newsletter one stop

DESCRIPTION

one stop newsletterTRANSCRIPT

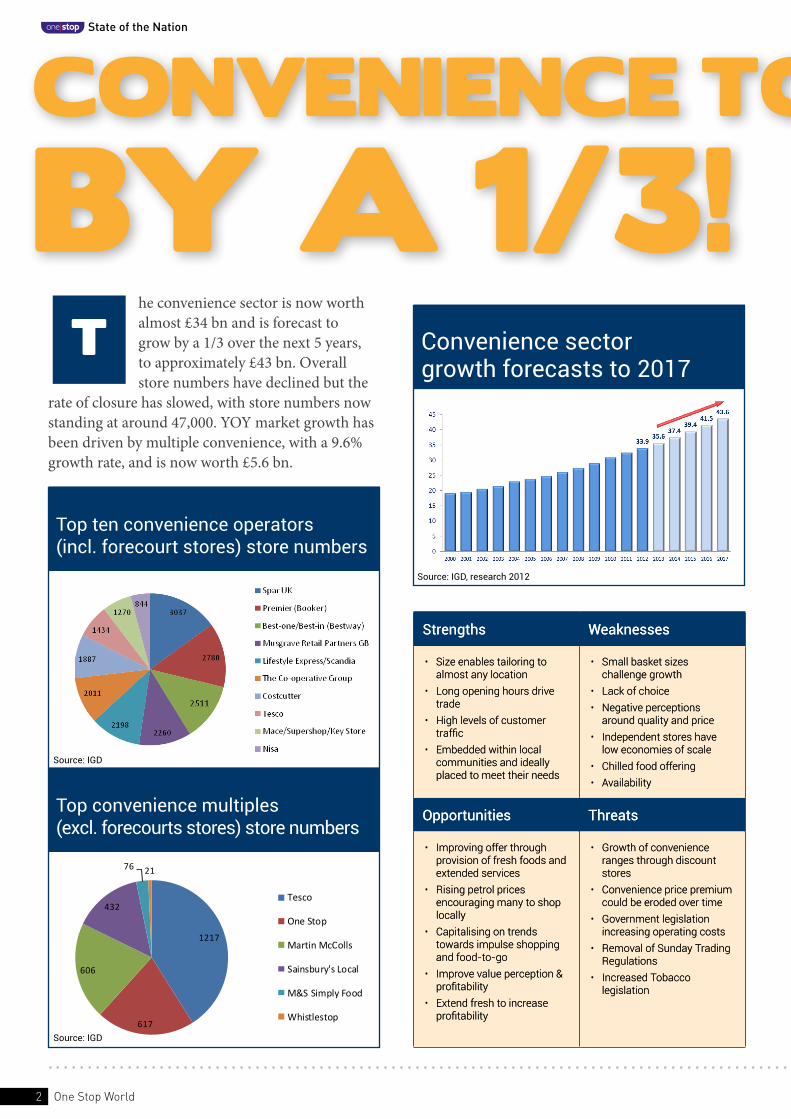

ConvenienCe set to grow by 1/3!

50

00

18

71

32

50

6

One Stop World

Top ten convenience operators (incl. forecourt stores) store numbers

Top convenience multiples (excl. forecourts stores) store numbers

1217

617

606

432

76 21

Tesco

One Stop

Martin McColls

Sainsbury's Local

M&S Simply Food

Whistlestop

Strengths Weaknesses

• Sizeenablestailoringtoalmostanylocation

• Longopeninghoursdrivetrade

• Highlevelsofcustomertraffic

• Embeddedwithinlocalcommunitiesandideallyplacedtomeettheirneeds

• Smallbasketsizeschallengegrowth

• Lackofchoice• Negativeperceptionsaroundqualityandprice

• Independentstoreshaveloweconomiesofscale

• Chilledfoodoffering• Availability

Opportunities Threats

• Improvingofferthroughprovisionoffreshfoodsandextendedservices

• Risingpetrolpricesencouragingmanytoshoplocally

• Capitalisingontrendstowardsimpulseshoppingandfood-to-go

• Improvevalueperception&profitability

• Extendfreshtoincreaseprofitability

• Growthofconveniencerangesthroughdiscountstores

• Conveniencepricepremiumcouldbeerodedovertime

• Governmentlegislationincreasingoperatingcosts

• RemovalofSundayTradingRegulations

• IncreasedTobaccolegislation

Convenience sectorgrowth forecasts to 2017

7%

-‐14%

5%

12%

17%

7%

-‐1%

1%

4%

9%

-‐20%

-‐15%

-‐10%

-‐5%

0%

5%

10%

15%

20%

Cooked Meats inc Prepack

Meat Snacks Pastry Natural Cheese BuAer Spreads & Mar

ONE STOP

IMPULSE

Source: Nielsen Scantrack: Impulse MAT Value Sales % Change to 21.07.12. One Stop Sales In MAT to Week 34

One Stop World

7%

-‐14%

5%

12%

17%

7%

-‐1%

1%

4%

9%

-‐20%

-‐15%

-‐10%

-‐5%

0%

5%

10%

15%

20%

Cooked Meats inc Prepack

Meat Snacks Pastry Natural Cheese BuAer Spreads & Mar

ONE STOP

IMPULSE

Source: Nielsen Scantrack: Impulse MAT Value Sales % Change to 21.07.12. One Stop Sales In MAT to Week 34

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

01.2012

02.2012

03.2012

04.2012

05.2012

06.2012

07.2012

08.2012

09.2012

10.2012

11.2012

12.2012

13.2012

14.2012

15.2012

16.2012

17.2012

18.2012

19.2012

20.2012

21.2012

22.2012

23.2012

24.2012

25.2012

26.2012

27.2012

28.2012

29.2012

30.2012

31.2012

32.2012

33.2012

Revenue Act Revenue LY

Sandwich launch wk 26 May range review wk 22

£25.3m -‐ 2012 £21.5m -‐ 2011 Difference -‐ +17.6% (+£3.8m) Incremental sales coming from Sandwiches Other categories driving growth are Produce (+£1.2m ) , Salads (£363k),Ready Meals (+£263k)

One Stop World

One Stop World

• Increase basket size • Increase drop size

• Improve choice & extend • Extend range with more chilled range categories

• Shorter leadtime • Shorter leadtime

• Increase quality • Increase quality

• Reduced wastage • Reduced wastage

• Drive fresh food performance • Drive business performance

• JBP • JBP

• Streamlined supply chain • Streamlined supply chain

• Flowers & frozen • Longer term commitment

• Improved forecasting

• Extend Kerry range

Joint Business Aims

Building brand identity in-store

6

Make it easier for shoppers to shop

7

Demonstrating appeal to the health-conscious shopper

8

Exploit technology

9

Targeting the full breadth of impulse

10

Creating a one-stop impulse solution

1

Making checkouts an in-store feature

2

Showcasing product attributes to add theatre

3

Merchandising to inspire and delight

4

Creating event impact

5