Duty E-Payment (for SSI, NON SSI & EOU)

07-Mar-16 TDS / TCS Payment / E-Payment Feb.'16

10-Mar-16 Excise Returns - ( Monthly Return by Large Units / Return by EOU / Monthly return of receipt & consumption of

each of Principal Inputs, assessees required to submit ER-5 return) Feb.'16

15-Mar-16 PF Payment Feb.'16

Professional Tax Return and Payment

Advance Income Tax payment / E-payment - All Assessees - Last Installment Asst. Yr.: 2016-17

21-Mar-16 ESIC Payment & Return Feb.'16

22-Mar-16 VAT / CST payment / E-payment Feb.'16

25-Mar-16 PF Return Feb.'16

31-Mar-16 E- payment of Service Tax - Monthly & Quarterly Cases March'16, Q4 - Fin. Yr.:

2015-16

31-Mar-16 Last date for Filing / e-filing of Income Tax / Wealth Tax return (without penalty) Asst. Yr.:15-16

individual or HUF) and withholding tax at30% applicable on payment in respect ofinvestment in a securitization trust (ifpayee is any other person).Withholding tax applicable on paymentin respect of investment in asecuritization trust (if payee is a non-resident), at the rate in force.Beneficial withholding tax rate for non-resident investor on income frominvestment funds regulated by SEBI.Incremental withholding tax for non-resident not having PAN has beenremoved subject to prescr ibedconditions.Increase in threshold limit of taxes to bewithheld at source on various paymentsunder section 192A, 194BB, 194C,194LA, 194D, 194G and 194H.Revision in rate of taxes to be withheld onvarious payments under section 194DA,194EE, 194D, 194G and 194H.Tax is to be collected at source at 1% byseller on sale of motor vehicle havingvalue more than INR 1 million, on sale ofgoods or services more than INR200,000 in cash; no tax is collected atsource where withholding tax isdeducted by payer.Introduction of new equalization levy of6% to address challenges of the “digitale c o n o m y ” o n t h e a m o u n t o fconsideration received by non-residentfor any specified services.Benefit of initial additional depreciationextended to business of transmission ofpower.Investment allowance in respect ofinvestment in new plant and machinery

�

�

�

�

�

�

�

�

�

rationalized.Deduction of 100% of profits and gainsderived from the business of developingand building affordable housing projectsapproved by competent authority.Deduction for expenditure incurred onspectrum fee paid for acquisition ofairwaves by assessee over a period ofright to use.Phasing out of various profit linkeddeductions, accelerated depreciation onassets and weighted deductions over aperiod of time.Additional levy of tax where thecharitable institution ceases to exist ormerges / converts into non-charitableorganization.Three year tax holiday proposed foreligible start-ups.Exemption from long term capital gainsavailable when proceeds are invested inthe Government’s Start-up Fund ofFunds.Provisions governing place of effectivemanagement of a company deferred byone year.Exemption available to a foreigncompany in respect of income arisingfrom sale of crude oil (stored in a facilityin India) to an Indian resident.Income arising to a foreign companywhich is subject to Equalisation Levy,exempt from tax.Sunset clause introduced under section10AA for SEZ units that commenceoperations on or after 1 April, 2020.Rule 8D amended to limit disallowance(of expenditure incurred for earningexempt income) to 1% of the average

�

�

�

�

�

�

�

�

�

�

�

st

monthly value of investments yieldingexe mp t i n c o m e o r t h e a c t u a lexpenditure, whichever is lower.GAAR provisions to be effective from 1April, 2017.A person earning exempt income fromsale of long term capital asset (sharesand units etc.) required to furnish returnof income within due date if the incomewithout giving effect to such exemptionexceeds the maximum amount which ischargeable to tax.For the purpose of carry forward oflosses of specified business, a personwould now be required to file a return ofincome within due date.Any person who has filed a belatedreturn can also file a revised return.A return filed without payment of self-assessment tax along with interest shallnot be treated as a defective return.The scope of adjustments whileprocessing the return of income undersection 143(1) widened to includecertain other items. Further, processingof return before passing the assessmentorder has been made mandatory.Time limit for completion of assessmentor reassessment has been reduced by 3months.Time lines for passing appeal effectorder has been provided.Interest on refund will be allowed on self-assessment tax. Further, additionalinterest to be granted at the rate of 3% incase of delay beyond prescribed time

�

�

�

�

�

�

�

�

�

st

Memory LaneCampus Orientation Program on 04 02 2016 Workshop on ICDS on 13 02 2016

Tax Clinic - Series II on 15 02 2016

Interactive Meet with CIT – TDS, Vadodara on 22 02 2016Tennis Ball Cricket League For CA Members on 21 02 2016

Two days seminar on Business Improvement – Restructuring & Turnaround on 26-27 02 2016

Annual Study Circle Program on 24 02 2016 Recent Government initiatives forStart-ups on 16 02 2016

Half

day

sem

inar

onP

erm

anen

t Est

ablish

men

tson

20 0

2 2

016

11

CA. Ankur Maheshwari

CA. Manish Baxi

CA. Bimal Bhatt

CA. Pranay Mehta

CA. Hemant Bhatt

CA. Sanjiv S. Shah

STU

DY

CIR

CLE

CA. Mansi Shah CA. R. C. Thakkar

Adv. Ajay Shaw

CA. Nitant Trilokekar

CA. Rutvik Sanghvi

CA. Sanjeev S. Shah CA. Shailendra Jindal CA. Shefali Goradia CA. Shrirang Tambe

CA. Ajay Agashe CA. Amisha Singhal CA. Anup Shah

DISCLAIMER : The ICAI and the Baroda Branch of WIRC of ICAI is not in any way responsible for the result of any action taken on the basis of the advertisement published in the Newsletter. The members,however, may bear in mind the provisions of the Code of Ethics while responding to the advertisements. The views and opinion expressed or implied in the Newsletter are those of the authors / contributors and donot necessarily reflect those of Baroda Branch. Unsolicited matters are sent at the owner's risk and the publisher accepts no liability for loss or damage. Material in this publication may not be reproduced, whetherin part or in whole, without the consent of Baroda Branch. Members are requested to kindly send material of professional interest to The same may be published inthe newsletter subject to availability of space & editorial editing.

[email protected]/[email protected]

If undelivered, please return to :

Baroda Branch of WIRC ofThe Institute of Chartered Accountants of India

www.baroda-icai.org WIRC : www.wirc-icai.org ICAI: www.icai.orgl l

Back Cover (4 color) 15,000 Inside Front/Back Cover (4 color) Full Page (1 Color) Half Page (1 Color) 5,000

ADVERTISEMENT TARIFF : * Discount - 3 to 6 issue of 10%, 7 to 12 issue 15% * Circulated to more than 1800 Chartered Accountants

ADVERTISEMENTS :

SUBSCRIPTION RATES :

PRINTED AND PUBLISHED BY : Published at

Printed at

The tariff for advertising given below are duly approved by the Managing Committee of the Baroda Branch. Advertisements are received directly by the Branch and no advertising agency hasbeen appointed for this purpose.

This Newsletter is circulated without any charges to its members and other important categories of recipients as per ICAI Advisory on Newsletters. Subscription rate is Rs. 20/- per issuefor others.

CA. Viral Shah on behalf of Baroda Branch of WIRC of ICAI. “ICAI Bhawan”, Kalali-Tandalja Road, Atladra, Vadodara - 390 012

Multiprints, 30/B, Gandhi Oil Mill Compound, Near BIDC, Gorwa, Vadodara - 390016. Ph.: 0265-2285592

“ICAI Bhawan”, Kalali-Tandalja Road,

Atladra, Vadodara - 390 012.

+91 265 2681115 / 2680593 8511077115Telefax : M:

7,50010,000

WICASA JAN 2016 WICASA FEB 2016

12

THE INSTITUTE OF CHARTEREDACCOUNTANTS OF INDIA

Tel. :E-mail :

Web :

ICAI Bhawan, Post Box No. 7100,Indraprastha Marg, New Delhi - 110002.

+91 (11) [email protected]

www.icai.org

WESTERN INDIA REGIONAL COUNCIL

Tel. :Email :

Web :

ICAI Tower, Plot no C-40, G BlockOpp MCA Ground, Bandra Kurla Complex,

Bandra (E), Mumbai - 400 051+022-33671400/33671500

BARODA BRANCH OF WIRC OF ICAI

M.:Chairman Mobile:

Telefax :E-mail:

Web :

“ICAI Bhawan”, Kalali-Tandalja Road, Atladra,Vadodara - 390 012. +91 8511077115

+91 8511125959+91 (265) 2681115 / 2680593